28432 expert perspectives - advisory › ... › 28432_expert_perspectives_fullversi… · 4 |...

TRANSCRIPT

28432

2445 M Street NW, Washington DC 20037

P 202.266.5600 | F 202.266.5700advisory.com

Perspectivesexpert

spring 2014 | volume 2

THE TraNSiTioN To

PopulationHealth

Note to readers

Michael Koppenheffer

Executive DirectorResearch and Insights

Not so long ago, the most common questions we heard from our members concerned the transition from fee-for-service medicine to value-based care—and these questions ultimately boiled down to, “Should we?”

Today, the value-based care transition remains at the forefront of our members’ minds, but their strategic questions have shifted in focus. No longer ruminating over whether to retool for value-based care delivery, health care providers are now struggling with the challenges associated with making the transition— asking: “How, when, where?”

accordingly, in the first months of 2014, our experts have been focused on the tangible and practical details of the american health care industry’s transformation. From Jim Field’s perspective on why health systems haven’t reaped more benefit from scale to Hiten Patel’s anecdotes on retail clinic site planning, the 10 articles in this publication reflect our latest thinking on how to navigate the transition.

For more insights and research, visit advisory.com —and join us for an upcoming webconference or national member meeting.

LEGaL CaVEaTThe advisory Board Company has made efforts to verify the accuracy of the information it provides to members. This report relies on data obtained from many sources, however, and The advisory Board Company cannot guarantee the accuracy of the information provided or any analysis based thereon. in addition, The advisory Board Company is not in the business of giving legal, medical, accounting, or other professional advice, and its reports should not be construed as professional advice. in particular, members should not rely on any legal commentary in this report as a basis for action, or assume that any tactics described herein would be permitted by applicable law or appropriate for a given member’s situation. Members are advised to consult with appropriate professionals concerning legal, medical, tax, or accounting issues, before implementing any of these tactics. Neither The advisory Board Company nor its officers, directors, trustees, employees and agents shall be liable for any claims, liabilities, or expenses relating to (a) any errors or omissions in this report, whether caused by The advisory Board Company or any of its employees or agents, or sources or other third parties, (b) any recommendation or graded ranking by The advisory Board Company, or (c) failure of member and its employees and agents to abide by the terms set forth herein.

advisory.com | 1

contents

CLINICAL INTEGRATION | 16

Physicians and hospitals working together on improving care and being rewarded for their success.

MEDICAL hOME | 4

If you work on the medical home, you’ve heard it: the primary care physician is the quarterback of the care team. Is it still true?

SITING RETAIL CLINICS | 26

Retail clinics are expected to double in number across the next few years. And apparently our members have heard.

Time for a new quarterback for the medical home team

The extreme pessimist’s argument for population health

Why my post on health care costs made one member very angry

Three reasons health systems are stuck in neutral

Why good clinical integration networks fail—and what to do about it

What health care should be—in 7 words

Is the patient-centered medical home a Neanderthal?

Siting your next retail clinic? Follow the coffee smell.

Hybrid concierge: The best of both worlds?

How to attract the high-deductible patient

4

6

10

14

16

20

22

26

28

30

2 | Expert Perspectives spring 2014

Jim FieldExecutive Vice PresidentResearch and Insights

Jim heads up the health care research department at the Advisory Board, leading more than 150 professionals who cover a full range of programmatic, clinical, and technology-specific topics.

14

Michael KoppenhefferExecutive DirectorResearch and Insights

Michael is an expert advisor on health care product development, marketing, and technological innovation, with two decades of experience as a consultant and researcher.

10

Megan ClarkPractice ManagerResearch and Insights

An expert on care management redesign, patient engagement, and more, Megan helps hospitals on the transition path toward population health management.

4

Christopher KernsManaging DirectorResearch and Insights

A health care financial analyst by training, Christopher leads many of the firm’s strategic research efforts, with a special focus on hospital financial management.

6

FEATURED WRITERS

This issue’s contributing experts

advisory.com | 3

Laurie Sprung, PhDExecutive Vice PresidentSouthwind

Laurie is a leading expert on the creation of clinical integration programs. She leads a team of attorneys and consultants building CI networks and ACOs across the country.

16

Rob LazerowPractice ManagerResearch and Insights

Rob is the firm’s go-to expert on accountable payment. He spends much of his time educating members on major market developments and the implications for provider strategy.

20

Lisa Bielamowicz, MDExecutive Director and Chief Medical OfficerResearch and Insights

Our chief medical officer and an expert on physician strategy, Lisa serves as a strategic advisor to executives from the country’s largest health systems and medical groups.

22

Hiten PatelManaging DirectorResearch and Insights

A former consultant with scientific training in the development of quantitative research tools and analytics, Hiten focuses on technology adoption and developing markets.

26

Cabell JonasConsultantResearch and Insights

Cabell leads research on all things care management, from program development to staffing models to high-risk patient care and more.

28

Alicia DaughertyPractice ManagerResearch and Insights

While leading research on growth strategy, Alicia focuses on ambulatory investments, health system integration, employer partnerships, and new product development.

30

4 | Expert Perspectives spring 2014

If you work on the medical home, you’ve heard it: the primary care physicianis the quarterback of the care team.

However, as organizations tackle population health, we fi nd the metaphor actually falls short of our goals for the medical home. There are limits to how far we can scale and grow the medical home if we rely on PCPs to be the linchpin. Healthy patients shouldn’t rely on PCPs to drive care goals, and the sickest patients need a dedicated care manager more than they need a PCP.

BY: MEgAN CLARk

Time for a

New Quarterback

Medical Home TeamFOR THE

To watch the video on who the quarterbackof the medical home team is, visitadvisory.com/medhomequarterback

advisory.com | 5

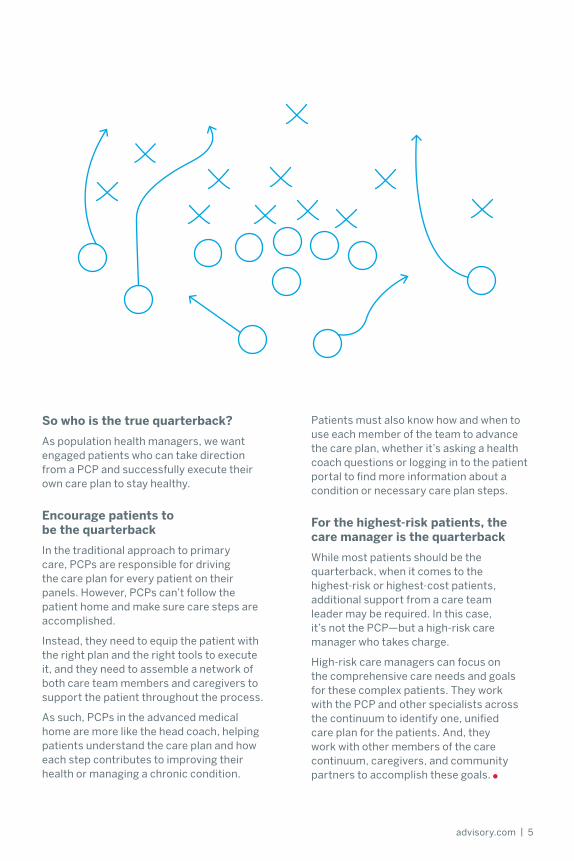

So who is the true quarterback?

As population health managers, we want engaged patients who can take direction from a PCP and successfully execute their own care plan to stay healthy.

Encourage patients to be the quarterback

In the traditional approach to primary care, PCPs are responsible for driving the care plan for every patient on their panels. However, PCPs can’t follow the patient home and make sure care steps are accomplished.

Instead, they need to equip the patient with the right plan and the right tools to execute it, and they need to assemble a network of both care team members and caregivers to support the patient throughout the process.

As such, PCPs in the advanced medical home are more like the head coach, helping patients understand the care plan and how each step contributes to improving their health or managing a chronic condition.

Patients must also know how and when to use each member of the team to advance the care plan, whether it’s asking a health coach questions or logging in to the patient portal to find more information about a condition or necessary care plan steps.

For the highest-risk patients, the care manager is the quarterback

While most patients should be the quarterback, when it comes to the highest-risk or highest-cost patients, additional support from a care team leader may be required. In this case, it’s not the PCP—but a high-risk care manager who takes charge.

High-risk care managers can focus on the comprehensive care needs and goals for these complex patients. They work with the PCP and other specialists across the continuum to identify one, unified care plan for the patients. And, they work with other members of the care continuum, caregivers, and community partners to accomplish these goals.

6 | Expert Perspectives spring 2014

Unless you’ve just returned from a multi-year vacation, you’ve almost certainly heard industry experts, including my Advisory Board colleagues, contend that many health care providers will need to take on population health management capabilities in the future.

(In fact, our entire Care Transformation Center program is dedicated to that proposition: it’s all about insights, guidance, and case studies from the front lines of population health transformation.)

The arguments in favor of population health management are convincing, as far as they go. The U.S. population is, indeed, growing older and sicker, and health care costs continue to rise (albeit at a slower rate recently than in the previous decade), so the need for more efficient, more effective care is ever-increasing.

What’s more, there are now mainstream payment mechanisms for provider-led population health management, such as the Medicare Shared Savings Program and direct-to-employer contracting.

BY: CHRISTOPHER kERNS

The extreme pessimist’s argument for population health

advisory.com | 7

Skepticism about today’spopulation health eff orts

For all that, there are reasonable counterarguments. Health care costs have been on the upswing for decades, and yet economists still disagree as to whether there will be an upper limit on our society’s spending on health care—perhaps health care costs could continue to climb for decades more, with no ill eff ect.

The new payment mechanisms are by no means a sure thing, either. CMS recently reported that only one in four shared-savings ACOs saved enough money to generate bonus payments. And direct-to-employer contracting has proven to be challenging for many of our members as well.

And yet, population health managementmay still be health care providers’ best chance at long-term fi nancial stability, especially if you consider a plausible, if pessimistic, future scenario for the fee-for-service business.

Private exchanges + narrownetworks = inevitable price erosion

Imagine that private exchanges really take off as a way for private-sector employers to provide health benefi t coverage. With private exchanges, employees—your potential patients—are given a fi xed sum to purchase the coverage they need, but make their own decisions about which plan to purchase.

(And if you think this will never happen, just remember the shift from pensions to 401(k) programs a generation ago. Many people thought 401(k)s would never catch on; pensions were just too great a lever for retaining talent. Now pensions are almost extinct. It’s the same idea—the move from defi ned benefi t to defi ned contribution—and it’s certainly no less likely to happen today.)

Now, let’s think through the implications of private exchanges. For one thing, private exchanges would almost certainly depress insurance pricing growth—and thus health care provider pricing.

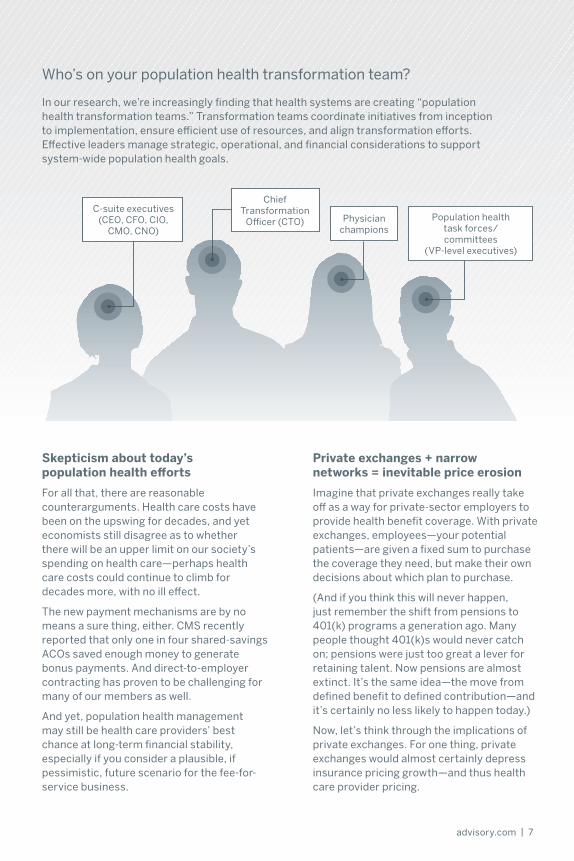

Population healthtask forces/committees

(VP-level executives)

C-suite executives(CEO, CFO, CIO,

CMO, CNO)Physician

champions

ChiefTransformation

Offi cer (CTO)

Who’s on your population health transformation team?

In our research, we’re increasingly fi nding that health systems are creating “populationhealth transformation teams.” Transformation teams coordinate initiatives from inceptionto implementation, ensure effi cient use of resources, and align transformation eff orts.Eff ective leaders manage strategic, operational, and fi nancial considerations to supportsystem-wide population health goals.

8 | Expert Perspectives spring 2014

Once employers stop paying the insurance bill directly, it will be easier for them to peg their annual contribution to overall cost-of-living changes rather than to the historically much-higher rate of medical infl ation, so their contribution will rise slower year after year, and price-sensitive consumers will have to make up the diff erence or choose less expensive insurance.

But the picture for fee-for-servicepricing in a private-exchanges world iseven worse than that, because marketshare would no longer matter in the way providers have thought about it in the past. Broad geographic coverage and large physician networks would cease to be a competitive advantage or a means to extract pricing leverage from insurers.

That’s because individual patients,

who could potentially select tailored, ultra-narrow provider networks through private exchanges, usually care most about convenience and access relative to themselves—not the overall size of a plan’s network.

To state the obvious, a world in which health care providers lose their pricing leverage would be a signifi cant, and unwelcome, change from the status quo for most health systems. Across the country, most of the revenue growth that hospitals experienced in the last decade was from price increases.

Population health management:The inevitable path forward?

If private fee-for-service prices becomeless and less attractive over time, what’s a health system to do?

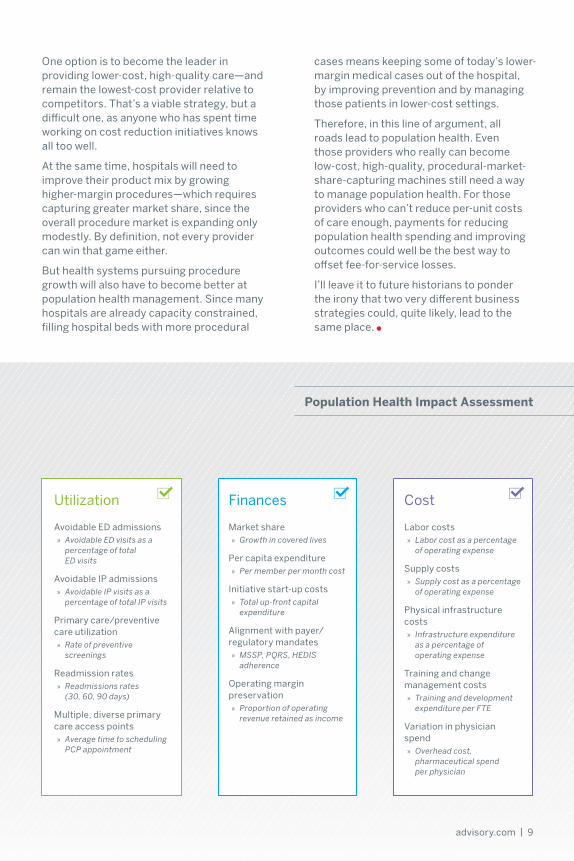

How do you evaluate the return on your population health investments?

When you are making decisions about population health investments, you need clear, defi ned criteria. Our Population Health Advisor team has identifi ed 30 metrics that let you assess the business impact of your population health transformation.

Targeting high-impact populations

» Population segmentation by risk, disease

Physician engagement » Impact on aligned physicians

Synergies with existing initiatives

» Eff ective integration of initiative into overall population health strategy

Cultural/organizational fi t » Alignment with population

health objectives

Impact on existing, desired case mix

» Case mix index (CMI)

Strategy

Team-based care management approach

» Percentage of staff performing at top of license

PCMH development » Percentage of primary

care practices operating as medical homes

IT readiness » Meaningful Use Stage 1

requirements

PAC high-performance network development

» Percentage of patients discharged to high-performing PAC partners

Community partnerships » Year-over-year increase in

patient utilization of non-clinical ancillary services

Care Coordination

Disease-specifi c outcomes » Disease-specifi c

composite scores

Targeted patient engagement and activation

» Percentage of patients adhering to care plans

Patient satisfaction » Patient experience surveys

Medical mortality » Mortality rate

Clinically appropriate utilization of imaging scans/diagnostic tests

» Rate of adherence to evidence-based standards

Quality Outcomes

advisory.com | 9

One option is to become the leader in providing lower-cost, high-quality care—and remain the lowest-cost provider relative to competitors. That’s a viable strategy, but a diffi cult one, as anyone who has spent time working on cost reduction initiatives knows all too well.

At the same time, hospitals will need to improve their product mix by growing higher-margin procedures—which requires capturing greater market share, since the overall procedure market is expanding only modestly. By defi nition, not every provider can win that game either.

But health systems pursuing procedure growth will also have to become better at population health management. Since many hospitals are already capacity constrained, fi lling hospital beds with more procedural

cases means keeping some of today’s lower-margin medical cases out of the hospital, by improving prevention and by managing those patients in lower-cost settings.

Therefore, in this line of argument, all roads lead to population health. Even those providers who really can become low-cost, high-quality, procedural-market-share-capturing machines still need a way to manage population health. For those providers who can’t reduce per-unit costs of care enough, payments for reducing population health spending and improving outcomes could well be the best way to off set fee-for-service losses.

I’ll leave it to future historians to ponder the irony that two very diff erent business strategies could, quite likely, lead to the same place.

Population health Impact Assessment

Avoidable ED admissions » Avoidable ED visits as a

percentage of total ED visits

Avoidable IP admissions » Avoidable IP visits as a

percentage of total IP visits

Primary care/preventive care utilization

» Rate of preventive screenings

Readmission rates » Readmissions rates

(30, 60, 90 days)

Multiple, diverse primary care access points

» Average time to scheduling PCP appointment

Utilization

Market share » Growth in covered lives

Per capita expenditure » Per member per month cost

Initiative start-up costs » Total up-front capital

expenditure

Alignment with payer/regulatory mandates

» MSSP, PQRS, HEDIS adherence

Operating margin preservation

» Proportion of operating revenue retained as income

Finances

Labor costs » Labor cost as a percentage

of operating expense

Supply costs » Supply cost as a percentage

of operating expense

Physical infrastructure costs

» Infrastructure expenditure as a percentage of operating expense

Training and change management costs

» Training and development expenditure per FTE

Variation in physician spend

» Overhead cost, pharmaceutical spend per physician

Cost

10 | Expert Perspectives spring 2014

Health care costs are a hot-button issue. But I have to admit I was still surprised at the furious email I got recently from one Advisory Board member who read my blog post on the difference between

“cost” and “cost.” What did I do wrong?

made one member very angry

Why my post on

health care costs

BY: MICHAEL kOPPENHEFFER

advisory.com | 11

Too imprecise about accounting terms

It wasn’t a disagreement about politics, or a dust-up over who’s responsible for bending the health care curve. My sin was imprecision. The member, a financial analyst at a community hospital, took me to task for not clearly delineating the difference between fixed and variable costs, on one hand, and direct and indirect costs on the other.

What I originally wrote was:

First of all, there are “hospital input costs,” by which I mean, “the costs that a hospital incurs to provide care.” This includes the “variable costs” of everything it takes to treat an individual patient: the salaries of nurses and techs, as well as costs of supplies and drugs. It also includes the “fixed costs” of keeping the hospital in operation, such as electricity, major pieces of equipment, and even the land and buildings.

CMS and other insurers sometimes track “direct” and “indirect” hospital input costs, which are almost, but not exactly, the same as fixed and variable costs.

As my correspondent pointed out, direct costs and variable costs are not the same thing in the world of cost accounting; in fact, a cost can be direct but not be variable. The classic health care example of this is the salary of a hospital nursing supervisor, whose work is directly attributable to patient care, and therefore “direct,” but does not vary directly based on the number of patients in the hospital—and thus is “fixed.”

Getting more specific about direct vs. variable costs

So I tried to clarify the original post as much as I could, adding a sentence that says:

“Direct costs” are those costs directly associated with patient care, while “indirect costs” are other costs.

(Inelegant, perhaps, but I didn’t want to further confuse what was already a complicated post about five different other types of costs.)

But this whole episode got me thinking: Why do these accounting distinctions really matter? Especially for people in health care who may not know (or care) about the difference between a balance sheet and an income statement?

The more I thought about it, though, the more I wondered whether cost accounting could be one of the keys to population health management success.

Why? Because effective population health management will inevitably result in the elimination of certain health care services consumed today: better prevention will obviate the need for health care, better management will result in the substitution of less intensive procedures, and better practice will result in more compliance with clinical guidelines and therefore, in many cases, fewer diagnostics or procedures.

(If you want evidence, just check out the sometimes amazing levels of variation our Crimson research teams found when they mined inpatient imaging utilization data from across the cohort of participating hospitals.)

12 | Expert Perspectives spring 2014

Why accounting matters to care transformation

From the perspective of the insurer (or the accountable care organization) the financial impact of eliminating ten $1,000 MRI scans is equivalent to eliminating one $10,000 knee replacement: $10,000 in costs not incurred.

But from the perspective of the health care provider, the impact is not at all the same.

The MRI story: The real variable cost associated with providing an MRI procedure is the cost of the radiology technician’s time, the cost of the contrast agent (if any), and the cost of the radiologist’s time for reading and interpreting the MRI exam. In sum, those costs might total $200 per exam, a small fraction of the price. This is because the lion’s share of the cost associated with MRI exams is fixed: health providers need to defray the million-dollar cost of an MRI scanner, so they spread the scanners’ cost over many thousands of exams.

Still, because most of the MRI costs are fixed, eliminating one hypothetical MRI exam would result in $1,000 less revenue for the provider, but reduce only $200 of the provider’s costs. The net impact for the provider would be $800 less per exam, or $8,000 for ten exams.

The knee replacement story: For MRIs, technology accounts for a great deal of the procedure cost, but in the case of knee

replacement it is the cost of the implant—say, $5,000 of the $10,000 total. That implant cost is a variable cost; the hospital incurs it only if the patient actually has the knee replacement procedure. And the other costs associated with the procedure—nursing care, drugs, supplies, and so forth—are largely variable as well.

What that means is that variable costs might account for as much as $8,000 of our hypothetical $10,000 knee replacement procedure. And so if one of those procedures is averted, the negative impact on the health care provider is only the $2,000 difference, which would have otherwise gone to pay for fixed costs and profit on the procedure.

In other words, eliminating the MRI scans would have a much bigger negative impact on health care provider finances than eliminating the knee replacement procedure.

But you would only know that if you were careful about tracking the different types of costs associated with each procedure. And that’s a discipline that not every health care provider has—let alone the ability to pull up and analyze the data correctly in their information systems.

The moral? For success in the value-based health care market, maybe all of us (and our information systems too) need to take a refresher course in cost accounting.

advisory.com | 13

=$2,000 =$8,000

x10 x1

=$10,000 =$10,000

x10 x1

The payer’s perspective

The provider’s perspective

Variable cost savings

Variable cost savings

Fixed cost to defray machine

Fixed cost

14 | Expert Perspectives spring 2014

BY: JIM FIELD

Three reasons health systems are stuck in neutral

Across the past few years, I’ve held many informal strategy sessions with executive teams of both large and small provider systems.

After participating in dozens of these sessions, it is becoming clear to me that while their markets are unique, these executives and the systems they lead are virtually clones of one another. They are wrestling with the same problems, and plagued by the same shortcomings, as they attempt to transform fee-for-service mind-sets and organizations into entities aligned to where health care is headed.

Specifically, provider systems across the country, with very few exceptions, are alike in three important ways.

A complex and sometimes irrational portfolio of assets1

First, practically every health system I encounter is an aggregation of disparate assets: acute care hospitals, employed physicians, urgent care centers,ambulatory surgical centers, ambulatory clinics, skilled nursing facilities, and so on.

Rather than select assets according to a master plan, health systems accrue them over time at the direction of successive CEOs for any number of reasons—some principled and others

expedient, often to counter competitors. This being the case, there is little logic to the system’s geographic footprint.

Worse still, within the inventory of assets, there is redundancy, excessive capacity, an undesirable weighting of physician types, and a tangle of vendor relationships. As things now stand, some of the assets benefit the system, while others are an iron ball around its neck.

advisory.com | 15

Strategic uncertainty about how to leverage those assets

Reluctance to upset the status quo

The single active ingredient: Leadership

2

3

Second, sitting atop these assets, executive teams have little idea what to do with them. To be sure, some progress has been made in taking advantage of scale, mostly in back-office functions.

And the executives agree that under health care reform they must mobilize

against three main imperatives: cost reduction, revenue growth, and clinical transformation. But having these objectives in sight, they have no sense of how to take what they have—a mixed bag of assets—and reconfigure it into the provider entity they know they’ll need.

Considering how challenging the road ahead will be, I’m convinced the health systems that succeed will do so because of the quality of their leadership.

Successful health system leaders will need to be able to form a compelling vision of where health care is headed and what will be required of providers. They will need

conviction—the fortitude to steer the organization where it must go, despite the expected turbulence. And they will need to communicate that vision and that conviction with the entirety of the organization.

Will your executive team rise to the challenge?

Third, even when there is a clear strategic direction, executive teams are reluctant to move far enough or fast enough.

Their timidity is understandable: to transform disparate assets into integrated health systems capable of assuming risk-based payment and delivering value-based care, health system executives will need to overturn the status quo—comprehensively and decisively—and shoulder the resulting fallout.

There’s no way around it: the transitional work to be done will be arduous, prolonged, and loathed by nearly everyone. For starters, duplicative facilities—hospitals included—will have to be shut down or converted to a new activity. Clinical services will have to be consolidated. Hospital management will have to be streamlined or disbanded entirely in favor of centralized control.

On the physician side, health systems will need to reach a suitable proportion of PCPs

to specialists, potentially by shedding the latter selectively. They will need to impose order on autonomous clinical practice by adopting and enforcing guidelines, and closely monitoring physician performance and “coaching” outliers. All this will require some physicians telling other physicians what to do, and expecting compliance.

In many markets, solo physicians and small independent practices will cease to exist.

Radical change, after all, cannot occur without an equivalent amount of disruption to the existing order. The transition can’t bring everything and everyone with it; old-world behaviors can’t be preserved; and many, many people will have their interests crossed and feelings hurt.

Provider systems cannot be true systems by asking employees to “do the right thing” on a voluntary basis. Nor will they survive by propping up pervasive inefficiencies.

16 | Expert Perspectives spring 2014

BY: LAURIE SPRUNg, PhD

Why good clinical integration networks fail—

and what to do about it

advisory.com | 17

The legal rules for organizing CI networks require that physicians take a leadership role in the network, although the hospital can set up the infrastructure and the network itself can provide administrative support.

This can be a tricky balance to achieve, as too much independence can lead to redundancy or even rivalry among care management efforts. In some markets, we’ve seen big inefficiencies develop when the CI network is not sufficiently aligned with health system administrators and other system-affiliated physician entities, such as employed medical groups.

However, the CI network needs to be sufficiently independent and physician-led that physicians want to participate. So when a health system sets up the CI network, it also needs to make sure that there are true physician champions, including independent physicians, not just at the table but driving the discussion. Otherwise, it could be a great party, but nobody will come.

As I’ve told more than one client, “If these physicians were natural joiners, they would have joined something already!”

Clinical integration is one of the few effective models we’ve found for getting physicians and hospitals to work together on improving care and to be rewarded for their success.

Today, we estimate there are more than 500 clinically integrated provider networks from coast to coast—and my colleagues and I in the Advisory Board’s Southwind consulting division have personally been involved in setting up 85 of them.

Not all CI networks that look good on paper end up succeeding in the real world, though. Here are three reasons we see good CI networks fail—and how to position yourself for the best chance of success.

oneThe network isn’t truly physician-led

18 | Expert Perspectives spring 2014

A CI network only works if payers or employers agree to provide performance-based incentives to the network. And the reality is, not every market has payers or employers eager to create those kinds of contracts.

How can CI networks thrive in a market that isn’t on the forefront of value-based reimbursement? Many health systems start by creating incentives around caring for their own employee population. But beyond that, the health system needs to help bring payers to the table—and be willing

to use its analytics, its expertise, and even concessions on other contract terms to get a favorable CI contract in place.

When my Southwind colleagues and I work with health systems on clinical integration strategy, we typically create a thorough economic analysis to understand the full impact of the CI network. That way, the health system can make an informed decision about how hard to fight, and for which CI terms, in the context of overall payer contracting negotiations.

Although we haven’t seen many shared savings-related failures yet, the reality of shared savings programs, including MSSP, is that not all participants will be able to generate the anticipated savings. Across the next several years, CI networks that are banking on shared savings payments to bolster the case for participation are likely to see physicians

back out if the shared savings payments don’t live up to initial projections.

We advise CI programs to think about shared savings as “maybe money” —nice if it materializes, but not what anyone should be relying on to get, or keep, physicians engaged in performance improvement efforts.

two

three

The CI network never gets appropriate contracts—and the hospital doesn’t help

The financial case for the CI network relies too heavily on shared savings contracts

advisory.com | 19

“If these physicians were natural joiners, they would have joined something already!”

20 | Expert Perspectives spring 2014

BY: ROB LAzEROW

What health care should be—in 7 words

Last year, I had the privilege of presenting the keynote address at the D.C. Primary Care Association’s Policy Forum—an annual conference that brings providers, policymakers, and community leaders together to discuss how to collectively transform health care in Washington, D.C.

To kick off the meeting’s theme, “From Visits to Value: Serving Patients in the New Marketplace,” I explored key attributes of the future health care delivery system.

Here’s why your organization needs to become scalable, team-based, patient-centered, comprehensive, collaborative, interconnected, and inclusive.

Even the largest systems won’t own all the social and support services required to deliver comprehensive, patient-centered care.

advisory.com | 21

Scalable

Patient-centered

Team-based

Inclusive

Comprehensive

Interconnected

Collaborative

01 05

04

02 06

03 07

The future delivery system will provide care through scalable, efficient models by managing three different patient populations: low, rising, and high risk. Achieving a flexible delivery model will become even more critical if coverage expansion efforts reveal new access gaps.

While “patient-centered care” is a buzzword right now, providers need to reflect on what it actually means. At a minimum, providers will need to develop specific care plans that support patients’ holistic health needs. Progressive organizations will go further and reorganize around patient needs, instead of specialties or academic disciplines.

As part of achieving scale, providers will increasingly deploy team-based care models—especially for primary care. The medical home and similar models ensure all providers practice to the full extent of their training and skills.

Leading population health managers already recognize how much behavioral health, economic stability (especially housing), and emotional support contribute to overall health and well-being. In the future, providers will have a large role to play in addressing these psychosocial determinants of health.

Effectively managing a network of hospitals, physicians, post-acute care providers, and community organizations will require a new level of interconnectivity. Many provider organizations have ended the quest for the perfect EMR system and instead are focusing on data exchange across their networks.

Delivering comprehensive care will require an array of services, many of which extend beyond the traditional purview of health care providers. Partnership management must be a core competency to coordinate networks of partners with aligned objectives.

Finally, the future delivery system will be much more inclusive than today’s health care system. It begins with the partnerships that will make care more collaborative, but does not stop with formal providers or community organizations. In the future, patients, family members, and lay caregivers will be more directly involved in both care planning and delivery.

22 | Expert Perspectives spring 2014

BY: LISA BIELAMOWICz, MD

home a Neanderthal?patient-centered medical

Is the

advisory.com | 23

In my recent meetings with health system executives, I’ve been asking this deliberately provocative question:

It may seem odd to compare the medical home to extinct relatives of the human race, famed for their heavy brow ridges and limited use of tools. After all, the medical home has been rightly praised as an important advance in primary care delivery, especially suited for “rising-risk” patients who have chronic disease and comorbidities but are not at immediate risk for poor outcomes.

There is no question that organizations can advance primary care delivery by adopting the medical home model. But as health systems push medical homes to their limits, the argument is emerging that population health managers will need something more.

A few years from now, will we say that the patient-centered medical home was just a blind alley on the way toward a more highly evolved form of population health management?

24 | Expert Perspectives spring 2014

Not enough primary care capacity

The more health systems adopt the medical home concept, the more I’m realizing a fundamental flaw with the model.

There is simply not enough primary care capacity—not enough physicians, to be specific—to treat every “rising-risk” patient in a medical home, at least not as they’re currently being implemented.

In our study Playbook for Population Health, we explore the impact of panel expansion on physician workload. If an organization pushes panel size to 4,500, a primary care physician would need 68 hours per week to accommodate every patient, even under the highest standards of medical home efficiency.

Does that mean the tenets of the patient-centered medical home are untenable?

Not at all. A medical home is a way to provide patients with expanded access, enhanced care coordination, holistic care, and proactive disease management—all which are of undeniable benefit to rising-risk patients.

Thinking beyond the practice setting

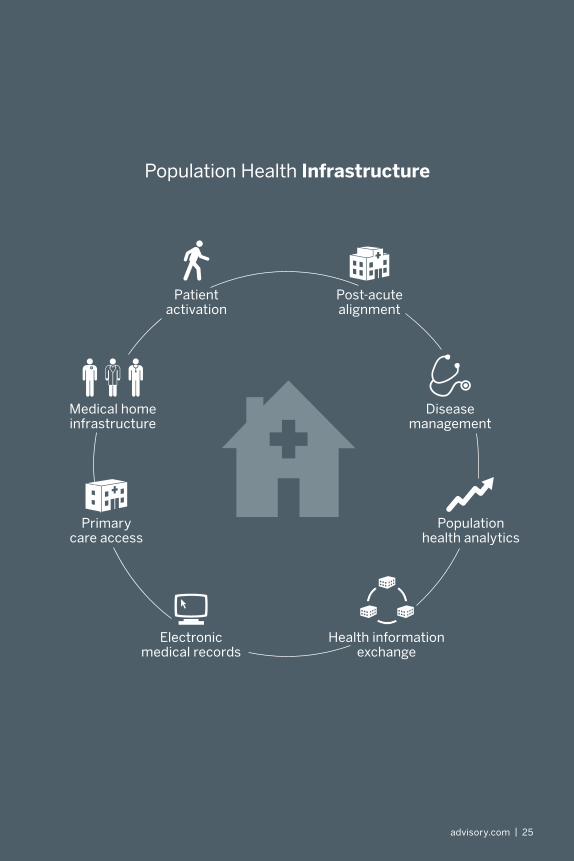

However, most “medical homes” to date have been conceived at the physician practice level, with nurses, social workers, and other allied staff organized within practice units. What we’re realizing is that to be scalable, many elements of the medical home, such as health coaching and disease management, will need to be delivered centrally, across (or beyond) an entire health system.

Indeed, that’s what many of the most advanced population health management organizations in the country are already doing, building out a central population health infrastructure to complement what they’re doing at the practice level.

For example, at Montefiore Medical Center in the Bronx, care management investments are centralized through Montefiore Care Management. This allows the organization to map out workflows

and standardize activities across the organization, essentially acting as air traffic control to ensure a seamless patient experience.

Creating a more tailored population health product

I also predict that successful population health management organizations will develop more gradations within their delivery models.

For instance, if I went for a checkup next week and found out I had diabetes, I wouldn’t personally need all the services of a typical patient-centered medical home, though I might benefit greatly from telephone-based health coaching.

By contrast, someone who doesn’t have reliable transportation, who doesn’t eat a healthy diet, who suffers from mental illness, and who also gets a new diagnosis of diabetes would almost certainly benefit from the full set of medical home services.

Even that individual, though, might be better and more efficiently served by certain centralized services rather than all of the services being provided through a practice-based medical home.

Keeping one eye on the end state

I’m not trying to warn anyone away from medical home implementation. In fact, if I were in charge of a health system’s primary care strategy, I’d be moving full speed ahead with medical home implementation in many, though not all, of the system’s owned practices.

But as systems implement the medical home model, they would be well served to look for opportunities to centralize certain population health management services. And I would also focus on understanding which patients benefit most from the “full-on” medical home package and which patients could be well served by a more selective, less physician-based approach.

advisory.com | 25

Population health analytics

Disease management

Primary care access

Medical home infrastructure

Health information exchange

Post-acute alignment

Electronic medical records

Patient activation

Population Health Infrastructure

26 | Expert Perspectives spring 2014

Siting your next retail clinic? Follow the coffee smell.

Retail clinics are expected to double in number across the next few years. And apparently our members have heard. In recent months, our researchers have gotten tons of inquiries from members who are considering investing in their retail health care capabilities.

Health systems seem to be grappling with all aspects of the retail clinic business model: the underlying economics, the staffing structure, even the right ownership approach.

BY: HITEN PATEL

advisory.com | 27

Top retail clinics question: Location

One of the most common inquiries we get is, “Where do we put it?”

Health system planners generally know how to choose the location for a new primary care practice or surgery center, but retail clinics just feel…different.

In reality, they’re not as different as they seem. Just as for any other bricks-and-mortar health care investment, institutions need to consider the current and future supply and demand in the market. We recommend that members ask a few basic questions:

• Will the location attract the “right” patient demographic? Location will make a big difference as to which patients will visit the new retail clinic—and you need to make sure the clinic’s proposed location supports the patient population that is in your business model.

• Is there unmet primary care need in this location? A retail clinic is less likely to succeed if there is ample primary care appointment availability close by. Swelling volumes in nearby emergency departments is one good indicator of unmet need.

• How are the local demographics—and demand—expected to change? It stands to reason that investing an area likely to see population growth is a better bet than a market in decline.

Health care planners are used to asking and answering these kinds of questions—and their existing sources of data will probably help answer these questions satisfactorily. But there’s at least one other consideration that is critically important for retail clinics: traffic patterns.

Pinpointing the right site is all about traffic patterns

Much more than other health care facilities, retail clinics rely on proximity and convenience. Planners need to figure out how a potential location plays into existing

patterns of traffic—and precision matters. The wrong block, or the wrong side of the street, could mean a meaningful difference in patient volumes.

There are consultants who specialize in retail traffic pattern analysis, and some of our members have retained them to evaluate potential retail clinic sites.

But there’s a shortcut to traffic analysis that several of our members have arrived at independently: look at where well-run national chains that rely on casual traffic place their outlets and try to get as close to them as possible.

The “Starbucks shortcut”

I first came across this idea working with one of our health system members last year. They’d already determined that they needed a retail clinic strategy, and they specifically wanted to target the urban middle class.

They identified the right area of town, and they knew the demographic projections were in their favor. But all the data at their disposal still left them with 10 city blocks to choose for the site, and they asked us if we had any data that could help them pinpoint the location more specifically.

On a whim, we suggested they look where all the Starbucks had been located. One of the strategic planners laughed and said, “Actually, that’s exactly what we did.”

When I came back to our office, I told a couple of our primary care experts about this exchange. To my surprise, they told me the “Starbucks shortcut” was not an uncommon approach. Some of our most resourceful members are piggybacking on the site selection expertise of big national chains.

After all, national chains are also looking at current demographics, population projects, and (most of all) traffic patterns. And retail chains, especially those like Starbucks that are corporate-run rather than franchise-based, are likely to exercise considerable discipline in choosing their locations.

28 | Expert Perspectives spring 2014

One inclusive alternative is a hybrid concierge practice, where about 10% of the panel pays a retainer fee for enhanced service, while the remaining majority continues to access care traditionally.

Hybrid models can mean no dismissals outside of natural attrition, and though the panel is smaller than a traditional primary care practice (2,000 patients) it is still much larger than a full concierge model (400 to 600 patients). Most importantly, the retainer fees allow physicians to deliver quality service to all patients while improving the practice bottom line.

There are three main benefits to implementing a hybrid concierge model for existing primary care practices:

• Earn additional revenue through the retainer fees paid by a portion of the patients

• Patients who aren’t interested in concierge care don’t need to change physicians or practices

• Convert existing patients into concierge patients, eliminating the need to populate an entirely new concierge practice (which takes time and investment)

You may have read our recent post on the One Medical concierge model, an emerging primary care network that provides value to patients by focusing on convenience and access.

The One Medical model overcomes two of the biggest challenges of concierge medicine (physicians are able to maintain a larger panel size and patients are charged an affordable price)—but building a low-fee concierge practice still may require established patients who opt out of concierge care to leave the practice.

We’re here to tell you that not every viable model has this drawback.

The best of both worlds?

hybrid concierge:

BY: CABELL JONAS

The hybrid concierge model

advisory.com | 29

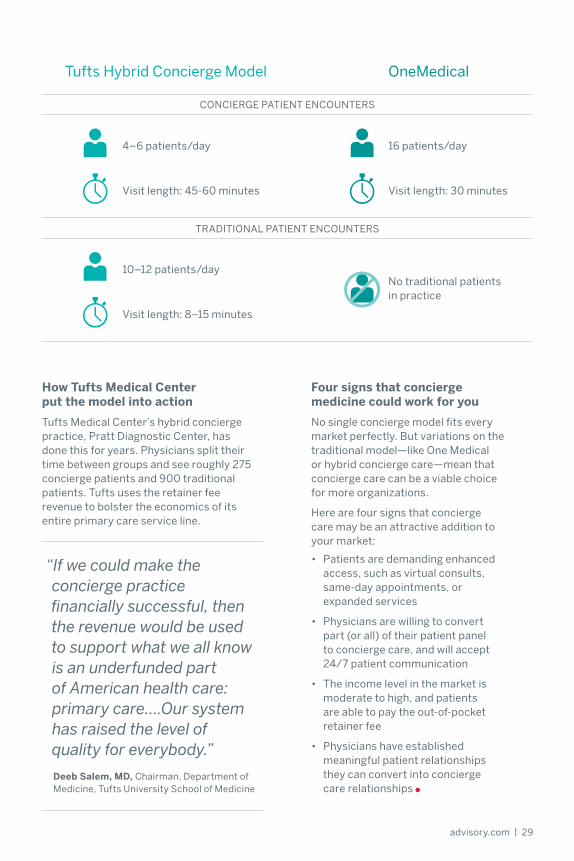

Four signs that concierge medicine could work for you

No single concierge model fits every market perfectly. But variations on the traditional model—like One Medical or hybrid concierge care—mean that concierge care can be a viable choice for more organizations.

Here are four signs that concierge care may be an attractive addition to your market:

• Patients are demanding enhanced access, such as virtual consults, same-day appointments, or expanded services

• Physicians are willing to convert part (or all) of their patient panel to concierge care, and will accept 24/7 patient communication

• The income level in the market is moderate to high, and patients are able to pay the out-of-pocket retainer fee

• Physicians have established meaningful patient relationships they can convert into concierge care relationships

how Tufts Medical Center put the model into action

Tufts Medical Center’s hybrid concierge practice, Pratt Diagnostic Center, has done this for years. Physicians split their time between groups and see roughly 275 concierge patients and 900 traditional patients. Tufts uses the retainer fee revenue to bolster the economics of its entire primary care service line.

“If we could make the concierge practice financially successful, then the revenue would be used to support what we all know is an underfunded part of American health care: primary care….Our system has raised the level of quality for everybody.”

Deeb Salem, MD, Chairman, Department of Medicine, Tufts University School of Medicine

Tufts Hybrid Concierge Model OneMedical

CONCIERgE PATIENT ENCOUNTERS

TRADITIONAL PATIENT ENCOUNTERS

4–6 patients/day

10–12 patients/day

16 patients/day

No traditional patients in practice

Visit length: 45-60 minutes

Visit length: 8–15 minutes

Visit length: 30 minutes

30 | Expert Perspectives spring 2014

How to attract the

high-deductible patientALICIA DAUgHERTY

Guide the value conversation

Typical consumers do not have a good working definition of value when it comes to health care, which can cause them to focus exclusively on price. Shift the conversation to the key components of value, including quality, convenience, and service, as well as price. For example, CarePilot, a company that contracts with providers to offer available medical appointments for variety of procedures, defines value as cost and convenience.

Through their websites, providers can list open appointments for a variety of services, with varying prices depending on the day and time. Off-peak appointments are often priced at a 10% to 30% discount, allowing consumers to make trade-offs based on their priorities.

Other institutions are highlighting the different components of value in their consumer messaging. The advertising campaign from Overlake Medical Clinic highlights quality and price to give consumers a comprehensive understanding of the value of urgent care centers.

A recent survey suggests that consumer-driven health plans (CDHPs) may become the most commonly offered form of employer-sponsored coverage for large companies in the next three to five years, with 56% of surveyed employers with 500 or more employees currently offering CDHPs and another 30% considering offering one.

Moreover, at 10% of firms, CDHPs are the only coverage option, and another 44% say they are considering offering only this option in the future. Even today, platforms like Castlight, CarePilot, and Optimal Hospital are helping patients take health care decisions into their own hands using price, quality, and patient satisfaction information.

As employers ask them to bear more costs, consumers are asking more from their care providers, seeking additional value from conveniences like online scheduling, email communication, and on-demand care via e-visits and retail clinics.

To compete for increasingly selective consumers, providers must be able to accomplish the following objectives.

advisory.com | 31

hardwire effortless interactions

All clinical providers should be able to help patients navigate across their networks by proactively identifying and scheduling needed services. At kaiser Permanente Orange County Women’s Health Services, the EMR alerts physicians about patient care needs regardless of which physician the patient is currently seeing.

This means that specialists can schedule preventive care visits with the patient’s PCP and vice versa, resulting in high levels of screening compliance and improved health outcomes.

Offer ‘anytime, anywhere’ service

In a world with one-click shopping, Netflix, and over one million iPhone apps, consumers are coming to expect on-demand service in health care as well. To meet patient expectations for 24/7, no-waiting service, many health care organizations are investing in online services and patient portals.

For example, Catholic Health Initiatives (CHI) invested in Carena, a telehealth company, whose CareSimple product offers patients 24/7 access to doctors and nurses. CHI and Carena plan to scale this model nationally.

CareSimple’s Virtual Visit Model

Individual or family pays an annual membership fee

1

Patients can access doctors 24/7 for $5 per visit

2

If ED or urgent care referral needed, CareSimple calls ahead, waives virtual visit fee

3

For More Advisory Board Thought LeadershipVisit our blogs at advisory.com/blogsSign up for email alerts at advisory.com/subscriptions

Accelerate the TransitionLearn more about how the Advisory Board is supporting the industry’s transition to population health at advisory.com/solutions/population-health

Note to readers

Michael Koppenheffer

Executive DirectorResearch and Insights

Not so long ago, the most common questions we heard from our members concerned the transition from fee-for-service medicine to value-based care—and these questions ultimately boiled down to, “Should we?”

Today, the value-based care transition remains at the forefront of our members’ minds, but their strategic questions have shifted in focus. No longer ruminating over whether to retool for value-based care delivery, health care providers are now struggling with the challenges associated with making the transition— asking: “How, when, where?”

accordingly, in the first months of 2014, our experts have been focused on the tangible and practical details of the american health care industry’s transformation. From Jim Field’s perspective on why health systems haven’t reaped more benefit from scale to Hiten Patel’s anecdotes on retail clinic site planning, the 10 articles in this publication reflect our latest thinking on how to navigate the transition.

For more insights and research, visit advisory.com —and join us for an upcoming webconference or national member meeting.

LEGaL CaVEaTThe advisory Board Company has made efforts to verify the accuracy of the information it provides to members. This report relies on data obtained from many sources, however, and The advisory Board Company cannot guarantee the accuracy of the information provided or any analysis based thereon. in addition, The advisory Board Company is not in the business of giving legal, medical, accounting, or other professional advice, and its reports should not be construed as professional advice. in particular, members should not rely on any legal commentary in this report as a basis for action, or assume that any tactics described herein would be permitted by applicable law or appropriate for a given member’s situation. Members are advised to consult with appropriate professionals concerning legal, medical, tax, or accounting issues, before implementing any of these tactics. Neither The advisory Board Company nor its officers, directors, trustees, employees and agents shall be liable for any claims, liabilities, or expenses relating to (a) any errors or omissions in this report, whether caused by The advisory Board Company or any of its employees or agents, or sources or other third parties, (b) any recommendation or graded ranking by The advisory Board Company, or (c) failure of member and its employees and agents to abide by the terms set forth herein.

28432

2445 M Street NW, Washington DC 20037

P 202.266.5600 | F 202.266.5700advisory.com

Perspectivesexpert

spring 2014 | volume 2

THE TraNSiTioN To

PopulationHealth