a union perspective on the global financial crisis peter conway secretary n z council of trade...

TRANSCRIPT

A UNION PERSPECTIVE ON A UNION PERSPECTIVE ON THE GLOBAL FINANCIAL THE GLOBAL FINANCIAL

CRISISCRISIS

Peter ConwaySecretaryN Z Council of Trade Unions

International crisisInternational crisisBegan as financial crash in the USSpread to Europe and rest of worldVery quickly because of integration, lack of regulation of

international capitalUS$30 trillion loss in sharemarkets to March 2009 – largest

everUS$1.9 trillion internationally to bail out banks

2

Causes?Causes?Leverage – from 8 or 12:1 to 30:1 or even

higherCollaterised debt obligations, credit default

swaps, derivatives – pooling/securitisationMexican strawberry picker in the US

earning an average of $14,000 a year and granted a 100% mortgage to buy a house for $750,000

More on causes….More on causes….

Deregulation - repeal of the Glass-Steagall Act in 1999

Derivatives excluded from Commodity Futures Modernization Act in 2000.

Bush's policy of "voluntary" regulation of investment banks at the SEC

Global imbalancesFinancialisation, hollowing out, and growth of

private equity/hedge funds

Finance Sector GrowthFinance Sector Growth

From 1973 to 1985, the financial sector never earned more than 16 percent of domestic corporate profits.

This decade, it reached 41 percent. From 1948 to 1982, average compensation in

the financial sector ranged between 99 percent and 108 percent of the average for all domestic private industries. From 1983, it shot upward, reaching 181 percent in 2007.

Finance Sector GrowthFinance Sector Growth

Alternative ViewsAlternative ViewsGreenspan held interest rates too low for

too long, thus distorting the prices to which the market responded.

US Government was actually encouraging banks to lend to sub-prime borrowers.

Government spending far more than it raised in taxes and thus running protracted budget deficits.

Alternative ViewsAlternative Views

Community Reinvestment Act, which prevents banks from "redlining" minority neighbourhoods as not creditworthy.

Fannie Mae and Freddie Mac for causing the trouble by subsidising and securitising mortgages with an implicit government guarantee.

Mark to market accounting.

Decline in Bank Market Value Decline in Bank Market Value 2007 to 20092007 to 2009

Global ImbalancesGlobal Imbalances

Bollard to Jobs SummitWestern countries need to save more,

export more and adjust to lower currencies

Eastern countries have to consume more, run down Reserves and adjust to higher exchange rates

The real economyThe real economy

11

Spread to real economy:

Rapidly falling house pricesCompanies unable to expand or renew

debtPeople and firms cut spendingParticularly affected trade …

World tradeWorld trade

New York Times, 11 April 2009 12

… … and manufacturing:and manufacturing:

Industrial ProductionIndustrial Production

Effects of crisis so farEffects of crisis so far

14

“73 to 103 million more people will remain poor or fall into poverty” as a result – mainly in East and South Asia (UN)

4.1% contraction expected in the OECD in 2009, 8.3% unemployment in 2009, 9.8% in 2010

Huge loss in outputHuge loss in output

15

US$8 trillion loss so far –almost two months output of the world economy

US$5.5 trillion stimulus so far in the US, Europe and Asia

OECD expects to contract by 4.1% in 2009 Unemployment:

– OECD forecast 8.3% in 2009, 9.8% in 2010– Currently 10.2 % in US (26 year high)

16

IMF now says!IMF now says!

IMF blames policymakers for "a general belief in light-touch regulation based on the assumption that financial market discipline would root out reckless behaviour and that financial innovation was spreading risk, not concentrating it. Both these assumptions proved wrong, and the result was a massive asset price bubble ...".

Bank of England says..Bank of England says..

Andrew Haldane, the Bank of England’s executive director for financial stability, says failures due to “disaster myopia” (the tendency to underestimate risks), a lack of awareness of “network externalities” (spill overs from one institution to the others) and “misaligned incentives” (the upside to employees and the downside to shareholders and taxpayers).

Australia and New Zealand Australia and New Zealand New Zealand and Australia not as hard hit

– Sounder banking system – less competition? Less savings? Banks would have if they could have? (Former Governor of the Reserve Bank of Australia, Ian Macfarlane)

Australia hit less – Partly due to China; partly government

response– Did not go into recession, unemployment at

5.7% - less than New Zealand

19

New Zealand New Zealand

Trade falls, commodities hit less Economy appears to have stopped contracting Unemployment at 6.5%, still rising – consensus

forecasts for over 7% in 2010 and 2011 (but Reserve Bank forecasts 6.9% peak in March 2010)

Manufacturing and construction particularly hard hit Exchange rate over US$0.70 – hurting exporters But cautious optimism

20

Recession + Familiar Recession + Familiar ProblemsProblems

Current account deficitLow productivity levels and growthGDP per capita trendsLow savingsSmall export sectorHigh dollar/monetary policy

Real GDP per capita as ratio of Real GDP per capita as ratio of OECD averageOECD average

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Australia Denmark New Zealand United Kingdom United States

Household Debt 1995 to 2009Household Debt 1995 to 2009

Source: Treasury Monthly Economic Indicators, October 2009

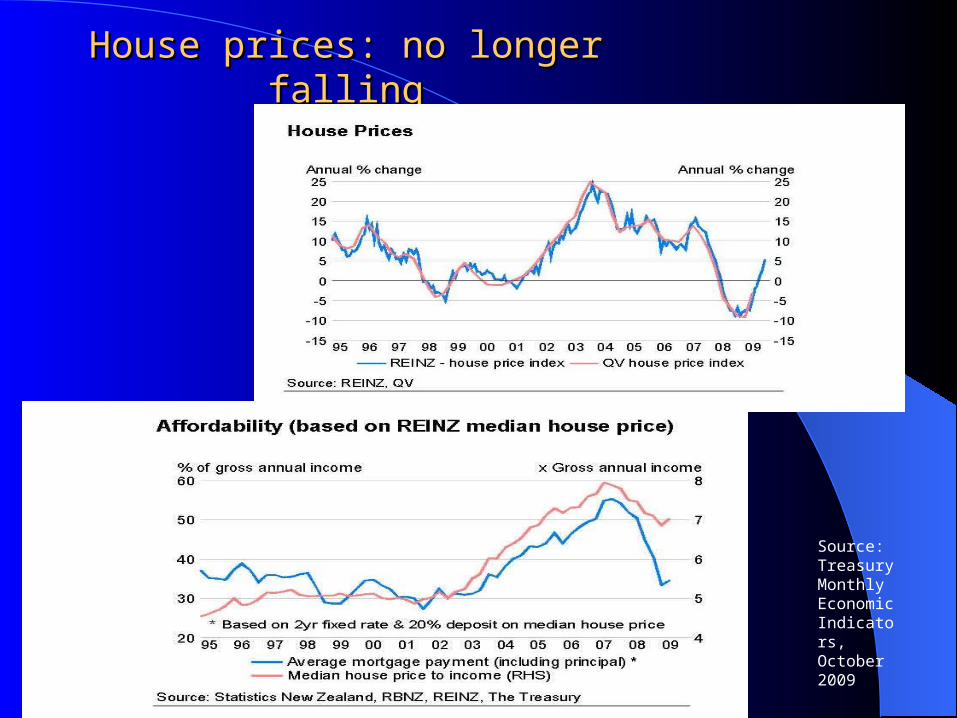

House prices: no longer fallingHouse prices: no longer fallingDespite Despite predictionspredictions

Treasury Budget forecast: House prices to decline nearly •8% in the year to March 2010•4% in the year to March 2011.

In fact – values are now only 1.1% below the same time last year, but 7.1% below 2007 peak

September 2009September 2009(Quotable Value)(Quotable Value)

House prices: no longer fallingHouse prices: no longer falling

Source: Treasury Monthly Economic Indicators, October 2009

31

Budget 2009Budget 2009 Increased expenditure $3 billion this Budget Of which “operating allowance” for new spending $1.45 billion

(down from $1.75 b) But only $1.1 billion in future years (growing at 2% per year).

Health usually takes $750 m! Capital allowance $1.45 billion for Budgets 2009 to 2012 Cuts in spending to pay for new priorities

– Superannuation fund– Adult and Community Education– Pay and Employment Equity Unit– Public service redundancies and continuing reviews…

Greatly increased debt Did they do enough?

33

Public Debt Public Debt (Percent of GDP)(Percent of GDP)

36

Source: IMF World Economic, Sept 2009

New Zealand

More on DebtMore on Debt

September net debt 11.8% of GDPUK net debt 59.2% of GDPNZ Gross debt 26.9% of GDPWas 35.7% in 1999

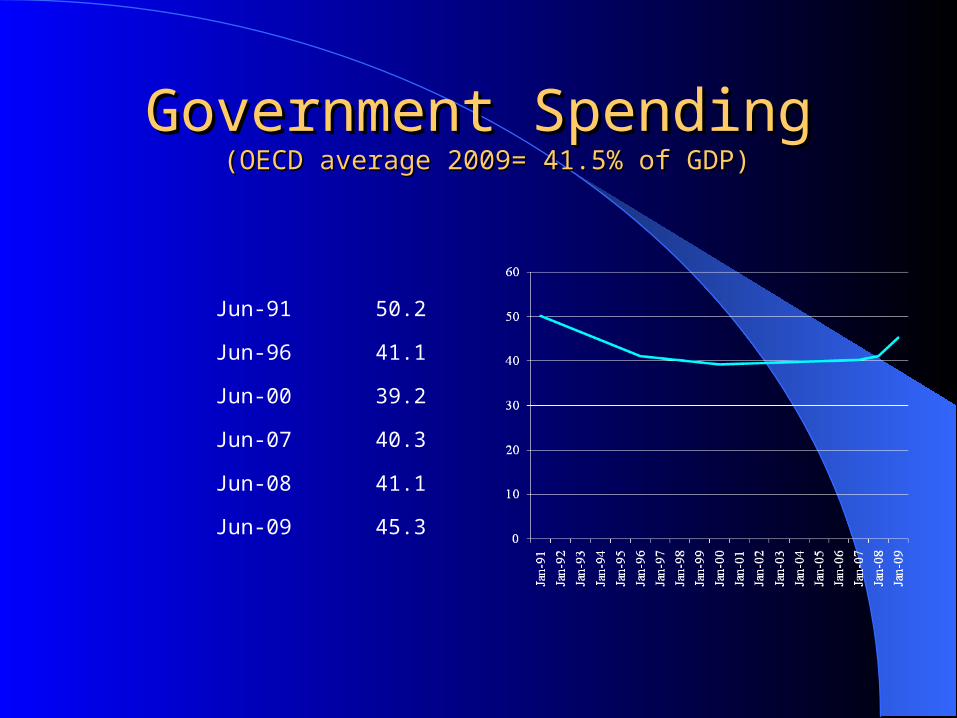

Government SpendingGovernment Spending (OECD average 2009= 41.5% of GDP) (OECD average 2009= 41.5% of GDP)

Jun-91 50.2

Jun-96 41.1

Jun-00 39.2

Jun-07 40.3

Jun-08 41.1

Jun-09 45.3

The Wages QuestionThe Wages Question

Share the pain… weren’t so keen on sharing the gain

Still shortages in many areas

Pressures – CPI, affordability, line-by-line reviews, tax cuts, jobs focus

Catch up with Australia – ever?

Is it over?Is it over?New ZealandNew Zealand

Unemployment will continue to rise – but not as much as originally feared

Banks safe – but finance sector still shaky Exports down, exchange rate a barrier, but

commodity prices holding Manufacturing and construction seem to have

bottomed out But big risk of housing price bubble reigniting Risk of jobless growth Constraints on government spending – some real,

some political

Is it over? - Is it over? - OverseasOverseas UK still in recession, US coming out – due to govt Still very high unemployment, low trade Still concerns about the financial sector…

– CIT Group, 100-year-old lender, filed for bankruptcy yesterday, will probably cost US taxpayers around US$2.3 billion. “Stocks tumbled around the world amid renewed fears about the state of the U.S. financial sector.”

…and back to their old ways– The biggest US banks (e.g. Goldman Sachs, JPMorgan Chase) which have grown even bigger due

to takeovers and have received tens of billions of US government money “are once more betting big on bonds, commodities and exotic financial products, trading that nearly stopped during the financial crisis”

– “the five biggest banks’ average potential losses from a single day of trading topped $1 billion, up 76 percent from two years ago”

– Bailouts came quickly, but new financial regulation has been slow, in large part because of resistance from the financial sector.

“

Now on the agenda… Now on the agenda… A lot of rethinking of old assumptions –

– More, not less government– Stabilisation approach– Address underlying causes of domestic recession

and economic vulnerability– Green New Deal?– Case for nationalisation– Regulation and global supervision of local and

international finance– Changing power relationships – e.g. G20– Greater development focus internationally

44

Principles to stand byPrinciples to stand by Fairness

– Greater equality, equity and valuing diversity Participation

– Te Tiriti, and greater voice in workplaces and society Security

– Security of employment and income, role of the state Improving living standards

– Wages, social wage, leisure, our environment Sustainability

– Economic, social, cultural, environmental

A framework for changeA framework for change

Sustainable economic development– A strong economy which takes account of

its side effects on the environment, society and cultures

Decent work and a good life– Good and fair wages, rewarding jobs,

effective unions, secure employment, social protections , low inequality, social equity

Voice: real participation in workplace, economic and community decision-making

Economic DevelopmentEconomic Development

Government support of firms, with conditionsi.e. employment creation / export or import substitution potential / industry standard employment agreements / commitment to skills development / fair remuneration / progress to pay equity

Buy back Telecom’s physical network and begin to buy back the electricity system

Support Māori economic development Encourage worker cooperatives and other

alternative investment

47

Financial and Monetary PolicyFinancial and Monetary PolicyCloser oversight over financial institutionsStabilise exchange rate

– Management of international capital flows / currency controls / cooperation with other nations

Reserve Bank to:– Take action on exchange rate and

international capital flows– Have broader monetary policy including

employment, living standards, etc.Finance for investment in NZ (Kiwi bonds, NZ

Super Fund) 48

International Economic International Economic RelationshipsRelationships

Support better international financial regulation and supervision

Support a cross-border financial transactions (Tobin) tax

Manage international capital movements to and from NZ

New internationalism: need for cooperation rather than market approach (e.g. trade agreements)

Controls on foreign direct investment49

TaxationTaxation

Introduce a 45% tax rate for incomes $150,000+

End deductibility of losses in investment property against personal income

Capital gains tax exempting primary homes

Land tax exempting most primary homes Research and development funding for

firms

50

EnvironmentEnvironment

Green New Deal– Tax breaks for investment in

environmentally beneficial technology or services

Investment in skills for a low carbon economy

Just transition for workers and communities affected by climate change policies

Alternatives to gross domestic product (GDP) to measure progress

51

ProductivityProductivity

Establish Productivity Commission which includes support for workplace initiatives

Address poor returns to workers from productivity gains– Living Standards Review Authority

with tripartite involvement

52

EmploymentEmployment Skills Investment Fund Booster package (after 13 weeks

unemployment) Flexisecurity

– 90% income replacement on job loss– Active labour market policies– Support for up-skilling– Tripartite design and governance

Increase minimum wage: $16.87 (66% of average wage) Good employer criteria for those seeking permanent

skilled migrants Pay and Employment Equity workplace assessments

53

HousingHousing Low interest funding for new housing through Reserve Bank Assessment of housing need to create a National Housing

Strategy More low cost housing

– Expand NZ’s housing stock by 20%– Local council/developers to meet quota of affordable

housing– Increase tenant security by reforming tenancy laws– Sponsor designs of low cost, green, healthy housing

Increase affordability by – Subsidised lending for low income/disadvantaged groups– Expand shared equity and Kiwisaver house purchase

schemes

54

RetirementRetirement

Enhanced Kiwisaver scheme:– 6% compulsory employer contributions

(phased in over 4 years)– 2% compulsory employee contribution– 2% government top-up

Allow beneficiaries and non-working parents to receive government contributions equivalent to 6% of average wage

Inquiry into equity issues for those on low pay rates and women

55

ParticipationParticipation

Improve worker participation through:– Representative structures in workplaces– Industry sector councils (productivity/ skills/

industry development / firm networking)– Mechanisms for workers voice

Enterprises (20+ workers) to provide access for community organisations /local govt to consult workers

Increase depth and diversity of NZ media– Trust-owned ‘public service’ newspapers and

other media– Funding for investigative print journalism

56

ConclusionConclusion Workers did not create this economic crisis Worst financial crisis in 70 years Opportunity to rethink unfair and

unsuccessful economic and social policies