accountig for tax

TRANSCRIPT

THE SYSTEM OF ACCOUNTING

Volume III

WRITTEN BY:SYED AQEEL RAZA

C O N T E N T SCHAPTER NINE TAXES-----------------------------------------------------------------------------------------

Accounting for taxes 9.1- Income tax 9.2-5

o Income Tax Slab salaried persons 9.6o Income tax salaries 9.7-8o Income Tax W/H on goods and services 9.8o How to maintain Income Tax on goods and services 9.9o What is National Tax Number NTN? 9.10

- Sales Tax 9.11-15o What is value-added tax (VAT)? 9.16o What do you mean by F.B.R. & S.R.B.? 9.16.18o Maintenance of Sales Tax record 9.19-23

- Writer’s view 9.25

Accounting for Taxes

ACCOUNTING FOR TAXES

In accounting, no one can deny the importance of taxes and taxes involves various stages of various kinds end to the result covering the period of Accounting. Therefore, all accounting process revolves around taxes and taxes force to owners to keep a complete set of the book of accounts audited by the chartered accountant or may be required to tax offices for verification of the purity of tax matters.

Besides other taxes, there are mainly two kinds of taxes involve in the business of manufacturing, trading, and services wherein taxes on sales and income are under discussion.

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

Accounting for Taxes

INCOME TAX

Accounting for Taxes

INCOME TAXTaxation according to a person’s ability to pay is universally accepted the principle. Income Tax is, therefore, generally recognized as a highly equitable from taxation. Tax rates and method of calculating taxable income varies with the fiscal status of the taxpayer.

Following are the broad categories of taxpayers:-

- Companies- Association of Persons (AOP)- Non-salaried Individuals- Salaried individuals

Companies

A company is a person who encompasses all legal rules and regulations for businesses under registered with the security and exchange commission of Pakistan (S.E.C.P.) The SECP checks financial and corporate entities to ensure stakeholder’s interest.

The corporate sector in Pakistan is governed by the Companies Ordinance 1984 which was promulgated on 8th October 1984 and repealed the Companies Act, 1913.

There are two kinds of companies;

PRIVATE COMPANY -Private Company has the following restriction while these restrictions do not apply to other companies.

(1) It cannot have members more than 50 excluding those are the employees of the company.

(2) It cannot invite the general public to subscribe the share of the company. (3) It restricts freely transfer of share.

PUBLIC COMPANY - Companies Ordinance define the public company as a company that is not a private company. It means every company that is registered in Pakistan either it is a private company or a public company.

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

Accounting for Taxes

Association of Persons (AOP)

An association of persons (AOP) under the Income Tax Act is an entity or unit of assessment. It means two or more persons who join for a common purpose with a view to earning an income. The term Person includes any company or association or body of individuals, whether incorporated or not.

Non-salaried individual

Non-salaried individual means the total earnings of a person from wages, investment, interest and other sources. This kind of individual is not employed in any business concern but we say him the self-employed who works himself by means of performing services or he generates income with his investments and other sources which become the cause of earnings from him.

Salaried individual

The salaried individual means a person who is employed in the business concern. Actually, he sells his knowledge and efforts and the amount which he gets comes under services business. If he comes under the specified limit of income tax, the concern where he works deducts his income tax because of having withholding agent; a withholding agent is responsible for deducting income tax and deposit to bank on behalf of income tax.

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

Accounting for Taxes

Capital Value Tax

It is payable by individuals, firms, and companies which acquire an asset by purchase or a right to use for more than 20 years.

Corporate Asset Tax

It is levied under section 12 of the Finance Act, 1991. This is one-time levy payable by a company as defined in Companies Ordinance, 1984, on the value of fixed assets of the company on the “specified date”.

The withholding agent is who that deducts taxes on salaries and goods/services on behalf of the government and deposit them to the bank under the specified rates declared from time to time. The taxes which it deducts are chargeable in returns or shown in return as to employee when he shall fill his return shows the amount which has been deducted by his behalf and like this, the entity shall adjust the deducted amount at the time of filing income tax or sales tax returns.

The rates which are presently declared are shown below;<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

Accounting for Taxes

Income Tax Slabs 2016-17 Salaried Persons Finance Act 2016

Where the income of an individual chargeable under the head “salary” exceeds fifty percent of his taxable income, the rates of tax to be applied are as follows:

Z

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

Accounting for Taxes

INCOME TAX SALARIES:

The withholding agent means the employer who is liable to deduct tax from salaries of his employees according to the declared slab from government and the employee whose tax was deducted is bound to fill his return wherein he will show his incomes from salaries or any other source. Now a day, the government has introduced electronic e-filing of return where anyone can easily register himself and fill the required fields within the given time.

The employer is only responsible for deducting tax from salaries and deposit into the bank. He is also responsible for filing the return electronically monthly, quarter and annually.

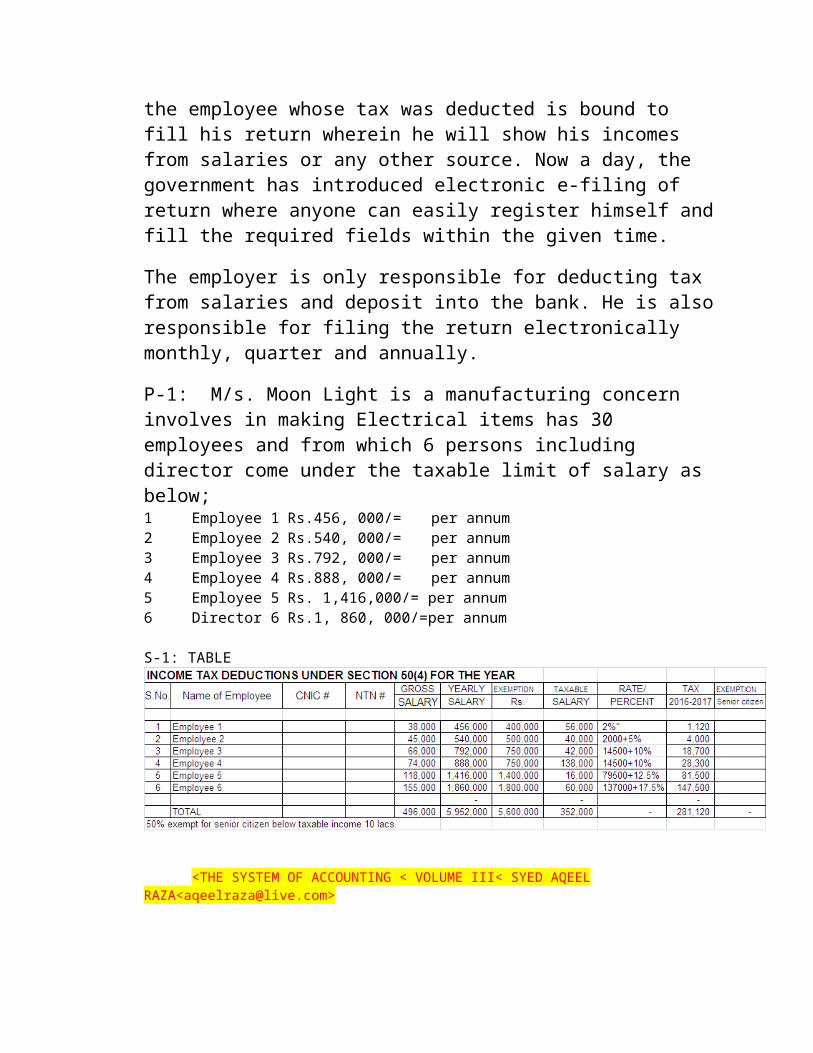

P-1: M/s. Moon Light is a manufacturing concern involves in making Electrical items has 30 employees and from which 6 persons including director come under the taxable limit of salary as below;1 Employee 1 Rs.456, 000/= per annum2 Employee 2 Rs.540, 000/= per annum3 Employee 3 Rs.792, 000/= per annum4 Employee 4 Rs.888, 000/= per annum5 Employee 5 Rs. 1,416,000/= per annum6 Director 6 Rs.1, 860, 000/=per annum

S-1: TABLE

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

Accounting for Taxes

TABLE2

INCOME TAX WITHHOLD ON GOODS AND SERVICES

The Income tax withholding rates W.E.F. 01.07.2014;

- Supply of goods by Companies = 4%- Supply of goods by other than companies 4.5% (Previously 4%)- Services rendered by Companies 8% (Previously 6%)- Services rendered by other than companies 10% (Previously 7%)- Execution of contract by Companies 7% (Previously 6%)- Execution of contract by other than companies 7.5% (Previously 6.5%)- Export-oriented services 1% (Previously 0.5%)- Commission (Excluding advertising agents) including Petrol Pump

operators 12% (Previously 10%).- Advertising agents 7.5% (Previously 10%) U/S233- The rate of tax to be deducted under section 155, in the case of

company shall be 14% of the gross amount of rent (Previously 15%)

The above rates are in respect of payment u/s 153, 155, 233.<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

Accounting for Taxes

How to maintain income tax withholding on goods and services?

The withholding agent has the responsibility to deduct tax according to the nature of the business transaction and deposit it into Bank and gives the proof of its deduction and deposition to the party and submits the return monthly, quarterly or annually.

The withholding agent has to keep the summary of taxes withheld for quick reference as in table;

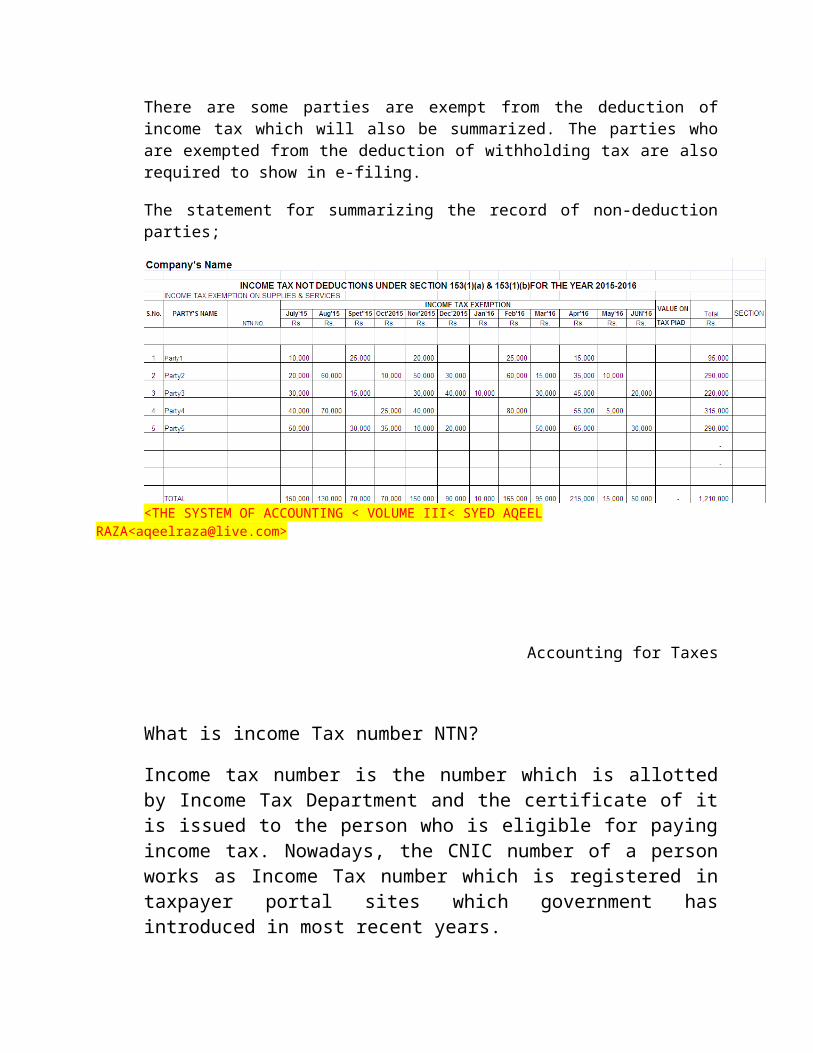

There are some parties are exempt from the deduction of income tax which will also be summarized. The parties who are exempted from the deduction of withholding tax are also required to show in e-filing.

The statement for summarizing the record of non-deduction parties;

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

Accounting for Taxes

What is income Tax number NTN?

Income tax number is the number which is allotted by Income Tax Department and the certificate of it is issued to the person who is eligible for paying income tax. Nowadays, the CNIC number of a person works as Income Tax number which is registered in taxpayer portal sites which government has introduced in most recent years.

Who is Withholding Agent?

The withholding agent is the entity whose responsibility is to withhold tax and deposited into the treasury of government. It works on behalf of another and is responsible under laws. The benefit of making withholding agent is to ensure the increase in taxes and transparency in checking system of taxes.

Do you mean by Income tax withholding?

The income tax withholding may be called the advance system of taxes and who deduct taxes is called withholding agent. The tax which is withheld may be adjusted or refunded. The income tax withholding may be on the salaries of employees and of material or services.

What is an advance tax?

The tax which is deducted by the purchaser comes under the advance tax. This kind of tax is for purchaser withholding income tax which he shall deposit into the bank and deliver the copy of the paid challan. The purchaser shall debit his account as account receivable debit and credit to income tax withholding parties and like his seller

The purchaser does debit his account as an advance income tax and credit to party account and seller does debits account receivable and does credit advance

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

Accounting for Taxes

SALES TAX

Accounting for Taxes

SALES TAX

The Sales tax is a tax which is paid to a governing body for the sales of certain goods and services. Usually, laws allow the seller to collect tax from the consumer at the point of purchase. Often laws provide for the exemption of certain goods of services from sales.

A system of licensed manufacturers and wholesalers was instituted whereby they were allowed to purchase goods free of sales tax from each other and pay tax on sales to unlicensed traders. Imports were chargeable to sales tax but the licensed manufacturers and wholesalers were allowed to import goods without the payment of sales tax. Later on, Sales Tax became chargeable on locally produced & imported goods at the time of their sales & import, respectively. The sales tax was collected under the Finance Ordinance, 1956, on goods which were chargeable to Central Excise Duty, as if it were a duty of Central Excise. In April 1981, by virtue of an amendment to the Sales Tax act, 1951, the collection of Sales Tax on non-excisable goods was also entrusted to the Central Excise Department.

In the late eighties, the government decided to replace Sales Tax with the Value Added Tax in the country as a part of its structural adjustment program which was undertaken to correct anomalies & distortions both in our tax & non-tax regimes. Accordingly, new enactment titled Sales Tax Act 1990 replaced Sales Tax Act 1951 with effect from 1-11-1990.

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

Accounting for Taxes

LIABILITY OF SALES TAX

Following sectors are required to get registration for sales tax and charge sales tax on their supplies/services;-

- Manufacturing- Import- Services- Distribution, Wholesale and Retail stage

Previously it was being charged at the manufacturing and import stage, and its scope has been extended now to remaining sectors.

Sales tax is chargeable on all locally produced and imported goods except computer software, poultry feeds, medicines and unprocessed agricultural produce of Pakistan and other goods specified in Sixth Schedule to the Sales Tax Act, 1990.

REGISTRATION

Every person in sectors mentioned above, who makes a taxable supply in Pakistan is required to be registered under the Sales Tax Act. However, manufacturers having taxable turnover below five million rupees and also utility bill below rupees seven hundred thousand during the last twelve months are exempted from registration and payment of sales tax. Similar exemption is also available to retailers having total turnover below rupees five million in the last twelve months.

The rate of sales tax is 16% of the value of supplies. However, there are some items which are chargeable to sales tax at 18.5% or 21% of the value of supplies (see SRO 644(I)/2007 as amended by SRO 537(I)/2008 dated 11th June 2008.

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

Accounting for Taxes

The Registration Form(s) are submitted to the Central Registration Office, FBR, or Sales Tax Collect-orates/ RTOs for the allotment of a Registration Number by the persons liable to be registered under the Sales Tax Act. The taxpayer has then issued a Certificate of Registration.

RETURNS

As per law, each registered person must file a return by the 15th of each month regarding the sales made in the last month.

All registered persons are required to file returns electronically and in such cases, the payment is to be made by the 15th and return can be submitted on FBR’s e-portal by 18th.

A detailed procedure in this respect is given in Sales Tax General Order no. 04 of 2007.

There are some sectors which are required to file returns on a quarterly (tri-monthly) basis e.g. retailers including dealers of specified electric goods and CNG dealers.

MAINTENANCE OF RECORDS

All registered persons are required to maintain records at their business premises of the goods purchased and supplied made by them. All the records are required to be kept for a period of 5 years.

REFUNDS OF SALES TAX

In cases where the Input Tax exceeds the Output Tax due from the registered person in respect of a tax period because of exports or other zero-rated supplies, the excess amount of input is refunded back to the taxpayer within 45 days. In all other cases of excess input tax, the Board can specify the procedure for refund.

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

Accounting for Taxes

ADDITIONAL TAX

If a registered person does not pay the tax within the specified time or claims a tax credit or refund which is not admissible to him or incorrectly applies the rate of zero percent to the supplies made by him, he has to pay the additional tad at the following rates:

One and a half percent of tax due or the part thereof per month;However, in case of tax fraud, the rate of additional tax shall be two percent per month.

ARREARS

The work regarding Arrears gets initiated in the following cases:

Late or no submission of the Returns Amount paid is less than the tax amount payable

A demand is raised after an audit/ scrutiny is upheld after adjudication.

SALES TAX WITHHOLDING

Sales tax withholding means some portion of sales tax as declared by Federal Board of Revenue from time to time is retained by the sales tax withholding agent; the sales tax withholding agent refer to the party which purchased goods/services, and that amount is adjusted by the entity whose tax was withheld.

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

Accounting for Taxes

What is value-added tax (VAT)?

A value-added tax (VAT), known in some countries as a goods and services tax (GST), is a type of general consumption tax that is collected incrementally, based on the value added, at each stage of production and is usually implemented as a destination-based tax, where the tax rate is based on the location of the customer.

Therefore, sales tax, general sales tax, and value added tax work same with the procedures and regulations of the country where it enforced.

What do you mean by F.B.R. & S.R.B.?

FEDERAL BOARD OF REVENUE

FBR means Federal Board of Revenue formerly known Central Board of Revenue under enactment of FBR Act 2007. The Federal Board of Revenue is a federal agency of Pakistan responsible for enforcing fiscal laws and collecting revenue for the government of Pakistan.

FBR has two major wings; Inland Revenue and Customs. The Inland Revenue Services formerly known as Income Tax Department administers domestic taxation including Sales Tax, Income Tax, and Federal Excise Duties. The Pakistan Customs service administers import duties and other taxes collected at import stage as well regulates international trade with regard to prohibitions and restrictions imposed by the government. For the purpose of collection of revenue and pursuing tax evaders, FBR’s powers and functions also include but are not limited to; carrying out inquiries and audits/investigations into the tax affairs, commanding arrests, attachment as well as public auction of movable and immovable assets of non- compliant.

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

Accounting for Taxes

SINDH REVENUE BOARD

SRB means Sindh Board of Revenue controlled under provincial government Sind, Pakistan is responsible for collecting all tax revenues for

the government of Sindh. Sindh Board of revenue is the controlling authority in all matters connected with the administration of Revenue collection including land taxes, land revenue, preparation of land record, sales tax on services, and other matters relating thereto. The Ministry of Revenue is the minister responsible for Board of Revenue, Sindh.

P-1: Print Tech packages (Pvt.) Ltd. supplied 4500 cartons of Rs. 33,750/=involving 17% sales Tax Rs.5, 738/= to Umair Enterprises (Pvt.) Limited vide Invoice # 1560 dated 2.2.2017.

In this problem, Print Tech is the seller and Umair Enterprises is purchaser. The purchaser is liable to withhold 20% on sales tax under head Sales Tax Withholding purchase F.B.R. being a sales tax withholding agent.

The purchaser Umair Enterprises will record journal entry in his ledger as;

Purchase Dr 33,750.-

Sales Tax on Purchase (FBR) Dr 5,738.-Print Tech Packages Dr 1,147.-

Sales Tax withholding Purchase FBR Cr 1,147.-Print Tech Packages Cr 39,488.-

At the time of payment to Print Tech Packages, Umair Enterprises debit the liability account of Print Tech as;

Print Tech Packages Dr 38,341.-Income Tax payable 1,724.-

Cash/Bank Cr. 36,617.-

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

Accounting for Taxes

We have to deduct withholding tax on sales tax as soon as we receive invoice or at the time of creating liability account of seller because the sales tax department has no concern the payment of invoice but involves in deduction resulting in e-filing of sales tax return of that month.

The amount which was withheld will be paid or adjusted in sales automatically in sales tax return by purchaser.

The seller Print Tech Packages (Pvt.) Ltd will record journal entry as;

A/c Receivable Umair Dr 38,341.-Advance Sales Tax W/H 1,147.-

Sales Tax Payable Cr 5,738.-Sales 33,750.-

On receiving the amount in balance, Print Tech Packages will record the transaction as;

Cash/Bank Dr 38,341.-A/c Receivable Umair Cr 38,341.-

The Sales tax payable account will be reversed on payment of tax as;

Sales Tax payable Dr 5,738.-Advance Sales Tax W/H 1,147.-Cash/Bank 4,591.-

The sales tax and advance tax which was withheld by the purchaser will be adjusted automatically in the sales tax return of the seller.

The income tax which the withholding agent withheld will be journalized as;

Advance Income Tax 1,724.-Print Tech Packages 1,724.-

The advance income tax is the asset of the company may be claimed from Income Tax Department or adjustment in finalizing the return.

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

Accounting for TaxesMAINTAINANCE OFSALES TAX RECORD

Sales tax is the main issue of any concern dealing with business. The product which the seller sells and the purchaser buys includes sales tax.

It is the requirement of sales tax to have accurate records of the sales and all transactions made to each customer up to 5 years as evidence of transaction. Additionally, proper upkeep of electronically stored data on accounting or sales tax programs is essential to stay compliant with these rules and regulations.

OUT PUT TAXOut put tax means the supplies of products which include sales tax to registered or unregistered persons who may be distributor, whole seller, person etc.

The output tax requires Tax Invoice Section 23 of sales tax act 1990 containing;

- Serior number and date- Name, address and registration number of the supplier- Name, address and registration number of the recipient- Discription and quantity of goods- Value exclusive of tax- Amount of sales tax- Amount of further tax as specified, if the supplies are made to an

undregistered person.- Value inclusive of tax.

- <THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

Accounting for Taxes

KIND OF SUPPLIES

1- Taxable supplies2- Exempt supplies3- Zero-rate supplies

TAXABLE SUPPLIESTaxable supplies mean a supply of taxable goods made by an importer, manufacturer, whole seller, distributor or retailer.

Exempt suppliesExempt supplies mean a supply which is exempted from levy of the sales tax by the Federal Board of Revenue as in the list of sixth schedule.

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

Accounting for TaxesZERO RATE SUPPLIES

It means a taxable supply, which is charged to tax of zero percent under section 4. In other words, where a supply is exported to a foreign country, tax is charged at the rate of 0% on that supply and the output tax becomes zero. In case of zero rate supply the person making the supply is entitled to refund of all input tax paid on raw materials used in the manufacturing of the product.

INPUT TAXPurcahse made by registered persons for busienss purposes are nown as inputs and the tax which includes in it is called input tax.

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

Accounting for Taxes

ADJUSTMENTS:The seller adjusts input tax which he pays on purchasing of goods, electricity, telephone, and service in taxable supplies and can carry forward or refund the excess amount under the provision of sub-section (2).

In case of cancellation of supply or return of goods or a change in the nature of supply or change in the value of supply or some such event, the amount shown in the tax invoice or the return needs to be modified, the registered person may issue a debit or credit note and make corresponding adjustment against input tax in the return.

E-FILINGE-filing is automatic system of maintenance of records relating to sales tax which may be studied under user guide for sales tax on taxpayer facilitation portal of FBR.

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

Accounting for Taxes

The Accounting for taxes is not matter to say that the concept of debit and credit are the same as its basic but the creation of head of accounts according to the situation is a separate matter. The party whose tax will be deducted by someone will create receivable account as advance tax which perhaps return or adjusted from tax departments and the party who will withhold tax will create liability account and responsible to deposit into government treasuries and deliver the evidence of deposition to the party whose tax was withheld.

The tax chapter is an essential to businesses for operation any business and then it is very necessary to care keeping clean in taxes. The rules and regulation of government are being changed from time to time which may be studied and applied.

Everything has no end and the change is end but for the time being.

Writer’s view

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>