a mar ket po tential analysis for t he tcaap site in...

TRANSCRIPT

Prepared

RamseSt. Pau Janua

A Mar

d for:

ey Countul, Minn

ry 2013

rket Po

ty nesota

tential Analyssis for tArden

he TCAHills, M

1SM6

AAP SiteMinneso

1221 NicolleSuite 218 Minneapolis,612.338.001

e in ota

t Mall

, MN 554032

3

January 8 Ms. HeatDeputy CSuite 25015 West St. Paul, Dear Ms. AttachedMinnesocommercdifferentand indu The studmarket cdevelopmspace. Rneeded icompetitland use Please co Sincerely MAXFIEL

Matt MuVice Pres Attachm

8, 2013

ther M. WorCounty Mana0 Court HousKellogg BlvdMN 55102

. Worthingto

d is the analyta”. This Phcial/industriat types of owstrial uses in

y addresses onditions; foment potentecommendan the Marketive properticomponent

ontact us if y

y,

LD RESEARCH

ullins sident

ent

rthington, ICager, Ramsese d.

on:

ysis titled, “Ahase I marketal real estatewned housingn the Market

the demogror‐sale houstial for commations are pret Area. A Phies in the mas and recom

you have que

H INC.

1221 N

MA‐CM ey County

A Market Pot analysis exe markets ang, rented hot Area.

raphic and esing; senior hmercial spacerovided for thase II analyarketplace tommend speci

estions or re

(main) 612‐338‐Nicollet Mall, Su

www.ma

tential Analyxamines currnd determinousing, comm

conomic chahousing suppe; and, an asthe various rysis would pro provide anific developm

equire additi

Joe HollmanSenior Anal

‐0012 (fax) 612ite 218, Minneaaxfieldresearch.c

ysis for the Trent conditiones the markmercial uses

aracteristicsply and demssessment oreal estate tyrovide detain indication oment concep

ional inform

n yst

2‐904‐7979 apolis, MN 5540com

TCAAP Site ions in the hoket potentias (retail, offic

s of the Markmand; an anaof the demanypes identifled informaof pricing fopts to optim

mation.

03

n Arden Hillousing and l for developce, and hote

ket Area; renalysis of the nd for industied as beingtion regardior the variouize absorpti

s,

ping el),

ntal

trial g ng s on.

TABLE OF CONTENTS Section Title Page i. EXECUTIVE SUMMARY ................................................................................... 1 Purpose and Scope............................................................................................. 1 Site Analysis ....................................................................................................... 1 Demographic Analysis ........................................................................................ 1 Employment Trends ........................................................................................... 3 Housing Market Analysis .................................................................................... 3 Senior Housing Market Analysis ........................................................................ 4 Retail Market Analysis ....................................................................................... 5 Office Market Analysis ....................................................................................... 5 Hotel Market Analysis ........................................................................................ 6 Industrial Market Analysis ................................................................................. 6 Demand Summary ............................................................................................. 6 ii. PURPOSE AND SCOPE OF STUDY .................................................................... 8 A. SITE LOCATION ANALYSIS ............................................................................... 9 Introduction ....................................................................................................... 9 Regional Location ............................................................................................... 9 Arden Hills Characteristics ................................................................................. 10 Site Location and Characteristics ....................................................................... 14 Access and Visibility ........................................................................................... 16 Proximity to Housing, Employment, and Retail ................................................. 19 Appropriateness of the Subject Site for Redevelopment .................................. 20 B. DEMOGRAPHIC ANALYSIS .............................................................................. 24 Introduction ....................................................................................................... 24 Market Area Definition ...................................................................................... 24 Population and Household Growth Trends ....................................................... 25 Age Distribution ................................................................................................. 28 Household Income ............................................................................................. 30 Household Tenure .............................................................................................. 34 Household Type ................................................................................................. 36 Summary of Demographic Trends ..................................................................... 38 C. EMPLOYMENT TRENDS ................................................................................... 40 Introduction ....................................................................................................... 40 Employment Growth ........................................................................................ 40 Resident Employment ........................................................................................ 42 Covered Employment by Industry ..................................................................... 44 Commuting Patterns of Area Workers .............................................................. 47

TABLE OF CONTENTS (continued)

D. HOUSING MARKET ANALYSIS ......................................................................... 49 Introduction ....................................................................................................... 49 Residential Construction Trends ........................................................................ 49 Overview of Rental Market Conditions ............................................................. 52 Pending Rental Developments ........................................................................... 56 Rental Housing Demand Analysis ...................................................................... 57 Home Sales ......................................................................................................... 61 For‐Sale Housing Market Demand Analysis ....................................................... 67 E. SENIOR HOUSING MARKET ANALYSIS ............................................................. 70 Introduction ....................................................................................................... 70 Senior Housing Defined ..................................................................................... 70 Senior Housing Market Area Definition ............................................................. 72 Older Adult (Age 55+) Population and Household Trends ................................ 73 Older Adult and Senior Household Incomes ...................................................... 75 Homeownership Rate ........................................................................................ 78 Home Sale Values .............................................................................................. 79 Supply of Senior Housing in the Market Area.................................................... 80 Pending Senior Housing Developments in the Market Area ............................. 82 Market Rate Adult/Few Services Senior Housing Demand ............................... 83 Demand for Congregate Senior Housing ........................................................... 85 Assisted Living Demand Estimate ...................................................................... 87 Demand for Memory Care Senior Housing ........................................................ 90 Senior Housing Demand Summary .................................................................... 92 F. RETAIL MARKET ANALYSIS .............................................................................. 93 Introduction ....................................................................................................... 93 Consumer Expenditure Patterns ........................................................................ 93 Retail Demand Potential and Leakage ............................................................... 96 Types of Retail Goods and Customer Shopping Patterns .................................. 98 Twin Cities Retail Market Conditions ................................................................. 99 Retail Development Potential ............................................................................ 102 G. OFFICE MARKET ANALYSIS ............................................................................. 104 Introduction ....................................................................................................... 104 Twin Cities Office Market Conditions ................................................................ 104 Business Growth by Type of Business ................................................................ 106 Growth of Office‐Using Jobs .............................................................................. 109 Office Development Potential ........................................................................... 110 Corporate Campus ............................................................................................. 112

TABLE OF CONTENTS (continued)

H. HOTEL MARKET ANALYSIS .............................................................................. 114 Introduction ....................................................................................................... 114 Regional Conditions ........................................................................................... 114 Regional Attractions ........................................................................................... 116 Metro Area Visitor Profile .................................................................................. 118 Hotel Demand .................................................................................................... 119 I. INDUSTRIAL MARKET ANALYSIS ..................................................................... 121 Introduction ....................................................................................................... 121 Multi‐Tenant Industrial Market Conditions ....................................................... 121 Business Growth by Type of Business ................................................................ 126 Growth of Industrial‐Type Jobs .......................................................................... 131 Industrial Demand Estimates ............................................................................. 132 J. CONCLUSIONS & RECOMMENDATIONS .......................................................... 134 Introduction ....................................................................................................... 134 Residential Demand ........................................................................................... 134 Commercial/Industrial Demand ........................................................................ 137 Final Conclusions ................................................................................................ 139

LIST OF TABLES Table Number and Title Page A‐1 Traffic Volume Trends, TCAAP Site Area ................................................................... 16 B‐1 Population Growth Trends and Projections, TCAAP Site Market Area ..................... 26 B‐2 Household Growth Trends and Projections, TCAAP Site Market Area ...................... 27 B‐3 Age Distribution, TCAAP Site Market Area ................................................................ 30 B‐4 Household Income by Age of Householder, Primary Market Area ........................... 32 B‐5 Household Income by Age of Householder, Secondary Market Area ....................... 33 B‐6 Tenure by Age of Householder, TCAAP Site Market Area ......................................... 35 B‐7 Household Type, TCAAP Site Market Area ................................................................ 38 C‐1 Employment Growth Trends and Projections, TCAAP Site Market Area .................. 41 C‐2 Local Area Unemployment Statistics, TCAAP Site Market Area ................................ 43 C‐3 Quarterly Census of Employment and Wages, TCAAP Site Market Area .................. 45 C‐4 Commuting Patterns .................................................................................................. 47 C‐5 Commuting Inflow/Outflow Characteristics .............................................................. 48 D‐1 Residential Building Permit Trends, 2000 – 2011 ...................................................... 49 D‐2 Residential Units Permitted by City, TCAAP Site Primary Market Area .................... 51 D‐3 Average Rents/Vacancies Trends, TCAAP Site Market Area ...................................... 55 D‐4 Pending Market Rate Rental Developments, TCAAP Site Primary Market Area ....... 56 D‐5 Projected Demand for Market Rate Rental Housing, TCAAP Site Market Area ........ 59 D‐6 Residential Sale Transactions, TCAAP Site Market Area ............................................ 62 D‐7 Single‐Family Detached Residential Sales, TCAAP Site Market Area ......................... 63 D‐8 Multifamily Residential Sales, TCAAP Site Market Area ............................................ 64 D‐9 For‐Sale Housing Demand, TCAAP Site Market Area ................................................. 69 E‐1 Older Adult (55+) Population and Household Age Distribution ................................ 74 E‐2 Older Adult (55+) Income Distribution ...................................................................... 77 E‐3 Older Adult Household Tenure .................................................................................. 79 E‐4 Sale Trends of Single‐Family Homes .......................................................................... 80 E‐5 Market Rate Senior Housing Properties .................................................................... 81 E‐6 Market Rate Adult/Few Services Housing Demand ................................................... 84 E‐7 Congregate Living Demand ........................................................................................ 86 E‐8 Market Rate Assisted Living Demand ........................................................................ 88 E‐9 Memory Care Demand ............................................................................................... 91 E‐10 Senior Housing Demand Summary ............................................................................ 92 F‐1 Household Expenditures by Selected Product Type, TCAAP Site PMA ..................... 94 F‐2 Retail Demand Potential and Leakage, TCAAP Site PMA .......................................... 97 F‐3 Retail Vacancy and Absorption, Twin Cities, 2011 – 2012 ......................................... 100 F‐4 Demand for Retail Space, TCAAP Site PMA ............................................................... 103 G‐1 Office Vacancy and Absorption, Twin Cities, 2011 – 2012 ........................................ 105 G‐2 Businesses by Industry and Size of Business, Arden Hills .......................................... 107 G‐3 Employment Growth Trends and Projections, TCAAP Site PMA ............................... 110 G‐4 Projected Demand for Office Space, TCAAP Site PMA .............................................. 111

LIST OF TABLES (continued)

H‐1 Lodging Industry Performance, Year‐Over‐Year Percent Change ............................. 114 H‐2 Most Popular Tourist Attractions in Minnesota, 2010 Attendance .......................... 117 I‐1 Industrial Space Vacancy and Absorption, Twin Cities, 2011 – 2012 ........................ 123 I‐2 Industrial Space Vacancy and Absorption by Property Type ..................................... 125 I‐3 Industrial Businesses by Industry and Size of Business, Arden Hills .......................... 129 I‐4 Employment Growth Trends and Projections, TCAAP Site PMA ............................... 132 I‐5 Projected Demand for Industrial Space, TCAAP Site PMA ........................................ 133 J‐1 Housing Demand Summary, TCAAP Site Market Area .............................................. 134 J‐2 Commercial/Industrial Demand Summary, TCAAP Site Market Area ....................... 137

EXECUTIVE SUMMARY

MAXFIELD RESEARCH INC. 1

Purpose and Scope of Study

Maxfield Research Inc. was engaged by Ramsey County (the “Client”) to conduct an analysis of the market potential to develop various uses on a portion of the property generally re‐ferred to as the Twin Cities Army Ammunition Plant (TCAAP) Site in Arden Hills, Minnesota. Uses evaluated include housing, commercial, and industrial.

The scope of this study includes: a site evaluation; an analysis of the demographic and economic characteristics of the Market Area; a review of rental market conditions in the area; a review of the for‐sale housing market; a senior housing supply and demand analysis; an analysis of the development potential for commercial uses (retail, office, and hotel); and an assessment of the demand for industrial space.

Site Analysis

The Site location within the Metro Area can be reached within a 30 minute drive time from much of the Metro Area, and both Downtown Minneapolis and Downtown St. Paul can be reached within a 15‐minute drive. The subject property has several other positive attrib‐utes that make it an attractive location for redevelopment. The property is one of the larg‐est tracts of undeveloped land near the Metro core and has convenient access to I‐35W and interstate highway network. It is situated along a major north‐south commuter route with heavy traffic volumes on I‐35W and the surrounding road network. Solid household growth is projected in the market area and there are several large employment centers located nearby. Additionally, the property contains many natural amenities and features.

Some environmental remediation will be required which could negatively impact the marketability of the Site as a location for residential development. In addition, some exist‐ing infrastructure (monitoring wells, pump station) will need to remain in place or be relo‐cated on the Site which could hinder the overall design and layout of development on the property.

Demographic Analysis

Maxfield Research determines the Market Area for housing, retail, office, hospitality, and industrial space based on geographic and man‐made boundaries, commuting patterns, community orientation, places of employment, and our knowledge of the area. Considering these factors, we determined a Primary Market Area (PMA) for the Twin Cities Army Am‐munition Plant (TCAAP) Site in Arden Hills consisting of the following communities: Arden Hills, Blaine, Centerville, Circle Pines, Columbia Heights, Columbus, Falcon Heights, Fridley, Ham Lake, Hilltop, Lauderdale, Lexington, Lino Lakes, Little Canada, Mounds View, New Brighton, North Oaks, Roseville, Shoreview, Spring Lake Park, St. Anthony, and Vadnais

EXECUTIV

MAXFIELD

HeighArea reloc

As of2010gestinhas dsons declinThe Cmode

By 20(+7.1Blainof agdensideveportio

VE SUMMA

D RESEARCH IN

hts. The rem(SMA), wheate from.

f 2010, the P, the populang a trend todecreased stper househone of ‐6.1% fCity of Ardenestly, from 3

020, the PMA%). The maje and Lino Ling areas in ity residentiloped cities.on of this gr

RY

C.

mainder of Are a portion

Prima

PMA containation increaso shrinking headily over told. This numfrom 1990 ton Hills was an3.17 in 1990

A is projectejority of theLakes where established al uses will g In additionrowth.

Anoka County of the pote

ary and Seco

ed 305,567 sed +5.8% whousehold sithe years. Inmber declineo 2010. Thisn exception,to 3.23 in 20

ed to add an population there is mocommunitiegenerate somn, the TCAAP

y and Ramsential deman

ondary Mark

people and hile the numizes. Withinn 1990, the aed to 2.59 ins trend is an, as the num010.

other 21,135and househre land availes like Rosevme househoP Site in Arde

ey County cond not curren

ket Area Ma

120,199 houmber of housn the PMA, thaverage houn 2000 and 2n indication omber of perso

5 people (+6hold growth lable for devville and Newold and popuen Hills will l

omprise a Sently in the P

ap

useholds. Beseholds grewhe average husehold size 2.54 in 2010,of an aging hons per hous

6.9%) and 8,is expected velopment. w Brighton inulation growikely captur

econdary MaMA would li

etween 2000w by +7.6%, household swas 2.71 pe, representinhousehold bsehold incre

515 househto occur in Redevelopmnto higher‐

wth in these fre a substant

2

arket ikely

0 and sug‐ize er‐ng a ase. eased

olds

ment

fully‐tial

EXECUTIVE SUMMARY

MAXFIELD RESEARCH INC. 3

The greatest growth is predicted to occur among the older adults in the Market Area. Aging of baby boomers will generate growth in all cohorts age 55 or greater over the next five years, particularly the 65 to 74 age group, suggesting that there will be a growing oppor‐tunity for retail goods and services catering to these age groups.

In the PMA, 24% of all households rented in 2010, giving it a rental rate that was slightly lower than the SMA (31% of households rented in 2010) and the Metro Area (30% rented). The percentage of PMA renter households increased for all age cohorts between 2000 and 2010 as the total number of renter households residing in the PMA grew approximately 13% during the decade. The number of owner‐occupied households grew roughly 6%. In the PMA, the 45 to 54 and 55 to 64 age cohorts experienced the largest increase in the number of renters. These increases were due, in large part, to the bursting of the housing bubble which pushed many occupants out of home ownership and into rental units.

Employment Trends

In light of the economic recession, between 2000 and 2010, employment declined by ‐8,182 jobs in the PMA. Arden Hills experienced a slight gain in employment during the decade, adding 76 jobs. Between 2010 and the second quarter of 2012, the PMA has gained over 5,500 jobs. Much of the job growth occurred in the Professional and Business Services sec‐tor and the Trade, Transportation, and Utilities industry sector.

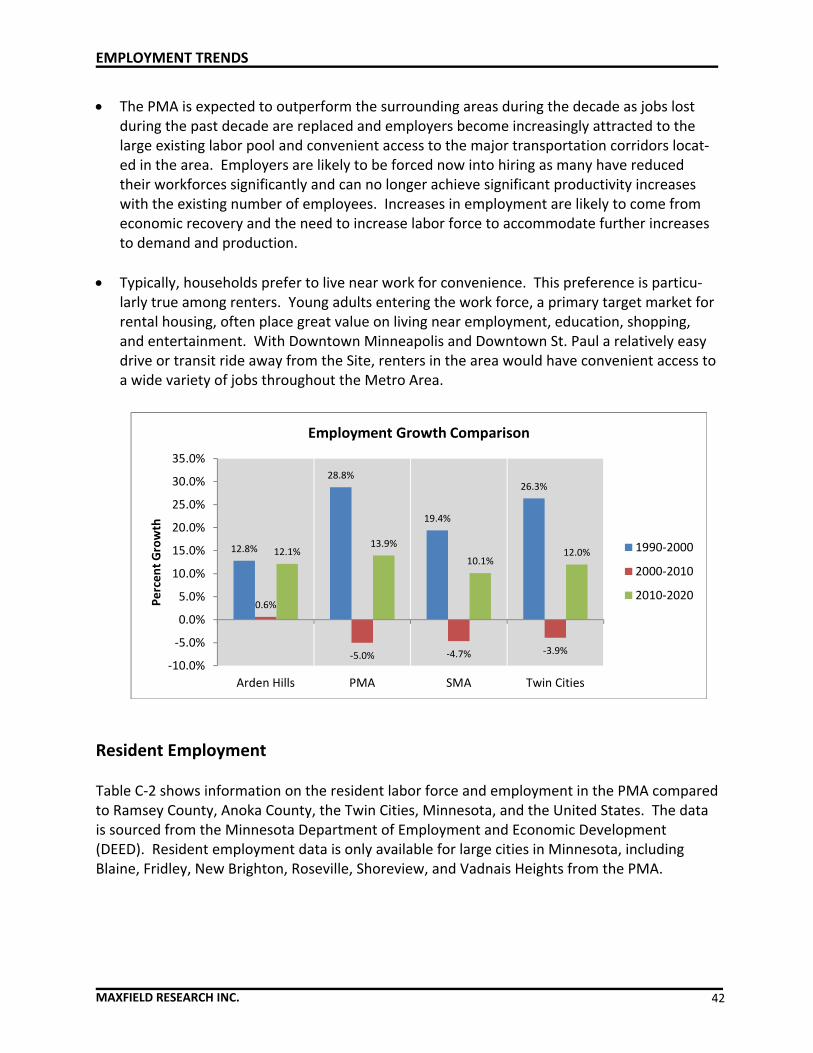

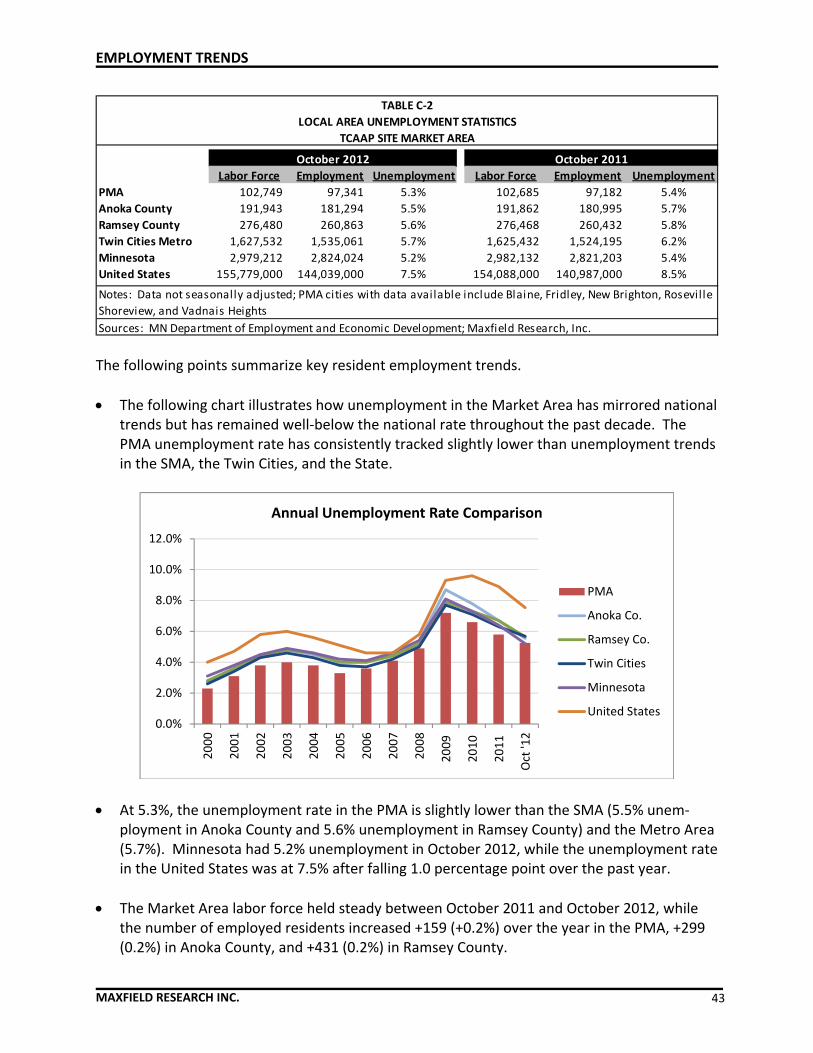

Solid job growth is expected in the Market Area between 2010 and 2020. The PMA is projected to experience a 13.9% gain during the decade while SMA employment is expected to increase by 10.1%. Employment in the Twin Cities Metro Area is projected to expand by 12.0%. The PMA is expected to outperform the surrounding areas during the decade as jobs lost during the past decade are replaced and employers become increasingly attracted to the large existing labor pool and convenient access to the major transportation corridors located in the area.

Arden Hills is a strong importer of workers as a significantly higher number of nonresidents commute into the City for work. Over 14,600 workers come into Arden Hills for employ‐ment while nearly 3,600 leave. Arden Hills experiences Net Job Inflow of 11,069.

Housing Market Analysis

The total number of residential units permitted declined steadily from 2005 to 2009 after reaching a peak of 2,469 units in the PMA in 2004. Detached single‐family homes have been the most common housing type developed in the PMA since 2000, representing 51.4% of all units permitted. Multifamily units represented 27.7% of all residential construction activity while townhomes represented 20.9% of all units permitted.

EXECUTIVE SUMMARY

MAXFIELD RESEARCH INC. 4

The equilibrium vacancy rate for rental housing is considered to be 5.0%. This allows for normal turnover and an adequate supply of alternatives for prospective renters. During the 3rd Quarter 2012, the vacancy rate was 2.7% in the Twin Cities Metro Area. The Arden Hills/Shoreview submarket had a vacancy rate of 3.2% while the other PMA communities had a vacancy rate of 2.5%. In effect, the overall supply of rental housing in the Market Ar‐ea is below the adequate level to meet demand.

We estimate that a general occupancy market rate rental development on the subject property could capture approximately 10% and 15% of the total demand in the Market Ar‐ea. We anticipate that the subject property could support approximately 423 to 634 units of new market rate general occupancy rental housing between 2012 and 2017.

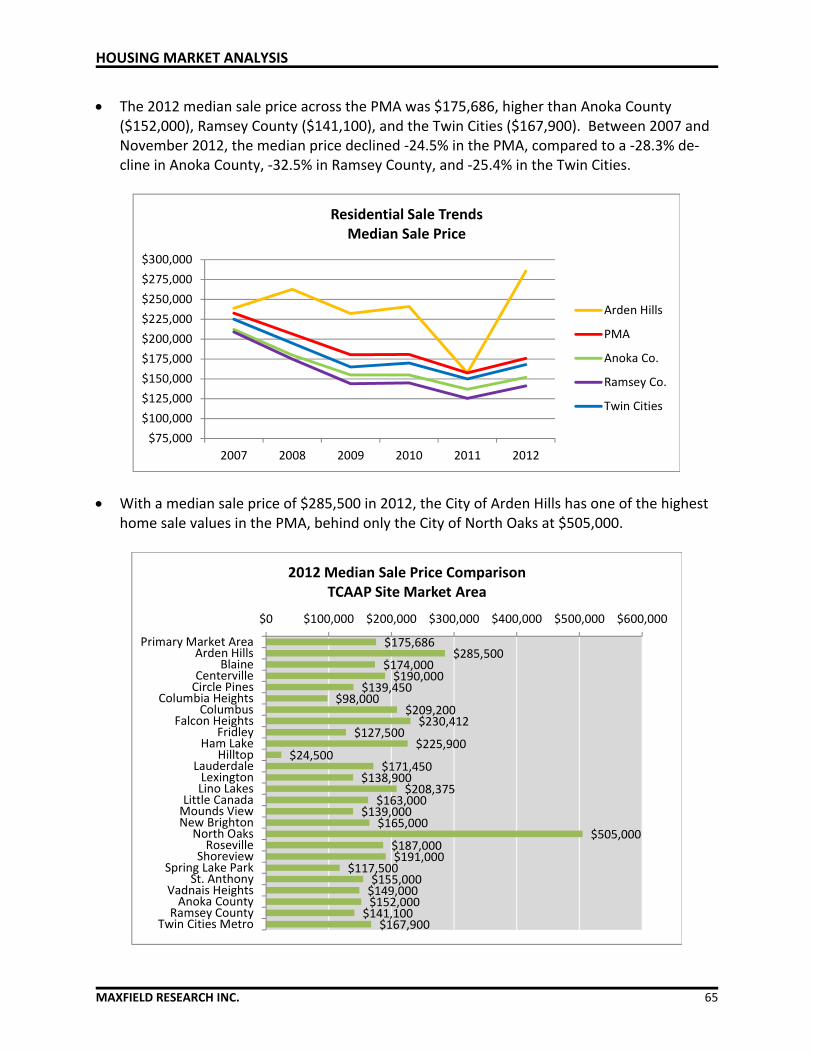

The 2012 median sale price across the PMA was $175,686, higher than Anoka County ($152,000), Ramsey County ($141,100), and the Twin Cities ($167,900). Between 2007 and November 2012, the median price declined ‐24.5% in the PMA, compared to a ‐28.3% de‐cline in Anoka County, ‐32.5% in Ramsey County, and ‐25.4% in the Twin Cities. It appears that pricing for single‐family detached homes is recovering, as the 2012 median sales price is higher than the 2011 median in nearly every community comprising the PMA, although prices are still down significantly from 2007. Multifamily housing has not experienced the pricing recovery that is occurring in the single‐family market as prices in several communi‐ties continued to decline in 2012.

Due to the Site’s desirability as a residential location, we estimate that the subject property could capture roughly 15% to 20% of the PMA demand and 10% of the demand from the SMA, equating to a total of 271 to 350 single‐family units and 116 to 150 multifamily units supportable on the Site between 2012 and 2017.

Senior Housing Market Analysis

A growing older adult and senior population should maintain long‐term demand for senior housing alternatives in the PMA, although pending growth in the supply of senior housing in the PMA will limit demand growth between 2012 and 2017.

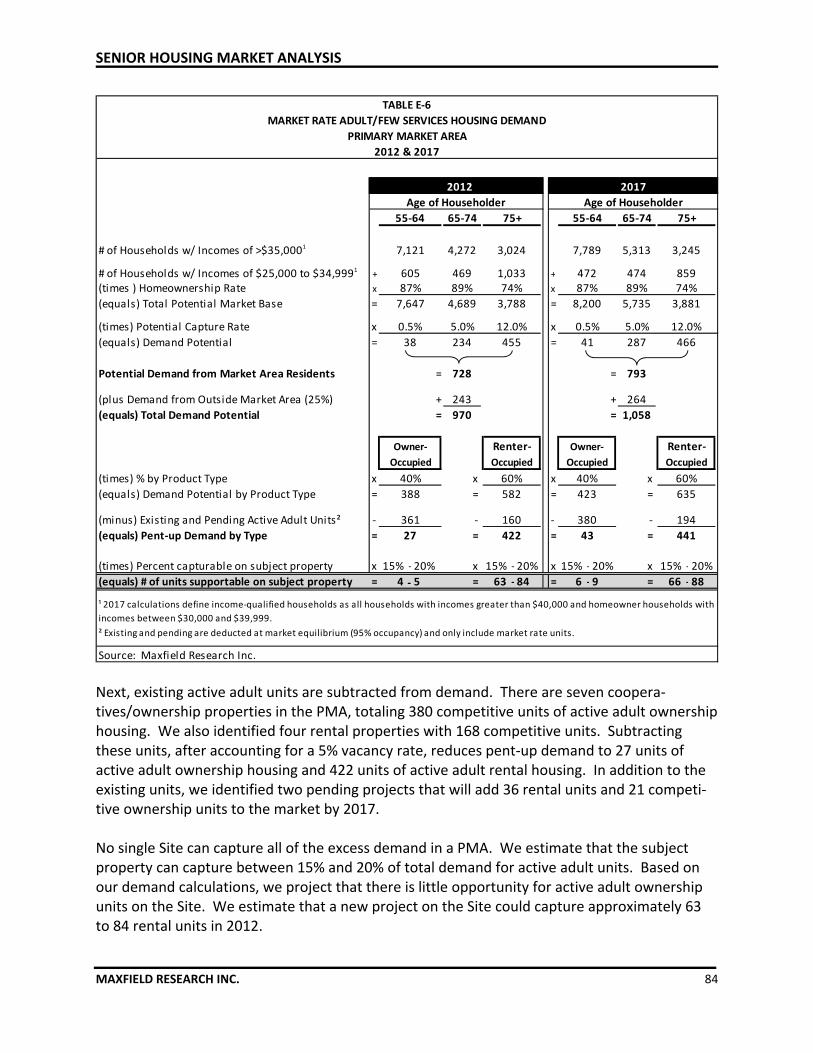

There appears to be pent‐up demand for 422 active adult rental units in the PMA. Based on a capture rate of 15% to 20%, we estimate that the subject property could support between 63 and 84 active adult rental units in 2012, increasing to a range of 66 to 88 active adult rental units in 2017. Due, in large part, to the large supply of active adult ownership units in the PMA, we found little demand for new active adult ownership housing.

There is currently demand to support an additional 32 to 42 congregate and 47 to 63 assisted living units on the Site in 2012, with little change in demand expected by 2017. We

EXECUTIVE SUMMARY

MAXFIELD RESEARCH INC. 5

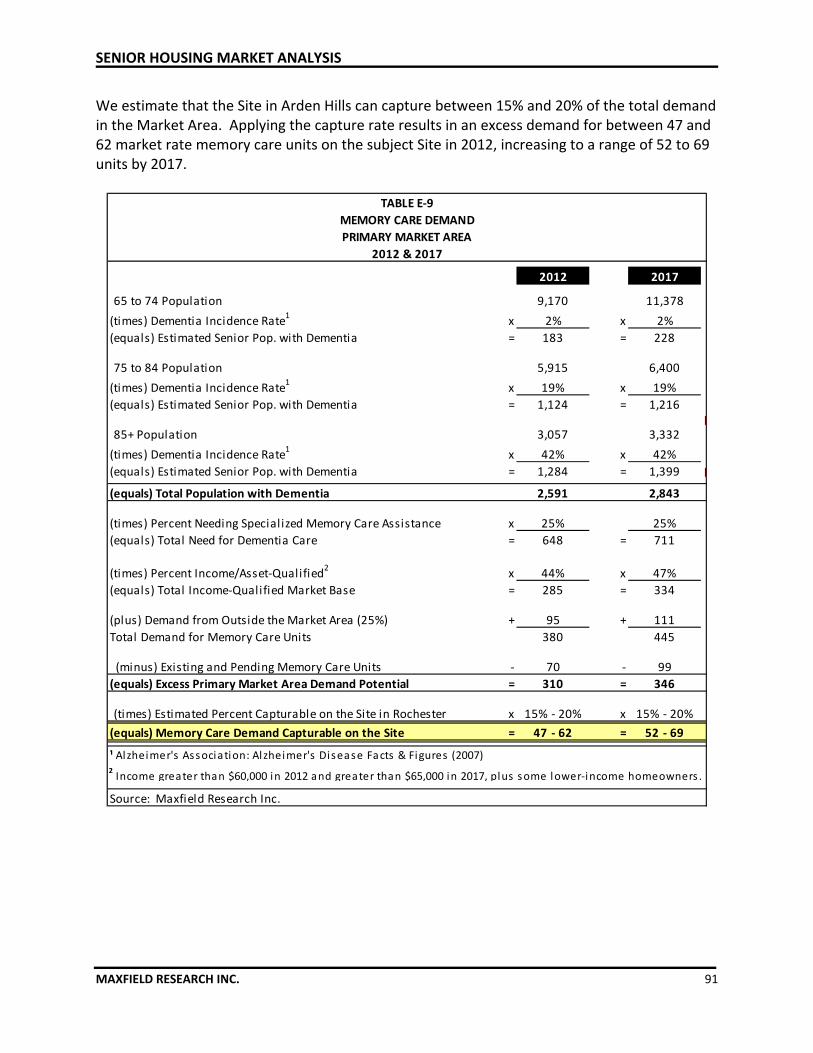

also find demand for 47 to 62 memory care units. By 2017, memory care demand is ex‐pected to grow to between 52 and 69 units.

Retail Market Analysis

Because of the relatively large size of the PMA and the Site’s location within the PMA along I‐35W and Highway 10, we estimate that the subject property could capture roughly 15% to 20% of the growth in retail demand, resulting in demand from PMA households for approx‐imately 195,000 to 259,000 square feet of retail space between 2012 and 2020.

Total leakage of retail expenditures (including food and drink) from the PMA was estimated to be at 14%, indicating a substantial loss of potential retail sales. The subject property will likely attract stores in the retail categories where there is existing leakage. By dollar vol‐ume, retail leakage was greatest in Automobile Dealers, Grocery Stores, Food Services and Drinking Places, and General Merchandise Stores. Retail businesses with the greatest po‐tential are community/neighborhood‐oriented retailers serving the local population, such as grocery, full‐service restaurants, and health and personal care stores. Because many big box retailers are already located in the trade area, the potential to draw a big box store to the Site unless there is limited competition may be difficult.

While exhibiting signs of improvement, the local retail market has not yet fully‐recovered from the recession. As such, the demand for retail on the Site will not likely be realized until the second half of the decade.

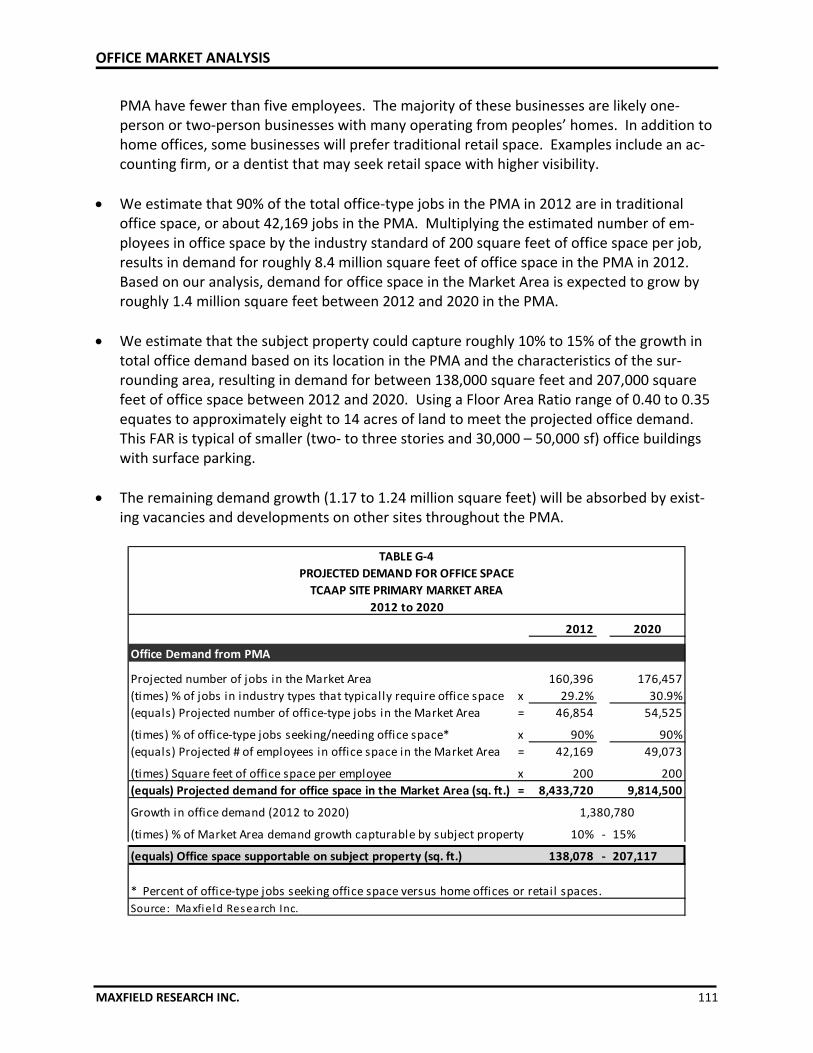

Office Market Analysis

We estimate that the subject property could capture roughly 10% to 15% of the growth in total office demand based on its location in the PMA and the characteristics of the sur‐rounding area, resulting in demand for between 138,000 square feet and 207,000 square feet of office space between 2012 and 2020.

Because of the relatively high office vacancy rate in the submarket surrounding the TCAAP Site, we do not anticipate much demand for new office development in the short‐term. Sustained job growth in the Market Area will be needed to generate the demand necessary to absorb the existing vacancy in the market. We expect that market conditions will sup‐port a new office development on the Site during the second half of the decade.

The most likely target markets for office space on the Site would be businesses in the industry sectors that are projected to grow and have an existing presence in the Market Ar‐ea. The PMA has a large employment base in the Professional and Business Services sector as well as the Education and Health Services industry, both of which are expected to experi‐

EXECUTIVE SUMMARY

MAXFIELD RESEARCH INC. 6

ence substantial growth by 2020. In addition to traditional multi‐tenant office space, the Site would also likely be an attractive location for a corporate campus as well as less‐traditional office users such as governmental agencies and medical services.

Hotel Market Analysis

According to published data, the Minneapolis‐St. Paul Metro Area has experienced flat occupancies over the past year (58.2%), but experienced growth in average daily rates (ADR) and in revenue per available room. Generally, a 65% occupancy rate is considered the equilibrium for a hotel to be profitable.

Due to the Site’s close proximity to several major employers and employment centers, as well as the National Sports Center in Blaine, the subject property would likely be a suitable location for a hotel. The development of additional retail and entertainment uses on the Site would increase the attractiveness of the Site to a hotel operator. There appears to be a market from leisure travelers, but the ability to support a hotel on the site is going to be dependent on the ability to attract weekday business which will come from developing of‐fice and industrial uses that will have business travelers requiring overnight hotel space. Also, there are several large employers in the surrounding area, such as Medtronic, Land O’Lakes, and Deluxe, which will likely generate demand for overnight hotel stays from busi‐ness travelers.

Industrial Market Analysis

Due to the Site’s access to Highway 10 and I‐35W and the central location of the property within the Northeast industrial submarket, we project that the TCAAP Site could capture approximately 400,000 to 445,000 square feet of industrial space on the property.

Bulk Warehouse properties with 32‐foot clear height ceilings appear to be in highest de‐mand currently and forecasted job growth in the Transportation and Warehousing subsec‐tor will continue to support demand for this product type. Functionally well‐designed Office Warehouse facilities that have 24‐foot or higher clear height ceilings, are energy efficient, have ample parking and good lighting are also in demand.

Demand Summary

The table on the following page illustrates the level of demand by property type capturable on the TCAAP Site along with an estimate of the amount of land required to support the projected demand.

EXECUTIVE SUMMARY

MAXFIELD RESEARCH INC. 7

General‐Occupancy Housing Units

Market Rate Rental 20.0 ‐ 30.0 21 ‐ 32

For‐Sale Housing 190 ‐ 225

Single‐Family, Detached 1.7 ‐ 2.0 175 ‐ 206

Multifamily 8.0 ‐ 10.0 15 ‐ 19

Total General Occupancy Housing 211 ‐ 256

Market Rate Senior Housing Units

Senior Housing Total 193 ‐ 256 204 ‐ 272 20.0 ‐ 30.0 9 ‐ 14

Commercial/Industrial Square Feet

Retail ‐ 0.25 ‐ 0.20 24 ‐ 30

Office ‐ 0.40 ‐ 0.35 12 ‐ 14

Industrial ‐ 0.35 ‐ 0.20 29 ‐ 51

Commercial/Industrial Total ‐ 65 ‐ 94

Total Acres Required 285 ‐ 364

Source: Maxfield Research Inc.

404,400 444,840

737,033 911,364

2012 ‐ 2020 FAR Acres

194,555 259,407

138,078 207,117

150

1,134

2012 2017 Units/Acre Acres

2012 ‐ 2017 Units/Acre Acres

634

500

350

SUMMARY OF DEMAND

TCAAP SITE MARKET AREA

December 2012

Demand Capturable

on Site

Maximum Land Area

Requirements

PURPOSE AND SCOPE

MAXFIELD RESEARCH INC. 8

Study Purpose Maxfield Research Inc. was engaged by Ramsey County (the “Client”) to conduct an analysis of the market potential to develop various uses on a portion of the property generally referred to as the Twin Cities Army Ammunition Plant (TCAAP) Site in Arden Hills, Minnesota. Uses evalu‐ated include housing, commercial, and industrial. It is our understanding that the Client executed an offer to purchase with the United States General Services Administration for approximately 427 acres of the TCAAP property. The Ramsey County Board has also entered into an agreement with Carl Bolander and Sons Co. for hazardous material abatement, demolition and site remediation of the 427‐acre site.

Scope of Services The scope of this study includes: a site evaluation; an analysis of the demographic and econom‐ic characteristics of the Market Area; a review of rental market conditions in the area; a review of the for‐sale housing market; a senior housing supply and demand analysis; an analysis of the development potential for commercial uses (retail, office, and hotel); and an assessment of the demand for industrial space. This report includes both primary and secondary research. Primary research includes inter‐views with local officials and real estate professionals. Secondary research is credited to the source when used, and is usually data from the U.S. Census, the Minnesota Department of Employment and Economic Development, or regional planning agencies. Secondary research is always used as a basis for analysis, and is carefully reviewed in light of other factors that may impact projections such as residential building permit data or migration trends. All of the information on pending developments was gathered by Maxfield Research Inc. and is accurate to the best of our knowledge.

SITE LOC

MAXFIELD

Introdu This sectpropertythe propsubject pFinally, th

Regiona Arden HiencompaHills is sitpopulouspopulatiocounty co

CATION ANA

D RESEARCH IN

uction

ion of the rey in Arden Hierty’s generproperty andhis section d

al Location

lls is a commasses 13 coutuated in thes county in Mon of 508,64ore of the M

ALYSIS

C.

eport presenlls, Minnesoral characterd the Site’s pdiscusses the

n

munity of 9,5unties and ine northern MMinnesota, b40 people. TMetro Area.

nts an analysota discussinristics. Adjacproximity to e appropriat

552 people lcludes abouMetro in Rambehind HennThe map beloNon‐urbaniz

Regio

sis of the locg the regioncent land usemploymeneness of the

ocated in thut 3.0 millionmsey Countynepin Countyow shows thzed portions

Map 1

onal Locatio

cation and chnal location, es, accessibnt, shopping e Site for red

he Twin Citien people as oy. Ramsey Cy. As of 201he Site’s locas of the regio

on

haracteristicthe City of Aility to and vand servicedevelopmen

es Metropoliof the 2010 CCounty is the10, Ramsey Cation within on are shade

cs of the subArden Hills, avisibility of ths are present.

tan Area, wCensus. Arde second moCounty had athe seven‐ed green.

9

bject and he nted.

hich den st a

SITE ANALYSIS

MAXFIELD RESEARCH INC. 10

The map shows that the Site is located in an area designated as “Developed” by the Metropoli‐tan Council, the regional planning agency serving the Twin Cities seven‐county metropolitan area. With the exception of North Oaks, to the east of Arden Hills, all communities in Ramsey County area considered to be developed by the Metropolitan Council. Much of the area to the north of Arden Hills in Anoka County is designated as either a developing area, diversified rural, or rural residential. Developing communities focus on accommodating growth, supporting centers along corridors, encouraging connected land use patterns for new development and encouraging the develop‐ment of communities where shopping, jobs and a variety of housing choices coexist. The rural residential designation is used for areas that have large numbers of individual sewage treat‐ment systems at densities of 2.5 acres or less. Diversified rural communities are comprised of a variety of farm and non‐farm land uses that mix large‐lot residential and clustered housing with agriculture. Developed communities are focused on maintaining or improving current infra‐structure; and, renewing or improving land and buildings to provide for additional growth, particularly along transit corridors, in a manner supporting development that integrates land uses. The subject Site is unique within the developed area as it has been held out of availability because of its ownership by the United States government. The strong market dynamics of the Primary Market Area should encourage this area to fill out due to its key location and the lack of available sites elsewhere in the Primary Market Area.

Arden Hills Characteristics The City of Arden Hills covers approximately 9.6 square miles in northern Ramsey County. Interstate Highway 35W and the City of New Brighton (pop. 21,456) form most of the western border of Arden Hills. The City of Shoreview (pop. 25,043) is located north and east of Arden Hills and the City of Roseville (pop. 33,660) forms the southern border. The City of Mounds View (pop. 12,155) is adjacent to the northwestern portion of Arden Hills, directly west of I‐35W from the subject property. Arden Hills experienced rapid growth between 1970 and 1990, adding approximately 941 households between 1970 and 1980 and another 620 households between 1980 and 1990. The 1990s were a period of slower growth for Arden Hills, adding 55 households during the decade (+1.9%), an average of 5.5 per year. The number of households remained essentially un‐changed during the 2000s. In comparison, the Twin Cities Metro Area household base expand‐ed 16.6% between 1990 and 2000 which was followed by 9.4% growth between 2000 and 2010. Excluding open water, Arden Hill’s land area is approximately 71% developed and 29% unde‐veloped (1,587 acres) according to existing land use information from the Metropolitan Council. The undeveloped land is concentrated in the TCAAP property.

SITE ANALYSIS

MAXFIELD RESEARCH INC. 11

Map 2 shows existing land uses in Arden Hills and Map 3 illustrates the 2030 projected land use as identified in the Arden Hills Comprehensive Plan. These maps show that Arden Hills’ land uses include a diverse mix of residential, commercial and industrial uses. The TCAAP Site is currently designated as mixed use industrial and undeveloped. Surrounding land to the south across County Road 96 is a mix of institutional, undeveloped and single‐family residential uses. The area to the west across Highway 10 is a manufactured home park and across I‐35W in Mounds View is a mix of industrial and residential (including single‐family along with a manufactured home park). Properties to the north of the TCAAP Site are generally single‐family residential. The area east of the subject property is undeveloped land on the larger TCAAP property and single‐family residential east of Lexington Avenue in Shoreview. Roughly 24% of Arden Hills’ land area is developed for residential uses, 19% is developed for industrial or mixed‐used industrial uses, 7% is institutional, and 5% is developed for commercial uses. As mentioned previously, approximately 29% of the land area in Arden Hills is undevel‐oped, the largest proportion in the City. Of the 3,941 developed acres, single‐family detached residential comprised the greatest pro‐portion of land use in 2010 at 30%. Mixed use industrial represented nearly 23% of the devel‐oped land area. Park, recreational or preserve land represented 14% of the City’s 2010 land area while institutional represented 9% of the total. Industrial/utility and office uses each comprised just over 4% of the developed land area. Multifamily represented nearly 3% of the developed land area while retail and other commercial uses totaled 2%. Major roadways comprised nearly 10% of the developed land area. The 2030 land use plan indicates that the undeveloped portion of the TCAAP property is desig‐nated as park and recreation land which would total nearly 34% of Arden Hills land area. Much of the subject property is designated for multifamily residential and multi‐optional develop‐ment. According to the Metropolitan Council, the multiple use designation was changed to “Multi‐Optional Development” to help avoid confusion with the generalized land use category “Mixed Use”. The definition of the category essentially remains the same ‐ describing an area marked for development that could be developed into one of many possible land uses. By 2030, the amount of land dedicated for single‐family and multifamily residential develop‐ment will be 21% for single‐family and 7% for multifamily. Multi‐optional development is anticipated to make up 13% of the total land area in Arden Hills.

SITE ANA

MAXFIELD

ALYSIS

D RESEARCH INC.

Cityy of Arden HMap 2

Hills Existing Conditions

12

SITE ANA

MAXFIELD

ALYSIS

D RESEARCH INC.

City of Arden Hills FutuMap 3

ure Land Use

e Guide Map, 2030

13

SITE ANA

MAXFIELD

Site Loc The TCAAboundaryCounty Rsouth. ACounty aand Coun

ALYSIS

D RESEARCH IN

cation and

AP Site is locy descriptionRoad I on theAs illustratedre located innty Road 96.

C.

Character

cated just eans for the ene north, I‐35 on the follon the wester.

ristics

ast of I‐35W ntire TCAAP W and Highwowing aerial rn half of the

Ae

and Highwaproperty incway 10 on thmap, the 42e TCAAP pro

Map 4 erial View

ay 10 in Ardeclude Lexinghe west, and27 acres to boperty, adjac

en Hills, Mington Avenued County Robe purchasedcent to I‐35W

nesota. Gen on the east

oad 96 on thed by RamseyW, Highway

14

neral t, e y 10,

SITE ANA

MAXFIELD

Map 5 shlocated wMounds Blaine, n

ALYSIS

D RESEARCH IN

hows Arden within a five‐View, Fridleorthern Ros

C.

Hills and the‐mile radius y, Spring Lakeville, and s

e Site’s positof several cke Park, St. Aouthwestern

TCAA

tioning in theommunitiesAnthony, Con Lino Lakes

Map 5 AP Site Area

e northern Ms, including; olumbia Heigs.

a

Metro. The New Brightoghts, the sou

property is on, Shorevieuthern half o

15

ew, of

SITE ANALYSIS

MAXFIELD RESEARCH INC. 16

Access and Visibility Excellent access and visibility are vital to the success of commercial business establishments while industrial businesses rely on efficient access to transportation and shipping corridors. Currently, access to the Site can be obtained from Highway 10 or via the County Road H exit off I‐35W from the north. County Road H does not currently have an exit off I‐35W for northbound traffic. Table A‐1 displays the 2000 and 2011 estimated traffic volumes (measured in annual average daily trips) and the 2030 projected traffic volumes for adjacent roads surrounding the Site. The table also presents estimated heavy commercial average daily traffic for 2011.

Traffic near the intersection of I‐35W and Highway 10 declined between 2000 and 2011, with AADT dropping by ‐13,000 (‐10.8%) to 107,000. This drop was likely due in large part to road construction rerouting traffic in the area. Highway 10 experienced 13.3% more traffic (+5,500 AADT) and traffic along County Road 96 increased 19.4% (+3,400). County Road I experienced modest growth in traffic, as AADT increased 2.9% to 7,000. Significant growth in AADT is expected to occur over the next 20 years. I‐35W is projected to receive an AADT increase of nearly 35% while County Road 10 is expected to experience a 27% increase in AADT. Traffic along County Road 96 and County Road I is also projected to increase, growing +12.4% and +22.9%, respectively. During the summer of 2013, County Road 96 will be reconstructed to pass beneath Highway 10 and the existing traffic signal will be removed. In addition, the section of Highway 10 between I‐694 and I‐35W is planned to be resurfaced during 2013. These projects will improve traffic flow and safety on the road network surrounding the TCAAP Site.

HCADT

Estimate Estimate Projected Estimate

2000 2011 2030* 2011 No. Pct. No. Pct.

I‐35W 120,000 107,000 144,000 6,000 ‐13,000 ‐10.8% 37,000 34.6%

Highway 10 41,500 47,000 59,900 1,650 5,500 13.3% 12,900 27.4%

County Rd 96 17,500 20,900 23,500 NA 3,400 19.4% 2,600 12.4%

County Rd I 6,800 7,000 8,600 NA 200 2.9% 1,600 22.9%

AADT = Annual Average Daily Traffic

HCADT = Heavy Commercial Average Daily Traffic

* As projected in the City of Arden Hi l l s 2030 Comprehens ive Plan

Sources: MnDOT; City of Arden Hills; Maxfield Research Inc.

TABLE A‐1

Change, 2011 ‐ 2030

TRAFFIC VOLUME TRENDS

TCAAP SITE AREA

2000, 2011, & 2030

Annual Average Daily Traffic (AADT)

Change, 2000 ‐ 2011

Annual Average Daily Traffic (AADT)

SITE ANA

MAXFIELD

Map 6 illdraw areploymencommuteDowntowthe Site cdrive timMichael tthe east.ban com

ALYSIS

D RESEARCH IN

ustrates drivea for variout centers as e distance wwn Minneapcan be reachme reaches asto the north However, dmunities in t

C.

ve times froms services onpotential ho

when decidinolis and Dowhed within a s far as Northwest, Lakevduring peak the south an

m the propen the Site. Itome buyers ng to purchawntown St. P30 minute dth Branch in ville and Eagatravel timesnd west met

TCAAP

erty. This inft is also usefare likely tose or rent a Paul can be drive from mChisago Couan to the sos (such as rustro area wou

Map 6 Site Drive T

formation isful to determo give strong home. As sreached witmuch of the Munty to the nuth, and mosh hour), could be much

ime

s helpful in dmine access consideratihown on thethin a 15‐minMetro Area.north, Albertost of Washimmute timemore than 3

determining to major emon to their e map, bothnute drive a. The 30 mintville and Stngton Countes to the sub30 minutes.

17

a m‐

nd nute . ty to bur‐

SITE ANA

MAXFIELD

Map 7 illroundingwestern down to As such, the higheshould cramenity

ALYSIS

D RESEARCH IN

ustrates theg area. As shside of the S900 feet nea

the Site shoer elevationsreate a broato potential

C.

e United Stathown, the SitSite to over 1ar Lexington

uld have goos near the ead viewshed residential

tes Geologicte elevation1,000 feet nn Avenue.

od visibility fastern edge of the surrouses.

To

al Survey to changes froear the midd

from the surof the porti

ounding area

Map 7 opography

pographic mom approximdle of the TC

rrounding roon being pua which wou

map for the Smately 900 feCAAP proper

oad networkrchased by

uld likely be a

Site and sur‐eet along thrty, then bac

k. AdditionaRamsey Couan attractive

18

‐e ck

ally, unty e

SITE ANA

MAXFIELD

Proximi Redeveloretail nodindustrianoted onwithin anretail spations in Bretail spaRosedaleon the mfoot Rivecustome

ALYSIS

D RESEARCH IN

ity to Hous

opment possdes. The subl uses and isn the followin approximaace in the coBlaine and Roace within the Center, Nomap, the City erdale Villagers and tenan

C.

sing, Empl

sibilities are bject propers near majorng map, thetely five‐milommunities loseville. Hohree miles ofrthtown Maof Coon Rape located nents away fro

Major

oyment, a

partly influerty is surrounr employmenre are severe radius of tlocated withowever, therf the Site. Tall, The Villagpids has a laear the intersm some of t

r Retail ConcDece

and Retail

enced by pronded by a mnt concentraral large conthe Site. Thehin five milese are only sihe largest shge of Blaine, rge retail prsection of Hthe older cen

Map 8 centrations ember 2012

oximity to homix of residenations and ncentrations ere is nearlys of the Site,ix centers anhopping cen and Har Maresence, partighway 10 anters in the

Near the Sit2

ousing, empntial, commeodes of retaof retail sery 8.0 million , with the hind 408,000 snters in the aar Mall. Whticularly thend Highwayarea like No

te

ployment andercial, and ail activity. Avices locatedsquare feet ghest concesquare feet oarea include hile not show 950,000‐sqy 242, which orthtown Ma

19

d

As d of

entra‐of

wn uare pulls all.

SITE ANALYSIS

MAXFIELD RESEARCH INC. 20

Large employment centers in the neighboring area can be found at established busi‐ness/industrial parks surrounding the Site. Arden Hills and the surrounding communities are home to several large employers, including: Medtronic, Boston Scientific, Land O’Lakes, Smiths Medical, Presbyterian Homes and Services, Deluxe Corporation, Cummins Power Generation, Wells Fargo, and FICO. Additionally, the Site is approximately a 15‐mile drive to both Down‐town Minneapolis and Downtown St. Paul. Highway visibility and access will be key drivers of demand for commercial or industrial uses on the subject property. There are also several colleges and universities, such as Bethel College, Northwestern College, and United Theological Seminary in relatively close proximity to the Site which will make it an attractive location for a rental housing development marketed to the younger age groups.

Appropriateness of the Subject Site for Redevelopment The following summarizes some of positive and negative attributes of the Site in regards to potential redevelopment.

Site Strengths Site Limitations

The property has convenient access to I‐35W and the interstate highway net‐work.

It is one of the largest tracts of unde‐veloped land near the Metro core.

The Site is situated along a major north‐south commuter route with heavy traffic volumes on I‐35W and the surrounding road network.

Solid household growth is projected in the market area.

Several large employment centers are located in the neighboring area.

The property contains many natural amenities and features.

Some environmental remediation will be required which could negatively im‐pact the marketability of the Site as a location for residential development.

There is some existing infrastructure (monitoring wells, pump station) that will need to remain in place or be relo‐cated on the Site which could hinder the overall design and layout of devel‐opment on the property.

SITE ANA

MAXFIELD

Groundw

Existin

ALYSIS

D RESEARCH IN

Gate 4, o

water monit

ng building o

C.

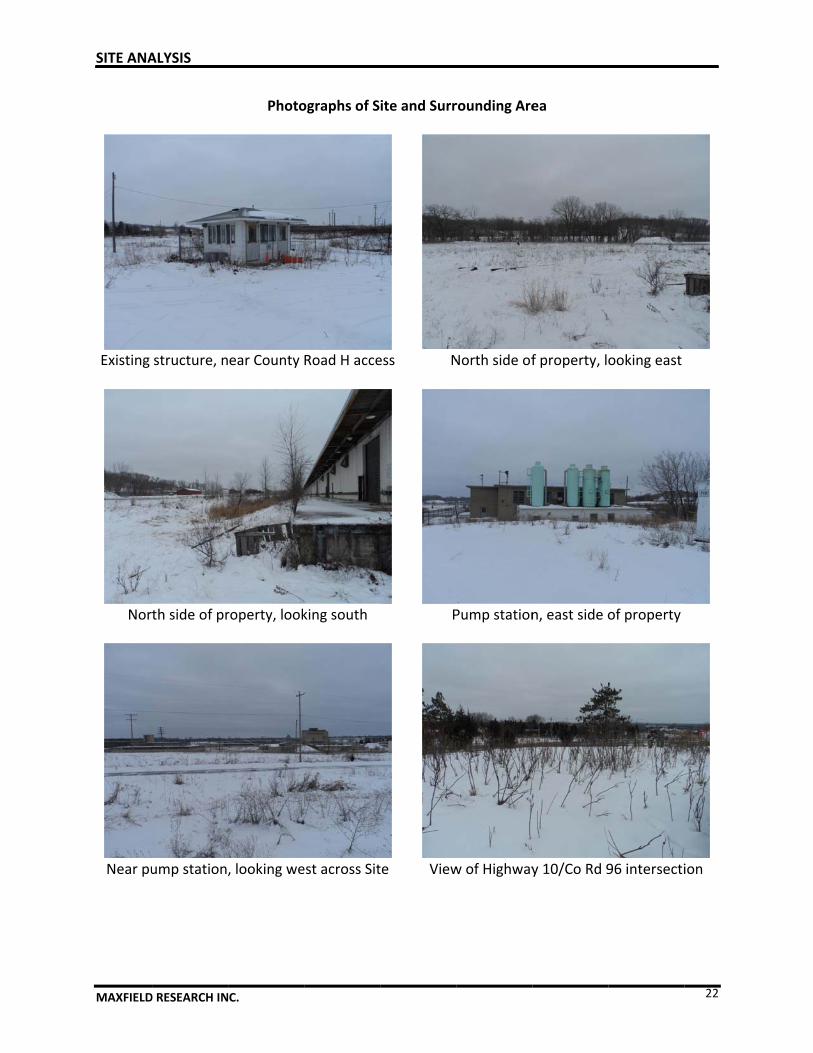

Photo

off Highway

oring station

on Site near

ographs of S

10

ns near Gate

Highway 10

ite and Surr

e 4 Nea

Ga

rounding Are

At Gate 4

r Gate 4, loo

ated access

ea

4, looking so

oking northe

point off Co

utheast

east across S

ounty Road H

21

Site

H

SITE ANA

MAXFIELD

Existing

Nor

Near pu

ALYSIS

D RESEARCH IN

structure, n

th side of pr

ump station,

C.

Photo

ear County

roperty, look

, looking we

ographs of S

Road H acce

king south

est across Sit

ite and Surr

ess N

P

te View

rounding Are

North side of

Pump station

w of Highway

ea

f property, lo

n, east side o

y 10/Co Rd 9

ooking east

of property

96 intersecti

22

ion

SITE ANA

MAXFIELD

South

Big Ten

Housing

ALYSIS

D RESEARCH IN

side of prop

n Tavern, acr

across Coun

C.

Photo

perty, lookin

ross Hwy 10

nty Rd I, nor

ographs of S

g northwest

0 from Gate 4

rth of proper

ite and Surr

t Sou

4 Ma

rty Hou

rounding Are

th side of pr

anufactured

using across

ea

roperty, look

housing, we

Hwy 96, sou

king northea

est of Hwy 1

uth of prope

23

ast

10

rty

DEMOGR

MAXFIELD

Introdu Demograestate nedraw areines the dfor specif

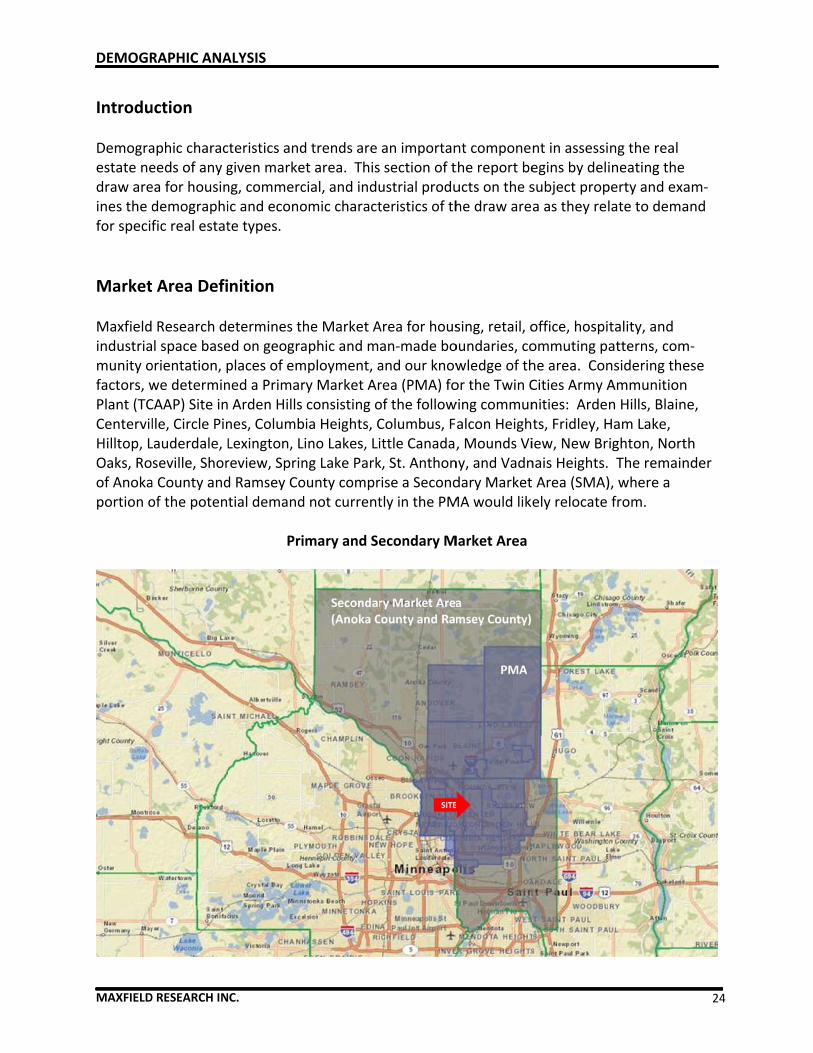

Market Maxfieldindustriamunity ofactors, wPlant (TCCentervilHilltop, LOaks, Roof Anokaportion o

RAPHIC ANA

D RESEARCH IN

uction

aphic characeeds of any gea for housindemographific real estat

Area Defi

Research del space baseorientation, pwe determinCAAP) Site inlle, Circle PinLauderdale, Lseville, Shora County andof the poten

ALYSIS

C.

cteristics andgiven markeng, commercic and econote types.

nition

etermines thed on geograplaces of emned a Primar Arden Hills nes, ColumbLexington, Lreview, Sprind Ramsey Cotial demand

Pri

d trends are et area. Thiscial, and induomic charact

he Market Aaphic and mamployment, ary Market Arconsisting oia Heights, Cino Lakes, Ling Lake Parkounty comprd not current

mary and Se

an importan section of tustrial produteristics of th

Area for housan‐made boand our knowrea (PMA) foof the followColumbus, Fittle Canada,k, St. Anthonrise a Secondtly in the PM

econdary M

nt componethe report beucts on the she draw are

sing, retail, ooundaries, cowledge of thor the Twin Cwing communalcon Heigh, Mounds Viny, and Vadndary MarketMA would like

Market Area

nt in assessiegins by delisubject propa as they rel

office, hospiommuting phe area. ConCities Army Anities: Ardets, Fridley, Hiew, New Brnais Heights. Area (SMA)ely relocate

ng the real ineating theperty and exalate to dema

tality, and atterns, comnsidering theAmmunitionn Hills, BlainHam Lake, ighton, Nort The remain), where a from.

24

am‐and

m‐ese n ne,

th nder

DEMOGRAPHIC ANALYSIS

MAXFIELD RESEARCH INC. 25

Population and Household Growth Trends Tables B‐1 and B‐2 present population and household growth trends in the Primary Market Area (PMA) from 1990 to 2030. The 1990, 2000 and 2010 population and household figures were obtained from the U.S. Census Bureau. The 2012 estimate and projections for 2017, 2020, and 2030 were based on forecasts made by ESRI (a nationally recognized demographics firm) and the Metropolitan Council, with adjustments made by Maxfield Research, Inc. Adjust‐ments were made to better reflect the unique local dynamics of the area based on our under‐standing of the residential development slowdown that began late last decade which impacted household growth throughout the Twin Cities Metro Area. The following are key figures from Tables B‐1 and B‐2.

As of 2010, the PMA contained 305,567 people and 120,199 households. Between 2000 and 2010, the population increased +5.8% while the number of households grew by +7.6%, sug‐gesting a trend to shrinking household sizes. During this same time period, the SMA popu‐lation grew 3.8% against household growth of 5.3%.

Within the PMA, the average household size has decreased steadily over the years. In 1990, the average household size in the PMA was 2.71 persons per household. This number de‐clined to 2.59 in 2000 and 2.54 in 2010, representing a ‐6.1% decline from 1990 to 2010. This trend is an indication of an aging household base. The City of Arden Hills was an excep‐tion, as the number of persons per household increased modestly, from 3.17 in 1990 to 3.23 in 2010.

‐2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

Arden Hills PMA SMA Twin Cities

Household Growth ComparisonPercent Growth by Decade

1990‐2000

2000‐2010

2010‐2020

2020‐2030

DEMOGRAPHIC ANALYSIS

MAXFIELD RESEARCH INC. 26

Estimate

1990 2000 2010 2012 2017 2020 2030 No. Pct. No. Pct.

Primary Market Area 264,762 288,867 305,567 310,397 320,708 326,702 353,584 16,700 5.8% 21,135 6.9%

Arden Hills 9,199 9,652 9,552 9,753 10,193 10,457 11,316 ‐100 ‐1.0% 905 9.5%

Blaine 38,975 45,014 57,186 58,810 61,452 64,094 72,830 12,172 27.0% 6,908 12.1%

Centervil le 1,633 3,202 3,792 3,787 3,780 3,780 4,091 590 18.4% ‐12 ‐0.3%

Circle Pines 4,704 4,663 4,918 4,991 5,146 5,239 5,670 255 5.5% 321 6.5%

Columbia Heights 18,910 18,520 19,496 19,772 20,215 20,348 22,020 976 5.3% 852 4.4%

Columbus 3,690 3,957 3,914 3,960 4,043 4,126 5,023 ‐43 ‐1.1% 212 5.4%

Falcon Heights 5,380 5,572 5,321 5,279 5,296 5,306 5,312 ‐251 ‐4.5% ‐15 ‐0.3%

Fridley 28,335 27,449 27,208 27,299 27,565 27,632 27,660 ‐241 ‐0.9% 424 1.6%

Ham Lake 8,924 12,710 15,296 15,458 15,743 16,028 18,212 2,586 20.3% 732 4.8%

Hilltop 749 766 744 736 724 722 722 ‐22 ‐2.9% ‐22 ‐3.0%

Lauderdale 2,700 2,364 2,379 2,301 2,214 2,223 2,405 15 0.6% ‐156 ‐6.6%

Lexington 2,279 2,142 2,049 2,043 2,037 2,038 2,038 ‐93 ‐4.3% ‐11 ‐0.5%

Lino Lakes 8,807 16,791 20,216 20,660 21,445 22,387 26,650 3,425 20.4% 2,171 10.7%

Little Canada 8,971 9,771 9,773 9,576 9,429 9,547 10,331 2 0.0% ‐226 ‐2.3%

Mounds View 12,541 12,738 12,155 12,436 13,070 13,197 13,353 ‐583 ‐4.6% 1,042 8.6%

New Brighton 22,207 22,206 21,456 21,908 22,990 23,152 23,176 ‐750 ‐3.4% 1,696 7.9%

North Oaks 3,386 3,883 4,469 4,619 4,945 5,141 5,563 586 15.1% 672 15.0%

Rosevil le 33,485 33,690 33,660 34,255 35,685 35,971 37,954 ‐30 ‐0.1% 2,311 6.9%

Shoreview 24,587 25,924 25,043 25,259 25,994 26,435 28,608 ‐881 ‐3.4% 1,392 5.6%

Spring Lake Park 6,532 6,772 6,412 6,760 7,335 7,335 7,335 ‐360 ‐5.3% 923 14.4%

St. Anthony 7,727 8,012 8,226 8,420 8,884 8,898 9,629 214 2.7% 672 8.2%

Vadnais Heights 11,041 13,069 12,302 12,315 12,523 12,648 13,687 ‐767 ‐5.9% 346 2.8%

Secondary Market Area 729,406 809,119 839,484 849,744 874,279 889,000 962,061 30,365 3.8% 49,516 5.9%

Twin Cities Metro Area 2,288,721 2,642,056 2,849,567 2,889,889 2,991,555 3,035,000 3,284,427 207,511 7.9% 185,433 6.5%

Note: Twin Cities Metro represents the 7‐County planning region

Sources: US Census Bureau; Metropolitan Council; ESRI; Maxfield Research, Inc.

TABLE B‐1

POPULATION GROWTH TRENDS AND PROJECTIONS

TCAAP SITE MARKET AREA

1990‐2020

Change

Census 2000‐2010 2010‐2020Forecast

Population

DEMOGRAPHIC ANALYSIS

MAXFIELD RESEARCH INC. 27

Estimate

1990 2000 2010 2012 2017 2020 2030 No. Pct. No. Pct.

Primary Market Area 97,843 111,730 120,199 121,783 126,497 128,714 138,786 8,469 7.6% 8,515 7.1%

Arden Hills 2,904 2,959 2,957 3,036 3,219 3,302 3,574 ‐2 ‐0.1% 345 11.7%

Blaine 12,825 15,926 21,077 21,565 22,672 23,647 26,870 5,151 32.3% 2,570 12.2%

Centervil le 519 1,077 1,315 1,309 1,316 1,316 1,424 238 22.1% 1 0.1%

Circle Pines 1,562 1,697 2,006 2,023 2,092 2,130 2,305 309 18.2% 124 6.2%

Columbia Heights 7,766 8,033 7,926 7,996 8,234 8,288 8,969 ‐107 ‐1.3% 362 4.6%

Columbus 1,129 1,328 1,416 1,429 1,474 1,504 1,831 88 6.6% 88 6.2%

Falcon Heights 2,016 2,103 2,131 2,106 2,110 2,114 2,116 28 1.3% ‐17 ‐0.8%

Fridley 10,909 11,328 11,110 11,116 11,333 11,360 11,372 ‐218 ‐1.9% 250 2.3%

Ham Lake 2,720 4,139 5,171 5,210 5,351 5,448 6,190 1,032 24.9% 277 5.4%

Hilltop 410 400 380 374 370 369 369 ‐20 ‐5.0% ‐11 ‐3.0%

Lauderdale 1,166 1,150 1,130 1,091 1,052 1,056 1,143 ‐20 ‐1.7% ‐74 ‐6.5%

Lexington 829 819 787 782 787 787 787 ‐32 ‐3.9% 0 0.0%

Lino Lakes 2,603 4,857 6,174 6,293 6,598 6,888 8,199 1,317 27.1% 714 11.6%

Little Canada 3,902 4,375 4,393 4,314 4,280 4,333 4,690 18 0.4% ‐60 ‐1.4%

Mounds View 4,702 5,018 4,954 5,055 5,312 5,364 5,427 ‐64 ‐1.3% 410 8.3%

New Brighton 8,523 9,013 8,915 9,119 9,625 9,693 9,703 ‐98 ‐1.1% 778 8.7%

North Oaks 1,085 1,300 1,746 1,807 1,942 2,019 2,185 446 34.3% 273 15.6%

Rosevil le 13,562 14,598 14,623 14,864 15,530 15,654 16,517 25 0.2% 1,031 7.1%

Shoreview 8,991 10,125 10,402 10,464 10,765 10,948 11,847 277 2.7% 546 5.2%

Spring Lake Park 2,343 2,724 2,672 2,811 3,076 3,076 3,076 ‐52 ‐1.9% 404 15.1%

St. Anthony 3,453 3,697 3,848 3,950 4,190 4,197 4,541 151 4.1% 349 9.1%

Vadnais Heights 3,924 5,064 5,066 5,069 5,169 5,221 5,650 2 0.0% 155 3.0%

Secondary Market Area 272,937 307,664 323,918 327,155 338,260 343,956 372,223 16,254 5.3% 20,038 6.2%

Twin Cities Metro Area 875,504 1,021,456 1,117,749 1,131,120 1,178,075 1,205,000 1,320,015 96,293 9.4% 87,251 7.8%

Note: Twin Cities Metro represents the 7‐County planning region

Sources: US Census Bureau; Metropolitan Council; ESRI; Maxfield Research, Inc.

TABLE B‐2

HOUSEHOLD GROWTH TRENDS AND PROJECTIONS

TCAAP SITE MARKET AREA

1990‐2020

Change

Census 2000‐2010 2010‐2020Forecast

Households

DEMOGRAPHIC ANALYSIS

MAXFIELD RESEARCH INC. 28

By 2020, the PMA is projected to add another 21,135 people (+6.9%) and 8,515 households (+7.1%). The majority of the population and household growth is expected to occur in Blaine and Lino Lakes where there is more land available for development. Redevelopment of aging areas in established communities like Roseville and New Brighton into higher‐density residential uses will generate some household and population growth in these fully‐developed cities. In addition, the TCAAP Site in Arden Hills will likely capture a substantial portion of this growth.

Between 2010 and 2020 the SMA population is projected to growth 5.9%, adding 49,516 people while the Twin Cities Metro Area grows by 185,433 people (+6.5%).

In 1990, the PMA contained 11.6% of the Metro Area’s population. This proportion dropped to 10.9% in 2000 and 10.7% in 2010 as much of the region’s residential growth oc‐curred beyond the I‐494/I‐694 loop in communities like Woodbury, Lakeville, Shakopee, and Maple Grove. With 9,552 people in 2,957 households, the City of Arden Hills contained 3.1% of the PMA’s population and 2.5% of its households in 2010.

These proportions are expected to increase slightly by 2020 as transportation costs and demographic shifts increase the desirability of residing closer to the Metro core.

Age Distribution The age distribution of a community’s population helps in assessing the type of housing and commercial services needed. For example, younger and older people are more attracted to higher density housing located near urban services and entertainment while middle‐aged people (particularly those with children) traditionally prefer lower‐density single‐family homes. Also, younger people are more likely to seek a variety of retail services including entertainment, electronics and specialty apparel. Child stores increase in popularity for the 25 to 34 and 35 to 44 cohorts while home furnishings are more frequently sought by the 45 to 54 and 55 to 64 age groups. Table B‐3 presents the age distribution of the TCAAP Site Market Area population from 2000 to 2017. Information from 2000 and 2010 is sourced from the U.S. Census. The 2012 estimates and projections for 2017 were calculated by Maxfield Research Inc. based on information from ESRI, a reputable national demographics firm, and the Metropolitan Council. The following are key trends about the age distribution of the Market Area’s population.

In 2010, the largest adult cohort by age in the PMA and SMA was 45 to 54, totaling 48,828 people (16% of the total population) in the PMA and 126,499 (15% of the total population) in the SMA. This age group is predicted to decline ‐6.2% between 2012 and 2017 for a loss of ‐3,019 people in the PMA and ‐6.4% (‐8,113 people) in the SMA.

DEMOGRAPHIC ANALYSIS

MAXFIELD RESEARCH INC. 29

In the City of Arden Hills, the largest age group was 55 to 64 in 2010. This cohort is project‐ed to increase +8.6% (+120 people) between 2012 and 2017.

The greatest growth is predicted to occur among the older adults in the Market Area. Aging of baby boomers led to an increase of 12,582 people (+48.3%) in the 55 to 64 population between 2000 and 2010 in the PMA. As this group ages, all cohorts age 55 or greater are predicted to see increases over the next five years, particularly the 65 to 74 age group which is projected to grow 23.6% in Arden Hills, 33.9% in the PMA, and 33.5% in the SMA.

The Market Area is expected to see a decline in the middle aged cohorts between 2012 and 2017. The 45 to 54 age cohort is expected to decline ‐3.8% in Arden Hills, ‐6.2% in the PMA, and ‐6.4% in the SMA. The 35 to 44 age group is expected to shrink slightly throughout the PMA (‐0.5%) and SMA (‐1.0%). The 20 to 24 age group is also projected to decline through‐out the Market Area, losing ‐1.0% (‐14 people) in Arden Hills, ‐2.4% (‐476 people) in the PMA, and ‐2.2% (‐1,352 people) in the SMA.

The weak growth projected for the middle aged population is a result the comparatively small number of people who will move into those age cohorts between 2012 and 2017, a phenomenon known as the “baby bust.” The “baby bust” is often referred to the genera‐tion of children born between 1965 and 1980, an era when the United States birthrate dropped sharply.

‐10.0 ‐5.0 0.0 5.0 10.0 15.0 20.0 25.0 30.0 35.0 40.0

Under 20

20 to 24

25 to 34

35 to 44

45 to 54

55 to 64

65 to 74

75+

Total

Percent Change

Projected Population Growth by Age2012‐2017

SMA

PMA

Arden Hills

DEMOGRAPHIC ANALYSIS

MAXFIELD RESEARCH INC. 30

Household Income Household income data helps ascertain demand for different types of retail services. People with lower incomes are likely to seek out discount retailers and spend a higher proportion of their income on necessities like grocery items. Retail services and goods such as dining and home furnishings will experience higher spending from more moderate‐income households while upper income households will also shop for specialty apparel, recreation and sporting

Estimate Projection

Age 2000 2010 2012 2017 No. Pct. No. Pct.

City of Arden Hills

Under 20 2,802 2,608 2,622 2,694 ‐194 ‐6.9 72 2.7

20 to 24 1,092 1,417 1,435 1,421 325 29.8 ‐14 ‐1.0

25 to 34 805 769 801 852 ‐36 ‐4.5 51 6.4

35 to 44 1,182 768 767 791 ‐414 ‐35.0 24 3.1

45 to 54 1,573 1,180 1,165 1,121 ‐393 ‐25.0 ‐44 ‐3.8

55 to 64 858 1,322 1,400 1,520 464 54.1 120 8.6

65 to 74 553 660 713 881 107 19.3 168 23.6

75+ 787 828 850 913 41 5.2 63 7.4

Total 9,652 9,552 9,753 10,193 ‐100 ‐1.0 440 4.5

Primary Market Area

Under 20 79,738 78,155 77,860 79,466 ‐1,583 ‐2.0 1,311 1.7

20 to 24 19,532 19,693 20,216 19,217 161 0.8 ‐476 ‐2.4

25 to 34 39,492 40,344 41,590 43,143 852 2.2 2,799 6.9

35 to 44 49,836 39,375 38,910 39,176 ‐10,461 ‐21.0 ‐199 ‐0.5

45 to 54 41,985 48,828 48,072 45,809 6,843 16.3 ‐3,019 ‐6.2

55 to 64 26,055 38,637 40,931 44,024 12,582 48.3 5,387 13.9

65 to 74 17,430 21,460 23,249 28,733 4,030 23.1 7,273 33.9

75+ 14,799 19,075 19,569 21,140 4,276 28.9 2,065 10.8

Total 288,867 305,567 310,397 320,708 16,700 5.8 15,141 5.0

Secondary Market Area

Under 20 241,380 229,950 228,455 232,815 ‐11,430 ‐4.7 2,865 1.2

20 to 24 58,270 62,674 64,388 61,322 4,404 7.6 ‐1,352 ‐2.2

25 to 34 121,213 120,751 124,097 128,811 ‐462 ‐0.4 8,060 6.7

35 to 44 137,329 109,228 107,628 108,186 ‐28,101 ‐20.5 ‐1,042 ‐1.0

45 to 54 108,127 126,499 124,250 118,386 18,372 17.0 ‐8,113 ‐6.4

55 to 64 62,216 96,969 102,478 110,211 34,753 55.9 13,242 13.7

65 to 74 41,348 49,907 53,940 66,614 8,559 20.7 16,707 33.5

75+ 39,236 43,506 44,508 47,934 4,270 10.9 4,428 10.2

Total 809,119 839,484 849,744 874,279 30,365 3.8 34,795 4.1

Sources: U.S. Census Bureau; ESRI; Maxfield Research, Inc.

AGE DISTRIBUTION

TABLE B‐3

2000‐2010 2012‐2017

2000‐2017

TCAAP SITE MARKET AREA

Change

Census

DEMOGRAPHIC ANALYSIS

MAXFIELD RESEARCH INC. 31

goods, and luxury items. This data also helps determine demand for different types of owned and rented housing based on the size of the market at specific cost levels. In general, housing costs of up to 30 percent of income are considered affordable by the Department of Housing and Urban Development (HUD). The next two tables present data on household income by age of householder in 2012 and 2017 for the Market Area. The data is estimated by ESRI, a nationally recognized demographic services firm, and adjusted by Maxfield Research Inc. to reflect the most current local house‐hold estimates and projections. The following are key points.

In 2012, the median household income was estimated to be approximately $64,000 in the PMA and $55,823 in the SMA. As such, it appears that PMA residents are relatively affluent compared to the SMA and have more resources to devote toward housing and retail goods than residents elsewhere in Anoka County and Ramsey County.

By 2017, the median household income is projected to increase 20% to $76,790 in the PMA and +18% in the SMA to $65,868. In both market areas, the average annual increase (4% in the PMA and 3.6% in the SMA) will exceed the historical annual inflation rate of 2.4% over the past ten years. As households age through the lifecycle, their household income tends to peak in their late 40s and early 50s. This trend is evident throughout the Market Area as the age 45 to 54 cohort has the highest estimated income at $81,944 in the PMA and $72,769 in the SMA.

Within the PMA, the 65 to 74 and 55 to 64 age cohorts are projected to experience the largest increases between 2012 and 2017, rising 22.5% (+3,257 households) and 6.7%

$‐

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

$100,000

Total <25 25‐34 35‐44 45‐54 55‐64 65‐74 75+

2012 Median Income by Age of Householder

PMA

SMA

DEMOGRAPHIC ANALYSIS

MAXFIELD RESEARCH INC. 32

(+1,600 households), respectively. Median incomes in these two age groups are also ex‐pected to climb significantly, suggesting that there will be a growing opportunity for retail goods and services catering to these age groups.

Based on average pricing of $1,179 for a new (built in the year 2000 or more recently) one‐bedroom rental unit in the Twin Cities Metro Area, a household would need to have an an‐nual income of $47,000 or greater to not exceed 30% of its monthly income on housing costs. In 2012, we estimate that approximately 79,852 PMA households (66% of the total) are estimated to have incomes of at least $47,000. By 2017, the total income‐qualified

Total <25 25‐34 35‐44 45‐54 55‐64 65 ‐74 75+

Less than $15,000 8,753 644 1,177 786 1,214 1,320 1,334 2,278

$15,000 to $24,999 8,764 557 1,123 817 1,111 1,178 1,177 2,801

$25,000 to $34,999 11,238 530 1,789 1,449 1,669 1,786 1,590 2,425$35,000 to $49,999 16,470 700 2,956 2,450 2,688 2,999 2,309 2,368

$50,000 to $74,999 23,995 884 4,378 4,139 5,128 4,647 3,187 1,632

$75,000 to $99,999 18,679 274 3,369 3,809 4,736 3,707 1,982 802

$100,000 or more 33,884 314 3,828 6,966 10,377 8,343 2,900 1,156

Total 121,783 3,903 18,620 20,416 26,923 23,980 14,479 13,462

Median Income $63,999 $38,600 $60,210 $77,722 $81,944 $75,294 $54,574 $31,036

Less than $15,000 8,811 612 1,149 672 1,010 1,247 1,562 2,559

$15,000 to $24,999 6,845 463 856 452 676 793 1,083 2,522

$25,000 to $34,999 8,535 418 1,320 882 1,017 1,273 1,482 2,143$35,000 to $49,999 14,551 628 2,549 1,959 1,999 2,561 2,398 2,457

$50,000 to $74,999 21,996 801 4,034 3,512 4,089 4,269 3,519 1,772

$75,000 to $99,999 24,882 348 4,543 4,757 5,518 5,056 3,357 1,303

$100,000 or more 40,877 361 4,777 8,206 11,161 10,381 4,335 1,656

Total 126,497 3,631 19,228 20,440 25,470 25,580 17,736 14,412

Median Income $76,790 $41,390 $72,419 $87,105 $90,988 $85,961 $64,352 $34,887

Less than $15,000 58 ‐32 ‐28 ‐114 ‐204 ‐73 228 281

$15,000 to $24,999 ‐1,919 ‐94 ‐267 ‐365 ‐435 ‐385 ‐94 ‐279

$25,000 to $34,999 ‐2,703 ‐112 ‐469 ‐567 ‐652 ‐513 ‐108 ‐282

$35,000 to $49,999 ‐1,919 ‐72 ‐407 ‐491 ‐689 ‐438 89 89

$50,000 to $74,999 ‐1,999 ‐83 ‐344 ‐627 ‐1,039 ‐378 332 140

$75,000 to $99,999 6,203 74 1,174 948 782 1,349 1,375 501

$100,000 or more 6,993 47 949 1,240 784 2,038 1,435 500

Total 4,714 ‐272 608 24 ‐1,453 1,600 3,257 950

Median Income $12,791 $2,790 $12,209 $9,383 $9,044 $10,667 $9,778 $3,851

Sources: ESRI; US Census Bureau; Maxfield Research Inc.

2012

2017

Change 2012 ‐ 2017

TABLE B‐4

HOUSEHOLD INCOME BY AGE OF HOUSEHOLDER

PRIMARY MARKET AREA

2012 & 2017

Age of Householder

DEMOGRAPHIC ANALYSIS

MAXFIELD RESEARCH INC. 33

households are projected to increase to nearly 88,200 households (+10%) after accounting for inflation. Households under the age of 35 are most likely to rent their housing. In 2012, 41% of households age 24 and below and 65% of households age 25 to 34 in the PMA are estimated to have incomes of at least $47,000. Additionally, because younger householders are often willing to live with roommates, the percent income‐qualified is likely somewhat higher. Between 2012 and 2017, the number of income‐qualified PMA households in the 25 to 34 age cohort is expected to increase by approximately 1,264 households (+10.4%). The age 24 or younger cohort will lose approximately ‐83 income‐qualified households (‐5%) during this period.

Total <25 25‐34 35‐44 45‐54 55‐64 65 ‐74 75+

Less than $15,000 34,949 3,779 5,909 4,144 5,360 5,576 4,039 6,142

$15,000 to $24,999 28,746 2,582 4,803 3,270 3,927 3,854 3,514 6,796

$25,000 to $34,999 33,393 1,911 6,373 5,051 5,138 5,333 4,114 5,473$35,000 to $49,999 46,367 2,552 9,399 7,599 7,913 8,098 5,529 5,277

$50,000 to $74,999 63,844 2,610 13,313 11,826 13,876 11,927 7,119 3,173

$75,000 to $99,999 45,499 837 8,802 9,961 11,602 8,749 4,036 1,512

$100,000 or more 74,357 848 9,205 16,170 22,853 17,770 5,651 1,860

Total 327,155 15,119 57,804 58,021 70,669 61,307 34,002 30,233

Median Income $55,823 $30,570 $53,031 $66,951 $72,769 $64,027 $49,282 $28,161

Less than $15,000 35,995 3,750 6,070 3,877 4,796 5,653 4,901 6,948

$15,000 to $24,999 22,776 2,103 3,802 1,985 2,554 2,690 3,398 6,244

$25,000 to $34,999 25,921 1,480 4,891 3,331 3,331 4,033 3,961 4,894$35,000 to $49,999 41,670 2,326 8,390 6,314 6,101 7,154 5,876 5,509

$50,000 to $74,999 59,807 2,444 12,708 10,387 11,407 11,280 8,054 3,527

$75,000 to $99,999 61,399 1,099 12,151 12,733 13,787 12,196 6,922 2,511

$100,000 or more 90,692 1,020 11,736 19,343 24,891 22,436 8,557 2,709

Total 338,260 14,222 59,748 57,970 66,867 65,442 41,669 32,342

Median Income $65,868 $33,132 $60,637 $79,450 $82,483 $77,875 $56,256 $30,315

Less than $15,000 1,046 ‐29 161 ‐267 ‐564 77 862 806

$15,000 to $24,999 ‐5,970 ‐479 ‐1,001 ‐1,285 ‐1,373 ‐1,164 ‐116 ‐552

$25,000 to $34,999 ‐7,472 ‐431 ‐1,482 ‐1,720 ‐1,807 ‐1,300 ‐153 ‐579

$35,000 to $49,999 ‐4,697 ‐226 ‐1,009 ‐1,285 ‐1,812 ‐944 347 232

$50,000 to $74,999 ‐4,037 ‐166 ‐605 ‐1,439 ‐2,469 ‐647 935 354

$75,000 to $99,999 15,900 262 3,349 2,772 2,185 3,447 2,886 999

$100,000 or more 16,335 172 2,531 3,173 2,038 4,666 2,906 849

Total 11,105 ‐897 1,944 ‐51 ‐3,802 4,135 7,667 2,109

Median Income $10,045 $2,562 $7,606 $12,499 $9,714 $13,848 $6,974 $2,154

2012

2017

Change 2012 ‐ 2017

TABLE B‐5

HOUSEHOLD INCOME BY AGE OF HOUSEHOLDER

SECONDARY MARKET AREA

2012 & 2017

Age of Householder

DEMOGRAPHIC ANALYSIS

MAXFIELD RESEARCH INC. 34

The SMA household base is projected to grow by 3.4% (+11,105) between 2012 and 2017. Like the PMA though, higher growth in the income‐qualified household base is projected in the 25 to 34 age cohort. Whereas the 25 to 34 age cohort is projected to gain 1,944 house‐holds (+3.4%), the income‐qualified base is projected to increase by +3,647 households, for an 11.0% gain.

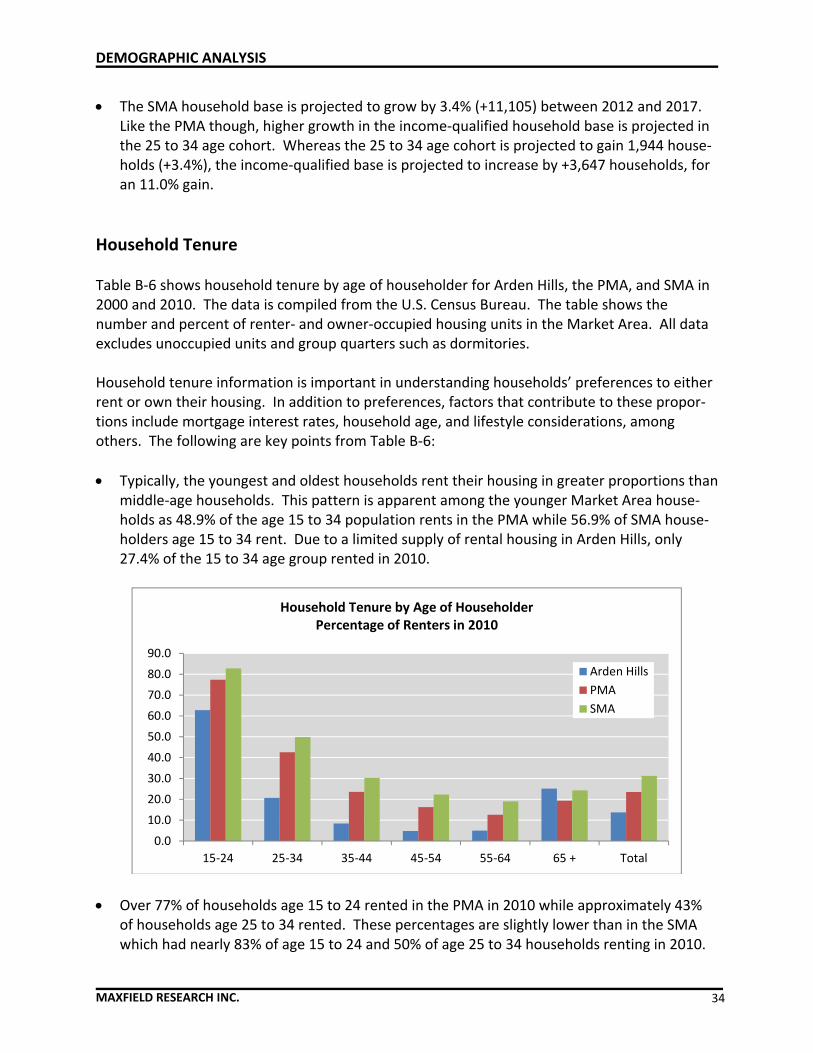

Household Tenure Table B‐6 shows household tenure by age of householder for Arden Hills, the PMA, and SMA in 2000 and 2010. The data is compiled from the U.S. Census Bureau. The table shows the number and percent of renter‐ and owner‐occupied housing units in the Market Area. All data excludes unoccupied units and group quarters such as dormitories. Household tenure information is important in understanding households’ preferences to either rent or own their housing. In addition to preferences, factors that contribute to these propor‐tions include mortgage interest rates, household age, and lifestyle considerations, among others. The following are key points from Table B‐6: