2841 willis construction risks cover · institutions. evolution of the market ... market continues...

TRANSCRIPT

Willis Construction RisksGlobal Construction Market OverviewJune 2005

2841 Willis Construction Risks COVER.qxd 07/06/2005 11:04 Page 1

Willis Group Holdings Limited is a leading global insurancebroker, developing and delivering professional insurance,reinsurance, risk management, financial and human resourceconsulting and actuarial services to corporations, publicentities and institutions around the world. With over 300offices in more than 74 countries, its global team of 14,500associates serves clients in some 180 countries. Willis ispublicly traded on the New York Stock Exchange under thecode WSH. Additional information on Willis may be found onits web site: www.willis.com.

2841 Willis Construction Risks COVER.qxd 07/06/2005 11:04 Page 2

Willis Construction Market Review – June 2005 1

Contents

Foreword 2

Introduction 4

Market Overview 5

London and European Market Overview 7

Willis Global Overview 15

Asia Pacific 15

Australia 18

Latin America 20

Middle East 21

United States of America 22

Bermuda 27

Marketing Strategy 28

Associated Product Reviews 29

Professional Indemnity (PI) 29

Political Risks 30

Inherent Defects Insurance 31

Marine Cargo 31

Market Security 33

Summary and Prognosis 34

Willis Group Contributors 36

2 Willis Construction Market Review – June 2005

Foreword

The global construction insurance market continuesto respond to high levels of demand andincreasingly challenging transactions. These arebeing generated by high levels of activity in theconstruction industry in many sectors and in variedgeographical locations.

The construction cost and project managers, DavisLangdon & Seah International, highlight the size ofthe opportunity: "Global construction spendingreached nearly USD 4 trillion in 2003 and isexpected to grow by 4.6% annually between 2004and 2007."1

Furthermore, according to the World Bank,"Between 1990 and 2002 more than 130developing countries introduced privateparticipation in at least one infrastructure sectorawarding almost 2,500 projects attractinginvestment commitments of USD 750 billion."2

So what are the challenges?

• The sheer size of some of the projects in thecontext of world Probable Maximum Loss (PML)construction insurance capacity;

• The contractual complexity of many projectswhich were in the public sector and are nowstructured under PFI/PPP arrangements;

• The rigorous requirements of the structuredfinancing arrangements which are fuelling somany large projects and the requirements of thedebt investors;

• The ever-more litigious world in which we arenow operating;

• The changing climatic conditions causing morenaturally occurring disasters;

• The changing world of Corporate Governance;

• The technological advances in design which areproducing "scale ups" and new processes.

How is the market responding to thesechallenges?

• Projects are being placed;

• Capacity is available and being committed;

• Policy coverage is being adapted to meet notonly the demands of the owners or contractors,but also the requirements of the lendinginstitutions.

Evolution of the Market

Before looking forward and predicting where themarket is going, we need to take a retrospectivelook at the non-marine construction market overthe last couple of decades.

11111 Davis Langdon & Seah International – “World Construction Review/Outlook 2003/4”22222 World Bank – “2004 World Development Indicators”

Willis Construction Market Review – June 2005 3

Foreword – continued

Having evolved from the non-marine propertymarkets, it is no surprise that the constructionmarket is still heavily influenced by itsantecedents.

The evolutionary development has, however, beenquite remarkable.

The construction market is successfully providing:-

• long term capacity (five to six years is notunknown);

• a combination of Physical Damage, Third PartyLiability and Business Interruption;

• coverage for a multitude of parties engagedwith a project, including owner, contractor, sub-contractors, lenders and engineers/consultants;

• full value physical damage cover (in themajority of cases);

• strong insurer security ratings, which are morecritical on long-term construction placements;

• flexibility on coverage to suit the needs of theinsured, including design and maintenancecover.

This is in spite of poor underwriting returns in the1980s and 1990s (with the odd positive year)!

So why do those markets hang in there?

It is certainly not in the expectation of getting rich!However, the experience has improved, particularlysince Q1 2001. In our last survey in June 2004, weidentified the net loss of construction marketcapacity.

Long term "A"-rated insurance capacity is a rarecommodity. The appetite for construction businessis still strong. But we live in a reactive and hugelyvolatile market. Many insurers are committingcapacity to a single risk that far exceeds theirannual premium income for the class! It requires ahigh level of reserving to protect "long-tail"business. Willis is continually looking to forgestronger links between the buyer and the seller ofthis capacity. That ultimately is how the businesswill endure.

It is time that the true value of construction coveris appreciated. It is still considered, like manyother classes of insurance, as an expense. In manycases the insurance cover is a condition precedentto project financing, yet is not regarded for whatit truly is: contingent equity. We have clients whohave experienced truly destructive losses. To themthe value of their insurance programme and theirrelationship with their construction insurers isparamount and beyond pure cost. The value shouldbe considered in the context of all of the ingredientparts: coverage, security, claims service, valueenhancements and the premium, which should beregarded as an investment or hedge againstfuture events.

The construction insurance market will remainalert and responsive to these needs in the nextfew years.

David G Turner, Chief Executive OfficerWillis Construction Risks, London

4 Willis Construction Market Review – June 2005

The insurance market moves, at times, with a degreeof unpredictability. Ensuring that clients are periodicallyupdated on the status of the insurance market is justone of the key tasks in which Willis takes a great dealof pride.

Within this Construction Market Review, we aim toprovide our clients with a complete overview of theconstruction market for both UK and internationalbusiness, including commentary from various globalmarket centres. This outlines our in-depth awarenessof the construction market globally.

We have also expanded our review this year to provideyou with commentary from other Willis business unitson market conditions affecting insurance coverages witha close affinity to the construction industry.

Introduction

Willis Construction Market Review – June 2005 5

Market Overview

The market continues to service the needs of itsclient base on a global scale, from the most basicconstruction activity to some of the world's mostextravagant project developments and risk transferneeds.

The market remains open to business solutions forits client base, regardless of how diverse a client'srisk transfer needs are. From a variety of industryprofessions covering a multitude of annual and/orsingle project business on a global scale, ourmarket continues to know and understand itsbusiness and its customers' needs.

Losses

Past problems associated with "attritional" losseshave been addressed through a more stringentapproach to self-insured retentions/deductibles.Fortunately, the frequency of severe, catastrophiclosses in the non-marine construction market hasbeen very low. Historically, the adverse impact onloss experience has been caused by the frequencyand repetition of less severe losses.

Premium levels charged have not been sufficient tooffset against both attrition and catastrophe withthe consequence that, where there is a combinationof the two, the loss experience has rocketed.

Challenges to the Non-MarineConstruction Market

The long-tail nature of the construction market hasensured greater discipline and a longer period toassess underwriting performance.

However, the non-marine construction sector willcontinue to face challenges:

• The ratings imposed by the various securityagencies will continue to be at the forefront ofthe minds of potential purchasers. There will bea "premium" on top security;

• Insurers are racing to keep abreast of theenhancements in technology and the changingrisk profiles that these cause. This is mostapparent in the energy sector, where the drivefor greater efficiency will continue to stretch thedesign parameters. It is also a factor in “high-rise” buildings, power generation and manyother industry sectors;

• Insurers have seen natural catastrophe losses inareas never previously considered as beingexposed - the recent tsunami, for example - aswell as those located in areas associated withnaturally-occurring catastrophes - hurricanes inFlorida and the Caribbean or earthquakes inJapan and California.

6 Willis Construction Market Review – June 2005

Market Overview – continued

Insurance "cycles" move quite often atunbelievable speed, especially those classes ofcoverage underwritten on an annual basis.However, the construction sector has shown that,whilst historically it follows market trends, it hasbeen far more consistent in recent years.

Willis Construction Market Review – June 2005 7

London and European Markets

The London and European markets remain theworld's most significant providers of risk capacity tothe construction industry.

In the context of market cycles, we are currently ina "softening" cycle. This is due to the favourableexperience over the last three years, supported byimproved terms and conditions. New capacity hasentered the market, although we do not see this ashaving a significant impact on this trend.

The rate of "softening" is not, however, as dramaticas in other associated classes, such as property orenergy. Those markets have much shorter cyclesand generally have a considerable surplus of supplyover demand.

In recent years the construction market's capacityhas never really matured to its fullest potential and,while it has had every opportunity to do so, itsprimary characteristic has been capacitywithdrawal, with an estimated loss in the region ofUSD 175 million during the last four years. Whencompared to its larger counterparts, for examplethe property market, this seems insignificant but,when the worldwide global construction capacity isno greater than USD 1 billion based uponMaximum Probable Loss (MPL), it does represent asizeable proportion.

We are continuing to see fresh new capacitycoming into the construction market and thearrival of the Illium Syndicate (Lloyd's) and Mitsui

Sumitomo last year has provided some renewedrisk appetite.

There are several recent changes of note in theLondon market which should provide alternativeopportunities when seeking new solutions for ourclients:

• Beazley Syndicate at Lloyd's has brought in ateam of four construction underwriters from GEFrankona which has an impressive reputationfor leading many annual programmes andsingle project placements on a worldwideaccount;

• GE Frankona has rebuilt its team and continuesto maintain a high profile as a serious leader inthe construction sector;

• New capacity has emerged from the CatlinSyndicate at Lloyd's, who will focus theirattention on small to medium-sized UK/European contractors;

• Tokio Marine and Fire have transferred theirinternational construction team from Tokyo toLondon.

It is likely that market security ratings will againcome under scrutiny following some of the industrysector's losses. Thus far the impact has beenminimal, with only the regrettable loss ofConverium in Switzerland, now rated by Standard& Poor's as BBB+ and, therefore, falling belowmost brokers' security committee acceptance levels.

London and European Market Overview

8 Willis Construction Market Review – June 2005

The London/European construction markets weredirectly impacted by quite significant volume lossesfollowing Hurricane Ivan. The tragic eventsfollowing the tsunami in the Indian Ocean arealso certain to affect insurance markets, althoughthe extent of claims against the constructioninsurance market seems relatively minor at thetime of going to print.

Insurers are, however, more likely to focus theirclose attention on the aggregation of capacity incatastrophe zones and those zones willundoubtedly be redefined in the coming months.

Insurers continue to focus very heavily on a client'sapproach to risk management and loss preventionand it remains fundamentally important for us toguide our clients on the market's expectationsconcerning identification of hazard, riskassessment/ control and how this is implementedand monitored throughout the term of the policy.

The market is starting to consider once againpackaged-style programmes incorporating marinecargo and the first year of operation. While themarket has some way to go to develop this to itsfullest potential, as was seen in the late 1990s, it isclearly evident that construction insurers arerecognising that the project market is worthy ofconsideration. We would suggest this option isinvestigated on a case-by-case basis, as monetarysavings on premiums are achievable when a varietyof insurance classes are grouped together.

London and European Market Overview – continued

Heavy civil engineering risks (dams, tunnels, etc.)will continue to receive the closest scrutiny.Reinsurance treaty capacity, as well as terms andconditions for such risks, will continue to becarefully managed by those few markets still willingto consider them. Major loss incidents persist in"civils" projects, with one example being therecent collapse of a section of tunnel on the Linea5 in Barcelona and, while the quantum of the lossis still unknown, extensive damage is apparent,especially to third parties.

"Full guarantee" maintenance has historically beena coverage extension available in the constructionmarket, with appropriate deductible and premiumconsiderations. It has been under close scrutinyrecently, especially on project business whereseveral significant capacity providers are nowextremely reluctant to offer this level of coverage.Certain markets consider that the Principal Insuredsshould mitigate their potential exposures with theuse of warranties and guarantees from the keysuppliers and vendors and that their risk of failingto provide a product fit for its intended purposeshould remain theirs, and theirs alone.

Insurers focus on understanding the manufacturers'guarantees in place on all key items of plant andequipment and on having a knowledge of thosecircumstances in which the suppliers'/vendors'guarantees would not be enforceable. Withoutquestion the financial cost of purchasing guaranteemaintenance can be significant, however, theprincipal concern should be whether or not full risktransfer to the commercial insurance markets isachievable on some of the major projects.

Willis Construction Market Review – June 2005 9

Within the tables which follow, we outline aselection of the “Lead” and “Follow” markets, theirfinancial strength rating, capacities and theirpreferred construction business focus. Each markethas at least one dedicated resource for thisspecialisation.

It should be recognised that many global marketcentres have some of the same carriers but these willbe limited to business within their dedicated regionand are more often than not limited by size and/ortype of account they can underwrite without referralto head office. Our aim here is to provide you with acomprehensive summary of global market optionsthat we have at our disposal.

London and European Market Overview – continued

Contractors’ “All Risks”/Erection “All Risks” (CAR/EAR) Markets

10 Willis Construction Market Review – June 2005

*Based on Sum Insured not PML

London and European Market Overview – continued

Company Standard & Poor's PML Capacity CommentaryRating (USD)

GE Frankona A+ 75,000,000 Lead market on International and UK business, bothEAR and CAR. Prefer not to underwrite heavy civilrisks. Currently rebuilding their construction team

AIG* AA+ 100,000,000 Lead market. EAR risks are preferred but areexpanding into some of the larger civils buildingprojects

Generali AA 35,000,000 Prefer long-term accounts contractor business, littleproject involvement. Can write both CAR and EAR

ACE Europe A+ 50,000,000 Mainly UK annuals and UK building projects. Noheavy civils and only support line market for oil, gasand petrochemical accounts. Lead market forpower/utility business in UK and International

Swiss Re AA+ 100,000,000 Major market leader for all industry types

Munich Re A+ 100,000,000 Major market leader for all industry types

Zurich Specialties A- 75,000,000 Major market leader for all industry types

Allianz Cornhill AA- 100,000,000 Lead market for all UK industry types. Utiliseregional offices for business generated outside theUK under £500m. Strong focus on internationalenergy business

Liberty International A+ (Best) 75,000,000 Mainly EAR business only. Lead market capability onoil, gas, petrochemical, power and utilities

Royal & SunAlliance A- 30,000,000 UK domestic business only. Lead market on CAR butnot heavy civil projects

Mitsui AA- 20,000,000 New entrant. CAR business only but limitedappetite for heavy civil projects. Predominantly UKfocus with some European business. Annual andproject business including PPP/PFI

Beazley Syndicate (Lloyd’s) A 50,000,000 New entrant. EAR/CAR business worldwide

Lead Markets

Willis Construction Market Review – June 2005 11

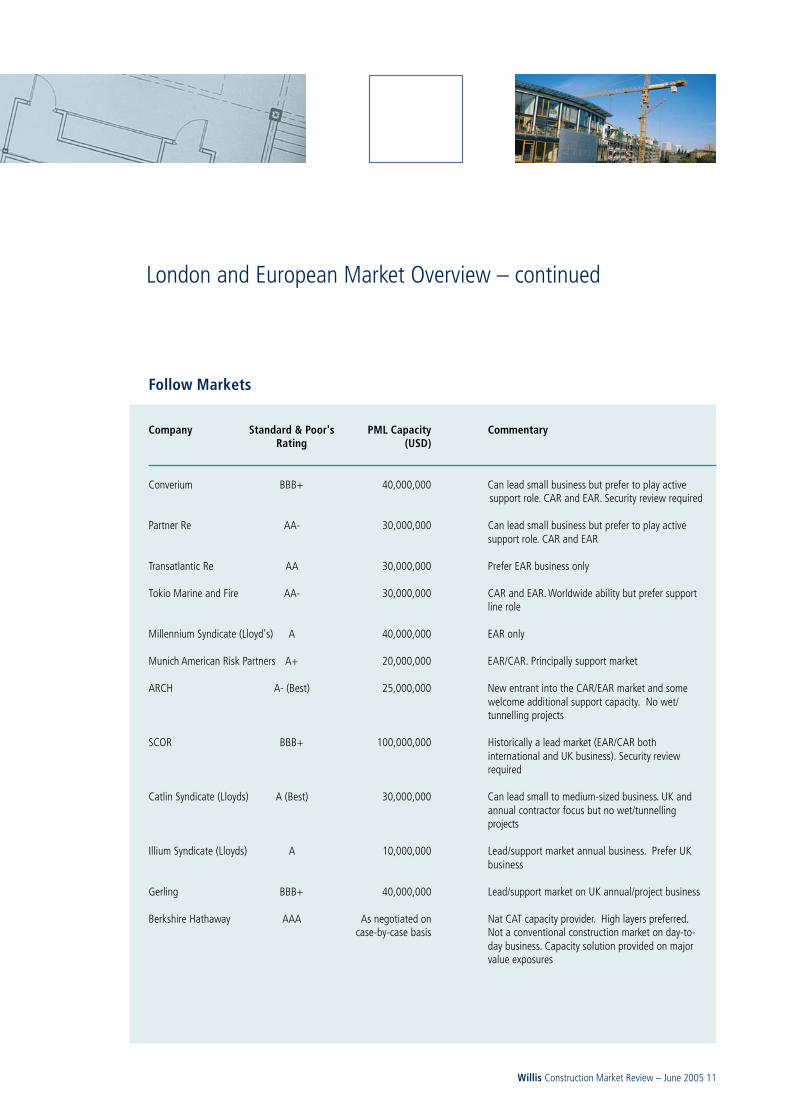

Follow Markets

Company Standard & Poor's PML Capacity CommentaryRating (USD)

Converium BBB+ 40,000,000 Can lead small business but prefer to play activesupport role. CAR and EAR. Security review required

Partner Re AA- 30,000,000 Can lead small business but prefer to play activesupport role. CAR and EAR

Transatlantic Re AA 30,000,000 Prefer EAR business only

Tokio Marine and Fire AA- 30,000,000 CAR and EAR. Worldwide ability but prefer supportline role

Millennium Syndicate (Lloyd's) A 40,000,000 EAR only

Munich American Risk Partners A+ 20,000,000 EAR/CAR. Principally support market

ARCH A- (Best) 25,000,000 New entrant into the CAR/EAR market and somewelcome additional support capacity. No wet/tunnelling projects

SCOR BBB+ 100,000,000 Historically a lead market (EAR/CAR bothinternational and UK business). Security reviewrequired

Catlin Syndicate (Lloyds) A (Best) 30,000,000 Can lead small to medium-sized business. UK andannual contractor focus but no wet/tunnellingprojects

Illium Syndicate (Lloyds) A 10,000,000 Lead/support market annual business. Prefer UKbusiness

Gerling BBB+ 40,000,000 Lead/support market on UK annual/project business

Berkshire Hathaway AAA As negotiated on Nat CAT capacity provider. High layers preferred. case-by-case basis Not a conventional construction market on day-to-

day business. Capacity solution provided on majorvalue exposures

London and European Market Overview – continued

12 Willis Construction Market Review – June 2005

Liability Market

Third Party Liability markets peaked in the firstquarter of 2004, where prices in some instanceshad increased by 100% since 9/11, driven by bothlack of capacity and poor loss records.

They are now in a softening market cycle wherecapacity is again competing for market share andrating is reducing, although not to the dramaticlevels of the property markets. Insurers have haddifficulty meeting their aggressive revenue targetsin 2004 and it appears 2005 will see continuedhunger for business and more price flexibility.

London and European Market Overview – continued

Certain industry sectors will continue to remainchallenging, particularly aviation, rail and risksexposed to the US legal system.

Although pricing is under attack, insurers areresisting a widening of coverage and exclusions ofterrorism, asbestos, toxic mould and silica remain.

The Employers' Liability market is now alsoexperiencing rate reductions. New capacity haseased the difficulties of limited options for clients.However, insurers still require a clear understandingof the client's own Health and Safety programmebefore committing to pricing.

Willis Construction Market Review – June 2005 13

Company Standard & Poor's PML CapacityRating

ACE UK A PL £ 35 millionEL £ 25 million

ACE Global A PL USD 50 millionEur 50 milllion

EL USD 50 millionEur 50 milllion

AIG UK AA+ PL £ 35 millionEL £ 35 million

AIG INT AA+ PL USD 50 millionEL USD 50 million

BRIT A Strong Lloyd's Rating UK £ 15 millionINT USD equivalent

CNA A- UK £ 10 millionINT USD 15 million

DAC A Strong Lloyd's Rating PL UK £ 50 millionEL £ 50 millionPL INT USD 90 millionEL USD 90 million

Frankona A+ INT USD 25 millionUK £ equivalent

New Line A Strong Lloyd's Rating PL UK £ 15 millionINT USD equivalent

QBE A+ PL,EL UK £ 15 millionPL USD 30 million

Liberty A+ PL UK £ 10 millionEL £ 10 million

Illium Syndicate (Lloyds) A Strong Lloyd's Rating PL UK £ 15 millionEL £ 15 millionPL INT USD 22.5 million

London and European Market Overview – continued

Liability Market - continued

14 Willis Construction Market Review – June 2005

London and European Market Overview – continued

Facultative and Treaty ReinsuranceMarket

This renewal season saw reinsurers puttingincreased emphasis on confidence and completetransparency in the underwriting ability of theircedants. This has led to ever-more detailed renewalpresentations including everything necessary toanalyse and rate a treaty. It was also apparent thatreinsurers continued to refine the requirementsthey had set during the 2003 and 2004 renewalseasons.

Reinsurers need to understand, and agree with,their cedants' approach to managing the marketcycle. Tighter profitability targets are beingadhered to on treaty business, with deductionscoming under increasing pressure.Reinsurers are continually enhancing theirinformation requirements, including that for originalUltimate Nett Loss Ratio projections, broken downby attritional, severity and natural perils'experience. Reinsurers have placed greateremphasis on pricing and expect cedants to monitordevelopments in this respect. As the inherentnature of our business is cyclical, this is part of theirchange in outlook from being "reactive" to"proactive", so as to avoid the largely reflexreactions experienced in the past.

To an extent this new attitude reflects the growinginfluence of actuaries in the business and mostmajor reinsurers now employ dedicated teams.

There is pressure on proportional treaties, wherequestions have been raised as to the viability ofceding too much "good" business to reinsurersversus paying away a lesser amount of premium forExcess of Loss cover. What is called for now is a"hybrid" to maintain the characteristics of"partnership" associated with proportional,combined with the lower economic cost of Excessof Loss, and we are actively working towards asolution.

There has been a lot of resistance from reinsurersto new direct capacity entering the market, evenwhen this has been as a result of experiencedteams moving.

Rating movements for construction projects remainfirm but annual covers are coming underdownward pressure. Property markets are onceagain encroaching on Operational "All Risks"covers and causing some reduction in rates. So farwe have not seen the same pressure applied toconditions or deductibles, which remain firm.

Willis Construction Market Review – June 2005 15

Asia Pacific

The Asian construction reinsurance market hasdeveloped rapidly over the past ten years or so to aposition today where significant capacity exists forAsian-based construction projects.

To talk of Asia as a single marketplace is tounderestimate the influences of the local marketsand traditions that remain. Many locationsmaintain strict non-admitted policies, as well ascompulsory requirements to reinsure withgovernment-owned companies. Having said this,the markets of Singapore and Hong Kong have animportant regional role to play for Asian-basedprojects and provide much of the facultativecapacity required for the larger CAR and EARplacements.

Hong Kong and Singapore

Most major CAR and EAR reinsurers have aregional presence in either Hong Kong orSingapore, and often both. Companies in manyinstances have arranged their underwritingguidelines so that Hong Kong responds to projectsin northern Asia and Singapore to southern Asia.The majority of the capacity available is provided bythe 'international' reinsurance companies fromEurope and America with very little capacityavailable from Asian reinsurance companies. Mostof these international firms have dedicatedengineering underwriters on staff, plus risksurveyors servicing construction as a dedicated lineof business. These underwriters' access to Groupcapacity is generally high, with referral to HeadOffice only required for the very largest and mostunusual risks. It is, therefore, true to say that thebest place to find reinsurance capacity for an Asian-based construction project is in Asia.

The Asian insurance market has traditionally beencompetitive when compared to Europe and theUSA and this remains broadly true today.International companies continue to view Asia as along-term growth market and are disposed to offerclients attractive pricing in order to improve theirpenetration and grow their top line revenue.

Willis Global Overview

16 Willis Construction Market Review – June 2005

Willis Global Overview – continued

China

As can be seen from Figures 1 and 2, China isbecoming the largest and most dynamicconstruction market in the world. It is also a marketwhich is constantly changing from an insuranceand reinsurance view point.

Major treaty reinsurance deals offered in the 1990sand early 2000s, coupled with a very restrictivelegal environment where essentially only threeinsurers were able to transact business, has createda market where price has been virtually the onlycriteria on which the insurers could differentiatethemselves. Pricing of standard CAR and EAR

insurance products has been somewhere in theorder of 50% of the rate attracted by similarprojects outside of China.

The restrictive market has, however, discouragedinnovation in the area of policy coverage and/orvalue added services, such as risk engineering andrisk management. Coupled with security concerns,this has resulted in most of the majorinternationally-funded projects seeking to partnerthe Chinese insurers, along with their traditionalinternational reinsurance providers.

US$bn 600

Figure 1 Global constructionSpending 2003

800200 400

USA

Japan

China

Germany

Italy

France

UK

Brazil

Spain

Korea

Mexico

Australia

India

Hong Kong

Other countries

Source: DLSI and Global Insight (2003)

Figure 2 Global constructionSpending 2003-04

Source: DLSI and Global Insight (2003)

% 6 82 4 10

Japan

China

Germany

Italy

France

UK

Brazil

Spain

Korea

Mexico

Australia

India

Hong Kong

Other countries

USA

Willis Construction Market Review – June 2005 17

The gradual deregulation of the Chinese insurancemarket following China's membership of the WTOis starting to have some effect, with a greaterdegree of choice for the insurance buyer in China.Restrictive requirements on policy forms previouslygoverned by the China Insurance RegulatoryCommission (CIRC) are now showing signs ofbeing more flexible and the number of foreigninsurers licensed to transact business in China isever increasing.

Capacity still exists and very attractive pricing forthe right type of project can be achieved if acarefully planned marketing strategy is adopted bythe client. Significant risks, such as tunnels, gas-fired turbines and major oil and gas projects, oftenfall outside the local market's treaty arrangements,requiring lead and support capacity from theLondon and European reinsurers on a facultativebasis. Delay in Start-up insurance is also a treatyexclusion for the domestic insurers, again requiringan international approach to the marketingstrategy.

Willis Global Overview – continued

18 Willis Construction Market Review – June 2005

Willis Global Overview – continued

Australia

The tough insurance market conditions experiencedby contractors in recent years have easedconsiderably in the past twelve months. The marketgenerally is now providing adequate capacity for allproject types and is competing vigorously for good,well-engineered risks. The reputation of thecontractor, as well as a good claims history, stillattracts discount from insurers.

Our marketing strategies last year involved morediscussion about the quality of projects, contractorreputation, risk engineering and risk managementof the contract than in previous years. This willcontinue in 2005. Whilst the market is not soft byany means, it is eager to write well-structuredprogrammes that are presented professionally.

We see the market in Australia softening further in2005/2006. Major world disasters have had littlefinancial effect on the Australian insurance market.Local insurers had very positive results in 2004,reporting good underwriting results and increaseddividends to shareholders from record profits.

Executives of the major insurers need to grow theirbusinesses to meet shareholder expectations. Webelieve this will lead to even more competition andinnovative approaches to marketing and sales.Interest rates are low by historical standards andany upward movement will create an environmentfor premium rate reductions.

Whilst the Australian market is still competitive, theLondon market has always provided a more

sophisticated approach and greater capacity, withbroader wordings for those clients who believecover is the most important issue. We areconstantly reviewing policy coverage with ourmajor Australian insurers.

Our predictions in relation to key market segmentsand policy types are as follows:

CAR/EAR Market

Since December 2003 we have seen a generaleasing of rates in the Australian market, particularlyin relation to the building sector.

Civil and mechanical engineering risks are stilltreated with caution by leading experiencedinsurers, with each project being rated on its merits.

It is, therefore, vital that the project andconstruction methods, contract conditions andmanagement of risk are fully understood so thatthe project is considered in the best possible light.Failure to do so will see the insurer erring on theside of caution and loading the rate to compensatefor the unknown.

The engineering insurance market in Australia is, forthe most part, controlled by the two leading globalreinsurers, Munich Re and Swiss Re, who influencelocal insurers in both the scope of coverageprovided and the level of premium rates charged tocontractors.

Willis Construction Market Review – June 2005 19

Willis Global Overview – continued

Whilst premium rates may be in decline, there is astrong tendency among local insurers to restrictcoverage by issuing their standard policy wordings,which leaves the contractor exposed in critical riskareas.

Willis Construction has fought hard to achieveacceptance of bespoke wordings and we currentlyhave manuscript wordings agreed with most majorinsurers.

The past 12 months have also seen the entry intothe market of a number of smaller insurers orunderwriting agencies. Some of these are notacceptable to principals or Willis Construction.Restrictive policy wordings are again an issue withthese markets.

Capacity in the local market has increaseddramatically over the past six months and it ispleasing to note that a large proportion of localprojects can now be placed in the Australianmarket.

Third Party Liability Market

An over-reaction by insurers during the "hard"market cycle caused rates to escalate and policydeductibles to rise dramatically. This situation isnow easing and we are seeing a reduction in ratesof between 10% - 15%. However, this variesdepending on the contractor's claims record.

Insurers also became extremely concerned aboutwhat are termed "Worker to Worker" claims, to theextent that in some cases contractors had difficultyin obtaining coverage for injury caused tosubcontractor employees. Recent governmentlegislation in most states has lessened the "Workerto Worker" threat to some degree. However, it isstill an issue with some insurers imposing highexcesses.

It is also of interest to note that various statejurisdictions within Australia have introduced"Serious Injury" legislation, essentially aimed atceasing the flow of smaller bodily injury claims byhaving minimum thresholds on pain, injury or lossand putting more onus on individuals to take care.Early evidence indicates that the number of CountyCourt writs issued for bodily injury claims havefallen by 75% in some states. This means lessclaims and presumably less premium. Someinsurers who exited the market in 2003 are now re-entering following evidence of a more sensiblelitigation approach by the governments and thecourts.

20 Willis Construction Market Review – June 2005

Willis Global Overview – continued

As with the contract works policy, coverage is thecritical issue for third party liability. The last fewyears have seen some insurers introduce wordingsinto the market that, in our view, clearly do notaddress the contractor's exposures.

The London market has traditionally been moreresponsive to providing appropriate coverage,generally by acceptance of the broker formwordings, and there is still a flow of Australianplacements into London.

Once again Willis Construction has maintained itsagreed third party liability wordings with localinsurers.

Excess layer liability premiums have reducedwhilst capacity has increased. This market isusually supported by the large American-basedinsurers through their local representatives.Premiums for limits in excess of AUD 20 millionare priced extremely competitively for most risks,other than larger rail, bridge or tunnellingcontracts.

Latin America

The Latin American local/regional market tends tobe more competitive than the international marketson most construction risks. The main reason for thisis that there has been a lack of major projects insome of the territories and wordings required arenormally standard Munich Re forms.

The major capacity is provided by Munich Re,Swiss Re, AIG, Zurich and SCOR who haveapproximately USD 50 million capacity each butthis can be increased with additional capacityfrom headquarters in Europe/US in some cases ifneeded.

Recently windstorm capacity has been reducedfollowing the 2004 hurricanes and the market hasseen restricted cover, sub limits and increased ratesin this respect. The provision of earthquakecapacity also requires strenuous, challengingmarketing efforts, particularly in Chile, Mexico,Ecuador and Central America.

Energy projects have seen the most investment inLatin America, along with mining and metalprocessing. Infrastructure projects, such as majorroads and airport expansions, are expected tofeature extensively in the immediate future.

Willis Construction Market Review – June 2005 21

Middle East

This has been a very active market for the pastfew years, due in part to the recent surge in oilprices and the opening of some new markets.Approximately USD 300 billion of investmentprojects are planned or taking place in the region,from energy to real estate and infrastructureprojects.

The energy-related project sector has traditionallybeen the most active and important in the MiddleEast requiring the involvement of the internationalmarkets and, therefore, the application ofinternational rates. In recent years, with the onsetof major real estate and infrastructuredevelopment, the Middle Eastern market trend hascontinued to experience extremely competitiverates, especially on risks with a lower PML, whencompared to the international markets. Theabundance of local insurers in certain states willingto underwrite risks at extremely small margins andat competitive rates in order to win the businesshas resulted in rates unheard of in other markets.Rates for civil structures, e.g. 30-70 storeybuildings, can be priced between 0.09% - 0.15%.To a limited extent the markets have seeninternational rates applied when requiring supportfrom the major international carriers on higherPML risks.

Willis Global Overview – continued

Some local insurers do have large capacitiesunder their treaties. However, most insurers placefacultative reinsurance in the regional market.Wet risks are generally excluded under mosttreaties and are, therefore, priced by the leadinginternational reinsurers.

For major developments, most states do not allownon-admitted policies. Therefore, the business offronting and utilizing the local and government-owned insurance companies is another tactic toenhance revenues.

There are some local insurers with "A" ratedsecurity and some of the global players do have aregional presence, such as Allianz, AIG and RoyalSunAlliance.

22 Willis Construction Market Review – June 2005

United States of America

Construction in the US shows signs that 2005 willhave stronger growth compared to 2004, withcommercial work starting to pick up again afterseveral years of uncertainty. We expect this growthwill differ by region, with the industry continuing togrow faster in the residential sector, and all areas ofthis type of construction (from homebuilding tomulti-family to military housing) experiencingsignificant growth. At this point, residentialconstruction represents over 50% of totalconstruction in the US and this percentage isgrowing.

This presents significant challenges for insurancecarriers, as they have yet to understand fully how toaddress adequately the risk exposures associatedwith this sector, specifically from a constructiondefect perspective (completed operations andproperty damage coverage). We expect that, in thelonger term, the insurance industry will developnew products to help but, in the short term, mostbuilders will struggle to get affordable coveragewhich truly addresses their risks.

In non-residential construction, we expect modestgrowth in work programmes in 2005. Street androad, general building in the areas of health careand education, and sewer/water projects shouldincrease this year. Education continues to be anarea of great need and state-wide bond issues inseveral states will increase construction activity. Ingeneral, these types of work are viewed favorablyby the industry, with a few exceptions related tocertain building systems (EIFS for example) which

can be problematic from a long-term coverageperspective.

Overall, we expect a good year for theconstruction economy as demonstrated by the USDept. of Commerce table opposite, althoughpressures on the industry will continue due toswings in the price of materials, including fuel,and from the uncertainty of risk managementtools as the insurance industry continues to adjustits appetite for different risks.

Key Insurance Challenges for 2005

Many of the challenges in 2005 will be acontinuation of the trends in insurance that wehave seen for the last few years, such as:

1. Underwriters' inability to address fully riskexposures in the residential sector;

2. Coverage restrictions and changes, includingthe new Additional Insured wordings;

3. Specific state issues which cause each carrier tohave a different view of risks depending onjurisdiction. New York and Illinois are two stateswhere statutes have reduced carrier appetitesfor General Liability;

4. Continued lack of support for certain types ofconstruction systems -EIFS is a good example;

5. Uncertainty in the market due to underwriterconsolidations and the entrance of newinsurers.

Willis Global Overview – continued

Willis Construction Market Review – June 2005 23

Commercial Workers' Commercial General Umbrella AverageAuto Comp Property Liability

3Q 2004 -2.5% -2.7% -10.7% -5.3% -3.6% -5.0%2Q 2004 0.5% 1.0% -9.3% -1.1% -1.3% -2.1%1Q 2004 3.1% 4.3% -6.0% 2.6% 3.9% 1.6%4Q 2003 7.9% 8.8% -0.7% 6.3% 10.9% 6.6%3Q 2003 7.5% 10.0% 1.2% 8.1% 11.5% 7.6%High 28.6% 24.9% 45.4% 26.0% 51.9% 35.3%Low -2.5% -2.7% -10.7% -5.3% -3.6% -5.0%

By-Line 3Q 2004 Rate Changes Ranged From -10.7% to -2.5%

Willis Global Overview – continued

Source: Council of Insurance Agents and Brokers. Table prepared by Lehman Brothers Equity Research

PERCENT CHANGETYPE OF CONSTRUCTION 2003 2004 2005 03-04 04-05

TOTAL CONSTRUCTION 915.7 1,000.2 1,058.0 +9.2 +5.8Residential 482.9 550.5 592.0 +14.0 +7.5Lodging 11.1 11.8 12.2 +6.3 +3.4Office 41.5 44.8 47.5 +8.0 +6.0Commercial 62.3 64.8 67.4 +4.0 +4.0Health Care 29.9 32.9 35.5 +10.0 +7.9Educational 74.2 74.9 77.2 +0.9 +3.1Religious 8.5 8.2 8.3 -3.5 +1.2Public Safety 9.0 8.7 9.0 -3.3 +3.5Amusement and Recreation 20.0 20.0 20.4 0.0 +2.0Transportation 25.3 25.6 24.8 +1.2 -3.1Communication 12.5 12.5 12.5 0.0 0.0Power 33.2 33.9 34.9 +2.1 +3.0Highway and Street 62.9 67.9 70.6 +8.0 +4.0Sewerage and Waste Disposal 13.7 14.8 15.5 +8.0 +4.7Water Supply 10.4 10.6 11.1 +1.9 +4.7Conservation and Development 4.0 4.2 4.4 +5.0 +4.8Manufacturing 14.3 14.2 14.6 -0.7 +2.8

U.S. Dept. of Commerce Construction Put-in-Place USD billions

Source: U.S. Dept. of Commerce Figures for 2004 are estimated. Federal industrial includes weapons R&D and production, atomic waste isolationand reprocessing and environmental cleanup; conservation and development, includes electric power dams.

24 Willis Construction Market Review – June 2005

All of these are expected to have an impact in2005, although the market had already started toflatten in 2004. In primary casualty lines,moderation in increases marked early 2004 andmore competition impacted the pricing for mid tolate 2004; we expect that trend to continue. Eachof these trends will need to be understood bycontractors, owners, designers and suppliers inconstruction, as they should be key considerationsin the construction continuum.

This competition was driven by increased profits inthe insurance industry as rate increases over thelast three years have started to have an impact onindustry results. The Council of Agents and Brokers,for example, has measured pricing trends for theindustry as a whole and its survey results areshown on page 23. Construction is consideredamong the most hazardous industries and, as aresult, pricing has not fallen quite as fast as inother industries. However, the fact remains thatthere has been evidence of increased competitionfor construction accounts in 2004.

It is important to note that, while pricing by line issoftening, there are hidden rate increasesthroughout the underwriting process as coveragesare being significantly restricted. The total impactof this narrower coverage will not be fully knownfor some time.

Coverage restrictions: The latest coveragechanges in General Liability center on AdditionalInsured forms. The industry has re-filed these formsto narrow the amount of coverage available toAdditional Insureds, which will cause generalcontractors and owners to rethink the drafting oftheir construction contract requirements. Theseendorsements have historically been used to allowowners and general contractors to pass significantamounts of risk (including in many cases solenegligence) to subcontractors' insurance policies.The new endorsement wording restricts thatcoverage to only those instances where thesubcontractor had some negligence. This will,potentially, have a major impact on the ability ofthe general contractor to pass losses, such asAction Over cases, back to the subcontractors'policies.

In addition, there has been movement in theindustry to start excluding silica-related losses ingeneral liability. This is in response to adeterioration in the history of losses from long-termsilica exposure, which started to accelerate as anissue in the second half of 2004.

Willis Global Overview – continued

Willis Construction Market Review – June 2005 25

Market consolidations and new players:The impact of uncertainty and new capacitytypically means an increase in competition andmarketing of insurance programmes. When thisoccurs, it is not uncommon for contractors todevelop new insurance partnerships andprocesses. The new capacity has come from bothtraditional insurance companies expanding theircorporate appetites and completely newcompanies entering the market. This has been keyto the stability of pricing in the 2004 market. Ithas also put pressure on the legacy carriers, whichare still filling holes from poor experience in the1990s as the new carriers are starting with cleanbalance sheets which allow them to offer adifferent approach to certain risks. 2005 will seean increase in activity of these new markets witha related increase in personnel changes in theinsurance industry as underwriters and supportstaffs are built.

Builders' Risk

These lines were very competitive in 2004 withprice decreases being the rule. Appetites were highfrom a number of carriers which caused rates todrop and coverages to expand. The impact of therecent storm season may temper this appetite forcatastrophe regions, but in many cases, thoselosses were within substantial deductibles, whichmeans losses may not have a major impact on the

line countrywide. Builders' Risk is showing signsof additional capacity coming into the market,including London-based underwriters. Individualcapacities can accommodate risks in excess ofUSD 100 million readily. Coverage expansion intocontingent areas does not appear to be likely(force majeure, liquidated damages, and efficacyall have little or no capacity available).

Willis Global Overview – continued

26 Willis Construction Market Review – June 2005

Willis Global Overview – continued

WrapUps

The WrapUp marketplace has changed in the lastseveral years as carriers have started to becomemore cautious. Several carriers have shifted theirfocus from Owner Controlled InsuranceProgrammes (OCIPs) to Contractor ControlledInsurance Programmes (CCIPs) as they perceivethat contractor results have a better claims history.However, there are many situations where OCIPsare still successful.

WrapUp markets have reduced from over seven tojust three or four. In addition, WrapUps havemorphed from individual major single site projectsto entire work programmes called "RollingWrapUps". These have been used by both ownersand contractors, including residential homebuilders.In many respects, the approach has moved back tothe original goal of WrapUps: to ensure coverageconsistency and coordinated claims handling on asite.

As coverage continues to deteriorate, many ownersand major contractors see this approach as a goodway to assure coverage consistency. This willpresent challenges for contractor participants dueto the need to coordinate their other coverages, butthe trend toward controlling insurance placementsin the face of continuing deterioration of coverageon individual contractors’ policies, will continue.We also expect new types of WrapUps to emergeincluding "General Liability-only WrapUps" -coordinated programmes where the owner andcontractor have a joint interest in the outcome ofthe WrapUp from a financial perspective.

Conclusions

2005 will feel both more competitive from aninsurance standpoint and, at the same time, morechallenging for the construction industry. Whilepricing seems to be moderating and shouldcontinue to become more competitive, coverageterms will vary widely on General Liability and theentire concept of contractual risk transfer will needto be looked at closely. New insurers will beentering the market, while legacy carriers attemptto both fill holes and confront the new competition.Contractors will need to take a hard look at theirbusiness strategies related to residential work,including apartments and condominiums, andunderstand that long-term risk financing optionsmay require different approaches to risk. It will bea year in which contractors will need to spend moretime understanding their coverages and how theymay impact their business appetites and, ultimately,their bottom lines.

Willis Construction Market Review – June 2005 27

Bermuda

CAR/EAR Market

Although the Bermudian market has grownenormously since 9/11, there are still only a limitednumber of carriers writing construction business.

Construction is a target class for Endurance whowant to write this on a quota share basis and haveUSD 50 million capacity, but they will only considerwriting North American business out of theirBermudian office.

Ace Bermuda are also keen to write constructionbut only on an Excess of Loss basis and theirappetite is normally for the top layers, where theyhave USD 50 million capacity. However, Ace willlook at the more unusual coverages, such as Delayin Start-Up as a stand-alone placement without thephysical damage. This can be a very useful methodof completing large placements, but this is notAce's first choice on construction business and they

still require this to be Excess of Loss. Ace Bermudaaccess the same capacity as Ace Europe.Montpelier Re will happily write construction butonly if it is Excess of Loss and if the premium isacceptable. It is not a target class of business forthem but something they are willing to commit to ifthe deal is right.

All of the markets are prepared to write up to five-year policies.

Liability Market

Ace, Endurance, Starr, XL and AWAC are all happyto write casualty for construction risks, but theopportunities are few because they can all beapproached in London/Europe and that is wheremost brokers have their expertise.

Willis Global Overview – continued

28 Willis Construction Market Review – June 2005

Marketing Strategy

Willis fully recognises that each individual clienthas bespoke needs and risk transfer requirements.It is fundamentally important to map out clearly aplatform for marketing in order to ensure that thechosen strategy factors in all possible options.

The point of access to insurers remains a crucialdecision from the outset of any programme'splacement in order to ensure that the best possibleinfluences are brought to the negotiating table.

The key to the success of the placement often liesin the selection of the market and especially theleader, who should work in partnership with and besupportive of the client at every opportunity. Thiswe actively encourage from the outset.

Marketing strategy needs to be based around keyprinciples in order to achieve the best product atthe most competitive terms and conditions. Theseare:

• a clear understanding of the design andexecution methods of a project;

• an intimate knowledge of the appetite and keyissues of the major players in the constructioninsurance market;

• the proven ability to maintain a competitiveedge throughout the market tender process;

• the design of a broad form and tailor-madepolicy coverage;

• achieving the optimum balance betweencontractual risk allocation, risk retention andrisk transfer;

• involving our clients in the marketing process atevery step of the way.

It remains critical that sufficient time is allowed formarketing. The buyer and their broker must ensurethat they have total control of this process from thequotation stage all the way through to the finalplacement.

A successful placement should always start fromsolid foundations and the depth and quality of theunderwriting submission is absolutely crucial in thisprocess. Knowing and understanding what theinsurance market needs to evaluate fully a client'sprogramme is paramount.

Willis Construction Market Review – June 2005 29

Professional Indemnity (PI)

In common with other sectors of the insurancemarket offering risk transfer solutions to theconstruction industry, the late 1990s saw theglobal PI market experience an acute reduction incapacity, resulting in a rapid increase in premiumrates and narrower coverage options being offeredas the hard market took hold for a three yearperiod from mid-2001.

Whilst the revitalisation of this market has beenless spectacular, the introduction of new financialcapacity has resulted in a reduction in premiumrates, with 10-15% commonly achieved in 2004.

However, insurers are increasingly taking a moreselective approach to the risks they accept.

Programme design remains key to ensure that theincreased capacity is utilised to secure the bestpossible value from a risk transfer programme.

As the hard market of the last few years began tounwind in 2004, insurers continued to differentiatebetween risks, with those insureds able todemonstrate sound, effective risk managementsecuring more significant rate reductions andtechnically broader coverage. During this period, itbecame possible to obtain enhanced coveragewhere total exclusions were previously the norm;Asbestos and Terrorism being two prime examples.

Primary Lead Primary Follow Excess Lead Excess Follow

DAC Amlin Wurtt Swiss ReACE Newline GE MAGMarkel Great Lakes HannoverMitsui SVB CNAHeritage AWAC QBEBeazleyHiscoxCatlinMarketformWR BerkleyZurich

RSA

All primary lead markets shown above will also act as follow markets and will lead/follow excess layers.

The key markets for Professional Indemnity insurance are as follows:

Associated Product Reviews

30 Willis Construction Market Review – June 2005

Political Risks

Terrorism remains a standard exclusion in theinternational construction/engineering "all risks"market and looks likely to be excluded for theforeseeable future. As the property andconstruction carriers are no longer able to provideonshore terrorism cover due to reinsurance treatyexclusions, the stand-alone terrorism market hasrapidly responded to global demand. The WillisTerrorism Practice is at the forefront of placing anddeveloping business in this evolving market and isconsidered a market leader.

Market capacity continues to grow. There havebeen notably few new entrants with increasedcapacity coming mainly from the existing market,which has, in turn, created competition andreduced rates. The total amount of commercialcapacity now stands in the region of USD 750million but the availability of that capacity is verymuch dependent on underwriters' aggregates andthe territory where the risk is situated.

As competition continues, a section of the stand-alone terrorism market is providing policies on alonger term basis, commonly 36 months, butperhaps up to 48 months. Between Lloyd's, AIGand Bermuda, we anticipate that up to USD 300million is available for these longer term policies.

Alternatively USD 250 million capacity can beprovided through OPIC (Overseas PrivateInvestment Corporation). This is a relatively newarrangement and can only be accessed where

Associated Product Reviews – continued

there is significant US ownership or as areinsurance of a US insurance company.

The immediate outlook for the Terrorism market, inthe absence of a major event, appears to be one ofgrowth in the face of continued strong demand. Italso appears that there remains pressure on themarket to keep driving premium rates down. It isimportant to note that the Terrorism marketremains vulnerable to a major insured event, whenit is strongly anticipated that prices would againrise and capacity suffer from withdrawal.

Willis Construction Market Review – June 2005 31

Inherent Defects Insurance

Inherent Defects insurance continues to be a veryspecialist line of insurance. Although there arevariations in coverage dependent upon the insurer,the policy is still largely based upon a commonform.

The total market capacity is approximately £150million for UK business only and is providedthrough an established panel of Aviva (NorwichUnion), Munich Re, Swiss Re, Allianz Cornhill,SCOR and Gerling. There is currently littlelikelihood of either a broadening of policycoverage or an increase in available capacity.

Inherent Defects insurance is available fortraditional building projects (office blocks, shoppingcentres, mixed developments etc). There is stillreluctance by insurers to consider heavy civil works(tunnels, bridges or dams).

Most policies are underwritten in the UK, althougha number of contractors, developers and consortiahave effected policies throughout the EU (wherelegally permissible) and within Middle Eastern andFar Eastern territories; such placements are oftendriven by contractual obligation, e.g. lenders'requirements. The provision of this coverage forprojects outside the UK largely restricts themarketing options further to Swiss Re, Munich Reand SCOR.

A number of EU territories, along with Australiaand Canada, are subject to, or are in the processof adopting, legislation that requires themandatory provision of cover for defects inbuildings. Such cover linked to statutoryobligations is normally provided by local specialistinsurance markets.

The most notable insured loss in this market wasthe recent terminal collapse at Charles de GaulleAirport for an estimated £75 million claim.

Marine Cargo

Over the last few years, the Project Cargo markethas remained fairly stable and has tended to followthe fortunes of the cargo market as a whole intohard and softening cycles.

However, cargo rates are sometimes drivendownwards when full Delay in Start-Up (DSU) isincluded. This arises from the fact that insurers canlook at the overall premium spend and, ifacceptable and as the covers are placed together,make allowances.

The marketing of projects including DSU variesdepending on size in that, whereas the overallmarket capacity is in the region of USD 400 - USD500 million, it is only on those with a large limitwhere the pricing is flat. There is much morecompetition when there is a combined limit lessthan USD 100 million.

Associated Product Reviews – continued

32 Willis Construction Market Review – June 2005

Associated Product Reviews – continued

Typically, underwriters' lines would not be morethan USD 25 million combined vessel limit and DSU(with a few exceptions) and many would be aroundUSD 10 million but, as there are at least 20 playersin London alone, there remains no shortage ofcapacity.

With the increase in Corporate capital in Lloyd's,coupled with the pressure on underwriters forincome, we have seen instances where most Cargounderwriters are prepared to lead the class. Thismay seem a good situation for clients but it doeshave its drawbacks.

This is very much a specialist class of business, notso much from an engineering point of view butfrom a position of understanding the risk - thelogistics, timelines, handling and risk management.The established leaders would utilise the services ofa supervisory surveyor to assist in managing theprocess and, although the client pays for this, it isundoubtedly to the benefit of all.

We prefer to work with recognised leaders (albeitin a competitive situation) and they would includethe following:

St Paul; ACE; RSA; Allianz; AIG; LibertyInternational; ERC Frankona.

This list is not exhaustive but it is probable thatthe lead on any given project would come from it.They are all also prepared to follow.

Going forward, and in line with the cargo market,we would anticipate some softening in rates -probably around 10% reduction from those in thelast two years - but little change in policy wordings,which are already fairly extensive.

The trend among clients to achieve premiumsavings has been with the use of largerdeductibles/self-retention. The normal cargodeductible is between USD 10,000 - USD 25,000and for DSU 30 days but we are increasingly beingasked to quote with USD 50,000 - USD 100,000and 45, 60 or even 90 days for DSU.

This has the effect of removing the "run-of-the-mill" and attritional type claims, while protectingthe project from catastrophe losses, and we seethis trend continuing.

Project Principals are becoming more sophisticatedin their purchasing of insurance and projects arebenefiting from supervision surveyors workingalongside risk managers to a mutually beneficialend. The whole class has moved from one of risktransfer to one of risk control.

Willis Construction Market Review – June 2005 33

Market Security

with the approved list of carriers, which is held ona global electronic system, is mandatory.

Willis operates security guidelines which are basedon rating and financial size. These standards are asfollows:

• Minimum rating: A- financial strength ratingfrom A.M.Best's/Standard & Poor's orequivalent rating agency

• Minimum policyholders' surplus (shareholders'equity):

– USD 100 million for international carriers

– USD 50 million for North Americanproperty/casualty carriers

– USD 75 million for North American life/health carriers.

Willis' Market Security Department has threeanalysts who each have over ten years' experienceassisting clients in the event that a carrier becomesinsolvent, goes into provisional liquidation,rehabilitation or orderly run-off.

Interest in and awareness of market security issuesis growing all the time, as companies increasinglyfocus on protecting their balance sheets. Willis'market security function is a vital tool in providingsupport to our clients.

Willis monitors closely the security of insuranceand reinsurance markets worldwide. We seek toensure, as far as we are reasonably able, that ourclients' risks are placed with secure and solventcarriers, who will meet valid claims as and whenthey fall due. Whilst we do not guarantee thefinancial strength or solvency of any carrierutilised, Willis does attach the highest priority tosecurity issues.

Willis has a team of 25 professionals globally,trained in a range of disciplines, including financialand management accountancy, insurance, banking,insolvency and general research. This includesanalysts who have particular responsibility andexperience in respect of Lloyd's of London.

Willis' Market Security Department monitors allcarriers in use on an annual basis, which requiresan in-depth understanding of the factors andinfluences affecting different markets around theworld. The review includes consideration of theopinions of rating agencies and marketcommentaries worldwide. Comprehensive factualreports on carriers can be made available to clientsupon request.

Market security decision-making is theresponsibility of the Market Security Committee,which comprises members of the Willis PartnersGroup, again reflecting the importance assignedwithin Willis to this function. In addition, anAnalytical Review Committee meets on a weeklybasis to consider which carriers should be approvedand to monitor market developments. Compliance

34 Willis Construction Market Review – June 2005

The construction market will continue to servicethe needs of its client base throughout 2005 andbeyond.

Renewed interest in the form of new capacity willprovide certain industry segments with alternativeoptions and at every opportunity these should beinvestigated.

Doubt remains as to whether the 2004 naturalcatastrophes will directly impact premium ratingstructures in the construction market.

Insurance markets are likely to focus primarily onaccumulated capacity commitments which willaggregate across a combination of insuranceclasses.

Whilst we see signs of premium reduction acrossthe majority of our industry client segments, certainsectors, for example, the civil engineering sector,will remain tough for some time to come.

Client and insurer relationships allowing totaltransparency should always be encouraged and wesee this being a key issue moving into this year.

Insurers will continue to have a greater focus onthe extent of policy coverage over premium and wesee this trend being maintained throughout thisyear in certain industry sectors which haveconsistently sustained heavy losses.

Summary and Prognosis

Willis Construction Market Review – June 2005 35

36 Willis Construction Market Review – June 2005

Willis Group Contributors

London Ten Trinity Square,London EC3P 3AX+44 (0)20 7488 8111

David G Turner Chief Executive Offiicer, Willis Construction Risks

Richard Maxted Executive Director, Willis Construction Risks

Alistair Urquhart Executive Director, Willis Construction Risks

Maria Sanchis Latin America, Willis Construction Risks

John Latter Marine Cargo

Mike Quy Treaty Reinsurance

Nick Rudnai Professional Indemnity

Toby Wemyss Political Risks

Willis Construction Market Review – June 2005 37

Willis Group Contributors

Worldwide

Australia Willis Australia LimitedMike Griggs Level 10, 71 Queens Road

MelbourneVictoria 3004Australia+61 3 9529 5122

Bermuda Willis (Bermuda) LimitedPaul Blackmore F B Perry Building

40 Church Street, PO Box HM 1995Hamilton HM HXBermuda+1 441 295 1272

Dubai Al-Futtaim Willis (Pte) LtdTalal Soghaier PO Box 152

DubaiUnited Arab Emirates+971 4 206 8307

Hong Kong Willis China (Hong Kong) LtdMatthew Hooker 3502 The Lee Gardens

33 Hysan AvenueCauseway BayHong Kong+852 2830 6678

USA Willis Construction Practice USAPaul Becker One Century Place

26 Century BoulevardNashville, Tennessee 37214USA+615 872 3464

38 Willis Construction Market Review – June 2005

Notes

Willis Construction Market Review – June 2005 39

Notes

40 Willis Construction Market Review – June 2005

Notes

2841 Willis Construction Risks COVER.qxd 07/06/2005 11:04 Page 3

4 Willis International Construction Market Overview May 2004

Willis Limited

Ten Trinity SquareLondon EC3P 3AXTelephone: +44 (0)20 7488 8111

www.willis.com

If you need any more information or need to address any specific enquiries please contact

David Turner

Chief Executive Officer Willis Construction Risks

Tel: +44 (0)20 7488 8738

Richard Maxted

Broking Director Construction Risks

Tel: +44 (0)20 7488 8937

Alistair Urquhart

Executive Director Construction Risks

Tel: +44 (0)20 7488 8949

CON/2177/05/04

Willis Limited, Registered number: 181116 England and WalesRegistered address: Ten Trinity Square, London EC3P 3AX

Lloyd’s Broker and Member of the General Insurance Standards Council

Willis Limited

Ten Trinity SquareLondon EC3P 3AXTelephone: +44 (0)20 7488 8111

www.willis.com

Willis Limited, Registered number: 181116 England and Wales

Registered address: Ten Trinity Square, London EC3P 3AX

Lloyd's Broker. Authorised and regulated by the Financial Services Authority.CON/2841/05/05

2841 Willis Construction Risks COVER.qxd 07/06/2005 11:04 Page 4