8 deem er 2010 • palem ang - peter cockcroft...... (jambi, central palembang and south palembang...

TRANSCRIPT

CBM in South Sumatra8 DECEMBER 2010 • PALEMBANG

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 1

The presentation may contain forward-looking statements and estimates regarding the intentions of the Company, and these will be affected by movements in share markets, commodity prices, technical variabilities and many other factors beyond the control of Company and its personnel. The presentation must be considered in the light of these estimates and uncertainties and investment in European Gas Limited should be considered as speculative in nature.

Disclaimer

• Geology

• Resources

• CBM Drivers for success

• Indicative Project Economics

Contents

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 2

Geology

DECEMBER 2010 • PALEMBANGSlide 2

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 3

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 4

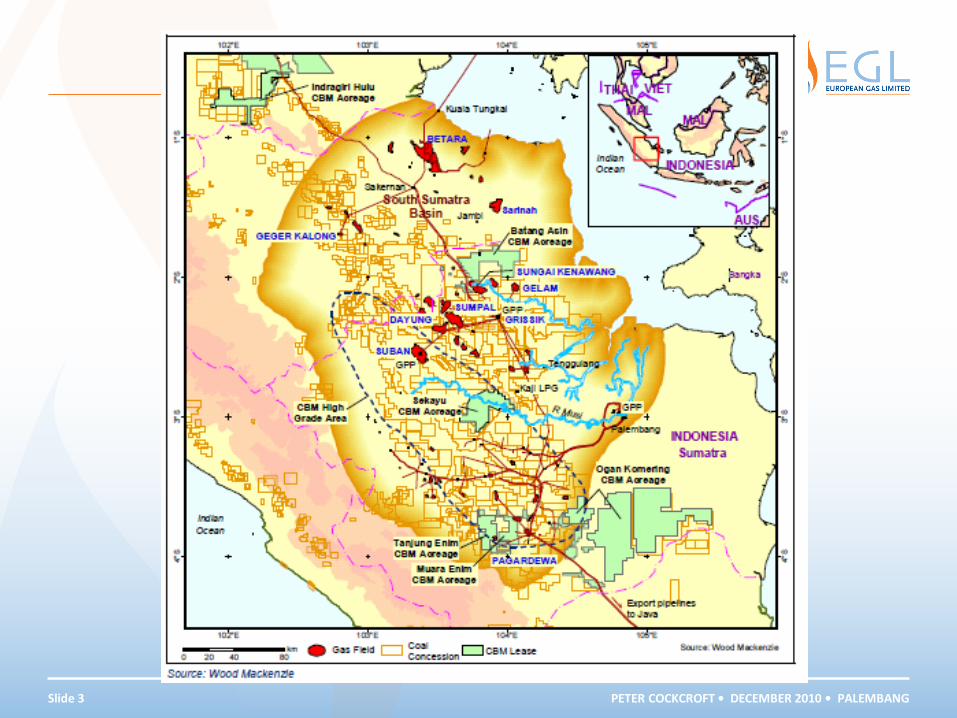

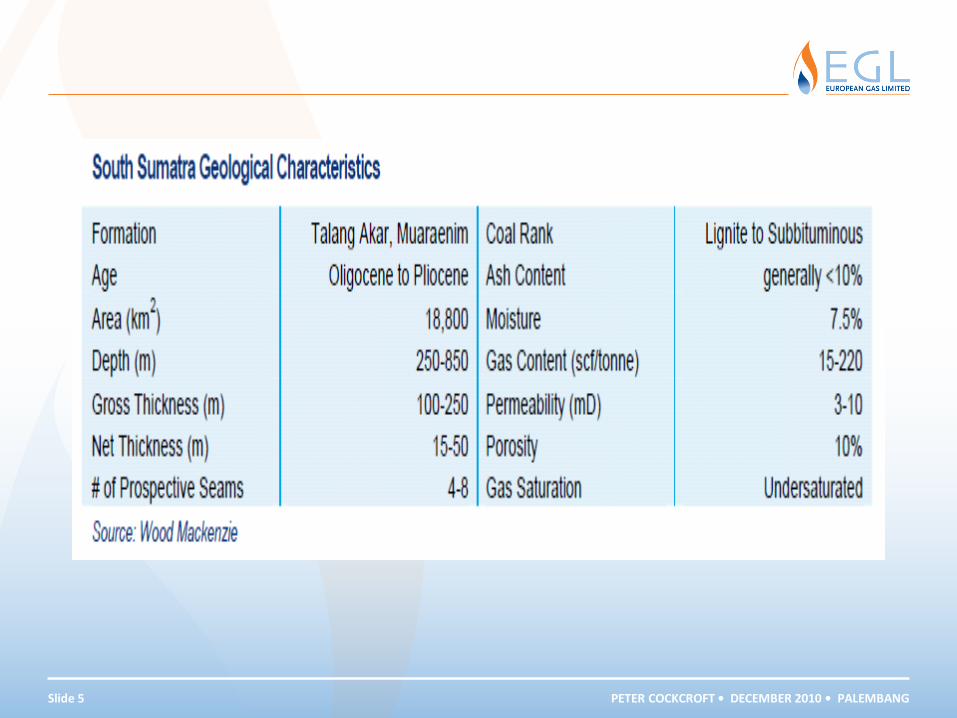

• The South Sumatra coal basin is a large asymmetrical structure, with a number of small to medium sized sub-basins containing coal deposits. The majority of the South Sumatra deposits are low rank, although in one of the small sub-basins higher rank, export quality coal is being mined. In at least one instance, a sub-bituminous deposit increases in rank to semi-anthracite as a result of igneous intrusive activity.

• The basin is sub-divided into a series of fault-controlled sub-basins separated by basement structural highs. The depressions (Jambi, Central Palembang and South Palembang/Lematang) contain the thickest coal sequences at optimal CBM depths. Although coal rank is low, the seams are contiguous over large distances, with deeper seams estimated to have higher ranks due to the high heat gradient of the back arc basin setting.

• Individual prospective seams within South Sumatra have reported thicknesses of up to 17 metres, although a seam thickness of between 5 to 8 metres is closer to the norm throughout the area.

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 5

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 6

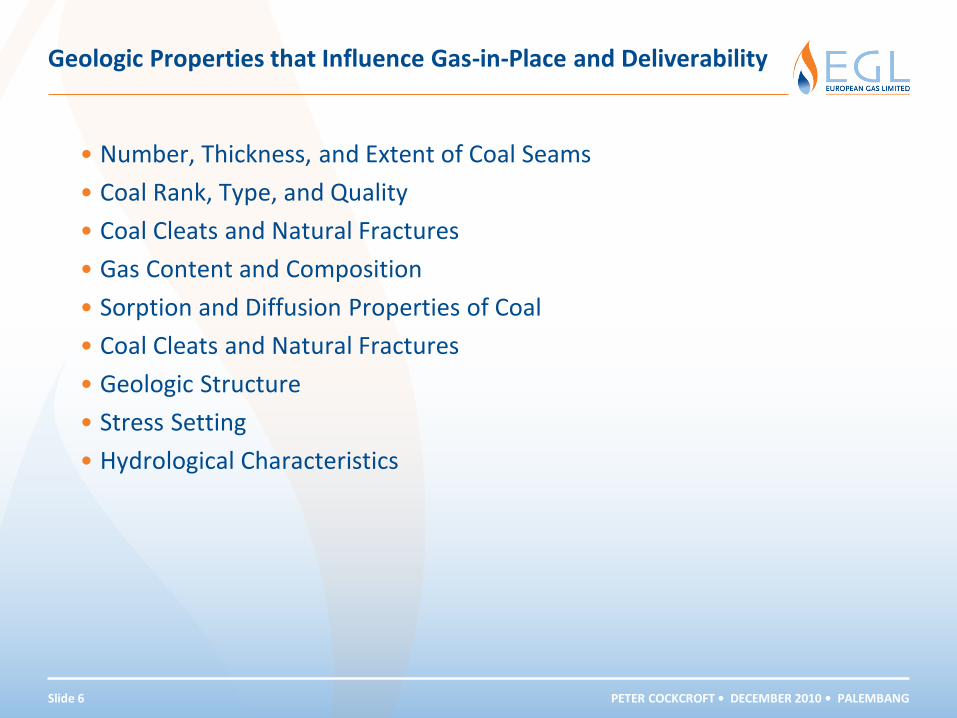

Geologic Properties that Influence Gas-in-Place and Deliverability

• Number, Thickness, and Extent of Coal Seams

• Coal Rank, Type, and Quality

• Coal Cleats and Natural Fractures

• Gas Content and Composition

• Sorption and Diffusion Properties of Coal

• Coal Cleats and Natural Fractures

• Geologic Structure

• Stress Setting

• Hydrological Characteristics

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 7

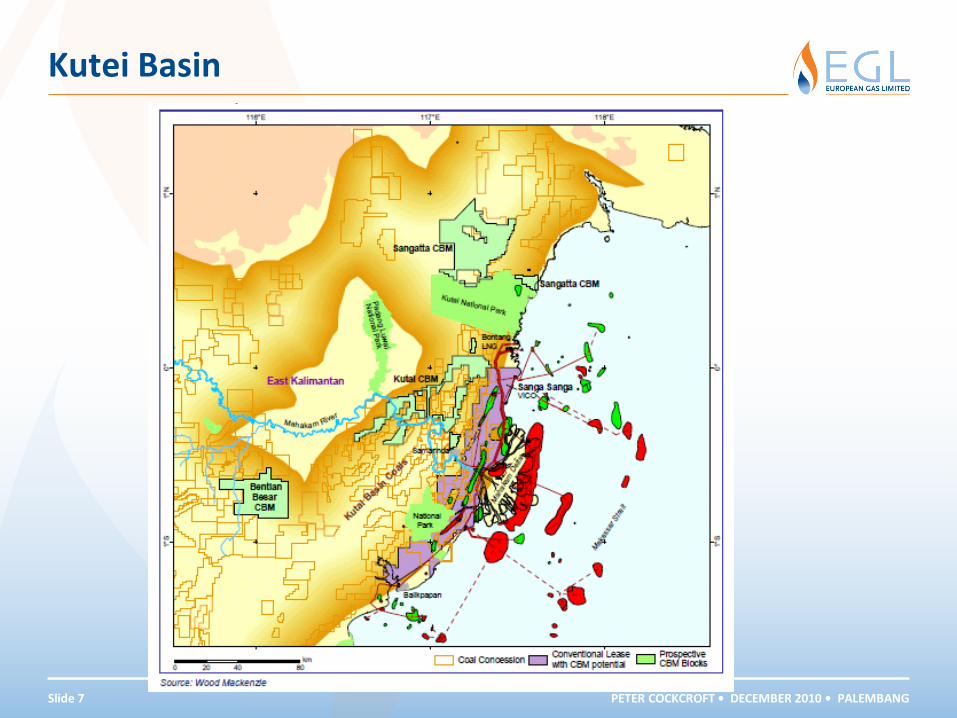

Kutei Basin

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 8

Resources

DECEMBER 2010 • PALEMBANGSlide 2

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 9

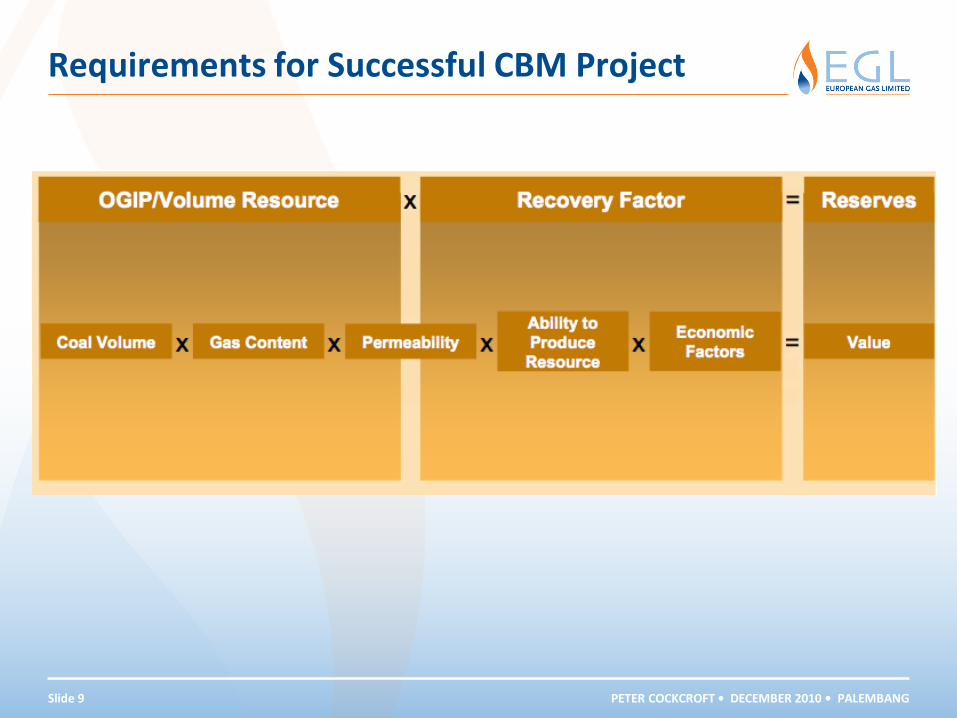

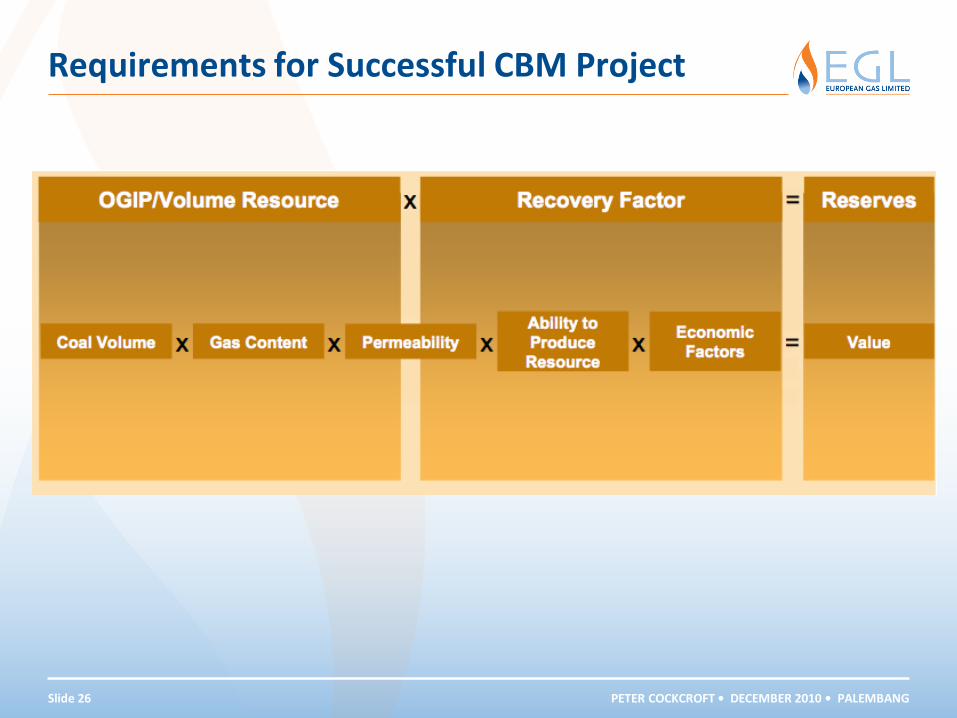

Requirements for Successful CBM Project

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 10

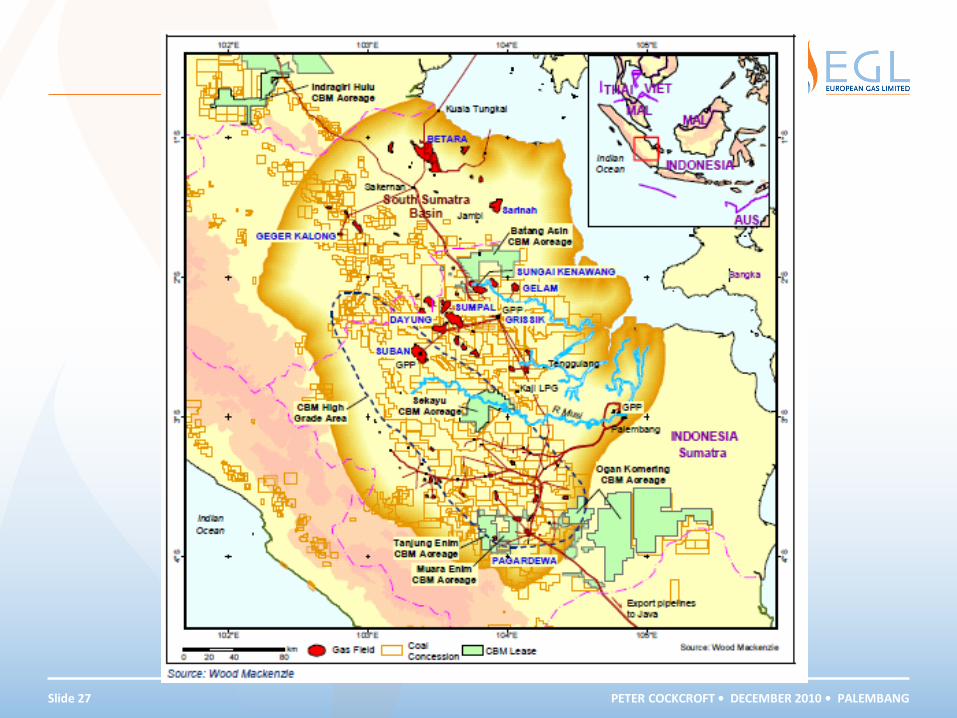

• The GOI estimates the country’s CBM resource base at 453 tcf, of which 183 tcf (~40%) is reported to be within South Sumatra. Given the uncertainties around the access to both drillable locations and gas market, the portion of this resource that could be categorized as commercial is currently unclear

• Despite land access issues, the resource potential in South Sumatra could be considerable. Based on 160 acre spacing and an EUR per well of 1.2 bcfe, the resource potential could be as high as 24 TCF across the basin. However, until pilot drilling is completed and a better understanding of the coals is ascertained, technically recoverable volumes will remain uncertain

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 11

Assumptions

Resources/Reserves

• The GIIP estimate of 183 tcf was based on various Government presentations identifying the CBM potential in Indonesia.

• Since the basin is still in a pilot testing stage, we have assumed no commercial reserves at this time.

• Wood MacKenzie (October 2010) estimates the play to cover an area of 18,800 square kilometres (7,313 square miles), of which 70% is assumed to be commercially accessible. Additionally, with 160 acre well spacing, this generates 20,477 potential drill locations.

• Based on an average EUR of 1.2 bcfe per well, they estimate the play to have a resource potential of 23.9 tcf with an expected recovery factor of 19%. It is expected that this number will evolve considerably once more definite information on the play extension and deliverability is available.

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 12

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 13

Competitor Review

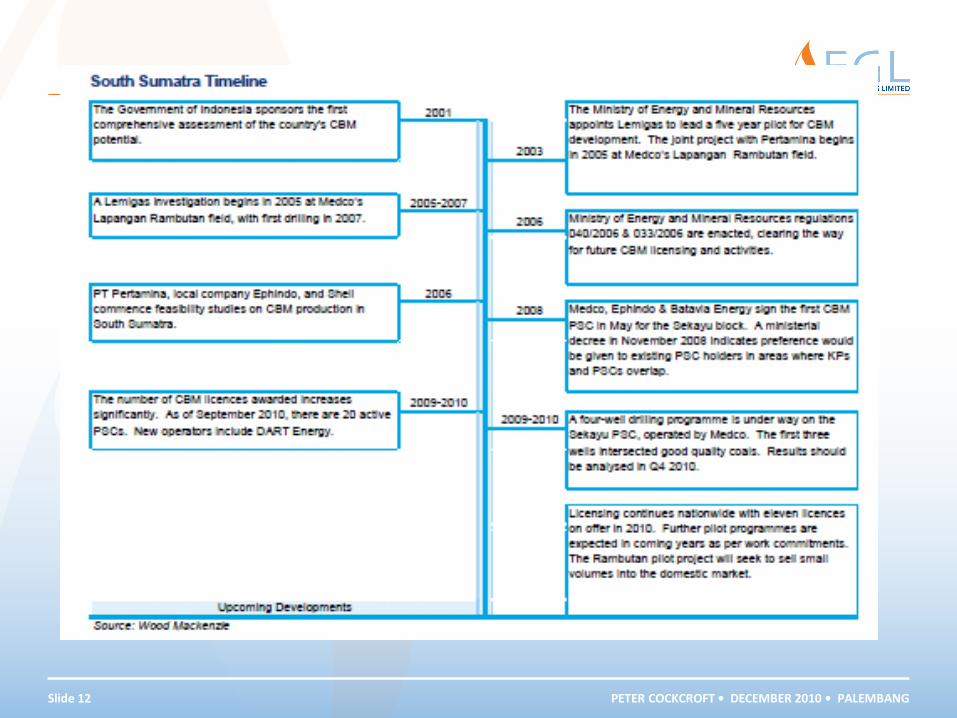

• Even before the official award of CBM licenses, CBM pilot operations were underway in Indonesia. Ephindo and Ilthabi Rekatama have looked at gas content and coal quality across their operations in eight coal licenses . The most advanced CBM project is the Rambutan pilot. In 2004, Medco Energistarted a CBM study on the field, which is located on its conventional South Sumatra PSC. The coals are currently producing gas at higher levels than expected, due to a shorter than anticipated dewatering time. Produced volumes remain very small, but talks are ongoing with the government regarding gas sales to the local market.

• The CBM industry in Indonesia is very much in its infancy, with the first licenses having been awarded in 2008 in Sumatra and Kalimantan. As at October 2010, six CBM PSCs are operational in South Sumatra, owned by several companies of varying levels of CBM expertise.

• Medco also holds a 50% interest in the Sekayu CBM PSC in South Sumatra, with partner South Sumatra Energy (a company owned by Ephindo, CBM Asia and Batavia). Medco’s conventional PSC and Ephindo’s coal concession overlap and so the two companies are jointly evaluating CBM potential with a three-well drilling programme. The wells are targeting the Palembang and Panagdang coals. Initial testing of core samples indicated gas contents of 75-85 sfc/ton and permeability of 500 millidarcies. Indonesian coal producer Ephindo, has built relationships with several larger players, and now has interests in three CBM PSCs across Indonesia.

• One of the most experienced CBM operators in Indonesia is Dart Energy. Dart is the owner of the residual, international assets of Arrow Energy. Dart operates the Tanjung Enim PSC in South Sumatra for partners Pertamina and PT Bukit Asam (Persero), and plans to drill six pilot wells in the PSC area by the end of 2010. Furthermore, Dart and Medco have signed an HoA to explore and develop CBM in Medco’s conventional South Sumatra PSC.

• National Oil Company Pertamina has interests in two CBM PSCs in South Sumatra (Tanjung Enimabove, and Muara Enim), with small Indonesian players holding interests across a number of other PSCs..

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 14

CBM Drivers for Success

DECEMBER 2010 • PALEMBANGSlide 2

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 15

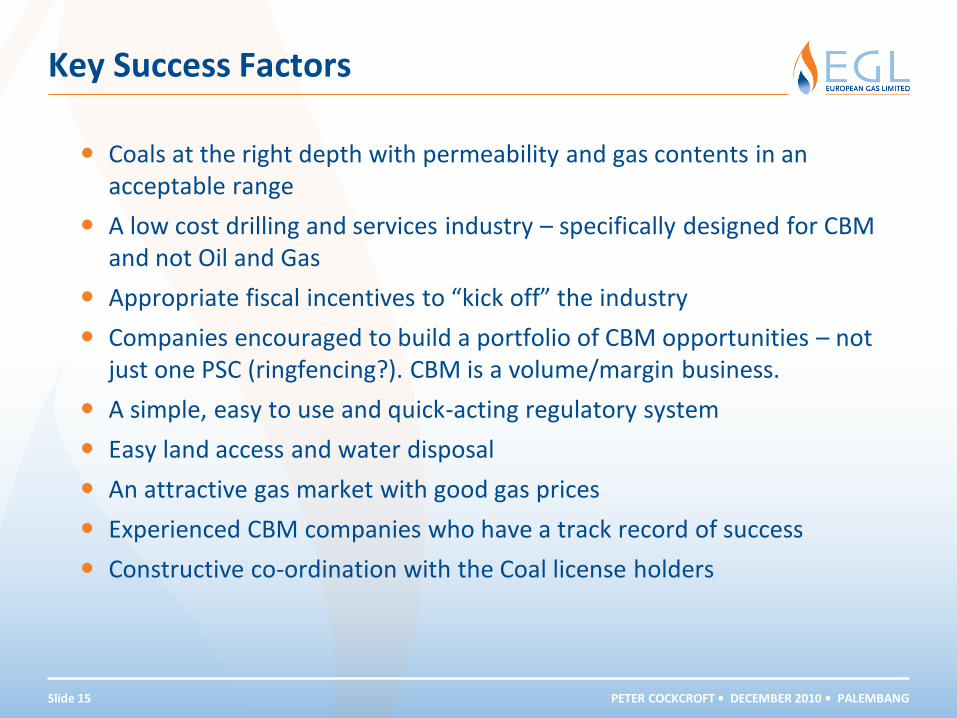

Key Success Factors

Coals at the right depth with permeability and gas contents in an acceptable range

A low cost drilling and services industry – specifically designed for CBM and not Oil and Gas

Appropriate fiscal incentives to “kick off” the industry

Companies encouraged to build a portfolio of CBM opportunities – not just one PSC (ringfencing?). CBM is a volume/margin business.

A simple, easy to use and quick-acting regulatory system

Easy land access and water disposal

An attractive gas market with good gas prices

Experienced CBM companies who have a track record of success

Constructive co-ordination with the Coal license holders

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 16

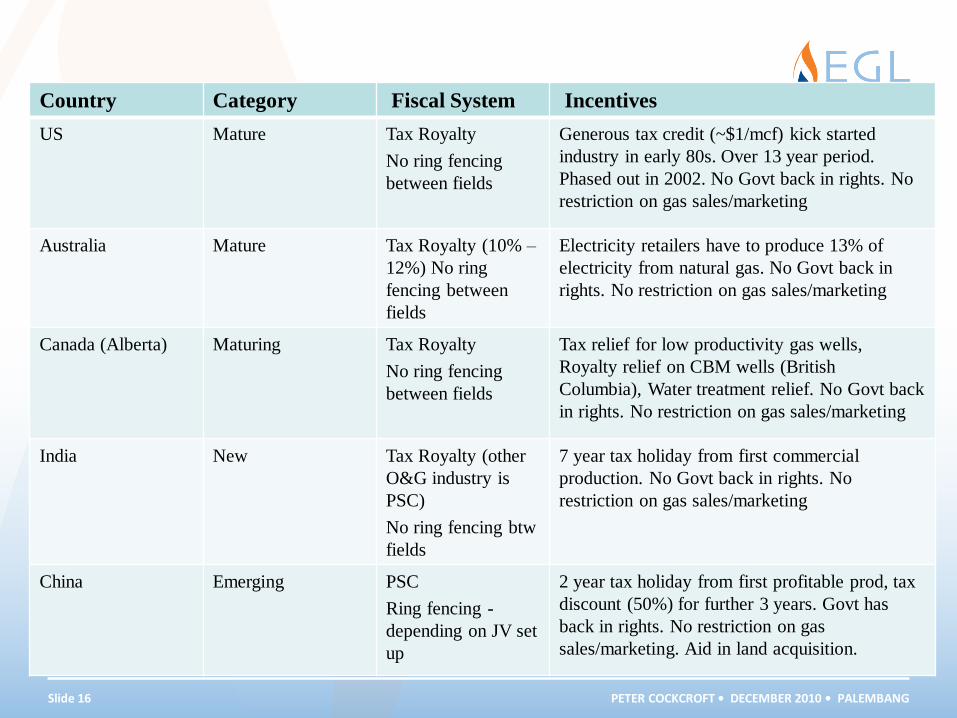

CBM COUNTRIES – FISCAL AND INCENTIVES

Country Category Fiscal System Incentives

US Mature Tax Royalty

No ring fencing

between fields

Generous tax credit (~$1/mcf) kick started

industry in early 80s. Over 13 year period.

Phased out in 2002. No Govt back in rights. No

restriction on gas sales/marketing

Australia Mature Tax Royalty (10% –

12%) No ring

fencing between

fields

Electricity retailers have to produce 13% of

electricity from natural gas. No Govt back in

rights. No restriction on gas sales/marketing

Canada (Alberta) Maturing Tax Royalty

No ring fencing

between fields

Tax relief for low productivity gas wells,

Royalty relief on CBM wells (British

Columbia), Water treatment relief. No Govt back

in rights. No restriction on gas sales/marketing

India New Tax Royalty (other

O&G industry is

PSC)

No ring fencing btw

fields

7 year tax holiday from first commercial

production. No Govt back in rights. No

restriction on gas sales/marketing

China Emerging PSC

Ring fencing -

depending on JV set

up

2 year tax holiday from first profitable prod, tax

discount (50%) for further 3 years. Govt has

back in rights. No restriction on gas

sales/marketing. Aid in land acquisition.

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 17

Gas Market

• A key hurdle for the future CBM development is competing for market share, particularly given the current surplus of conventional gas in South Sumatra. Even if operators are able to develop economic projects, access to market would remain a significant hurdle.

• The supply surplus in South Sumatra is expected to outstrip demand through the medium-term. The most readily available market would be West Java, which is currently gas-short. There are two South Sumatra to West Java pipelines in operation, but the lines are expected to be fully utilised with contracted volumes. There is potential that sufficient conventional and CBM gas reserves could be proven-up to justify a third SSWJ pipeline. If this new pipeline materialized, the need for Indonesia LNG to meet future gas demand would be removed.

• The Singaporean market would be another option, but it is not expected that any further gas sales from Sumatra to Singapore would be approved by the Indonesian authorities until significant additional gas reserves are proven in South Sumatra. Singapore is also constructing an LNG import terminal, set for completion in 2013, which will reduce its need for pipeline imports.

• The South Sumatra gas price trend for sales to industrial buyers has been positive, rising to over US$5.00/MMBtu and is expected to increase in the future, although a discount to this can be expected for CBM gas until reliable production can be assured. However, if CBM were able to achieve this price, projects would generate positive rates of return.

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 18

Infrastructure

• Overall South Sumatra has a developed gas infrastructure and established local and export gas markets, although local demand is small. Looking farther afield, new export pipelines to the West Java market are almost completely contracted.

• Future development of the Sekayu block will require gas gathering lines, processing and compression in order to get CBM production to surrounding infrastructure. Currently the block has no infrastructure in place.

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 19

Supply Chain

• South Sumatra has seen extensive conventional oil and gas activity, but full-scale CBM developments will require specific services that no company is currently offering in South Sumatra. Having a domestic service base would allow developers to avoid import duties currently in place for drilling and completion equipment.

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 20

Land Access/Permitting

• MIGAS awards CBM PSCs, usually through a tender process. The greatest issue regarding the permitting has been the resolution of rights when there are pre-existing rights on the areas for either oil and gas activities, coal extraction, or both.

• In 2006, the Government adopted a ministerial decree to regulate CBM in Indonesia. This decree stipulated that the Coal Contract of Work holder and the holder of an overlapping oil and gas concession have the first opportunity to make application for an area on an equal basis, and have six months to state their intentions before work areas are classified as open areas for CBM and put out to tender.

• In November 2008, the Government adopted a subsequent decree, which held that in areas where a coal concession and a conventional oil and gas block overlap, participants in the conventional oil and gas PSC are given priority to apply for a direct offer CBM block. The regulatory move appears to have been successful in addressing mineral right issues.

• CBM projects will need support for land clearing requiring coordination with local governments, and operators are calling for new legislation to allow access to land rights for CBM developments. An estimated 5%-30% of land is used for municipality housing and government installations, and therefore off limits for upstream activities.

• Topography in South Sumatra will represent a challenge with large tracts of forested areas and jungle, and swampy or river-prone areas in lower lying areas. Thus far CBM production has not been carried out successfully in a tropical climate.

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 21

Environment/Regulation

• Currently there is no environmental legislation specifically targeting CBM operations, but given the heightened sensitivities to onshore drilling operations following the Banjarpanji mud volcano incident in Java, there are likely to be calls for environmental guarantees from both the public and legislators.

• If a CBM operation is in a pre-existing coal development area, and not involving the coal concessionaire, then the CBM operations are not allowed to make any disturbances to the mining operation. In addition, if CBM activities use a mining facilities, then the CBM operator will be responsible for any maintenance of those facilities.

• There are currently a number of areas for improvement in the legislation relating to CBM operations. It is unclear how conventional gas/oil found in a CBM license will be handled. In addition, the well approval process will have to be streamlined to ensure that applications for hundreds of wells can reviewed efficiently. Currently, significant delays are common in the processing of conventional project applications. The government has recognised that CBM projects will require specific regulations.

• Given the infancy of CBM operations in Indonesia, guidelines for water disposal have yet to be fully defined. Given the humid tropic conditions in Indonesia, evaporation ponds used in North America are probably not a viable solution.

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 22

Fiscal Terms

• One of the initial hurdles to the CBM industry was that the Government and regulators initially treated CBM the same as conventional resources. The government has now recognised the specificities of CBM developments, and has adjusted fiscal terms to encourage investment. The initial CBM PSCs had terms based on conventional oil and gas PSCs, but since March 2010, two PSC options are available to CBM players: the CBM Net PSC and the Gross PSC.

• All CBM PSCs require certain criteria to be met as part of the work commitments of the contract award, including core-hole drilling, and a pilot project to evaluate CBM potential, the dewatering process, and production testing. A signature bonus of US$1.0 million is payable, and work commitment investment for the first three years has ranged from US$1.0 million up to US$40 million. A domestic market obligation of 25% will also be applied to all PSCs, which will have a lifetime of 30 years.

• Under the Gross PSC, the production split between the Contractor and the Government is based on gross production, without any deduction for cost recovery. The Gross PSC also allows for gas to be sold before a Plan of Development (PoD) is approved – which has been a stumbling block for many conventional projects.

• Under the CBM (Net) PSC, First Tranche Petroleum (FTP) is set at 10%, and the contractors pre and post-tax profit split is 80.36% and 45% respectively. Cost recovery is 100% for the first five years, decreasing to 90% thereafter. Approvals for development plans are also required before projects can proceed.

• In contrast, PoD approvals will not be required before commercial production, meaning companies can seek to sell volumes produced under pilot schemes. With uncertainty in recent years over the level of cost recovery, the Gross PSC may prove to be more popular amongst CBM operators. Field “ring-fencing” is unlikely to be an issue, as cost recovery will not be used, and as a result tender processes and construction contracts could be agreed upon more quickly. The Pre-Tax profit split is currently unknown, and will be key to operators’ decisions on which terms to choose. Another benefit of the Gross PSC is the removal of FTP.

• Whilst the Gross PSC appears to offer greater flexibility, the CBM (Net) PSC may provide greater security. Exploration and development costs in the initial projects are likely to be uncertain until better data are obtained of coal thickness and quality.

• The government is thought to be considering further incentives to stimulate CBM activity, particularly looking at offering an exemption on import duties on equipment for exploration work, as well as value added tax breaks.

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 23

Project Economics

DECEMBER 2010 • PALEMBANGSlide 2

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 24

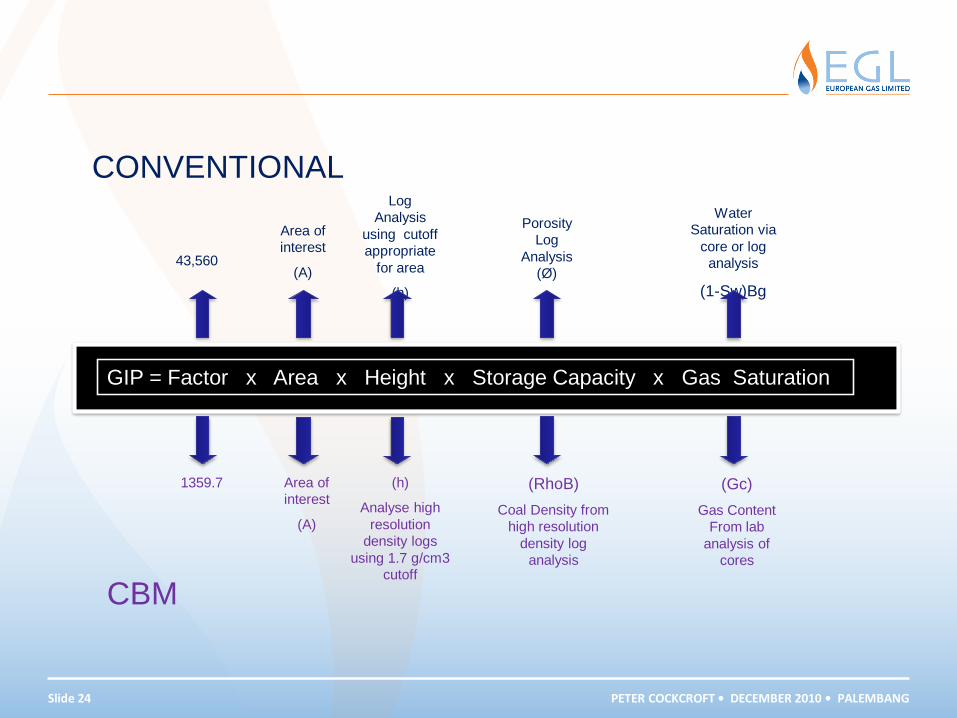

GIP = Factor x Area x Height x Storage Capacity x Gas Saturation

1359.7

43,560

Area of

interest

(A)

Area of

interest

(A)

(h)

Analyse high

resolution

density logs

using 1.7 g/cm3

cutoff

Log

Analysis

using cutoff

appropriate

for area

(h)

(RhoB)

Coal Density from

high resolution

density log

analysis

Porosity

Log

Analysis

(Ø)

(Gc)

Gas Content

From lab

analysis of

cores

Water

Saturation via

core or log

analysis

(1-Sw)Bg

CONVENTIONAL

CBM

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 25

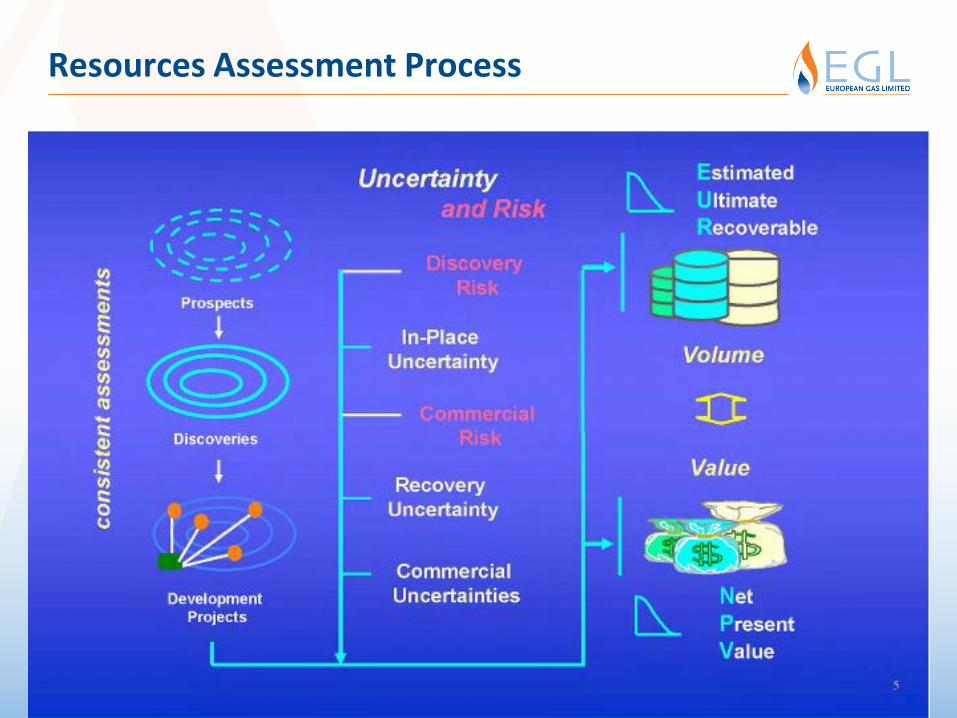

Resources Assessment Process

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 26

Requirements for Successful CBM Project

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 27

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 28

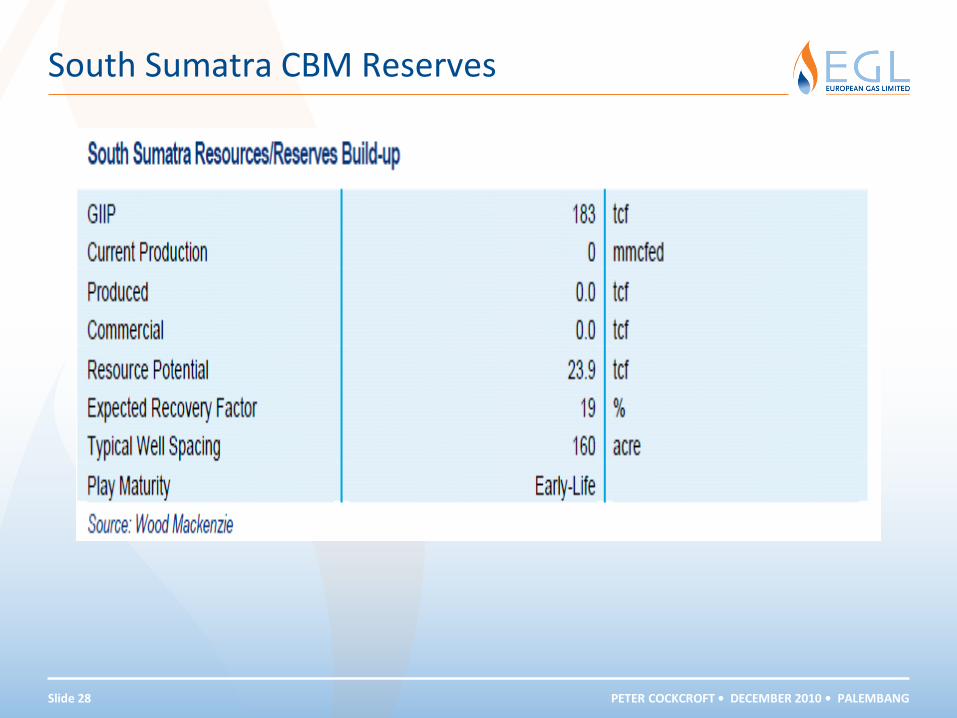

South Sumatra CBM Reserves

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 29

Assumptions

Resources/Reserves

• The GIIP estimate of 183 tcf was based on various Government presentations identifying the CBM potential in Indonesia.

• Since the basin is still in a pilot testing stage, we have assumed no commercial reserves at this time.

• We estimate the play to cover an area of 18,800 square kilometres(7,313 square miles), of which 70% is assumed to be commercially accessible. Additionally, with 160 acre well spacing, this generates 20,477 potential drill locations.

• Based on an average EUR of 1.2 bcfe per well, we estimate the play to have a resource potential of 23.9 tcf with an expected recovery factor of 19%. It is expected that this number will evolve considerably once more definite information on the play extension and deliverability is available.

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 30

Economics/Production Assumptions

• Wells are assumed to cost, on average, US$0.34 million each.

• We assume fracced vertical wells with an EUR of 1.2 bcfe per well and an IP initially of 0.00 mmcfed rising to 0.32 mmcfed after five years when optimum desorption is achieved. Production is then assumed to plateau for approximately two years before declining steadily.

• Spud to sales time has been assumed to be three months.

• Associated liquids production is not assumed.

• For a 500 bcf project development, we assume 428 wells would be required with five rigs drilling on 160-acre spacing.

• Given the fact that South Sumatra is not an established CBM production area, for a 500 bcf project development full-cycle economics, we assume a lead time between leasing and first production of five years, leasing costs of US$4.00 per acre (based on the Sekayu PSC’s US$1 million for 135,830 hectares), no seismic costs, and five pilot wells at an average cost of US$0.7 million each.

• Abandonment costs are included.

• The gas price is in line with average South Sumatra contracts, with a slight discount assumed since CBM is not a proven supply source in Indonesia. Wood Mackenzie has suggested a sales price of US$3.50/mcf in 2011, escalating at 2.0% per annum.

• Economics are modelled under an Indonesian CBM (Net) PSC terms with a 10% FTP (royalty). In addition, we assume a cost recovery ceiling of 100% for the first 5 years and 90% thereafter, 36% Government profit-sharing, and additional taxes of 20%.

• Discount rate is 10% nominal from 1 January 2011 while our long-term inflation assumption is 2.0% per annum from 2011.

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 31

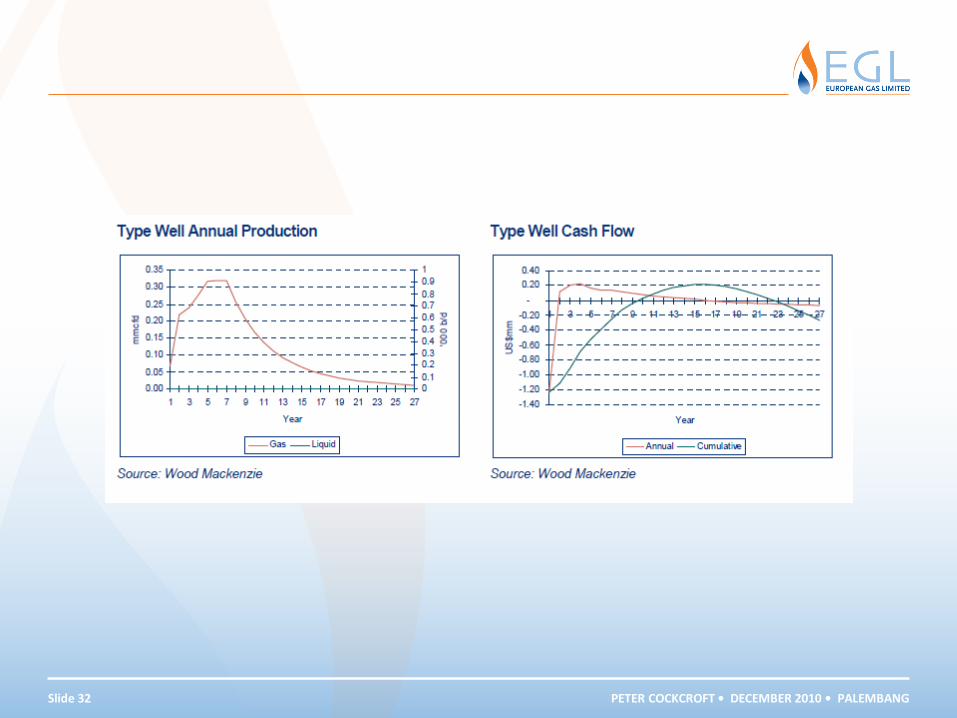

• The model assumes fractured vertical wells, with a well-spacing of 160 acres. Peak production is anticipated five years after initial dewatering at about 0.32 mmcfed.

• An assumed 34 year well life yields an EUR of 1.2 bcfe, although variability in gas content within seams could lead to zones that have significantly lower EURs.

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 32

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 33

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 34

Economics do not look attractive

• Based on this scenario, indicative economics do not look attractive, even with the better fiscal terms offered by the Government. Going forward, commerciality of the South Sumatran coals will depend on access to market, sufficient gas wellhead price and the lateral homogeneity of the coals. Current drilling costs are quite low because the seams are relatively shallow and the wells are simple to complete. However, additional capital costs per well are expected to be high to account for water disposal, pipeline tie-in, processing and land clearance. These costs have been reflected in the Other Capex category noted above.

• Key unknowns in Indonesia, given the early stage of CBM development, are the availability of rigs for extensive drilling and the quality of produced water and approved disposal methods. It has been assumed that rigs are not the limiting factor in this model, and that water can be re-injected into underground aquifers that are not currently used for potable water supplies.

• The gas price could provide considerable upside to this CBM play and will largely depend on the availability of conventional resources to fill the South Sumatra to West Java (SSWJ) pipeline, which is the assumed export route. Gas exports to Singapore could offer pricing upside, but are contingent on the GOI’s appetite to negotiate future exports.

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 35

… OR SHOULD WE PREPARE FOR THIS?

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 36

Contact details

Peter Cockcroft

PETER COCKCROFT • DECEMBER 2010 • PALEMBANG Slide 37

TERIMA KASIH