5 ways for a business loan preparation

TRANSCRIPT

wa

ys

Business

preparation

For a

LOAN

“It takes money to make money.”

One core essential of

business is

MONEY.

No business could start

WITHOUT FUNDS.

Turning to banks is the

ONLY OPTION.

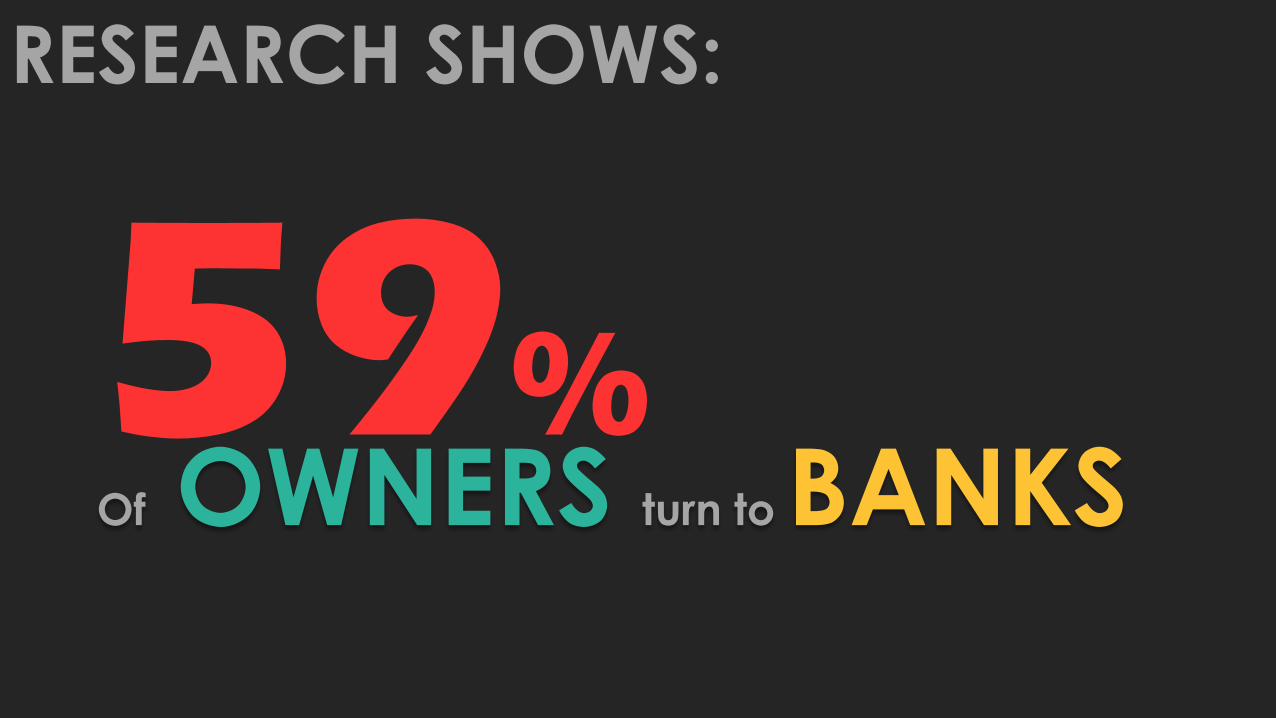

RESEARCH SHOWS:

%Of OWNERS turn to BANKS

%

RESEARCH SHOWS:

gets APPROVED

ONLY

Prepared businesseshave better chances of gaining

LOAN APPROVALS.

5 TIPS:

a fresh start and follow this

Give the company

HA

VE ADETAILEDBUSINESS

PLAN

Create a

BELIEVABLE ACHIEVABLEDOCUMENTATION OF

BUSINESS PLAN

and

INCLUDED IN THE PLAN ARE:

YOUR COMPANYPRODUCT

TARGET MARKET

TEAM

FINANCIALS

Do extra measures such as

providing enriching details to give

depth on how the funds will be

used.

Prepare to

SHARE ALLFINANCIALINFORMATION

BE READY PREPAREand

FINANCIAL BACKGROUND

OF THE COMPANY.

a DETAILED LIST of the

THE LIST INCLUDES:

CURRENT & PAST LOANS

INCURRED DEBTSALL BANKS & INVESTMENT ACCOUNTSCREDIT CARD ACCOUNTSSUPPORTING DOCUMENTS(tax id numbers)

ALSO, A LIST OF:

ACCOUNTS PAYABLEACCOUNTS RECEIVABLEAUDITED FINANCIAL STATEMENTS

Through the given summaries of

financial history of the company,

the lenders will then be able to

identify whether the company is

capable of paying back the loan.

CREDIT SCOREcalculated from reports generated by financial Institutions.

, a three-digit number

A CREDIT SCOREdetermines whether you’re eligible for a loan,

mortgage or credit card.

There are dedicated financial

institutions present to help you

determine your credit score.

They even give you advices on how

you could increase your score.

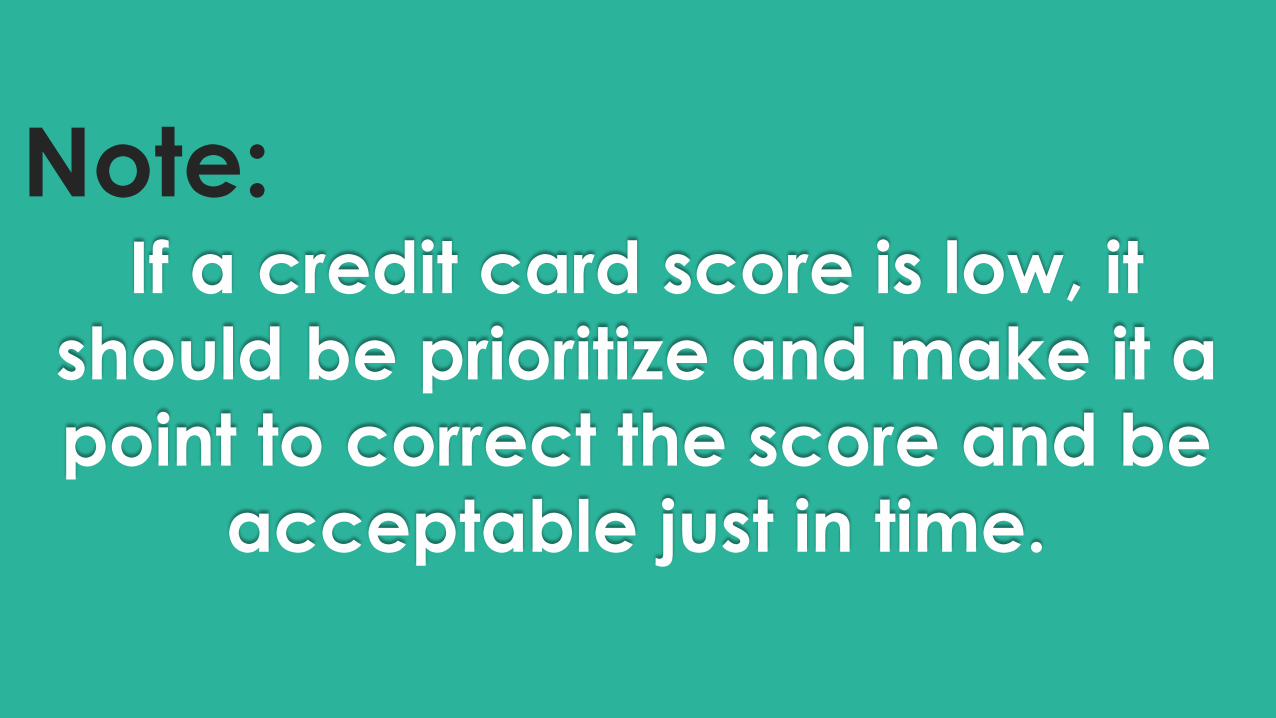

Note:If a credit card score is low, it

should be prioritize and make it a

point to correct the score and be

acceptable just in time.

Have

CAPITAL

“If they had capital, they wouldn’t be applying

for a loan in the first place.”

This misconception always triggers the

disapproval of most creditors.

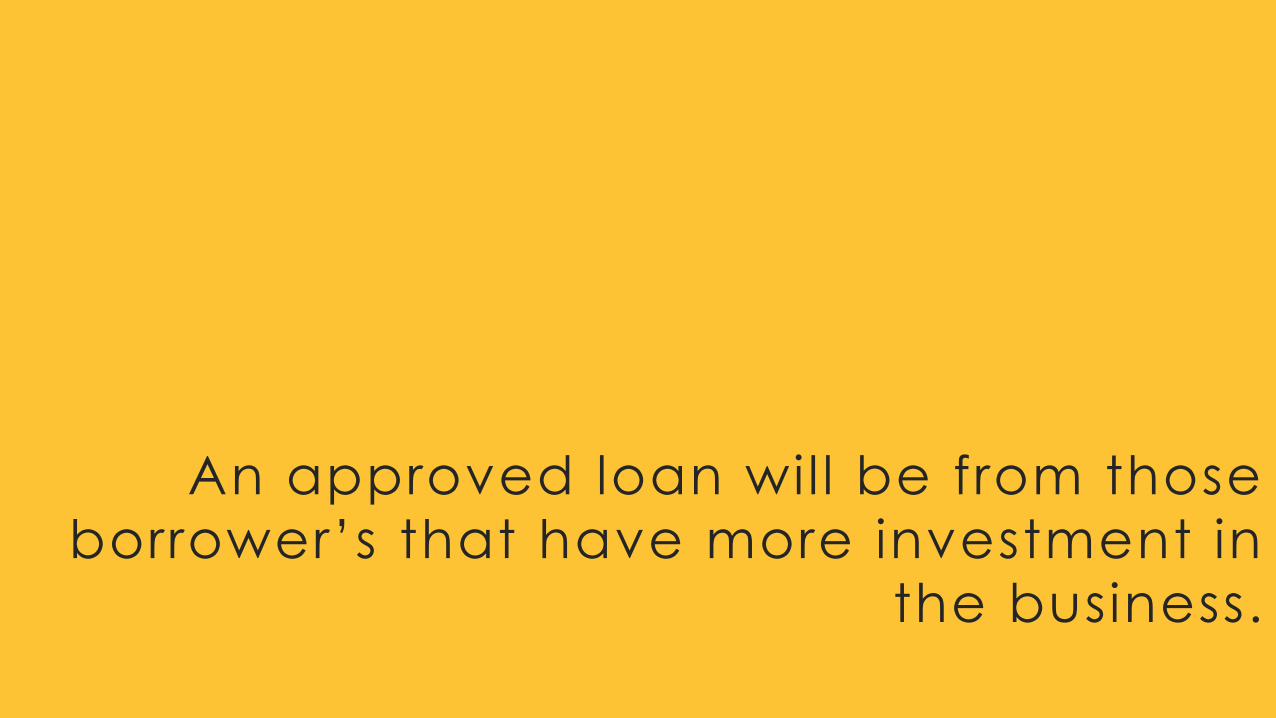

An approved loan will be from those

borrower’s that have more investment in

the business.

Lenders usually

accepts loans when

the potential

borrowers are the

ones who’s not

financially disabled.

They accept those who still has funds

giving them certainty that the loan

isn’t the last resort for the survival of the

company.

BE P

REP

AR

ED

DRAW UPCOLLATERAL

TO

Collaterals are assets which is used to be

the alternative before being able to pay back the loan.

PROPERTYEQUIPMENT

STOCK

Collaterals could be:

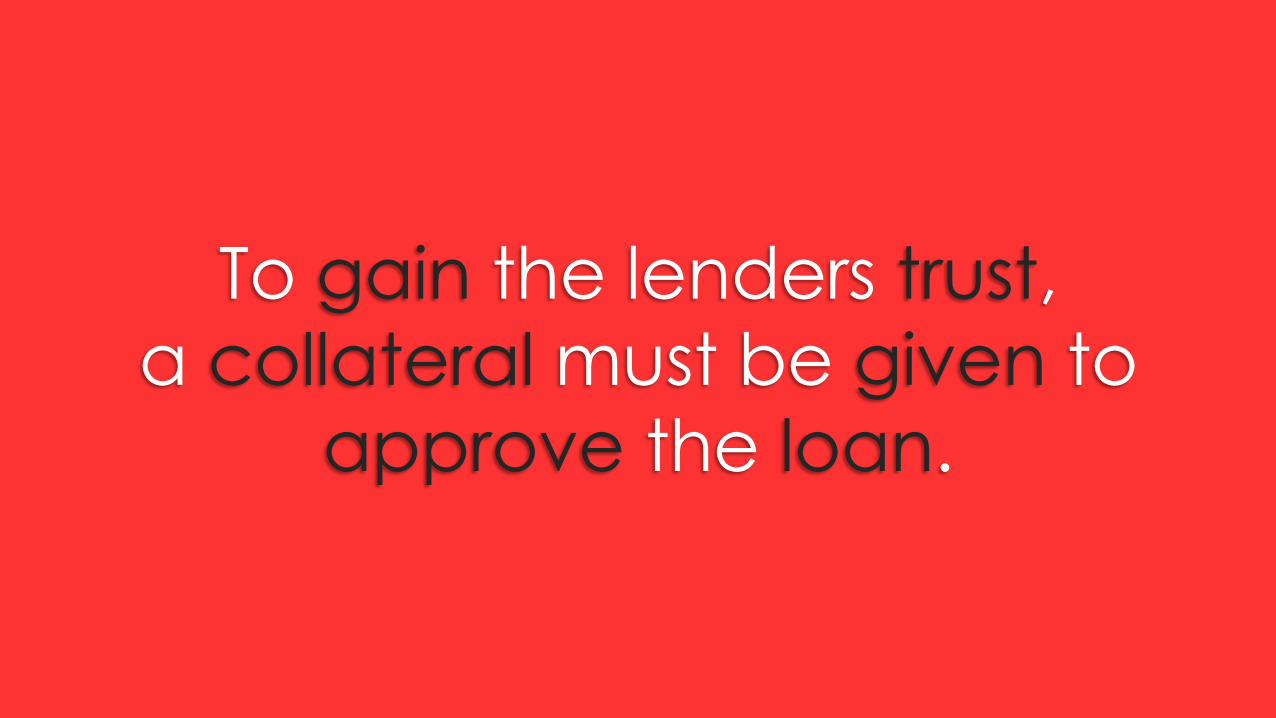

To gain the lenders trust,

a collateral must be given to

approve the loan.

FIRST STEP.Preparing for a business loan is just the

FINDING WAYS to mitigate any

weaknesses or risks that might deter you from gaining

loan approval is

what ultimately gets you

financing.

5 ways to prepare your company

for a business plan is brought to you by

Infinit Finance and Accounting,

an outsourced accounting company prepared to help you with your

accounting predicament.