a case study in value destruction: eastman kodak ...adamodar/podcasts/cfspr17/session3.pdf · a...

TRANSCRIPT

Acasestudyinvaluedestruction:EastmanKodak&SterlingDrugs

Kodakentersbiddingwar¨ Inlate1987,EastmanKodak

enteredintoabiddingwarwithHoffmanLaRocheforSterlingDrugs,apharmaceuticalcompany.

¨ ThebiddingwarstartedwithSterlingDrugstradingatabout$40/share.

¨ At$72/share,Hoffmandroppedoutofthebiddingwar,butKodakkeptbidding.

¨ At$89.50/share,Kodakwonandclaimedpotentialsynergiesexplainedthepremium.

Kodakwins!!!!

!

21

EarningsandRevenuesatSterlingDrugs

AswathDamodaran

21

Sterling Drug under Eastman Kodak: Where is the synergy?

0500

1,0001,5002,0002,5003,0003,5004,0004,5005,000

1988 1989 1990 1991 1992

Revenue Operating Earnings

22

KodakSaysDrugUnitIsNotforSale…but…

AswathDamodaran

22

¨ AnarticleintheNYTimesinAugustof1993suggestedthatKodakwaseagertosheditsdrugunit.¤ Inresponse,EastmanKodakofficialssaytheyhavenoplanstosellKodak’sSterlingWinthrop

drugunit.¤ LouisMattis,ChairmanofSterlingWinthrop,dismissedtherumorsas“massivespeculation,

whichfliesinthefaceofthestatedintentofKodakthatitiscommittedtobeinthehealthbusiness.”

¨ Afewmonthslater…Takingastrideoutofthedrugbusiness,EastmanKodaksaidthattheSanofiGroup,aFrenchpharmaceuticalcompany,agreedtobuytheprescriptiondrugbusinessofSterlingWinthropfor$1.68billion.¤ SharesofEastmanKodakrose75centsyesterday,closingat$47.50ontheNewYorkStock

Exchange.¤ SamuelD.Isalyananalyst,saidtheannouncementwas“verygoodforSanofiandverygood

forKodak.”¤ “Whenthedivestituresarecomplete,Kodakwillbeentirelyfocusedonimaging,” saidGeorge

M.C.Fisher,thecompany'schiefexecutive.¤ TherestoftheSterlingWinthropwassoldtoSmithklinefor$2.9billion.

23

Theconnectiontocorporategovernance:HPbuysAutonomy…andexplainsthepremium

AswathDamodaran

23

24

Ayearlater…HPadmitsamistake…andexplainsit…

AswathDamodaran

24

25

ApplicationTest:Whoowns/runsyourfirm?

AswathDamodaran

25

¨ Lookat:BloombergprintoutHDSforyourfirm¨ Whoarethetopstockholdersinyourfirm?¨ Whatarethepotentialconflictsofintereststhatyousee

emergingfromthisstockholdingstructure?

Control of the firm

Outside stockholders- Size of holding- Active or Passive?- Short or Long term?

Inside stockholders% of stock heldVoting and non-voting sharesControl structure

Managers- Length of tenure- Links to insiders

Government

Employees Lenders

26

Case1:SplinteringofStockholdersDisney’stopstockholdersin2003

Aswath Damodaran

27

Case2:VotingversusNon-votingShares&GoldenShares:Vale

Vale Equity

Common (voting) shares3,172 million

Preferred (non-voting)1,933 million

Golden (veto) shares owned

by Brazilian govt

Valespar(54%(Non/Brazilian(

(ADR&Bovespa)(29%(

Brazilian(Ins=tu=onal(6%(

Brazilian(retail(5%( Brazilian(

Govt.(6%(

Valespar(1%(

Non.Brazilian((ADR&Bovespa)(

59%(

Brazilian(Ins<tu<onal(18%(

Brazilian(retail(18%(

Brazilian(Govt.(4%(

Litel&Participaço 49.00%Eletron&S.A. 0.03%Bradespar&S.A. 21.21%Mitsui&&&Co. 18.24%BNDESPAR 11.51%

Valespar(ownership

Vale has eleven members on its board of directors, ten of whom were nominated by Valepar and the board was chaired by Don Conrado, the CEO of Valepar.

Aswath Damodaran

28

Case3:CrossandPyramidHoldingsTataMotor’stopstockholdersin2013

Aswath Damodaran

29

Case4:LegalrightsandCorporateStructures:Baidu¨ TheBoard:Thecompanyhassixdirectors,oneofwhomisRobinLi,

whoisthefounder/CEOofBaidu.Mr.LialsoownsamajoritystakeofClassBshares,whichhavetentimesthevotingrightsofClassAshares,grantinghimeffectivecontrolofthecompany.

¨ Thestructure:BaiduisaChinesecompany,butitisincorporatedintheCaymanIslands,itsprimarystocklistingisontheNASDAQandthelistedcompanyisstructuredasashellcompany,togetaroundChinesegovernmentrestrictionsofforeigninvestorsholdingsharesinChinesecorporations.

¨ Thelegalsystem:Baidu’soperatingcounterpartinChinaisstructuredasaVariableInterestEntity(VIE),anditisunclearhowmuchlegalpowertheshareholdersintheshellcompanyhavetoenforcechangesattheVIE.

Aswath Damodaran

30

Thingschange..Disney’stopstockholdersin2009

AswathDamodaran

30

31

II.Stockholders'objectivesvs.Bondholders'objectives

AswathDamodaran

31

¨ Intheory:thereisnoconflictofinterestsbetweenstockholdersandbondholders.

¨ Inpractice:Stockholderandbondholdershavedifferentobjectives.Bondholdersareconcernedmostaboutsafetyandensuringthattheygetpaidtheirclaims.Stockholdersaremorelikelytothinkaboutupsidepotential

32

Examplesoftheconflict..

AswathDamodaran

32

¨ Adividend/buybacksurge:Whenfirmspaycashoutasdividends,lenderstothefirmarehurtandstockholdersmaybehelped.Thisisbecausethefirmbecomesriskierwithoutthecash.

¨ Riskshifting:Whenafirmtakesriskierprojectsthanthoseagreedtoattheoutset,lendersarehurt.Lendersbaseinterestratesontheirperceptionsofhowriskyafirm’sinvestmentsare.Ifstockholdersthentakeonriskierinvestments,lenderswillbehurt.

¨ Borrowingmoreonthesameassets:Iflendersdonotprotectthemselves,afirmcanborrowmoremoneyandmakeallexistinglendersworseoff.

33

AnExtremeExample:UnprotectedLenders?

AswathDamodaran

33

34

III.FirmsandFinancialMarkets

AswathDamodaran

34

¨ Intheory:Financialmarketsareefficient.Managersconveyinformationhonestlyandandinatimelymannertofinancialmarkets,andfinancialmarketsmakereasonedjudgmentsoftheeffectsofthisinformationon'truevalue'.Asaconsequence-¤ Acompanythatinvestsingoodlongtermprojectswillberewarded.

¤ Shorttermaccountinggimmickswillnotleadtoincreasesinmarketvalue.

¤ Stockpriceperformanceisagoodmeasureofcompanyperformance.

¨ Inpractice:Therearesomeholesinthe'EfficientMarkets'assumption.

35

Managerscontrolthereleaseofinformationtothegeneralpublic

AswathDamodaran

35

¨ Informationmanagement(timingandspin):Information(especiallynegative)issometimessuppressedordelayedbymanagersseekingabettertimetoreleaseit.Whentheinformationisreleased,firmsfindwaysto“spin”or“frame”ittoputthemselvesinthebestpossiblelight.

¨ Outrightfraud:Insomecases,firmsreleaseintentionallymisleadinginformationabouttheircurrentconditionsandfutureprospectstofinancialmarkets.

36

Evidencethatmanagersdelaybadnews?

AswathDamodaran

36

DO MANAGERS DELAY BAD NEWS?: EPS and DPS Changes- byWeekday

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

Monday Tuesday Wednesday Thursday F r i d a y

% Chg(EPS) % Chg(DPS)

37

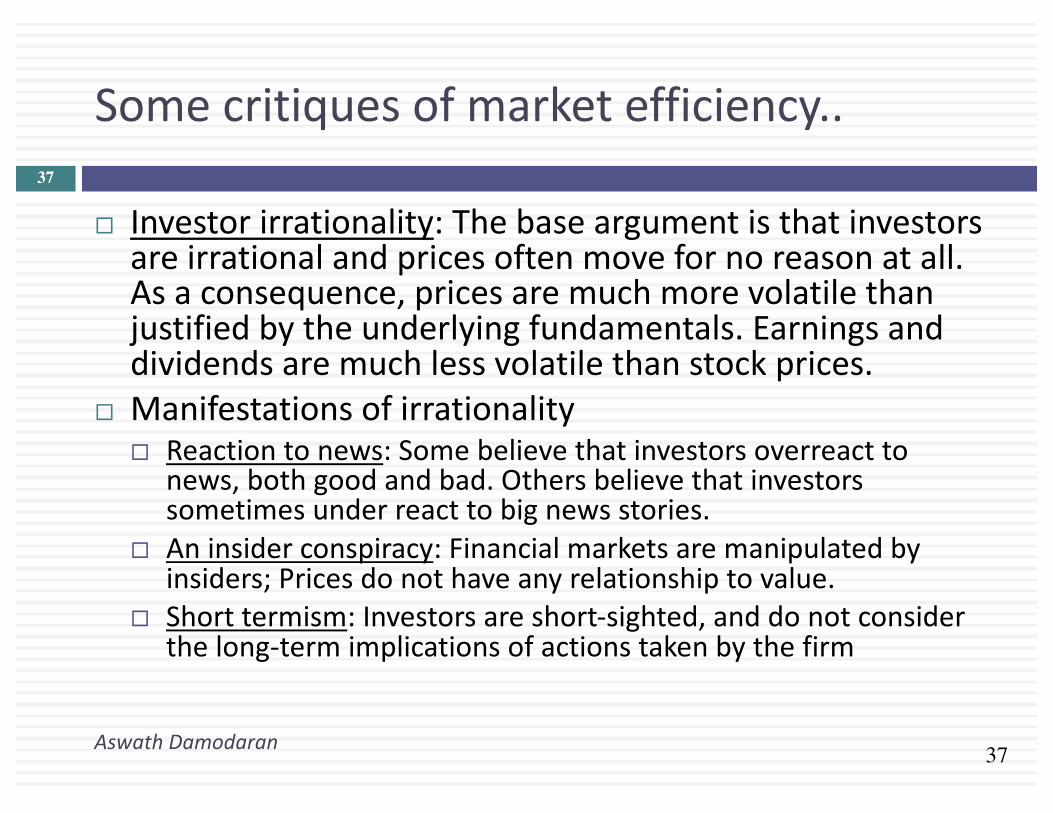

Somecritiquesofmarketefficiency..

AswathDamodaran

37

¨ Investorirrationality:Thebaseargumentisthatinvestorsareirrationalandpricesoftenmovefornoreasonatall.Asaconsequence,pricesaremuchmorevolatilethanjustifiedbytheunderlyingfundamentals.Earningsanddividendsaremuchlessvolatilethanstockprices.

¨ Manifestationsofirrationality¨ Reactiontonews:Somebelievethatinvestorsoverreactto

news,bothgoodandbad.Othersbelievethatinvestorssometimesunderreacttobignewsstories.

¨ Aninsiderconspiracy: Financialmarketsaremanipulatedbyinsiders;Pricesdonothaveanyrelationshiptovalue.

¨ Shorttermism:Investorsareshort-sighted,anddonotconsiderthelong-termimplicationsofactionstakenbythefirm

38

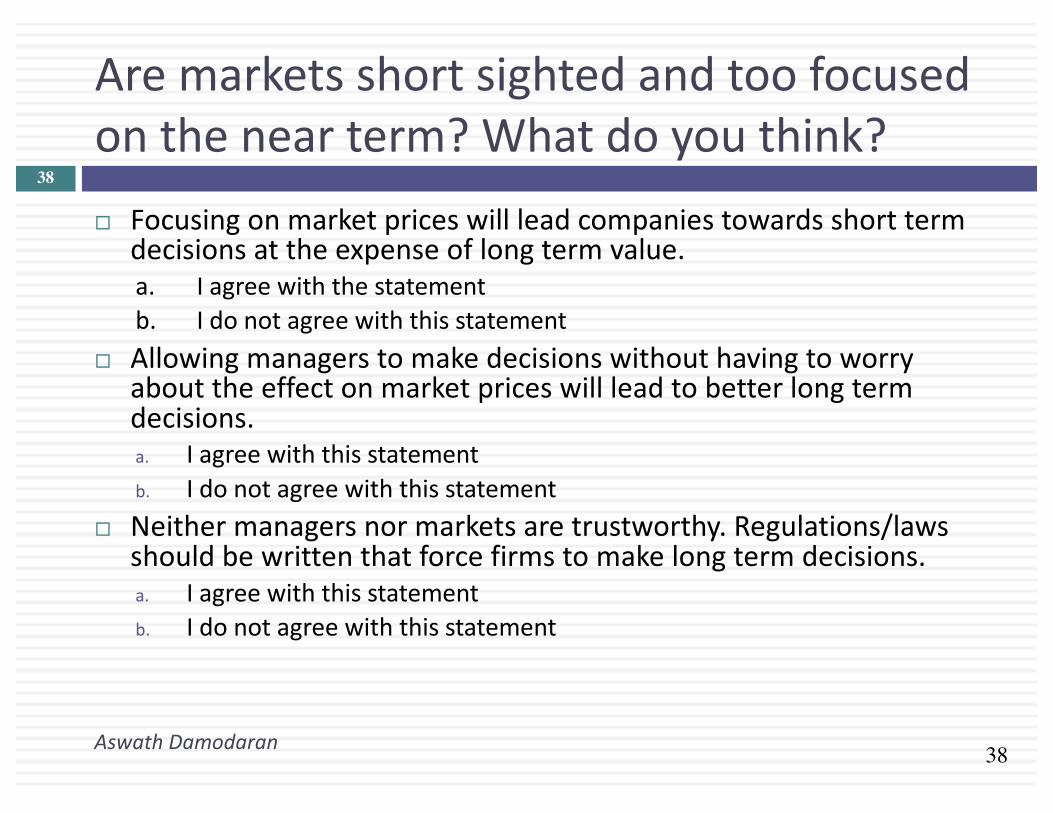

Aremarketsshortsightedandtoofocusedonthenearterm?Whatdoyouthink?

AswathDamodaran

38

¨ Focusingonmarketpriceswillleadcompaniestowardsshorttermdecisionsattheexpenseoflongtermvalue.a. Iagreewiththestatementb. Idonotagreewiththisstatement

¨ Allowingmanagerstomakedecisionswithouthavingtoworryabouttheeffectonmarketpriceswillleadtobetterlongtermdecisions.a. Iagreewiththisstatementb. Idonotagreewiththisstatement

¨ Neithermanagersnormarketsaretrustworthy.Regulations/lawsshouldbewrittenthatforcefirmstomakelongtermdecisions.a. Iagreewiththisstatementb. Idonotagreewiththisstatement

39

Aremarketsshortterm?Someevidencethattheyarenot..

AswathDamodaran

39

¨ Valueofyoungfirms:Therearehundredsofstart-upandsmallfirms,withnoearningsexpectedinthenearfuture,thatraisemoneyonfinancialmarkets.Whywouldamyopicmarketthatcaresonlyaboutshorttermearningsattachhighpricestothesefirms?

¨ Currentearningsvs Futuregrowth:Iftheevidencesuggestsanything,itisthatmarketsdonotvaluecurrentearningsandcashflowsenoughandvaluefutureearningsandcashflowstoomuch.Afterall,studiessuggestthatlowPEstocksareunderpricedrelativetohighPEstocks

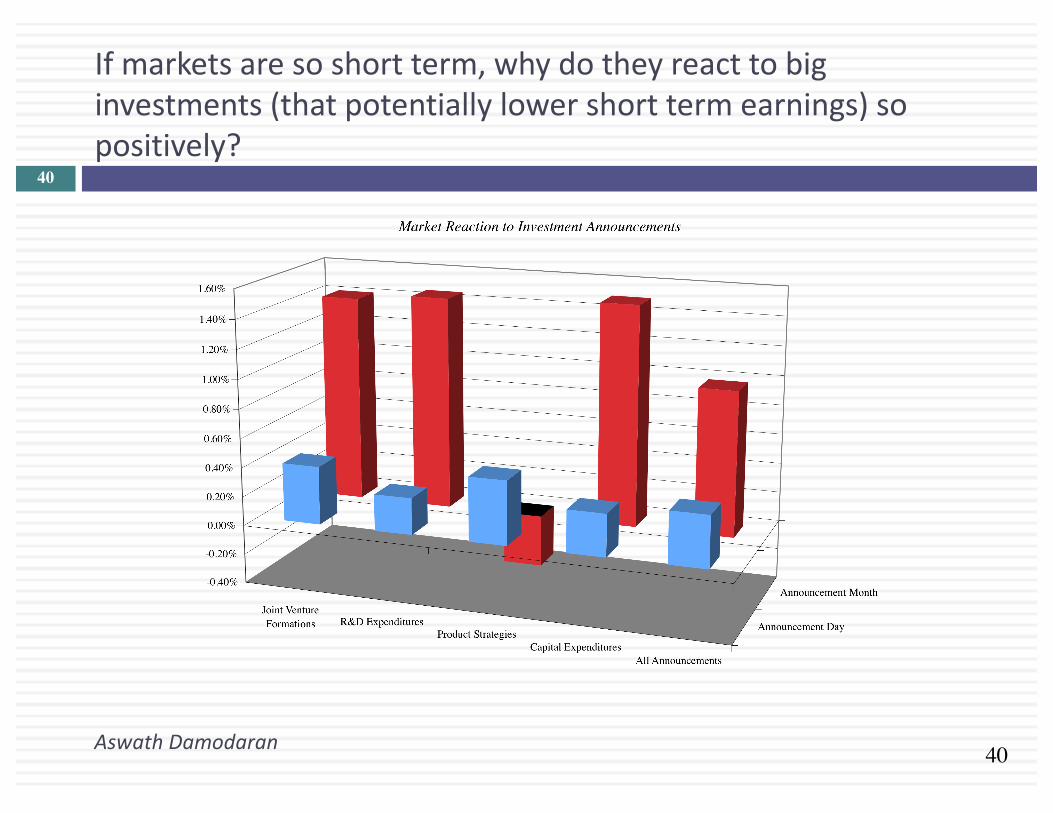

¨ Marketreactiontoinvestments:Themarketresponsetoresearchanddevelopmentandinvestmentexpendituresisgenerallypositive.

40

Ifmarketsaresoshortterm,whydotheyreacttobiginvestments(thatpotentiallylowershorttermearnings)sopositively?

AswathDamodaran

40

41

Butwhataboutmarketcrises?

AswathDamodaran

41

¨ Marketsaretheproblem:Manycriticsofmarketspointtomarketbubblesandcrisesasevidencethatmarketsdonotwork.Forinstance,themarketturmoilbetweenSeptemberandDecember2008ispointedtoasbackingforthestatementthatfreemarketsarethesourceoftheproblemandnotthesolution.

¨ Thecounter:Therearetwocounterargumentsthatcanbeoffered:¤ Theeventsofthelastquarterof2008illustratethatwearemore

dependentonfunctioning,liquidmarkets,withrisktakinginvestors,thaneverbeforeinhistory.Aswesaw,nogovernmentorotherentity(bank,Buffett)isbigenoughtostepinandsavetheday.

¤ Thefirmsthatcausedthemarketcollapse(banks,investmentbanks)wereamongthemostregulatedbusinessesinthemarketplace.Ifanything,theirfailurescanbetracedtotheirattemptstotakeadvantageofregulatoryloopholes(badlydesignedinsuranceprograms…capitalmeasurementsthatmissriskyassets,especiallyderivatives)

42

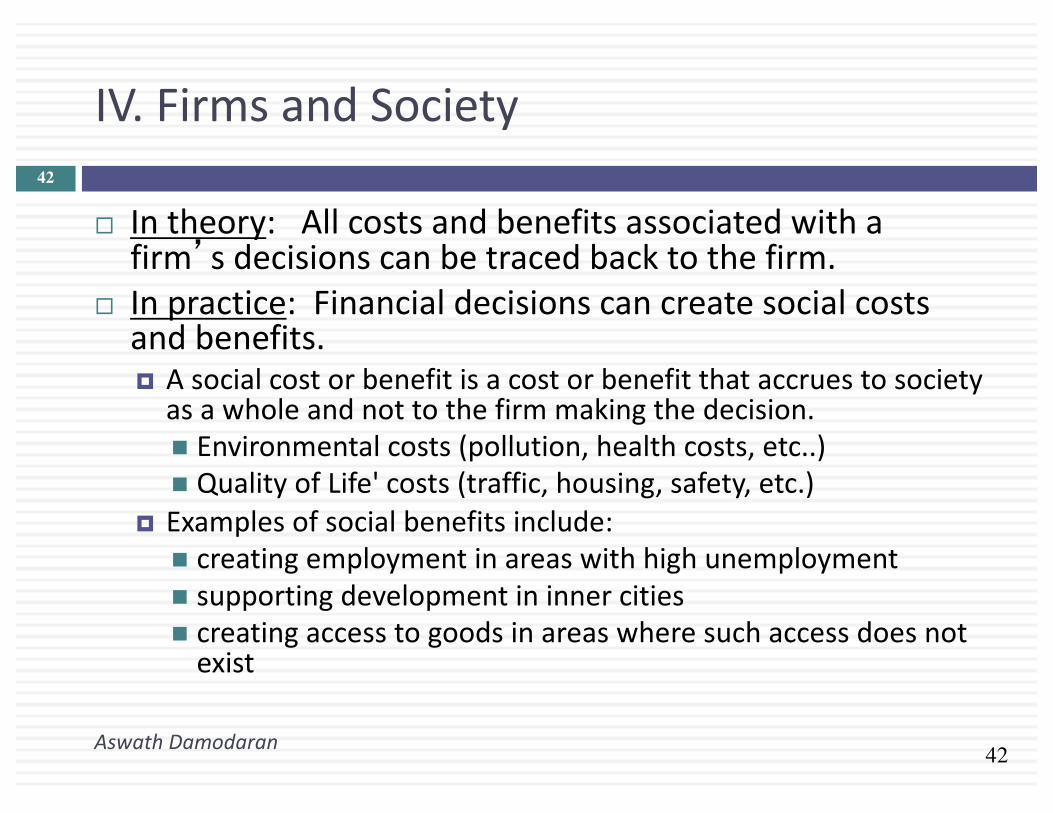

IV.FirmsandSociety

AswathDamodaran

42

¨ Intheory:Allcostsandbenefitsassociatedwithafirm’sdecisionscanbetracedbacktothefirm.

¨ Inpractice:Financialdecisionscancreatesocialcostsandbenefits.¤ Asocialcostorbenefitisacostorbenefitthataccruestosocietyasawholeandnottothefirmmakingthedecision.n Environmentalcosts(pollution,healthcosts,etc..)n QualityofLife'costs(traffic,housing,safety,etc.)

¤ Examplesofsocialbenefitsinclude:n creatingemploymentinareaswithhighunemploymentn supportingdevelopmentininnercitiesn creatingaccesstogoodsinareaswheresuchaccessdoesnotexist

43

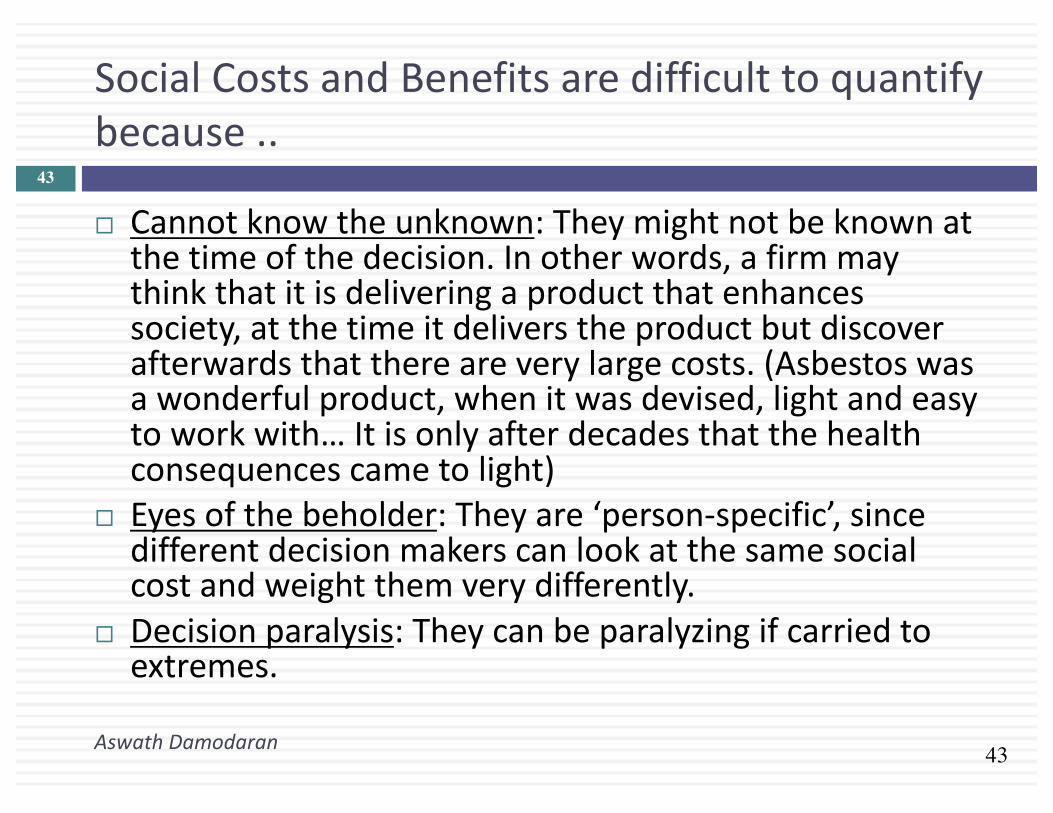

SocialCostsandBenefitsaredifficulttoquantifybecause..

AswathDamodaran

43

¨ Cannotknowtheunknown:Theymightnotbeknownatthetimeofthedecision.Inotherwords,afirmmaythinkthatitisdeliveringaproductthatenhancessociety,atthetimeitdeliverstheproductbutdiscoverafterwardsthatthereareverylargecosts.(Asbestoswasawonderfulproduct,whenitwasdevised,lightandeasytoworkwith…Itisonlyafterdecadesthatthehealthconsequencescametolight)

¨ Eyesofthebeholder:Theyare‘person-specific’,sincedifferentdecisionmakerscanlookatthesamesocialcostandweightthemverydifferently.

¨ Decisionparalysis:Theycanbeparalyzingifcarriedtoextremes.

44

Atestofyoursocialconsciousness:Putyourmoneywhereyoumouthis…

AswathDamodaran

44

¨ AssumethatyouworkforDisneyandthatyouhaveanopportunitytoopenastoreinaninner-cityneighborhood.Thestoreisexpectedtoloseaboutamilliondollarsayear,butitwillcreatemuch-neededemploymentinthearea,andmayhelprevitalizeit.

¨ Wouldyouopenthestore?¤ Yes¤ No

¨ Ifyes,wouldyoutellyourstockholdersandletthemvoteontheissue?¤ Yes¤ No

¨ Ifno,howwouldyourespondtoastockholderqueryonwhyyouwerenotlivinguptoyoursocialresponsibilities?