a new market for energy regulation: advancing the … new market for energy regulation: advancing...

TRANSCRIPT

1

NCSL Task Force on Energy Supply

December 5, 2012

David W. Cash

Commissioner

Massachusetts Department of

Public Utilities

A New Market for Energy Regulation:

Advancing the Clean Energy

Revolution

The Energy Landscape in

Massachusetts, or

The Case for an Aggressive

Clean Energy Agenda

2

3

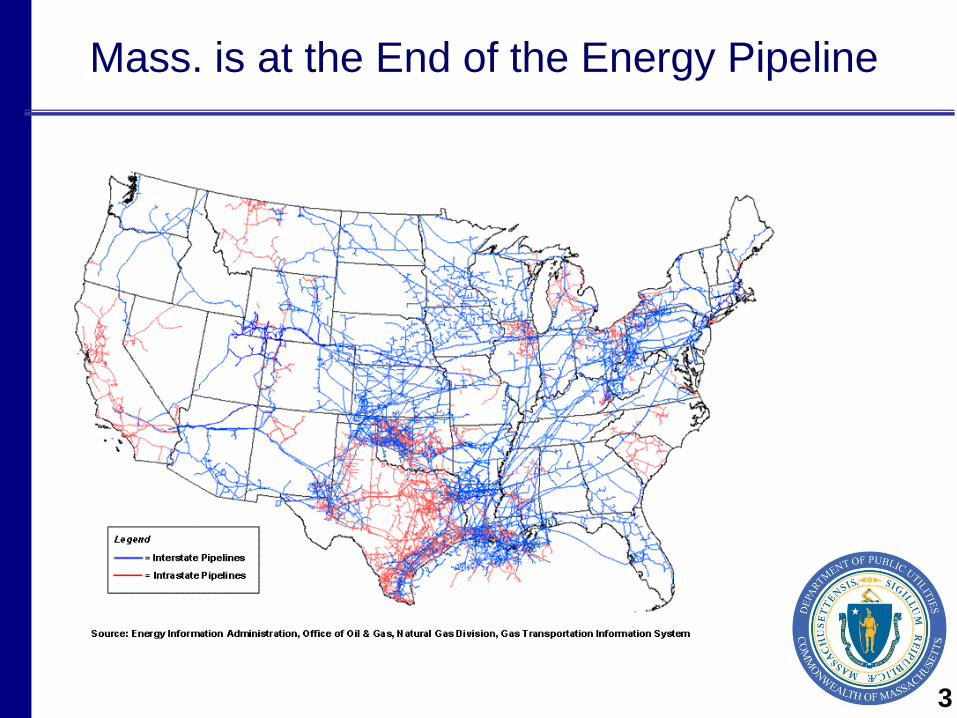

Mass. is at the End of the Energy Pipeline

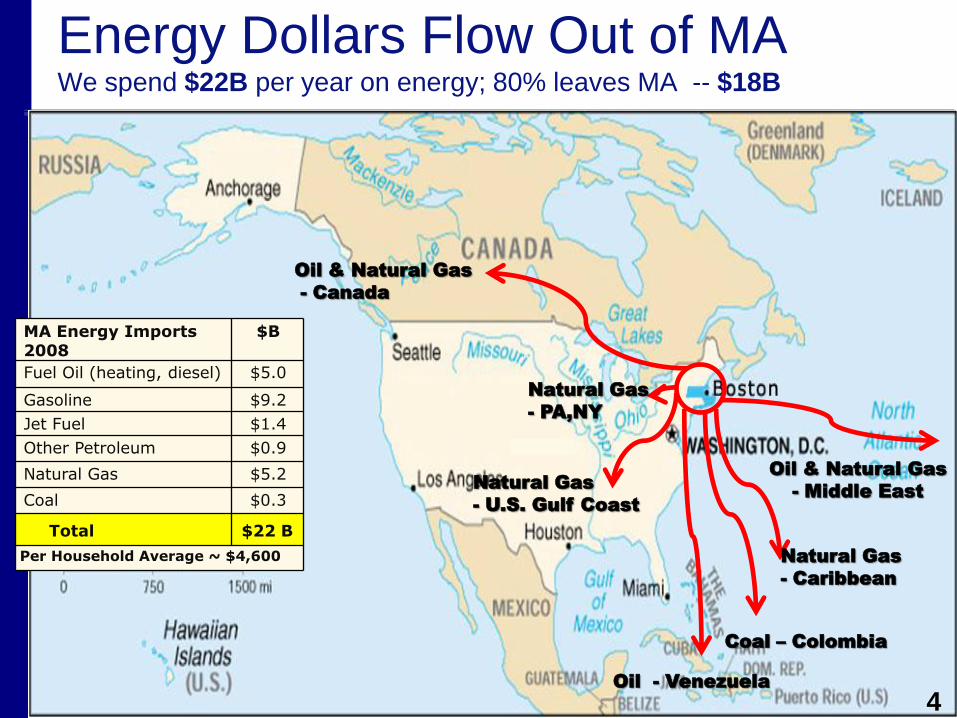

Energy Dollars Flow Out of MAWe spend $22B per year on energy; 80% leaves MA -- $18B

Oil & Natural Gas

- Canada

Oil - Venezuela

Oil & Natural Gas

- Middle East

Coal – Colombia

MA Energy Imports 2008

$B

Fuel Oil (heating, diesel) $5.0

Gasoline $9.2

Jet Fuel $1.4

Other Petroleum $0.9

Natural Gas $5.2

Coal $0.3

Total $22 B

Per Household Average ~ $4,600 Natural Gas

- Caribbean

Natural Gas

- U.S. Gulf Coast

4

Natural Gas

- PA,NY

Energy Costs: Low now; Will inevitably increase

and remain volatile in the future

5

Concerns about Fuel Diversity

ISO-NE 6

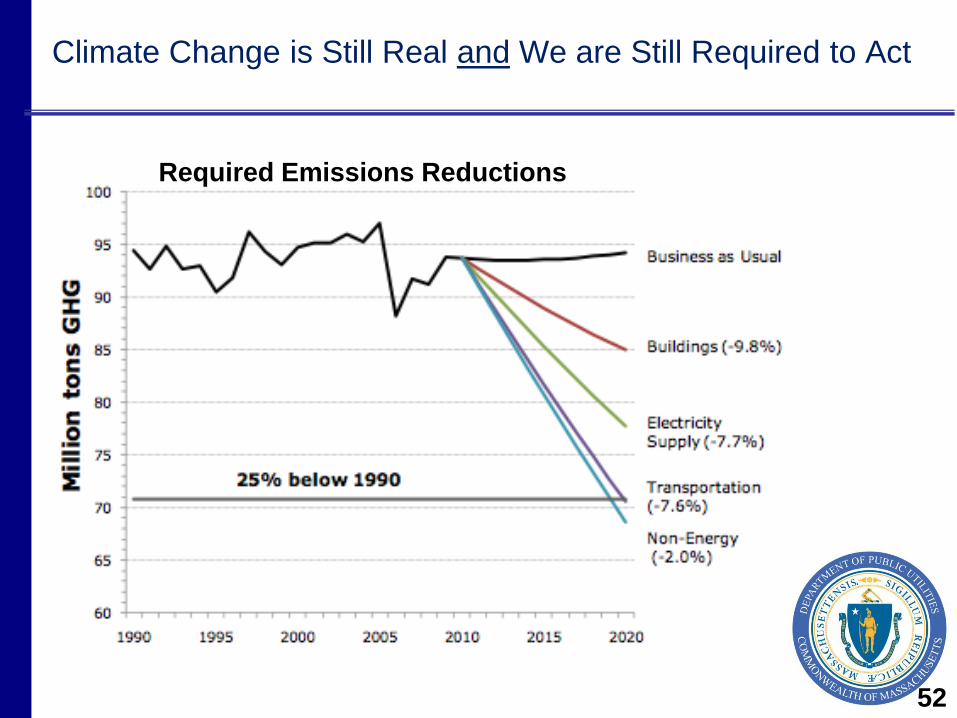

Mass. Has One of the Most Aggressive Climate

Policies

7

Required Emissions Reductions

Seizing the Window of

Opportunity

8

A Clean Energy Policy Revolution Since

2007

9

An integrated approach in legislation,

regulation and investment to:

• Lower energy costs

• Mitigate volatility

• Grow clean energy sector

• Become more energy independent

• Improve the environment

A Clean Energy Policy Revolution Since

2007

10

New Tools:

• All cost-effective Energy Efficiency

must be procured by distribution

utilities

• De-coupling to align incentives for

utilities

• Renewable Portfolio Standard to

send the right market signals

A Clean Energy Policy Revolution Since

2007

11

New Tools:

• Requirement of long-term contracts

to provide certainty for the

development community

• Incentivize and remove regulatory

barriers to net-metering to expand

distributed generation

• Remove regulatory barriers to

expedited interconnection

A Clean Energy Policy Revolution Since

2007

12

New Tools:

• Create a level playing field for demand

resources and renewable energy in

Regional Markets

• Open proceeding to explore the right

regulatory path for grid modernization

and dynamic pricing.

• Create innovation center and state

funding to help fund clean energy

development and job growth

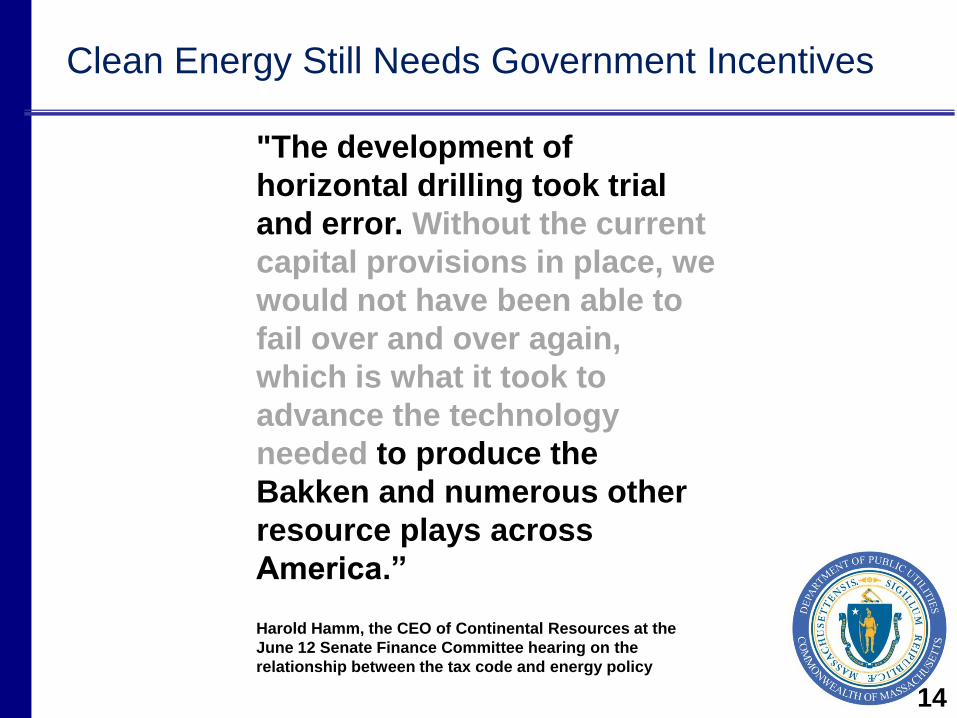

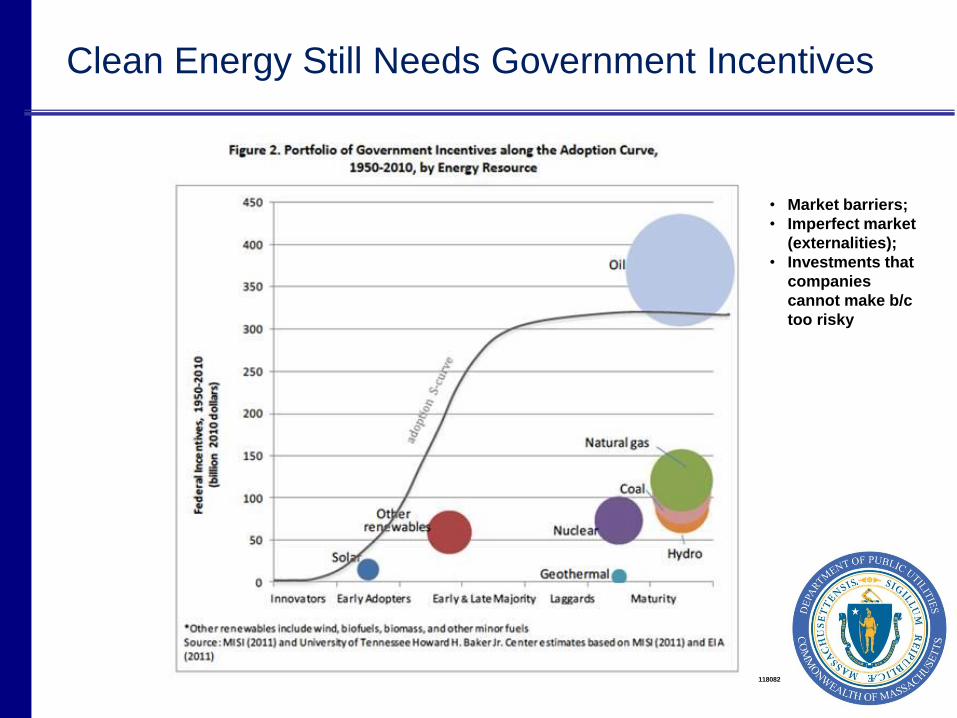

Clean Energy Still Needs Government Incentives

“…Without the current

capital provisions in place, we

would not have been able to

fail over and over again,

which is what it took to

advance the technology

needed…”

13

Clean Energy Still Needs Government Incentives

"The development of

horizontal drilling took trial

and error. Without the current

capital provisions in place, we

would not have been able to

fail over and over again,

which is what it took to

advance the technology

needed to produce the

Bakken and numerous other

resource plays across

America.”

Harold Hamm, the CEO of Continental Resources at the

June 12 Senate Finance Committee hearing on the

relationship between the tax code and energy policy

14

The Results

15

Solar PV in MA (through Sept, 2012)C

um

ula

tive

Ca

pa

cit

y (

MW

)

-

20

40

60

80

100

120

140

160

180

200 Non-RET Funded

Commonwealth Solar II

Commonwealth Solar

Stimulus

Small Renewables Initiative

GAHI

Solar to Market Initiative

Utility Scale Renewable Grants

Utility Congestion Relief

16

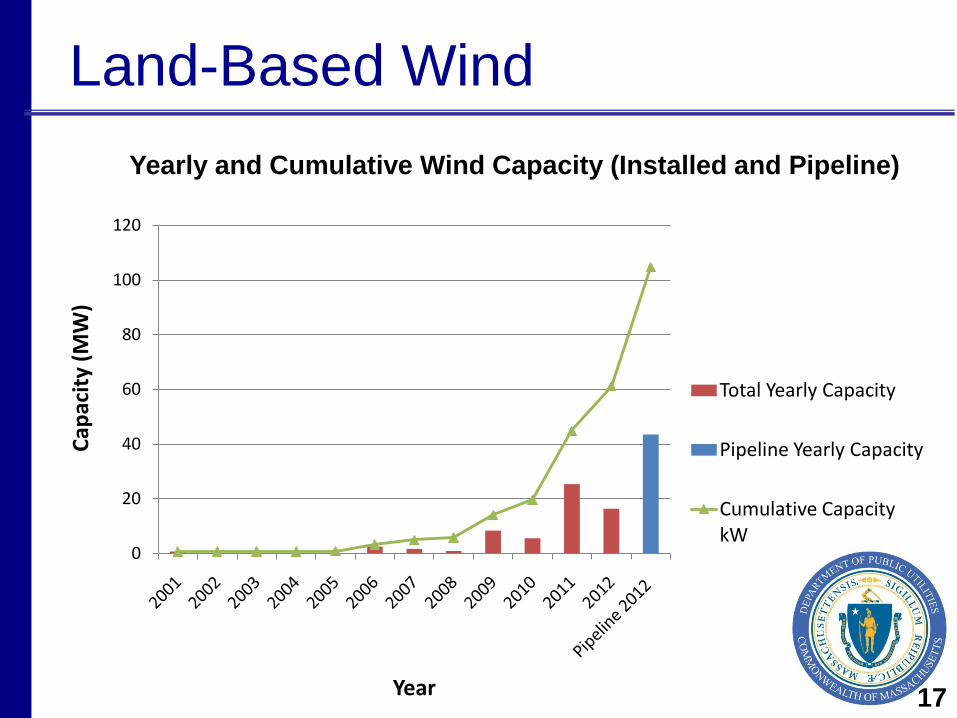

Land-Based Wind

0

20

40

60

80

100

120

Cap

acit

y (M

W)

Year

Total Yearly Capacity

Pipeline Yearly Capacity

Cumulative CapacitykW

Yearly and Cumulative Wind Capacity (Installed and Pipeline)

17

Adding Renewables to the Mix Can Lower

Prices

18

DG Growth from net-

metering/interconnection

19

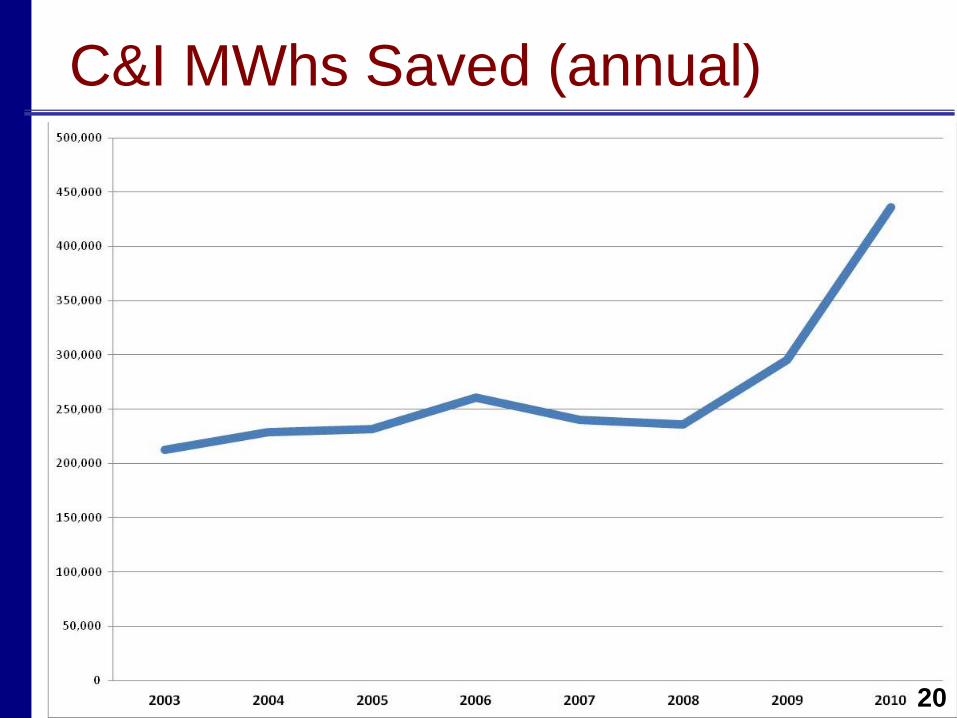

C&I MWhs Saved (annual)

20

New Resources, including NTAs, in the

Capacity Market Since 2010

* Renewables include wood waste solids, municipal solid waste, wind, landfill gas, tire-

related, biomass, and solar. 21

22

A market for load shedding

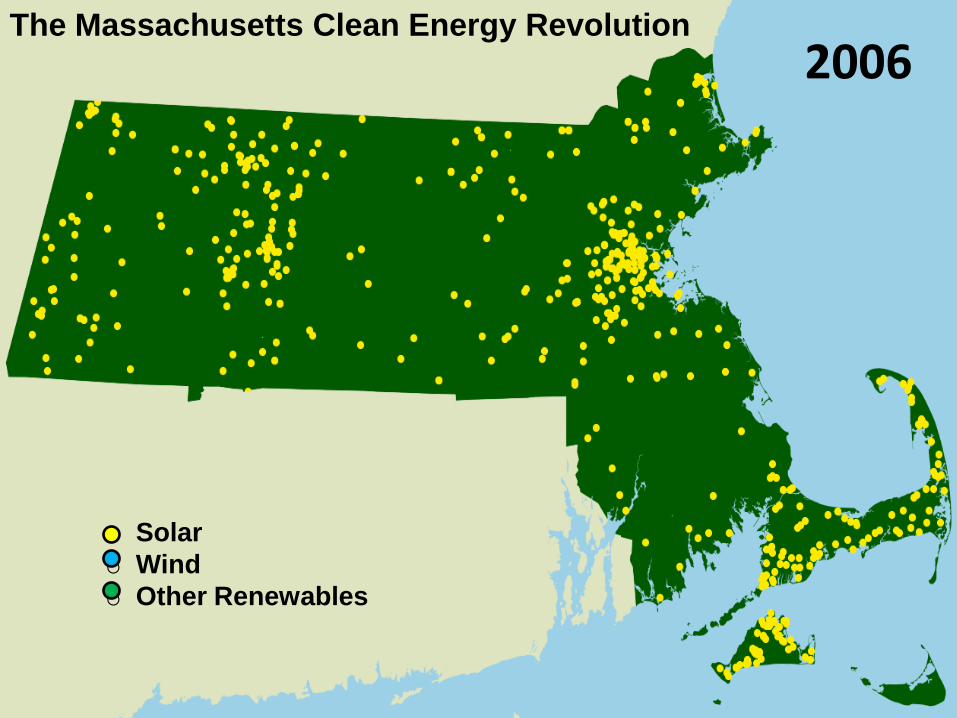

2006The Massachusetts Clean Energy Revolution

o Solar

o Wind

o Other Renewables

2007The Massachusetts Clean Energy Revolution

o Solar

o Wind

o Other Renewables

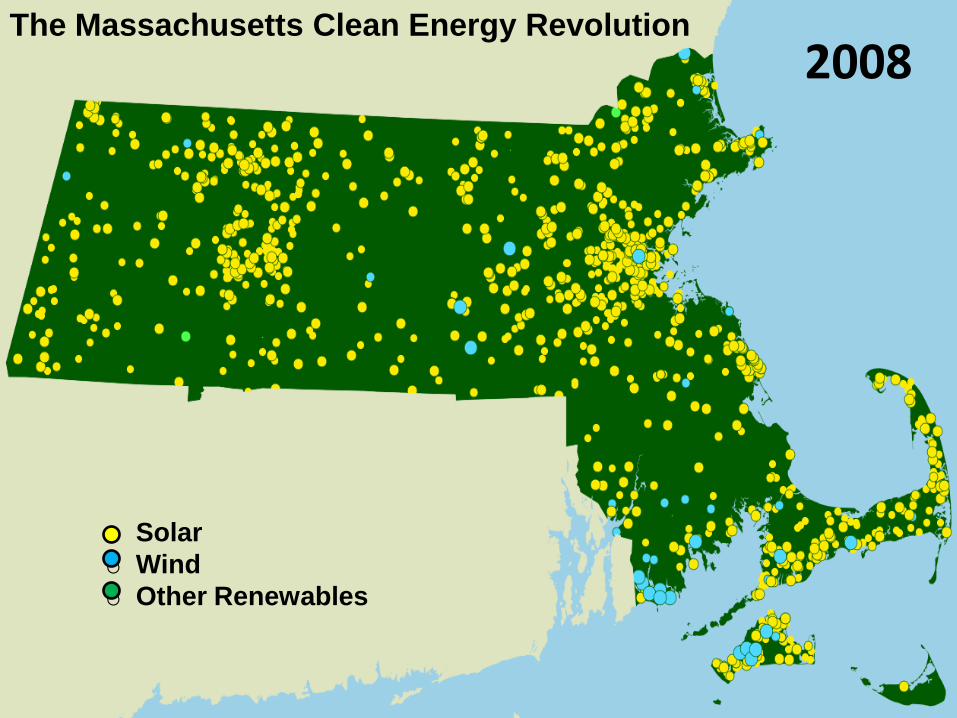

2008The Massachusetts Clean Energy Revolution

o Solar

o Wind

o Other Renewables

2009The Massachusetts Clean Energy Revolution

o Solar

o Wind

o Other Renewables

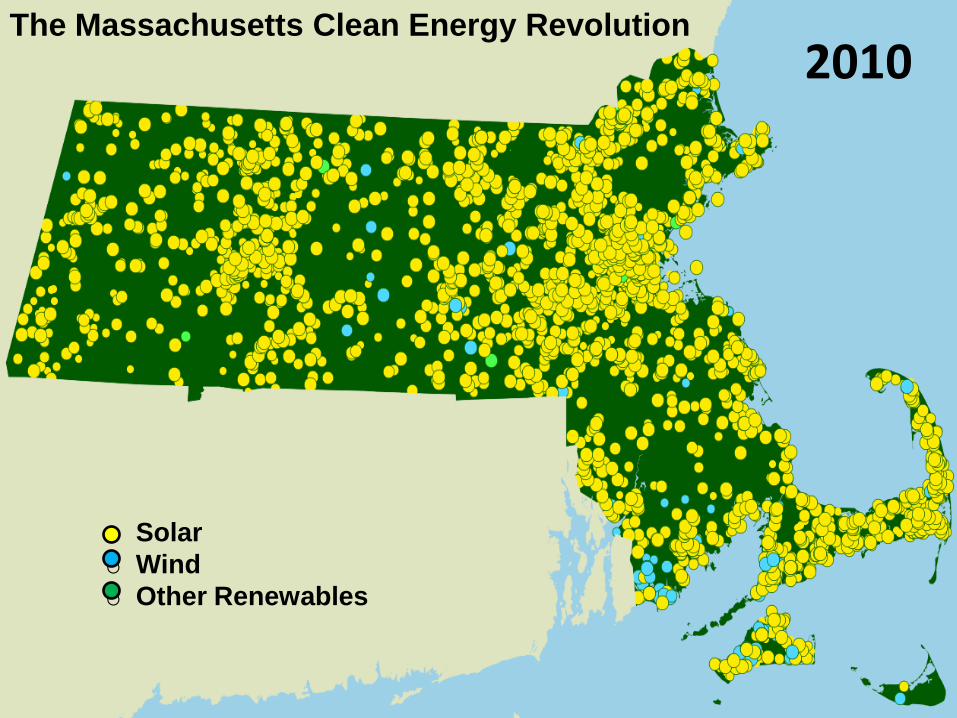

2010The Massachusetts Clean Energy Revolution

o Solar

o Wind

o Other Renewables

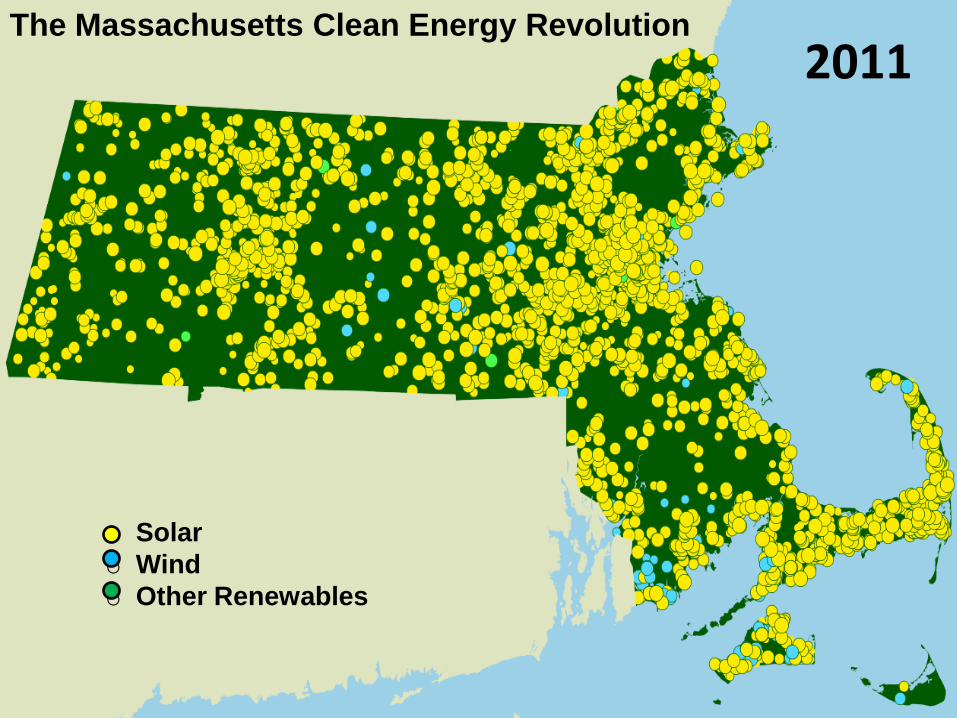

2011The Massachusetts Clean Energy Revolution

o Solar

o Wind

o Other Renewables

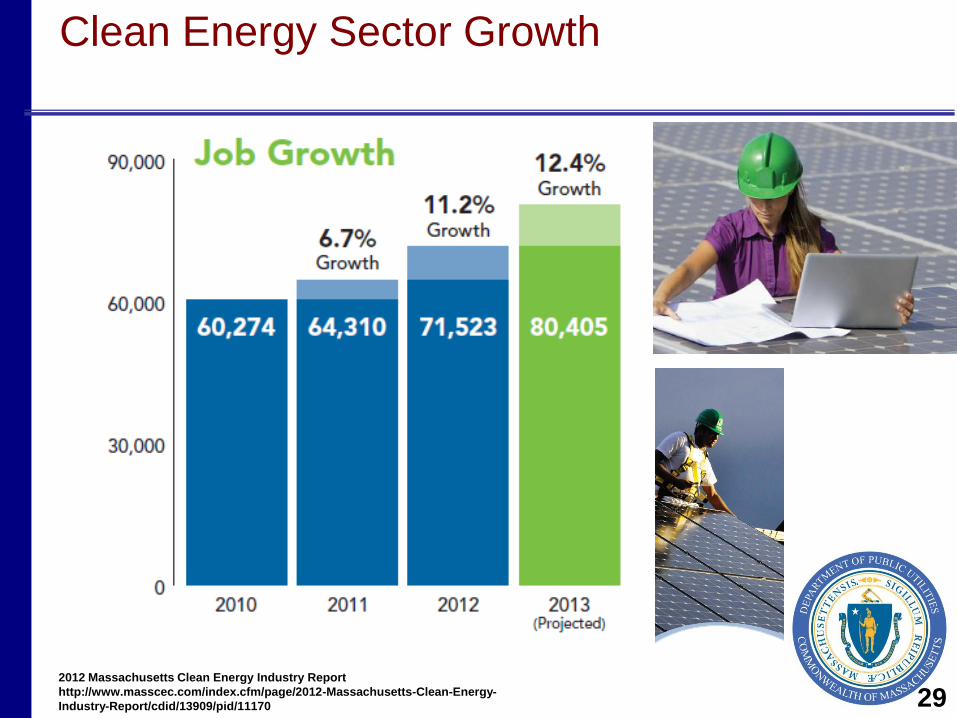

Clean Energy Sector Growth

2012 Massachusetts Clean Energy Industry Report

http://www.masscec.com/index.cfm/page/2012-Massachusetts-Clean-Energy-

Industry-Report/cdid/13909/pid/11170 29

PROGRAM INVESTMENTS & NET BENEFITS OF

ENERGY EFFICIENCY AND RENEWABLE ENERGY

30

• Siting

• Maintaining grid reliability and

stability

• Cost allocation

• New Pricing Regimes

• Grid modernization/Smart Grid

Challenges/Opportunities

31

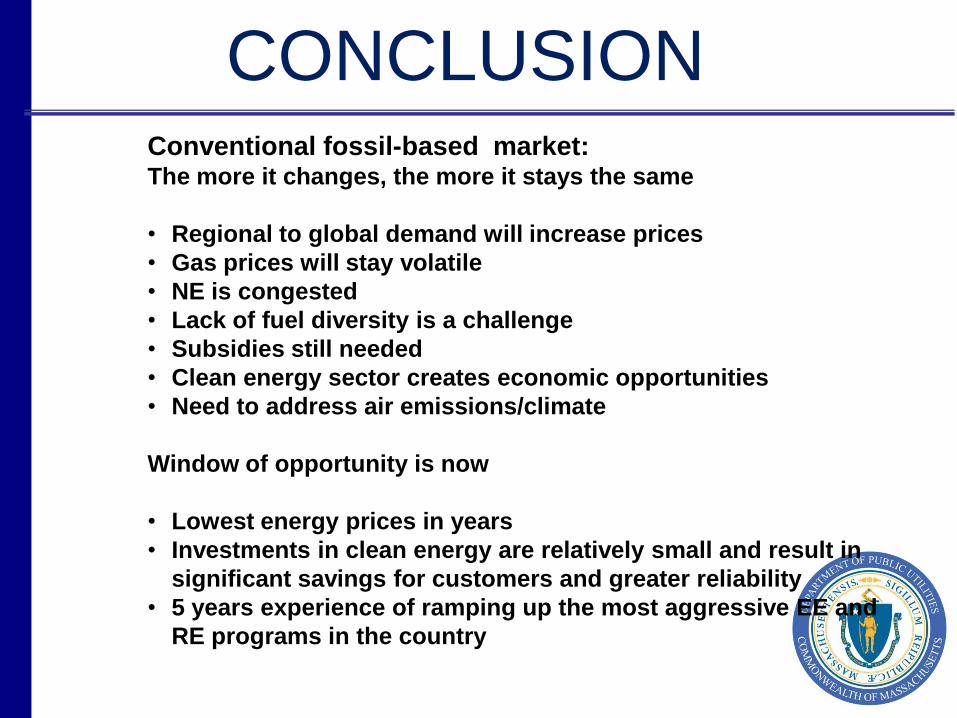

CONCLUSIONConventional fossil-based market:The more it changes, the more it stays the same

• Regional to global demand will increase prices

• Gas prices will stay volatile

• NE is congested

• Lack of fuel diversity is a challenge

• Subsidies still needed

• Clean energy sector creates economic opportunities

• Need to address air emissions/climate

Window of opportunity is now

• Lowest energy prices in years

• Investments in clean energy are relatively small and result in

significant savings for customers and greater reliability

• 5 years experience of ramping up the most aggressive EE and

RE programs in the country

Demand Resources Growing in New

EnglandCapacity Market has stimulated DR growth

FCM

2010/11–2014/16: Total DR cleared in FCAs #1 – #6; real-time emergency generation capped at 600 MW

Enrollment in ISO programs before the start of

FCM

Demand Resource Participation in Region

3

4

Passiv

e (EE)

Activ

e

Real-

Time

EG

Active

Real-

Time

DR

We have a perfect window

right now to make clean

energy investments.

- Governor Deval Patrick, May 30, 2012

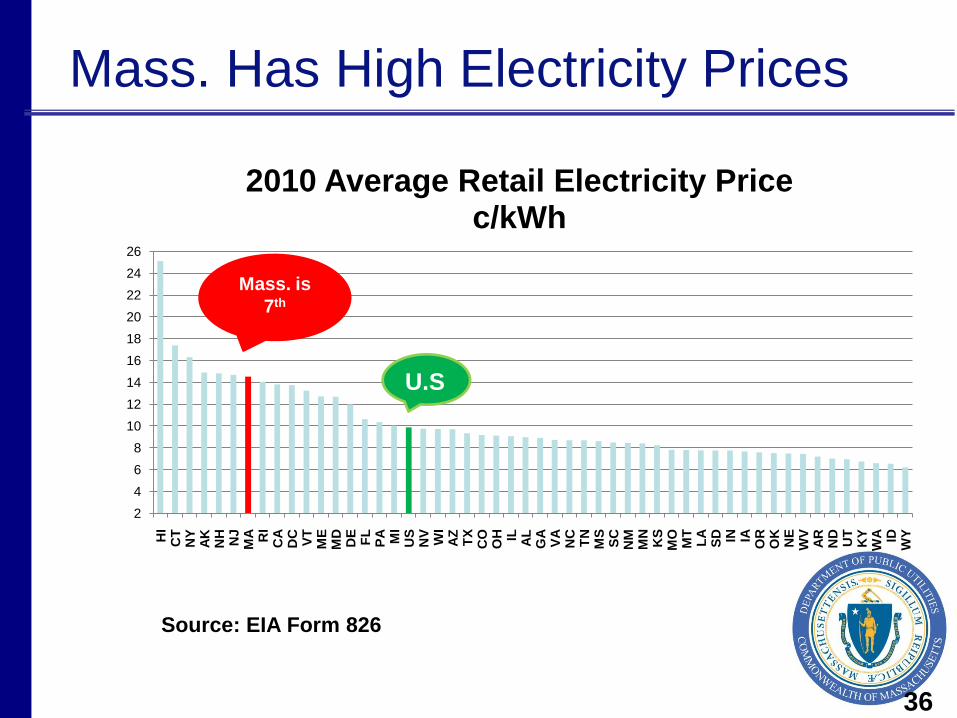

Mass. Has High Electricity Prices

36

2

4

6

8

10

12

14

16

18

20

22

24

26

HI

CT

N

Y

AK

N

H

NJ

MA

R

I C

A

DC

V

T

ME

M

D

DE

F

L

PA

M

I U

S

NV

W

I A

Z

TX

C

O

OH

IL

A

L

GA

V

A

NC

T

N

MS

S

C

NM

M

N

KS

M

O

MT

L

A

SD

IN

IA

O

R

OK

N

E

WV

A

R

ND

U

T

KY

W

A

ID

WY

2010 Average Retail Electricity Price c/kWh

Mass. is

7th

U.S

Source: EIA Form 826

Transmission Costs in New England

3

7

$-

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

$/k

W-Y

ear

Actual

Forecast

Source: ISO-

NE

Demand Resources Growing in New EnglandCapacity Market has stimulated DR growth

38

FCM

2010/11–2014/16: Total DR cleared in FCAs #1 – #6; real-time emergency generation capped at 600 MW

Enrollment in ISO programs before the start of

FCM

Demand Resource Participation in Region

Passive

(EE)

Active

Real-

Time

EG

Active

Real-

Time

DR

Changes in rates over time

From and Industry Group:“D&T Costs Are Increasing Rapidly”

-50%

0%

50%

100%

150%

200%

250%

Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10

% Change in commodity unit cost vs. Dec '05

% Change in D & T unit cost vs. Dec. '05 40

Perc

en

t C

han

ge s

ince 2

005

Previous data, partially corrected

41

Pe

rce

nt

of

To

tal B

ill

Costs and Benefits

Incremental impact of GCA on

rates

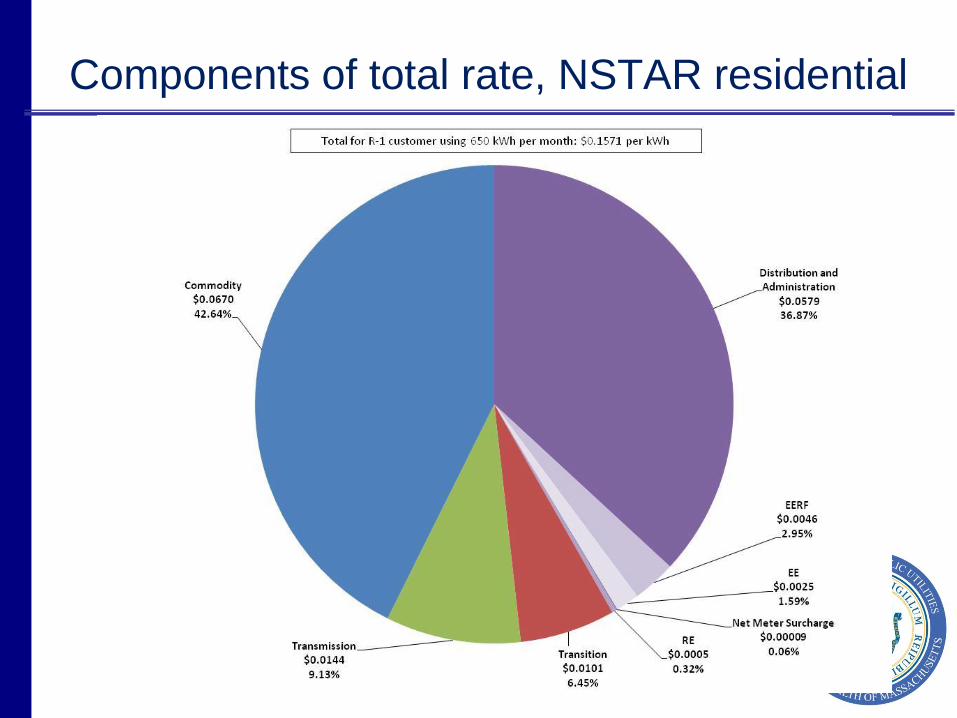

Components of total rate, NSTAR residential

45

Components of total rate, NSTAR Commercial

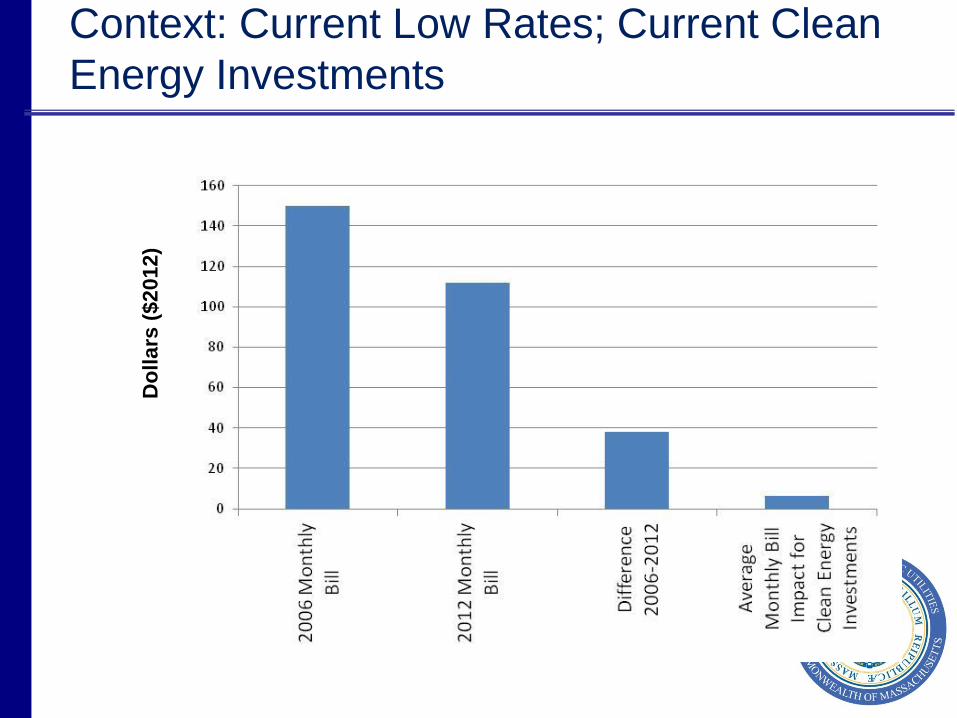

Context: Current Low Rates; Current Clean

Energy Investments

Do

llars

($2012)

Clean Energy Subsidies

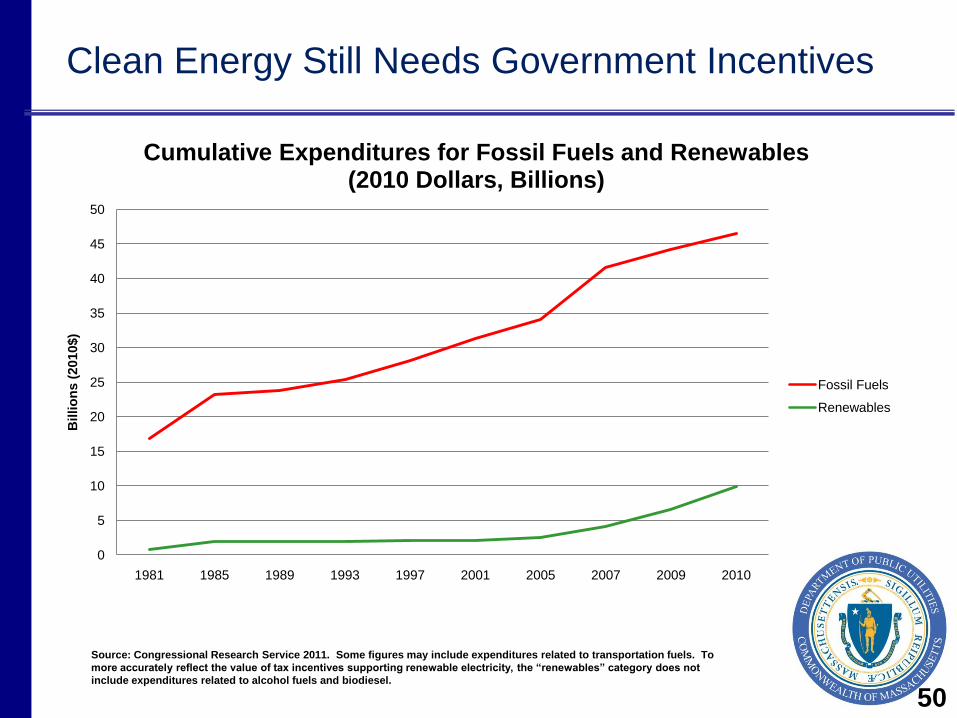

Clean Energy Still Needs Government Incentives

“…Without the current

capital provisions in place, we

would not have been able to

fail over and over again,

which is what it took to

advance the technology

needed…”

48

Clean Energy Still Needs Government Incentives

"The development of

horizontal drilling took trial

and error. Without the current

capital provisions in place, we

would not have been able to

fail over and over again,

which is what it took to

advance the technology

needed to produce the

Bakken and numerous other

resource plays across

America.”

Harold Hamm, the CEO of Continental Resources at the

June 12 Senate Finance Committee hearing on the

relationship between the tax code and energy policy

49

Clean Energy Still Needs Government Incentives

Source: Congressional Research Service 2011. Some figures may include expenditures related to transportation fuels. To

more accurately reflect the value of tax incentives supporting renewable electricity, the “renewables” category does not

include expenditures related to alcohol fuels and biodiesel.

0

5

10

15

20

25

30

35

40

45

50

1981 1985 1989 1993 1997 2001 2005 2007 2009 2010

Billio

ns (

2010$)

Cumulative Expenditures for Fossil Fuels and Renewables(2010 Dollars, Billions)

Fossil Fuels

Renewables

50

http://www.forexpros.com/analysis/why-us-natural-gas-prices-are-so-low---are-changes-needed%20-118082

Clean Energy Still Needs Government Incentives

• Market barriers;

• Imperfect market

(externalities);

• Investments that

companies

cannot make b/c

too risky

Climate Change is Still Real and We are Still Required to Act

52

Required Emissions Reductions

Adding Renewables to the Mix Can Lower

Prices

53

Context: Current Low Rates; Current Clean

Energy InvestmentsD

ollars

($2012)

54

Wind Resources in N.E.

55

Mass. Governor Spearheads the 'Costco' of

Wind Energy DevelopmentA first-of-its-kind program will allow New England states to buy

wind projects in bulk, slashing costs and speeding up

development.http://insideclimatenews.org

New England Governors Plan Massive

Renewable Energy Procurement for

End of 2013At the New England Governors’ Conference (NEGC) on

July 30th, 2012…all six governors signed a resolution

stating their intent to launch a coordinated regional

procurement by the end of 2013.

http://www.solsystemscompany.com/blog/2012/08/20/new-england-governors-plan-massive-

renewable-energy-procurement-for-end-of-2013/

Regional Procurement Opportunities

56

57

Components of total rate, NGRID Commercial

DPU’s Next Hot Topic

58

Grid Modernization

• Enhancing reliability

• Lowering system costs

• Aligning costs and price

• Giving customers greater control

of energy use

• Preparing for a future of

innovation

Comparison of Sandy v. October

NE Load Curve: Last 10% Drives Capacity

Need and Price

60

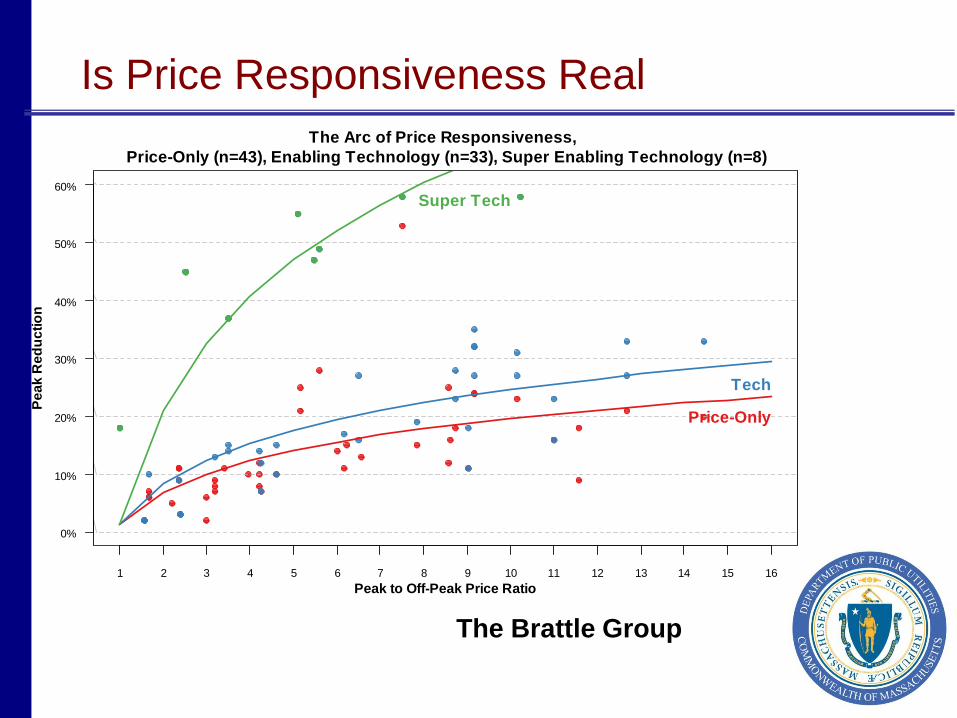

Is Price Responsiveness Real

The Brattle Group

The Arc of Price Responsiveness,

Price-Only (n=43), Enabling Technology (n=33), Super Enabling Technology (n=8)

Peak to Off-Peak Price Ratio

Pe

ak

Re

du

cti

on

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

0%

10%

20%

30%

40%

50%

60%

Price-Only

Tech

Super Tech

Grid Modernization Process

6

2

• Kick off meeting – 11/14/2012

• Working Group through June

2013

• Report and Recommendations to

DPU June, 2013

• 2013-2014 DPU Actions

Energy Costs: Increasing and Volatile

636

3