a copper-gold producer in the making - northisle · northisle company snapshot company overview...

TRANSCRIPT

A Copper-Gold Producer

in the Making

100% owned North Island Project on

Vancouver Island in British Columbia, Canada

February 2018

TSXV: NCX 2

Northisle Company Snapshot

Company Overview Capital Structure(November 30, 2017)

Project Location 1 Year Share Price

Head Office Vancouver, Canada

Project Hushamu located in Port Hardy, Canada

Ownership 100%

Stage PEA

ResourceM&I: 2.1 B lbs Cu, 3.4 M oz Au & 66M lbs Mo

Inf: 0.6 B lbs Cu, 0.9M oz Au & 19M lbs Mo

Economics(1) NPV8% of C$ 550.4m and IRR 14.3%

1. Commodity prices used in the PEA are as follows: US$ 3.10/lb Cu, US$ 1,300/oz Au, US$ 9.00/lb Mo, US$ 9/t Py con, US$:C$ 0.75x

Listing TSXV – NCX

Share 114.5 M shares

Market Cap. C$ 11.5 M

Options &

Warrants

7.7 M options,

5.9 M warrants avg price $0.16

Cash C$ 744 K

Debt None

Covers a 50km porphyry

belt

Two deposits and multiple

exploration targets

TSXV: NCX 3

Northisle Investment Case

Technically de-

Risked

Proven

Management

Robust Mining

Project(1)

Superior economics with significant exposure to Cu, Au and Mo

‒ LOM copper production of 82mlbpa at C1 cost of US$ 0.88/lb (net of by-products) for 22 years, subsequent

to a initial capital cost of US$ 1bln

‒ Inaugural after-tax NPV8% of C$ 550.4m and IRR of 14.3%

Technically de-risked through inaugural Preliminary Economic Assessment (“PEA”)

‒ Historical resources converted to NI 43-101 current resources

‒ Resource expanded by nearly 100%

‒ Initial starter pit acquired in nearby Red Dog deposit

Current management has a proven track record of creating shareholder value

‒ Dale Corman, CEO of Western Silver up to merger with Glamis (now Goldcorp)

‒ Jack McClintock, Winner of the PDAC prospector of the year award for discovery of Spence deposit, Chile.

Safe Jurisdiction

British Columbia ranks as the 27th best mining jurisdiction

‒ Five copper-gold mines already in production with similar grade profiles to Hushamu

‒ The Fraser Institute ranks British Columbia as the 27th best jurisdiction to invest in.

Expansion &

Optimization

Resource is open to the south east direction with a number of further engineering optimisations to come

‒ District play with over 50 km of strike and 5 number of exploration targets

‒ Further potential to enhance recoveries and mine design to improve economics

1. Commodity prices used in the PEA are as follows: US$ 3.10/lb Cu, US$ 1,300/oz Au, US$ 9.00/lb Mo, US$ 9/t Py con, US$:C$ 0.75x

Northisle is just beginning a long journey of value creation…

TSXV: NCX 4

Board of Directors

Dale Corman B.Sc, P.Eng, Chairman

40 years experience as a senior corporate officer of publicly listed companies.

Extensive expertise in mineral exploration & development, financing, property

evaluation and acquisition. Currently Executive Chairman of Western Copper and

Gold Corporation.

Jack McClintock MBA, P.Eng Director,

President and CEO

30 years experience in all facets of the mineral exploration business and

formerly Exploration Manager for BHP Billiton.

Martino De CiccioCFA, Director

Over 10 years in the mining industry with a track record of significant value creation.

Currently VP Strategy & Investor Relations at Endeavour Mining since 2015. Prior to

Endeavour, held the position of Strategy and Business Development Manager at La

Mancha Resources.

David Douglas CA, Director and CFO

Chartered Accountant with over 30 years of experience in the accounting, corporate

finance, and mining industries. He has participated in the sale or financing of over 30

private and public enterprises with a combined value

of over $300 million.

Brandon Macdonald B.Sc., MBA, Director

Over 20 years in the mining industry with experience in field geology, investment

banking, and company management.

Larry YauCA, Director

20 years of financial and business experience, gained primarily in the mining and

resources sectors. Most recently served as CFRO for two junior mining companies

where he was heavily involved in raising capital and the successful construction of

mines in North America. Previously was Manager, Corporate Development, at Placer

Dome Inc. until its acquisition by Barrick Gold Corp.

The right mix of exploration, engineering and finance…

TSXV: NCX 5

History of Hushamu

Northisle has significantly improved the project since 2011

Consensus Investment Community perception in 2011 was Hushamu deposit too smalland lacked near surface, high-grade starter pit to be economic

Northisle’s work since 2011 has corrected this wrong perception by:

Re logging and properly interpretation of geology in 2011 showed deposit was openin multiple direction

Drilling in 2012 through 2014 found extensions and increased tonnage of indicatedmineralization from 250 Mt to current indicated resource of 370 Mt

Acquired nearby Red Dog project in 2015 for initial starter pit. Red Dog depositgrade higher by 50% than Hushamu and has a 0.15 to 1 strip ratio

Drilling in 2017 demonstrated:

That Hushamu deposit remains open for 300 m southeast of ultimate pit limitused in PEA and deposit could be significantly larger

A previously supposed 300 m diameter, under drilled barren area in thesouthern part of the Hushamu has significant sections of above cut-off grademineralization. This potentially could decrease the strip ratio and add to theresource base

TSXV: NCX 6

Summary Economics

After Tax Base Case Spot Price

NPV8% C$ 550.4m C $549.0

IRR 14.3% 14.3%

Payback 5.1 years 5.1 years

C1 Cash Cost(1) US$ 0.88/lb Cu C1 Cash Cost(1) US$ 542/oz

Capital Cost C$ 1,344m Sustaining Capital C$139.0m

C$ 550.4m 14.3%NPV8% After-tax IRR After-tax

5.1 Years

Payback After-tax

1. Commodity prices used in the PEA are as follows: US$ 3.10/lb Cu, US$ 1,300/oz Au, US$ 9.00/lb Mo, US$ 86/t Py con, US$:C$ 0.75x

2. Spot prices US$ 3.12/lb Cu, US$ 1,333/oz Au, US$ 7.14/lb Mo, US$ 86/t Py con, US$:C$ 0.75x

Base Case Robust Economics…

The Preliminary Economic Assessment (“PEA”) is preliminary in nature and includes inferred mineral resources that are considered too speculative geologically to have the economic

considerations applied to them that would allow them to be categorized as mineral reserves and there is no certainty that the preliminary economic assessment will be realized.

TSXV: NCX 7

Economics – Base Case

Financial Parameters Production Parameters

Capital Cost C$ $1,344 Mine Life Years 22

Sustaining C$ $139 Cu M lb pa 82

Operation Cost per

TonneC$M $8.66 Au Koz

79

After-tax Net Revenue C$M $2,350 Mo M lb pa 3

After Tax NPV8%(1) C$M $550.4 Py Concentrate ktpa 0.64

After Tax IRR % 14.3% C1 Cash Costs US$/lb0.88

Metal Prices

Cu US$/lb 3.10 Mining Inventory Mt600

Au US$/oz 1,300 Cu Grade %0.18%

Mo US$/oz $9.00 Au Grade %0.24

Py Concentrate US$/t $86 Mo Grade %0.008%

Exchange Rate x 0.75 Py Grade %9%

A material amount of metal production at a low-cost of production

1. Commodity prices used in the PEA are as follows: US$ 3.10/lb Cu, US$ 1,300/oz Au, US$ 9.00/lb Mo, US$ 9/t Py con, US$:C$ 0.75x

TSXV: NCX 8

Catalyst for Value Creation

I. Improve gold recoveries through additional flotation metallurgical testing (higher revenue per tonne)

II. Demonstrate potential for rhenium credits in the Mo concentrate through metallurgical flotation testing (rhenium could contribute the same as Mo revenue)

III. Using BHP pit located 30 km away for waste disposal via slurry pipeline (it would both decrease initial capital and sustaining capital)

IV. Optimize production rate: if going to 85ktpa or 90ktpa throughput (further economies of scale)

V. Brownfields expansion of Hushamu resource: the deposit is open to the southeast (potentially expand the deposit by up to 300m)

VI. A previously supposed 300 metre diameter low grade to barren area in the south of the deposit was found by 2017 drilling to have significant intervals above cut-off grade (further decrease strip ratio)

Low-risk value enhancements likely to further improve economics

TSXV: NCX 9

Catalyst for Value Creation

I. Red Dog – Resource Expansion:

− drilling in 2016 and 2017 shows potential for buried porphyry deposit to south ofknown deposit

− 1.2km x 0.8 km area of high level porphyry alteration

− Shallow drill holes show increasing copper grades with depth

II. Pemberton Hills – Exploration Target:

− 3.5 km by 1.5km area of intense high-level alteration.

− Mapping and clay studies show it is the upper part of a buried Cu-Au porphyry.

− Shallow hole ended in 0.14% copper

III. NW Expo – Exploration Target:

− Large 1.5 km long IP anomaly

− Three holes tested to the northwest intersected intervals of +80m averaging 0.1% Cuand 0.1 g/t Au or better

Game changer – 50km porphyry district play and just beginning…

TSXV: NCX 10

Comparable Projects IRR’s

Project

IRR

After-

tax

Cu

US$/lb

Au

US$/oz

Mo

US$/lb

Northisle 14.3% $3.10 $1,300 $9.00

Seabridge 8% $3.45 $1,320 $15.00

Shaft Creek 8% $3.25 $1,445 $14.64

Blackwater 9.3% na $1,300 na

Ajax 11.1% $3.21 $1,200 na

Ann Maison 13.7% $3.00 na $11.00

Pumpkin

Hollow15.6% $3.15 $1,200 na

Rose Mount 15.5% $3.00 na $11.00

Casino 20.8% $2.85 $1,260 $7.00

Average 12.9% $3.12 $1289 $11.27

Hushamu PEA compares favorable with other regional deposits

Expected IRR at NCX’s Projectcompares well with other NorthAmerican projects due to anumber of factors:

− Low-strip ratio 0.72:1 with potential tofurther reduce with exploration byconverting barren and low-grade areasto the resource category

− Near brownfields developmentopportunity with existing infrastructureincluding ports, power, town andairport equals low execution risk andsignificantly lower capital cost

− Local communities that understandand support mining

Compiled from the best of the Company’s knowledge as of August 2017

TSXV: NCX 11

Comparable Resources at Operating British Columbian Mines

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

Mt P

olle

y

Hucklb

err

y

Copp

er

Mtn

.

Mt M

illig

an

Gib

ralta

r

*Husham

u

%

Copper %

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

Mt P

olle

y

Hucklb

err

y

Copp

er

Mtn

.

Mt M

illig

an

Gib

ralta

r

*Husham

u

g/t

Gold%

0

0.1

0.2

0.3

0.4

0.5

0.6

Mt P

olle

y

Hucklb

err

y

Copp

er

Mtn

.

Mt M

illig

an

Gib

ralta

r

*Husham

u

Cu

Eq

%

Copper equivalent %

Comparable Operating Mines

Hushamu Deposit

Grades compare well with current operating mines in BC

(Based on Cu Eq at $2.50, $1,100 Au, $14 Mo)

TSXV: NCX 12

Simple and straight forward mining

Power Supply via a new, 30 kmlong 138 KV overhead line from theexisting BC Hydro sub-station nearPort Hardy

Process water supply from contactwater from pit & WSF and potablewater from wells

Concentrate receiving, storage, andloadout to ships at a facility to bedeveloped by a third party on thesite of former Island Copper marineterminal. Approximate concentratehaul distance is 27 km

Base case is for 55/45 LNG/dieselfuel mixture for haulage fleet using227 tonne trucks

Cross Section of Hushamu

Cross Section of Red Dog

TSXV: NCX 13

Conventional floatation

Single grinding lineconsisting of a 40 ft.diameter SAG mill with 23MW drive, and two – 28 ft.diameter ball mills with 20MW drives

Sub-aqueous co-disposalof mine waste and tailingsin a single waste storagefacility (WSF)

Bulk concentrate isseparated in to copper-gold, molybdenum andpyrite

LOM recoveries for copper78%, gold 38% and moly60%

Hushamu’s flowsheet will be a straight forward floatation

TSXV: NCX 14

Exploration Upside

New Deposit

Discovery

Hushamu

Expansion

It is still early stage in terms of exploration…

Expansion of Hushamu Resource

− Deposit open for 300m to southeast for major expansion

− Previously supposed barren zone in poorly drilled southern partdetermined by 2017 infill drilling to have long sections ofmineralization above cut-off grade. If confirmed will convert wastearea to mineralization

Multiple Additional targets for copper-gold porphyrydeposits including:

− Pemberton Hills: 3.5 by 1.5 high-level intense alteration zone withdeepest hole ending in 0.14% copper

− Northwest Expo: 1.5 km open IP anomaly, partially tested with 3holes all in copper – gold mineralization

− Red Dog South: 1.2 by 0.8km high-level porphyry alteration withshallow holes showing increasing copper and gold with depth

TSXV: NCX 15Deposit open to southeast

Hushamu Resource Upside

Cross Section

Deposit

remains open

to the SE

Previously assumed

barren zone, 2017

drilling shows above

cut-off grade between

historical vertical

holes

1. Deposit Expansion to southeast

2. Converting supposed waste to mineralization

TSXV: NCX 16

NW Expo

Pemberton Hills

Red Dog

Deposit

Additional Targets May Add Further Resources

Pemberton Hills and NW Expo

have indications of stand alone

porphyry deposits

TSXV: NCX 17

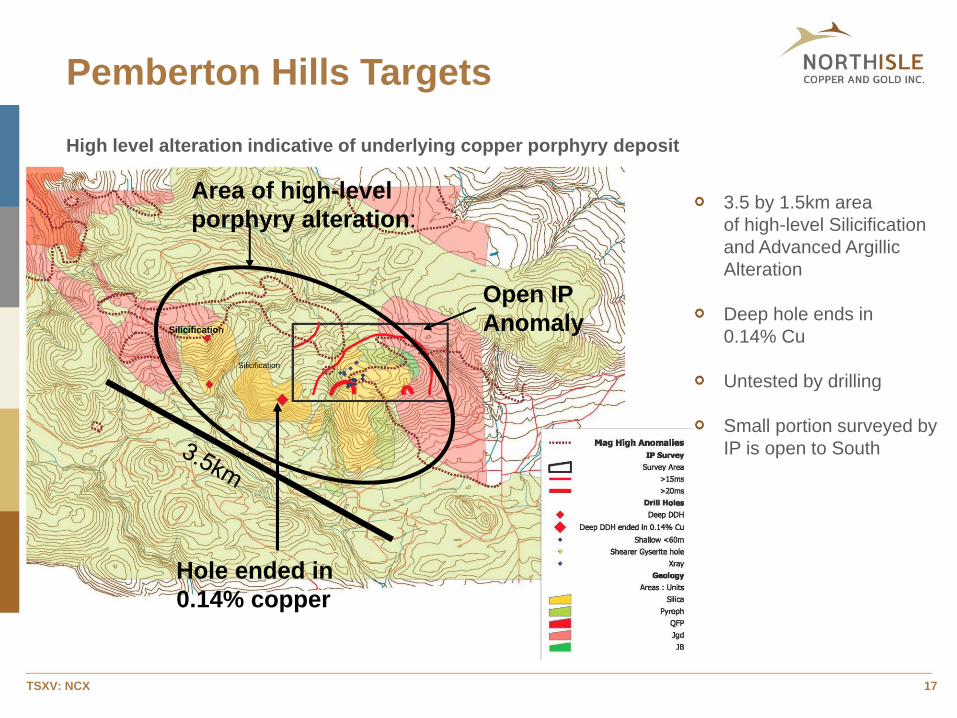

Pemberton Hills Targets

High level alteration indicative of underlying copper porphyry deposit

3.5 by 1.5km area

of high-level Silicification

and Advanced Argillic

Alteration

Deep hole ends in

0.14% Cu

Untested by drilling

Small portion surveyed by

IP is open to South

Silicification

Open IP

Anomaly

Silicification

Area of high-level

porphyry alteration:

Hole ended in

0.14% copper

TSXV: NCX 18

North West Expo Targets

Soil and rock sampling indicates Red Dog zone continues to IP anomaly

Historical Red

Dog Resource(open to NW)

Hole

abandoned in

Overburden

Untested IP

Anomaly >15mv/v

0.12%Cu &

0.09gpt Au / 176m

Mineralized drill

hole

Non mineralized or

abandoned hole

0.16% Cu & 0.14gpt Au / 61m

Scale2 Km0 Km

Slide

Zone

TSXV: NCX 19

Red Dog South Target

Current

Resource

High Level

Alteration

Indicates Buried

Deposit at Depth

Red Dog Alteration Map

TSXV: NCX 20

Cautionary Disclaimer Regarding Forward-Looking Statements and Information

Certain of the statements and information in this press release constitute “forward-looking statements” within the

meaning of the United States Private Securities Litigation Reform Act of 1995 and “forward-looking information”

within the meaning of applicable Canadian securities laws. Forward-looking statements and information generally

express predictions, expectations, beliefs, plans, projections, or assumptions of future events or performance and do

not constitute historical fact. Forward-looking statements and information tend to include words such as “may,”

“expects,” “anticipates,” “believes,” “targets,” “forecasts,” “schedules,” “goals,” “budgets,” or similar terminology.

Forward-looking statements and information herein include, but are not limited to, statements with respect to the

completion of the Proposed Arrangement and the expected structure thereof; anticipated shareholder, court and

regulatory approvals; and the expected timing of closing of the Arrangement. All forward-looking statements and

information are based on NorthIsle’s or its consultants' current beliefs as well as various assumptions made by and

information currently available to them. These assumptions include, without limitation that shareholder and court

approvals to the Proposed Arrangement will be obtained in a timely manner, and that regulatory approvals will be

available on acceptable terms. Although management considers these assumptions to be reasonable based on

information currently available to it, they may prove to be incorrect. Forward-looking statements and information are

inherently subject to significant business, economic, and competitive uncertainties and contingencies and are

subject to important risk factors and uncertainties, both known and unknown, that are beyond NorthIsle’s ability to

control or predict. Actual results and future events could differ materially from those anticipated in forward-looking

statements and information. Examples of potential risks are set forth in Northisle's annual report most recently filed

with the U.S. Securities and Exchange Commission and the Canadian Securities Administrators as of the date of

this press release. Accordingly, readers should not place undue reliance on forward-looking statements or

information. NorthIsle expressly disclaims any intention or obligation to update or revise any forward-looking

statements and information whether as a result of new information, future events or otherwise, except as otherwise

required by applicable securities legislation.

John McClintock, P Eng. is the Qualified person responsible for the technical content of this presentation

TSXV: NCX 21

Combined Hushamu and Red Dog Resource

TOTAL INDICATED CONTAINED METAL

Cut-off

(%Cu) Tonnes %Cu ppm Au %Mo ppm Re Copper B lbs Gold M oz Mo M lbs Re Kgx1000

0.15 341,600,000 0.24 0.30 0.008 0.482 1.83 3.3 67.3 164.7

TOTAL INFERRED CONTAINED METAL

Cut-off

(%Cu) Tonnes %Cu ppm Au %Mo ppm Re Copper B lbs Gold M oz Mo M lbs Re Kgx1000

0.15 147,700,000 0.18 0.23 0.006 0.34 0.59 1.1 19.5 49.9

Indicated Resourceo Copper: 1.83 Billion lb

o Gold: 3.3 Million oz

o Molybdenum: 67.3 Million lb

TSXV: NCX 22

www.northisle.ca

T: 604-638-2515

F: 604-669-2926

15th Floor – 1040 West Georgia Street

Vancouver, BC V6E 4H1