a growing pure play peruvian e&p independent

TRANSCRIPT

Ltd.

A Growing Pure Play Peruvian E&P Independent

Investor Presentation

June 2018

Investment Highlights

1

Figures in US$

1) 330 MMBO OOIP (Best Estimate) & 39.8 MMBO 2P reserves as evaluated by NSAI (December 31, 2017)

2) PetroTal internal estimates based on NSAI’s Dec 31, 2017 report and strip pricing on May 10, 2018

Strategic Partnership with

Gran Tierra in Peru

▪ Gran Tierra spin-out Peruvian assets for $35MM equity consideration into

Sterling Resources (TSX-V: SLG)

▪ Strategic partnership to develop & explore high impact properties

▪ Approximate market cap of CAD ~$110 million

Bretaña Oil Field

Development – A Unique

Value Proposition

▪ Low risk, high impact oil field with ~40 MMBO of certified 2P reserves(1)

▪ Accelerating first production from Bretaña (100% WI) in Q2-2018, and water

treatment and re-injection equipment expected to be in place by mid Q4-2018

▪ Anticipate $24.5MM capital expenditure to first production reduced by ~25%

▪ >5,000 bopd expected in Q2-2019; ramping up to >10,000 bopd(2)

▪ NPV10 of approx. $346MM(1) and 90% IRR(2) based on 12% recovery factor

Upside Potential -

Unrisked NPV10 Potential

of >$1 Billion

▪ Increasing Bretaña recovery factor from 12% to 24% will result in >2x increase

in NPV10 to over $705MM(2) based on the base case of 300mmbo OOIP

▪ Possible Bretaña oil pool size of 500 mmbo(1), and recovery factor of 24%, sets

the stage for significant additional upside

▪ Block 107 Osheki prospect brings significant upside

Block 95

Marañón Basin

Blocks

107/133

Blocks 123/129

Ucayali

Basin

Gran Tierra Blocks

Oil Pipeline

Gas Pipeline

Gas Pipeline (Construction)

River System

Lima

Corporate Overview

▪ Peru focused independent E&P company listed on the TSX-V

▪ Focused on acquisition, development and exploration of material oil assets in Peru

▪ Near term production from Bretaña – a material, high quality, low risk development asset

▪ 39.8 MMBO 2P reserves(1) with production

estimated to exceed 10,000 bopd by 2020

▪ Exploration potential from Osheki prospect in Block 107

▪ Fully funded capital program and no debt.

▪ Management and technical team with in depth expertise and proven track record in Peru(2)

2

Figures in US$

1) Block 95 Bretaña: 39.8 MMBO 2P reserves (NSAI Reserves Assessment dated December 31, 2017)

2) Occidental Petroleum was the largest oil producer in Peru from the mid 1970’s to the mid 1990’s.

Peru LNG

Talara Refinery

Experienced Leadership and Board

3

Private & ConfidentialFigures in US$

Management Board of Directors

▪ Manolo Zúñiga - Chief Executive Officer and Director

▪ Native Peruvian with >30 years of experience in petroleum engineering

▪ Started career with Occidental in Bakersfield & Block 192 in Peru

▪ Founder and former CEO of BPZ Energy

▪ Helped shape policies promoting oil investments in Peru, including the

current long-term test regulation

▪ Greg Smith - Executive Vice President & Chief Financial

Officer

▪ >20 years oil and gas experience, involved in over $3 billion in debt and

equity transactions

▪ Executive level finance and investor relations experience at Energy XXI

and BPZ Energy

▪ Estuardo Alvarez-Calderon – Vice President, Operations

▪ >35 years of oil and gas experience with focus on exploration and new

discoveries, and bringing those fields to initial production

▪ Various senior roles across the Americas for Occidental

▪ Former VP of Exploration and Production at BPZ Energy

▪ Chuck Fetzner - Vice President, Asset Development

▪ 35 years of experience managing exploration and development projects

spanning the USA, Peru, Colombia, Argentina, Chile, China and Africa

▪ 19 years at Apache as New Ventures Exploration & Development

Manager and Exploration Manager Worldwide Exploration

▪ Gary Guidry▪ President & CEO of Gran Tierra with >35 years as a Professional

Engineer with APEGA

▪ Former President & CEO of Caracal Energy, Orion O&G, Tanganyika Oil

▪ Senior operational roles at Occidental in Nigeria / West Africa, Yemen

and Venezuela

▪ Ryan Ellson▪ >15 years experience as a Chartered Accountant

▪ CFO of Gran Tierra

▪ Former Head of Finance at Glencore E&P Canada and VP Finance at

Caracal Energy

▪ Douglas Urch▪ Chartered Professional Accountant with >35 years experience in

international oil & gas

▪ Executive VP & CFO of Bankers Petroleum, former VP & CFO of Rally

Energy

▪ Gavin Wilson

▪ Director of Sterling & Investment Manager for Meridian

▪ Former founder & manager of RAB Energy & RAB Octane listed

investment funds

▪ Mark McComiskey▪ Founding Partner of Vanwall Capital, LLC. and was a Managing Partner of

Prostar Capital Ltd

▪ Former Principal of Clayton, Dubilier & Rice, Inc. He was an associate at

the law firm of Debevoise & Plimpton, LLP

PetroTal Team Has Significant Experience in Peru

4

Private & ConfidentialFigures in US$

Peruvian Projects PetroTal Team Has Worked Strong Occidental Background

Block / Field BasinPeak Daily

Production(1)

Recovery

To Date(1)

Exp

lore

d

Dis

co

ve

red

De

ve

lop

ed

Block 192

(1-AB)Marañón

106,180

bopd719 MMBO a a a

Block 8 Marañón 41,593 bopd 297 MMBO a a a

Block 107 Ucayali -- -- a

Block 56/88

CamiseaUcayali

286,000

boepd760 MMBOE a a a

Block 22 / 23Lancones /

Tumbes-- -- a a

Block 11 Talara 19,560 bopd 61 MMBO a a a

Block Z-1 Tumbes 8,000 bopd 11 MMBO a a a

Block Z-2B Talara 35,000 bopd 360 MMBO a a a

Jun

gle

—V

ivia

n /

Ch

on

taN

ort

hw

est

Pe

ru

Team Member and

PositionRelevant Experience from Occidental(2)

Occidental

Tenure

Jim

TaylorDirector

• Discovered & developed giant Caño Limón oilfield in

Colombia

• Involved in Block 1-AB appraisal & development

• COO of Canadian Occidental, directed the discovery

& development of the giant Masila oilfield in Yemen

28 years

Gary

GuidryDirector

• President & General Manager in Nigeria

• Manager Petroleum Engineering in Yemen

• Chief Reservoir Engineer in Venezuela

18 years

Estuardo

Alvarez-

Calderon

Manager

Exploration &

Development

• Senior roles at Occidental spanning the Americas

• Exploration Manager for Peru including Block 1-AB.

• Having published many technical papers, he is

recognized as an expert of Peru’s northern jungle

28 years

Luis

Pantoja

Production

Engineer

• Occidental production engineering supervisor for

Block 1-AB.

• Set standards for ESP performance and water

disposal wells in Block 192 (1-AB)

• Led the production and engineering operations in

Pluspetrol’s Camisea Field

18 years

Antonio

Zegarra

Reservoir

Engineer

• Experience spans Oman, Qatar, Libya

• Marañón & Talara basins in Peru, including Block 1-

AB where he led reservoir management to optimize

oil production while minimizing water production

34 years

Orestes

Orrego

Operations

Geologist

• Geologist involved in Occidental projects spanning

Qatar, Libya, Yemen, Russia, Venezuela, Paraguay,

Bolivia, Colombia, Texas (Permian), and Block 1-AB

35 years

▪ Previously held by Occidental (in Bold)

1) See endnotes for source data

2) Occidental & Yemen Ministry reports - see endnotes for source data

Asset Overview

■ Current portfolio consists of high quality development & exploration assets

■ Bretaña (Block 95) oil development located in the Marañon basin along the Ucayali river

– 39.8 MMBO 2P reserves(1)

– 79.3 MMBO 3P reserves(2)

– First production in Q2 2018 with production

estimated to exceed 10,000 bopd by 2020

■ Osheki exploration prospect (Block 107) located in the Ucayali basin

– On trend with several large fields

– Looking to drill an exploration well in 2019

funded through carry from contemplated

farm-out to credible partner(s)

– Several leads to be de-risked by Osheki

5

Figures in US$

1) Assumes ~12% Recovery Factor on 330 MMBO OOIP (Best Estimate), as evaluated by NSAI (December 31, 2017)

2) Assumes ~16% Recovery Factor on 500 MMBO OOIP (High Estimate), as evaluated by NSAI (December 31, 2017)

3) PetroTal internal management forecasts

Bretaña Oil Production Forecast(3)

■ Large Oil Field Close to First Production

– 330 MMBO of OOIP(1)

– First production well tested 3,095 bopd, 18.5o API, from

horizontal sidetrack in 2013

– $285MM previously invested – anticipated $24.5MM

capital expenditure to first production now reduced by ~25%

■ 2P Reserves With Financing Completed

– 39.8 MMBO of 2P Reserves(1)

– 100% oil production with nominal gas

■ Development Plan in Place

– First production expected in Q2-2018 (commissioning)

– Full development targeting plateau >10,000 bopd from

11 oil producing wells in 2020

– Infrastructure and export routes in place – established

barging and pipeline route to tide-water market

– Expected $31.50/bbl netback with oil at $65/bbl(2)

■ Exploration Upside on Trend

– 5 exploration prospects / leads on trend with Bretaña

Bretaña: Large Undeveloped Oil Field

6

Figures in US$

1) Based on NSAI Reserves Report dated December 31, 2017

2) Based on $65.00/bbl Brent crude price less $8.50 quality discount, $11.00 lifting costs, $11.00 transportation

costs, and $3.00 royalty payments

Development Rights Per

License Contract

■ Modern 3D seismic acquired in 2014

– Simple 4 way closing anticline

– Good velocity control for depth conversion

■ Five wells define structure and continuity of reservoir

– Consistent correlations across the field

– Massive Vivian reservoir - 300 feet thick in all wells

with ~100 foot gross oil column

– No variation in petrophysical properties

■ Consistent oil-water contact across the structure

– Petrophysics and pressure data support a

consistent contact and communication

– DST’s indicate high production index with little

drawdown and strong aquifer support

■ Similar trapping style to majority of producing fields in the basin

– Unfaulted, low amplitude 4 way closures

– Filled to structural spill point

– Massive and continuous reservoir

– Strong aquifer support

7

Figures in US$

Bretaña Field: Well Defined Low Risk Development

Bretaña’s Analog Fields Indicate Higher Recoveries

8

Figures in US$

• Bretaña estimated recovery factor of 12% is based on data set of three

wells & one core

• Every analog field in country has achieved >12% recovery factor (ranging

from 19.1% to 41.6%(1))

• These analog fields benefitted from horizontal reservoir barriers that

slowed down the water coning – also seen in Bretaña’s core

• Management believes that Bretaña has similar reservoir barriers and

could deliver >24% Recovery Factor

Reservoir Transmissibility

Analog Table(1,2)Bretaña

#1

Capahuari N.

#2

Carmen

#3

Yanayacu

#4

San Jacinto

#5

Jibaro

#6

Jibarito

API (o Gravity) 18.5o 35.2o 19.7o 19.0o 12.5o 10.6o 10.8o

Oil Viscosity (cp) 28.0 2.7 9.2 11.6 55.0 67.0 66.0

Permeability (Darcy) 2.2 0.3 1.0 1.0 2.0 2.0 4.0

Net Thickness (Feet) 32.0 23.7 26.3 29.0 46.1 47.7 54.6

Water Saturation (%) 38% 34% 49% 53% 36% 36% 28%

Porosity (%) 23% 13% 16% 19% 20% 18% 19%

OOIP (MMBO) 330 48 45 65 209 152 262

EUR / 2C (MMBO) 39.8 20.0 13.5 23.6 46.3 29.0 74.2

Recovery (%) 12.0% 41.6% 29.9% 36.1% 22.2% 19.1% 28.3%

1) NSAI Reserves Report (December 31, 2017) for Bretaña and Perupetro S.A. / Pluspetrol for all analog fields

2) Reservoir Transmissibility = Permeability x Net Thickness / Oil Viscosity

(Properly Sized) Facilities Going Back to Bretaña

9

Figures in US$

March 2017February 2015

May 2018May 2018

Accelerating Opening of Existing Horizontal Well

10

Figures in US$

• The Bretaña oil well expected to initially produce 100% crude oil, so oil production facilities are being installed first to be

able to open the well in June at ~1,000 bopd. Currently, we are 80% complete installing the oil production facilities.

• Water treatment and reinjection facilities on schedule to be ready by October 31st, at which time the oil well would be

opened up to produce ~2,250 bopd; though we will try to increase the choke in September to ~1,500 bopd.

Potential to produce ~50% more oil than the 218,000 bbl initially forecast, delivering important cash flow.

Op

en

well a

t ~

1,0

00

bo

pd

Op

en

ch

ok

e t

o ~

2,2

50

bo

pd

1 week lost due to

rainy season. Will

catch up now that we

are in the dry season.

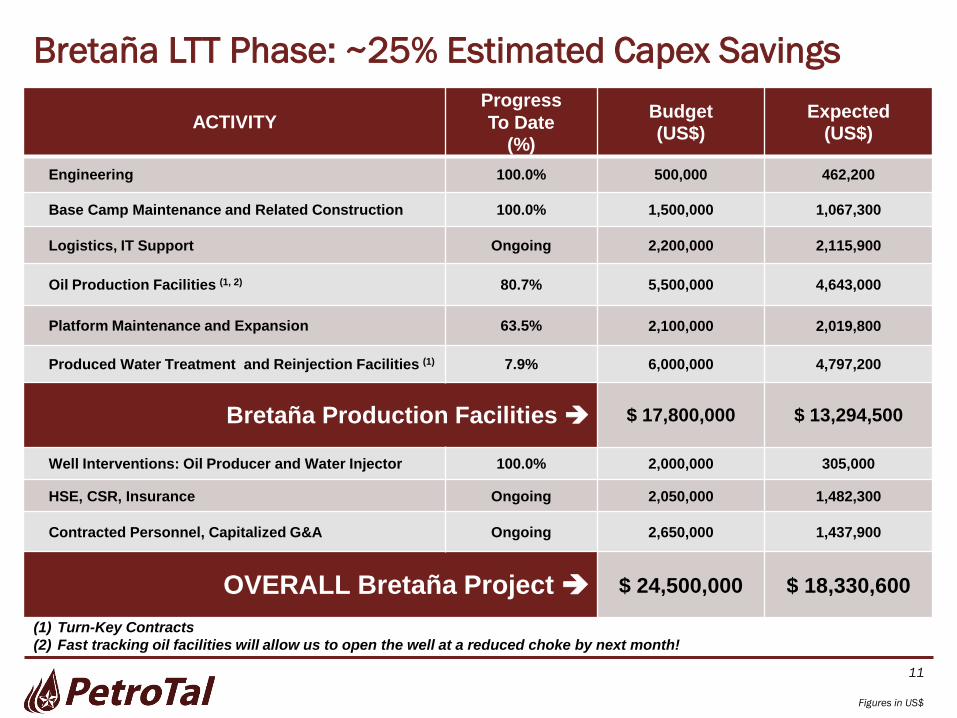

Bretaña LTT Phase: ~25% Estimated Capex Savings

11

Figures in US$

ACTIVITYProgress

To Date(%)

Budget (US$)

Expected(US$)

Engineering 100.0% 500,000 462,200

Base Camp Maintenance and Related Construction 100.0% 1,500,000 1,067,300

Logistics, IT Support Ongoing 2,200,000 2,115,900

Oil Production Facilities (1, 2) 80.7% 5,500,000 4,643,000

Platform Maintenance and Expansion 63.5% 2,100,000 2,019,800

Produced Water Treatment and Reinjection Facilities (1) 7.9% 6,000,000 4,797,200

Bretaña Production Facilities $ 17,800,000 $ 13,294,500

Well Interventions: Oil Producer and Water Injector 100.0% 2,000,000 305,000

HSE, CSR, Insurance Ongoing 2,050,000 1,482,300

Contracted Personnel, Capitalized G&A Ongoing 2,650,000 1,437,900

OVERALL Bretaña Project $ 24,500,000 $ 18,330,600

(1) Turn-Key Contracts

(2) Fast tracking oil facilities will allow us to open the well at a reduced choke by next month!

Early Production Confirmed for Iquitos Refinery

12

Figures in US$

Block 95

Iquitos

Refinery

Br

2

Bretaña Export Route

■ Initial 1,000 bbl/d expected to be sold at Iquitos Refinery

■ With full production, barge oil north-then-west to Pump Station #1 (est. $6.00/bbl)

■ Deliver oil to Bayóvar via Northern Oil Pipeline (200,000 bopd capacity / ~10% utilized) for marketing and sale (est. $7.50 tariff/bbl and forecast to drop to $5.50/bbl on increased volumes)

■ Bretaña crude oil would be ideal for the Talara Refinery, whose ongoing expansion and upgrade is expected to be completed by late 2020

Pump Station #1

San José de

Saramuro

Bayóvar

1

2

3

Talara Refinery

4

4

3

1

Bretaña LTT Timeline

13

Figures in US$

Close

transaction

Commence

installation of

facilities

Convert 2C

resources to 2P

reserves

Workover or

Slickline

intervention of

existing wells

First production

from existing oil

well ready

2 wells

producing

~5,000 bopd

Drill second oil

development

well

Commence full

field

development

Development

EIA Approval

2020:

Ramp-Up

>10,000

bopd

Period

End Cash:

Q4-17

$49M

M

Q1-18

$41MM

Q2-18

$30MM

Q3-18

$22MM

Q4-18

$19MM

Q1-19

$24MM

Q2-19

$24MM

Q3-19

$19MM

Q4-19

$25MM

Early Oil Production

(50% incremental oil production)

Saved $1.7mm

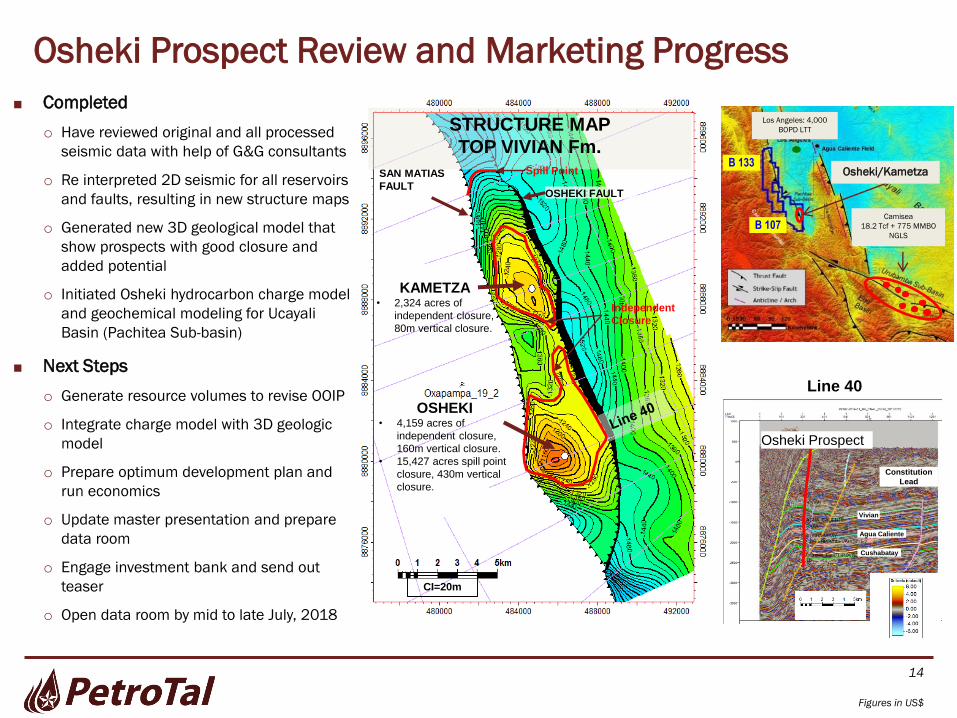

■ Completed

o Have reviewed original and all processed

seismic data with help of G&G consultants

o Re interpreted 2D seismic for all reservoirs

and faults, resulting in new structure maps

o Generated new 3D geological model that

show prospects with good closure and

added potential

o Initiated Osheki hydrocarbon charge model

and geochemical modeling for Ucayali

Basin (Pachitea Sub-basin)

■ Next Steps

o Generate resource volumes to revise OOIP

o Integrate charge model with 3D geologic

model

o Prepare optimum development plan and

run economics

o Update master presentation and prepare

data room

o Engage investment bank and send out

teaser

o Open data room by mid to late July, 2018

Osheki Prospect Review and Marketing Progress

14

Figures in US$

Line 40

Vivian

Agua Caliente

Cushabatay

Osheki Prospect

Constitution

Lead

OSHEKI• 4,159 acres of

independent closure,

160m vertical closure.

• 15,427 acres spill point

closure, 430m vertical

closure.

CI=20m

SAN MATIAS

FAULTOSHEKI FAULT

KAMETZA• 2,324 acres of

independent closure,

80m vertical closure.

STRUCTURE MAP

TOP VIVIAN Fm.

Camisea

18.2 Tcf + 775 MMBO

NGLS

Los Angeles: 4,000

BOPD LTT

Osheki/KametzaB 133

B 107

Spill Point

Independent

Closure

Bretana NAV Shows Pre-production Discount

15

Figures in US$

(in millions)

CORE NAV OOIP

Recovery

Factor Net EUR NPV10 NAV Price

MMBO 12% MMBO $MM USD (per share) (core NAV)

(unrisked)

Bretana Oil Field 330 39.8 39.8 $346

Net Cash (year-end) $48

CORE VAV $394 $0.73 0.22X

Upside NAV @

24% recovery factor 79.9 $705 $1.31 0.12X

Assumptions:

Price deck is strip prices on May 10, 2018

Share price assumes closing price of $0.16 (USD)

Total share out 537,735,991

Corporate Summary

16

Figures in US$

2-3 Year Term:

Deliver 2 - 3x ROI

5 Year Term:

Achieve 6 - 8x NAV/Share Growth

1. Bring Bretaña fully online in Q4 2018

2. Confirm Bretaña’s original-oil-in-place

estimate

3. Establish Bretaña plateau at >10,000 bopd

4. Secure WI partner and drill Osheki Prospect

1. Demonstrate Bretaña’s ability to achieve

higher recovery factors

2. Develop Osheki upon successful discovery

3. Pursue synergistic oil projects to Bretaña

4. Pursue complementary projects in other

Peruvian oil regions

Unlock Peruvian Asset Value & Create Scalability to Maximize Shareholder Value

Manolo Zuniga

(713) 609-9101

Greg Smith

(713) 609-9026

17

Figures in US$

PetroTal

Suite 500

11451 Katy Freeway

Houston, TX 77079

Legal Counsel (Canada): McCarthy Tetrault LLP

Legal Counsel (USA): Seyfarth Shaw LLP

Legal Counsel (Peru): Estudio Gálvez Abogados

Independent Reservoir Engineering Firm: Netherland Sewell & Associates

Audit Firm: Deloitte (Canada)

Ltd.

Peru: Country Overview

■ Stable & Growing Pro-Business Country

– 5.9% average GDP growth over the past decade

• Projected 3.8% average over next two years

– Democratic, investment grade government with stable /

positive outlook: A3 (Moody’s) / BBB+ (S&P and Fitch)

– Standardized contracts signed into law by supreme decree

– Excellent fiscal/royalty terms and tax regime

■ Established Oil & Gas Industry

– Production: ~135,000 bopd (oil & NGLs) + 1.25 Bcf/d

– Discovered Resources: 11.0 BNBOE, 55% Liquids

– Operators include Pluspetrol, CNPC, Repsol, Hunt, CEPSA,

Perenco, Ecopetrol, Anadarko, Tullow, Shell, GeoPark

– Oilfield services: Baker Hughes, Parker Drilling, Halliburton,

Schlumberger, Weatherford, ENI / Petrex

– Established infrastructure with capacity and transparent

pricing

– 240,000 bopd (oil & NGL) consumption with refining

capacity of 193,000 bopd (2016 PetroPeru)

– Net importer of ~69,000 bopd of crude oil & oil products

from USA (2016)

18

Figures in US$

Talara Refinery: Key Market for Bretaña Oil

Peru Liquid Fuels Demand

2016 demand growth of 9% -

demand growth of 20% in

preceding 4 years

~$3B expansion & upgrade, expected completion 2020

Source: Ministry of Energy and Mines, PETROPERU S.A. Includes sales

of TurboJet (A1) to foreign airlines.

Experienced Leadership and Board

19

Figures in US$

Management Board of Directors

Manolo Zúñiga - Chief Executive Officer and Director

• Native Peruvian with >30 years of experience in petroleum engineering

• Started career with Occidental in Bakersfield & Block 192 in Peru

• Founder and former CEO of BPZ Energy

• Helped shape policies promoting oil investments in Peru, including the

current long-term test regulation

Greg Smith - Executive Vice President & Chief Financial Officer

• >20 years oil and gas experience, involved in over $3 billion in debt and

equity transactions

• Served as CFO for PetroTal LLC prior to the amalgamation

• Executive level finance and investor relations experience at Energy XXI

and BPZ Energy

Estuardo Alvarez-Calderon – Vice President, Operations

• >35 years of oil and gas experience with focus on exploration and new

discoveries, and bringing those fields to initial production

• Various senior roles across the Americas for Occidental

• Former VP of Exploration and Production at BPZ Energy

Chuck Fetzner - Vice President, Asset Development

• 35 years of experience managing exploration and development projects

spanning the USA, Peru, Colombia, Argentina, Chile, China and Africa

• 19 years at Apache as New Ventures Exploration & Development

Manager and Exploration Manager Worldwide Exploration

Gary Guidry• President & CEO of Gran Tierra with >35 years as a Professional

Engineer with APEGA

• Former President & CEO of Caracal Energy, Orion O&G, Tanganyika Oil

• Senior operational roles at Occidental in Nigeria / West Africa, Yemen

and Venezuela

Ryan Ellson• >15 years experience as a Chartered Accountant

• CFO of Gran Tierra

• Former Head of Finance at Glencore E&P Canada and VP Finance at

Caracal Energy

Douglas Urch• Chartered Professional Accountant with >35 years experience in

international oil & gas

• Executive VP & CFO of Bankers Petroleum, former VP & CFO of Rally

Energy

Gavin Wilson

• Director of Sterling & Investment Manager for Meridian

• Former founder & manager of RAB Energy & RAB Octane listed

investment funds

Mark McComiskey

• Founding Partner of Vanwall Capital, LLC. and was a Managing Partner of

Prostar Capital Ltd

• Former Principal of Clayton, Dubilier & Rice, Inc. He was an associate at

the law firm of Debevoise & Plimpton, LLP

• Holds a J.D., magna cum laude, from Harvard Law School and an A.B.

degree, magna cum laude, in Economics from Harvard College

Disclaimers

20

Figures in US$

Forward-Looking Information

Certain information included in this presentation constitutes forward-looking information under applicable securities legislation. Forward-looking information typically containsstatements with words such as “anticipate”, “believe”, “expect”, “plan”, “intend”, “estimate”, “propose”, “project” or similar words suggesting future outcomes or statementsregarding an outlook. Forward-looking information in this presentation may include, but is not limited, statements about: the Company’s corporate strategy; potentialdevelopment opportunities and drilling locations, expectations and assumptions concerning the success of future drilling, development, transportation and marketing activities,the performance of existing wells, the performance of new wells, decline rates, recovery factors, the successful application of technology and the geological characteristics ofproperties; capital program and capital budgets; future production levels; net cash; debt; primary and secondary recovery potentials and implementation thereof; potentialacquisitions; regulatory processes; drilling, completion and operating costs; commodity prices and netbacks; realization of anticipated benefits of acquisitions; NAV valuations.Statements relating to “reserves” are also deemed to be forward looking statements, as they involve the implied assessment, based on certain estimates and assumptions, thatthe reserves described exist in the quantities predicted or estimated and that the reserves can be profitably produced in the future.

The forward-looking information is based on certain key expectations and assumptions made by the Company, including, but not limited to, expectations and assumptionsconcerning the ability of existing infrastructure to deliver production and the anticipated capital expenditures associated therewith, reservoir characteristics, recovery factor,exploration upside, prevailing commodity prices and the actual prices received for Sterling’s products, the availability and performance of drilling rigs, facilities, pipelines, otheroilfield services and skilled labour, royalty regimes and exchange rates, the application of regulatory and licensing requirements, the accuracy of Sterling’s geologicalinterpretation of its drilling and land opportunities, current legislation, receipt of required regulatory approval, the success of future drilling and development activities, theperformance of new wells, the Company’s growth strategy, general economic conditions, availability of required equipment and services and prevailing commodity prices.Although the Company believes that the expectations and assumptions on which the forward-looking statements are based are reasonable, undue reliance should not be placedon the forward-looking statements because the Company can give no assurance that they will prove to be correct. Readers are cautioned that the foregoing list is not exhaustiveof all factors and assumptions which have been used.

Since forward-looking statements address future events and conditions, by their very nature they involve inherent risks and uncertainties. Actual results could differ materiallyfrom those currently anticipated due to a number of factors and risks. These include, but are not limited to, risks associated with the oil and gas industry in general (e.g.,operational risks in development, exploration, production and transportation; delays or changes in plans with respect to exploration or development projects or capitalexpenditures; the uncertainty of reserve and resource estimates; the uncertainty of estimates and projections relating to production, costs and expenses, and health, safety,environmental and regulatory risks), commodity price and exchange rate fluctuations, legal, political and economic instability in Peru, access to transportation routes andmarkets for the Company’s production, changes in legislation affecting the oil and gas industry, and uncertainties resulting from potential delays or changes in plans withrespect to exploration or development projects or capital expenditures. Please refer to the risk factors identified in the Company’s annual information form and management’sdiscussion and analysis for the year ended December 31, 2017 which are available on SEDAR at www.sedar.com. Forward-looking information is based on current expectations,estimates and projections that involve a number of risks and uncertainties which could cause actual results to differ materially from those anticipated by the proposedmanagement and described in the forward-looking information. The forward-looking information contained in this presentation is made as of the date hereof and the proposedmanagement undertakes no obligation to update publicly or revise any forward-looking information, whether as a result of new information, future events or otherwise, unlessrequired by applicable securities laws. The forward-looking information contained in this presentation is expressly qualified by this cautionary statement.

Financial Outlook

This presentation contains future-oriented financial information and financial outlook information (collectively, “FOFI”) about Sterling’s prospective results of operations, netcash, netbacks, operating costs and components thereof, all of which are subject to the same assumptions, risk factors, limitations and qualifications as set forth in the aboveparagraphs and the assumption outlined in the Non-GAAP measures section below. FOFI contained in this presentation was made as of the date of this presentation and wasprovided for the purpose of providing further information about Sterling’s anticipated future business operations. Sterling disclaims any intention or obligation to update orrevise any FOFI contained in this presentation, whether as a result of new information, future events or otherwise, unless required pursuant to applicable law. Readers arecautioned that the FOFI contained in this presentation should not be used for purposes other than for which it is disclosed herein.

Disclaimers (continued)

21

Figures in US$

Oil and Gas Advisories

Reserves Disclosure. The reserve estimates contained herein are estimates only and there is no guarantee that the estimated reserves will be recovered. Volumes of reserveshave been presented based on a company interest. Readers should give attention to the estimates of individual classes of reserves and appreciate the differing probabilities ofrecovery associated with each category as explained herein. The estimates of reserves for individual properties may not reflect the same confidence level as estimates ofreserves for all properties, due to the effects of aggregation.

Where discussed herein “NPV10” or similar expressions represents the net present value (net of capex) of net income discounted at 10%, with net income reflecting theindicated oil, liquids and natural gas prices and IP rate, less internal estimates of operating costs and royalties. It should not be assumed that the future net revenues estimatedby Sterling’s independent reserves evaluators represent the fair market value of the reserves, nor should it be assumed that Sterling’s internally estimated value of itsundeveloped land holdings or any estimates referred to herein from third parties represent the fair market value of the lands.

Reserve Categories. Reserves are classified according to the degree of certainty associated with the estimates. Proved reserves (1P) are those reserves that can be estimatedwith a high degree of certainty to be recoverable. It is likely that the actual remaining quantities recovered will exceed the estimated proved reserves. Probable reserves (2P) arethose additional reserves that are less certain to be recovered than proved reserves. It is equally likely that the actual remaining quantities recovered will be greater or less thanthe sum of the estimated proved plus probable reserves. Possible reserves (3P) are those additional reserves that are less certain to be recovered than probable reserves. It isunlikely that the actual remaining quantities recovered will exceed the sum of the estimated proved plus probable plus possible reserves.

BOE Disclosure. The term barrels of oil equivalent (“BOE”) may be misleading, particularly if used in isolation. A BOE conversion ratio of six thousand cubic feet per barrel(6Mcf/bbl) of natural gas to barrels of oil equivalence is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent avalue equivalency at the wellhead. All BOE conversions in the report are derived from converting gas to oil in the ratio mix of six thousand cubic feet of gas to one barrel of oil.

Analogous Information. Certain information in this document may constitute "analogous information" as defined in National Instrument 51-101 – Standards of Disclosure for Oiland Gas Activities ("NI 51-101"), including, but not limited to, information relating to areas, wells and/or operations that are in geographical proximity to or on-trend with landsheld by Sterling and production information related to wells that are believed to be on trend with Sterling's properties. Such information has been obtained from governmentsources, regulatory agencies or other industry participants. Management of Sterling believes the information may be relevant to help define the reservoir characteristics in whichSterling may hold an interest and such information has been presented to help demonstrate the basis for Sterling's business plans and strategies.

However, to Sterling’s knowledge, such analogous information has not been prepared in accordance with NI 51-101 and the Canadian Oil and Gas Evaluation Handbook andSterling is unable to confirm that the analogous information was prepared by a qualified reserves evaluator or auditor. Sterling has no way of verifying the accuracy of suchinformation. There is no certainty that the results of the analogous information or inferred thereby will be achieved by Sterling and such information should not be construed asan estimate of future production levels. Such information is also not an estimate of the reserves or resources attributable to lands held or to be held by Sterling and there is nocertainty that the reservoir data and economics information for the lands held or to be held by Sterling will be similar to the information presented herein. The reader iscautioned that the data relied upon by Sterling may be in error and/or may not be analogous to such lands to be held by Sterling.

Initial Production Rates. Any references in this document to test rates, flow rates, initial and/or final raw test or production rates, early production, test volumes and/or "flush"production rates are useful in confirming the presence of hydrocarbons, however, such rates are not necessarily indicative of long-term performance or of ultimate recovery.Such rates may also include recovered "load" fluids used in well completion stimulation. Readers are cautioned not to place reliance on such rates in calculating the aggregateproduction for Sterling. In addition, the resource play which may be subject to high initial decline rates. Such rates may be estimated based on other third party estimates orlimited data available at this time and are not determinative of the rates at which such wells will continue production and decline thereafter.

OOIP Disclosure. The term original-oil-in-place (“OOIP”) is equivalent to total petroleum initially-in-place (“TPIIP”). TPIIP, as defined in the Canadian Oil and Gas EvaluationHandbook, is that quantity of petroleum that is estimated to exist in naturally occurring accumulations. It includes that quantity of petroleum that is estimated, as of a givendate, to be contained in known accumulations, prior to production, plus those estimated quantities in accumulations yet to be discovered. A portion of the TPIIP is consideredundiscovered and there is no certainty that any portion of such undiscovered resources will be discovered. If discovered, there is no certainty that it will be commercially viableto produce any portion of such undiscovered resources. With respect to the portion of the TPIIP that is considered discovered resources, there is no certainty that it will becommercially viable to produce any portion of such discovered resources. A significant portion of the estimated volumes of TPIIP will never be recovered.

Disclaimers (continued)

22

Figures in US$

US Disclaimer

This presentation is not an offer of the securities for sale in the United States. The securities have not been registered under the U.S. Securities Act of 1933, as amended, and may not be offered or sold in the United States absent registration or an exemption from registration. This presentation shall not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the securities in any state in which such offer, solicitation or sale would be unlawful.

All figures in US dollars unless otherwise denoted.

Abbreviations

bbl barrel API an indication of the specific gravity of crude oil measured on the American Petroleum Institute gravity scale. Liquid

petroleum with a specified gravity of 28° API or higher is generally referred to as light crude oil

bopd barrel of oil per day NAV net asset value

mmbo million barrels of oil Mcf million cubic feet

NGL natural gas liquids Bcf/d billion cubic feet per day

BNBOE billion barrels of oil

equivalent

IRR internal rate of return

NGL natural gas liquids WI working interest

NPV net present value EUR estimated ultimate recovery