accelerating into the curve

TRANSCRIPT

8/15/2019 Accelerating Into the Curve

http://slidepdf.com/reader/full/accelerating-into-the-curve 1/20

AcceleratingInto the Curve

Achieving Success in a

Challenging Market

Findings of the 2003

McKinsey/U.S. Institute

Asset Management

Benchmarking Survey

8/15/2019 Accelerating Into the Curve

http://slidepdf.com/reader/full/accelerating-into-the-curve 2/20

Introduction 2

A Difficult Environment 3

Keys to Future Growth and Profitability 6

Growing and Retaining Assets 6

Achieving Market-Leading Profitability 9

Appendix – Survey Participants 17

Contents1

8/15/2019 Accelerating Into the Curve

http://slidepdf.com/reader/full/accelerating-into-the-curve 3/20

8/15/2019 Accelerating Into the Curve

http://slidepdf.com/reader/full/accelerating-into-the-curve 4/20

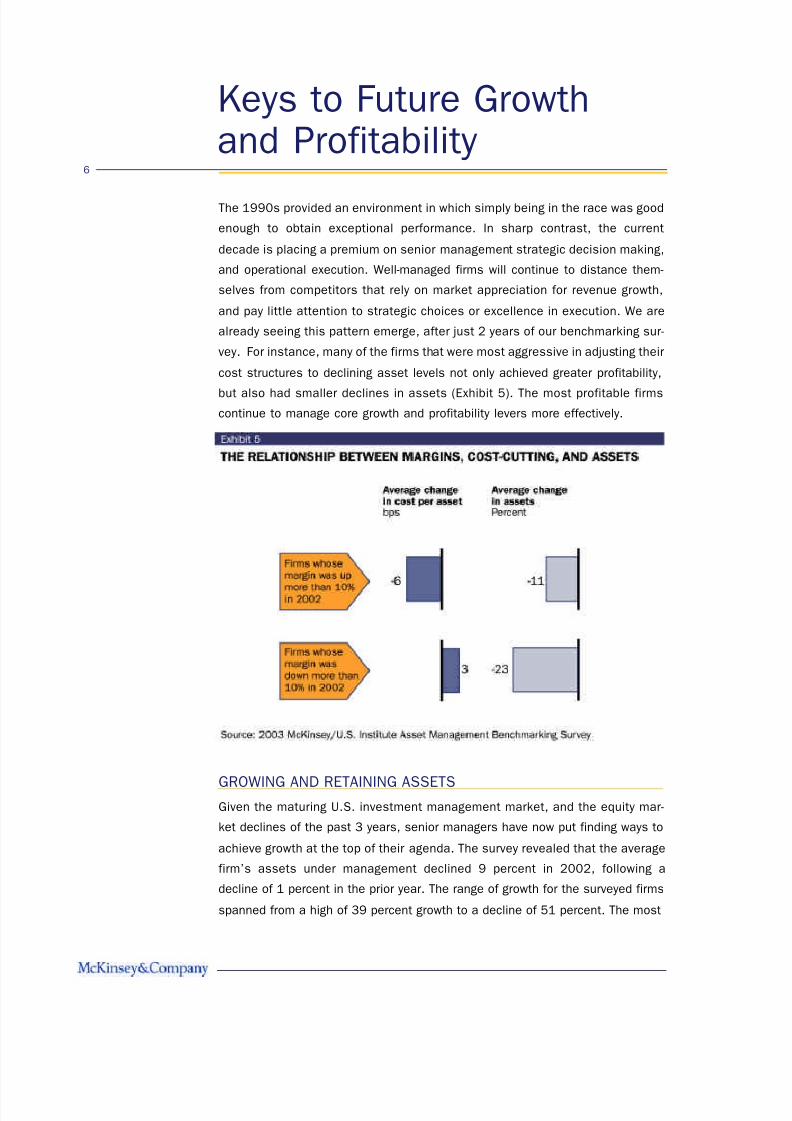

It is not news to any active participant that the asset management industry has

faced a difficult operating environment for several years, coupled with double-

digit equity market declines. What is news is that, in the face of these chal-

lenges, a minority of leading firms achieved strong profits and/or maintained

significant asset growth while, industrywide, margins and assets fell.

As a whole in 2002, the U.S. asset management industry delivered average prof-

it margins of 25 percent, down 2 percent from the previous year. This reduced

profitability for the industry was caused by average asset declines of 9 percent,

offset in part by average cost reductions of 8 percent (Exhibit 1). However, theindustry’s increasing challenges are separating the winners from the rest of the

pack, creating a dramatic gap with bottom performers. Indeed, while the top

third of all firms had average profit margins of 46 percent, the bottom third aver-

aged only 3 percent. However, it was not only large fixed-income or money mar-

ket firms that excelled. There are firms of all sizes, client segments and asset-

class focuses that delivered outstanding profitability (Exhibit 2).

A Difficult Environment3

8/15/2019 Accelerating Into the Curve

http://slidepdf.com/reader/full/accelerating-into-the-curve 5/20

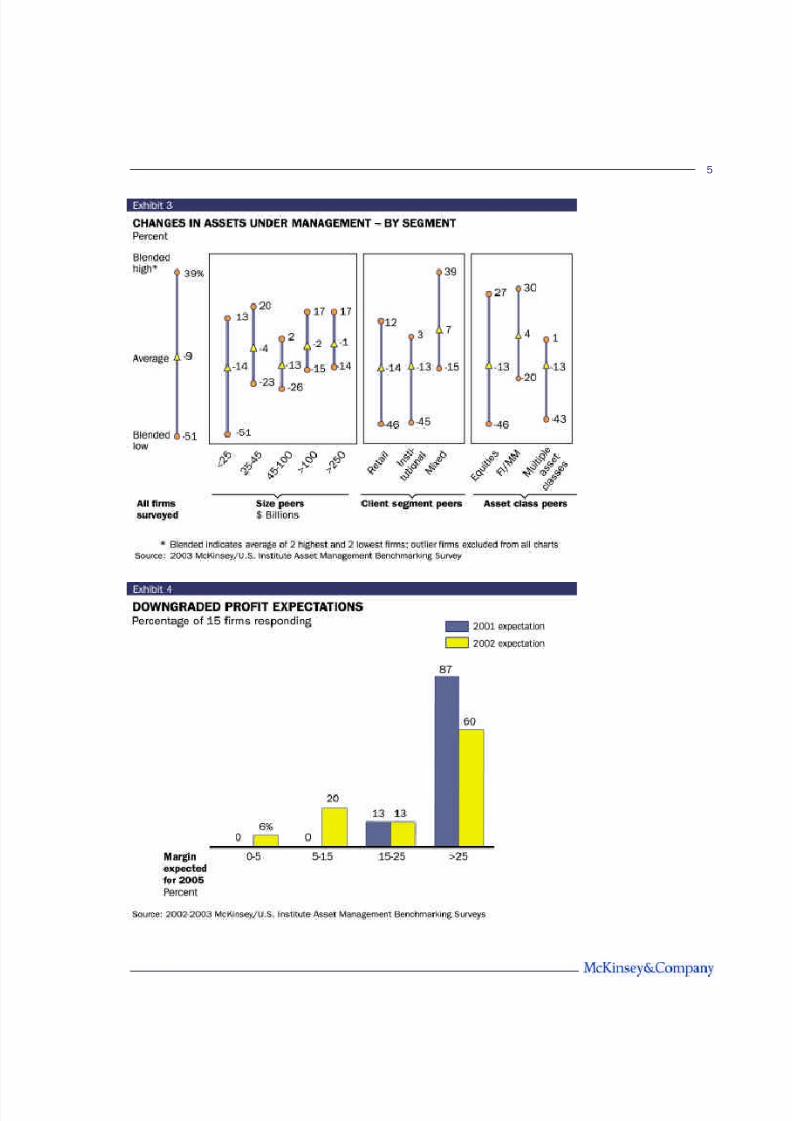

Just as with profits, the gap in asset growth between winners and losers was

also stark. While the top 10 percent grew assets by greater than 10 percent,

fully 20 percent had asset declines in excess of 20 percent. Broken down by

segment, fixed-income firms, on average, clearly grew more than others in

2002. However, there were a number of firms in each segment that delivered

market-leading growth (Exhibit 3).

Looking forward, the challenges of the industry will likely continue to increase the

performance gap, with a minority of firms achieving distinctive growth and prof-

itability, while the majority work hard just to maintain assets and their currentprofit margins. Most firms believe that achieving the profitability levels of the late

1990s will be challenging. Therefore, many have lowered their forward-looking

profitability targets (Exhibit 4). However, we believe the future should not be about

lowered expectations. Rather, we feel firms should place an increased focus on

developing the skills and capabilities required to achieve market-leading prof-

itability and growth levels.

4

8/15/2019 Accelerating Into the Curve

http://slidepdf.com/reader/full/accelerating-into-the-curve 6/20

5

8/15/2019 Accelerating Into the Curve

http://slidepdf.com/reader/full/accelerating-into-the-curve 7/20

8/15/2019 Accelerating Into the Curve

http://slidepdf.com/reader/full/accelerating-into-the-curve 8/20

successful firms understand that, in the future, organic growth in most U.S.

markets will continue to be modest. As a result, they are focusing on growing

through three alternative levers:

Leverage core strengths. The most successful firms continuously leverage their

core strengths and aggressively extend into new markets and products that will

augment growth and profitability. For example, over the past few years, many

successful institutional firms have focused on the sub-advisory market, achiev-

ing double-digit growth rates. Many of these winners have also launched prod-

ucts that satisfied investors’ current needs, such as high-yield bond funds.However, careful assessment of new growth opportunities is critical, not only to

drive growth, but also to maintain and enhance profitability, as the evidence

shows that dabbling is a major drag on profits (Exhibit 6).

Improve sales skills to steal share. There is little doubt that institutional and

retail clients are continuing to become more sophisticated, and are demanding

new and improved sales and service capabilities from their asset managers. On

the institutional side, leading firms are discovering ways to provide better serv-

ice across DB and DC plans, by segmenting their servicing and client relation-

7

8/15/2019 Accelerating Into the Curve

http://slidepdf.com/reader/full/accelerating-into-the-curve 9/20

ship management approaches, improving reporting, broadening their participant

servicing and education, and other steps. In retail, the bar for distinctive whole-

saling is rising, as is the cost, due to a number of factors. These include the

proliferation of new products, such as 529s and separate account wraps, and

the addition of new channels for many of these products, such as independent

broker dealers, coupled with rising advisor expectations for service. Advisory

firms and their advisors want investment solutions linked to holistic advice, not

“the product of the day.”

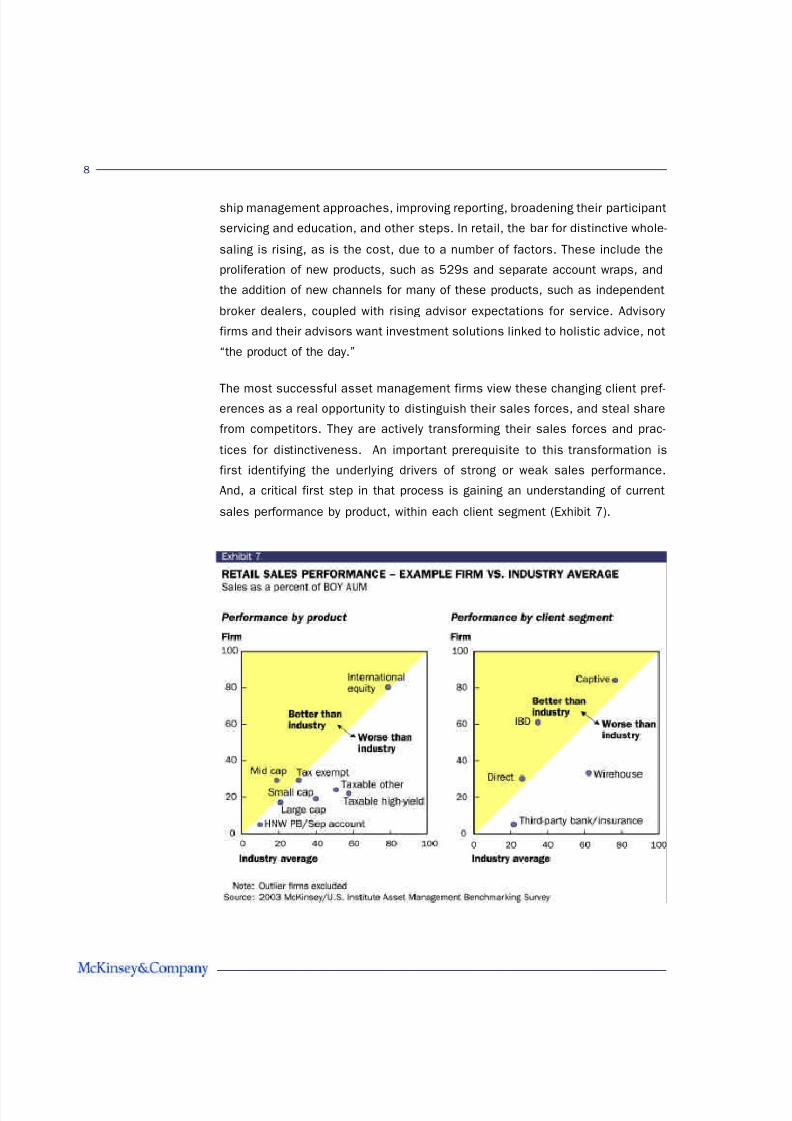

The most successful asset management firms view these changing client pref-erences as a real opportunity to distinguish their sales forces, and steal share

from competitors. They are actively transforming their sales forces and prac-

tices for distinctiveness. An important prerequisite to this transformation is

first identifying the underlying drivers of strong or weak sales performance.

And, a critical first step in that process is gaining an understanding of current

sales performance by product, within each client segment (Exhibit 7).

8

8/15/2019 Accelerating Into the Curve

http://slidepdf.com/reader/full/accelerating-into-the-curve 10/20

Focus on existing asset base to boost retention. Many in the industry have

long believed that investment performance is the only thing that influences

retention. While it is clearly a major driver, our survey reveals that there are

other important levers that can have real impact on reducing outflows. For

example, firms that invest in client servicing also realized substantially lower

outflow levels (Exhibit 8). In addition to investing wisely in client servicing, firms

with strong retention also pay their sales people (at least in part) on net sales

rather than purely gross sales, and have a deliberate retention management

approach tailored to each client segment.

ACHIEVING MARKET-LEADING PROFITABILITY

As we have discussed, many firms appear to have given up hope, for the

foreseeable future, of achieving profit margins that were common in the last

decade (i.e., in the mid-40 percent range). While our belief is that such profit

levels will no longer be the industry average, we believe that this level of prof-

9

8/15/2019 Accelerating Into the Curve

http://slidepdf.com/reader/full/accelerating-into-the-curve 11/20

itability, and even higher, is achievable for the best-run firms. The most prof-

itable firms will be those that excel at seven major revenue and cost levers:

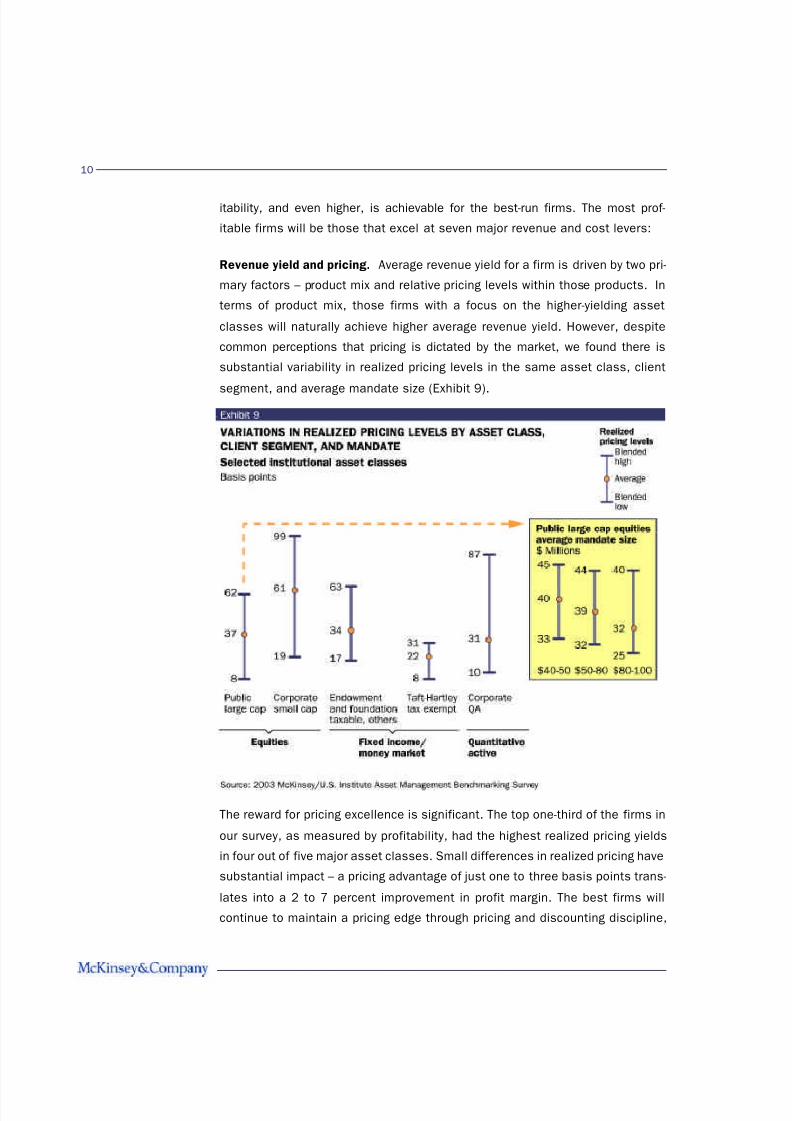

Revenue yield and pricing. Average revenue yield for a firm is driven by two pri-

mary factors – product mix and relative pricing levels within those products. In

terms of product mix, those firms with a focus on the higher-yielding asset

classes will naturally achieve higher average revenue yield. However, despite

common perceptions that pricing is dictated by the market, we found there is

substantial variability in realized pricing levels in the same asset class, client

segment, and average mandate size (Exhibit 9).

The reward for pricing excellence is significant. The top one-third of the firms in

our survey, as measured by profitability, had the highest realized pricing yields

in four out of five major asset classes. Small differences in realized pricing have

substantial impact – a pricing advantage of just one to three basis points trans-

lates into a 2 to 7 percent improvement in profit margin. The best firms will

continue to maintain a pricing edge through pricing and discounting discipline,

10

8/15/2019 Accelerating Into the Curve

http://slidepdf.com/reader/full/accelerating-into-the-curve 12/20

8/15/2019 Accelerating Into the Curve

http://slidepdf.com/reader/full/accelerating-into-the-curve 13/20

can result in closing or merging products when necessary. These processes

involve both manufacturing and distribution professionals, who are increasingly

adopting best practices from other industries, where many of these capabilities

are well-advanced.

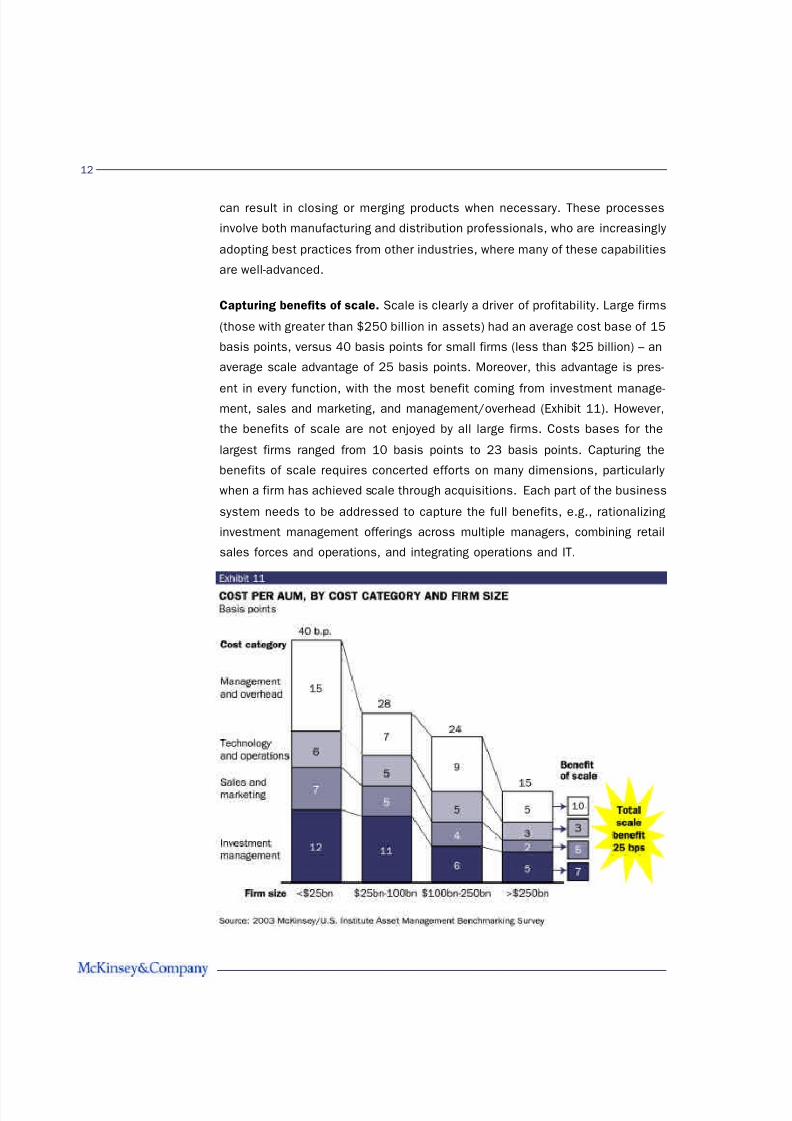

Capturing benefits of scale. Scale is clearly a driver of profitability. Large firms

(those with greater than $250 billion in assets) had an average cost base of 15

basis points, versus 40 basis points for small firms (less than $25 billion) – an

average scale advantage of 25 basis points. Moreover, this advantage is pres-

ent in every function, with the most benefit coming from investment manage-ment, sales and marketing, and management/overhead (Exhibit 11). However,

the benefits of scale are not enjoyed by all large firms. Costs bases for the

largest firms ranged from 10 basis points to 23 basis points. Capturing the

benefits of scale requires concerted efforts on many dimensions, particularly

when a firm has achieved scale through acquisitions. Each part of the business

system needs to be addressed to capture the full benefits, e.g., rationalizing

investment management offerings across multiple managers, combining retail

sales forces and operations, and integrating operations and IT.

12

8/15/2019 Accelerating Into the Curve

http://slidepdf.com/reader/full/accelerating-into-the-curve 14/20

Investment management productivity. The most successful firms are beginning

to focus on managing themselves as professional services firms, and paying

particular attention to their talent management approach. We believe that

investment professionals can be managed for productivity, as well as invest -

ment performance. However, currently the productivity of investment profes-

sionals varies considerably across firms – even when controlling for the asset

classes managed (Exhibit 12). Those firms that have the most productive

investment management professionals have total investment management

costs of five to seven basis points, considerably below the average of 10. Firms

that manage investment management costs most successfully did it through acombination of actions, including appropriate use of junior portfolio managers,

routine product rationalization, and use of commingled vehicles for smaller

accounts.

Sales and marketing productivity. With sales levels down for most asset man-

agers in both retail and institutional markets, many asset managers still need

13

8/15/2019 Accelerating Into the Curve

http://slidepdf.com/reader/full/accelerating-into-the-curve 15/20

to determine what is the sustainable size and composition of their sales and

marketing forces. Just as in investment management, the productivity gaps

between average and distinctive performers are high (Exhibit 13). Sales forces

need to be managed for the long term, not dramatically restructured simply

because of short-term product performance or market-related issues. Still,

many firms have substantial room for improvement in sales productivity, with

the cost of sales and marketing for institutional firms varying from 1 to 10 basis

points, and for retail firms varying from 3 to 20 basis points. In the institution-

al market, leading players are optimizing their sales force roles across asset

classes as well as major functions (e.g. specialized roles for client servicing).Success in retail wholesaling is primarily contingent on skilled external and

internal wholesalers who concentrate on three things: maintaining a few distri-

bution partners, as opposed to covering the waterfront; developing true part-

nerships with the distribution gatekeepers; and smartly targeting the most

productive advisors.

14

8/15/2019 Accelerating Into the Curve

http://slidepdf.com/reader/full/accelerating-into-the-curve 16/20

Technology and operations. Aggressive management of technology and oper-

ations spending has traditionally taken a distant back seat to meeting the

needs of investment and sales professionals for the latest applications.

However, this has come at a cost, with technology and operations spending cur-

rently accounting for an average of five basis points of assets under manage-

ment, and up to 20 basis points for some players (Exhibit 14). Leading firms

are taking a hard look at all of their operations, determining which functions are

strategic, and using multiple approaches to reducing costs, including process

redesign, outsourcing, and early forays into offshoring.

Management and overhead. Despite significant belt-tightening over the past 2

years, management and overhead currently accounts for almost 10 percent of

a typical firm’s cost base. The best firms have eliminated all non-essential cor -

porate services and consistently deliver high-quality, low-cost support to the

15

8/15/2019 Accelerating Into the Curve

http://slidepdf.com/reader/full/accelerating-into-the-curve 17/20

organization. The right approach for capturing potential savings in these areas

varies by type of firm. For firms that have grown organically (versus by acquisi-

tion) substantial cost reduction in the overhead functions typically requires a

clean sheet approach, in which the specific activities of each overhead function

are assessed to determine if their value exceeds their costs, and whether they

should be in-sourced or outsourced. For firms that have been built up via merg-

er, there are often substantial savings to be realized by combining duplicative

support activities across managers and business areas.

* * *

The U.S. asset management industry is maturing, and the competitive intensi-

ty is continuing to rise, leaving no doubt that strong growth and profitability will

be increasingly difficult to capture. However, the best firms are using this as an

opportunity to pull away from the pack, and are accelerating their investments

in managerial talent and capabilities. Now more than ever, we believe there are

real opportunities for senior managers to greatly influence the future of their

firms. Those who combine strategic and operational excellence will be best

positioned to achieve the outstanding returns this industry has to offer.

16

8/15/2019 Accelerating Into the Curve

http://slidepdf.com/reader/full/accelerating-into-the-curve 18/20

8/15/2019 Accelerating Into the Curve

http://slidepdf.com/reader/full/accelerating-into-the-curve 19/20

8/15/2019 Accelerating Into the Curve

http://slidepdf.com/reader/full/accelerating-into-the-curve 20/20

North American Asset Management Practice

September 2003

Designed by the New York Design Center

Copyright © McKinsey & Company

http://retail.mckinsey.com