2.6 cf for asean stakeholders (28 - 29 march...

TRANSCRIPT

2.6 CF for ASEAN stakeholders (28 - 29 March 2016)

i

Introduction

Impactofclimatechangecannowbeseenallovertheworld.EspeciallySoutheastAsiaregionisoneofthe

mostvulnerableareasintheworldandactionsforclimatechangearetheimportantandimmediateagenda

forthisregion.

The United Nations Framework Convention on Climate Change (UNFCCC) and other UN agencies have

established financial mechanisms to provide funds to both climate change mitigation and adaptation

measuresindevelopingcountries.TheGlobalEnvironmentFacility(GEF)isoperatingfinancialmechanism

under the UNFCCC. At COP17 in 2011, Parties decided to designate the Green Climate Fund (GCF) as an

operatingentityoftheFinancialMechanismoftheUNFCCC.Furthermore,Internationaldecisionconcluded

long‐termclimatefinanceandtheGCF’sinitialcapitalizationtargetof10billionUSDhasbeenmetin2014.

However, many countries are still facing barriers and difficulties to access such international financial

sources,andalsofacingbudgetconstraintstoimplementclimatechangerelatedactions.

Thailand Greenhouse Gas Management Organization (Public Organization) (TGO), a responsible

agencyofclimatechangemitigationundertheMinistryofNaturalResourcesandEnvironment(MONRE)of

Thailand,hasbeenconductingvariousactivitiestopromotelowcarbonandresilientsociety,oneofwhichis

theestablishmentofClimateChange InternationalTechnicalandTrainingCenter(CITC) inThailand,

whichaimstobea“one‐stoptechnicalandtrainingcenter”andnetworkingplatformonclimatechangefor

various stakeholders in Southeast Asian countries. CITC project is receiving support from Japan

InternationalCooperationAgency(JICA).

CITChassetupavarietyoftrainingcoursesthataimtoenhancethecapacityofawiderangeofstakeholders

andnetworkingamongthem,includingpolicymakersandpractitionersfromcentralandlocalgovernment

inSoutheastAsia,aswellasprivatecompanies.Beingawareofthesignificanceofaccessingclimatefinance

andalsotheneedsforcapacitydevelopmentonthisissueforstakeholdersintheregion,CITChasdeveloped

atrainingprogramforASEANstakeholdersrelatedtoclimatefinance.

This training material was developed for a “Regional Training on Climate Finance in Southeast Asian

countries”trainingcourseofCITC,whichaimstoprovideageneralunderstandingofthecurrentnatureand

varietyofclimatefinancingopportunitiesandthetypesofclimatemitigationandadaptationprojectsthat

theycansupport.

ii

AcknowledgementsandListofContributors

ExecutiveAdvisors

Mr.SunthadSomchevita Chairman

ClimateChangeInternationalTechnicalandTrainingCenter(CITC)

Mrs.PrasertsukChamornmarn ExecutiveDirector

ThailandGreenhouseGasManagementOrganization(TGO)

Dr.NatarikaWayuparbNitiphon DeputyExecutiveDirector

ThailandGreenhouseGasManagementOrganization(TGO)

DirectingEditor

Dr.JakkanitKananurak Director

ClimateChangeInternationalTechnicalandTrainingCenter(CITC)

Editors

Ms.ApaphatchHunsiritrakun ThailandGreenhouseGasManagementOrganization(TGO)

Ms.TomokoIshikawa InstituteforGlobalEnvironmentalStrategies(IGES)

Mr.TetsuyaYoshida OrientalConsultantGlobalCo.,Ltd.

Authors

Dr.TomonoriSudo CollegeofAsiaPacificStudies,RitsumeikanAsiaPacificUniversity

Dr.ShuzoNishioka(Chapter1) InstituteforGlobalEnvironmentalStrategies(IGES)

Dr.RobertJ.Didham InstituteforGlobalEnvironmentalStrategies(IGES)

Mr.JuichiroSahara(Annex) GreenClimateFund(GCF)

CoverDesign

Mr.ThitipongPiboongulsamlit ThailandGreenhouseGasManagementOrganization(TGO)

iii

TableofContents

Chapter1 Introductiontoclimatechange

1.1 Climatechangescienceandclimatechangeimpacts·························································· 1

1.2 Overviewofclimatechangemitigationandadaptation······················································ 6

Chapter2 ClimateFinanceMechanisms

2.1 IntroducingMitigationInvestmentsandtheEnergyEconomy··········································· 8

2.2 Climate Finance mechanisms and Institutional Landscape (international, multi‐lateral,

bi‐lateral,private)············································································································ 15

2.3 TypologiesofClimateFinance·························································································· 17

2.4 ClimateFinancetrendsinAsia·························································································· 25

Chapter3 AccessingClimateFinancingandManagingProjects

3.1 AccessingClimateFinancing ··························································································· 32

3.2 ManagingClimateFinanceProjects ················································································· 36

Chapter4 DevelopingSupportiveInfrastructuresforClimateFinance

DevelopingSupportiveInfrastructuresforClimateFinance ······················································· 38

Annex CaseStudy:GreenClimateFund(GCF)

I BackgroundofGreenClimateFund(GCF)········································································· 41

II GCFandResourceMobilizationandFinanceCriteria························································· 42

III AccessingClimateFinancing····························································································· 45

iv

Abbreviations

Abbreviation Description ADA Agency for Agricultural Development of Morocco ADB Asian Development Bank ADBI Asian Development Bank Institute AF Adaptation Fund AFC Africa Finance Corporation AFD Agence Française de Développement AfDB African Development Bank AFOLU Agriculture, Forestry and Other Land Use AR Afforestation and Reforestation AR5 Fifth Assessment Report ASEAN Association of Southeast Asian Nations BAU Business As Usual BUR Biennial Update Reports CAF Corporación Andina de Fomento CCCCC Caribbean Community Climate Change Centre CDM Clean Development Mechanism CERs Certified Emission Reductions CFC Chlorofluorocarbon CH4 Methane CI Conservation International CITC Climate Change International Technical and Training Center CO2 Carbon Dioxide COP Conference of the Parties CPI Climate Policy Initiative CPI Climate Policy Initiative CSE Centre de Suivi Écologique DBSA Development Bank of Southern Africa EBRD European Bank for Reconstruction and Development EIB European Investment Bank EIF Environmental Investment Fund ESG Environment, Social and Governance ESS Environmental and Social Safeguards FAO Food and Agriculture Organization FDI Foreign Direct Investment GCF Green Climate Fund GDP Gross Domestic Product GEF Global Environment Facility GHG Greenhouse Gas GWP Global Warming Potential IBRD International Bank for Reconstruction and Development IDA International Development Association IDB Inter-American Development Bank IDFC International Development Finance Club IEA International Energy Agency IFC International Finance Corporation IGES Institute for Global Environmental Strategies IPCC Intergovernmental Panel on Climate Change IRENA International Renewable Energy Agency IRR Internal Rate of Returns

v

IUCN International Union for Conservation of Nature JCM Joint Crediting Mechanism JICA Japan International Cooperation Agency KfW Kreditanstalt für Wiederaufbau LCOE Levelized Cost of Electricity LDCs Least Developed Countries MAC Marginal Abatement Cost MINIRENA Ministry of Natural Resources of Rwanda

MOFEC Ministry of Finance and Economic Cooperation of the Federal Republic of Ethiopia

MONRE Ministry of Natural Resources and Environment MRV Measurement, Reporting and Verification N2O Nitrous Oxide NABARD National Bank for Agriculture and Rural Development NDA National Designated Authority NEMA National Environment Management Authority of Kenya NIE National Implementing Entity NTFP Non-Timber Forest Product OAS Online Accreditation System ODA Official Development Assistance OECD Organisation for Economic Co-operation and Development OOF Other Official Flows PPP Public private partnership PROFONANPE Fondo de Promoción de las Áreas Naturales Protegidas del Péru RBF Results-based Finance RE Renewable Energy REDD Reducing Emissions from Deforestation and Forest Degradation ROI Return on Investment SD Sustainable Development SIDs Small Island Developing States SPREP Secretariat of the Pacific Regional Environment Programme TC Transitional Committee TGO Thailand Greenhouse Gas Management Organization UCAR Unidad Para el Cambio Rural from Argentina (Unit for Rural Change) UN United Nations UNCTAD United Nations Conference on Trade and Development UNDP United Nations Development Programme UNEP United Nations Environment Programme UNFCCC United Nations Framework Convention on Climate Change USD United States Dollars WEF World Economic Forum WFP World Food Programme

WMO World Meteorological Organization

1

Climate Change International Technical and Training Center (CITC)

CHAPTER1 INTRODUCTIONOFCLIMATECHANGE

Whatreaderscanlearninthischapter

Chapter1 illustratesthescientificbackgroundofclimatechange; itscausesandeffects.Alsobyreflectingthe

futureprojectionand impactsofclimatechange, thechapter summarizes the importanceofclimateactions

bothinmitigationandadaptation.

1.1 Climatechangescienceandclimatechangeimpacts

1.1.1 Anthropogenicandnaturalclimatechange

Climate routinely and naturally changes in the long‐term and short‐term. Causes of the routine climate

changes vary from variations in earth’s axial revolution and rotation, changes in solar activity, and an

increaseoffineparticlesintheatmospherebyvolcanicactivity.

Sincetheindustrialrevolutioninthelate18thcentury,emissionsofGreenhouseGas(GHG),typicallyinthe

formofcarbondioxide(CO2),havedramatically increaseddue tohumanactivitiessuchasdeforestation

and fossil fuel combustion. Such gases have been accumulated in the atmosphere, and escalating the

greenhouseeffect.Asa result, air temperaturehasraisedandanthropogenic(human‐induced)climate

change has emerged. In a scientific term, both ‘anthropogenic’ changes and ‘natural’ changes are called

‘climate change.’ On the other hand, international communities such as the United Nations Framework

ConventiononClimateChange(UNFCCC)andcountrieslimitthecauseofclimatechangeto‘anthropogenic’

changes.UNFCCCdefinesinits

Article 1 climate change as “a

change of climate which is

attributeddirectlyorindirectly

to human activity that alters

the composition of the global

atmosphere and which is in

addition to natural climate

variability observed over

comparabletimeperiods.”

Figure1‐1Anthropogenicglobalwarming(Source:IGES)

2

Climate Change International Technical and Training Center (CITC)

1.1.2 Greenhouseeffect:howglobaltemperatureisdetermined

Energy from the sunwhose surface temperature is approximately 6,000 °C enters into the earth, which

heatsuptheearthsurfacetemperatureto15°Conoverallaverage.Theenergybalanceismaintainedbythe

earthemittingthesameamountofenergyobtainedfromthesun intothespace.Climateontheground is

formulated by the atmosphere in the troposphere up to a height of about 10,000 meters. Atmospheric

constituentiscomposedof78%nitrogen,21%oxygenandlessthan1%argon,andcontainsatinyamount

ofGHGsuchas carbondioxide (concentrationof260ppm inpre‐industrial era and400ppm=0.04%at

present),methaneandnitrousoxide.Shortwavelengthenergyemittedfromthehightemperaturesurfaceof

thesunpassesthroughatmosphericlayerswithoutinterferinginthegreenhousegases.Ontheotherhand,

energyemittedfromtheearthsurfacewithlowertemperature(about15°C)haslongwavelength.GHGsare

activatedinsynchronizationwiththeenergyandraisetheatmospherictemperature.

This is called ‘greenhouseeffect.’ If there is noGHG in the atmosphere, the temperature of the earth is

estimatedtobeminus18°C.Thus,the33°Cdifferencefromthe15°Cisthetemperatureraisegeneratedby

thegreenhouseeffect.

Afterall,asurfaceoftheearthcankeepwarmtemperaturewhichissuitabletotheexistingorganismsby

holding GHGs in the atmosphere. However, as the concentration of GHGs increases, the atmospheric

temperature becomes higher due to enhancement of greenhouse effect. The greenhouse effect is

theoretically supportedbySwedishscientistSvanteAugustArrheniusandothers in the late19th century,

andisascientificallyestablishedphenomenon.Controversyissometimescreatedbyskepticswhoquestion

aboutthecausesofglobalwarmingotherthangreenhouseeffect(e.g.solaractivityandearthrevolutionand

rotationchanges)andtheuncertaintiesinclimatemechanisms(e.g.suchastheformationofcloudandthe

degree of greenhouse effect).

Figure1‐2Observedchangein

surfacetemperature1901–2012

(Source:IPCCFifthAssessmentReport)

3

Climate Change International Technical and Training Center (CITC)

1.1.3 Anthropogenic‘globalwarming’

Since the industrial revolution, GHG emissions have dramatically increased mainly due to the increased

carbon dioxide emissions generated from fossil fuel combustion (account for about 60%ofworldGHG

emissions today) and from deforestation (17%) due to farmland development in response to the

population growth, methane emissions from rice paddies (14%), and nitrous oxide from agricultural

activities (8%). Thus, the ‘anthropogenic’ greenhouse effect was added to the conventional ‘natural’

greenhouseeffect,andearth'satmospheretemperaturefurtherincreasesandleadtoglobalwarming.

Consequently,climatechangethatalterstheentireclimatesystemhascometobeaconcern.Climatesystem

isdefinedbytheUNFCCCinitsArticle1paragraph3as“thetotalityoftheatmosphere,thehydrosphereand

geosphereandtheirinteraction.”

As global warming continues, present stable climate will change in terms of temperature, rainfall, wind,

ocean temperature and extreme events such as typhoon. Global average temperature rises, but the

temperature temporarily increases in someplacesanddecreases inotherplaces. In this sense, theuseof

term‘climatechange’ismorescientificallyappropriatethan‘globalwarming.’

1.1.4 Presentsituationandprojectionofclimatechange

Climateontheearthsurfacewherehumanslivehasshiftedfromiceagetowarmerinterglacialageabout

15,000yearsago.Then,althoughtheclimatechangedbyrepeatingnaturalvariabilitywithinapproximately

1 °C range, under the relatively stable climate, agriculturewas started and humans have obtained stable

foods and maintained their productions

andliving.

But in the20th century, the temperature

began to rise. Although the rise in

temperature once became stationary

coinciding with natural variability of

temperature decrease during 1940’s –

70’s, the increase in temperature has

been accelerated again since. The

increase since pre‐industrial periods is

estimated tobe0.85°Cnow. Ithasbeen

accelerated in recent years, and the

increasesince1880hasbeenobservedto

be 0.85 °C. On the other hand, GHGFigure1‐3Variationsofearth’ssurfacetemperature:

Year1000toYear2100(Source:IPCCsynthesisreport2001)

4

Climate Change International Technical and Training Center (CITC)

concentrationsintheatmospherehaveincreasedtoanunprecedentedlevelinthepast800,000years.They

exceeded the preindustrial level by about 40% in carbon dioxide and 150 % in methane. Report by

Intergovernmental Panel on Climate Change1 (IPCC) concluded that “it is extremely likely that human

influencehasbeenthedominantcauseoftheobservedwarmingsincethemid‐20thcentury.”

IfhumanscontinuesuchactivitiesthatdependheavilyupontheuseoffossilfuelsinaBusiness‐as‐Usual

(BAU)condition,accordingtotheFifthAssessmentReportbyIPCC,about4°Ctemperatureriseisexpected

bytheendofthe21stcentury.Thistemperatureriseisexpectedtocausegreatdamagesworldwide.In2010,

at the 16th Conference of the Parties (COP) to UNFCCC held in Cancun,Mexico, international community

agreedtoestablishanewinternational frameworktoholdany temperature increase tobelow2°Cabove

preindustriallevels.

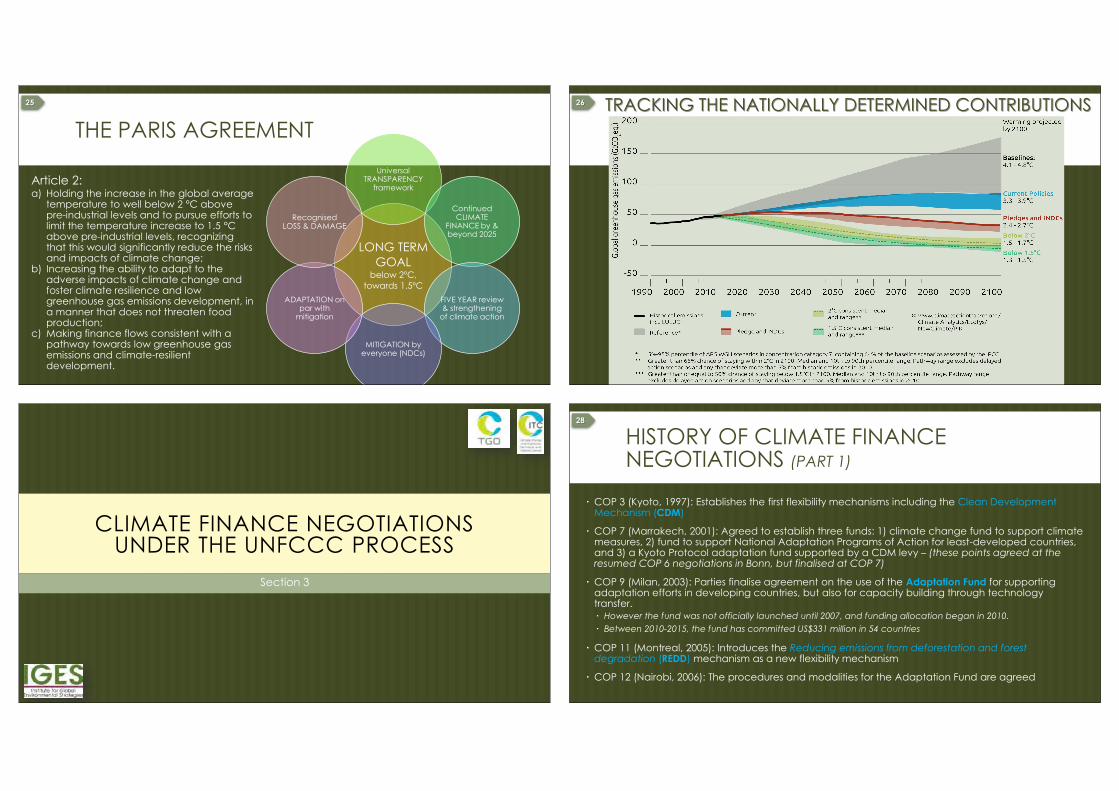

Inaddition,recently,theParisAgreementmarksachangeindirectiontowardsanewworld.Itconfirmsthe

targetofkeepingtheriseintemperaturebelow2°C.Theagreementevenestablishes,forthefirsttime,that

weshouldbeaiming for1.5 °C, toprotect islandstates,whichare themost threatenedby the rise in sea

levels.

1.1.5 GHGandGlobalWarmingPotential

Major anthropogenic greenhouse gases are carbondioxide (CO2) resulting from fossil fuel combustions

anddeforestation,methane(CH4)resultingfrompaddy,ruminationoflivestockandwaste,nitrousoxide

(N2O) fromnitrogen‐based fertilizer andadipic acidproduction, sulfurhexafluoride (SF6) andalternative

forchlorofluorocarbon(CFC).

Eachperweightgashasdifferenteffects (radiative forcing) toglobalwarming.Themeasurementofhow

muchheateachgreenhousegastrapsintheatmosphereperunit,incomparisontocarbondioxide,iscalled

GlobalWarmingPotential(GWP).Whenthesame1kgisemittedtotheatmosphere,CH4is28times,N2O

is265timesandCFCsisthousandstimesmorethanCO2accordingtoIPCCFifthAssessmentReport(AR5).

IPCC AR5 states CO2 is the major anthropogenic GHG accounting for 76% of total anthropogenic GHG

emissionsin2010,16%comefromCH4,6%fromN2O,and2%fromfluorinatedgases.

1 Intergovernmental Panel on Climate Change (IPCC) was established by an initiative of the United Nations Environment Programme (UNEP) and the World Meteorological Organization (WMO) in 1988. It is an international panel for scientists, policymakers and international organizations. Generally, the evaluation or assessment reports are issued in every 5 to 7 years. Latest report was issued from 2013 to 2014 as its fifth report (Fifth Assessment Report (AR5). Functions of IPCC include regular survey of the latest scientific knowledge indicated by a number of academic papers, scientific assessment of such knowledge, and utilization of such knowledge for policymaking process.

5

Climate Change International Technical and Training Center (CITC)

1.1.6 ClimateChangeImpacts

Climatechangealterstheecosystems,waterresources

andweather inmanyparts of theworld.A change in

the occurrence of extreme natural events such as

typhoon,droughtorheavyrainfall isexpectedto lead

to water shortage, damages to agriculture and food,

andincreasesinnaturaldisasters.

Flooding in coastal mega‐city and salinization of

coastalfarmlandoccursalongwithsealevelrisedueto

melting land ice and expansion of sea water. Heat

stroke and expansion of vector‐born infectious

diseasesarealsoexpected.

Someof thedamagesarealmost irreversible suchasecosystemchangeandextinctionof speciesandsea

levelrisethatcertainlyproceedsforalongtime.Whilethereisalsoapossibilitythattemperaturerisemay

expandsuitableagriculturallandinthenorthernregion,thereisapossibilitytohavegeographicallyuneven

occurrenceofdamagesespeciallyindevelopingcountrieswhereadaptationcapacitytotheclimatechangeis

ratherlimited.

TheimpactofGHGemissionsandtheiraccumulationhavegivenrisetotemperatureincreases,resultingin

thedestabilizationoftheclimaticsystem.Responsestothissituationhavebeenundertakenbycommunities,

ecosystems, enterprises and institutions. These responses have been broadly defined as ‘adaptation’ to

climatechangeinducedevents.Overthelasttwodecades,adaptationmeasuresarebecomingmorevisible

across the world and an adaptation science is emerging. Adaptation has become central to climate

negotiations.

Whatisbecomingmoreevidentisthatthereisa‘limittoadaptation.’Morerecentlytheconceptoflossand

damage is drawing attention. This is more true for small island developing states (SIDs) and Least

Developed Countries (LDCs) which have been demanding that the climate convention addresses the

questionof ‘lossanddamage’dueto impactsofclimatechange.Asclimate finance‐relateddiscoursesand

approachesmoveforward,thereisaneedtoundertakeresearch,developmethodologiesanddeterminereal

financial,tangibleandnon‐tangiblelossanddamagetoclimate‐inducedimpactsbysocieties,ecosystemand

economies.

Photo1‐1Climatechangeimpacts

6

Climate Change International Technical and Training Center (CITC)

1.2 Overviewofclimatechangemitigationandadaptation

1.2.1 Climatechangemitigation

Objective of the UNFCCC is defined in its Article 2 as “to achieve… stabilization of greenhouse gas

concentrationsintheatmosphereatalevelthatwouldpreventdangerousanthropogenicinterferencewiththe

climate system.Sucha level shouldbeachievedwithina time‐frame sufficient toallowecosystems toadapt

naturally to climate change, to ensure that food production is not threatened and to enable economic

developmenttoproceedinasustainablemanner.”

AlthoughsomeofGHGsemittedintotheatmosphereisabsorbedbytheforestandsoil,morethanhalfofthe

GHGs remain and are accumulated in the atmosphere. Therefore, as long as the emissions continue, the

concentrations of atmosphericGHGs continue to grow.The temperature continues to rise accordingly. In

order to stabilize the climate, it is necessary to reduce GHG emissions and eventually reach to zero

emission,inotherwords,mitigateclimatechange.

GHGhasbeenemittedfromallsectorsofhumanactivities.AccordingtoIPCCFifthAssessmentReport,the

shares of sectoral emissions are: energy supply (35%), agriculture, forestry andother landuse (24%) in

AFOLU,industry(21%),transport(14%)andbuildings(6.4%).

Intechnologicalsocietythatisdeeplydependentonenergy,GHGsarecloselyrelatedtopeople’slivingand

production activities, thus we are facing great difficulties to reduce GHG emissions. In order to prevent

furtherhugeclimatedamagesinthefuture,thereisnootheroptionsbuttoreduceGHGemissionsbycutting

offfossilfuels.

1.2.2 Adaptationtoclimatechangeimpacts

Climate change has been already progressed and anthropogenically‐derived changes have influenced the

ecosystem and human life in many parts of the world. In facing these issues, human beings have made

efforts toadapt to theclimatechange, throughsuchmeasuresasdeveloping infrastructure, changing the

cropvarieties,installingairconditioners,etc.

In Japan, forexample,qualityofricehasworsenedinthesouthandimproved inthenorthduetoclimate

change.Inordertoadapttothischange,farmersinthesouthhavedevelopedstrongricewhichisresilient

toclimatechange,inthiscase,resilienttohighertemperatureinordertosecureagriculturalproduction.

Onecannotexpectadaptationmeasurescanfullycoverthedamagefromclimatechange,andtheycannotbe

effective if the climate change is escalated. Therefore, mitigation of climate change still is the best

adaptationmeasure.

7

Climate Change International Technical and Training Center (CITC)

Bibliography

IPCC,2007:ClimateChange2007:Impacts,AdaptationandVulnerability.ContributionofWorkingGroupII

totheFourthAssessmentReportoftheIntergovernmentalPanelonClimateChange,M.L.Parry,

O.F.Canziani,J.P.Palutikof,P.J.vanderLindenandC.E.Hanson,Eds.,CambridgeUniversityPress,

Cambridge,UK,976pp.

IPCC,2007:ClimateChange2007:Mitigation.ContributionofWorkingGroupIIItotheFourthAssessment

ReportoftheIntergovernmentalPanelonClimateChange[B.Metz,O.R.Davidson,P.R.Bosch,R.

Dave,L.A.Meyer(eds)],CambridgeUniversityPress,Cambridge,UnitedKingdomandNewYork,

NY,USA.

IPCC,2013:ClimateChange2013:ThePhysicalScienceBasis.ContributionofWorkingGroupItotheFifth

AssessmentReportoftheIntergovernmentalPanelonClimateChange[Stocker,T.F.,D.Qin,G.‐K.

Plattner, M. Tignor, S.K. Allen, J. Boschung, A. Nauels, Y. Xia, V. Bex and P.M. Midgley (eds.)].

CambridgeUniversityPress,Cambridge,UnitedKingdomandNewYork,NY,USA,1535pp.

IPCC, 2014: Climate Change 2014: Impacts, Adaptation, and Vulnerability. Part A: Global and Sectoral

Aspects. Contribution of Working Group II to the Fifth Assessment Report of the

IntergovernmentalPanelonClimateChange[Field,C.B.,V.R.Barros,D.J.Dokken,K.J.Mach,M.D.

Mastrandrea,T.E.Bilir,M.Chatterjee,K.L.Ebi,Y.O.Estrada,R.C.Genova,B.Girma,E.S.Kissel,A.N.

Levy, S. MacCracken, P.R. Mastrandrea, and L.L.White (eds.)]. Cambridge University Press,

Cambridge,UnitedKingdomandNewYork,NY,USA,1132pp.

IPCC,2014:ClimateChange2014:MitigationofClimateChange.ContributionofWorkingGroup III to the

FifthAssessmentReport of the Intergovernmental Panel on Climate Change [Edenhofer, O., R.

Pichs‐Madruga, Y. Sokona, E. Farahani, S. Kadner, K. Seyboth, A. Adler, I. Baum, S. Brunner, P.

Eickemeier, B. Kriemann, J. Savolainen, S. Schlömer, C. von Stechow, T. Zwickel and J.C. Minx

(eds.)].CambridgeUniversityPress,Cambridge,UnitedKingdomandNewYork,NY,USA.

LeTreut,H.,R.Somerville,U.Cubasch,Y.Ding,C.Mauritzen,A.Mokssit,T.PetersonandM.Prather,2007:

Historical Overview of Climate Change. In: Climate Change 2007: The Physical Science Basis.

Contribution of Working Group I to the Fourth Assessment Report of the Intergovernmental

PanelonClimateChange[Solomon,S.,D.Qin,M.Manning,Z.Chen,M.Marquis,K.B.Averyt,M.

TignorandH.L.Miller(eds.)].CambridgeUniversityPress,Cambridge,UnitedKingdomandNew

York,NY,USA.

8

Climate Change International Technical and Training Center (CITC)

CHAPTER2 CLIMATEFINANCEMECHANISMS

Whatreaderscanlearninthischapter

Thischapteroutlinesmitigationinvestmentsandtheenergyeconomy,climatefinancemechanismsand

institutionallandscape(international,multi‐lateral,bi‐lateral,andprivate),aswellasthetypologiesofClimate

Finance.

2.1 IntroducingMitigationInvestmentsandtheEnergyEconomy

WhatisFinanceandInvestment?

Financeisdefinedasatransactionofmoneyfrommoneyholderwhohasnoneedtousemoneynowtouser

ofmoneywhoneedstospendmoneynow.Akeypointinfinanceisthetimevalueofmoney,whichstates

thatpurchasingpowerofoneunitofcurrencycanvaryovertime.Financeaimstopriceassetsbasedon

theirrisklevelandtheirexpectedrateofreturn.

Aninvestmentisoneoffinancialtransactions.Ingeneral,aninvestmentisanassetoritemthatis

purchasedwiththehopethatitwillgenerateincomeorappreciateinthefuture.Inaneconomicsense,an

investmentisthepurchaseofgoodsthatarenotconsumedtodaybutareusedinthefuturetocreatewealth.

Infinance,aninvestmentisamonetaryassetpurchasedwiththeideathattheassetwillprovideincomein

thefutureorappreciateandbesoldatahigherprice.Akeypointininvestmentistheownership.Asa

resultofinvestmenttransaction,theassetoritemisobtainedbyinvestor.Thus,investorshavearightto

manageassetoritembytheirownwill.

WhatisClimateFinance?

Climatefinancereferstolocal,nationalortransnationalfinancing,whichmaybedrawnfrompublic,private

andalternativesourcesoffinancing.Climatefinanceiscriticaltoaddressingclimatechangebecause

large‐scaleinvestmentsarerequiredtosignificantlyreduceemissions,notablyinsectorsthatemitlarge

quantitiesofgreenhousegases.Climatefinanceisequallyimportantforadaptation,forwhichsignificant

financialresourceswillbesimilarlyrequiredtoallowcountriestoadapttotheadverseeffectsandreduce

theimpactsofclimatechange.

InaccordancewiththeUNFCCC,developedcountryParties(AnnexIIParties)aretoprovidefinancial

resourcestoassistdevelopingcountryPartiesinimplementingtheobjectivesoftheUNFCCC.Itisimportant

forallgovernmentsandstakeholderstounderstandandassessthefinancialneedsdevelopingcountries

havesothatsuchcountriescanundertakeactivitiestoaddressclimatechange.Governmentsandallother

stakeholdersalsoneedtounderstandthesourcesofthisfinancing,inotherwords,howthesefinancial

9

Climate Change International Technical and Training Center (CITC)

resourceswillbemobilized.

Equallysignificantisthewayinwhichtheseresourcesaretransferredtoandaccessedbydeveloping

countries.Developingcountriesneedtoknowthatfinancialresourcesarepredictable,sustainable,andthat

thechannelsusedallowthemtoutilizetheresourcesdirectlywithoutdifficulty.

Fordevelopedcountries,itisimportantthatdevelopingcountriesareabletodemonstratetheirabilityto

effectivelyreceiveandutilizetheresources.Inaddition,thereneedstobefulltransparencyinthewaythe

resourcesareusedformitigationandadaptationactivities.Theeffectivemeasurement,reportingand

verificationofclimatefinanceiskeytobuildingtrustbetweenPartiestotheConvention,andalsofor

externalactors.

MitigationInvestments

TheCO2emissionsofAsiaandthePacificaccountedforabout42.8%ofworldCO2emissionsin2010.

However,through2035,CO2emissionsinAsiaandthePacificwillincreaserapidlyatanannualrateof

2.0%,comparedwiththeworldaveragegrowthrateof1.3%peryearthrough2035.Thus,theshareofAsia

andthePacificisprojectedtoreachmorethanhalfofworldCO2emissionsin2035.

ADB(2013)analyzedthefactorsaffectingCO2reductionfromtheBAUcasetothealternativecase.Itshows

thatenergyintensitywillaccountfor52.6%andCO2intensityfor47.4%ofthetotalreductioninCO2

emissionsfromBAUcasetothealternativecase.ThisimpliesthatAsianandthePacificregionneedsfurther

energyconservationandfuelshifttoless‐carbon‐intensiveenergyforfurtherreductionofCO2emissions

(Fig.2‐1).

10

Climate Change International Technical and Training Center (CITC)

Figure2‐1.Decompositioncomponentsofcarbondioxideemissionreductionfrombusiness‐as‐usual

(2035)tothealternativecase(2035)inAsiaandthePacific.

SourceADB(2013)

Alternativecasecannotberealizedifeffectiveactionstoimproveenergyefficiencyandfuelshiftarenot

taken.

Thereareseveraleffortstoestimateinvestmentandfinanceneedsfordevelopment.136Amongothers,the

WorldEconomicForum(2013)summarizedestimatesofnecessaryinfrastructureinvestmentcalculatedby

severalinstitutions,i.e.InternationalEnergyAgency(IEA)(2012),FoodandAgricultureOrganization(FAO)

(2009),OrganisationforEconomicCooperationandDevelopment(OECD)(2006)andOECD(2012),and

UnitedNationsEnvironmentProgramme(2011)(seeTable2‐1).

11

Climate Change International Technical and Training Center (CITC)

Table2‐1.Annualestimatedinvestmentsneededunderabusiness‐as‐usualandlow‐carbonscenario

(US$billionsperyearbetween2010and2030)

Business‐as‐usualscenarioinvestmentneeds

2Cscenarioinvestmentneeds

Incrementalinvestmentrequired

Sector

Cumulative

2010‐2030

AnnualAverage

Cumulative

2010‐2030

AnnualAverage

Cumulative

2010‐2030

AnnualAverage

Sources

Powergeneration 6,933 347 10,136 507 3,203 160 IEA

Powertransmissionanddevelopment 5,450 272 5,021 251 ‐429 ‐21 IEA

EnergyTotal 12,383 619 15,157 758 2,774 139

Buildings 7,162 358 13,076 654 5,914 296 IEA

Industry 5,100 255 580 290 700 35 IEA

Building&Industrytotal 12,262 613 18,876 944 6,614 331

Road 8,000 400 8,000? 400? ‐ ‐ OECD

Rail 5,000 250 5,000? 250? ‐ ‐ OECD

Airports 2,300 115 2,300? 115? ‐ ‐ OECD

Ports 800 40 800? 40? ‐ ‐ OECD

TransportVehicles 16,908 845 20,640 1,032 3,732 187 IEA

Transporttotal 33,008 1,650 36,740 1,837 3,732 187

Water 26,400 1,320 26,400? 1,320? ‐ ‐ OECD

Agriculture 2,500 125 2,500? 125? ‐ ‐ FAO

Tele‐communications 12,000 600 12,000? 600? ‐ ‐ OECD

Forestry 1,280 64 2,080 104 800 40 UNEP

Othersectors unknown unknown unknown unknown unknown unknown

TotalInvestment 99,833 4,991 113,753 5,689 13,934 698

~$100tr ~$5tr ^$114tr ~$5.7tr ~$14tr ~$0.7tr

Source:ExtractedfromWorldEconomicForum(2013)

TheWEF(2013)arrivedataninvestmentgapunderabusiness‐as‐usualscenario(thatis,withouttaking

intoaccountclimatechange)of$100trilliontoaccommodateclimatechange.Respondingtoananticipated

2°Ctemperaturerisewilladdonly$14trillion,or14%tothetotalgap.Thebiggestinvestmentchallenges,

therefore,appeartoexistindependentofclimatechange.

IncontextofAsia,ADBandADBI2009reportedthatAsia’soverallinvestmentrequirementfor

infrastructurebetween2010and2020isapproximately$8trillion.Whileabouthalfthetotalinfrastructure

neededisforprovidingelectricity,transportation(mostlyroads)coversabout30%ofthetotal,

telecommunications13%,withtherestneededforwaterandsanitation(Table2‐2).

12

Climate Change International Technical and Training Center (CITC)

Table2‐2Asia’sTotalInfrastructureInvestmentNeedsbySector,2010–2020(in2008$million)

SourceExtractedfromADBandADBI(2009)

However,thesefiguresshowthe“Business‐asUsual”investmentneedsanddonotaccountforthe“Low

Carbon”Scenario.Therefore,weshouldestimatetheamountofincrementalinvestmentrequired.Here,we

simplyassumeitapplyingcoefficientbasedontheestimationbytheWEF(2013).AccordingtotheWEF

(2013),incrementalinvestmentrequiredinEnergysectoris2774billionUSdollar,whichis22.4%of

investmentneedsatBusiness‐as‐usualscenario.Incaseoftransportsector,incrementalcostis11.3%of

Business‐as‐usualinvestmentneeds.IfthosecoefficientsareappliedinthefiguresshowninADBandADBI

2009,incrementalinvestmentneedsinEnergysectorandtransportsectorare915,855millionUSDollar

and246,612millionUSDollars,respectively.Thatis,58billionUSdollarsareincrementallyrequired

annuallyforlowcarbondevelopment.

EnergyEconomy

In2015,severalimportantconferenceswereheldwhereimportantdecisionshavebeenmadetoshowthe

directionoffuturedevelopment,suchastheThirdConferenceonFinanceforDevelopmentinJuly,United

NationsGeneralAssemblyonPost2015DevelopmentAgenda/SustainableDevelopmentGoalsinSeptember,

andthe21stConferenceofthePartiestotheUNFrameworkConventiononClimateChange(COP21)in

December.IntheprocessofpreparationonPost2015DevelopmentAgendaandSustainableDevelopment

Goals,theimportanceof“Sustainableenergyforall”hasbeenhighlightedandenergyissueswereproposed

asoneofnewsustainabledevelopmentgoals,foradoptionattheUNGeneralAssembly.Thegoalandits

targetsonenergyshowasfollows;

13

Climate Change International Technical and Training Center (CITC)

Goal7.Ensureaccesstoaffordable,reliable,sustainableandmodernenergyforall

7:1By2030,ensureuniversalaccesstoaffordable,reliableandmodernenergyservices

7:2By2030,increasesubstantiallytheshareofrenewableenergyintheglobalenergymix

7:3By2030,doubletheglobalrateofimprovementinenergyefficiency

7:aBy2030,enhanceinternationalcooperationtofacilitateaccesstocleanenergyresearchandtechnology,

includingrenewableenergy,energyefficiencyandadvancedandcleanerfossil‐fueltechnology,andpromote

investmentinenergyinfrastructureandcleanenergytechnology

7:bBy2030,expandinfrastructureandupgradetechnologyforsupplyingmodernandsustainableenergy

servicesforallindevelopingcountries,inparticularleastdevelopedcountriesandsmallislanddeveloping

Statesandland‐lockeddevelopingcountries,inaccordancewiththeirrespectiveprogrammesofsupport

(UnitedNations2015a)

ThisgoalandtargetsdeemsappropriateinthecontextofAsiaandthePacificRegion.

Recently,costsofrenewablepowergenerationtechnologiesaredeclining.IRENA(2015)reportedthatthe

large‐scaledeploymentofwindandsolarPVsince2000hasseentheirinstalledcostsdrivendownby

learninginvestmentsatthesametimethattechnologyimprovementshaveimprovedyields,resultingin

levelizedcostofelectricity(LCOE)declines.IRENA(2015)notedthatregional,weightedaveragecostsof

electricityfrombiomassforpower,geothermal,hydropowerandonshorewindareallnowintherange,or

evenspanalowerrange,thanestimatedfossilfuel‐firedelectricitygenerationcosts.Becauseofstriking

LCOEreductions,solarPVcostsalsoincreasinglyfallwithinthatrange.Thus,renewableenergy

technologiesbecomeenoughcompetitivetothetraditionalfossilfuelpowergenerationandthosemaybe

realisticoptionsforAsiancountries(Fig.2‐2).

14

Climate Change International Technical and Training Center (CITC)

Figure2‐2.Weightedaveragecostofelectricitybyregionforutility‐scalerenewabletechnologies,

comparedwithfossilfuelpowergenerationcosts,2013/2014.SourceIRENA(2015)

Eventhoughthecostofrenewableenergytechnologydeclines,mobilizationofinvestmentandfinancein

lowcarbondevelopmentisstilloneofthekeyissuesforAsiandevelopingcountriessincethereareseveral

barrierstolowcarbonproject.

InternationalDevelopmentFinanceClub(IDFC)(2014)identifyfollowingbarriers,suchas;

• Highupstreamcosts forprojectdevelopment.Publicsupportmaybeessential torealize the

initialphasesofprojectidentificationanddevelopmentthatmayseemunattractivetoprivate

investors.

• Highcapitalcostsrequiringadequatefinancialinstruments.

• High perceived risks, requiring specific risk mitigation measures—financial or

institutional—sincestandardriskmitigationtoolsareoftenunsuitableorunavailable forRE

projects.Whenperceivedriskishigherthanrealrisk,publicactionmaybeneededtoconvince

valuechainactorstochangetheirperception.

15

Climate Change International Technical and Training Center (CITC)

• Needtoadaptrulesand institutional frameworks forREprojects.Operational integrationof

RE into power grids or other energy systems often requires changes in institutional

frameworks,notablytoguaranteelongtermaccesstoresources.

• Smallersizeandreturnthatofferlowereconomiesofscale.

• HighfossilfuelsubsidiespreventREdeployment.

2.2 ClimateFinancemechanismsandInstitutionalLandscape (international,multi‐lateral,bi‐lateral,private)

Thereareavarietyoffinancialresourcesandschemesavailableforclimatechangerelatedactions.Figure

2‐3showsoverallsourcesofclimatechangefinance.

Figure2‐3.Financialflowsforclimatechangemitigationandadaptationindevelopingcountries

Source:Sudo(2015)

ClimatePolicyInitiative(CPI)(2015)estimatesclimatechangefinancialflowfromavarietysourcestoa

varietyofpurposes.AsshowninFigure4,CPI(2015)reportedthatUSD391billionhasidentifiedas

acclimatechangerelatedfinance.

16

Climate Change International Technical and Training Center (CITC)

Figure2‐4.GloballandscapeofClimateFinance

Source:CPI(2015)

Table2‐4summarizesthecomparisonofcharacteristics,potentialandrisksofeachfinanceresources.Each

financialsourcehasprosandcons.Amongothers,domesticfinance(bothpublicandprivate)deemsthe

moststableandlowriskfinancialsource.

Table2‐4Characteristics,potentialsandrisksoffinance

Characteristics Potential Risk

Domesticpublicfinance

• Nat’lbudget(Nat’ltax)

• Municipalitybudget

• Bonds• DomesticDFIs

• Moststableandlowriskfinancesource.

• Goodforfinanceinlowprofitpublicprojects

• Contributetoleveragingdomesticprivatefinance

• ImprovedgovernanceandfinancialsystemleadtoincreaseofdomesticfinanceflowsandFDI.

• Politicaldifficultyinincreaseoftaxrevenue

• Lackofcapacityofappropriatepublicfiscalmanagement

• Risktocrowd‐outprivatefinance

17

Climate Change International Technical and Training Center (CITC)

Characteristics Potential Risk

InternationalPublicFinance

• ODA• OOF• Multilaterals

• Stableandlowriskfinancebutlowpredictability

• Limitedvolumeoffinance

• Needtouseefficientlyandeffectively

• Leveragingprivatefinance

• Riskcrowd‐outprivatefinance.

• Needtoappropriateforeignreserveandforexmanagement

Privatefinance • Largestfinancesource.

• ContributetoSDbyinvestingintheprojectwheresocialbenefitwillbeincreasedwhileprivatebenefitwillbemaximized.

• Generateemploymentopportunityandsustainabledevelopmentimpactbyexpansionofbusiness.

• Increaseofprivatefinanceflowintodevelopingcountries

• Increaseoffinanceflowsbetweendevelopingcountries

• Unstableduetoeconomicsituationandsensitivetorisks

• Hardtocapturethetotalflowofprivatefinance

• Hardtomakesurethetransparencyandaccountabilityduetobusinessconfidentiality

Blendedfinance

• PPP• EUBlendingmechanism

• Sharingrisksandcostbypublic,privatefinancewillbemobilizedandcontributetoestablishbetterbusinessenvironmentandmarket.

• Increaseofprivatesectorparticipation

• Riskofmarketdistortion

• Riskofdependencytopublic

Source:Sudo(Forthcoming)

2.3 TypologiesofClimateFinance

2.3.1 MitigationFinanceandCDM

‘Mitigationfinance’referstothefinanceprovidedformitigationactivities.OECDdefinesMitigationFinance,

forthepurposetocollectODAdatacontributingclimatechange(RioMarker),as“Itcontributestothe

objectiveofstabilisationofgreenhousegas(GHG)concentrationsintheatmosphereatalevelthatwould

preventdangerousanthropogenicinterferencewiththeclimatesystembypromotingeffortstoreduceor

limitGHGemissionsortoenhanceGHGsequestration.”,andsetcriteriaforeligibilityas“Theactivity

contributesto:

18

Climate Change International Technical and Training Center (CITC)

a) themitigationofclimatechangebylimitinganthropogenicemissionsofGHGs,includinggases

regulatedbytheMontrealProtocol;or

b) theprotectionand/orenhancementofGHGsinksandreservoirs;or

c) theintegrationofclimatechangeconcernswiththerecipientcountries’development

objectivesthroughinstitutionbuilding,capacitydevelopment,strengtheningtheregulatory

andpolicyframework,orresearch;or

d) developingcountries’effortstomeettheirobligationsundertheConvention.“

CleanDevelopmentMechanism

CleanDevelopmentMechanism(CDM)isoneoftheKyotoMechanismsalongwithInternationalEmission

TradingandJointImplementation.TheobjectiveoftheCDMis

1) tocontributetosustainabledevelopmentofthehostcountry(developingcountry);and

2) toassistdevelopedcountriestoaccomplishtheirGHGreductiontargetundertheKyoto

Protocol.

TheconceptofCDMisshownintheFigure2‐5.UndertheCDM,GHGreductionprojectwillbeimplemented

atthedevelopingcountry(hostcountry)incollaborationwithdevelopedcountry.Developedcountry

providesinvestmentandfinanceandtechnologytoimplementtheproject.TheCDMprojectgeneratesat

leasttwotypesofbenefit;developmentbenefitandGHGreduction.Hostcountrywillbeabletoenjoy

developmentalbenefitfromCDM,andGHGreductionwillbetransferredtodevelopedcountry,intheform

ofCertifiedEmissionReductions(CERs),tocountasaGHGreductioneffortbydevelopedcountry.

19

Climate Change International Technical and Training Center (CITC)

Figure2‐5:ConceptofCDM

Source:Sudo

Intheory,CDMcontributestothecostreductionforGHGreductioninthegloballevel.Figure2‐6showsthe

theoreticalconceptoftheCDM.TherearetwoMarginalAbatementCost(MAC)curve;oneisfordeveloped

countryandanotherisfordevelopingcountry.IfdevelopedcountryneedstoreduceGHGemissionbyher

only,totalcostformeetingGHGemissionreductiontargetistheareaoftriangleAONOA.However,thereare

somecheaperGHGreductionmeasures/optionsinDevelopingcountries(TriangleCONq*).Thus,if

developedcountryimplementsCDMprojectsindevelopingcountry,developingcountrycanachieveher

GHGreductiontargetatlowercost,whiledevelopingcountryreceivestechnologytransferaswellas

developmentalbenefit.

Figure2‐6:TheoreticalconceptoftheCDM

Source:Sudo

20

Climate Change International Technical and Training Center (CITC)

However,thereareseveraldifficultiesandcriticisminCDMinpractice.Oneofcriticaldifficultiesishowto

identifyanddevelopCDMprojects.Inaddition,evenifappropriateprojectsareidentified,ittakeslongtime

tocompletetheproceduresforregisteringtheprojectasCDM.Asaresultofsuchdifficulties,onlyemerging

countriesenjoybenefitsfromCDM.

CooperativeApproaches(Variousapproaches)

DecisionmadeatCOP18inCancunsaidthat“AcknowledgesthatParties,individuallyorjointly,may

developandimplementvariousapproaches,includingopportunitiesforusingmarketsand

non‐markets,toenhancethecost‐effectivenessof,andtopromote,mitigationactions,bearinginmind

differentcircumstancesofdevelopedanddevelopingcountries”.ThisideawasincorporatedintheParis

Agreement.Paragraph1,Article6ofParisAgreementshowsthat“PartiesrecognizethatsomeParties

choosetopursuevoluntarycooperationintheimplementationoftheirnationallydeterminedcontributions

toallowforhigherambitionintheirmitigationandadaptationactionsandtopromotesustainable

developmentandenvironmentalintegrity.”And,inParagraph4ofArticle6,Agreementsays“Amechanism

tocontributetothemitigationofgreenhousegasemissionsandsupportsustainabledevelopmentishereby

establishedundertheauthorityandguidanceoftheConferenceofthePartiesservingasthemeetingofthe

PartiestotheParisAgreementforusebyPartiesonavoluntarybasis.Itshallbesupervisedbyabody

designatedbytheConferenceofthePartiesservingasthemeetingofthePartiestotheParisAgreement,and

shallaim:

(a)Topromotethemitigationofgreenhousegasemissionswhilefosteringsustainabledevelopment;

(b)Toincentivizeandfacilitateparticipationinthemitigationofgreenhousegasemissionsbypublic

andprivateentitiesauthorizedbyaParty;

(c)TocontributetothereductionofemissionlevelsinthehostParty,whichwillbenefitfrom

mitigationactivitiesresultinginemissionreductionsthatcanalsobeusedbyanotherPartytofulfilits

nationallydeterminedcontribution;and

(d)Todeliveranoverallmitigationinglobalemissions.”

JointCreditingMechanism(JCM)

TheJointCreditingMechanism(JCM)isoneof“Cooperativeapproaches”proposedbyJapan.Itisa

CDM‐typemechanismwhereGHGmitigationactivitywillbeconductedwithinabilateralframework.(See

Figure2‐7)JCMfacilitatesdiffusionofleadinglowcarbontechnologies,products,systems,services,and

infrastructureaswellasimplementationofmitigationactions,andcontributestosustainabledevelopment

ofdevelopingcountries.

21

Climate Change International Technical and Training Center (CITC)

ItappropriatelyevaluatescontributionstoGHGemissionreductionsorremovalsfromJapanina

quantitativemanner,byapplyingmeasurement,reportingandverification(MRV)methodologies,anduses

themtoachieveJapan’semissionreductiontarget.

Figure2‐7:ConceptofJointCreditingMechanism(JCM)

Source:GovernmentofJapan

2.3.2 AdaptationFinance

AdaptationFinancereferstothefinanceprovidedforadaptationactivities.Adaptationtotheadverseeffects

ofclimatechangeisvitalinordertorespondtotheimpactsofclimatechangethatarealreadyhappening,

whileatthesametimeprepareforfutureimpacts.

However,fromaviewoffinanciers,adaptationprojectsdeemsriskyintermsofprofitability.Actually,

nobodyknowswhenclimaterelateddisasterwillhappen,whattypeofdisaster,anditsscale,lossand

damage.Suchuncertaintywillinfluenceforfinancierstomakeinvestmentdecision.Inaddition,once

disasterhappens,additionalcost,suchasemergencycost,recoverycostandreconstructioncost,willbe

needed.Further,duetodisaster(orchangeofclimaticcondition)mayaffecttothegrowthpathofthe

countryorcompany.Therefore,adaptationfinanceisconsideredasasortofinsuranceforormeasuresto

mitigatefutureclimatechangelossanddamageand/oradditionalcost.

22

Climate Change International Technical and Training Center (CITC)

Figure2‐8:AdaptationFinance

Source:Sudo

OECD(2011)definedadaptationfinanceas“Itintendstoreducethevulnerabilityofhumanornatural

systemstotheimpactsofclimatechangeandclimate‐relatedrisks,bymaintainingorincreasingadaptive

capacityandresilience.Thisencompassesarangeofactivitiesfrominformationandknowledgegeneration,

tocapacitydevelopment,planningandtheimplementationofclimatechangeadaptationactions.”AndOECD

(2011)setcriteriaforeligibilityas;

a)theclimatechangeadaptationobjectiveisexplicitlyindicatedintheactivitydocumentation;and

b)theactivitycontainsspecificmeasurestargetingthedefinitionabove.

Carryingoutaclimatechangeadaptationanalysis,eitherseparatelyorasanintegralpartofagencies’

standardprocedures,facilitatesthisapproach.

MostoftheAdaptationactivitieswillbecarriedoutasapartofgeneraldevelopmentactivities.Therefore,it

seemsdifficultfordonorstorecognizetheprojectasanadaptationactivity.Therefore,OECDrequested

donorstoexplicitlyindicateit.

AdaptationFund

TheAdaptationFund(AF)wasestablishedin2001tofinanceconcreteadaptationprojectsandprogrammes

indevelopingcountryPartiestotheKyotoProtocolthatareparticularlyvulnerabletotheadverseeffectsof

climatechange.TheAdaptationFundisfinancedwithashareofproceedsfromthecleandevelopment

mechanism(CDM)projectactivitiesandothersourcesoffunding.Theshareofproceedsamountsto2per

23

Climate Change International Technical and Training Center (CITC)

centofcertifiedemissionreductions(CERs)issuedforaCDMprojectactivity.Thesefundscaneitherbe

accessedthroughanaccreditedMultilateralInstitution,orthroughanaccreditedNationalImplementing

Entity(NIE).

2.3.3 REDD+Finance

REDD+FinancereferstothefinanceprovidedfortheactivitiesonREDD+.REDD+isanabbreviationof

‘Reducingemissionsfromdeforestationandforestdegradationandtheroleofconservation,sustainable

managementofforestsandenhancementofforestcarbonstocksindevelopingcountries’.Therefore,REDD+

financeis,ingeneral,financeinreforestation,aforestationandforestconservationactivities.UndertheCDM

scheme,afforestationandreforestationactivitiesareconsideredasmitigationactivities,andgenerate

carboncredit(AR‐CDM).InadditiontoAR‐CDM,forestconservationandsustainableforestmanagement

activitiesarealsoconsideredasmitigationactivity.Therefore,UNFCCCdiscussapossibilitytogenerate

carboncreditforsuchconservationandsustainableforestmanagementactivity.

Figure2‐9:ConceptofREDD+

Source:Sudo

24

Climate Change International Technical and Training Center (CITC)

Figure2‐10:GHGemissionandREDD+

Source:Sudo

Inviewoffinanciers,forestwillproducetimbersasmonetaryvaluableproducts,butotherproductssuchas

NonTimberForestProducts(NTFP)andindirecteffectofforestsuchascarbonsequestration,biodiversity

anddisasterprotectioneffectarenotconsideredasvaluableproducts.Therefore,oneoftheissueson

REDD+financeishowtoincorporatesuchindirectvaluesinfinancialappraisaland/orturnsuchindirect

valuesintomonetaryvalue.

2.3.4 Results‐BasedFinance(RBF)

Results‐basedFinance(RBF)referstothefinancewhichdisbursementwillbemadebasedonthe

achievementtotheexpectedresult.SinceRBFwillbeprovidedbasedonthe“Results”,someindicatorsfor

monitoringandevaluationwillbesetbeforeconcludingfinancialagreement.Onceindicatorsachievethe

targets(ortrigger),thendisbursementwillbemade.Inthissense,thisschemedeemssimilartothe

conditionalfinanceandStructuredAdjustmentLoanin1980s.(SeeFigure2‐11)

25

Climate Change International Technical and Training Center (CITC)

Figure2‐11:SchemeonRBF

Source:Spors,F.(2014)

2.3.5 ProjectTypeseligibleforuseofClimateFinance

Ingeneral,anytypesofprojectswhicharerecognizedasclimaterelatedactivitieswillbeeligiblefortheuse

ofclimatefinance,eventhoughitdependsonthefinancialinstitutions’policy.

2.4 ClimateFinancetrendsinAsia

TheAsia‐PacificRegionwillrequirebillionsofdollarstotransitiontolow‐carbongrowthpathsandtoadapt

totheunavoidableimpactsofclimatechange.Nevertheless,Asiandevelopingcountriesareinagood

positionasfinanceforclimatechangeactionisalreadyavailablefromavarietyofsources.

26

Climate Change International Technical and Training Center (CITC)

Figure2‐12Trendsinfinancetodevelopingcountries

($billion,2011prices),2002–2011

Source:EuropeanReportonDevelopment(2015)

EuropeanReportonDevelopment(2015)showsthetrendsinfinancetodevelopingcountries(Figure2‐12).

Itshowsfinancetodevelopingcountriesisdramaticallyincreasing.Particularly,domesticresources(both

publicandprivate)contributelargelyinincreaseofvolumeoffinance.Incontrast,contributionsof

internationalresourcesinincreaseofvolumeoffinancearestablebutrelativelylimited,eventhoughthose

internationalfinanceresourcesstillplayanimportantroleindevelopmentindevelopingcountries.

0

1000

2000

3000

4000

5000

6000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Domestic public resources

Domestic private resources

International private resources

International public resources

27

Climate Change International Technical and Training Center (CITC)

Figure2‐13ShareofForeignDirectInvestmentFlowsintoAsianDevelopingCountries(2013,

$million)

SourceUNCTAD(2015).

Figure2‐13showstheshareofforeigndirectinvestment(FDI)inflowsindevelopingAsiancountriesin

2013.AccordingtodatafromUnitedNationsConferenceonTradeandDevelopment(UNCTAD)(UNCTAD

2015),$381billionhasbeeninvestedinAsiandevelopingcountries.Ofthis,themajoritywenttothe

People’sRepublicofChina(PRC)(includingHongKong,China)—$203billion.AmongdevelopingAsian

countries,thetop10recipientcountrieswere:PRC($203billion),Singapore($64billion),India($28

billion),Indonesia($18billion),Thailand($13billion),Malaysia($12billion),Kazakhstan($10billion),Viet

Nam($9billion),ThePhilippines($4billion)andTurkmenistan($3billion). Thesecountriesshare95%of

theFDIinflowinAsia.Sudo(forthcoming)arguesthattheprivatesectortendstoinvestinprofitableand

low‐riskprojects,whichiswhyFDIflowsintocountrieswheretheeconomicscaleislargeandthe

investmentenvironmentiswellestablished.

28

Climate Change International Technical and Training Center (CITC)

Figure2‐14:ShareofClimateChangeOfficialDevelopmentAssistanceFlowintoAsianDeveloping

Countries(2013,$million)

Source:OECD(2015)

ODAisalsoanimportantfinancialsourceoffinance.Figure2‐14showstheclimatechangebilateralODA

financeflowinAsiaandPacificcountries.AccordingtodatafromtheOrganisationforEconomic

Co‐operationandDevelopment(OECD2015),Asiancountriesreceivedapproximately$11billionforclimate

changeactivitiesthroughbilateralODAin2013.India,Indonesia,VietNamwererankedasthelargest

recipientsofbothFDIandclimatechange‐relatedODA.However,Uzbekistan,Bangladesh,andSriLanka

weretheleadingrecipientsofclimatechangeODA(thesecountriesreceivedlimitedFDI).Thevolumeof

ODAissignificantlysmallerthanthatofFDI,butitisimportantforlow‐incomeandleastdeveloped

countries.

ClimateFinanceFlowinAsia

Amongothers,EastAsiaandthePacificremainedthelargestdestinationofclimatefinanceflows,accounting

for31%ofthetotalorUSD119billion,upby22%from2013.Chinaaloneaccountedfor22%(USD84

billion)oftotalfinance.(Figure2‐15)

29

Climate Change International Technical and Training Center (CITC)

Figure2‐15:Totalclimatefinancebreakdownbyregion,2014inUSDbillion

Source:CPI(2015)

Mostofthosefinancesareusedformitigationactivities,andverylimitedfinanceflowstoadaptationand

REDD+activities.

30

Climate Change International Technical and Training Center (CITC)

Bibliography

AsianDevelopmentBank(ADB).(2013).EnergyOutlookforAsiaandthePacific.Manila:AsianDevelopment

Bank.

Climate Policy Initiative (CPI). (2015). Global Landscape of Climate Finance 2015.

http://climatepolicyinitiative.org/wp‐content/uploads/2015/11/Global‐Landscape‐of‐Climate‐

Finance‐2015.pdf

Food and Agriculture Organization (FAO). (2009). Capital requirements for agriculture in developing

countriesto2050.Rome:FAO.

http://www.fao.org/fileadmin/templates/esa/Global_persepctives/Long_term_papers/Capitalr

equirements‐agriculture.pdf

International Development Finance Club (IDFC). (2014). Scaling up renewable energy investments. IDFC

DiscussionNote.Frankfurt:IDFC.

http://www.idfc.org/Downloads/Publications/02_other_idfc‐expert_documents/IDFC_Sustaina

ble_Infrastructure_Paper_01‐12‐14.pdf

InternationalEnergyAgency(IEA).(2012).Energytechnologyperspectives.Paris:IEA.

InternationalRenewableEnergyAgency(IRENA).(2015).Renewablepowergenerationcostsin2014.Abu

Dhabi:IRENA.

http://www.irena.org/DocumentDownloads/Publications/IRENA_RE_Power_Costs_2014_report

OrganisationforEconomicCooperationandDevelopment(OECD).(2006).Infrastructureto2030:Telecom,

landtransport,waterandelectricity.Paris:OECDPublishing.

OECD.(2012).Strategictransportinfrastructureneedsto2030.Paris:OECDPublishing.

OECD. (2015). OECD Statistics on External Development Finance Targeting Environmental Objectives

IncludingtheRioConventions.Paris

http://www.oecd.org/environment/environment‐development/rioconventions.htm

Sudo,T. (2015). Climate finance and the role of international cooperation. InB.N. Lohani,M.Kawai&V.

Anbumozhi(Eds.),Managingthetransitiontoalow‐carboneconomy—Perspective,policies,and

practicesfromAsia.Tokyo:AsianDevelopmentBankInstitute.

http://www.adb.org/publications/adbi‐managing‐transition‐low‐carbon‐economy‐perspectives‐policies‐pr

31

Climate Change International Technical and Training Center (CITC)

actices‐asia

Sudo,T.(Forthcoming).DomesticandInternationalFinanceinaRegionalPerspective.InKaliappaKalirajan

andVenkatachalamAnbumozhi(eds.)InvestingonLow‐CarbonEnergySystems‐ Implicationsfor

RegionalCooperation.SpringerPublishing.

Spors,F.(2014).ResultsBasedFinancing:ItsrelevanceforclimatechangemitigationandtheCDM,Global

DNAForum,Bonn,13th‐14thNov,2014

https://www.google.com/url?q=https://cdm.unfccc.int/sunsetcms/storage/contents/stored‐fil

e‐20141112165251921/4)%2520Result%2520based%2520Finance,%2520World%2520Bank.

pdf&sa=U&ved=0ahUKEwjDyJHa39PLAhXIHKYKHYXCBrAQFggFMAA&client=internal‐uds‐cse&

usg=AFQjCNF2yWskasbCmh3A_0sSIM5QUjkZhg

UnitedNationsConferenceonTradeandDevelopment(UNCTAD).2015.UNCTADstat.On‐lineDatabase

http://unctadstat.unctad.org/CountryProfile/home/Indexen.html

United Nations Environment Programme (UNEP). (2011).Forests ina green economy:A synthesis. UNEP.

http://www.unep.org/pdf/PressReleases/UNEP‐ForestsGreenEcobasse_def_version_normale.pd

f

World Economic Forum (WEF). (2013). The green investment report—The ways and means to unlock

privatefinanceforgreengrowth—AreportoftheGreenGrowthActionAlliance.WEF:Davos.

http://www3.weforum.org/docs/WEF_GreenInvestment_Report_2013.pdf

32

Climate Change International Technical and Training Center (CITC)

CHAPTER3 ACCESSINGCLIMATEFINANCINGAND

MANAGINGPROJECTS

Whatreaderscanlearninthischapter

Thischapterincludesbriefexplanationontheeffectiveprojectdevelopmentandmanagement;application

processesandprojectcriteria/requirements;workingwithnationalclimatefinancefocalpoints;domestic

managementofclimatefinance;andmonitoringandevaluation,reportingcriteriaandMRV.

3.1 AccessingClimateFinancing

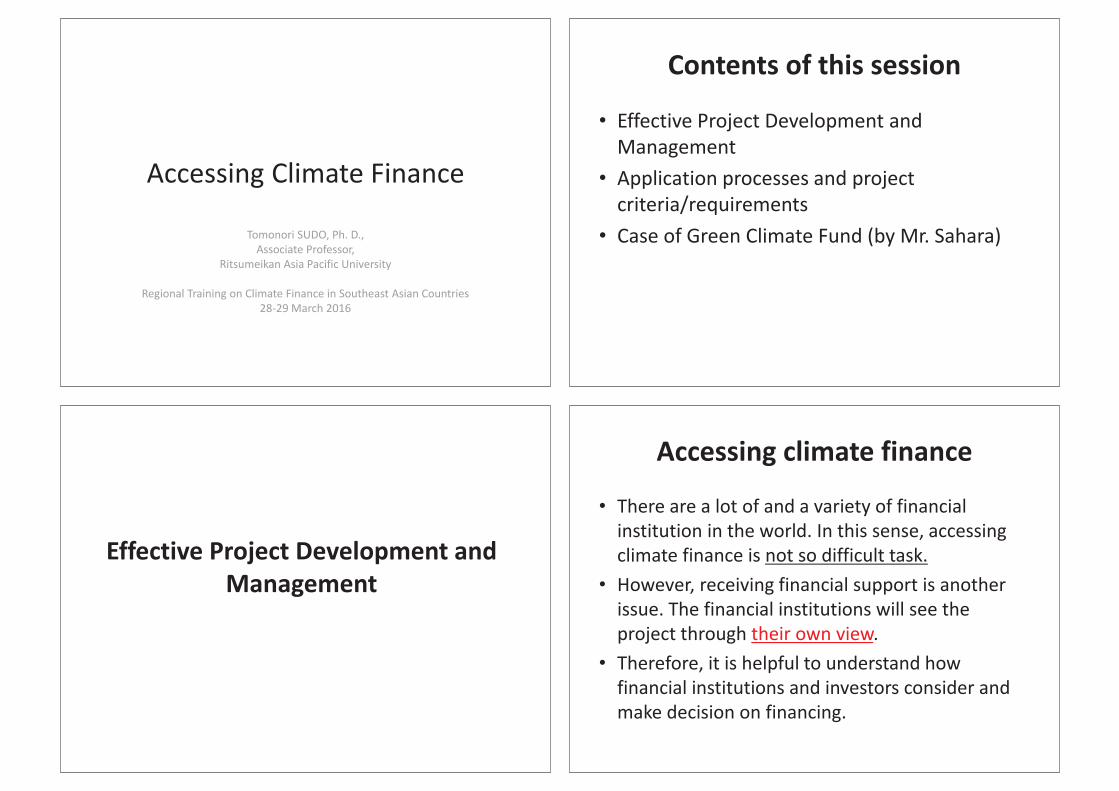

3.1.1 EffectiveProjectDevelopmentandManagement

Therearealotofandavarietyoffinancialinstitutionintheworld.Inthissense,accessingclimatefinanceis

notsodifficulttask.However,receivingfinancialsupportisanotherissue.Thefinancialinstitutionswillsee

theprojectthroughtheirownview.Therefore,itishelpfultounderstandhowfinancialinstitutionsand

investorsconsiderandmakedecisiononfinancing.

Behaviorofinvestorsandfinancialinstitutions

InvestorsandFinancialinstitutionsgenerallyconsiderhowtomanagetheirfund.Theyhavemonetaryasset

whichtheyhavenoplantousecurrentlybutmaybeusedinfuture.So,theymayconsidertoinvest/finance

infinancialproducts(suchassavingsanddeposit),commoditiesand/orprojects.Thisisexplainedbythe

conceptof“Timepreference”.Timepreferencereferstothepreferenceofassetholderswhethertheywill

usetheirassetnoworinfuture.Thedecisionfactormaybevarieddependingontheconditionofasset

holder.

Oncetheydecidetousetheirassetinfuture,theywillconsiderhowtokeeptheirassetuntilwhentheyneed

tospendtheirasset.Thereareseveraloptionsforthem,butthoseoptionsmaydifferdependingonthelevel

ofprofitabilityandRisks.

33

Climate Change International Technical and Training Center (CITC)

Figure3‐1:Financeflowsbetweendifferenttimes

Source:Sudo

Figure3‐1showstheflowsoffinanceoverthetime.Onceinvestorand/orfinanciersinvestorfinanceinthe

project,theymayexpectreceivesomerevenueintheformofinterestpaymentordividend.Generally,value

ofassetwillbediscountedoverthetime.Therefore,investorsandfinancialinstitutionneedtocoverthe

discountedvalueofasset.Inaddition,transactioncostandexpectedlossduetoriskswillbeaddedonthe

discountrate.Iffinancialrevenuewillexceedthefinancialcost,investorsandfinancierswillinvestor

financeintheproject.Generally,suchprofitabilitywillbeassessedbyReturnonInvestment(ROI),Return

onAsset,and/orInternalRateofReturns(IRR).

EffectiveProjectDevelopmentandManagement

Anotherfactorforinvestmentdecisionistherisks.Thereareseveralrisksassociatewiththeprojectas

showninTable3‐1.Ifsomeofthoserisksareexposed,theprojectwillnotberealizedorgeneratebenefitas

expected.Thus,riskassessmentandmanagementarethekeyfactorforinvestorsandfinanciers;otherwise

theymaylosetheirassetinvestedintheproject.

34

Climate Change International Technical and Training Center (CITC)

Table3‐1:majorrisksassociatedwithproject

Stage Country(Sovereign)Risk ProjectRisk

Planning&

Design

PoliticalandAdministrativeRisk

‐Policy,LawandInstitutionalChange

‐License,Approval

EconomicRisk

‐ExchangeRisk

‐TransferRisk

‐EconomicCrisisRisk

‐CreditRisk

War&RiotRisk

RegulatoryRisk

‐NoFeasibility

‐Failure/DelayofApproval

‐Failure/DelayofFinanceclosure

‐Stakeholder’sobjection

‐Failureofconclusionofcontract

andagreements

Implementation ConstructionRisk

‐Delayofcompletion

‐Defaultofcontractor

‐Stakeholder’sobjection

‐EnvironmentalImpact

‐ForceMajeure

Operation Operationrisk

‐Breakdown,accident

‐Lowproduction

‐DefaultofSuppliers/

Buyers/Projectitself

‐ForceMajeure

Inaddition,expectedoutputandoutcomearealsoimportantfactorfordecisionmakingbyinvestorsand

financiers.Recently,mostofinvestorsandfinancialinstitutionsconcernontheESG(Environment,Social

andGovernance)investment.Investorsandfinanciersarealsoapartofmemberofthesociety,sotheyneed

35

Climate Change International Technical and Training Center (CITC)

toconsiderhowtheirinvestmentandfinancewillleadtodegradationofenvironmentorimpactonthe

society.Rather,theyarethinkingthattheirinvestmentandfinancewillgenerateadditional(orindirect)

valueforthesociety.Thisisbecauseinvestorsandfinanciersneedtosecuretheirprudencefromthemarket

otherwisetheywillnotbeabletoraisefundfromthemarket.

Thus,foreffectiveprojectdevelopmentandmanagement,riskmanagementandrealizationofexpected

outcomebytheprojectareindispensable.Therefore,well‐documentedprojectcanshownotonlytherisks

andexpectedoutcomeidentifiedbutalsothemeasuresonhowtomitigaterisksandensuretherealization

ofexpectedoutcomes.

3.1.2 Applicationprocessesandprojectcriteria/requirements

Applicationprocessesforclimatefinancevariesdependingontheruleofeachfinancialinstitution.Major

climatefundssuchasGCF,GEFandAdaptationFundrequesttonominatenationalfocalpoint.Incaseof

developmentfinance,bilateraldonorswillfrequentlycommunicatewithnationalplanningministryand

multilateralfinancialinstitutionsoftencommunicatewiththeministryoffinance.

DirectAccess

Mostoftheinvestorsandfinancialinstitutionsallowrecipientstoaccessthemdirectly.Directaccessis

probablythemostidealwaytoobtainfinanceandinvestment,particularly,iftherecipientoften

communicateswithsomeoffinancialinstitutions.Inviewoffinancialinstitutions,itwouldbenobigmatter

iftheirclientsaccesstothemandrequestforfinance,sincefinanceinstitutionshavealreadyhadenough

informationontheirclientsandmaybefamiliarwiththebehaviouroftheclient.However,ifitisthefirst

contactfromrecipienttothefinancialinstitution,financialinstitutionsneedtocollectandanalyse

informationontherecipient,anddecidewhethertherecipientisappropriateforstartingnewtransaction.

AccessthroughNationalfocalpoints

Generally,internationalpublicfinanceinstitutionsincludinginternationalclimatefundsrequesttothe

recipienttocommunicatethroughnationalfocalpoint.Insuchcase,recipientsshouldconsultwithnational

focalpointwhentheyneedtoaccesstotheinternationalpublicfinanceinstitutions.

NationalfocalpointwillbedesignatedbytheGovernment.So,ministryoragencywhichisservingas

nationalfocalpointisvarieddependingonthepolicyofthegovernment.Duetoitsnature,nationalfocal

36

Climate Change International Technical and Training Center (CITC)

pointshouldknowtheirclimateanddevelopmentpolicyaswellasthecharacteristicsofandprocedurefor

applicationoffinancefromthefund.

Inviewoffinancialinstitutions,nationalfocalpointisconsideredasarepresentativeofthecountry

government.Therefore,ifnationalfocalpointworksappropriately,bothfinancialinstitutionsandrecipient

willbebenefittedfromnationalfocalpoint.

AccessthroughIntermediaries/implementingentities

Someoffinancialinstitutionsareassignedasintermediariesorimplementingentitiesofthefund.

Intermediariesshouldmeetthefiduciarystandardofthefund.Inthissense,Intermediaries/implementing

entitieswillrepresentthefund,andprovideservicestotheirclientsassimilartothedirectaccess.

Projectcriteriaand/orrequirement

Eachfund,financialinstitutionsandinvestorshavetheirowncriteriaand/orrequirements.Specialpurpose

fundssuchasclimatefundsrequesttherecipientstomeetthecriteriaand/orrequirements,sincepurpose

ofthefundsarestrictlyrestricted.Ontheotherhand,otherfinancialinstitutionssuchascommercialbanks

maysetverylimitedcriteriaand/orrequirement.

3.2 ManagingClimateFinanceProjects

Projectmanagementisoneofthemostimportantworkstorealizeobjectivesandexpectedoutcomesofthe

project.Well‐managedprojectcanreducerisksandcosts.Therefore,notonlyprojectownerbutalso

investorsandfinancialinstitutionsaswellasregulatorybodiesconcernonthebetterproject

implementation.

3.2.1 Workingwithnationalclimatefinancefocalpoints

Asnotedintheprevioussection,nationalfocalpointforclimatefundswillplayanimportantroletobridge

betweenthefundsandrecipientsofthefinance.Thenationalfocalpointisexpectedtoserveasawindow

forbothfundsandrecipient.

37

Climate Change International Technical and Training Center (CITC)

3.2.2 DomesticmanagementofClimateFinance

Sincetheprojectwillbeimplementedwithinthehostcountry,projectshouldbemanagedunderthe

domesticrulesandconditions.Ontheotherhand,frequentchangeofpolicies,vulnerabilityofmarketsand

legalsystemwillbeconsideredasrisksassociatedwiththeproject.Inthissense,stableconditionofnational

circumstanceswillbeessentialforbetterprojectmanagement.

Inaddition,whenthehostcountryreceivesinternationalclimatefinance,internationalmonetaryflowwill

takeplace.Thismayaffecttothecountry’spoliciessuchasmacroeconomicpolicy,monetarypolicy,

investmentpolicy,employmentpolicy,industrialdevelopmentpolicyetc.Therefore,itneedstoidentifythe

impactonthecountry’spolicyduetoinflowofclimatefinance,andtakeappropriatepoliciesandmeasures

reflectingsuchchanges.

3.2.3 MonitoringandEvaluation,ReportingCriteriaandMRV

Monitoringandevaluationprocessisindispensableforeveryclimatefunds,investorsandfinancial

institutionstocheckwhethertheprojectachievesitsobjectives,expectedoutcomes.Basedonthe

monitoringandevaluation,lessonslearnedwillbeidentifiedandappliedtoanotherprojects.Such

knowledgewillbereflectedFinancialInstitutions’appraisal/duediligenceprocessaswell.

Inaddition,accordingtotheUNFCCC,NonAnnexpartiesarealsorequestedtosubmitBURincluding

informationonthereceiptoffinanceandtechnologyaswellasinventoryofGHG.

38

Climate Change International Technical and Training Center (CITC)

CHAPTER4 DEVELOPINGSUPPORTIVEINFRASTRUCTURES

FORCLIMATEFINANCE

Asdiscussed,mitigationofrisksandimprovementofprofitability(ormakingidealbusinesscases)will

promotefurtherinvestmentandfinanceinclimaterelatedactivities.Tosupportonthis,thereareseveral

workstobedonebythepublic.

Figure4‐1:Relationsamongstakeholdersoftheproject

Source:Sudo

Figure4‐1showsarelationamongstakeholdersincludingthegovernment.Eveniftheprojectwillbe

implementedbyprivatesector,thegovernmentcouldplayasignificantroletomobilizefinancefrom

investorsandfinancialinstitutions.

Assessingdomesticneedsandprioritiesforclimatefinance

Domesticneedsarefundamentalsourceofbusinessseedsforprojectdevelopers,sincetheproject

developerswilldevelopprojectbasedontheneedsoftheirclientinthecountry.Higherneedsandpriority

totheprojectmeanshigherdemandtotheproject,thatis,higherandstablerevenuewillbeexpected.Thus,

informationonthedomesticneedsandprioritywillbebenefittedforinvestorsandfinanciers.

39

Climate Change International Technical and Training Center (CITC)

PolicyInstrumentsforFinancingClimateActivities

Policyinstrumentsareespeciallysignificantinthepolicymaking&implementationprocessastheyarethe

techniquesormeansthroughwhichstatesattempttoattaintheirgoals.Inviewofinvestorsandfinancial

institutions,drasticpolicychangeisrecognizedasapartofcountryrisks.Thus,strongpoliticalwilland

leadershipalongwithstablepolicycanmitigatetherisksforfinanciers.

Publicdevelopmentofsupportiveinstitutions&infrastructures

Projectsincludingfinanceinproject,ingeneral,willberesponsibleforapartofsystem,andprojectwillbe

implementedbasedonthekeysystemandinfrastructure.Forfinance,domesticmonetarysystemand

bankingsystemwillbefundamentalinfrastructure.Forexample,volatileexchangerateisconsideredasone

oftherisksforinvestorsandfinancialinstitutions.

SecuringMulti‐StakeholderCooperationandExpertiseinprojects

AsshowninFigure1,manyofstakeholdersshouldbeinvolvedintheproject.Somemaybeaffectedpositive

ornegativeimpactfromtheproject.Theconflictamongstakeholdersisalsoconsideredasoneofrisks.

Publicsector,asoneofstakeholders,shouldsecuresuchavarietyofstakeholdersintheproject.Inaddition,

eachcountryholdssomespecificexpertiseinthecountry,includingindigenousknowledgeand

technologies.

Strategiesforenhanceddeliveryofinternationalsupport

Internationalsocietyisalsorecognizedasapartofstakeholderoftheproject.Inclimatefinance,

internationalpublicdonorsandprivatesectorinvestorsarealsoplayanimportantroletosupportclimate

relatedactivities.Particularly,internationalprivateinvestorsareconcernedaboutthecountrysystemis

enoughcompatibletotheinternationalstandards.Thus,somestrategiesforenhancinginternational

supportandfinanceshouldbeconsidered.

CooperationmechanismsandSouth‐SouthCollaboration

Asnotedabove,bettercooperationamongstakeholdersisthekeyforsuccessofclimaterelatedactivities

includingfundraising.Oninternationalcooperation,developedcountriesarenotthesinglesourceof

cooperation.Insomecase,otherdevelopingcountriesmaybeabletosharebetterlessonslearnedfromtheir

experiencesandsuccess.Sudo(2015)andSudo(Forthcoming)highlightsaneffectivenessofregional

cooperationinclimatefinancing.Forexample,Figure4‐2showsanideaofASEANregionalcooperation

frameworkforeffectivelowcarbondevelopmentfinanceinAsia.

40

Climate Change International Technical and Training Center (CITC)

Figure4‐2:PotentialframeworkofalowcarbondevelopmentfinancefacilityinAsia

Source:Sudo(2015)

41

Climate Change International Technical and Training Center (CITC)

ANNEX CASESTUDY:GREENCLIMATEFUND(GCF)

I. BackgroundofGreenClimateFund

TheGreenClimateFund(GCF)wasconceivedatCOP15 inCopenhagen,Denmark in2009,as themain

multilateralfinancingmechanismtosupportdevelopingcountriestackleclimatechange,aspartiespledged

tomobilize $100 billion in long‐term financing per year by 2020. In 2010, at COP16 in Cancun,Mexico,

Parties,indecision1/CP.16establishedtheGCFasthemainoperatingentityoftheFinancialMechanismof

theConventionunderArticle11.

TheGCFwillsupportprojects,programmes,policiesandotheractivitiesindevelopingcountryParties.The

Fund is governedby theGCFBoard.Theassetsof theGCFwillbeadministeredbya trusteeonly for the

purposeof,andinaccordancewith,therelevantdecisionsoftheGCFBoard.TheWorldBankwasinvitedby

theCOPtoserveastheinterimtrusteeoftheGCF,subjecttoareviewthreeyearsafteroperationalizationof

theFund.TheCOPalsodecidedthattheGCFwastobedesignedbytheTransitionalCommittee(TC).AtCOP

17 held in Durban, the COP adopted decision 3/CP.17, in which Parties welcomed the report of the TC

(FCCC/CP/2011/6 and Add.1) and approved the Governing Instrument for the GCF. Parties, at COP 18,

endorsedtheconsensusdecisionoftheGCFBoardtoselectSongdo,Incheon,RepublicofKoreaasthehost

of the GCF. At COP 19, Parties welcomed the establishment of the independent GCF secretariat and the

selectionoftheExecutiveDirectoroftheGCFbytheGCFBoard.

TheGreen Climate Fundwas given themandate tomake ‘an ambitious contribution to the global efforts

towardsattainingthegoalssetbytheinternationalcommunitytocombatclimatechange’.TheConference

ofthePartiestotheUNFCCCestablishedGCFtopromoteaparadigmshifttowardslowemissionandclimate

resilient development pathways in developing countries and help achieve the goal of keeping a global

temperature riseunder2degreesCelsius.GCF is theonlystand‐alonemultilateral financingentitywhose

solemandateistoservetheConventionandwhichaimstodeliverequalamountsoffundingtoadaptation

andmitigation.

The Fund strives to ensure it adds value relative to other funds and financial institutions with similar

low‐emission,climate‐resilientdevelopmentobjectives.Itprovidesaddedvalueinsixkeyways:

1.Maximizecountryownership

2.Balancebetweenadaptationandmitigation

3.Balancedgovernancewithequalvoiceforcontributorsandrecipients

4.Diversityofpartners

5.Diversityoffinancialinstruments

6.LargestdedicatedclimateFundglobally

42

Climate Change International Technical and Training Center (CITC)

Through these unique approaches, the Fund will set itself apart and catalyse a paradigm shift in the

developmentpathwaysof its recipient countries. Itwillput themona trajectorymorecompatiblewitha

changingclimate,andmakethemmoreresilientandresponsivetoit.

The Green Climate Fund offers a full toolkit of financial instruments to deliver on itsmandate, including

concessionalseniorandsubordinated loans,equity,guaranteesandgrants,whereneeded.These financial

tools allow the Fund to tailor its financial support to the project needs of public, private and

nongovernmentalentities.Thisisparticularlyusefulforthosedevelopingcountriesinwhichclimateaction

requiresthefullflexibilityoffinancialinstrumentsandcounterpartrisktaking,beyondfiscally‐constrained

centralgovernments.

II. GCFandResourceMobilizationandFinanceCriteria

1 ResourceMobilization

Developing countries need long‐term, predictable flows of climate finance to aid their transformation to

low‐emissionandclimateresilienteconomies.Significantclimate finance isalsoneeded tobuild the trust

necessaryforanambitiousglobalclimatesettlement.

Torespondtothis,industrializedcountrieshavecommittedtomobilizesignificantclimatefinancingfroma

varietyofresources.GCFisexpectedtoplayadistinctiveroleinchannelingtheseclimateinvestments.The

Fund`s Initial ResourceMobilization period lasts from 2015 to 2018. By the end of 2015, the Fund had

raised overUSD10billion equivalent in pledges from46 state, region and city governments, including9

representingdevelopingcountries, and finalizedoverUSD6.6billionequivalent intoagreements.Further

contributionsareinvitedonanongoingbasis.

ScaleisessentialforGCFtodeliveronitsambitiousmandate,andtheFundexpectstodrawuponresources

frompublic, private andphilanthropic sources. The Fundwill (1) continue to have an active outreach to

states,regionsandcitygovernmentstoexpanditscontributorbase,(2)considerinnovativewaystoaccept

contributionsfromindividuals,and(3)workwiththeexistingnetworkofpartnerstotapintotheirnetwork

inordertoincreasethecontributorbasefromallsectors.

2 FinanceCriteria

The Fund must ensure that its investments drive a paradigm shift towards low emissions and climate

resilience. It considersbothmitigationandadaptationas criticalpartsof the response to climate change,

withalleightresultsareasholdingimportantpotential,andwillstrivetoachieveabalanceinitsportfolio.

The goal of the Fund will be to seek the “sweet spots” between national priorities, potential to deliver

concreteclimatebenefits,costconsiderations,andopportunitiestodeliverco‐benefits.

43

Climate Change International Technical and Training Center (CITC)

The Fund has a particular opportunity to differentiate itself from other climate finance channels by

catalysinggreaterinvestmentinadaptation,particularlyfromtheprivatesector.Accordingtosomefigures

on climate finance flows show that adaptation funding reaches less than 10% of the total dedicated to

mitigationefforts.Adaptationcosts,however,areprojectedtohaveasignificant–andoftenunderestimated

‐impactongrossdomesticproduct(GDP)output.

GDPwillbethehighestforcountriesinSub‐SaharanAfricaandsmall‐islanddevelopingstates(SIDS).These

countriesarehighlyvulnerableandaffectedbyadverseclimateevents.Climatechangeisprojectedtocost

SIDS1%oftheirGDP,fivetimeshigherthantheaverage.Africa,withone‐seventhoftheworld’spopulation,

ispoisedtobearnearly50%ofestimatedglobaladaptationcosts inhealth,watersupply,andagriculture

andforestry.LossoflifeandreductioninGDParealsolikelytobethehighestforLeastDevelopedCountries

(LDCs)andSIDS.Thepoorestpeople,andpoorestcountries,arelikelytobethemostaffectedbytheimpacts

ofclimatechange.

TheroleofprivateinvestmentisanotherareawheretheFund’sapproachwillbedifferentiated.TheFundis

determined to partner with the private sector and harness its implementation capacity, to catalyse

investmentintheresultsareasandmaximizetheimpactoftheFund’sowninvestments.

Therearemanygapsinthecurrentlandscape,andsomeareasthathavelargepotentialarenotadequately