abc theory ppt

TRANSCRIPT

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 1/29

ACTIVITY BASED COSTING

´ Vikas (37)

´ Ali (27)

´ Deepali (11)

´ Soumya (31)

´Mayur (08)´ Harish (25)

´ Sachin (50 batch 17)

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 2/29

INTRODUCTION

́Activity Based costing allows an organizationto determine the actual cost associated witheach product and service produced by the

organization.

´ The goal is to measure and then price out all

the resources used for activities that supportthe production and delivery of products andservices to customers

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 3/29

´ An organization performs activities to do itsbusiness. These activities define the businessyou are in.

´ All activities consume resources and the cost of these can be calculated.

´ The basis of ABC is to look at the activitiesrequired to produce the cost of the product or service.

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 4/29

WH AT¶SWH AT IN ABC?

´ Activity

´ Resource

´ Cost of the activity´ Cost driver

´ Activity driver

´ Cost object

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 5/29

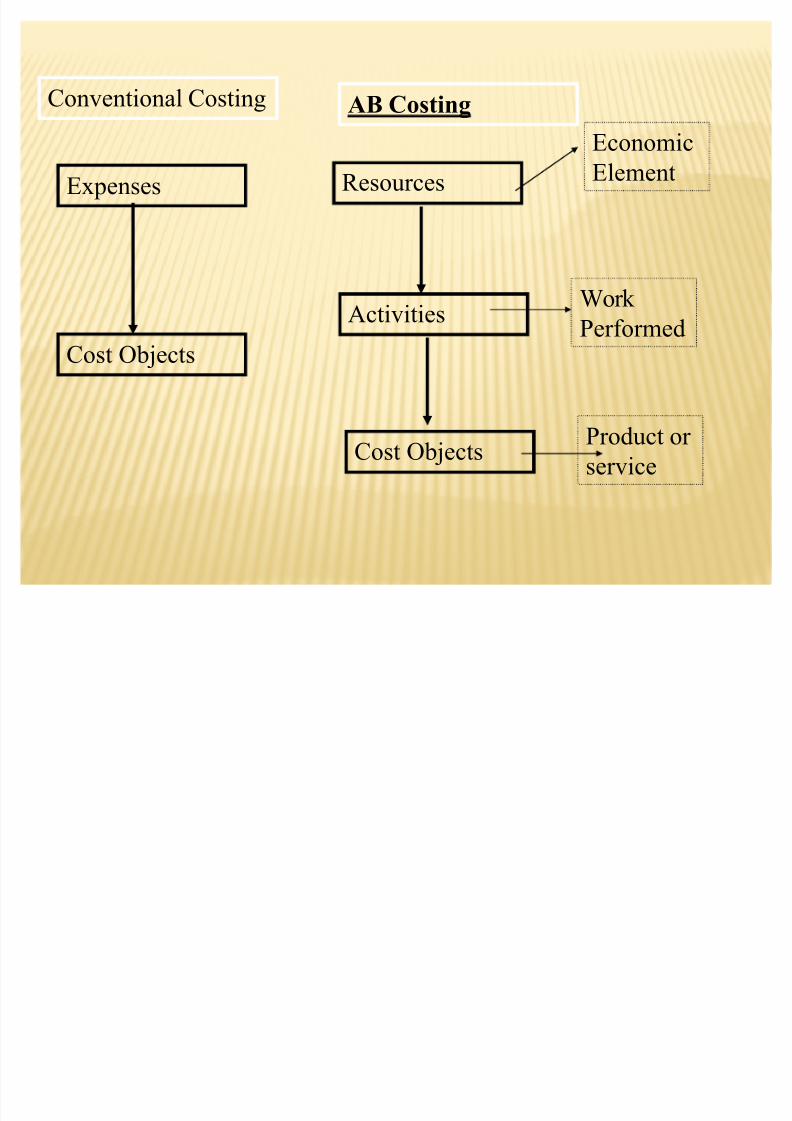

Conventional Costing

Expenses

Cost Objects

AB Costing

Resources

Activities

Cost Objects

EconomicElement

Work

Performed

Product or

service

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 6/29

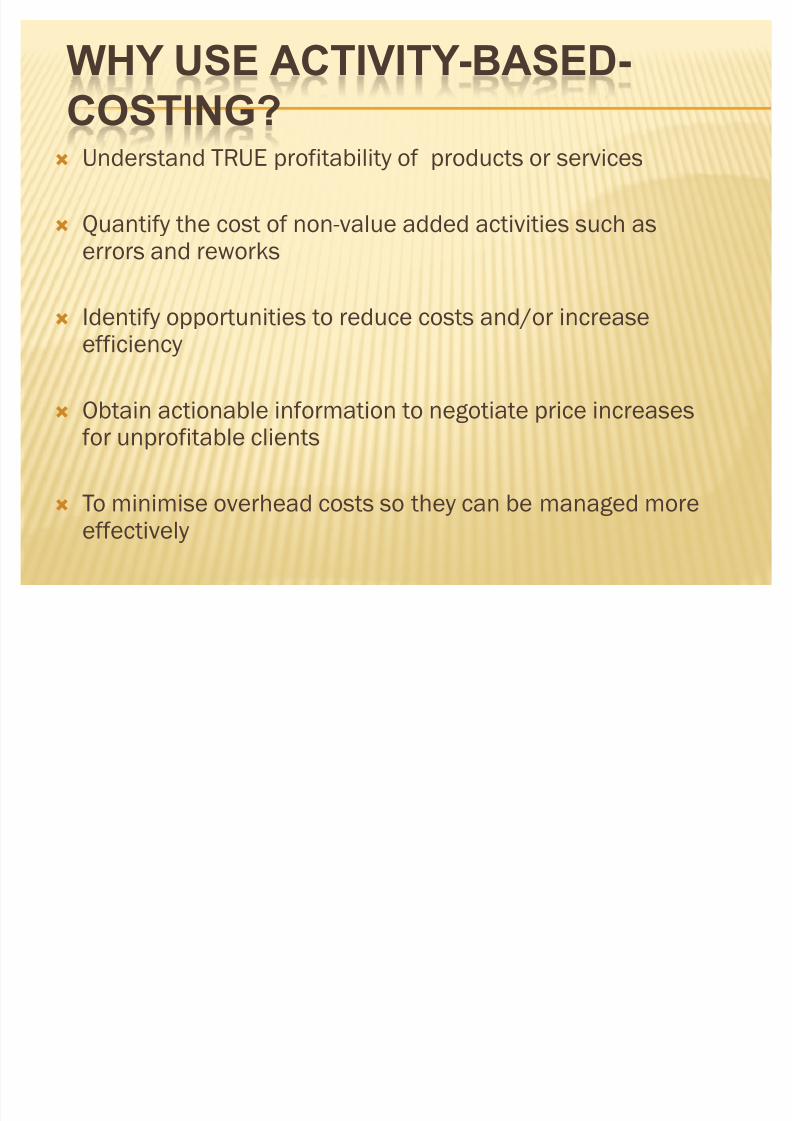

WHY USE ACTIVITY-BASED-

COSTING?

´ Understand TRUE profitability of products or services

´ Quantify the cost of non-value added activities such aserrors and reworks

´ Identify opportunities to reduce costs and/or increaseefficiency

´ Obtain actionable information to negotiate price increasesfor unprofitable clients

´ To minimise overhead costs so they can be managed moreeffectively

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 7/29

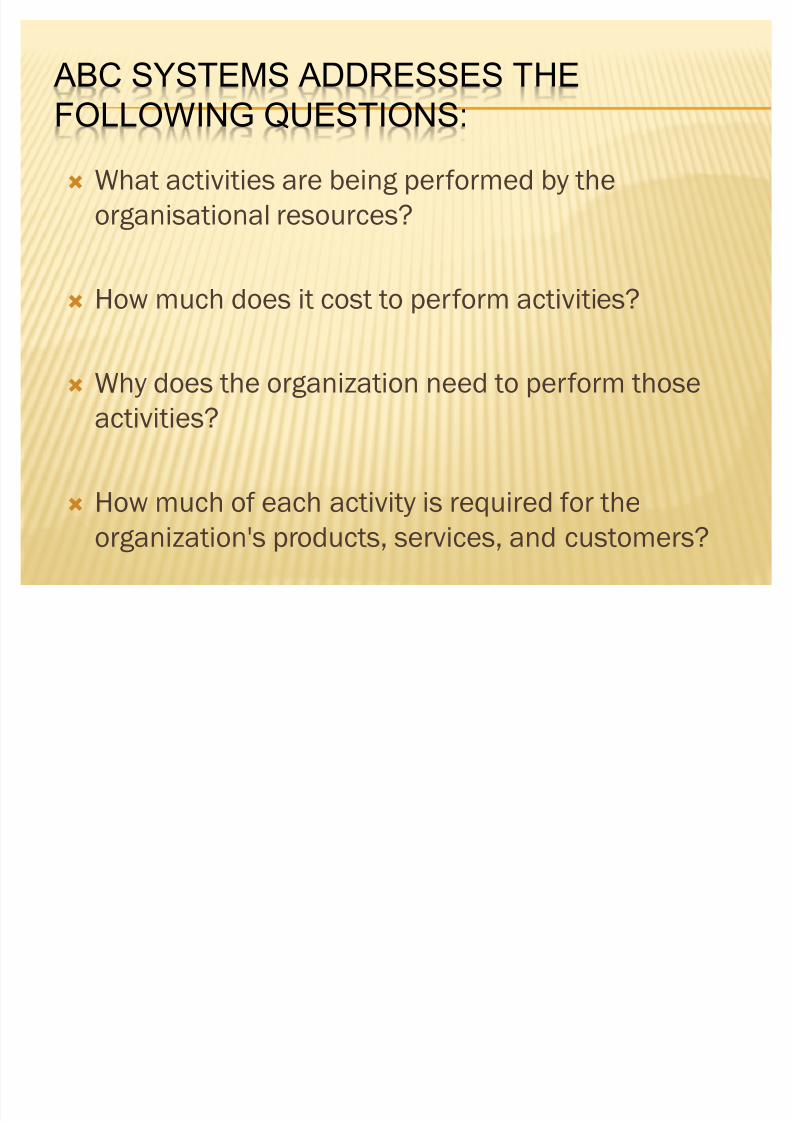

ABC SYSTEMS ADDRESSES THE

FOLLOWING QUESTIONS:

´ What activities are being performed by the

organisational resources?

´ How much does it cost to perform activities?

´ Why does the organization need to perform those

activities?

´ How much of each activity is required for the

organization's products, services, and customers?

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 8/29

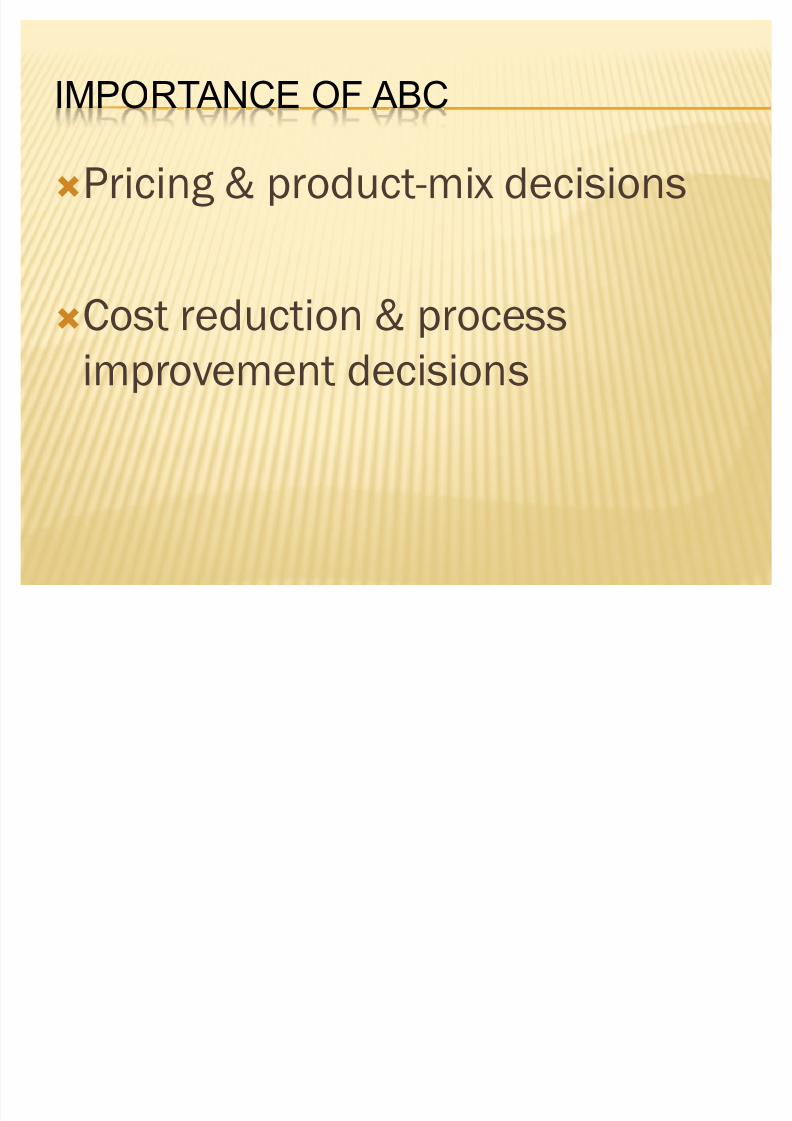

IMPORTANCE OF ABC

´Pricing & product-mix decisions

´Cost reduction & process

improvement decisions

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 9/29

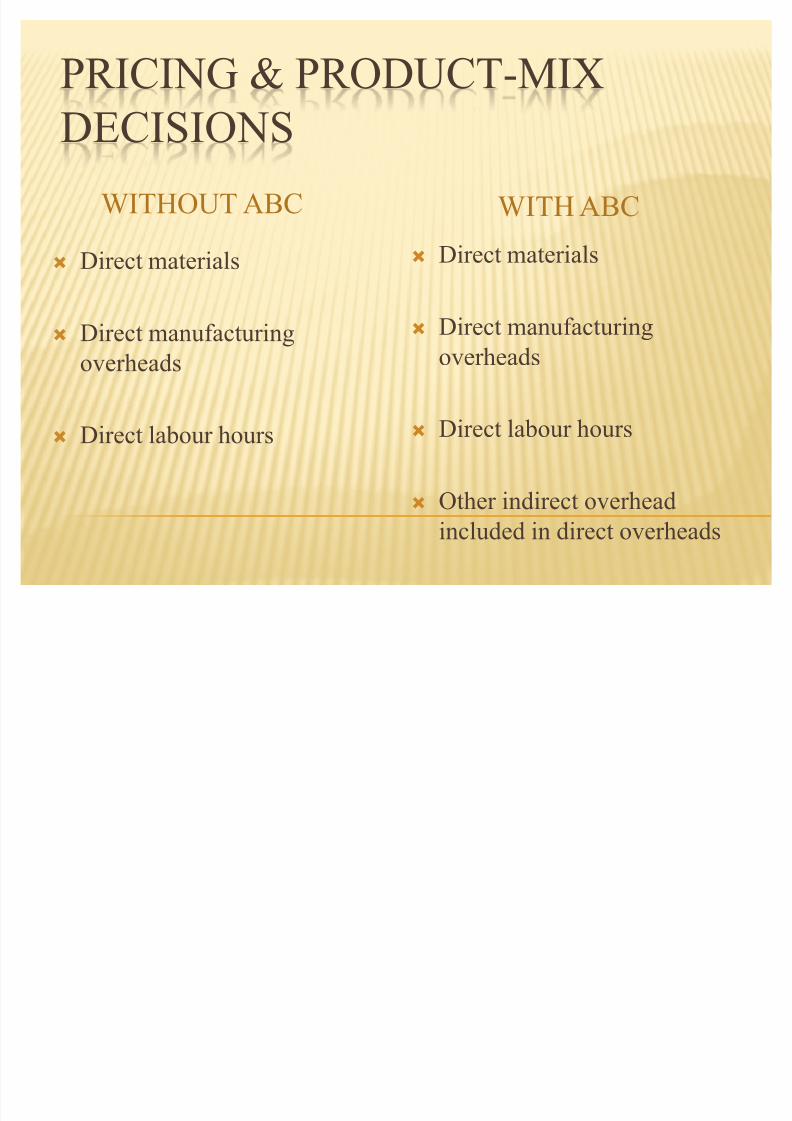

PRICING & PRODUCT-MIX

DECISIONSWITHOUT ABC WITH ABC

´ Direct materials

´ Direct manufacturing

overheads

´ Direct labour hours

´ Direct materials

´ Direct manufacturing

overheads

´ Direct labour hours

´ Other indirect overhead

included in direct overheads

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 10/29

ABC MODEL STRUCTURE

The first stage in an initial ABC study is to develop afundamental understanding of the Resources

(expenditures) and Activities (work performed) of anorganization. The Resources are then mapped to theActivities, thereby quantifying the cost of performing eachof these Activities. These costs are traced to Cost Objects(customers, products, or services) providing tremendousinsight into where an organization is making and losing money.

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 11/29

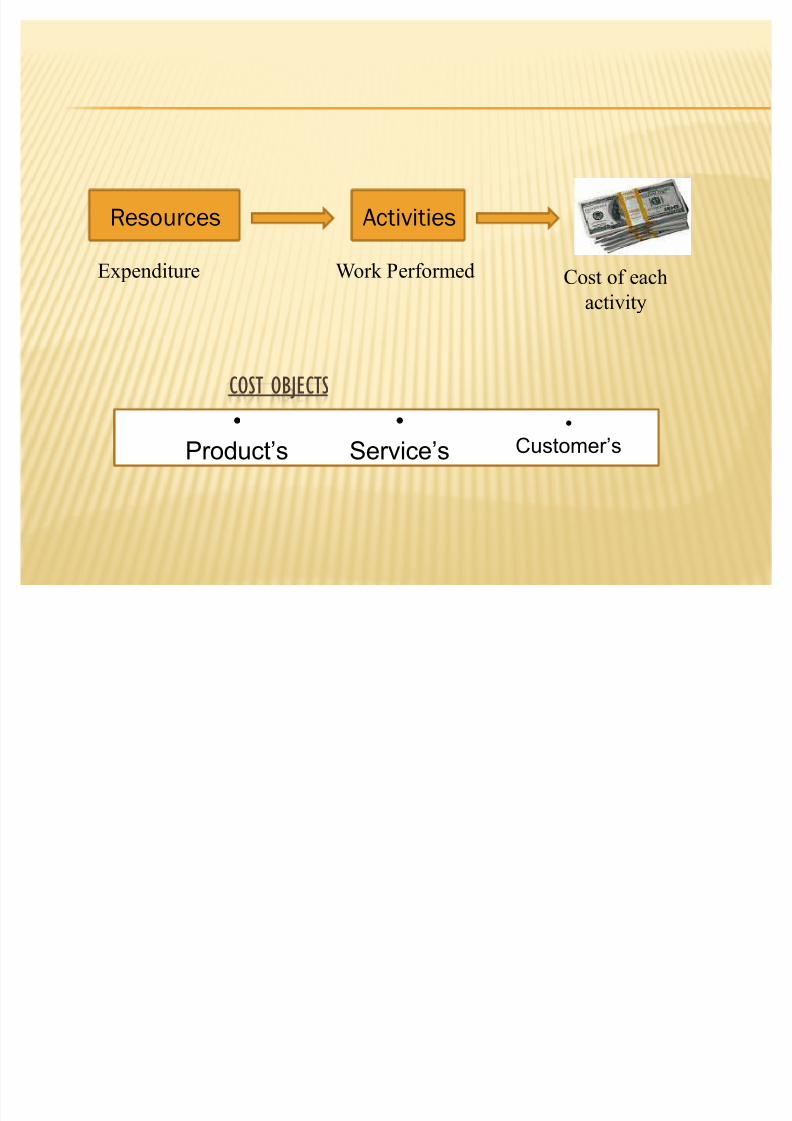

COST OBJECTS

Resources Activities

Expenditure Work Performed Cost of eachactivity

Product¶s

Service¶s

Customer¶s

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 12/29

MODEL/ STRUCTURE OF ABC

´ Identify the Resources

´ Determine Activities

´ Define Cost Objects´ Develop Resource Drivers

´ Develop Cost Drivers

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 13/29

IDENTIFY RESOURCES(EXPENDITURE OF AN ORGANIZATION)

´ Production Labour

´ Sales and Marketing Labour

´ Occupancy

´ Utilities

´ Expenses and Supplies

´ Etc..

Resources represent the expenditures of an organization.

These are the same costs that are represented in a

traditional accounting view; unlike traditional

accounting, ABC links these costs to products,customers, or services.

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 14/29

IDENTIFY ACTIVITIES(WORK PERFORMED)

´ Making sales calls to existing customers

´ Making sales calls to potential customers

´ Making customer service calls

´ Training product representatives

´ Evaluating products and improving product knowledge

´ Distributing samples

´ Attending trade shows and other events

Activities represent the work performed in an

organization. ABC Activities for the sales department in a

typical organization might include:

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 15/29

IDENTIFY COST OBJECTS(PRODUCT/ SERVICES/ CUSTOMERS)

ABC provides profitability by one or more cost object,

usually represented by products, customers, and/or

services.

Cost Object profitability is utilized to identify money

losing customers, to validate separate divisions or

business units, or to measure the performance of

individual projects, jobs, or contracts. Defining the

outputs to be viewed is an important step in a successful

ABC implementation.

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 16/29

DETERMINE RESOURCE DRIVERS(EXPENDITURE OF AN ORGANIZATION)

Resource Drivers provide the link between the

expenditures of an organization and the Activities

performed within the organization.

For example, the total salary of a customer service

representative would likely be allocated to the Activities

performed based on the amount of time spent performingthe Activity. If 50% of her time is spent performing the

activity, taking orders for existing customers, 50% of her

salary (including all costs such as benefits, taxes, and

insurance) would be allocated to this Activity.

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 17/29

DETERMINE COST DRIVERS(EXPENDITURE OF AN ORGANIZATION)

Determination of Cost Drivers completes the last stage of

the model. Cost Drivers trace, or link, the cost of

performing certain Activities to Cost Objects.

For example, taking orders for existing customers may be

linked to specific customers based on the number of

orders taken, if each order takes approximately the same

amount of time. If order taking time varies based on the

customer, this cost may be linked based on another driver

or multiple drivers.

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 18/29

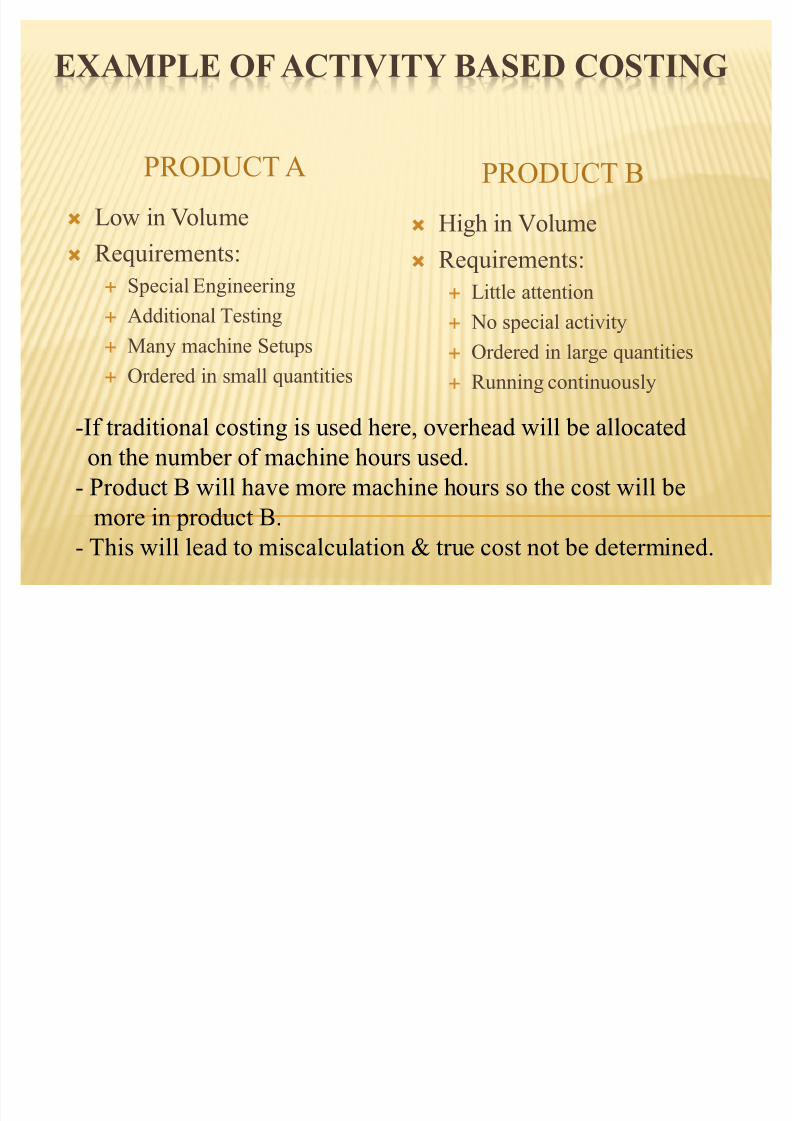

EXAMPLE OF ACTIVITY BASED COSTING

PRODUCT A PRODUCT B

´ Low in Volume

´ Requirements:

« Special Engineering

« Additional Testing

« Many machine Setups

« Ordered in small quantities

´ High in Volume

´ Requirements:

« Little attention

« No special activity

« Ordered in large quantities

« Running continuously

-If traditional costing is used here, overhead will be allocated

on the number of machine hours used.

- Product B will have more machine hours so the cost will be

more in product B.

- This will lead to miscalculation & true cost not be determined.

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 19/29

´ Activity Based Costing includes Special Engineering,

Special Testing, machine setups & other such activities

that include cost.

´ This cost will be assigned to the products that demands

such activities.

´ In our example product A will be charged with all suchcost. Whereas, in case of product B special activities cost

will not be include.

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 20/29

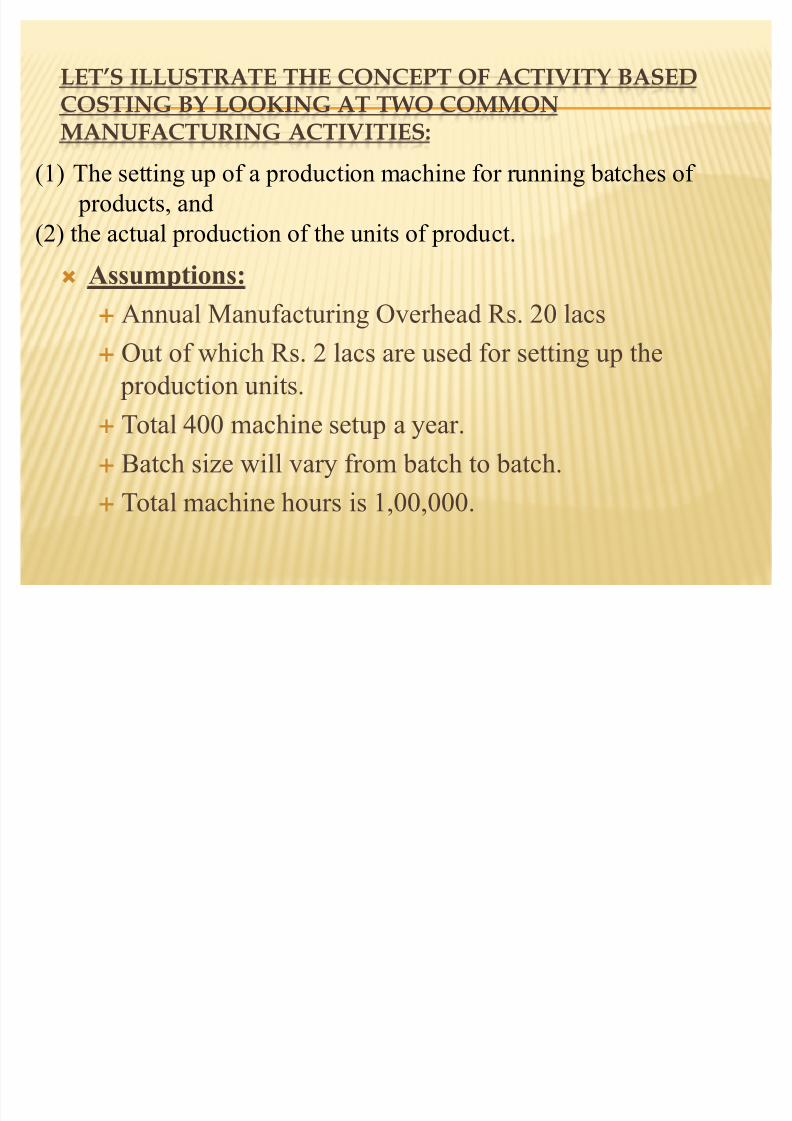

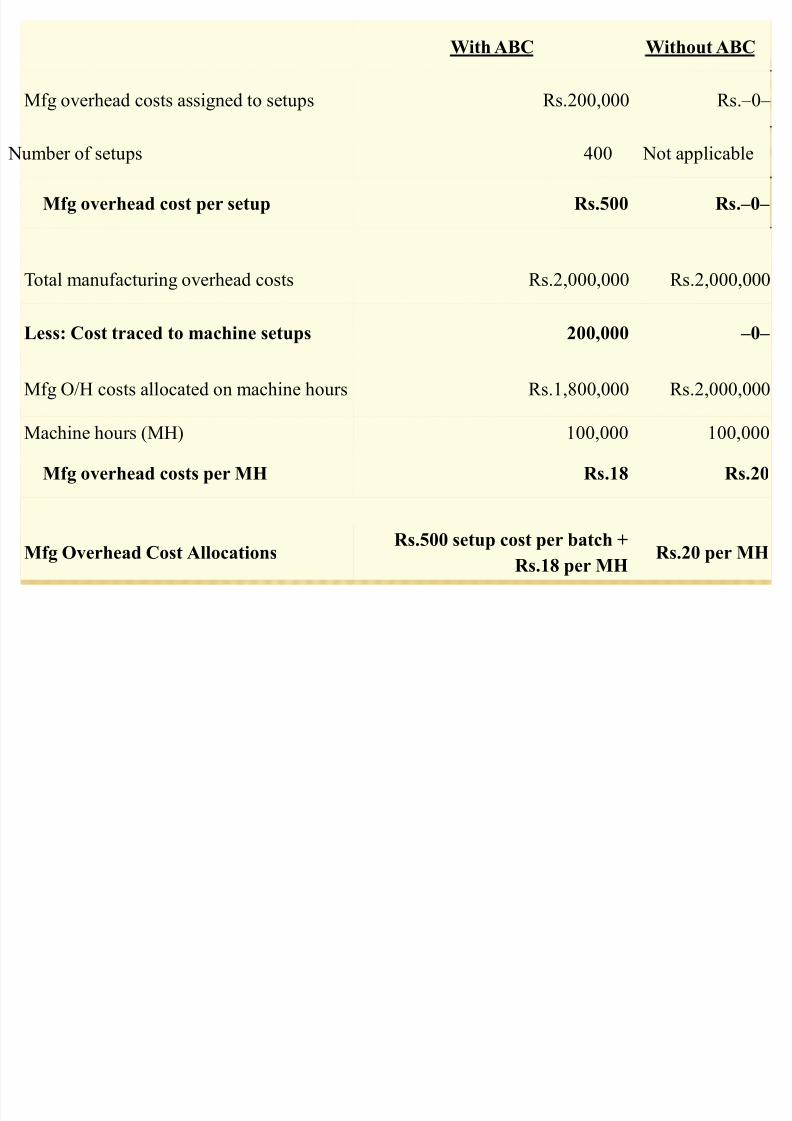

LET·S ILLUSTRATE THE CONCEPT OF ACTIVITY BASED

COSTING BY LOOKING AT TWO COMMON

MANUFACTURING ACTIVITIES:

´ Assumptions:« Annual Manufacturing Overhead Rs. 20 lacs

« Out of which Rs. 2 lacs are used for setting up the

production units.

« Total 400 machine setup a year.

« Batch size will vary from batch to batch.

« Total machine hours is 1,00,000.

(1) The setting up of a production machine for running batches of

products, and

(2) the actual production of the units of product.

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 21/29

With ABC Without ABC

Mfg overhead costs assigned to setups Rs.200,000 Rs.±0±

Number of setups 400 Not applicable

Mfg overhead cost per setup Rs.500 Rs.±0±

Total manufacturing overhead costs Rs.2,000,000 Rs.2,000,000

Less: Cost traced to machine setups 200,000 ±0±

Mfg O/H costs allocated on machine hours Rs.1,800,000 Rs.2,000,000

Machine hours (MH) 100,000 100,000

Mfg overhead costs per MH Rs.18 Rs.20

Mfg Overhead Cost Allocations

Rs.500 setup cost per batch +

Rs.18 per MH Rs.20 per MH

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 22/29

´ Let's see what impact these different allocation techniques

and overhead rates would have on the per unit cost of a

specific unit of output.

´ Assume that a company manufactures a batch of 5,000

units and it produces 50 units per machine hour, here is

how the cost assigned to the units with activity based

costing and without activity based costing compares:

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 23/29

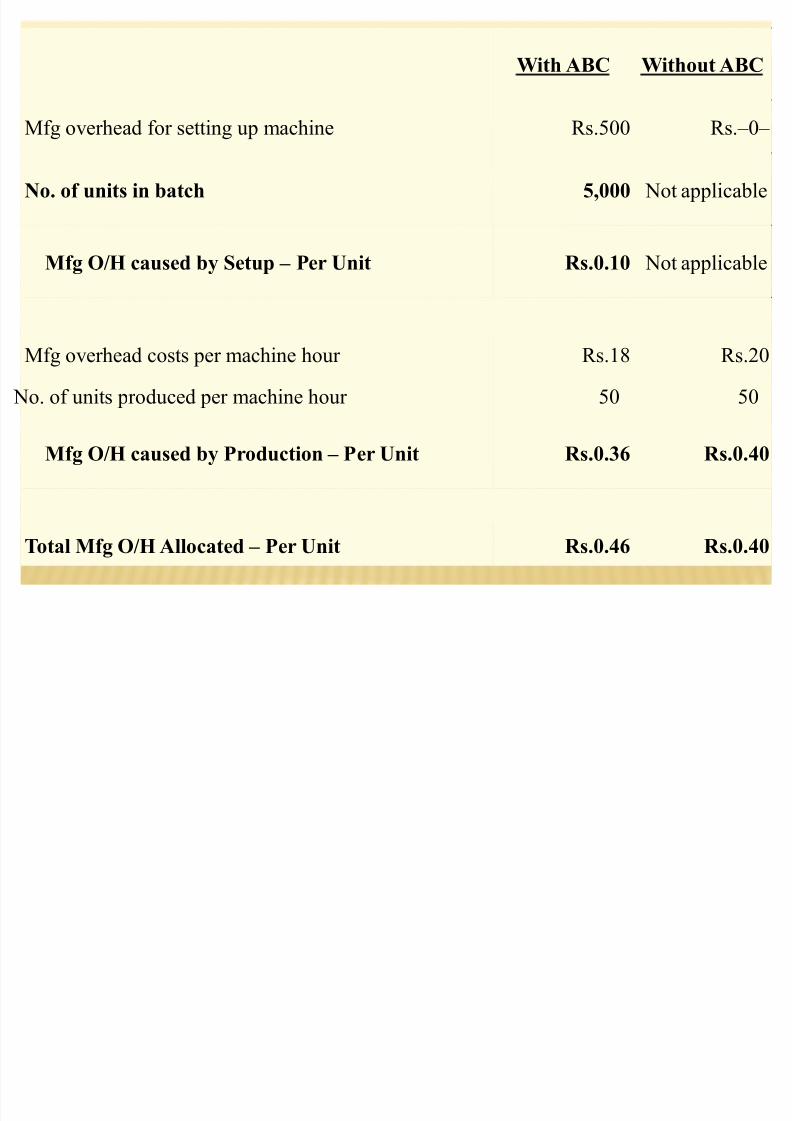

With ABC Without ABC

Mfg overhead for setting up machine Rs.500 Rs.±0±

No. of units in batch 5,000 Not applicable

Mfg O/H caused by Setup ± Per Unit Rs.0.10 Not applicable

Mfg overhead costs per machine hour Rs.18 Rs.20

No. of units produced per machine hour 50 50

Mfg O/H caused by Production ± Per Unit Rs.0.36 Rs.0.40

Total Mfg O/H Allocated ± Per Unit Rs.0.46 Rs.0.40

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 24/29

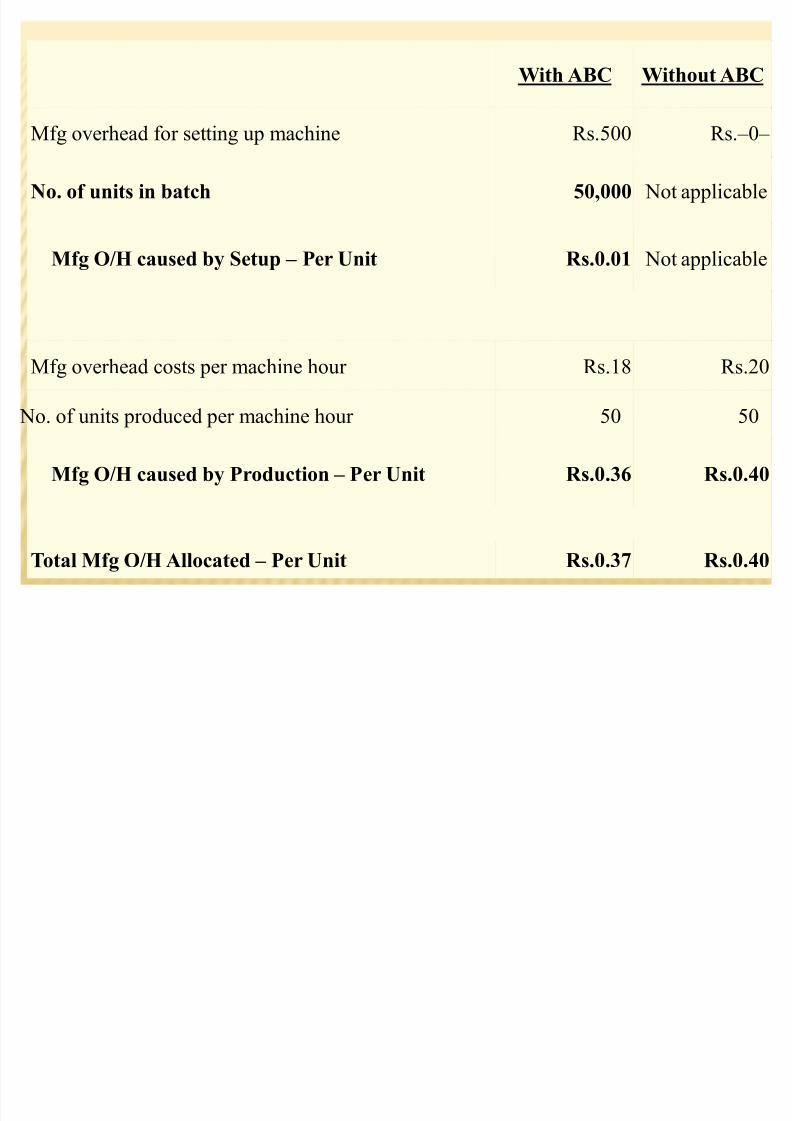

´ If a company manufactures a batch of 50,000 units

and produces 50 units per machine hour, here is how

the cost assigned to the units with ABC and withoutABC compares:

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 25/29

With ABC Without ABC

Mfg overhead for setting up machine Rs.500 Rs.±0±

No. of units in batch 50,000 Not applicable

Mfg O/H caused by Setup ± Per Unit Rs.0.01 Not applicable

Mfg overhead costs per machine hour Rs.18 Rs.20

No. of units produced per machine hour 50 50

Mfg O/H caused by Production ± Per Unit Rs.0.36 Rs.0.40

Total Mfg O/H Allocated ± Per Unit Rs.0.37 Rs.0.40

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 26/29

´ With activity based costing the cost per unit decreases from0.46 to 0.37 because the cost of the setup activity is spreadover 50,000 units instead of 5,000 units.

´ Without ABC, the cost per unit is 0.40 regardless of thenumber of units in each batch.

´ The company may end up doing lots of production for little or no profit.

´ The cost per unit using the activity based costing method ismore accurate in reflecting the actual efforts associated with

production.

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 27/29

LIMITATIONS

´ Costly to operate & difficult to understand

´ activity-cost rates needs to be updated

regularly

´ ABC surveys can be time-consuming, expensive

to perform and irritating to the employees who

have to provide the data

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 28/29

CONCLUSION

´ Better- informed decisions about pricing

´What type of customers to pursue

´What products or services to offer´ Helps to measure the costs & profits of an

organization based on the activities

´

Helps to determine accurately how eachprocess relates back to specific products,

customers, or services.

8/8/2019 ABC Theory Ppt

http://slidepdf.com/reader/full/abc-theory-ppt 29/29

TH ANK YOU