accountig ppt

TRANSCRIPT

TYPES OF DISCOUNT

TRADE DISCOUNT & CASH DISCOUNT

trade discount It is the deduction from the list price

or catalogue price, usually allowed by wholesalers to retailers on bulk purchases. It is deducted in the invoice from the list price and the net amount only is recorded in the books of accounts.

TREATMENT OF TRADE DISCOUNT WITH EXAMPLE

A sold to B goods of the catalogue price of R.s. 10000 at a tade discount of 10%. * The journal entry in the book of A : B's A /c Dr. 9000 Sales A/c 9000 ( sold goods on credit)( 10000-10% discount= 9000)

*journal entry in books of B is : Purchase A/c Dr. 9000 A's A/c 9000 ( Bought goods on credit)

cash discount

It is the reduction allowed by the creditor to the debtor, usually on making prompt payment. Such a reduction is an expense to the creditor who allows it and an income to the debtor who make the payment at a lesser amount.

TREATMENT OF CASH DISCOUNT WITH EXAMPLE

X owes an amount of R.s.1000 to Y. X makes the payment promptly and Y allows a reduction of R.s.50.

The reduction of R.s.50 is the cash discount, it

is an income to X and expense to Y.

*journal entry in the books of Y, on receipt of the amount :

Cash A/c Dr. 950 Discount A/c Dr. 50

X’sA/c 1000 (cash received &discount allowed)

*journal entry in the books of X on payment: Y’sA/c Dr. 1000 CashA/c 950

DiscountA/c 50 (cash paid and discount earned)

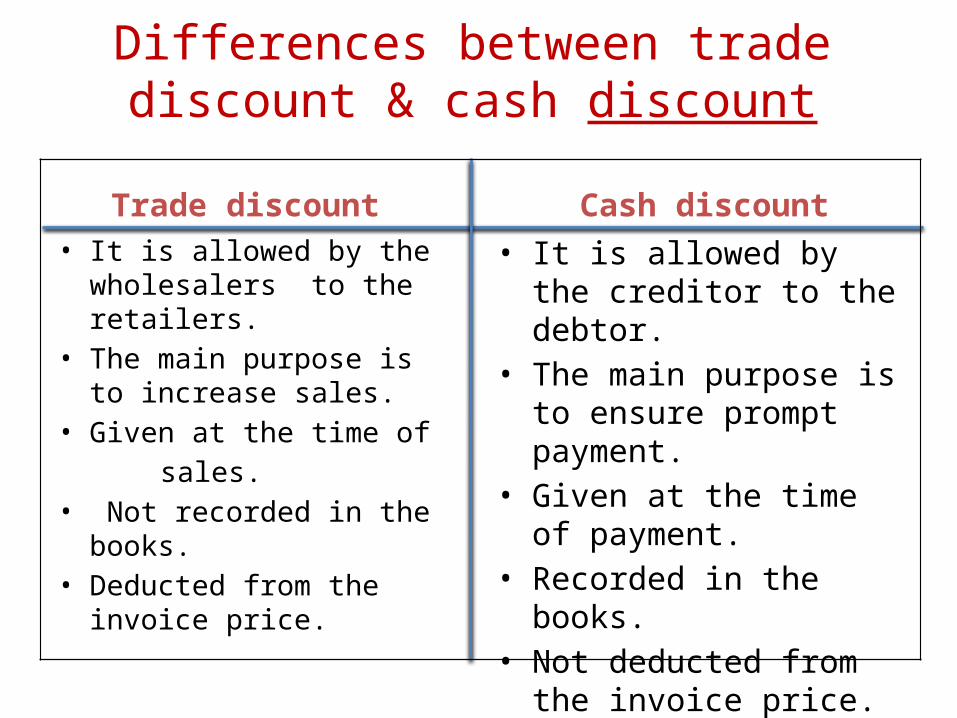

Differences between trade discount & cash discount

Trade discount• It is allowed by the

wholesalers to the retailers.• The main purpose is to

increase sales.• Given at the time of sales.• Not recorded in the books.• Deducted from the invoice

price.

Cash discount• It is allowed by the creditor

to the debtor.• The main purpose is to

ensure prompt payment.• Given at the time of

payment.• Recorded in the books.• Not deducted from the

invoice price.

Assignment Prepare a short note on discount and its

differences.