5.4 costs. costs objectives – what costs do business incur? – how can costs be classified;...

TRANSCRIPT

5.4 Costs

Costs

• Objectives– What costs do business incur?– How can costs be classified;• Direct or indirect.• Variable or fixed.

– Break-even analysis

What costs do business incur?

• Make a list of all the costs that you think Cambridge College incurs.

• What outputs does Cambridge College have?

Direct and indirect costs

• Direct costs – costs that can be clearly identified with each unit of production.

• Indirect costs – costs that cannot be identified with each unit of production. (These can also be called overhead costs).

• Sort your list of costs into either; direct or indirect.

Fixed and variable costs

• Fixed costs – costs that do not change with the level of output (production).

• Variable costs – costs that change with increasing or decreasing output (production).

• Sort your list of costs into variable or fixed.

Fixed and variable costs

Formulas• Total Variable Costs = Variable cost per unit * Q• TVC = VC * Q

• Total Costs = Fixed Costs + Total Variable Costs• TC = FC + TVC

• Revenue = Price * Q• R = PQ

THE Formula

• Profit or Loss = Revenue – Total Costs

• If R > TC = profit• If R< TC = loss

Case study: Suzy’s Driving SchoolSuzy Clarke has decided to set up her own driving school. She has the following costs:

Petrol:£10 per lesson

Maintenance:£5 per lesson

Insurance and tax:£50 per week

Repayments: £30 per week

Advertising:£30 per week

Wages:£250 per week

Phone bill:£1 per lesson

She charges £25 for a 30 minute lesson and can do no more than 60 lessons a week.

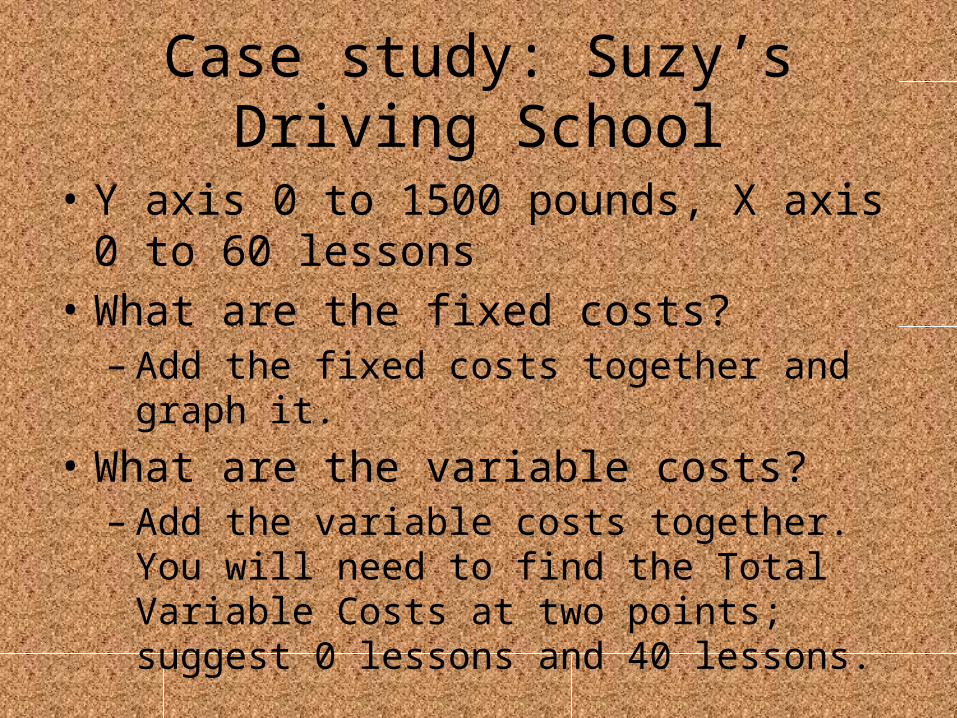

Case study: Suzy’s Driving School

• Y axis 0 to 1500 pounds, X axis 0 to 60 lessons • What are the fixed costs?– Add the fixed costs together and graph it.

• What are the variable costs?– Add the variable costs together. You will need to

find the Total Variable Costs at two points; suggest 0 lessons and 40 lessons.

Break Even Graph for Suzy’s Driving School

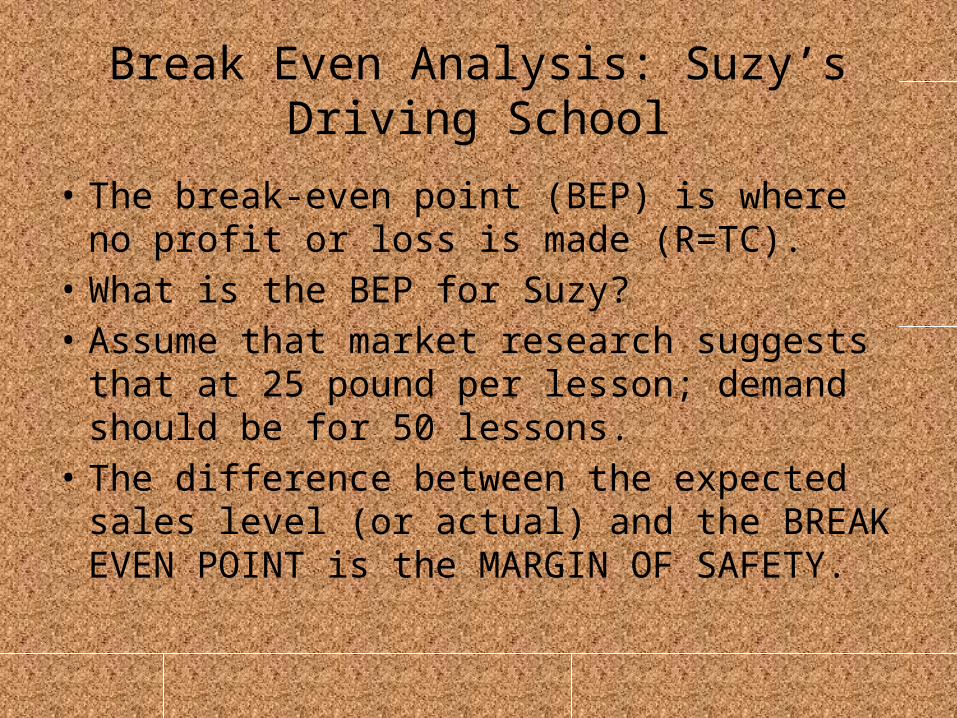

Break Even Analysis: Suzy’s Driving School

• The break-even point (BEP) is where no profit or loss is made (R=TC).

• What is the BEP for Suzy?• Assume that market research suggests that at

25 pound per lesson; demand should be for 50 lessons.

• The difference between the expected sales level (or actual) and the BREAK EVEN POINT is the MARGIN OF SAFETY.

Break Even Graph for Suzy’s Driving School

Calculating the BEP

• Contribution = P-VC

• BEQ = FC/Contribution

• Try it for Suzy;– FC = 360– VC = 16– Price = 25

• Draw a break even chart for the following:– Fixed Costs = $10,000– Variable Cost = $10– Selling price = $15– Maximum production quantity = 3,000

– What is the margin of safety if current is 2,200.

• Pages 512 and 513

• Activity 28.4 Q1

• Activity 28.3 all questions

Who wants to be an A* student?

Break Even Analysis

• Page 512• Make notes on– Break-even analysis further uses– Evaluation of break-even analysis

• Paper 2 Nov 11– 2aii, 2bi, 2bii– Extension: Have a look at 1c.

Break Even Analysis

• Warning:– Break-even assumes that the factory, school,

machinery, etc. already exists. Other investment appraisal techniques must be used to include these in the analysis.

Plenary

• Objectives– What costs do business incur?– How can costs be classified;• Direct or indirect.• Variable or fixed.

– Break-even analysis