45^f - app.lla.state.la.us · gilhertr. ska,\lei,jk., q'a c. couy white, jr., cpa, mk ron w....

TRANSCRIPT

45^f

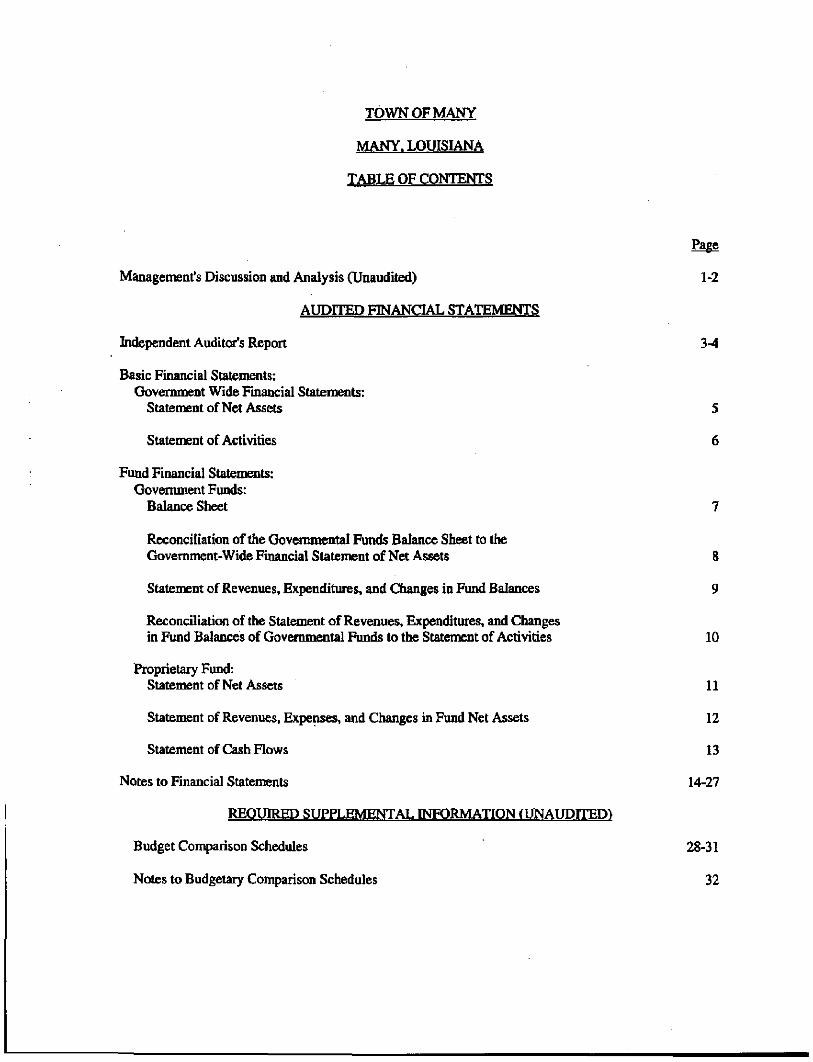

TOWN OF MANY

MANY, LOUISIANA

JUNE 30,2008

jnder provisions of state law, this report is a public document, Acopy of the report has been submitted to the entity and other approphale public officials. The report is available for public inspection at the Baton Rouge office of the Legislative Auditor and, where appropriate, at the office of the pansh clerk of court.

Release Date BJulof

TOWN OF MANY

MANY. LOUISIANA

TABLE OF CONTENTS

Page

Management's Discussion and Analysis (Unaudited) 1-2

AUDITED FINANCIAL STATEMENTS

Independent Audit<»:'s Report 3-4

Basic Financial Statements: Government Wide Financial Statements:

Statement of Net Assets S

Statement of Activities 6

Fund Financial Statements: Government Funds:

Balance Sheet 7

Reconciliation of the Govermnental Funds Balance Sheet to the

Govenunent-Wide Financial Statement of Net Assets 8

Statement of Revenues, Expenditures, and Changes in Fund Balances 9

Reconciliation of the Statement of Revenues, Expenditures, and Changes in Fund Balances of Governmental Funds to the Statement of Activities 10

Proprietary Fund: Statement of Net Assets 11

Statement of Revenues, Expenses, and Changes in Fund Net Assets 12

Statement of Cash Flows 13

Notes to Financial Statements 14-27

REOUIRED SUPPLEMENTAL INFORMATION (UNAUDITED)

Budget Comparison Schedules 28-31

Notes to Budgetary Comparison Schedules 32

TOWN OF MANY

MANY. LOUISIANA

TABLE OF CONTENTS

OTHER REPORTS

Report on Internal Control Over Financial Reporting and on Con^liance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards 33-34

Schedule of Findings and Responses 35

Schedule of Prior Year Rndings 36

Management's Corrective Action Plan for Cuirent Year Findings 37

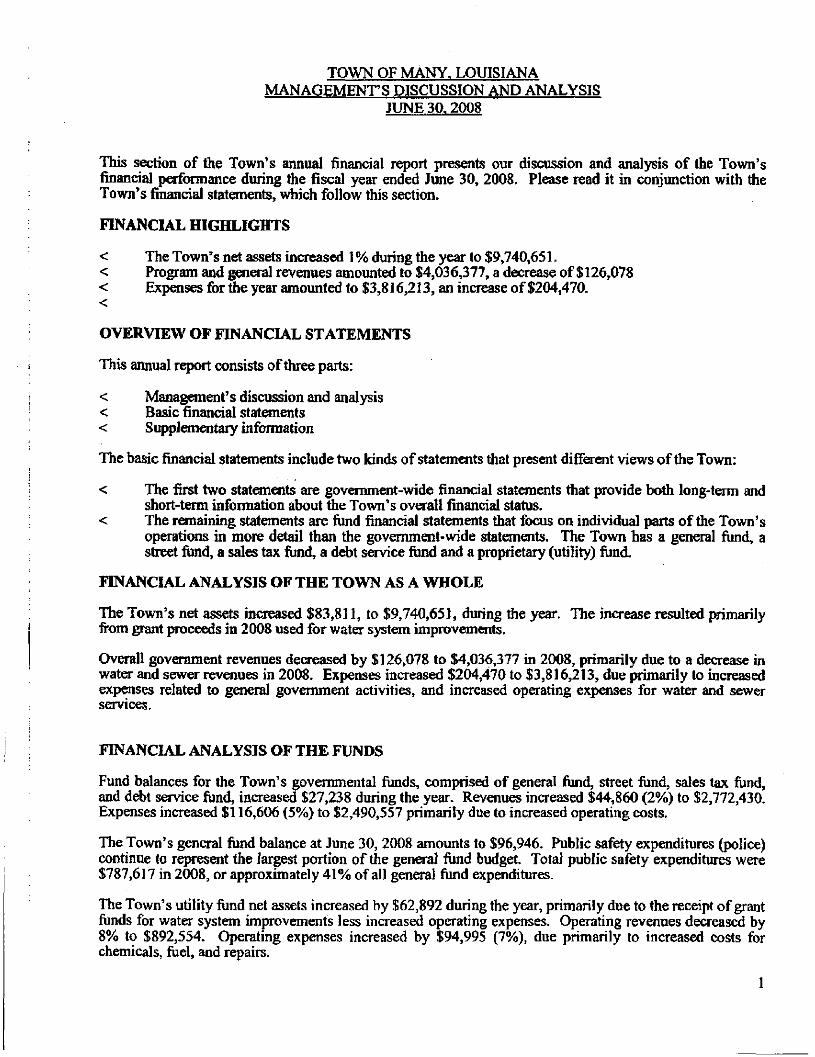

MANAGEMENT'S DISCUSSION AND ANALYSIS (UNAUDITED)

TOWN OF MANY, LOUISIANA MANAGEMENT'S DISCUSSION AND ANALYSIS

JUNE 30.2008

This section of the Town's annual financial report presents our discussion and analysis of the Town's financial performance during the fiscal year ended June 30, 2008. Please read it in conjunction with the Town's financial statements, which follow this section.

FINANCIAL HIGHLIGHTS

< The Town's net assets increased 1 % during the year to $9,740,651. < Program and general revenues amounted to $4,036,377, a decrease of $126,078 < Expenses for the year amounted to $3,816,213, an increase of $204,470. <

OVERVIEW OF FINANCIAL STATEMENTS

This annual report consists of three parts:

< Management's discussion and analysis < Basic financial statements < Supplementary information

The basic financial statements include two kinds of statements that present different views of the Town:

< The first two statements are government-wide financial statements that provide both long-term and short-term infoimation about the Town's overall financial status.

< The remaining statements are fund financial statements that focus on individual parts of the Tovra's operations in more detail than the govemment-wide statements. The Town has a general fimd, a street fimd, a sales tax fund, a debt service fund and a proprietary (utiHty) fimd.

FINANCIAL ANALYSIS OF THE TOWN AS A WHOLE

The Town's net assets increased $83,811, to $9,740,651, during the year. The increase resulted primarily fi"om grant proceeds in 2008 used for water system improvements.

Overall government revenues decreased by $126,078 to $4,036,377 in 2008, primarily due to a decrease in watCT and sewer revenues in 2008. Expenses increased $204,470 to $3,816,213, due primarily to increased expenses related to general government activities, and increased operating expenses for water and sewer services.

FINANCIAL ANALYSIS OF THE FUNDS

Fund balances for the Town's governmental fimds, comprised of general fund, street fimd, sales tax fiind, and debt service fund, increased $27,238 during the year. Revenues increased $44,860 (2%) to $2,772,430. Expenses increased $116,606 (5%) to $2,490,557 primarily due to increased operating costs.

The Town's general fimd balance at June 30, 2008 amounts to $96,946. Public safety expenditures (police) continue to represent the largest portion of the general fiind budget. Total public safety expenditures were $787,617 in 2008, or approximately 41% of all general fiind expenditures.

The Town's utility fimd net assets increased by $62,892 during the year, primarily due to the receipt of grant fiinds for water system improvements less increased operating expenses. Operating revenues decreased by 8% to $892,554. Operating expenses increased by $94,995 (7%), due primarily to increased costs for chemicals, fuel, and repairs.

TOWN OF MANY. LOUISIANA MANAGEMENT'S DISCUSSION AND ANALYSIS

JUNE 30.2008

CAPITAL ASSETS

During 2008 the Town invested z^proximately $613,000 in improvements to the water distribution system. In addition, investments were made in entrance signs ($34,000), street overlays ($36,000), theater improvements ($ 18,000), and new equipment ($51,000).

ECONOMIC FACTORS AND NEXT YEAR'S BUDGETS AND RATES

The Town is dependent on charges for services, and ad valorem and sales taxes, for approximately 35% and 38%, respectively, of the total revenues. The Town's sales tax rate decreased fi*om 1 VA percent to 1 percent effective October 1, 2008, the end of the ten year term, as the Town's related DEQ debt secured by a !4% sales tax was retired in December 2008. In addition, water rates were increased 24% effective September 1, 2008 to cover increased cost of operations in the water department. No other significant changes are expected in revenues during fiscal year 2009, however the current depressed state of the nation's economy could result in reductions of tax revenues during 2009.

The Town has received a Louisiana capital outlay grant of $1,900,000 to assist in the completion of the water line replacement program which began several years ago, to add generators to water and sewer operations as required by Louisiana, and to address the water production problems associated with the extremely tow level of Toledo Bend Lake encountered in &e fall of 2006. In 2008 the generator project was completed at the cost of $514,976. In 2009 the remaining wateriine replacement project and filter repair at the water treatment plant will be completed. Completion of these projects should result in fiiture decreases in repair costs and water losses fit)m leaks, more stable water production and improved operations in emergency situations

The Town has received a grant fix)m the Louisiana Community Development Block Grant program for Street Improvements in the amount of 260,780. These funds will be used to overlay four streets in the town.

CONTACTING THE TOWN'S FINANCIAL MANAGEMENT

This financial report is designed to provide our citizens, taxpayers, customers, and investors and creditors with a general overview of the Town's finances and to demonstrate the Town's accountability for the money it receives. If you have questions about this report or need additional financial information, contact Mr. Kenneth Freeman, Mayor, P O Box 1330, Many, LA 71449.

AUDITED FINANCIAL STATEMENTS

H E A R D M G E L R O Y & VESTAL

U P CERTTRED PUBLIC ACCOUNTANTS

333 TliXAS SlREIiT 15TH FLOOR

SuRnvEPOHT, LA 71101

338 429-1525

318 429-2070 FAX

P O S T O F H C E BOX 1607

SHREVEPORT, LA

71165-1607

PARTNERS

SPENCER BERNARD, JR. . CPA H.Q. GAHAOAN, JR. , CPA, AHC GiiRALo W. HEOGCOCK, JR., CPA, Arc TIM 13. NitLSKN, CPA, AI-C JOHN W . DEAN, CPA, APC MARK D . ELDRKDCE, CPA ROOEHTL. DEAN, CPA STEPHEN VC. CKAIG, CPA

ROY E . PRESTCI'OOD, CI'A

A. D. JOHNSON', JR., CPA

BENJAMIN C. WOODS, CPA/AHV, C\'A

AUCE V. FR.AZIER, CPA

MELISSA D . MITCHAM, CPA, cn»

O F COUNSEL

GILHERTR. SKA,\LEI,JK., Q'A

C. CouY WHITE, JR., CPA, MK

RON W . STTWABT, Q'A, APC

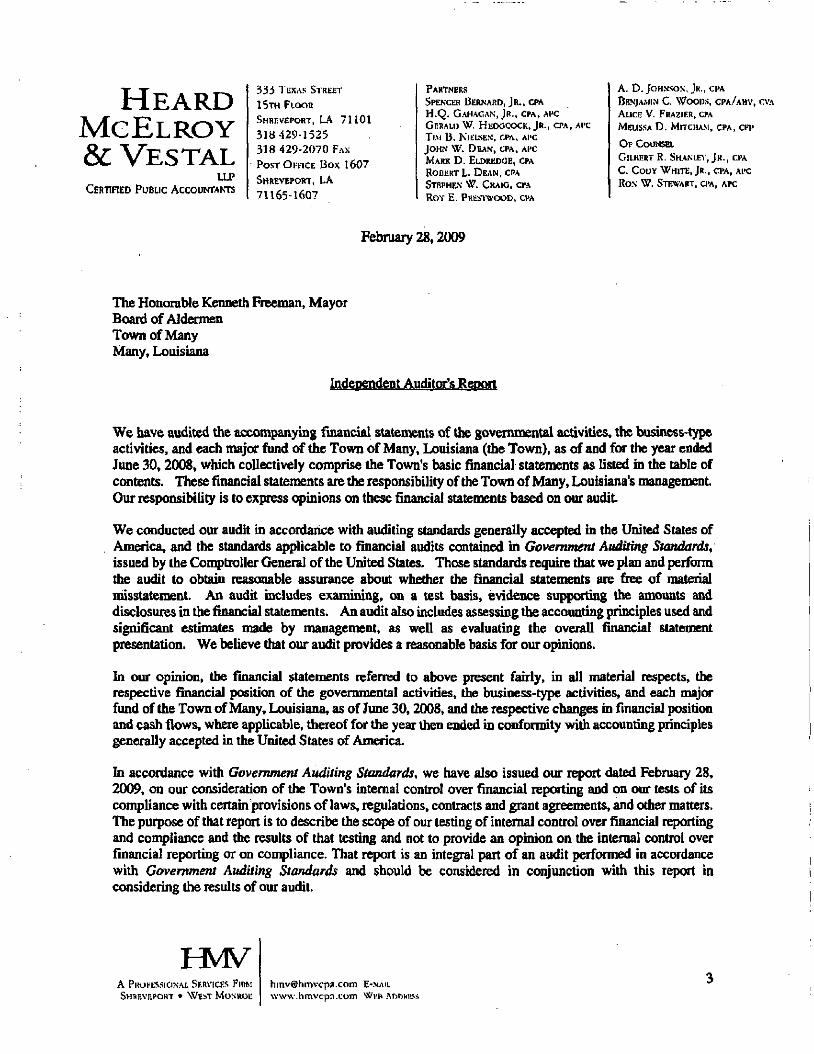

Febniary 28.2009

The Honorable Kenneth Freeman, Mayor Board of Aldermen Town of Many Many, Louisiana

Independent Auditor's Report

We have audited the accompanying financiai statements of the govemm&ntal activities, the business-type activities, and each major fimd of the Town of Many, Louisiana (the Town), as of and for the year ended June 30, 2008, which collectively comprise the Town's basic financial statements as listed in the table of contents. These financial statements are the responsibility of the Town of Many, Louisiana's management. Our responsibility is to express opinions on these financial statements based on our audit.

We conducted our audit in accordance with auditing standards generally accepted in the United States of America, and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Conq}troller General of the United States. Those standards require that we plan and perform the audit to obtain reascHiable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinions.

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, the business-type activities, and each major fund of the Town of Many, Louisiana, as of Jime 30,2008, and the respective changes in financial position and cash flows, where applicable, thereof for the year then ended in confomuty with accounting principles generally accepted in the United States of America.

In accordance with Government Auditing Standards, we have also issued our report dated February 28, 2009, on our consideration of the Town's internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts and grant agreements, and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing and not to provide an opinion on the internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards and should be considered in conjunction with this report in considering the results of our audit.

HVIV A pROhtSSlONAL SF.RVICHS FlRM SuREvnPOHT • W E M ' M O N R O E

hniv®limvcpfl.coin E-.MAIL www.hmvcpji .Lom WKM ADDhiiss

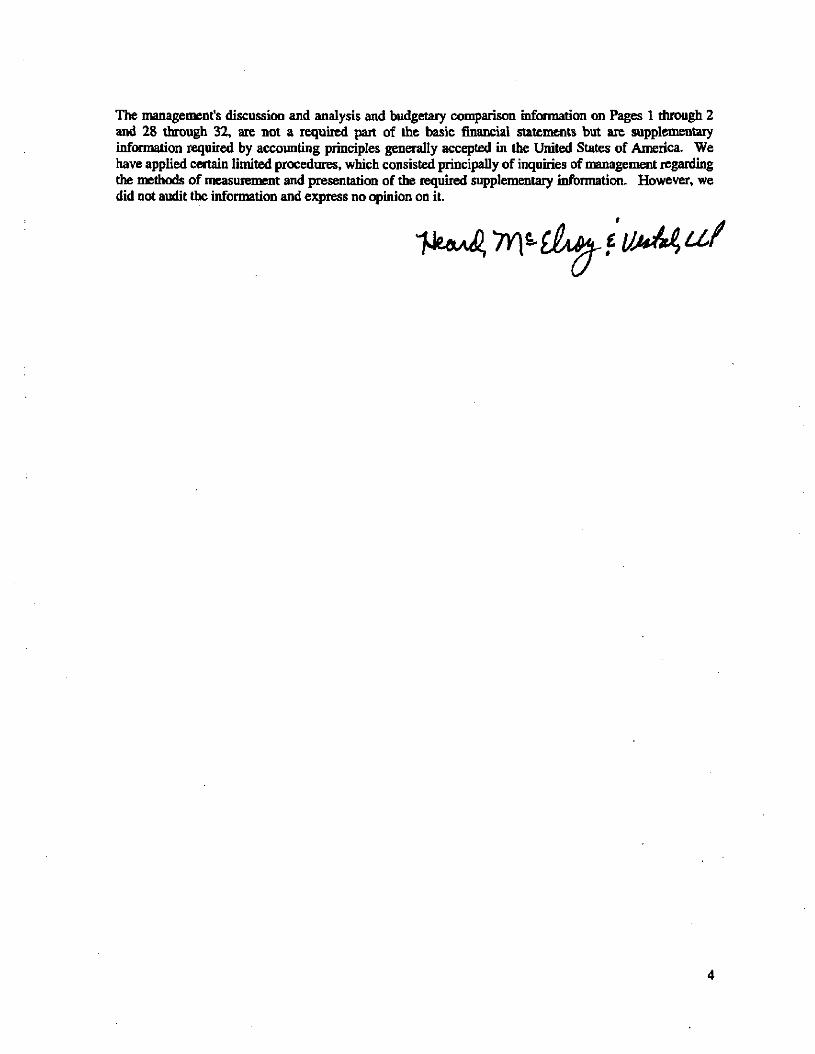

The management's discussion and analysis and budgetary comparison infcHination on Pages 1 through 2 and 28 through 32, are not a requireid part of the basic financial statements but are supplementary information required by accounting principles generally accepted in the United States of America. We have applied certain limited procedures, which consisted principally of inquiries of management regarding the methods of measurement and presentation of the required supplementary information. However, we did not audit the information and express no opinion on it.

1 ^ ^ ^ yy\ - £ ^ i u u M LLf

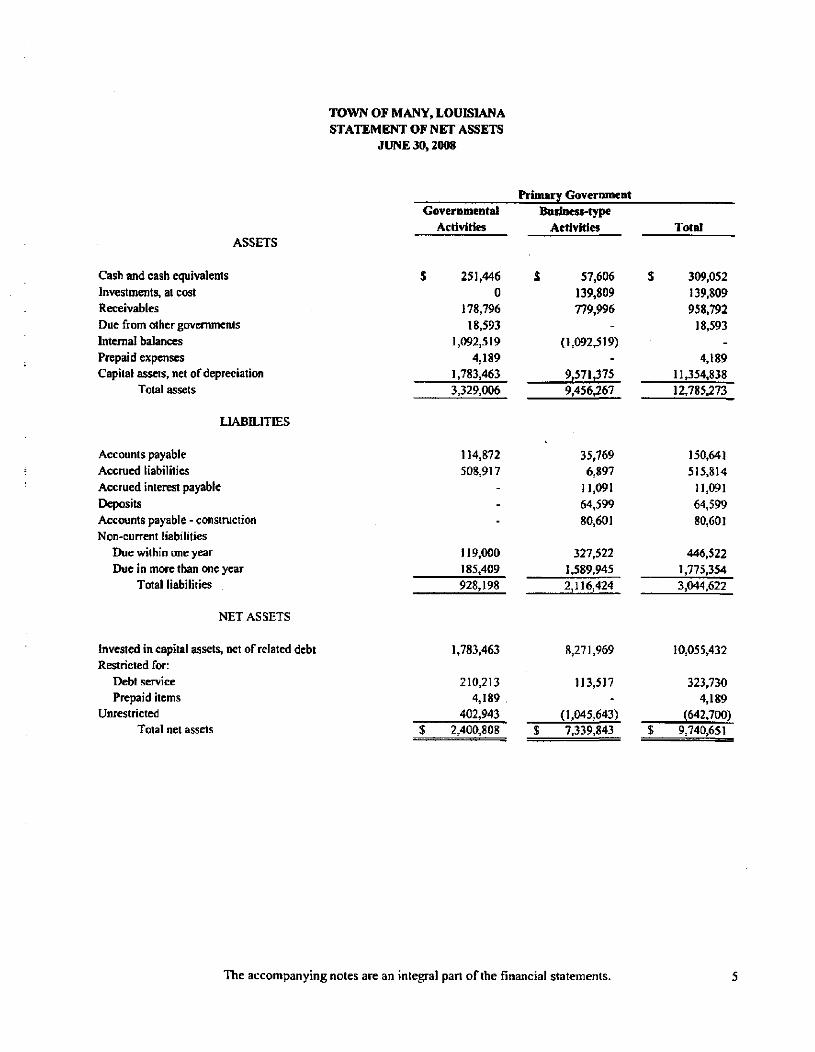

TOWN OF MANY, LOUISIANA STATEMENT OF NET ASSETS

JUNE 30,2008

Primarv Government

ASSETS

Cash and cash equivalents Investments, at cost Receivables Due from other govemmenis Internal balances Prepaid expenses Capital assets, net of depreciation

Total assets

LIABILITIES

Accounts payable Accrued h'abilities Accrued interest payable Deposits Accounts payable - construction Non-current liabilities

Due within one year Due in more than one year

Total liabilities

NET ASSETS

Governmental ActiviHes

$ 251,446 0

178,796 18,593

1,092.519 4,189

1,783,463 3,329,006

Business-type

Activities

$ 57,606

139,809 779,996

-(1,092,519)

-9,571.375 9,456.267

Total

$ 309,052

139,809 958,792

18,593 -

4,189 11,354,838 12,785.273

114,872 508,917

-

-

-

119,000 185,409 928,198

35,769 6,897

n,091 64,599 80,60]

327,522 1,589,945 2,116,424

150.641

515.814 11,091

64,599 80,601

446,522 1,775,354 3,044.622

Invested in capital assets, net of related debt Restricted for:

Dd>t service Prepaid items

Unrestricted Total net assets

1.783,463

210,213 4.189

402,943 $ 2,400,808

8,271.969

113,517 -

(1,045,643) $ 7,339,843

10.055.432

323,730 4,189

(642,700) $ 9.740,651

The accompanying notes are an integral pan of the financial statements.

r- ^ r- »-. oo o OO • « O 0» \ 0 CO C9 C7_ »n_ <7>. OV_ 04 — ^o c " NO r-" r-T i r t * n oo <*> O —-f * l * ^ T f — *—' •— »—' v_- -s^

<iA

oo m r-

•.• T l ;

r ^ r^

2 r > i

^

t ^ r-

g r * i

>cn " T L

\oi \oN

1

<o — 1 ^ o» • ^ o» v ^ «ri «r> r -— r n "T 'O C^ oo r^" w^ r ^ cN «o o 30 t N * c M r^ M

J c> r N CN

• *

o ( N " O

o

V I

o o • v

r o-

t i «

P ^ - s -—s «rt

C ^ o

^ * r t M

M «N <©

r-sn f N

r=-oO

c

•rt * * 1

b 4

1 ro i r t r ^

o «r»

O * OO

•*

PM l >

SO r ^

—

OO ' C

o r^ NO

ON 3 0 ( N

I N

'-.-

OO m r

^ •<r

*o — »o — OS »<*> * r» r ^

^ fO ^ so 3- »o 0^ t o

oe c! "o ^ ts ' t «n O OO ^ O t n (M CM r 4 r a

rsi —

oo^ OS r * *£> t o r^

(M

rs| ^ r- *o

r-^ rO SI

< Wl ^ r V - U l €S ^ 2 «o 5 H ttj

> u. O z O z < [_ ^

S z B: u. w < ^ fid >

* !; «^ > < X O H H

o

M

•S.J2 -c

111 " 5

6 6 ^ S

c « a

« e i g 0 ^ 3

i 8

v-1

c: o 5

• ^ o so

5

v% -o^ r o M O OO

O " ^ M r^ w*» r n c;, c_ OO o cT p^

r O r J

rs S.O OO

ro

wo O -•r 0 0 w-v < o

t r y

O •<r OO W-. 1-1

oof nr s o *

" f f ' T r--

t ^ •^> r> r^ •rt

T

«rt v> P i c* so

'ST V I V )

r M a* 0 0

r^

«rt sf> V >

t - ^

sTS

r-o o

r-

Os sO

t—

r o O i

r> sC r o

OO »C

r-«i^

o Drt l-M

rs )

*N v \ c Si^ T O

Ol

o O S

v» v \ • *

r . O S sT .

V ^

»o - « •

1^ 3 E

E 3 C _ „ _ tn O • = = ' a

8 ! g r S .s 1

JO « s "s E - 8 ^ I i H •" « o •*

a z

p V —

n ^ S

O

ie

"S £ o

2 I ' P g s U £ £ S § := i ? g « e - o , * * ^ - 2 c ^ O o i i

3

11 t o CO

2 i • ^ D.

CO

< H Z.

J Ld „ < S 9 H ^ z

g i g > O O

V C O S

r- O O

r--

fO Cf v \ oo" >->

f>i

^ oo r o O O

t ^

<r-oo

• ^

t n

^ O O

S O f O

<N 0 0 so

v o

*o

r-Cs

o w

rs( O S

r o cs"

f O ( N r o

<—• O S S O

<N

— > «n •—1

**!

210.213

4,189

707.352

O S

so so oo

i <N

u fey

Os

«

» oo

.336

o (N

s (N

6 9

ro «N

o t N

, o

.~> . — t

<N

V I

w a z u.

z <

5 S 00 o z e -" « S

5|S

O [d

z

CD

V)

< H

so • - r ^ <N r o sO

ro f O

* so

( N

f O f O

o rs i

r-* t o o« r o

r^ r o cs f O

f N V I

C r o

W

' O «0 rO ' Cs C- oo

KT, l/^^ OO* vO — -c V ,

OO

• ^

»A

sO

«

r o

r i

,457

r ^ ' T

oc g-1 sO

§ •c

oc M^ sC

i >c

« »r» 0 0

NO

c

• s t rs» so

' fO Cs rsi oo c- —. so* •**

c .

r^ s o r o

cT ao

—

C- O <N r ^ SO c r o ^f r o fsf sO cs ' c« o

o o l y ^

t--• *

• ~

rsi

- r o oo o —

o- t--oo m — t ^ TT rs)

c s

NO T T C S

sO

o

sf r o

^ OC

i3 C u S i OS > '5

S • 3 C

CO

O

1 re

1 i

^

>

i o i

u E

^ o £ o i : S Q

••r.

C

u

O

o ^ S Q

E u -:3

1. 2 &:

w

(0

2 fS

o

o.

o c CO

c •?s

c Ed o. B o u u CD

£ c

Si S g c: : E O

r r n» 4>

V. E a>

« O ?

::= o o -c < <

« £

TOWN OF MANY, LOUISIANA RECONCILIATION OF THE GOVERNMENTAL FUNDS BALANCE SHEET

TO THE STATEMENT OF NET ASSETS FOR THE YEAR ENDED JUNE 30,2008

Fund balances - total governmental funds 921.754

Amounts reported for govemmoitaj activities in the statement of net assets are difTerent because:

Capital assets used in governmental activities are not financial resources and therefore arc not reported in the governmental funds.

Governmental capital assets Less accumulated depreciation

3,399,842 (1,616,379) 1,783,463

Long-term liabilities including bonds payable are not due and payable in the current period and therefore are not reported in the governmental funds.

General Obligation Bonds Payable Accumulated unpaid vacation

(242,320) (62,089) (304,409)

Net assets of governmental activities 2,400.808

The accompanying notes are an integral part of the financial statements.

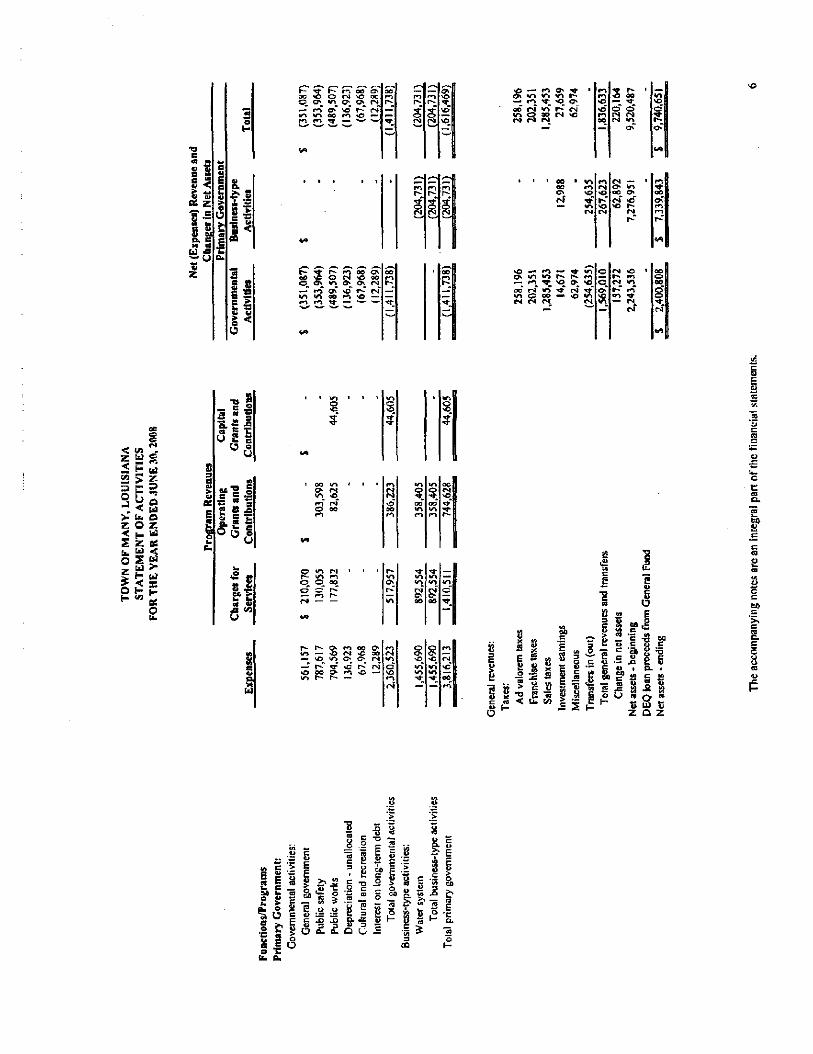

TOWN OF MANY, LOUISIANA STATEMENT OF REVENUES, EXPENDITURES^ AND CHANGES IN FUND BALANCES

GOVERNMENTAL FUNDS FOR THE YEAR ENDED JUNE 30,2008

RevcBues: Taxes Licenses and peimju lotasovenuiMiila] Charges roricraots Fines imerest Miscellaneoas

Total levenues

GENERAL

$ 303,610 210^070 423,228 177.832 130,033

8 ^ 1 «2,974

STREETT

S -

7,600

-.

3>290

-

SALES TAX

$ 1,283,453

----

2.645

-

DEBT SERVICE

S 156,937

--. -

675 -

TOTAL GOVERNMENTAL FUNDS

S 1,746.000 210.070 430.828 177.832 130,055 14,671 62.974

1,313.830 10,890 1,288.098 157,612 2,772.430

Expenditures: ConunuiiicatuHi COoiiBCted Seivkes Employee Benefits Great

Pnfessiooal Services Ca^Ul outlay Rental Repaiis Salaries Supplies Vehicle Miscellaneous Higliway aod Street

Debt service: Principal retiremert Interest and fiscal charges

Total expetidltures

Excess (defkieocy) of icvetme overexpenditares

Other financing sources (uses):

OpeiatiQg transfers in Operating u:ansfefs out

Total other finandng sources (uses)

Excess (defidency) (rf' revenues and oiber finandog sources over (under) expenditures and other fisancing uses

Bmd balances, beginnii\g of year

Hind balances, end of year

47.166 346.904 290.082

23.910 15.023 47.417 84,716 4.243

45,130 7 9 3 ^ 1 85,260 48,931 77.531

-

_ -

1,909.986

(594,156)

508,121

-

508.121

(86,035)

182.981

$ 96,946

-13.925 19.285

-27,610 5.160

69370 260

61.019 117393 66,602 30380

3.692 28.771

_ .

444.467

, (^3W77>

508.121

-

508,121

74.544

526,114

S 600,658

------. -----

9,815

-

. -

9,815

1.278.283

(1.270,877)

(1.270.877)

7.406

6.531

5 13.937

114.000 12.289

12639

31.323

-

.

31.323

178.890

S 210.213

47.166 360329 309.367 23.910 42,635 52,577

134,586 4.503

106,149 911.544 151.862 79311 1 91.058 I 28,771 1

114.000 1 a289

2.490357

281.873

1

1.016.242 I (1.270,877)

(254.635)

27.238

894316

S 921,754

The accort^wnying notes are an tniegraJ part of the financial statements.

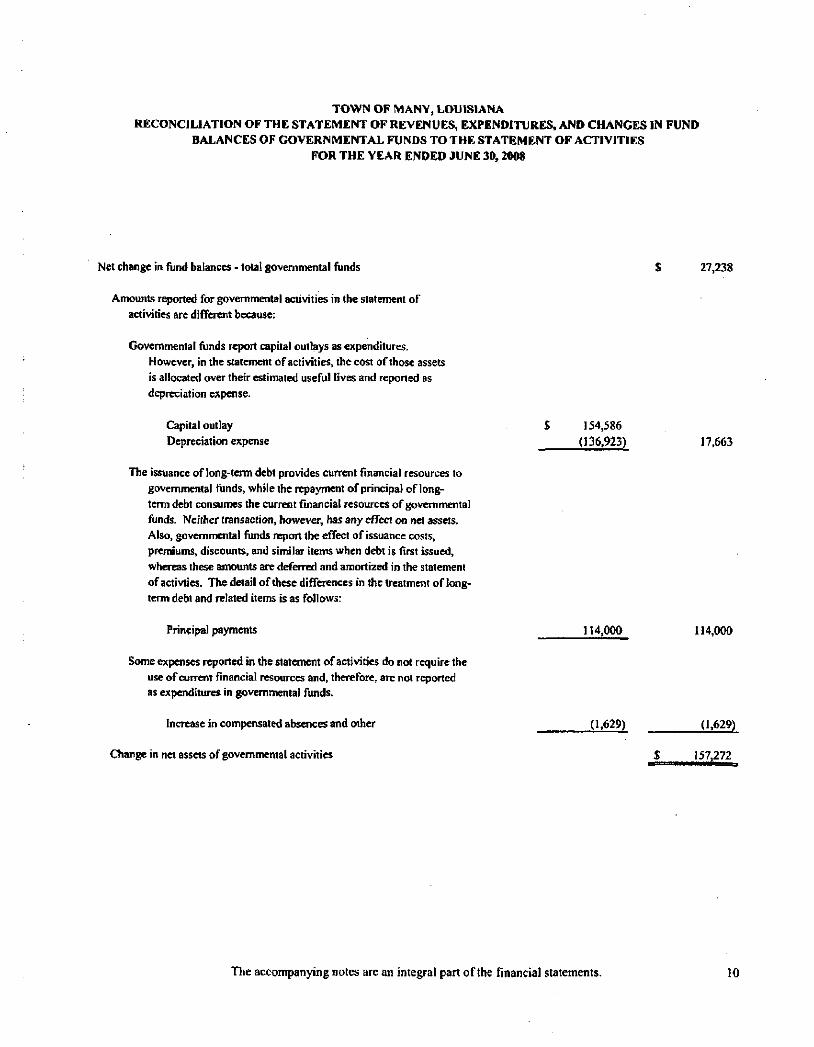

TOWN OF MANV, LOIJISIANA RECONCILIATION OF THE STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND

BALANCES OF GOVERNMENTAL FUNDS TO THE STATEMENT OF ACTIVITIES FOR THE YEAR ENDED JUNE 30,2008

Net change in fund balances - total governmental funds 27,238

Amounts reported for governmental activities in the statement of activities are difTerent because:

Goveromental funds report capital outlays as expenditures. However, in the statement of activities, the cost of those assets is allocated over their estimated useful lives and reported as depreciation expense.

Capital outlay Depreciation expense

The issuance of long-tenn debt provides current fmancial resources to governmental funds, while the repayment of principal of long-term debt consumes the current fmancial resources of governmental funds. Neither transaction, however, has any effect on nd assets. Also, governmental funds report the effect of issuance costs, premiums, discoimts. and similar items when debt is first issued, whereas these amounts are deferred and amortized in the statement of activties. The detail of these differaices in the treatment of long-term debt and related items is as follows:

Principal payments

Some expenses reported in the statement of activities do not require the use of current fmancial resources and, therefore, are not reported as expenditures in governmental funds.

Increase in compensated absences and other

Change in net assets of governmental activities

$ 154,586 (136,923) 17.663

114,000 114,000

(1.629) (1.629)

157,272

The accompanying notes are an integral part of the financial statements. 10

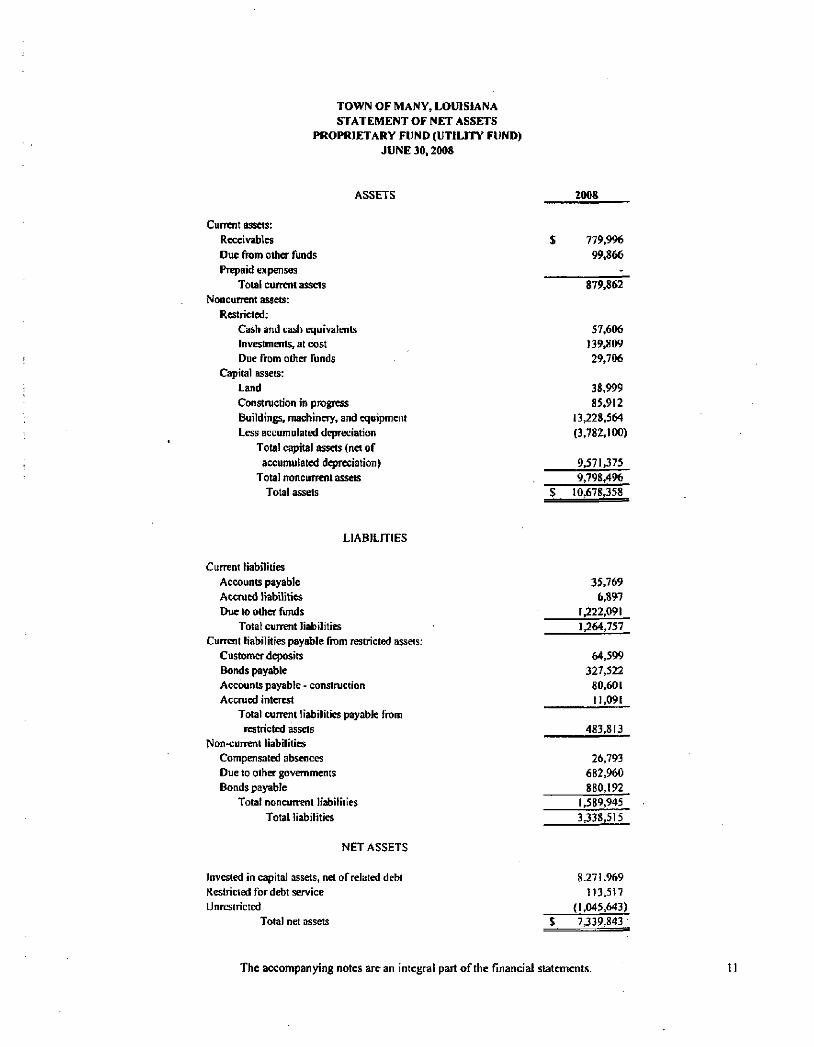

TOWN OF MANY, LOUISIANA STATEMENT OF NET ASSETS

PROPRIETARY FUND (UTILITY FUND) JUNE 30,200S

ASSETS 2008

Current assets: Receivables Due from other funds PTq>aid expenses

Total current assets Noncurrent assets:

Restricted: Cash and cash equivalents Investments, at cost Due from other funds

Capital assets: Land Construction in progress Buildings, machinery, and equipment Less accumulated depreciation

Total capital assets (net of accumulated depreciation)

Total noncurrent assets Total assets

$ 779,996 99.866

879,862

57,606 139,809 29,706

38,999 85,912

13228,564 (3,782,100)

9,571,375 9,798,496

10,678,358

LIABILITIES

Current liabilities Accounts payable Accrued liabilities Due to other funds

Total current liabilities Current liabilities pay^te from restricted assets:

Customer deposits Bonds payable Accounts payable - construction Accrued interest

Total current liabilities payable from restricted assets

Non-current liabilities Compensated absences Due to other governments Bonds payable

Total noncurrent liabilities Total liabilities

35.769 6,897

1,222,091

1,264,757

64.599 327,522

80.601 11.091

483,813

26,793 682,960 880,192

1,589,945 3338,515

NET ASSETS

Invested in capital assets, net of related debt Restricted for debt service Unrestricted

Total net assets

8.27 K969 113,517

(1.045,643) 7.339,843

The accompanying notes are an integral part of the fmancial statements. II

TOWN OF MAI«Y, LOUISUNA STATEMENT OF REVENUES, EXPENSES, AND CHANGES IN WffD NET ASSETS

UTILITY FUND PROPRIETARY FUND TYPE

FOR THE YEAR 0 W E D JUNE 30,2008

2008

Operating Revenues: Water charges Sewer charges Connection charges Miscellaneous

$ 684,592 170,170 10,027 27.765

Total (^xrating revemies

Operating expenses: Salaries Insurance Supplies Ccotract labor i^pai and accounting Repairs and maintenance Truck expense Tekpbone Rent

Office suiqi>lies and postage Retiiienient Payroll taxes Utilities Freight MiscellaDeous Testing fees Sewer plant supplies Water purchased Deprfciation Travel and seminars

T(Mal cq)erating expenses

Operating inccHne (loss)

892,554

296,720 43,704

126.196 96,040 18,459

100,394 19.089 15,450 7.398 7.044

14.824 21,441

146,281

17,404 18356

139,057 42.995

266,611 4,553

1,402.016

(509.462)

Nonoperating revenues (expenses): Interest tnccmie Interest expense Grants Loss on sale of assets

Total noDoperating revenues (expenses)

Income (loss) before conlribations and transfers Transfer frcmi sales tax fund

12.988 (53,674) 358,405

317,719

(191,743) 254.635

Change in n a assets

Net assets, beginning of year

DEQ loan proceeds from General FUnd

Net assets, end of year

62.892

7.276,951

0_

% 7339.843

Tbe accompanying notes are an integral part of the financial statements. 12

TOWN OF MANY, LOUISIANA STATEMENT OF CASH FLOWS - PROPRIFrARY FUND TYPE

UnLTTYFUND FOR THE YEAR ENDED JUNE 30,2008

2008

Cash flows from operaiiag activities: Cash received frcnn customers Cash paid to suppliers Cash paid to enq)lpyees Qistnners' deposits received Customers' deposits refunded

Net cash (used) by opendng activities

Cash flows ftDffl nmcEqntal financing activities Increase in due U) other funds biaease in due to other govemmoits Increase in due from other funds Cash received from grants

Net cash provided by noncapital financing activities

Cash flows frmi c ^ t a l and related financing activities: Proceeds from DEQ loans Sales taxes cdlected for ccxistmction C ^ t a l expenditures paid In cash Cash paid on principal amount of txmds payable DEQ loan proceeds from Geno^l Fund Interest on bcmds payable paid

Net cash i^ovided (used) by capital and related financii^ activities

Cash flows fnm investing activities: Interest received

Net imrease (decrease) in cash, cash equivalents, and investmoits

Cash, cash equivalents, aod investments: begianing of year

Cash, cash equivalents, and investments: end of year ($57,606 + 139.809)

1,035,165 (1,576304)

(343,522) 7,745

(17.653)

(894.769)

388,872 252,406 145,436 358,405

1.145,119

254,635 (525,517) (324,000)

0 (54,989)

(649,871)

12,988

(386,533)

583,948

$ 197.415

Reconciliation of t^wrating Income to net cash {Hovided by operations: Operating income (loss) Adjustments to reconcile operating income to n^ cash

provided by q>erating activities: Depreciation Increase in accounts receivable Decrease in iwepaid expenses Increase in payroll and payroll taxes payable Incfease in accounts payable Decrease in customers' deposits Decrease in accumulated unpaid vacation Increase in sales taxes payable

Total adjustments to operating income

Net cash (used) by operatiog activities

S (509.462)

266,611 142,610

(14356) (773344)

(9,908) 2.971

109

(385.307)

The accompanying notes are an integral part of the financial statements. 13

TOWN OF MANY. LOUISIANA

NOTES TO FINANCIAL STATEMENTS

JUNE 30.2008

Suimnarv of Sipnifficant Accounting Policies The Town of Many (the Town) was incorporated November 1» 1878, under the provisions of a special home nile charter. The Town began operating under the provisions of the Lawrason Act m January 1996 as a result of an election that was held in the Fall of 1995. The Town operates under a Mayor -Board of Aldermen form of government

The accounting and reporting policies of the Town of Many conform to generally accepted accounting principles (GAAP) as applicable to government imits. The Governmental Accounting Standards Board (GASB) is the accepted standard - setting body for establishing governmental accoimting and financial reporting principles. Such accounting and reporting procedures also conform to the requirements of Louisiana Revised Statutes 24:517 and to the guides set forth in the Louisiana Governmental Audit Guide, and to the industry audit guide of State and Local Governments.

The following is a summary of certain significant accounting policies.

Financial Reporting Entity In evaluating how to define the Town of Many, for fmancial reporting purposes, management has considered all potential component units. The decision to include a potential conqxsnent unit in the reporting entity was made by applying the criteria set forth in GAAP and outlines in GASB Statement 14. The basic, but not the only, criterion for including a potential component unit within the reporting entity is the governing body's ability to exercise oversight responsibility. The most significant manifestations of this ability to exercise oversight responsibility include, but are not limited to, the selection of governing authority, the designation of management, the ability to significantly influence operations, and accountability for fiscal matters. A second criterion used in evaluating potential component units is the scope of public service. Application of this criterion involves considering whether the activity benefits the government and/or its citizens, or whether the activity is conducted within the geographic boundaries of the government and is generally available to its citizens. A third criterion used to evaluate potential con^nent units for inclusion or exclusion from the reporting entity is the existence of special financing relationships, regardless of whether the government is able to exercise oversight responsibilities. Based upon the application of these criteria, the financial statements of the Town of Many (the primary government) consist of otdy the fimds and account groups of the Town since the Town has no oversight responsibility for any other governmental entity.

Govemment'Wide and Fund Financial Statements The govemment-wide financial statements (GWFS) (i.e., the statement of net assets and the statement of activities) report information on all of the nonfiduciary activities of the primary government. For the most part, the effect of interfund activity has been removed from these statements. Governmental activities, which normally are supported by taxes, intergovernmental revenues, and other nonexchange transactions, are reported separately from business-type activities, which rely to a significant extent on fees and charges for support

14

1. Summary of Significant Accounting Policies (Continued)

The statement of net assets presents information on all of the Town's assets and liabilities, with the difference between the two reported as net assets. Over time, increases or decreases in net assets may serve as a useful indicator of whether the financial position of the Town is improving or deteriorating.

The statement of activities demonstrates the degree to which the direct expenses of a given function or segment are offset by program revenues. Direct expenses are those that are clearly idratifiable with a specific function or segment Depreciation expense is identified by function and is included in the direct expense of each function. Interest on general long-term debt of governmental activities is considered an indirect expense and is reported separately on the statement of activities. Interest on long-term debt of business-type activities is recorded as direct expenses. Program revenues include 1) fees, fines, and charges to customers or applicants who purchase, use, or directiy benefit from goods, services, or privileges provided by a given function or segment and 2) grants and contributions that are restricted to meeting the operational or capital requirements of a particular function or segment. Taxes and other items not properly included among program revenues are reported instead as general revenues.

Separate fund financial statements (FFS) are provided for governmental funds and proprietary funds. Major individual governmental and enterprise fiinds are reported as separate columns in the FFS. The Town had no noiunajor funds.

Measurement Focus. Basis of Accounting, and Financial Statement Representation The govemment-wide financial statements are reported using the economic resources measurement focus and the accrual basis of accounting, as are the proprietary fimd financial statements. Revenues are recorded when earned and expenses are reccntled when a liability is incurred, regardless of the timing of related cash flows. Property taxes are recognized as revenues in the year for which they are levied. Grants and similar items are recognized as revenue as soon as all eligibility requirements have been met.

Government fimd financial statements are reported using the current financial resources measurement focus and the modified accrual basis of accounting. Revenues are recognized as soon as they are both measurable and available. Revenues are considered to be available when they are collectible within the current period or soon enough thereafter to pay liabilities of the current period. The Town considers revenues to be available if they are collected within 60 days of the end of the current fiscal period. Ad valorem taxes are recognized as revenues in the year in which final approval is received from the Louisiana Tax Commission, at which time a valid claim exists, to the extent considered available. Expenditures generally are recorded when a liability is incurred, as under accrual accounting. However, debt service expenditures, as well as expenditures related to con^nsated absences are recorded only when payment is due.

Ad valorem taxes are considered "measurable" at the time of levy. Substantially all other non-intergovemment revenues are susceptible to accrual and are recognized when earned or the underlying transaction occurs. Those revenues susceptible to accrual are ad valorem taxes, franchise taxes, sales taxes, interest revenue, licenses, intergovernmental revenues, and charges for services. Fines, permits, penalties and interest, and miscellaneous revenues are not susceptible to accrual because generally they are not measurable until received in cash. Anticipated refunds of taxes axe recorded as liabilities and reductions of revenue when they are measurable and their validity seems certain. Grants and similar items are recognized as revenues as soon as all eligibility requirements

15

1- Summary of Significant Accounting Policies (Continued)

have been met. Jn reimbursement type programs, monies must be expended on the specific purpose or project before any anwunts will be paid to the Town; therefore revenues are recognized based upon the expenditures recorded. In other programs in which monies are virtually unrestricted as to purpose of expenditiu^ and are usually revocable only for failure to comply with prescribed compliance requirements, the resources are reflected as revenues at the time of receipt or earlier if the susceptible to accrual criteria are met and all other eligibility requirements are met.

The accounts of the Town are organized on the basis of fimds, each of which is considered a separate accounting entity. The operations of each fimd are accounted for with a separate set of self-balancing accounts that conq)rise its assets, liabilities, fund balance/net assets, revenues expenditures/expenses and other changes in fund balance/net assets. The various fimds are sinnmarized by type in Uie financial statements. The following funds are used by the Town:

GoTemmental Funds -

General Fund The General Fund is the general operating fiind of the Town. It is used to account for all financial resources except those required to be accounted f in another fund.

Special Revenue Funds Special revenue fiinds are used to account for the proceeds of specific revenue sources that are legally restricted to expenditures for specific purposes. The special revenue funds consist of the Sales Tax and Streets and Sidewalks.

Debt Service Fund The Debt Service Fund is used to account for the accumulation of resources for, and the payment of,

general long-term debt principal, interest, and related costs.

Proprietary Fund -

Enterprise Fund The Enterprise Fimd is used to account for operations (a) that are financed and operated in a marmer similar to private business enterprises • where the intent of the governing body is that the costs (expenses, including depreciation) of providing goods or services to the general public on a continuing basis be financed or recovered primarily through user charges; or (b) where the governing body has decided the periodic determination of revenue earned, expenses incurred, and/or net income is appropriate for capital maintenance, public policy, management control, accountability, or other purposes. The Town applies all applicable GASB pronouncements in accounting and reporting for its govenunent-wide and business-type activities and its enterprise funds as well as the following pronouncements issued on or before November 30,1989, unless those pronouncements conflict with or contradict GASB pronouncements: Financial Accounting Standards Board Statements and interpretations, Accounting Principles Board opinions, and Accounting Research Bulletins.

Amounts reported as program revenues include (1) charges to customers or applicants for goods, services, or privileges provided, (2) operating grants and contributions, and (3) capital grants and contributions. Internally dedicated resources are reported as general revenues rather than as program revenues. Likewise, general revenues include all taxes.

16

1. Summary of Significant Accounting Policies (Continued)

Proprietary fimds distinguish operating revenues and expenses from nonoperating items. Operating revenues and expenses generally result from providing services and producing and delivering goods in coimection with a proprietary fimd's principal ongoing operations. The principal operating revenues of the enterprise fimds are charges to customers for sales and services. Operating expenses for enterprise fiinds and internal service fimds include the cost of sales and services, administrative expenses, and depreciation on capital assets. All revenues and expenses not meeting this definition are reputed as nonoperating revenues and expenses.

When both restricted and uru'estricted resources are available for use, it is the Town's policy to use restricted resources first, then unrestricted resources as they are needed.

Capital Assets Capital assets which include property, plant, equipment and infrastructure assets (e.g., roads, bridges, sidewalks, and similar items) are reported in the applicable governmental or business-type activities colunms in the govemment-wide financial statements. Capital assets are capitalized at historical cost or estimated historical cost based upon like items. The Town, a phase 3 govenunent, in accordance with GASB 34, has not retroactively reported infrastructure assets. As of July 1, 2003 the Town implemented a policy of capitalizing all infrastructure assets with a cost of $10,000 or more. All other assets are capitalized based upon a $5,000 threshold except land and construction in progress which are capitalized at cost.

The costs of normal maintenance and repairs that do not extend the assets lives or add value are not capitalized.

Capital assets are not reported in the governmental fund financial statements.

Depreciation has been provided over the estimated usefiil lives using the straight-line method. The estimated usefiil lives are as follows:

Water system 10-60 years Sewer system 5-60 years Fixtures and equipment 5-60 years Trucks and machinery 3-5 years Buildings and improvements 10-40 years

Long-Term Obligations In the govenmient-wide financial statements, and the proprietary fimd types in the fund financial statements, long-term debt and other long-term obligations are reported as liabilities in the applicable governmental activities, business-type activities, or proprietary fund type statement of net assets. Bond premiimis and discounts, as well as issuance costs, are deferred and amortized over the life of the bonds using the effective interest method. Bonds payable are reported net of the applicable bond premium or discount. Bond issuance costs are reported as deferred charges and amortized over the term of the related debt.

In the fund financial statements, governmental fund types recognize bond premiums and discoimts, as well as bond issuance costs, during the current period. The face amount of the debt issued is reported as other financing sources. Premiums received on debt issuances are reported as other financing sources while discounts on debt issuances are reported as other financing uses. Issuance costs, whether or not withheld from the actual debt proceeds received, are reported as debt service expenditures.

17

1. Sumniarv of Significant Accounting Policies (Continued)

Budgets and Budgetary Accounting The Town follows these procedures in establishing the budgetary data reflected in these financial statements:

1. The Town Qerk prepares a proposed budget and submits same to the Mayor and Board of Aldermen no later than fifteen days prior to the beginning of each fiscal year.

2. A summary of the proposed budget is published and the public notified that tiie proposed budget is available for public inspection. At the same time, a public hearing is called. This is included in minutes of the council meetings.

3. A public hearing is held on the proposed budget at least ten days after publication of the call for the hearing.

4. After the holding of the public hearing and conviction of all action necessary to finalize and inclement the budget, the budget is adopted through passage of an c»xiinance.

5. Budgetary amendments involving the transfer of fimds from one department, program or fimction to another or involving increases in expenditures resulting from revenues exceeding amounts estimated require the approval of the Board of Aldermen. All expenditures in excess of budgeted amounts are approved by the Board of Aldermen.

6. All budgetary appropriations lapse at the end of each fiscal year.

7. Budgets are adopted on a basis consistent with generally accepted accounting principles (GAAP). Budgeted amounts are as originally adopted, or as amended from time to time by the Board of Aldermen.

Investments State law and the municipality's investment policy allow tiie Town to invest in collateralized certificates of deposits, government backed securities, conunercial paper, the state sponsored investment pool and mutual funds consisting solely of government backed securities.

Investments for the Town are reported at fair value. The state investment pool (LAMP) operates in accordance with state laws and regulations.

Bad Debts Uncollectible amounts due for ad valorem taxes and customers' utility receivables are recognized as bad debts through the establishment of an allowance account at the time information becomes available which would mdicate the uncoUectibility of the particular receivable. No ad valorem taxes or customers' utility receivables were considered uncollectible at June 30,2008.

Prepaid Items Payn^nts made to vendors for services that will benefit periods beyond June 30,2008, are recorded as prepaid items.

18

1* Summary of Significant Accounting Polides (Continued)

Compensated Absences Accumulated vacation leave that is expected to be liquidated wi± expendable available financial resources is reported as an expenditure and a fiind liability of the governmental fimd that will pay it. Amounts of acctnnulated vacation leave that are not expected to be liquidated with expendable available financial resources are reported in the general long-term debt account group. No expenditure is reported for these amounts. Accumulated vacation leave of the proprietary fund is recorded as an expense and liability of that fimd as the benefits accrue to employees. In accordance witii the provisions of Statement of Fmancial Accounting Standards No. 43, Accounting for Compensated Absences, no liability is recorded for nonvesting accumulating rights to receive sick pay benefits.

Estimates The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America require management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues, exp^ditures, and expenses during the reporting period. Actual results could differ from those estimates.

Ad Valorem Taxes Ad valorem taxes attach as an enforceable lien on property as of January 1 of each year. Taxes arc levied in September and are payable upon receipt of notice. All ad valorem tax revenues are recognized in conq)liance with NCGA Interpretation - 3 and GASB Codification Section P70 (Revenue Recognition - Property Taxes) which states that such revenue is recorded when it becomes measurable and available. Available means due, or past due and receivable within die current period and collected no longer than 60 days after the close of the current period. Revenues from ad valorem taxes are budgeted in the year billed.

For the year ended June 30, 2008, taxes of 15.22 mills were levied on property with assessed valuations totaling $16,965,630 and were dedicated as follows:

General corporate purposes 5.97 mills DEQ General Obligation bonds 9.25 mills

Total taxes levied were $258,222.

3. Restricted Assets - Proprietary Fund Type The resolutions applicable to the 1977 Utility Revenue Bonds and the 2001 DEQ sales tax and revenue bonds require the establishment of various bond principal and interest sinking funds and the establishrnent of a debt service reserve fund. For fmancial reporting purposes these funds have been consolidated with the Utility Fund. Net assets of the Utility Fund have been restricted in accordance with the provision of the respective bond indentures in the amount of $113,517 at June 30, 2008, which represents the restricted assets included in the various debt service reserve funds and bond principal and interest sinking funds at that date less current liabilities payable from these restricted assets.

19

4. Changes in General Fixed Assets A summary of changes in general fixed assets for 2008 follows:

Land Buildings and inq)roveiiients Streets and traffic control equip Machinery and equipment Automobiles and trucks

Beginning Balance

116,366 1,820,708

5,935 965,051 337.196

Additions

77,671

57,916 18.999

Deletions Ending

Balance

116,366 1,898,379

5.935 1.022,967

356.195

Total general fixed assets 3.245.256

A summary of accumidated depreciation follows:

154.586

Buildings and in^rovements Machinery and equipment Automobiles and trucks

Totals

Begitming Accumulated

392,531 763,247 323.678

1.479.456

2008 Depreciation

75.003 34,093 27.827

136.923

3.399.842

Ending Accumulated

467,534 797,340 351,505

1-616.379

5. Long-Term Debt

General Obligation Bonds The Town of Many issues general obligation bonds to provide for the acquisition and construction of major capital facilities. General obligation bonds have been issued for both general government and proprietary activities. Bonds expected to be repaid from proprietary revenues are reported in the proprietary fiind. General obligation bonds are direct obligations and pledge the fiill faith and credit of the Town of Many. In June 2000. the Town autiiorized the issuance of $1,100,000 of general obligation bonds. The bcmds are issued through a Loan and Pledge Agreement with the Louisiana Department of Envux»nmental Quality (DEQ) for the purpose of primarily replacing the majority of water lines in the Town. During 2008 no additional bonds were purchased by DEQ, bringing the total purchased to date to $1,075,319. (jeneral obligation bonds outstanding at June 30, 2008, are as follows:

$1,100,000 General obligation bonds dated 12/19/00; due in annual instalhnents of $82,000 - $132,000 tiirough May 31, 2010; interest at 3.45%, plus .5% administrative fee 242.32Q

Revenue Bonds The Town of Many also issues bonds where the Town pledges income derived from the acquired or constructed assets to pay the debt service. Revenue bonds outstanding at June 30, 2008, are comprised of the following:

20

5. Long-Term Debt (Continued)

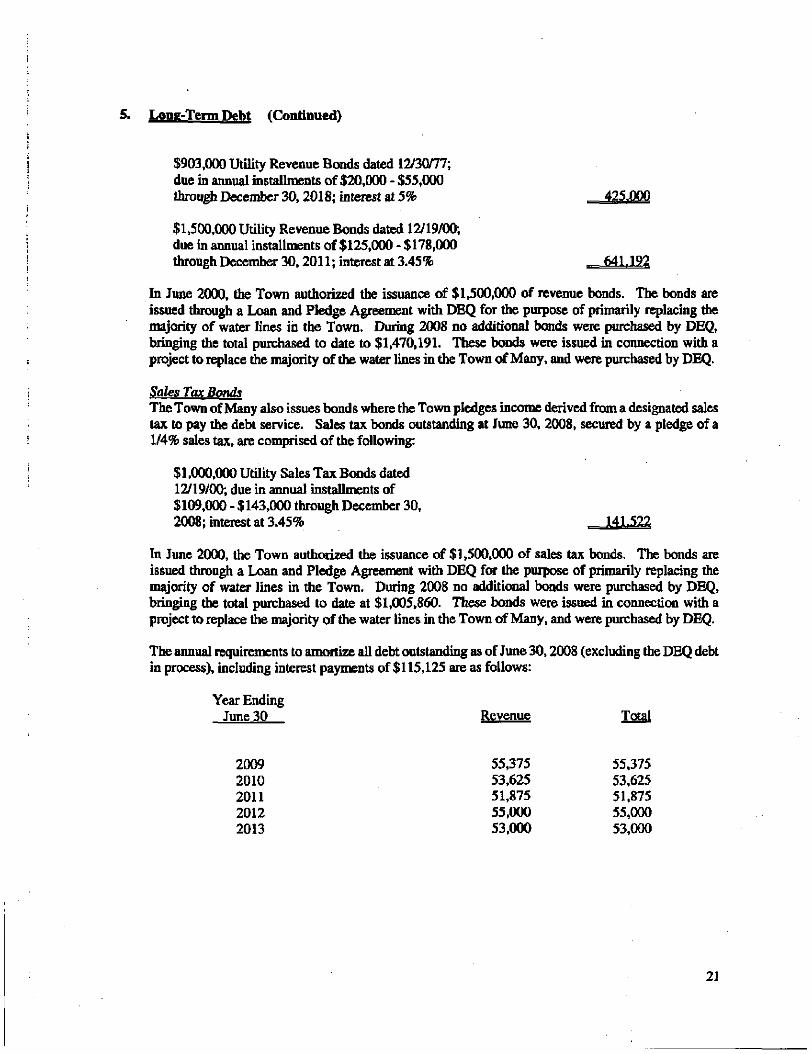

$903,000 UtiUty Revenue Bonds dated 12/30/77; due in annual installments of $20,000 - $55,000 tiu-ough December 30.2018; mterest at 5% 425.000

$1,500,000 Utility Revenue Bonds dated 12/19/00; due in annual installments of $125,000 - $178,000 tiuough December 30,2011; interest at 3.45% 641.192

In June 2000, tiie Town authorized the issuance of $1,500,000 of revenue bonds. The bonds are issued through a Loan and Pledge Agreement with DEQ for the purpose of primarily replacing the majority of water lines in the Town. During 2008 no additional bonds were purchased by DEQ, bringing the total purchased to date to $1,470,191. These bonds were issued in cormection with a project to replace die majority of the water lines in the Town of Many, and were purchased by DEQ.

Sales Tax Bonds The Town of Many also issues bonds where the Town pledges income derived from a designated sales tax to pay the debt service. Sales tax bonds outstanding at June 30, 2008, secured by a pledge of a 1/4% sales tax, are comprised of the following:

$1,000,000 Utility Sales Tax Bonds dated 12/19/00; due in aimual installments of $109,000 - $143,000 through December 30. 2008; interest at 3.45% 141.522

In June 2000, the Town authorized the issuance of $1,500,000 of sales tax bonds. The bonds are issued through a Loan and Pledge Agreement with DEQ for the purpose of primarily replacing the majority of water lines in the Town. During 2008 no additional bonds were purchased by DEQ, bringing the total purchased to date at $1,005,860. These bonds were issued in connection with a project to replace the majority of the water lines in the Town of Many, and were purchased by DEQ.

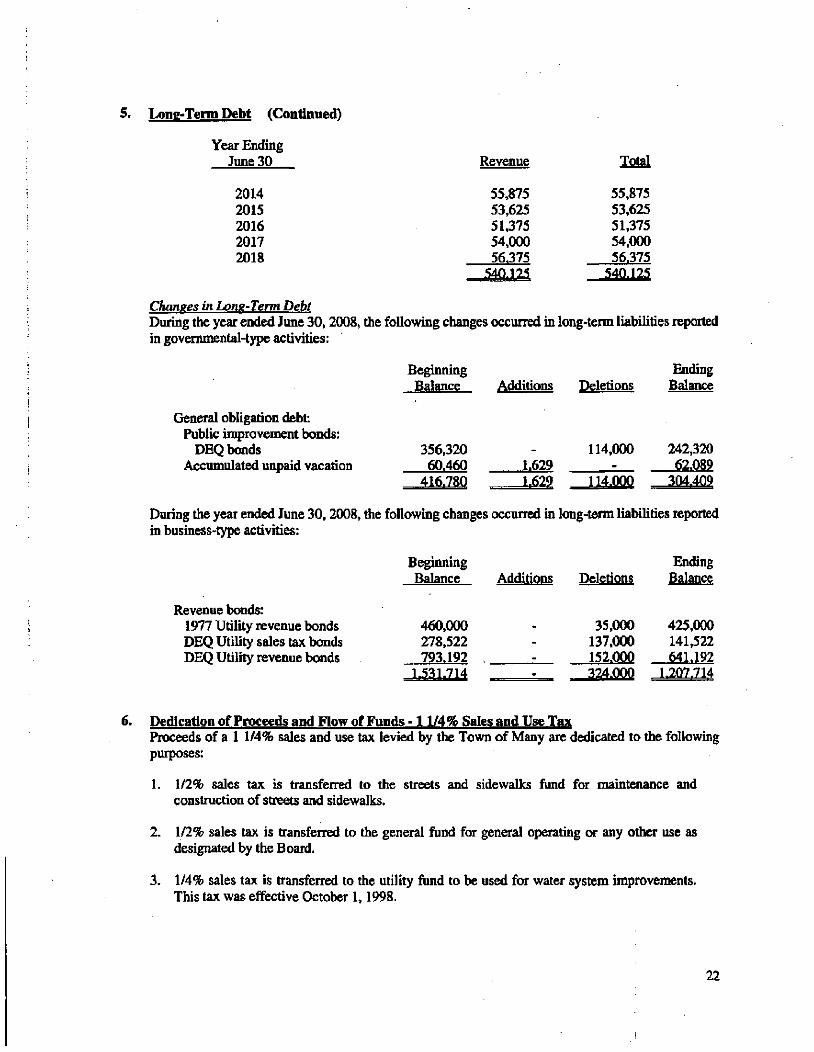

The armual requirements to amortize all debt outstanding as of June 30,2008 (excluding the DEQ debt in process), including interest payments of $115,125 are as follows:

Year Ending June 30 Revenue Total

2009 2010 2011 2012 2013

55,375 53,625 51,875 55,000 53,000

55,375 53,625 51,875 55,000 53,000

21

5. Long-Term Debt (Continued)

Year Ending June 30

2014 2015 2016 2017 2018

Revenue Total

55,875 53,625 51,375 54,000 56,375

540.125

55,875 53.625 51.375 54,000 56,375

S4ftll?5

Changes in Long-Term Debt During the year ended June 30,2008, the following changes occurred in long-term liabilities reported in govemmental-type activities:

General obligation debt: Public improvement bonds:

DEQ bonds Accumulated unpaid vacation

Beginning Balance

356,320 60.460

416,780

Additions

1,629 1,62?

Deletions

114,000

114.000

Elding Balance

242,320 62.089

304.409

During the year ended June 30,2008. the following changes occurred in long-term liabilities reported in business-type activities:

Revenue bonds: 1977 Utility revenue bonds DEQ Utility sales tax bonds DEQ Utility revenue bonds

Beginning Balance

460,000 278.522 793.192

1.531.714

Additions

-

-

Deletions

35,000 137,000 152.000 324.000

Ending Balance

425,000 141,522 641.192

1.207.714

6. Dedication of Proceeds and Flow of Funds -11/4% Sales and Use Tax Proceeds of a 1 1/4% sales and use tax levied by the Town of Many are dedicated to the following purposes:

1. 1/2% sales tax is transferred to the streets and sidewalks fund for maintenance and construction of streets and sidewalks.

2. 1/2% sales tax is transferred to the general fund for general operating or any other use as designated by the Board.

3. 1/4% sales tax is transferred to the utility fund to be used for water system improvements. This tax was effective October 1,1998.

22

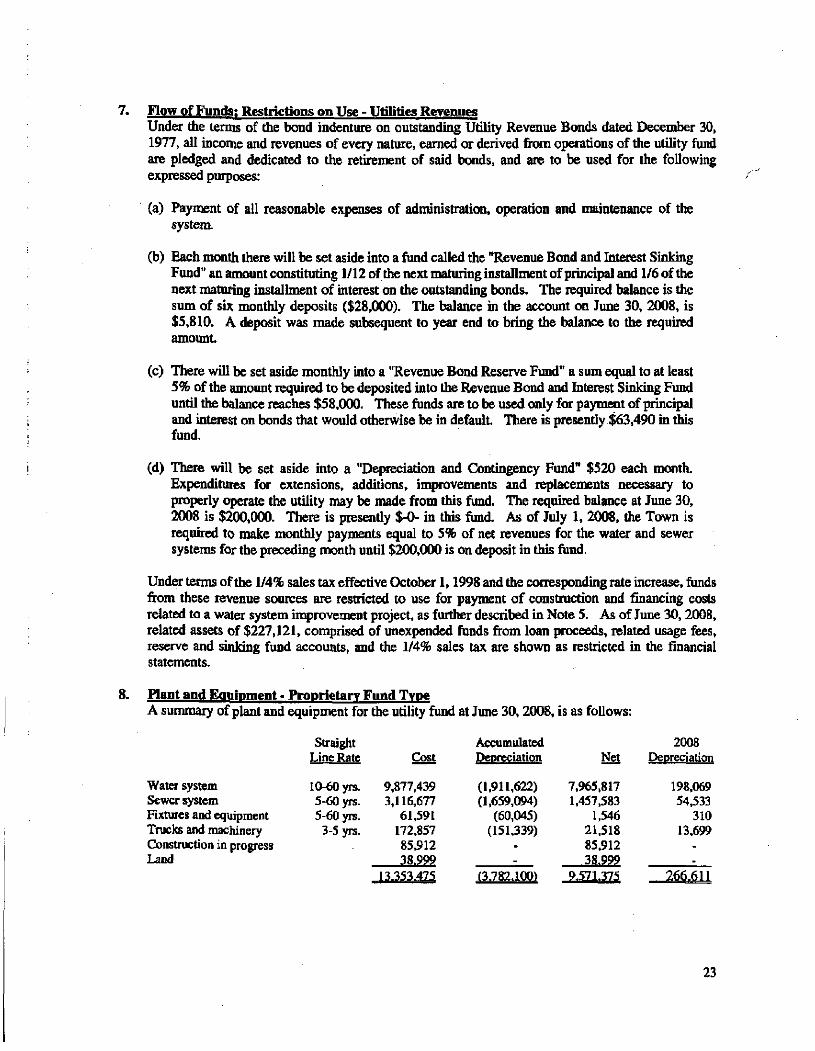

Flow of Funds; Restrictions on Use - Utilities Revenues Under the terms of the bond indenture on outstanding Utility Revenue Bonds dated December 30. 1977, all income and revenues of every nature, earned or derived fixtm operations of the utility fund are pledged and dedicated to the retirement of said bonds, and are to be used for the following expressed purposes:

(a) Payment of all reasonable expenses of administration, operation and maintenance of the system.

(b) Each month there will be set aside into a fimd called the "Revenue Bond and Interest Sinking Fund" an amount constituting 1/12 ofthe next maturing installment of principal and 1/6 of the next maturing installment of interest on the outstanding bonds. The required balance is the sum of six monthly deposits ($28,000). The balance in the account on June 30, 2008, is $5,810. A deposit was made subsequent to year end to bring the balance to the required amount.

(c) There will be set aside monthly into a "Revenue Bond Reserve Fund" a sum equal to at least 5% of the amount required to be deposited into the Revenue Bond and Interest Sinking Fund imtil the balance reaches $58,000. These fiinds are to be used only for payment of principal and interest on bonds that would otherwise be in default There is presentiy $63,490 in this fund.

(d) There will be set aside into a "Depreciation and Contingency Fund" $520 each month. Expenditures for extensions, additions, improvements and replacements necessary to properly operate the utility may be made from this fund. The required balance at June 30, 2008 is $200,000. There is presently $-0- in this fimd. As of July 1, 2008, die Town is required to make monthly payments equal to 5% of net revenues for the water and sewer systems for the preceding month until $200,000 is on deposit in this fiind.

Under terms ofthe 1/4% sales tax effective October 1,1998 and the corresponding rate increase, fiinds from these revenue sources are restricted to use for payment of construction and financing costs related to a water system in^rovement project, as further described in Note 5. As of June 30,2008, related assets of $227,121, conq)rised of unexpended funds from loan proceeds, related usage fees, reserve and sinking fund accounts, and the 1/4% sales tax are shown as restricted in the fmancial statements.

Plant and Equioment • Proprietary Fund Type A summary of plant and equipment for the utility fund at June 30,2008. is as follows:

Water system Scwcr system Fixtures and equipment Trucks and machinery Construction in progress Land

Straight Line Rate

10-60 yre. 5-60 yrs. 5-60 yrs.

3-5 yrs.

Cost

9.877.439 3,116.677

61,591 172,857 85.912 38.999

Accumulated Dqireciation

(1,911,622) (1,659,094)

(60,045) (151,339)

--

Net

7,965,817 1.457.583

1.546 21,518 85,912 38.999

2008 Depreciation

198.069 54,533

310 13.699

-.

n.353.475 f -782.10Q^ %57hm

23

Cost

12,830,987

1.449.322

(90,850) (835,984)

l^.\S:i,475

Accumulated Depreciation

(3,518,517)

-

3.028

r266.6in (^.782.100^

m 9.312,470

1,449,322

(87,822) (835,984) (266.610

9^71,375

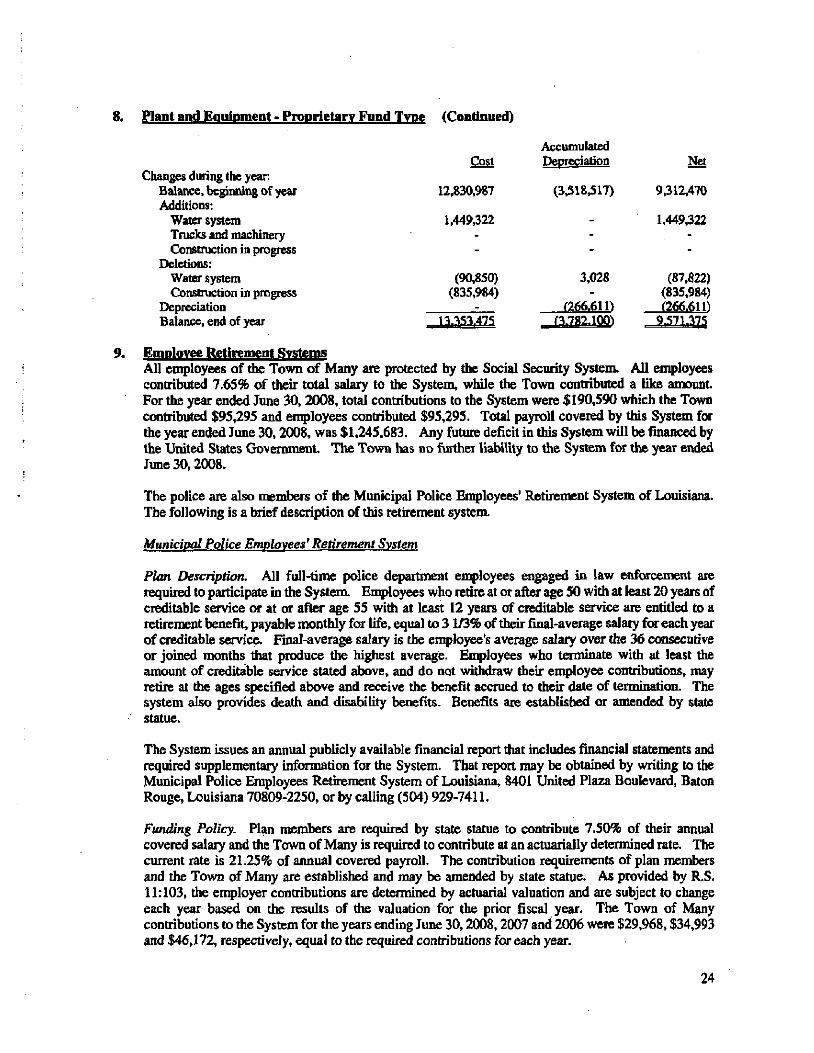

8. Plant and Equipment - Proprietary Fund Tvue (Continued)

Changes during the year: Balance, beginning of year Additions:

Water system Trucks and machinery Construction in progress

Deletions: Water system Construction in progress

Depreciation Balance, end of year

9. Employee Retirement Systems All enqjloyees of die Town of Many are protected by the Social Security Systent All eii >loyees contributed 7.65% of their total salary to the System, while the Town contributed a Uke amount For the year ended June 30.2008. total contributions to the System were $190,590 which the Town contributed $95,295 and en^)loyees contributed $95,295. Total payroU covered by this System for the year ended June 30.2008, was $1,245,683. Any future deficit in this System will be financed by the United States Government. The Town has no fiirther liability to the System for the year ended June 30, 2008.

The police are also members of the Municipal Police Employees' Retirement System of Louisiana. The following is a brief description of this retirement systenL

Municipal Police Employees* Retirement System

Plan Description. All firil-time police department employees engaged in law enforcement are required to participate in the System. Employees who retire at or after age 50 with at least 20 years of creditable service or at or after age 55 with at least 12 years of creditable service are entitled to a retirement benefit, payable nx)nthly for life, equal to 3 1/3% of their final-average sala^ for each year of creditable service. Final-average salary is the eixqjloyee's average salary over the 36 consecutive or joined months that produce the highest average. En^loyees who terminate with at least the amount of creditable service stated above, and do not withdraw their en^loyee contributions, may retire at the ages specified above and receive the benefit accrued to their date of termination. The system also provides death and disability benefits. Benefits are established or amended by state statue.

The System issues an annual publicly available financial report that includes financial statements and required supplementary information for the System. That report may be obtained by writing to the Municipal Police Employees Retirement System of Louisiana, 8401 United Plaza Boulevard, Baton Rouge. Louisiana 70809-2250. or by calling (504) 929-7411.

Funding Policy. Plan members are required by state statue to contribute 7.50% of their annual covered salary and the Town of Many is required to contribute at an actuarially determined rate. The current rate is 21.25% of armual covered payroll. The contribution requirements of plan members and the Town of Many are established and may be amended by state statue. As provided by R.S. 11:103, the employer contributions are determined by actuarial valuation and are subject to change each year based on the results of the valuation for the prior fiscal year. The Town of Many contributions to the System for the years ending June 30.2008.2007 and 2006 were $29,968, $34,993 and $46,172, respectively, equal to the required contributions for each year.

24

9. Employee Retirement Systems (Continued)

Municipal Employees'Retirement System

Plan description. Substantially all fuU-time en^loyees except poUce of tiie Town of Many are covered imder the Municipal Enq>loyees' Retirement System of Louisiana, (the "System") a cost sharing multiple employer public employee retirement system, controlled and administered by the Board of Trustees of the System. The System is mandatory for all employees who are employed on a permanent basis working at least 35 hours per week. Benefits are established by State statutes. The System issues a publicly available financial report that includes financial statements and required supplementary ii^ormation. That report may be obtained by writing the Board of Trustees. 7937 Office Park Blvd., Baton Rouge, Louisiana 70809, or by calling (504) 925-4810.

Funding Policy. Covered employees are required to contribute 5.0% of their annual compensation and the Town is required to contribute 6.75% of annual con^nsation. The contribution requirements are established and may be amended by State statute. The Town's contributions to the System for die years ended June 30. 2008 and 2007 were $24,951 and $40,750. which equal tiie required contributions for each year in accordance with GASB Statement No. 27. Accounting for Pensions by State and Local Governmental Employees. The net pension obligation was determined to be zero. Prior to adoption of GASB 27, the Town did not report a pension liability.

10. Receivables and Due from Other Goyenunents Receivables as of June 30,2(X)8, consisted ofthe following:

Customers Taxes Other Total

Governmental activities: General - 51.387 11.017 62,404 Special Revenue-

Sales tax - 116.224 - 116,224 Street - - 90 90

Debt service - - 78 78 Total governmental - 167.611 11.185 178.796

Included in taxes in the general fund is $3,320 due from the State of Louisiana for beer taxes. Also, $18,593 is reOected on the Statement of Net Assets as due from <Mher governments which is $3,8(X) due from the State of Louisiana ioc mowing, and $ 14,793 of grant receivables.

The receivables reflected in the Statement of Net Assets in the business-type activity is $183,074 from customers for utility billings, $ 1,345 of other receivables and $595,577 of grant receivables iae a total of $779,996.

11. Obligations under Leases The Town was not obligated under any capital lease commitments at June 30, 2008.

12. Litigation The Town is a party to legal proceedings involving suits filed against the Town for various reasons, however Town management does not believe the Town is exposed to any material losses in these proceedings. Accor^gly, no provision for losses is included in the financial statements.

25

13. Cash and Investments Louisiana Revised Statutes authorize the Town to invest in United States bonds, treasury notes or certificates, or to deposit fimds in demand deposits, interest bearing demand deposits, money market accoimts. or time d^>osits with state banks organized und^ Louisiana law and national banks having their principal offices in Louisiana.

Cash equivalents include all short term highly liquid investments that are readily convertible to known amounts of cash and are so near their maturity that they present insignificant risk of changes in value because of interest rates. Generally, only investments which, at the date of purchase, have a maturity date no longer than three months qualify under this definition.

At June 30.2008, the Town of Many rqxsrted cash and investments as follows:

Unrestricted Restricted Total

Cash 251.446 57.606 309,052 Investmente - 139,809 139.809

251.446 197.415 448.861

Investments consist of certificates of deposit.

The bank balances of cash and investments at June 30,2008. was $524,810. Of this total. $138,183 was secured through federal depository insurance and $386,627 was secured by the pledge of securities ($386,627 par value) owned by the depository banks. These securities are held in the name of the pledging banks in a custodial bank that is mutually acceptable to both parties. These secured deposits are considered uncollateralized (Category 3) under the provisions of GASB Statement 40; however. Louisiana Revised Statutes require the custodial bank to advertise and sell the pledged securities within ten (10) days of being notified by the Town that the pledgmg bank has failed to pay deposited funds upon demand. The Town's deposits were fiilly insured or collateralized at June 30. 2008.

14. Retained Earnings A portion of retained earnings is reserved to cover certain restricted assets pledged for future debt service on the revenue bonds issued by the Utility Fund, and on fimds collected in cormection with the above water line improvement project.

15. Compensation Paid to Mayor and Aldermen In accordance with the requirements of the Office of the Legislative Auditor. State of Louisiana, the following reflects compensation paid to the Mayor and member of the Town Council for the year ended June 30, 2008:

Mayc» Kenneth Freeman 24,000

Aldermen: Barbara Peterson 6.300 L D. Bostian 6.000 John Hoagland 6.000 Jeanette Dean 6.000 James D. Kennedy 6.000

26

16. Interfund Receivables and Payables A summary of interfund receivables and payables at June 30,2008 follows:

General Fund - Due From/To Utility fund Sales tax fund Street fund Debt service fund

Street and Sidewalks Fund - Due From Utility fund Sales tax fimd General fimd

Sales Tax Fund - Due To General fimd Street fimd Utility fund

Debt Service Fund - Due From (jeneral fimd Utility fimd

Utility Fund - Due To/From Genera] fiind Sales tax fund Debt service fimd Street fund

Receivable

913,184 93,739

308.907 92.688

164,988

-

310.202

29.706 99,866

jzmnm

Payable

164,988 310,202

-

93.739 92,688 29.706

99.866

913.184

308.907 2,0I3,;«Q

17. Risk Management The Town is exposed to various risks of loss related to torts; theft of. damage to, and destruction of assets; errors and omissions; injuries to employees; and natural disasters. The Town has purchased commercial insurance to cover or reduce the risk of loss that might arise should one of these incidents occur. No settiements were made during the current or prior three fiscal years that exceeded the Town's insurance coverage. The Town's management has not purchased commercial insurance or made provision to cover or reduce the risk of loss as a result of business interrupdon and certain acts of God.

18. Restatement The General Fund's beginning net assets were decreased $136,343. Accrued liabilities were inadvertently understated in the statement in 2007 due to an accounting error in recording those liabilities.

27

REOUIRED SUPPLEMENTARY INFORMATION (UNAUDITED^

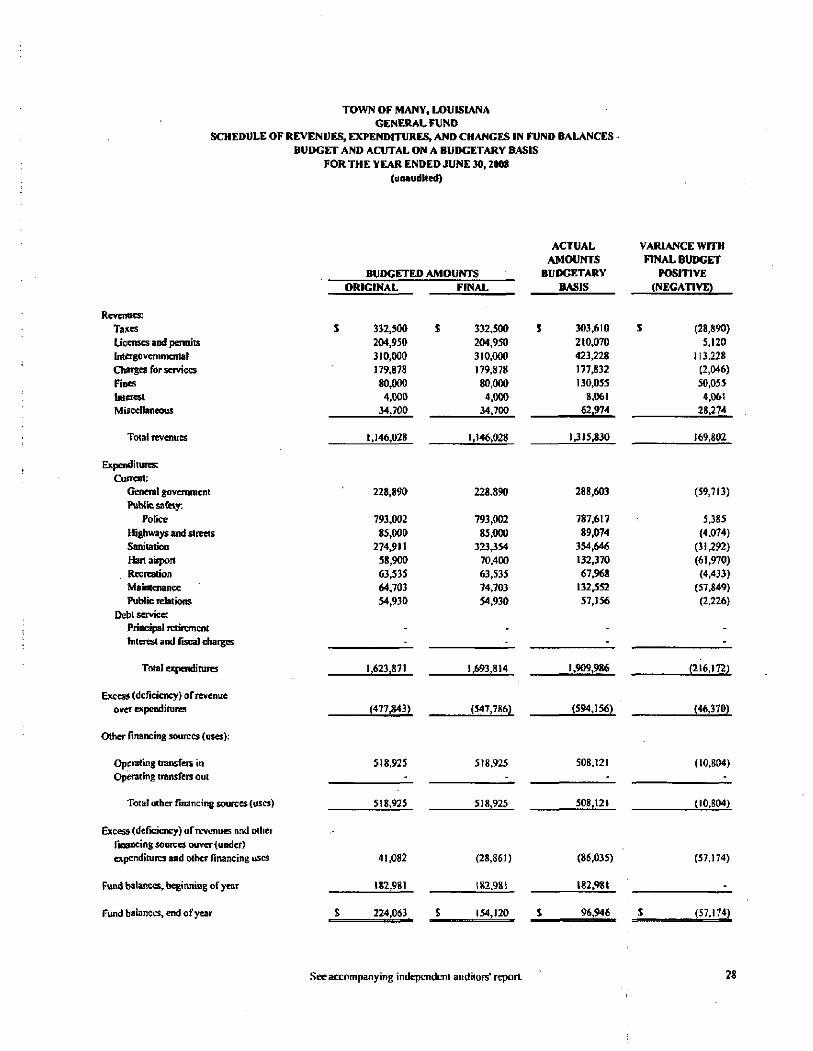

TOWN OF MANV, LOUISIANA GENERAL FUND

SCHEDULE OF REVENUES, EXPENDITURES. AND CHANGES IN FUND BALANCES BUDGET AND ACITTAL ON A BUDGETARY BASIS

FOR THE VEAR ENDED JUNE 30,200S (unaudited)

Revenues; Taxes Licenses and pennits Intergovernmental Charges for services Fines Interest Miscellaneous

Total revenues

BUDGETED AMOUNTS ORIGINAL

S 332^00 204.950 310.000 179.878 80,000 4,000

34,700

1,146,028

FINAL

$ 332,500 204,950 310,000 179.878 80,000 4.000

34.700

1,146,028

ACTUAL AMOUNTS

BUDGETARY BASIS

S 303,610 210,070 423,228 177.832 130,055

8,061 62.974

1315,830

VARIANCE WITH FINAL BUDGET

POSITIVE (NEGATIVE)

$ (28,890) 5,120

113.228 (2.046) 50.055 4,061

28,274

169,802

Expenditures: Cunvnt:

General govenunent Public safety:

Police Highways and streets Sanitation Hart atrpoil Recreation Maintenance

Public relations Debt service:

Piincipal retirement Interest and Hscal charges

Total expenditures

Excess (deficiency) of revenue over expenditures

Other financing sources (uses):

228.890 228.890 288.603 (59,713)

793,002 85,000

274,911 58,900 63.535 64,703 54,930

1,623,871

(477,843)

793,002 85,000

323,354 70,400 63,535 74,703 54.930

1,693,814

(547,786)

787,617 89,074

354,646 132.370 67,968

132,552 57,156

1.909,986

(594,156)

5485 (4,074)

(31 ^?2) (61,970) (4,433)

(57.849) (2,226)

(216,172)

(46,370)

Op^ruting transfers in Operating transfers out

Total other financing sources (uses)

Excess (deficiency) of revenues and other flnancing sources ouver (under) expenditures and other financing uses

Fund balances, beginning of year

Fund balances, end of year

518.925 518,925 508,121 (10,804)

s

518,925

41.082

182,981

224,063 S

518,925

(28.861)

182.981

154,120 S

508.121

(86.035)

182,981

96,946

(10.804)

(57.174)

(57.174)

See accompanying independent auditors' report 28

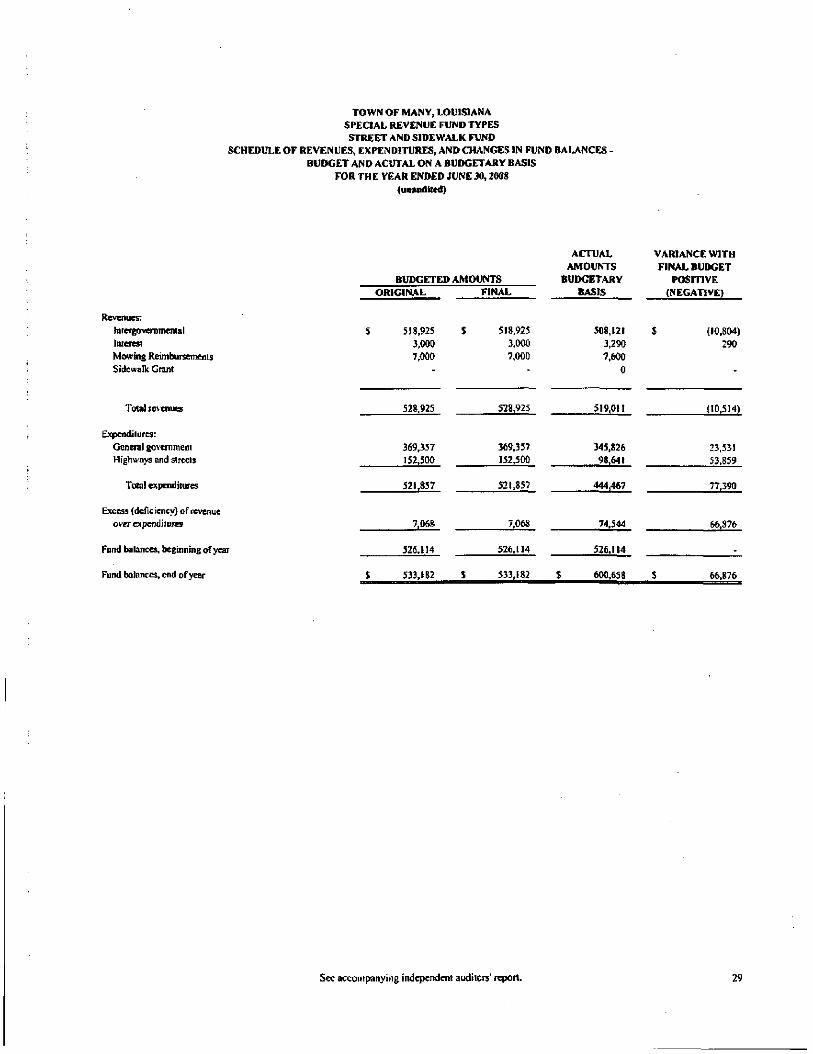

TOWN OF MANY, LOUISIANA SPECIAL REVENUE FUND TYPES STREET AND SIDEWALK FUND

SCHEDULE OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BAIJVNCES BUDGET AND ACUTAL ON A BUDGETARY BASIS

FOR THE VEAR ENDED JUNE 30,2008 (un»tidiied)

Revenues: hiiergovemnKntal Interest Mowing Reimbursemenis Sidewalk Grant

Total re\'cnues

Expenditures: General government Highways and streets

Total expenditures

Excess (deficiency) of revenue over expenditures

Fund balances, beginning of year

Fund balances, end ofyear

BUDGETED AMOUNTS ORIGINAL

S 518,925 3.000 7.000

528.925

369,357 152,500

521,857

7,068

526.114

$ 533.182

S

S

FINAL

518,925 3.000 7.000

528,925

369.357 152,500

521,85?

7,068

526.114

533,182

ACTUAL AMOUNTS

BUDGETARY BASIS

508,121 3,290 7.600

0

519,011

345.826 98,641

444,467

74.544

526.114

$ 600.638

VARIANCE WITH FINAL BUDGET

POSITIVE (NEGAtlVE)

$ (10,804) 290

-

(10.514)

23,531 53.859

77,390

66,876

_

S 66,876

Sec accompanying independent auditors' report. 29

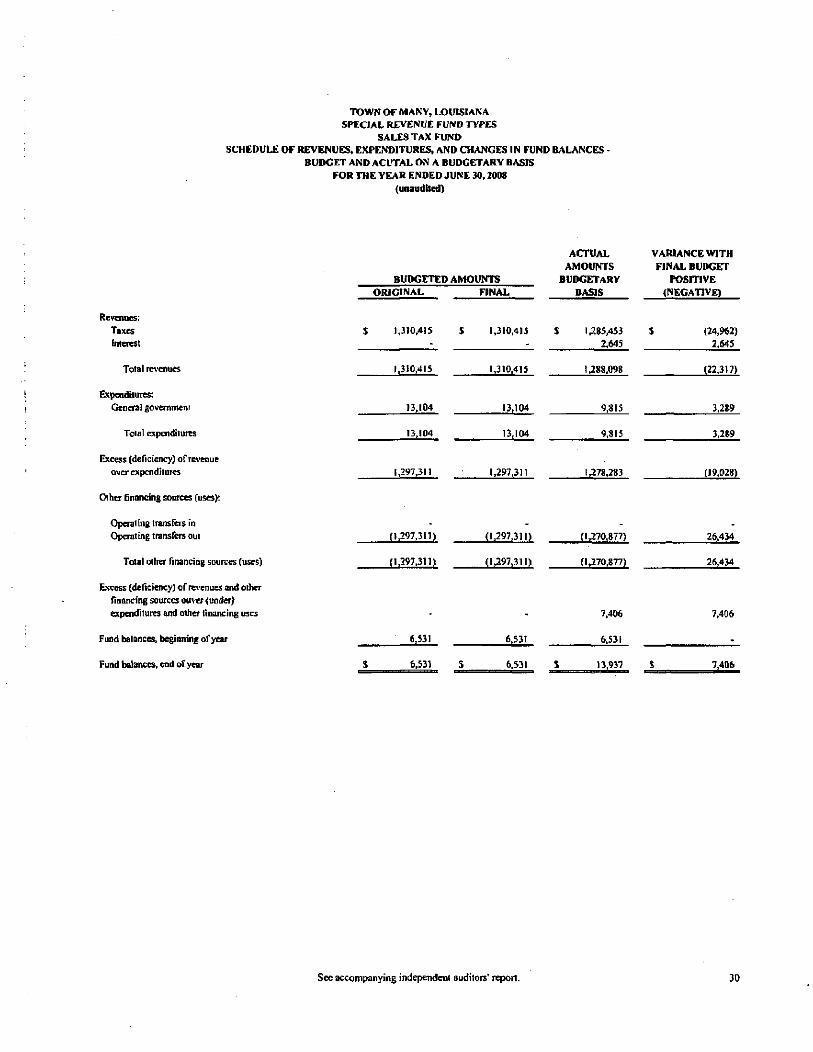

TOWN OF MANY, LOUISIANA SPECIAL REVENUE FUND TYPES

SALES TAX FUND SCHEDULE OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCES

BUDGET AND ACUTAL ON A BUDGETARY BASIS FOR THE YEAR ENDED JUNE 30,2008

(unaudited)

Revenues: Taxes

Interest

Total re\'enues

Expenditures: General govemmenr

Total expenditures

Excess (deficiency) of rcA-enue over expenditures

BUDGETED AMOUNTS ORIGINAL

$ 1,310.415

-

1,310,415

13.104

13.104

1,297,311

$

FINAL

1.310.4 IS

-

1,310.415

13.104

13,104

1,297,311

ACTUAL AMOUNTS

BUDGETARY

BASIS

$ 1,285,453 2,645

1,288.098

9.815

9.S15

1,278,283

VARIANCE WITH FINAL BUDGET

POSITIVE (NEGATIVE)

S (24.962)

2,645

(22.317)

3,289

3.289

(19,028)

Other financing sources fuses):

Operating transfers in C^>cnttlng transfers out

Total other financing sources (uses)

(1.297.311)

(1.297,3in

(1,297.311)

(U97.311)

(1^70.877)

(1,270.877)

26.434

26,434

Excess (deficiency) of revenues and other financing sources ou^^er (under) expenditures and other financing uses

Fund balances, beginning ofyear

Fund balances, end ofyear

6,531

6,531

A53I

6.531

7,406

6.5 31

13.937

7,406

7.406

See accompanying independent auditors' report. 30

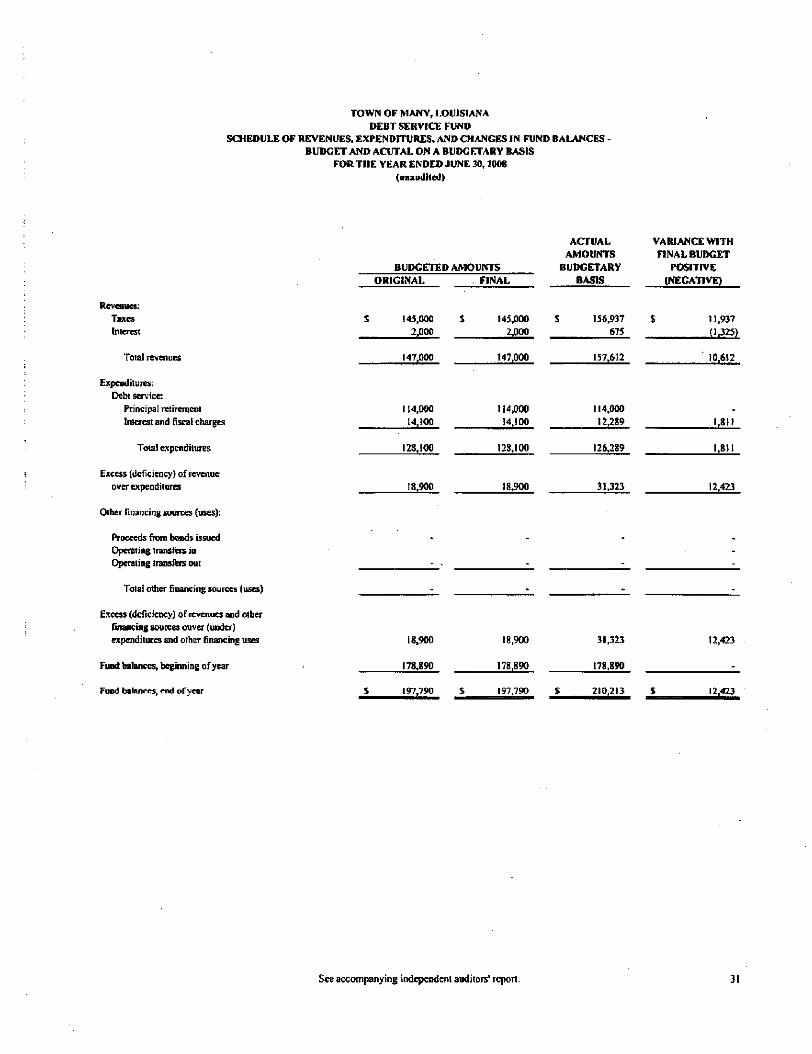

TOWN OF MANY, LOUISIANA

DEBT SERVICE FUND SCHEDULE OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCES

BUDGET AND ACUTAL ON A BUDGETARY BASIS FOR THE YEAR ENDED JUNE 30,2008

(nnaudlted)

Revenues: Taxes

Interest

Total revenues

BUDGETED AMOUNTS

ORIGINAL

S 145.000 2.000

147.000

s

FINAL

145,000 2,000

147.000

ACTUAL

AMOUNTS

BUDGETARY BASIS

S 156,937 675

157,612

VARIANCE WITH

FINAL BUDGET

POSITIVE (NEGATIVE)

$ 11.937

(1,325)

10,612

Expenditures: Debt service:

Principal retirement Interest and fiscal charges

Total expenditures

Excess (deficiency) of re\'enue over expenditures

114,000 14,100

128.100

18,900

114,000 14,100

128,100

18.900

114.000 12,289

126,289

31,323

-1,811

1,811

12.423

Other financing sources (uses):

Proceeds fiotn bonds issued Operating transfers in Operating transfers out

Total other financing sources (uses)

Excess (deficiency) of revenues and other financing sources ouver (under) expenditures and other financing uses

Fund balances, beginning ofyear

Fund balances, md or year s

18.900

178,890

197,790 S

18.900

178,890

197.790 £

31,323

178.890

210,213

12.423

12.423

See accompanying independent attditors' report. 31

TOWN OF MANY. LOUISIANA

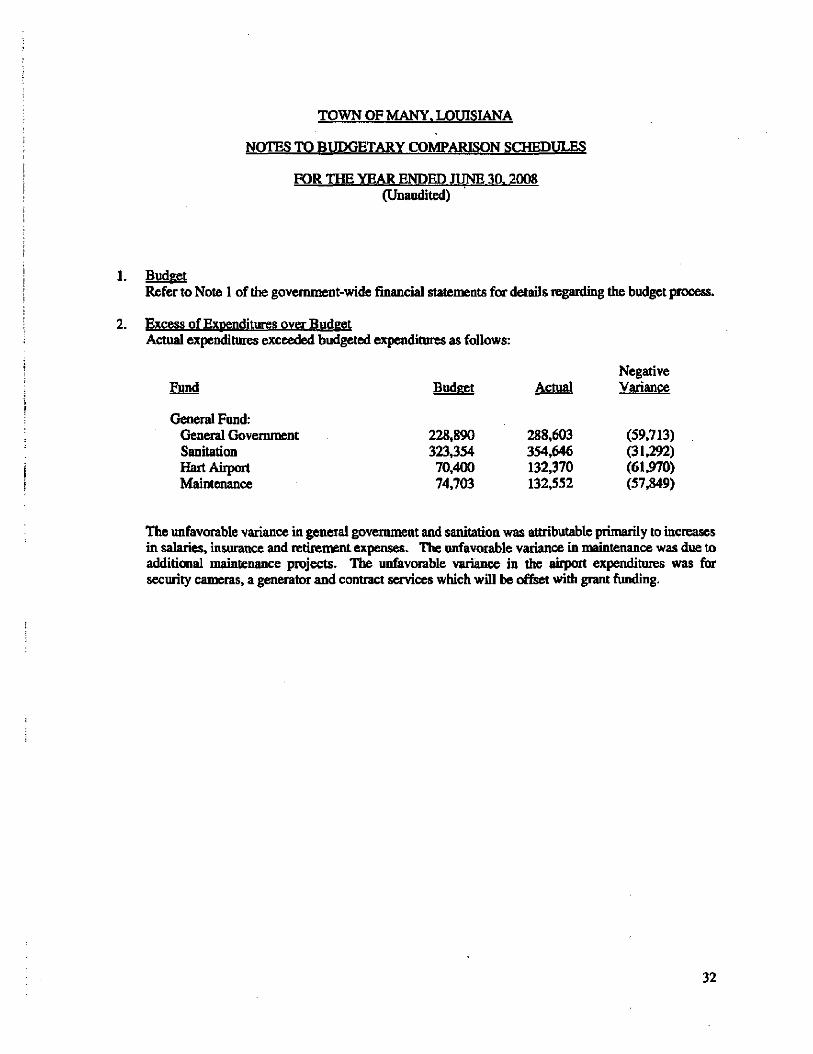

NOTES TO BUDGETARY COMPARISON SCHEDULES

FOR THE YEAR ENDED JUNE 30.2008 (Unaudited)

1. Budget Refer to Note 1 of the govenunent-wide financial statements for details regarding the budget process.

2. Excess of Expenditures over Budget Actual expenditures exceeded budgeted expenditures as follows:

Negative Fund Budget Actual Variance

General Fund: General Government 228.890 288,603 (59,713) Sanitation 323,354 354,646 (31,292) Hart Airport 70,400 132,370 (61,970) Maintenance 74,703 132,552 (57,849)

The unfavorable variance in general government and sanitatioa was attributable primarily to increases in salaries, insurance and retirement expenses. The unfavorable variance in maintenance was due to additional maintenance projects. The unfavorable variance in the airport expenditures was for security cameras, a generator and contract services which will be offset with grant funding.

32

OTHER REPORTS

H E A R D M C E L R O Y 6c VESTAL

LLP CERTIFIED PL'BUC ACCOUNTAKTS

333 TEXAS STREET

15TH FLOOR

SHRKVEPORT, LA 7U01

318 429-1525 318 429-2070 FAX POST OFFICE BOX 1 6 0 7

SHREVfcTORT, LA

71165-1607

PARTNERS

SPENCER BERNARD, JR., CPA H.Q. GAIIAGAA, JH., CFA, APC GERALD W. HEnococK, JR. , CPA, APC TIM B . NrtLSEN, CPA, APC JOHN W . DEA.N. CPA, APC MARK D . EIDREHCE, CPA ROBERT L. DEAN, CI'A STEPHEN W . CRAIG, CM

ROY E . PRESTWOOD, CPA

A. D. JOHNSON, JR., CPA

BENJAMIN C. WOODS, CPA/ADV, CVA

AucE V. FKAZIER, CPA

MEUSSA D . MrrcHA.M, CPA, CFI'

O F COUNSEL

GILBERT R. SHANLEY. JR., CPA

C. CODY WHITE, JK., CPA, APC

Ro.N' W. STEWART, CPA, APC

February 28, 2009

The Honorable Kenneth Freeman, Mayor Board of Aldermen Town of Many Many, Louisiana

Report on Internal Control over Financial Reporting and on Compliance and Other Matters

Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards

We have audited the fmancial statements of the Town of Many as of and for the year ended June 30,2008. and have issued our report thereon dated February 28, 2009. We conducted our audit m accordance with auditing standards generally accepted in the United States of America and the standards applicable to &iancial audits contamed in Government Auditing Standards, issued by the Con:q>troller General of the United States.

Internal Control OverKnancial Reporting

In planning and performing our audit, we considered the Town's internal control over financial reporting as a basis fcv designing our auditing procedures for the purpose of expressing our opinion on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of the Town's internal control over financial repeating. Accordingly, we do not express an opinion on the effectiveness of the Town's internal control over financial reporting.

Our consideration of internal control over financial reporting was for the limited purpose described in the preceding paragraph and would not necessarily identify all deficiencies in internal control over financial reporting that might be significant deficiencies or material weaknesses. However, as described below, we identified certain deficiencies in internal control over financial reporting that we consider to be significant deficiencies.

A conorol deficiency exists when the design c»- operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent or detect misstatements on a timely basis. A significant deficiency is a control deficiency, or combination of control deficiencies, that adversely affects the entity's ability to initiate, authorize, record, process, or report financial data reliably in accordance with generally accepted accounting principles such that there is more than a remote likelihood that a misstatement ofthe entity's financial statements that is more than inconsequential will not be prevented or detected by the entity's internal control. We consider the deficiencies described in the accompanying schedule of findings and responses as items 2008-1 and 2008-2 to be significant deficiencies in internal control over financial reporting.

HVIV A PROI-ESSIONAL SERVICES FIRM SHRFVTPORT • ^ v s j MONROE

hmv0hmvcpa.com E-MAH. \%TV\v.hmvcpa.com Wi-n ADIJRKSS

33

A material weakness is a significant deficiency, or conibinarion of significant deficiencies, that results in more than a remote likelihood that a material misstatement of the fmancial statements will not be prevented or detected by the entity's mtemal control.

Our consideration of the mtemal control over financial reporting was for the limited purpose described in the first paragraph of this section and would not necessarily identify all deficiencies in tl^ internal control that mi^t be significant deficiencies and, accordingly, would not necessarily disclose all significant deficiencies that are also considered to be material weaknesses. Howev^, of the significant deficiencies described above, we consider item 2008-1 to be a material weakness.

Compliance and Other Matters

As part of obtaining reasonable assurance about whether the Town's financial statements are free of material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on coiiq>liance with those provisions was not an objective of our audit and, accordingly, we do not express such an opinion. The results of our tests disclosed one instance of noncon^liance or other matters tluit are required to be reported under Government Auditing Standards and which are described in the accompanying schedule of findings and responses as item 2008-3.

This report is intended solely for the information and use of the Mayor, management, Board of Alderman, and federal awarding agencies and pass-through instances, and is not intended to be and should not be used by anyone other than these specified parties.

Thsu , r{ \ '&^ ivuU.uiP

34

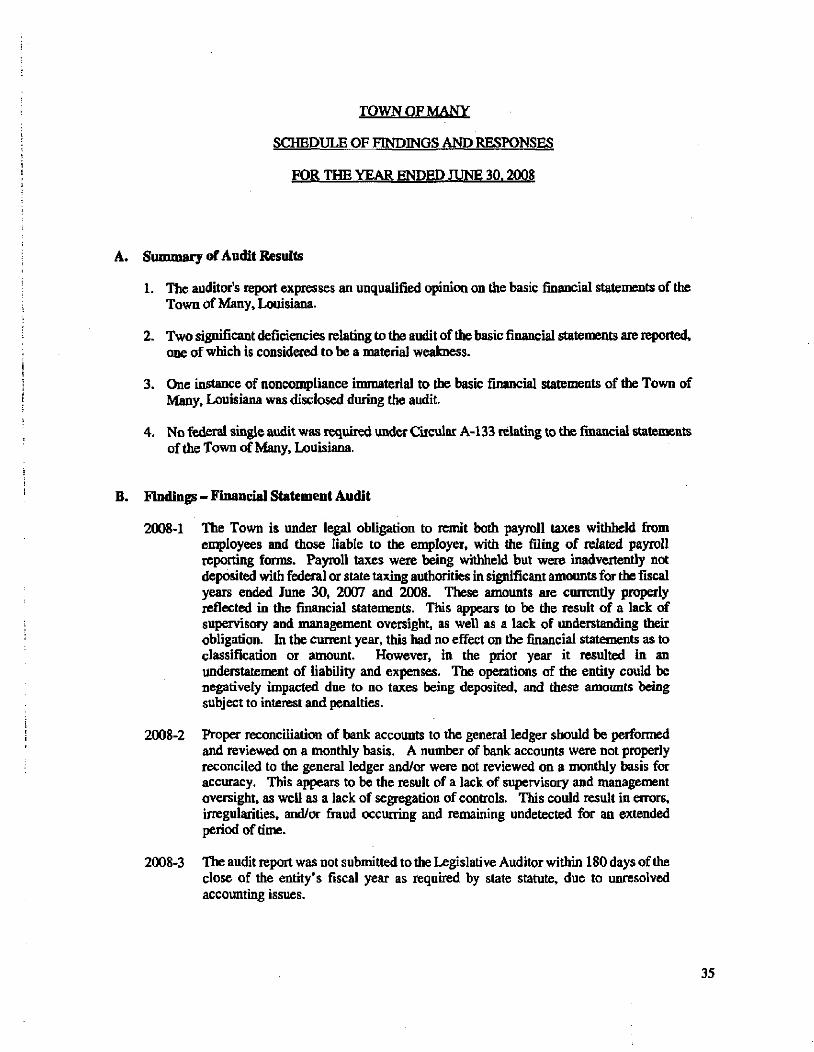

TOWN OF MANY

SCHEDULE OF FINDINGS AND RESPONSES

FOR THE YEAR ENDED JUNE 30.2008

A. Sumroaiy of Audit Results