223 final rpt bd15 - valuergeneral.nsw.gov.au · 1.3 liverpool lga demographics ... growth over the...

TRANSCRIPT

Independent Property Valuers& Consultants ACN : 099 913 210 ABN : 80 099 913 210 5/2 East Street, Five Dock, NSW 2046 PO Box 697 Five Dock NSW 2046 phone : (02) 9713-9077 Fax : (02) 9713-9022 email : [email protected]

FINAL REPORT

LAND TAX PROGRAMME DISTRICT 223 - LIVERPOOL BASE DATE - 1 JULY 2015

Prepared by SOUTHERN ALLIANCE VALUATION SERVICES PTY LTD

for VALUER GENERAL &

LAND & PROPERTY INFORMATION

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 2 of 63

Table of Contents

EXECUTIVE SUMMARY .......................................................................................................................... 4

1.0 GENERAL DESCRIPTION OF LOCAL GOVERNMENT AREA ................................................ 6

1.1 Introduction ....................................................................................................................................................................... 6

1.2 Liverpool LGA Built & Natural Environment .................................................................................................................. 7

1.2.1 Dwellings and Housing Tenure ................................................................................................................................. 7

1.3 Liverpool LGA Demographics .......................................................................................................................................... 8

1.3.1 Population Growth & Age ......................................................................................................................................... 8

1.3.2 Indigenous Population ............................................................................................................................................... 8

1.3.3 Birthplaces, Languages Spoken and Religion ........................................................................................................... 8

1.3.4 Income and Housing Costs ........................................................................................................................................ 9

2.0 NUMBER OF VALUATIONS IN THE ZONE CATEGORIES .................................................... 10

2.1 Zone Category Break-Up ................................................................................................................................................ 10

2.1.1 Table: All Zones ...................................................................................................................................................... 10

2.1.2 Table: Residential Uses ........................................................................................................................................... 10

2.1.3 Graph: All Zones ..................................................................................................................................................... 11

2.1.4 Graph: Residential Uses .......................................................................................................................................... 11

3.0 TOWN PLANNING & ZONING INSTRUMENTS ........................................................................ 12

3.1 Environmental Planning Instruments .............................................................................................................................. 12

3.1.1 Liverpool Local Environmental Plan 2008 .............................................................................................................. 12

3.1.2 State Environmental Planning Policy (Major Development) 2005 .......................................................................... 12

3.1.3 State Environmental Planning Policy (Sydney Region Growth Centres) 2006 ....................................................... 13

3.1.4 State Environmental Planning Policy (Western Sydney Parklands) ........................................................................ 13

3.2 Development Controls Plans ........................................................................................................................................... 13

3.3 State Environmental Planning Policies (SEPP) ............................................................................................................... 14

3.4 Regional Environmental Plans ........................................................................................................................................ 15

4.0 IDENTIFIED SIGNIFICANT CHANGES IN USE OR DEVELOPMENTS OF PROPERTY AND OTHER FACTORS WHICH MAY AFFECT VALUATIONS .................................................... 16

4.1 South West Growth Centre .............................................................................................................................................. 16

4.2 South West Rail Link ...................................................................................................................................................... 17

4.2.1 Status of the South West Rail Link .......................................................................................................................... 17

4.3 Moorebank Freight Intermodal Terminals....................................................................................................................... 18

4.3.1 Overview of Moorebank Freight Intermodal Terminals .......................................................................................... 18

4.3.2 Location of Moorebank Intermodal Freight Terminal ............................................................................................. 19

4.3.3 SIMTA Intermodal – Conditional Approval ............................................................................................................ 20

4.3.4 Alternate Locations – Badgerys Creek .................................................................................................................... 20

4.4 Badgerys Creek – Western Sydney Airport ..................................................................................................................... 21

4.4.1 Western Sydney Airport Timeline ........................................................................................................................... 21

4.4.2 Planning an airport for Western Sydney .................................................................................................................. 21

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 3 of 63

Table of Contents

4.5 Property Market Overview .............................................................................................................................................. 24

4.6 Economy Overview ......................................................................................................................................................... 25

4.7 Court Cases ..................................................................................................................................................................... 29

5.0 ADDED VALUE OF IMPROVEMENTS ......................................................................................... 30

5.1 Residential ....................................................................................................................................................................... 30

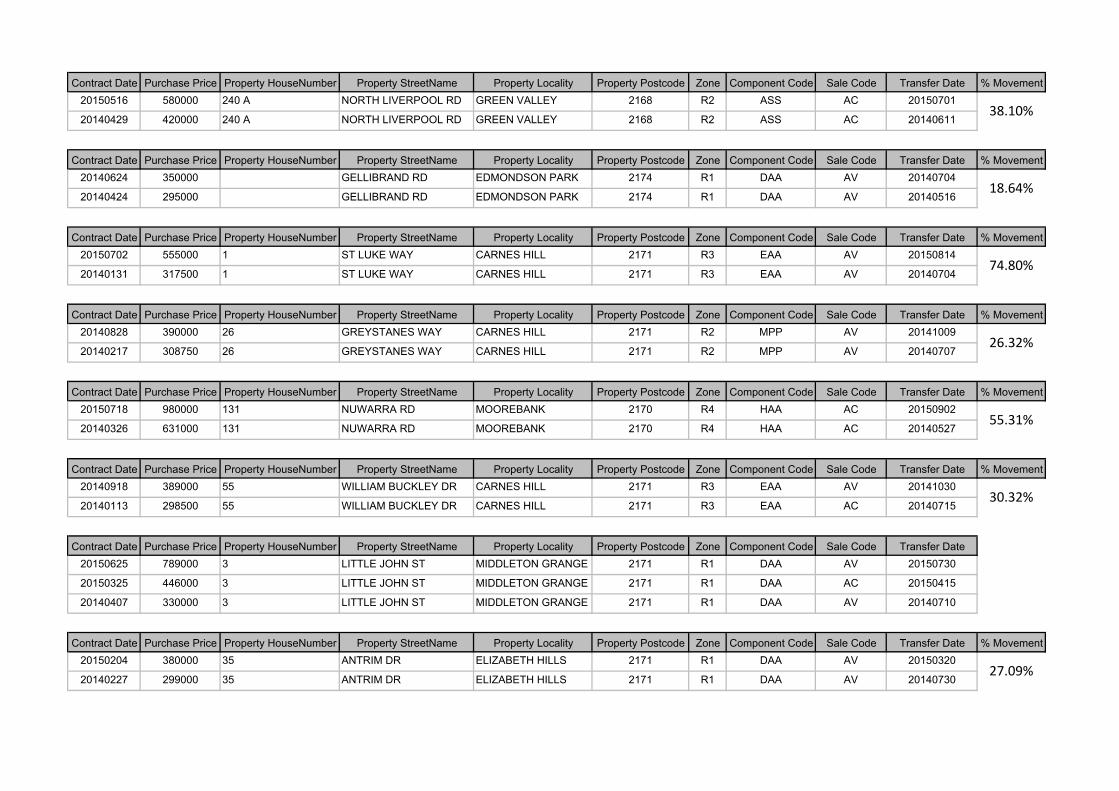

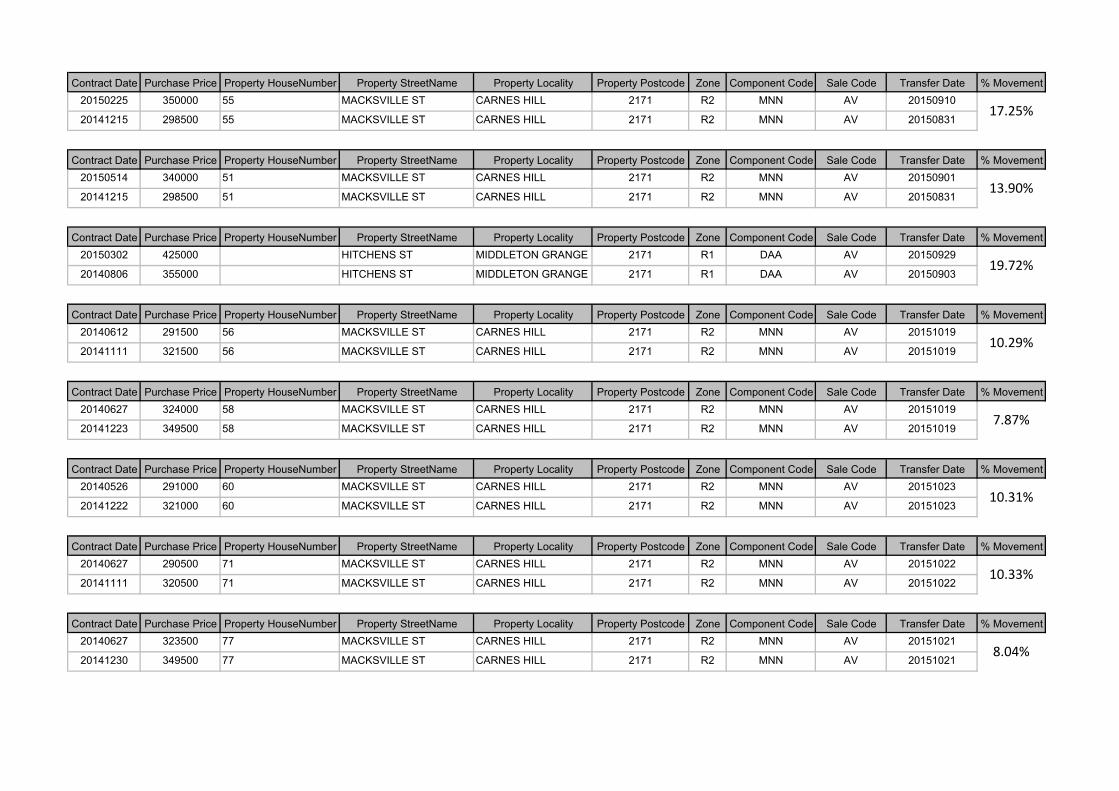

5.1.1 Paired Analysis ........................................................................................................................................................ 33

5.2 Commercial / Retail / Industrial ...................................................................................................................................... 40

6.0 CHANGES TO COMPONENTS ILLUSTRATED BY CHANGES TO THE EXISTING VALUE RELATIONSHIPS. ............................................................................................................................ 41

6.1 Value Levels - Typical Properties ................................................................................................................................... 41

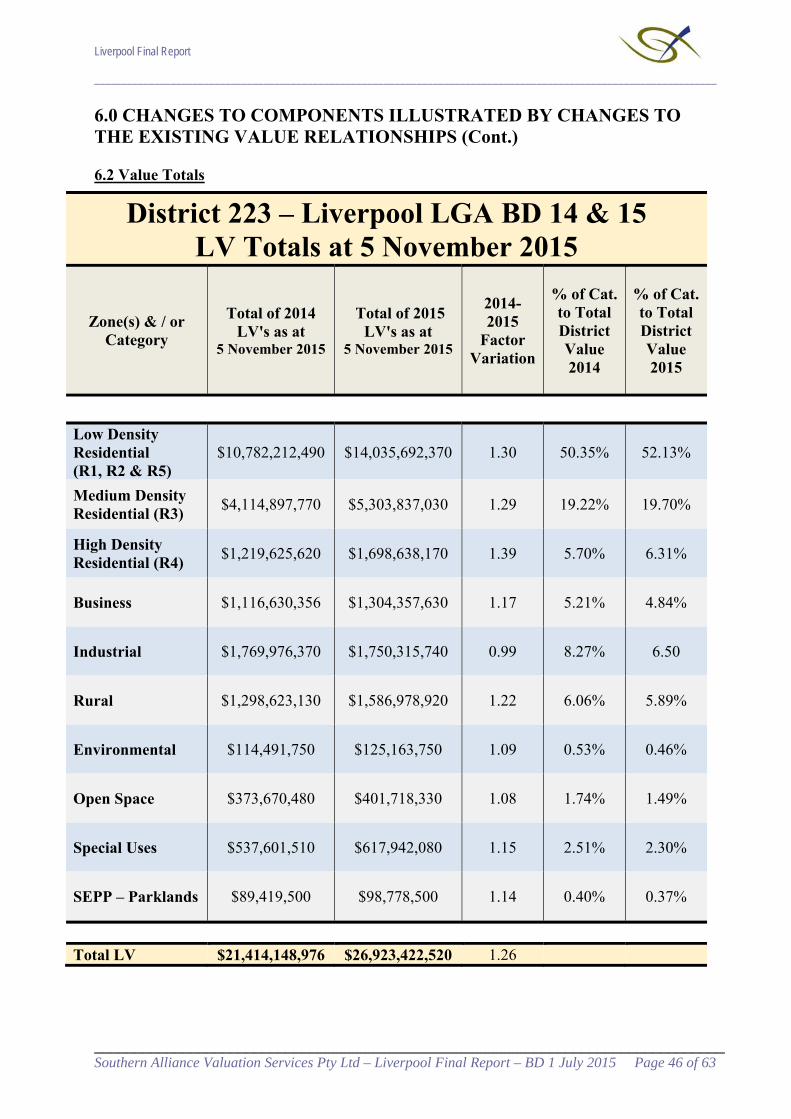

6.2 Value Totals .................................................................................................................................................................... 46

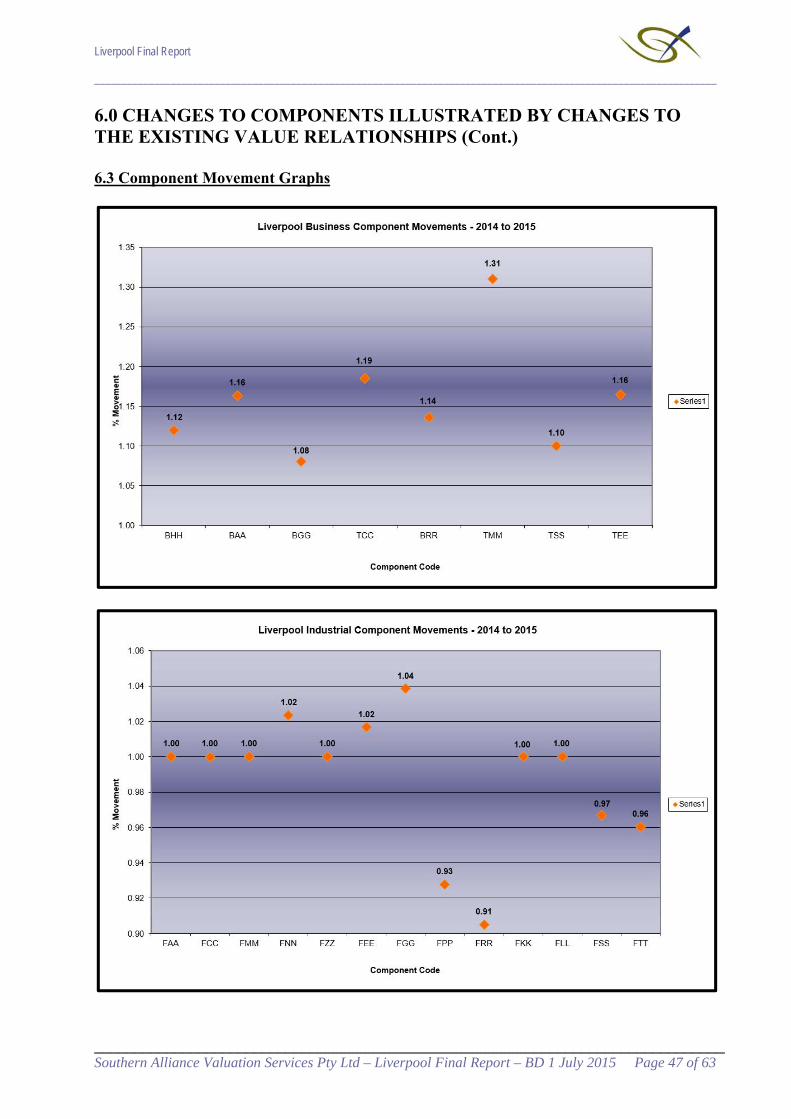

6.3 Component Movement Graphs ........................................................................................................................................ 47

7.0 MARKET COMMENTARY: ............................................................................................................ 49

7.1 Residential ....................................................................................................................................................................... 49

7.1.2 Sales and Resales ..................................................................................................................................................... 52

7.1.3 Change in Median Values ........................................................................................................................................ 56

7.1.4 Building Approvals .................................................................................................................................................. 56

7.2 Commercial / Retail ......................................................................................................................................................... 58

7.3 Industrial.......................................................................................................................................................................... 59

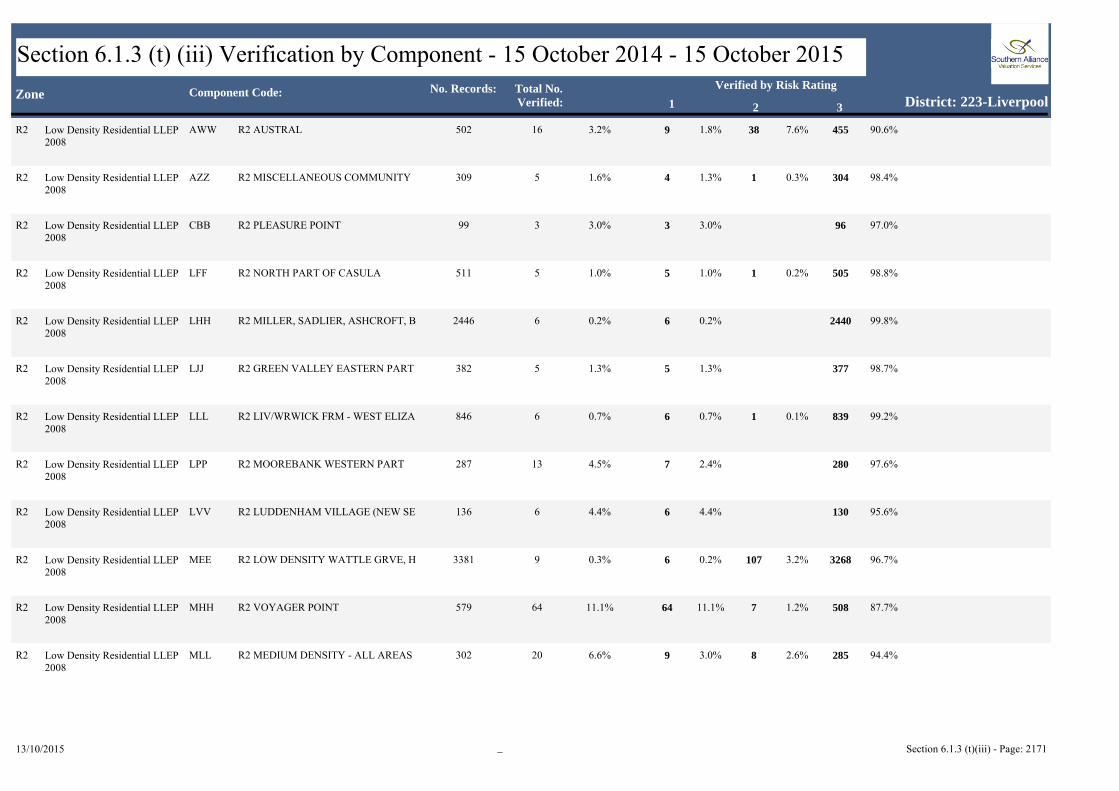

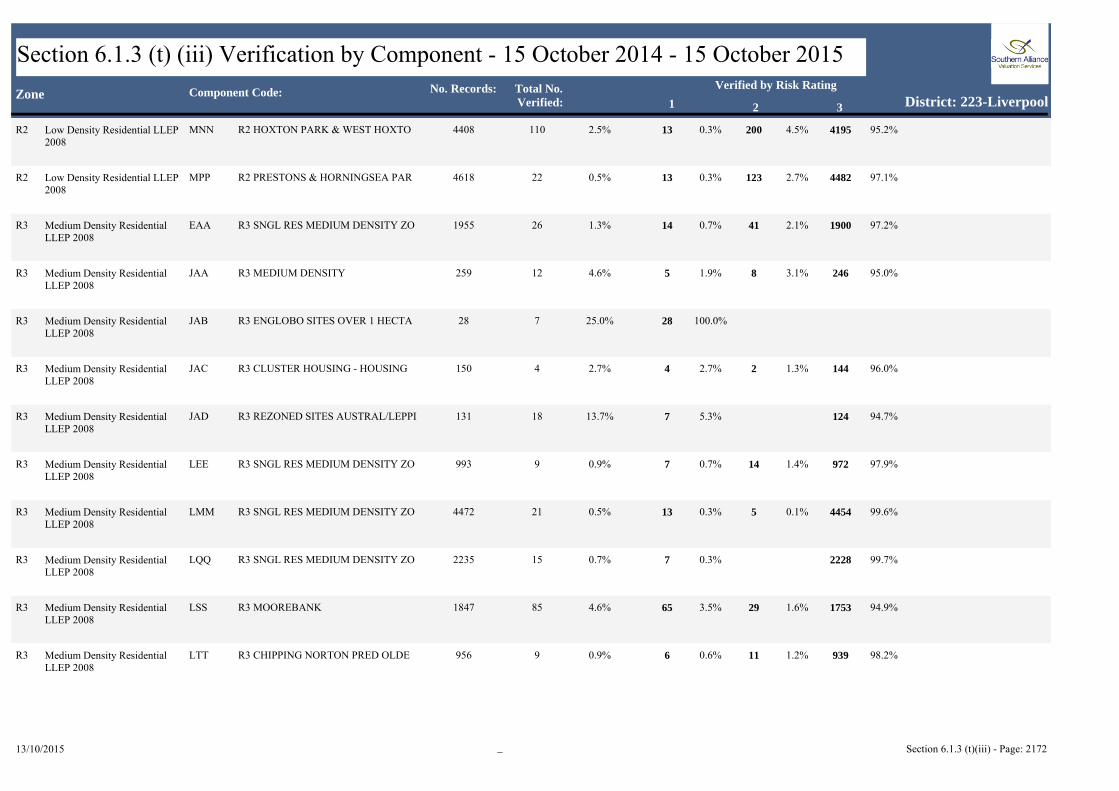

8.0 MANAGEMENT OF COMPONENTS, VERIFICATION& HANDCRAFTING ....................... 60

8.1 Verification ...................................................................................................................................................................... 60

9.0 QUALITY ASSURANCE ................................................................................................................... 61

9.1 Overview ......................................................................................................................................................................... 61

9.2 Coefficient of Dispersion (COD) .................................................................................................................................... 61

9.3 Mean Value to Price Ratio (MVP) .................................................................................................................................. 61

9.4 Price Related Differential (PRD) ..................................................................................................................................... 61

9.4 Subsequent Valuations upon Objection / Reascertainment ............................................................................................. 62

10.0 CONCLUSION .................................................................................................................................. 63

10.1 Purpose of this Report ................................................................................................................................................... 63

10.2 Signatory ....................................................................................................................................................................... 63

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 4 of 63

EXECUTIVE SUMMARY

All properties in NSW are valued each year for rating and land tax purposes. All valuations are issued to the Office of State Revenue for land tax. Valuations are also issued to councils either each year or every 2nd, 3rd or 4th year. This report details the land valuation programme for the Liverpool Local Government Area (LGA). The majority of land values are determined using mass valuation techniques. The Valuer-General's mass valuation system is applied as follows: 1) Properties that react to market forces in a similar way are grouped together in a component, and 2) The existing values of those properties in a component are updated by a market-based factor that is then used as a multiplier of the prior Land Value. The result is then checked by the Contract Valuer and individually verified values applied as appropriate. The use of mass valuation techniques does have limitations, particularly over a period of time. The continued application of factors may lead to a distortion in the relativity of values within a geographical area. Some types of properties are so few in number or likely to be so sensitive to localised changes that individually verifying values is the only appropriate method. Although a mass valuation system is used to determine the majority of land values, the Valuation of Land Act requires that each land value be a market value. Each land value must be capable of being tested and supported on its own against all the available market evidence. The total number of valuation entries (as at 5 November 2015) within Liverpool LGA – 55,929. The total land value in dollars (as at 5 November 2015) for BD 1 July 2015 within Liverpool LGA - $26,923,422,520.

The last local government base date or year when the valuation notice was issued was for the Base Date 1 July 2014. The total land value for Base Date 1 July 2014 (as at 5 November 2015) was $21,414,148,976 which represents a percentage change of 26% to Base Date 1 July 2015. The percentage change reflects the overall movement for land values within the Liverpool LGA based on market sales evidence. Residential – Overall the residential market within the Liverpool LGA exhibited signs of strong positive growth over the 12 months ending 30 June 2015. As a whole, components within each respective zone illustrated the following movement over the 2015 valuing year: ‘R1 – General Residential’ at 32.2%, ‘R2 – Low Density Residential’ at 29.7%, ‘R3 – Medium Density Residential’ at 28.9%, ‘R4 – High Density Residential’ at 39.3% and ‘R5 – Large Lot Residential’ at 29.0%. On average, residential land within each component, depending on locality and development potential, moved within a band of 9.8%% and 65.1% between the Base Date 1 July 2014 and 1 July 2015. In total, there are 44 residential components in the residential zones (noted above). 25 residential components recorded positive growth in excess of 30% between base date 1 July 2014 and base date 1 July 2015. There are 26 components in the ‘R2 – Low Density Residential’ zone, with 15 of those components recording positive growth greater than 30% over the 12 months ending 30 June 2015. Some components in the ‘R2’ zone which had shown considerable growth over the 2015 valuing year are: ‘AFF – Chipping Norton’ at 35.1%, ‘ALL – Warwick Farm’ at 35.4%, ‘AWW – Austral’ at 65.1%, ‘LPP – Moorebank (Western Part)’ at 37.7% and ‘MLL – Medium Density (LGA Wide)’ at 38%. Component ‘AWW’ recorded to the largest growth over the 2015 valuing year partly attributable to a rezoning of the land from ‘RU4 – Primary Production (Small Lots)’ under Liverpool LEP 2008 to ‘R2 – Low Density Residential’ under the SEP 2006 – Sydney Regional Growth Centres – the ‘R2’ zoning allowing a greater development potential of the land than that allowable under the ‘RU4’ zone. Other single residential component areas in the residential zoning that exhibited strong positive growth over the 2015 valuing year are: ‘MUU – R1 Large Parcels’ at 35.8% and ‘JAD – R3 Sites (Austral / Leppington)’ at 42.7%. Furthermore, density / development sites continued to be in demand as developers seek quality assets which can meet the market demand for residential property while providing more affordable housing options. Individual pockets can move against the trend for varying reasons, however on the whole properties within the Liverpool Municipality were relatively consistent.

Commercial / Retail – As a whole, from 1 July 2014 to 1 July 2015, commercial and retail property markets within the Liverpool LGA recorded mixed levels of growth. Overall, components within each respective zone illustrated the following movement over the 2015 valuing year: ‘B1 – Neighbourhood Centre’ at 12.0%, ‘B2 – Local Centre’ at 16.3%, ‘B3 – Commercial Core’ at 16.0%, ‘B4 – Mixed Use’ at 21.6%, ‘B5 – Business Development’ at 10.0% and ‘B6 – Enterprise Corridor’ at 16.5%.

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 5 of 63

EXECUTIVE SUMMARY (Cont.)

Individual components within each business zone show varying levels of growth for numerous reasons including, but not limited to, location, development potential and access to infrastructure / public transport – however, as a whole, business zoned components generally moved within a band of 8.0% and 29.5% over the 2015 valuation year. Component ‘TMM – B4 Town Centre Mixed Use’ in the ‘B4 – Mixed Use’ zone recorded strong positive growth over the 12 months ending 30 June 2015. Component ‘TMM’ comprises commercial, retail & mixed use properties and potential development sites within the Liverpool Town Centre and recorded growth of 29.5% over the valuation period. Retail properties across the Liverpool LGA have recorded good growth over the 2015 land valuing year with all retail sites (excluding components ‘BGG’ and ‘TSS’ – predominantly larger sites) exhibiting growth between 12% and 29.5%. Growth in retail spending (and ultimately retail asset values) is being supported by various factors. For example, increases in household net worth, driven by the uplift in residential dwelling values, are resulting in providing support for discretionary retail spending and retail spending on household goods. Additionally, a low Australian dollar and low interest rates are providing some overall support to retail properties and retail land values. Colliers International report that Neighbourhood Retail properties for the first half of 2015 illustrated a prime yield range from 6.50% up to 7.75% and a secondary yield range from 8.00% up to 10.00%. Additionally, Colliers International report that Sub-Regional shopping centres’ for the first half of 2015 exhibited a prime yield range from 6.50% up to 7.50% and a secondary yield range from 7.50% up to 9.50%.

Industrial – Overall, the industrial market within Liverpool LGA was fairly subdued with 6 components recording nil growth, 3 components recording a modest increase in values and 4 components exhibiting a contraction in values. Overall, each industrial zone exhibited the following results over the 2015 valuing year: ‘IN1 – General Industrial’ at 0.3%, ‘IN2 – Light Industrial’ at -1.4% and ‘IN3 – Heavy Industrial’ at -2.7%. Generally, industrial sites situated to the ‘East of Liverpool CBD’ performed better than those industrial sites situated to the ‘West of Liverpool CBD’. Colliers International report as a result of a reduction in available stock within the southern Sydney industrial market displacing owners and investors to assets located in the southwest Sydney region, combined with infrastructure upgrades and other developments within the southwest region including the Moorebank Intermodal Freight Precinct and Badgerys Creek Airport, have led to further yield compression with the yield range for prime assets, as at September 2015, being 6.5-7.5 per cent and 8-9 per cent for secondary assets. However, as highlighted in the body of this report, over the 2015 valuing year ending 30 June 2015, some industrial locale’s performed better than others and the above summarised comments are general in nature and may not apply to all industrial properties/locales within the Liverpool LGA.

TABLE OF TYPICAL VALUES Location Zone Size (square metres) 2015 Land Value Brearley Ave, Middleton Grange General Residential 364.1 $368,000 Weir Cres, Lurnea Low Density Residential 556.4 $340,000 Nottingham Cres, Chipping Norton Low Density Residential 693.9 $534,000 Pritchard Ave, Hammondville Low Density Residential 556.4 $381,000 Craig Ave, Moorebank Medium Density Residential 663.9 $410,000 Galloway St, Busby Medium Density Residential 607 $293,000 Bigge St, Warwick Farm High Density Residential 651 $599,000 Dwyer Rd, Bringelly Large Lot Residential 20,250 $869,000 Findley Rd, Bringelly Primary Production 386,200 $1,510,000 Denham Court Rd, Denham Court Rural Landscape 20,230 $1,120,000 Bellfield Ave, Rossmore Primary Production (small lots) 20,230 $780,000 Marsh Pde, Casula Neighbourhood Centre 297.2 $138,000 George St, Liverpool Commercial Core 613.3 $980,000 Moore St, Liverpool Mixed Use 501.2 $757,000 Regent Cres, Moorebank General Industrial 1,859 $647,000 Alfred Rd, Chipping Norton Light Industrial 9,194 $2,940,000 Enterprise Cct, Prestons Heavy Industrial 3,887 $1,160,000

Murray Edmondson Southern Alliance Valuation Services Pty Ltd

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 6 of 63

1.0 GENERAL DESCRIPTION OF LOCAL GOVERNMENT AREA

1.1 Introduction

Liverpool Local Government Area (LGA) is situated approximately 28 kilometres southwest of Sydney’s Central Business District and covers an area of 306 square kilometres, comprising 42 suburbs from Greendale in the west to Hammondville in the east. The 42 suburbs include: 1. Ashcroft 15. Green Valley 29. Middleton Grange 2. Austral 16. Greendale 30. Miller 3. Badgery’s Creek 17. Hammondville 31. Moorebank 4. Bringelly 18. Heckenberg 32. Mount Pritchard 5. Busby 19. Hinchinbrook 33. Pleasure Point 6. Carnes Hill 20. Holsworthy 34. Prestons 7. Cartwright 21. Horningsea Park 35. Rossmore 8. Casula 22. Hoxton Park 36. Sadleir 9. Cecil Hills 23. Kemps Creek 37. Silverdale 10. Cecil Park 24. Len Waters Estate 38. Voyager Point 11. Chipping Norton 25. Leppington 39. Wallacia 12. Denham Court 26. Liverpool 40. Warwick Farm 13. Edmondson Park 27. Luddenham 41. Wattle Grove 14. Elizabeth Hills 28. Lurnea 42. West Hoxton

Source: Liverpool Council Website – Maps of Liverpool

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 7 of 63

1.0 GENERAL DESCRIPTION OF LOCAL GOVERNMENT AREA (CONT.)

1.2 Liverpool LGA Built & Natural Environment Liverpool LGAs main commercial / retail facilities are located in the Liverpool Town Centre and the adjoining main road frontages to the Hume Highway, The Cumberland Highway and Newbridge Road. Liverpool LGAs main industrial locations include Moorebank, Chipping Norton, Warwick Farm and Prestons. It is understood the industrial lands account for only 2.73% of the total area in the Liverpool LGA (as at 2009). Prestons includes a higher proportion of vacant / yet to be developed sites, including the western section of the area which was rezoned form a rural zoning in 2007. Natural assets include the Georges River and Nepean River, Chipping Norton Lakes, Bents Basin and 7,459 hectares of bush land including Cumberland Plain Woodland. Liverpool also has over 250 parks, with recreation accounting for 5.83% of total land area and national parks 12.14% of total land area of the LGA (as at 2009). Major features of the Liverpool LGA include the Holsworthy Military Camp, Warwick Farm Racecourse, Westfield Liverpool, Sydney International Shooting Centre and Powerhouse Regional Arts Centre. Key educational facilities include TAFE NSW South Western Institute with colleges in Liverpool and Miller. Major health facilities include Liverpool Hospital and Sydney Southwest Private Hospital. Liverpool is well serviced by public transport with both the East Hills and Main South West railway lines passing through the LGA. Liverpool LGA also has access to many arterial roads including M5 & M7 motorways and the Hume Highway & Cumberland Highway. Urban areas of the Liverpool LGA are well serviced by local transportation options.

1.2.1 Dwellings and Housing Tenure

The overall number of occupied private dwellings grew by 6,709 (12%) to 55,958 in the five years to 2011. At the 2011 Census, 24% of occupied private dwellings in Liverpool were fully owned, 42% were being purchased and 30% were rented. The combined owned and being purchased tenure in Liverpool, at 66% of all dwellings, is almost identical to Sydney generally at 65%. At the same time, 8.1% of Liverpool residents were social housing tenants, a considerable drop from 19% in 1991. This is compared to 5% of people renting social housing in the Greater Sydney region in 2011. Separate houses continue as the dominant form of housing in Liverpool at 75% of all dwellings. This is significantly higher than the Sydney proportion of 61% of all dwellings. It is however far less than some of Liverpool's neighbours (95% in Wollondilly, 92% in Camden and 81% in Campbelltown).

(Source: Information summarised / data extracted from Liverpool City Council Website)

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 8 of 63

1.0 GENERAL DESCRIPTION OF LOCAL GOVERNMENT AREA (CONT.)

1.3 Liverpool LGA Demographics 1.3.1 Population Growth & Age

As at the 2011 Census, Liverpool's population was 180,143. This represents an increase of 15,181 people (8%) over the 2006 population figure of 164,962 and a 15% increase over the last ten years. The rate of population growth in Liverpool between 2006 and 2011 exceeded that of the Greater Sydney region (6%) and New South Wales (5%).

The Estimated Resident Population of Liverpool as at 30 June 2014 was 199,928. Liverpool continues to be a young city: the median age was 33 years in 2011. It is younger compared to neighbouring areas, and Greater Sydney which was 36 years. In Liverpool, 38% of the population was less than 25 years of age. Liverpool also has an ageing population: the 55+ age group was the fastest growing age group in 2011. There has been a 17% increase in this population since 2006.

1.3.2 Indigenous Population The number of Indigenous people in 2011 grew by 483 to 2,677 people and has increased to 1.5% since 2006. Liverpool has a larger proportion of Indigenous people compared to Greater Sydney's 1.2%.

1.3.3 Birthplaces, Languages Spoken and Religion

The number of persons born overseas increased by 9,548 (13%) to 71,715. The overseas born population rose to 40% of the population, an increase of 9% in the last 20 years. By comparison, 34% of Sydney's population was born overseas. Liverpool's people come from over 150 different birthplaces. The top ten overseas birthplaces in 2011 were Fiji (6,395), Iraq (6,114), Vietnam (5,230), India (4,213), Philippines (3,580), Lebanon (3,573), New Zealand (3,076), Italy (2,893), England (2,177) and Serbia / Montenegro (2,233). At the 2011 Census, English was stated as the only language spoken at home by 44.4% of Liverpool's population. Around half of Liverpool's residents said they spoke a language other than English at home. 8.7% of residents said they spoke English not well or not at all. Liverpool residents speak more than 140 different languages. The top ten languages spoken at home after English are: Arabic, Hindi, Vietnamese, Italian, Spanish, Serbian, Greek, Assyrian, Cantonese and Macedonian.

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 9 of 63

1.0 GENERAL DESCRIPTION OF LOCAL GOVERNMENT AREA (CONT.) The Catholic and Anglican religions remain the top two religious affiliations, however overall proportions have declined since 2006. The Islamic and Eastern Orthodox religions have seen increased proportions since the last Census, as has the proportion of people who have stated they have no religion. Buddhism and Hinduism have also increased since 2006.

1.3.4 Income and Housing Costs Median individual, household and family incomes in Liverpool have increased slightly since 2006, however people in Liverpool continue to pay a large proportion of their income on rent – 12% pay more than 30% of their household income on rent. Compared to its neighbours, Liverpool has higher median household incomes ($1,299) compared with Fairfield ($1,022), Bankstown ($1,091) or Campbelltown ($1,251), but lower compared with Camden ($1,727), Sutherland ($1,674), Wollondilly ($1,478) or Penrith ($1,398). Median monthly mortgage repayments in Liverpool are the same as the Sydney median at $2,167. This represents a 20% increase since 2006. However, more people in Liverpool pay over 30% of their household incomes on mortgage repayments - 17% compared to 12% in Sydney. This demonstrates the considerable "housing stress" in Liverpool. Compared to its neighbours, median monthly mortgage repayments are equal to Camden, Wollondilly and Penrith, higher than in Fairfield, Campbelltown and Bankstown but lower than in Sutherland.

(Source: Liverpool City Council Website)

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 10 of 63

2.0 NUMBER OF VALUATIONS IN THE ZONE CATEGORIES

2.1 Zone Category Break-Up 2.1.1 Table: All Zones

Zone Category Break-Up as at 5 November 15

Residential 50,947 91.09% Business 840 1.50% Industrial 696 1.24% Rural 1,722 3.08% Environmental 147 0.26% Open Space 885 1.58% Special Uses 570 1.02% SEPP – Parklands 122 0.22%

Totals 55,929 100.00%

2.1.2 Table: Residential Uses

Residential Uses Break-Up as at 5 November 15

Single Dwelling Sites 49,800 97.75% Medium Density 815 1.60% High Density 332 0.65%

Totals 50,947 100.00%

NOTE: The ‘Medium Density’ and ‘High Density’ numbers above exclude single residential sites within the ‘R3 – Medium Density Residential’ and ‘R4 – High Density Residential’ zones.

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 11 of 63

2.0 NUMBER OF VALUATIONS IN THE ZONE CATEGORIES (Cont.)

2.1.3 Graph: All Zones

2.1.4 Graph: Residential Uses

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 12 of 63

3.0 TOWN PLANNING & ZONING INSTRUMENTS 3.1 Environmental Planning Instruments

Environmental Planning Instruments are the statutory controls for land use and major development standards. They usually consist of a written statement and a series of maps. They include:

Controls for land uses

Controls for key development standards such as height of buildings, subdivision sizes and floor space limitations

Controls for other matters such as heritage, flooding, tree preservation

Identification of land acquisition by Council and government authorities

In Liverpool there are currently 4 primary Environmental Planning Instruments that apply to land and provide land use zoning. These are:

1. Liverpool Local Environmental Plan 2008 2. State Environmental Planning Policy (Major Development) 2005 – Edmondson Park South 3. State Environmental Planning Policy (Sydney Region Growth Centres) 2006 – Austral and

Leppington North 4. State Environmental Planning Policy (Western Sydney Parklands)

3.1.1 Liverpool Local Environmental Plan 2008 On 29 August 2008 Liverpool City Council adopted the Liverpool Local Environmental Plan (LLEP) 2008. It complies with the standardised LEP format required by NSW Planning. The Liverpool Local Environmental Plan 2008 (written statement and maps) applies to all land in Liverpool except for areas where other planning instruments have overridden the plan. Some new growth centre areas no longer use the Liverpool Local Environmental Plan 2008 and have now been overridden by new planning instruments listed below.

3.1.2 State Environmental Planning Policy (Major Development) 2005

The State Environmental Planning Policy (Major Development) 2005 (written statement and maps) applies to certain land at Edmondson Park South. This Planning Policy was applied to parts of Edmondson Park by the NSW Government and has overridden the Liverpool Local Environmental Plan 2008. Planning controls are found in Schedule 3 State Significant Sites – Part 31 Edmondson Park South Site. The Edmondson Park South Development Control Plan 2012 is to be used in conjunction with the Major Development State Environmental Planning Policy 2005. To find out if your land is located within the Edmondson Park South site please view the Land Application Maps, found under the maps tab of the Major Development SEPP 2005.

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 13 of 63

3.0 TOWN PLANNING & ZONING INSTRUMENTS (CONT.)

3.1.3 State Environmental Planning Policy (Sydney Region Growth Centres) 2006

The State Environmental Planning Policy (Sydney Region Growth Centres) 2006 (written statement and maps) applies to land at Austral and Leppington North and has overridden Liverpool Local Environmental Plan 2008. Planning controls for development in Austral and Leppington North are found under Appendix 8 Liverpool Growth Centres Precinct and are used in place of the Liverpool Local Environmental Plan 2008. The Liverpool Growth Centre Precincts Development Control Plan is to be used along with the Sydney Region Growth Centres State Environmental Planning Policy. To find out if land is located within the Austral and Leppington North area please view the Land Application Maps, found under the maps tab of the Sydney Region Growth Centres SEPP 2006.

3.1.4 State Environmental Planning Policy (Western Sydney Parklands)

The State Environmental Planning Policy (Western Sydney Parklands) 2009 applies to land in the Western Sydney Parklands.

3.2 Development Controls Plans Development Control Plans provide detailed design controls for development. They consist of a written statement, illustrations and in some areas include maps. They include controls that apply to:

All land covered by the Development Control Plan

Certain land use zones

Certain localities

In Liverpool there are currently 4 Development Control Plans that apply. These are:

1. The Liverpool Development Control Plan 2008 [adopted 28 July 2008] (written statement and maps) applies to all land in Liverpool except where the following Plans apply.

2. The Edmondson Park South Development Control Plan 2012(written statement and maps) applies to all land in Edmondson Park South that is specified in the State Environmental Planning Policy (Major Development) 2005 Land Application Maps.

3. The Liverpool Growth Centre Precincts Development Control Plan (written statement and maps) applies to all land in Austral and Leppington North that is specified in the State Environmental Planning Policy (Sydney Region Growth Centres) 2006 Land Application Maps

4. Austral Leppington North DCP Road Network

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 14 of 63

3.0 TOWN PLANNING & ZONING INSTRUMENTS (CONT.)

3.3 State Environmental Planning Policies (SEPP)

The NSW Government has established State Environmental Planning Policies (SEPP) to address significant issues of the state and the people of NSW. SEPPs provide flexibility with standard provisions and various SEPPs must be considered as part of any development application process. SEPPs fall under the Environmental Planning and Assessment Act 1979 and are classified as an environmental planning instrument. Please be advised that when assessing a development application, a SEPP overrides, or can be applied in conjunction with, the requirements of Council’s LEP or DCP.

The following SEPPs may be used when assessing development applications within Liverpool City Council:

SEPP 4 ‐ Development without Consent and Miscellaneous Exempt and Complying Development

(Only certain parts apply, please check the Liverpool Local Environmental Plan as to what parts

of the SEPP apply.)

SEPP 6 ‐ Number of Storeys in a Building

SEPP 19 ‐ Bushland in Urban Areas

SEPP 21 ‐ Caravan Parks

SEPP 22 ‐ Shops and Commercial Premises

SEPP 30 ‐ Intensive Agriculture

SEPP 32 ‐ Urban Consolidation (Redevelopment of Urban Land)

SEPP 33 ‐ Hazardous and Offensive Development

SEPP 44 ‐ Koala Habitat Protection

SEPP 50 ‐ Canal Estate Development (this SEPP prohibits all canal estate development)

SEPP 55 ‐ Remediation of Land

SEPP 62 ‐ Sustainable Aquaculture

SEPP 64 ‐ Advertising and Signage

SEPP 65 ‐ Design Quality of Residential Flat Development

SEPP 70 ‐ Affordable Housing (Revised Schemes)

SEPP ‐ (Building Sustainability Index: BASIX) 2004

SEPP ‐ (Housing for Older People or People with Disability) 2004

SEPP ‐ (Major Projects) 2005

SEPP ‐ (Sydney Region Growth Centres) 2006

SEPP ‐ (Infrastructure) 2007

SEPP ‐ (Mining, Petroleum Production and Extractive Industries) 2007

SEPP ‐ (Temporary Structures and Places of Public Entertainment) 2007

SEPP ‐ (Exempt and Complying Development Codes) 2008

SEPP ‐ (Rural Lands) 2008

SEPP ‐ (Western Sydney Parklands) 2009

SEPP ‐ (Affordable Rental Housing) 2009

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 15 of 63

3.0 TOWN PLANNING & ZONING INSTRUMENTS (CONT.) 3.4 Regional Environmental Plans Regional Environmental Plans help provide a framework for detailed local planning by Council. LEPs are required to be consistent with the objectives and intent of the relevant REP. REPs considered relevant to development applications within Liverpool City Council:

GMREP No. 2 ‐ Georges River Catchment

SREP No. 9 ‐ Extractive Industry (No. 2 ‐ 1995)

SREP No. 20 ‐ Hawkesbury‐Nepean River (No. 2 ‐ 1997)

Council is legally bound to follow the requirements of these policies where applicable to the Liverpool LGA.

Please Note:

The above information on planning controls were sourced from Liverpool’s Council Website.

It is understood the various planning policies may be amended or superseded over time, thus it is imperative that any person check the above planning information is current, at date of viewing, via Liverpool Councils Website (http://www.liverpool.nsw.gov.au/) or the relevant State Planning Website (http://www.planning.nsw.gov.au/) or NSW Legislation Website (http://www.legislation.nsw.gov.au/).

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 16 of 63

4.0 IDENTIFIED SIGNIFICANT CHANGES IN USE OR DEVELOPMENTS OF PROPERTY AND OTHER FACTORS WHICH MAY AFFECT VALUATIONS

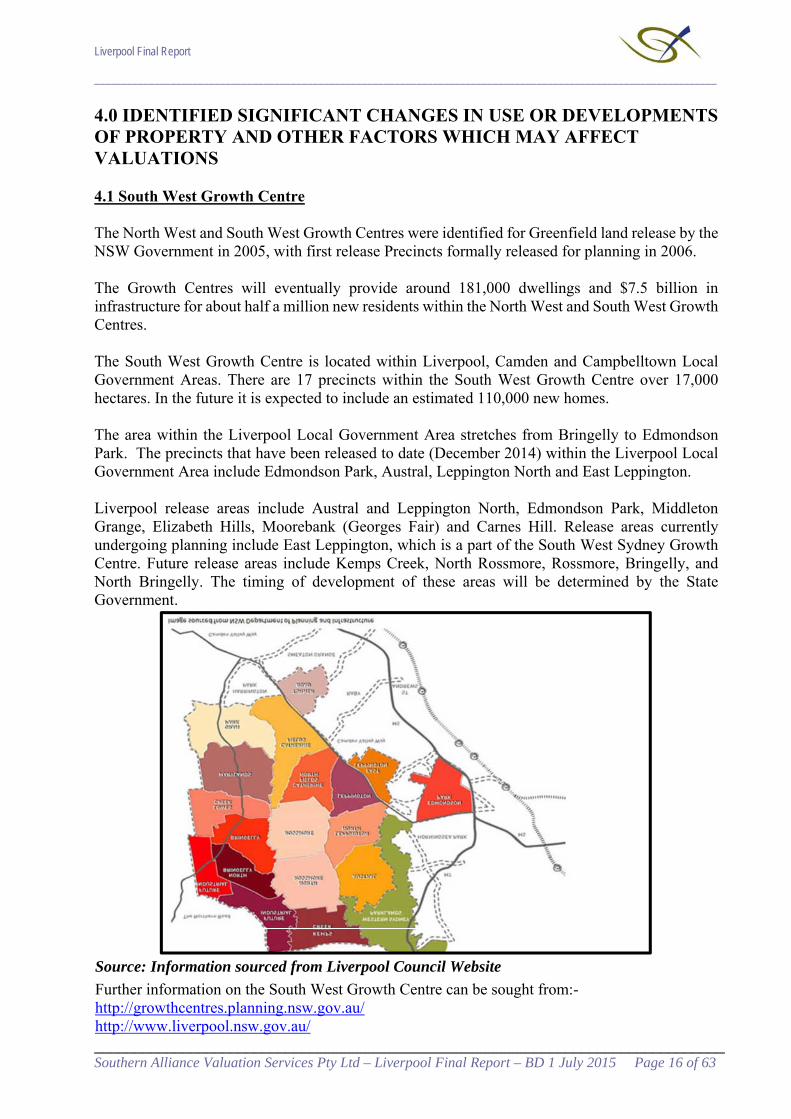

4.1 South West Growth Centre The North West and South West Growth Centres were identified for Greenfield land release by the NSW Government in 2005, with first release Precincts formally released for planning in 2006. The Growth Centres will eventually provide around 181,000 dwellings and $7.5 billion in infrastructure for about half a million new residents within the North West and South West Growth Centres. The South West Growth Centre is located within Liverpool, Camden and Campbelltown Local Government Areas. There are 17 precincts within the South West Growth Centre over 17,000 hectares. In the future it is expected to include an estimated 110,000 new homes. The area within the Liverpool Local Government Area stretches from Bringelly to Edmondson Park. The precincts that have been released to date (December 2014) within the Liverpool Local Government Area include Edmondson Park, Austral, Leppington North and East Leppington. Liverpool release areas include Austral and Leppington North, Edmondson Park, Middleton Grange, Elizabeth Hills, Moorebank (Georges Fair) and Carnes Hill. Release areas currently undergoing planning include East Leppington, which is a part of the South West Sydney Growth Centre. Future release areas include Kemps Creek, North Rossmore, Rossmore, Bringelly, and North Bringelly. The timing of development of these areas will be determined by the State Government.

Source: Information sourced from Liverpool Council Website

Further information on the South West Growth Centre can be sought from:- http://growthcentres.planning.nsw.gov.au/ http://www.liverpool.nsw.gov.au/

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 17 of 63

4.0 IDENTIFIED SIGNIFICANT CHANGES IN USE OR DEVELOPMENTS OF PROPERTY AND OTHER FACTORS WHICH MAY AFFECT VALUATIONS (Cont.)

4.2 South West Rail Link The South West Rail Link (SWRL) is a under construction and comprises of a 12 km twin track passenger rail line from Glenfield to Leppington via Edmondson Park. It includes stations at Edmondson Park and Leppington, an upgrade to Glenfield Station and a new train stabling (train parking) facility west of Leppington. Commuter car parks will be located at Edmondson Park and Leppington and will provide over 1,000 car spaces. The project is expected to be completed by 2016 with train services operating to Glenfield, Liverpool, Sydney CBD, and Parramatta. This rail link is the key to the success of the Edmondson Park and Leppington Town Centres. The project provides benefits to the areas directly serviced by the stations as well as the broader South West Sydney region including:

Promoting viability of higher residential densities close to the future Edmondson Park and Leppington Town Centres,

Improved viability of affordable housing in close proximity to the rail line and future town centres,

Supports development of large retail outlets at the future Edmondson Park and Leppington Town Centres,

Reduced reliance on the private vehicle and road based transport,

Reduced air pollution in western Sydney,

Improved mobility and independence for the community (particularly teenagers and the elderly), and

Reduced congestion on all roads, particularly motorway systems.

Source: Information sourced from Liverpool Council Website

4.2.1 Status of the South West Rail Link

The new South West Rail Link (SWRL) was opened to the public on 8 February 2015. The new Glenfield Transport Interchange and Glenfield Station were opened to the community on Sunday 23 September 2012. Major construction of the Glenfield to Leppington rail line component of the South West Rail Link commenced at the beginning of 2012 and works are 12 months ahead of schedule, with revenue services now commencing in 2015.

The Glenfield Junction northern flyover was built as part of the South West Rail Link project. The flyover was commissioned in early June 2014 and is helping to deliver a more efficient rail network for customers. The flyover separates T2 South Line services from T2 Airport Line services, reducing flow-on effects to other trains across the Sydney rail network if a service is delayed. Previously trains from the two lines had to take turns at Glenfield, slowing them down and creating a bottleneck whenever a train was delayed. The flyover now allows two trains to cross at the same time, one over the top of the other, meaning the network will flow much more effectively and predictably.

Source: Transport for NSW

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 18 of 63

4.0 IDENTIFIED SIGNIFICANT CHANGES IN USE OR DEVELOPMENTS OF PROPERTY AND OTHER FACTORS WHICH MAY AFFECT VALUATIONS (Cont.)

4.3 Moorebank Freight Intermodal Terminals 4.3.1 Overview of Moorebank Freight Intermodal Terminals

Two intermodal freight terminals have been proposed in Moorebank, on either side of Moorebank Avenue. The proposed intermodal terminal to the east of Moorebank Avenue is a private intermodal terminal. The proponent of this project is SIMTA. SIMTA is a joint venture, formed in 2007, comprising of Qube Logistics and Aurizon (formerly QR National). The proponent for the proposed intermodal terminal to the west of Moorebank Avenue is the Australian Government Department of Finance and Deregulation. It is known as the Moorebank Intermodal Terminal (MIT). The freight intermodals will be a destination for freight containers transported from the port via rail. From this terminal the freight containers will be distributed by trucks to their various destinations. The development is categorised as heavy industrial and is proposed to be operational 24 hours a day 7 days a week. The SIMTA intermodal has a maximum capacity of 1 million twenty foot equivalent unit (TEU) containers per year and the Moorebank Intermodal Terminal proposal is expected to have a maximum capacity of 1.2 million TEU containers per year. The proposals both also include warehousing and distributions facilities associated with the intermodal terminal. Intermodal terminals currently operating in Sydney

Enfield – 300 000 TEUs per year

Chullora – 300 000 TEUs per year

Minto – 45 000 TEUs per year

Yennora – 115 000 TEUs per year

Villawood – 15 to 20 000 TEUs per year

Total Maximum Capacity – 780 000 TEUs per year These sites are too small and too constrained to be able to move the forecast container demand. This is why the Government has identified a number of proposed sites for the development of additional intermodal facilities. If these freight intermodals are constructed, Moorebank will have more than double the total containers compared to the remainder of Sydney. It is considered that the distribution of containers should be more equitably spread across Sydney to better reflect the ultimate destination of the goods in the containers.

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 19 of 63

4.0 IDENTIFIED SIGNIFICANT CHANGES IN USE OR DEVELOPMENTS OF PROPERTY AND OTHER FACTORS WHICH MAY AFFECT VALUATIONS (Cont.) 4.3.2 Location of Moorebank Intermodal Freight Terminal

Image Source: http://www.micl.com.au/the-precinct/where-is-it-located.aspx

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 20 of 63

4.0 IDENTIFIED SIGNIFICANT CHANGES IN USE OR DEVELOPMENTS OF PROPERTY AND OTHER FACTORS WHICH MAY AFFECT VALUATIONS (Cont.)

4.3.3 SIMTA Intermodal – Conditional Approval

On 29th September 2014 the Planning Assessment Commission (PAC) released its determination in relation to the SIMTA intermodal terminal facility. The PAC have granted the project conditional approval, meaning that there are conditions and requirements that the applicant needs to meet before they can proceed with construction. The draft environmental assessment (EA) for the SIMTA intermodal terminal was publicly exhibited as required by NSW Planning and Infrastructure. The first draft of the EA exhibited from March to May 2012 was not adequate and a review of the EA and second exhibition period was undertaken in September and October 2013. Both times Council provided a comprehensive submission, prepared by the consultant Cardno, to the exhibition. Throughout this process, Council has maintained its objection to the SIMTA intermodal at Moorebank. Despite Councils objections, NSW Planning and Infrastructure provided Council with a draft conditional concept approval for the SIMTA intermodal terminal project in April 2014. The application was referred to the PAC for determination. The PAC held a public meeting as well as a meeting with Council officers in July 2014. The key condition to note is contained within the Schedule 2 titled "Limits of Approval". SIMTA have applied for approval to move 1 million containers per year with this concept approval. The conditions require that the operation not exceed 250 000 containers per year, with a potential to increase this to 500 000 containers subject to a further application.

4.3.4 Alternate Locations – Badgerys Creek

The announcement of the Badgerys Creek International Airport is a game changer for Western Sydney. A Deloitte report estimated that up to 28,500 jobs alone will be created as a result. It is a significant piece of infrastructure that demands a revisiting of the existing strategic framework for Sydney and New South Wales. As we speak, NSW Planning and Environment are updating the draft Metropolitan Strategy for Sydney to 2031 to incorporate the opportunities of the second airport at Badgerys Creek. The intermodal requirements of Western Sydney are a key consideration when discussing Sydney's second airport. The Badgerys Creek airport freight traffic would enhance existing land freight activity in Western Sydney. There are substantial efficiency opportunities when intermodals and international airports are co-located. This would create a strategic intermodal transportation hub connected to the outer Sydney Orbital and the rail network, and would potentially provide world-class global logistics to international and domestic transportation companies, while also being more cost effective. An intermodal would generate economic activity at the airport site from its first day of operation. Source: Information sourced from Liverpool Council Website

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 21 of 63

4.0 IDENTIFIED SIGNIFICANT CHANGES IN USE OR DEVELOPMENTS OF PROPERTY AND OTHER FACTORS WHICH MAY AFFECT VALUATIONS (Cont.)

4.4 Badgerys Creek – Western Sydney Airport

The Australian Government has confirmed that the site for Western Sydney's airport will be Badgerys Creek. The government has suggested that construction is expected to begin in 2016 and will be completed by mid-2020s. During the peak of the construction an estimated will 4000 jobs will be generated. The airport at Badgerys Creek is proposed to start out as a smaller sized airport with a single runway which will serve the expected moderate demand in the short term, but eventually will develop into a full scale airport with parallel runways as demand increases. The predicted initial cost of building the airport will be in the order of $2.4 billion based on estimated in the Joint Study on aviation capacity in the Sydney region, of which the majority of the investment is expected to come from the private sector. The Federal Government is expected to take the lead on facilitating the surrounding infrastructure, primarily focussing on roads.

Source: Information sourced from Liverpool Council Website 4.4.1 Western Sydney Airport Timeline

Date Event 1980s – 1990s Land at Badgerys Creek purchased by the Australian Government

1985 Environmental Impact Statement (EIS) produced, planning restrictions introduced

1997 – 1999 Second EIS produced 2012 – 2013 Site viability studies (assessing 80 locations a 18 sites in NSW) April 2014 Badgerys Creek announced as site for a Western Sydney Airport

2014 – 2016 Detailed planning and preparation underway, including the Airport Plan, EIS and meeting right of first refusal requirements

2014 – 2024 Road works progressing in Western Sydney Mid 2020s Operations could commence (single runway) Around 2050 Second runway potentially operational

4.4.2 Planning an airport for Western Sydney

Long-standing planning restrictions around the Badgerys Creek site—many in place for more than 30 years—have been designed to provide a buffer between the proposed airport and urban development. Unlike Sydney (Kingsford Smith) Airport, which is surrounded by built up areas, the nearest suburban residential area to a Western Sydney Airport will be kilometres away, making an airport in Western Sydney the most buffered of all of the major Australian airports. As a result, Western Sydney will be able to compete on an equal footing with its competition in Queensland and Victoria by having an airport operating on a curfew-free basis.

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 22 of 63

4.0 IDENTIFIED SIGNIFICANT CHANGES IN USE OR DEVELOPMENTS OF PROPERTY AND OTHER FACTORS WHICH MAY AFFECT VALUATIONS (Cont.) Curfew-free airports provide significant benefits to communities and businesses by supporting growth in not only local, but also regional and national economies. Melbourne Airport suggests its curfew-free status allows for the movement of an extra two million passengers a year and adds $590 million to the Victorian economy through visitor spending.

The Australian and NSW governments in partnership have already committed more than $3.6 billion to a 10-year road investment plan for Western Sydney, and planning has ensured an airport would expand to meet growing demand. The first steps towards this future are already being taken.

A draft Airport Plan and draft Environmental Impact Statement have been prepared and are now available for community comment until 18 December 2015. More information is available on the draft Airport Plan page and the draft EIS page.

Work has already begun on Stage one of the Bringelly Road upgrade and on the Werrington Arterial Road.

A rail corridor and station on the airport site are being planned. In parallel, Transport for NSW has already commenced consultation with the community to identify a suitable passenger rail corridor option to serve the proposed airport and the surrounding area.

It is expected work on the site could commence in 2016 with operations at the proposed airport planned to commence in the mid-2020s.

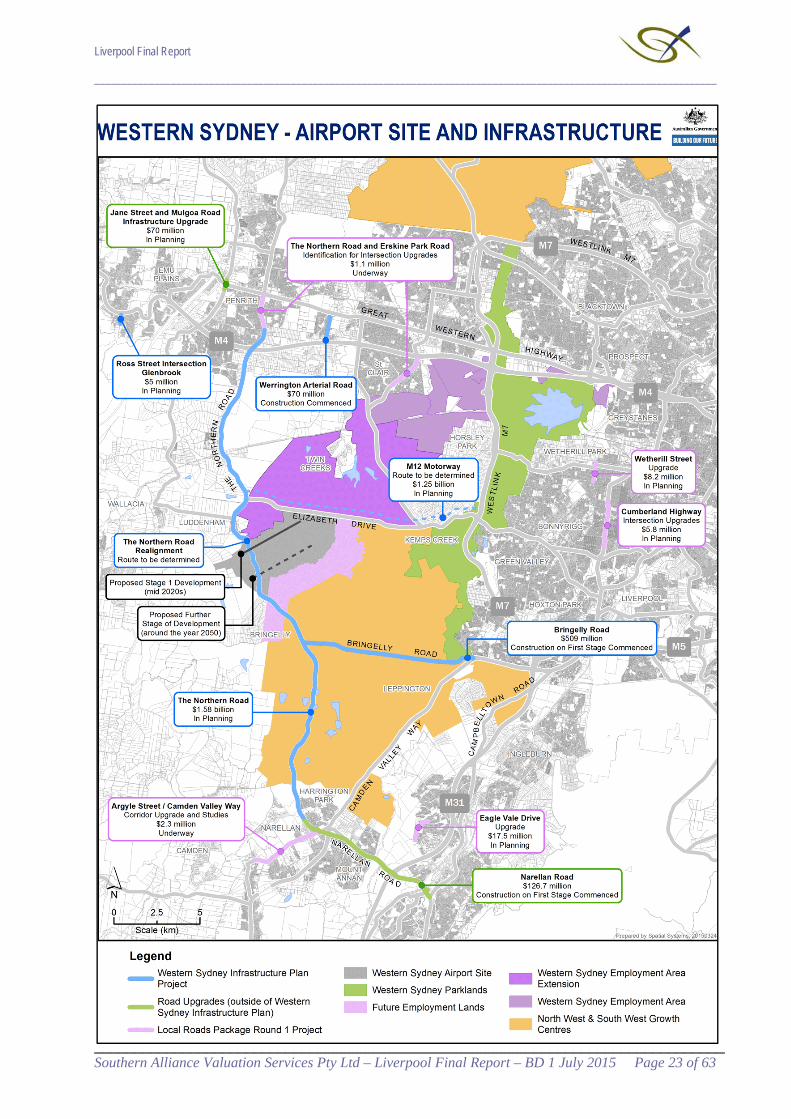

Note: A picture on the following page delineates the Wester Sydney (Badgerys Creek) Airport site and the commenced / proposed infrastructure upgrades to the surrounding area. Source: Information sourced from http://westernsydneyairport.gov.au/about.aspx

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 23 of 63

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 24 of 63

4.0 IDENTIFIED SIGNIFICANT CHANGES IN USE OR DEVELOPMENTS OF PROPERTY AND OTHER FACTORS WHICH MAY AFFECT VALUATIONS (Cont.)

4.5 Property Market Overview Australia’s residential property market exhibited mixed levels of growth over the 2014/15 financial year. The CoreLogic RP Data Home Value Index illustrates the combined capital city index rose 9.8% over the 12 months ending 30 June 2015. According to the index, Sydney residential properties showed an increase of 16.2% over the 12 months ending 30 June 2015 with Melbourne being the closest capital city to Sydney in terms of growth recording 10.2% over the same period. It is evident that the Sydney and Melbourne property markets have continued to increase in value at a faster pace than other Australian capital cities over the 2014/15 financial year. Some pockets of Sydney and noticeably some components of the Liverpool LGA had recorded stronger growth than others, however as a whole the Liverpool LGA moved homogenously showing considerable growth. The continued growth in the Sydney and Melbourne property markets and the imbalance between owner-occupied finance vs. investor finance has drawn the attention of regulatory bodies including the Australian Prudential Regulation Authority (APRA). APRA highlighted in December 2014 that authorised deposit-taking institutes (ADIs) must not exceed growth in investor loans above 10% per annum. Furthermore, in July 2015 APRA announced an increase in capital requirements for Australian residential mortgage exposures under the internal ratings-based (IRB) approach which would see the average risk weight of residential mortgage exposures using the IRB approach increase to at least 25% by mid-2016, from an average of around 17% at the end of June 2015. All big four banks (ANZ, NAB, Westpac & Commonwealth) increased the variable interest rates on residential investor loans between 0.27 and 0.29 percentage points over the two weeks ending 4 August 2015. Westpac notes the increases are a response following the introduction of investor lending growth benchmarks set by APRA. Furthermore, from 14 October 2015 to 23 October 2015, all big four banks increased their variable interest rates on residential owner-occupier and investor home loans between 15 and 20 basis points – with all four banks citing the decision was partly attributable to the requirement to increase the amount of capital applied to residential mortgages.

SQM Research has reported a notable increase in Sydney residential property listings over the year ending September 2015, whilst the national listing numbers declined over the same period. SQM noted Sydney residential listing numbers rose 7.6% over the month of September 2015 and rose 11.1% over the 12 months ending 30 September 2015 compared to the national residential listing numbers decreasing 0.1% over the 12 months ending 30 September 2015. Furthermore, Australian Property Monitors (APM) research indicates Sydney’s residential auction clearance rates last peaked at 89% in May / June 2015 which have since steadily declined to a clearance rate of 65% on Saturday 17 October. Expanding on the above, the information suggest that some of the heat of the Sydney residential property market – which was exhibited in the first half of 2015 – may have dissipated in recent months. However, as at date of report, there is no available information to suggest that in recent months the above has had any direct impact on residential property values.

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 25 of 63

4.0 IDENTIFIED SIGNIFICANT CHANGES IN USE OR DEVELOPMENTS OF PROPERTY AND OTHER FACTORS WHICH MAY AFFECT VALUATIONS (Cont.) Overall, retail property has benefited from an uplift in family net worth, driven by the increases in residential dwelling values, which help support discretionary spending and spending on consumer / household goods. Density / development sites continued to perform well over the 2014/15 financial year. Generally, residential development continues to outprice commercial development as the highest and best use and as such, sites with residential development potential remain in high demand across the Sydney Metropolitan Area. Industrial property across the Liverpool LGA was fairly subdued over the 2015 financial year. Industrial properties in the Liverpool LGA largely recorded mixed levels of growth, with (in-general terms) industrial sites situated to the ‘East of Liverpool CBD’ performing better than those sites situated to the ‘West of Liverpool CBD’. Individual pockets can move against the trend for varying reasons, however on the whole properties within the Liverpool LGA were relatively consistent. 4.6 Economy Overview

The following statement was issued by the Reserve Bank of Australia for the monetary policy decision held 7 July 2015 and provides a concise summary on the outlook for national and global economies as at the 2015 base date:- International Economic Conditions:

The Board's discussion about economic conditions opened with the observation that economic growth in Australia's major trading partners appeared to have been around average in the June quarter. Consumption growth had been little changed for most trading partners in recent months, although it was perhaps a bit stronger in the United States and somewhat weaker in China. The level of consumption in Japan remained well below that seen prior to the increase in the consumption tax in 2014. Core inflation rates had been stable in year-ended terms over recent months and remained below the targets of most central banks. Members also observed that trade volumes, particularly within the Asian region, appeared to have fallen recently. Consistent with this observation, growth in industrial production across a number of east Asian economies had slowed a little.

In China, there had been little change in the monthly indicators of economic activity, although conditions had been a bit more positive in some sectors than early in 2015. The Chinese property market had improved somewhat; residential property prices overall had risen for the first time in a year and floor space sold had increased in the past few months. Members reflected that the recent easing in monetary conditions would provide additional support to the property market and growth more broadly, although it could be some time before a significant pick-up in construction activity began. Recent efforts by central government authorities to increase infrastructure investment further and reform local government financing arrangements were also expected to support investment.

Commodity prices overall had fallen since the previous meeting, driven by iron ore and oil prices. Growth in crude steel production had been modest and steel prices had fallen noticeably over the past month. Iron ore production in China had continued to decline. Shipments of iron ore from Australia and Brazil appeared to have increased in June, which contributed to lower iron ore prices over the past month.

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 26 of 63

4.0 IDENTIFIED SIGNIFICANT CHANGES IN USE OR DEVELOPMENTS OF PROPERTY AND OTHER FACTORS WHICH MAY AFFECT VALUATIONS (Cont.)

Following quite strong output growth in Japan in the March quarter, more timely indicators pointed to modest growth in the June quarter. Labour market conditions had continued to improve, resulting in the unemployment rate falling further and the ratio of jobs to applicants continuing to rise. Wage growth and financial market measures of inflation expectations were higher than a year earlier and were expected to feed into higher core inflation over time. Members considered the importance for Japan of policy reforms designed to address some longer-term structural challenges, such as the ageing of the population.

In the United States, recent data pointed to moderate growth in economic activity in the June quarter following weakness in the March quarter. The labour market had strengthened further, with growth in non-farm payrolls employment rebounding in April and May and the unemployment rate falling. While there had been some increase in measures of wage growth, core measures of inflation remained below the Federal Reserve's inflation target.

In the euro area, the available indicators pointed to modest economic growth and above-average sentiment in the June quarter, continuing the recent trend of improved conditions in the euro area as a whole. Members noted that exports had made a significant contribution to the pick-up in growth in the region but investment was still well below the levels seen prior to the global financial crisis. The unemployment rate had continued to fall modestly since its peak two years earlier, but varied sharply across the euro area; the unemployment rate was highest in Greece, where output was more than 25 per cent below its level prior to the financial crisis.

Domestic Economic Conditions:

Members noted that output had increased by 0.9 per cent in the March quarter and by 2.3 per cent over the year. Resource exports had made a significant contribution to growth, reflecting better-than-usual weather conditions in the quarter. Dwelling investment had remained strong and while consumption growth had picked up over the past year or so, it had remained below average. Business investment had contracted in the quarter and there had been little growth in public demand. More recent economic indicators suggested that domestic demand had continued to grow at a below-average pace over recent months, but that labour market conditions had continued to improve.

Members observed that consumption grew faster than household income over the year to the March quarter. As a result, the saving ratio had declined further, although it remained well above the level it had been over much of the past 25 years. Year-ended growth in retail sales had been little changed over recent months and liaison suggested that this was likely to have continued into June. Retail sales growth had been relatively strong in New South Wales and Victoria but weaker in Queensland and Western Australia, in line with observed differences in economic conditions across the country. At the same time, surveys indicated that consumers had viewed their financial situation as being above average over the past year, notwithstanding the relatively weak growth in labour incomes. Members observed that this was likely to reflect the very low level of interest rates and strong growth in net household wealth.

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 27 of 63

4.0 IDENTIFIED SIGNIFICANT CHANGES IN USE OR DEVELOPMENTS OF PROPERTY AND OTHER FACTORS WHICH MAY AFFECT VALUATIONS (Cont.)

Dwelling investment increased by 9 per cent over the year to the March quarter. An increase in the construction of new dwellings accounted for most of this growth, but the alterations and additions component had also contributed more recently, recording the first increase in a year in the March quarter. Forward-looking indicators pointed to further strong growth in dwelling investment in the period ahead. Members noted that there had been ongoing divergence in conditions in established housing markets across the country, as well as between houses and apartments. Housing prices had continued to rise rapidly in Sydney and to a lesser extent in Melbourne. Elsewhere, there had been little change in housing prices over the past six months or so. Prices of apartments had been growing less rapidly than those of houses, which members considered to be consistent with the relatively strong growth in the supply of higher-density housing in many capital cities.

Growth in housing credit overall had been stable over recent months at around 7 per cent on an annualised basis, while growth in lending to investors had been steady at a bit above 10 per cent. Members observed that the household debt-to-income ratio, calculated by netting funds held in mortgage offset accounts from total household debt to the financial sector, had increased over the year to March but had not exceeded previous peaks. Members discussed the fact that high housing prices had different implications for existing home owners, who benefited from increased wealth, and potential new home owners, who were finding it more difficult to finance a home purchase.

Investment in both the mining and non-mining sectors appeared to have fallen in the March quarter, although the split between the two components remained subject to some uncertainty. Profits for non-mining firms had increased by 6 per cent over the past year. More recent survey measures of business conditions, confidence and capacity utilisation had picked up to be around, or even above, their long-run averages. In contrast, private non-residential building approvals had remained weak.

The monthly trade data suggested that resource exports, including iron ore and coal, had declined in the June quarter. Coal exports had been affected by the severe storms in the Hunter region of New South Wales in late April. Members noted that there had been further signs of growth in service exports, in part a response to the depreciation of the exchange rate. Over the past year, net service exports had made a similar contribution to output growth as exports of iron ore, even though total import volumes had increased in the March quarter.

Labour force data indicated further signs of improvement in May. Employment growth had picked up over the year to exceed the rate of population growth. As a result, the unemployment rate had been relatively stable since the latter part of 2014 and had fallen slightly in May to 6 per cent. Members observed that employment growth had been strongest in household services and that employment and vacancies had been growing for business services but had remained little changed in the goods sector. As with other state-based indicators, employment growth and job vacancies had been strongest in New South Wales and Victoria. Forward-looking labour market indicators had been somewhat mixed over recent months. The ABS measure of firms' job vacancies overall suggested that demand for labour could be sufficient to maintain a stable or even falling unemployment rate in the near term, while other forward-looking indicators suggested only modest growth in employment in coming months.

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 28 of 63

4.0 IDENTIFIED SIGNIFICANT CHANGES IN USE OR DEVELOPMENTS OF PROPERTY AND OTHER FACTORS WHICH MAY AFFECT VALUATIONS (Cont.)

Members noted that the latest estimates indicated that the population had increased by 1.4 per cent over the year to the December quarter, down from a peak rate of growth of 1.8 per cent over 2012. The slower growth was primarily accounted for by a decline in net immigration, which was particularly pronounced in Western Australia and Queensland, consistent with weaker economic conditions in those states. Members observed that the lower-than-expected growth in the population helped to reconcile the below-average growth in output over the past year with a broadly steady unemployment rate.

Despite recent improvements in labour market indicators, members reflected that there was still evidence of spare capacity in the labour market. Consistent with this, the latest national accounts data indicated that non-farm average earnings per hour had recorded the lowest year-ended outcomes since the early 1990s and that unit labour costs had been little changed for around four years.

Financial Markets:

International financial markets were mainly focused on developments in Greece and the fall in Chinese equity markets over the past month.

Members were briefed on recent developments in Greece. The ‘no’ vote in the referendum on the creditors' latest proposals raised several issues, first among which was how the Greek authorities could reopen the banks. A critical vulnerability in the near term was related to whether the European Central Bank would provide additional emergency liquidity assistance. A second issue was how Greece would be able to service its external debt and a third was the challenges faced by the Greek authorities in improving the competitive position of the economy. Although these issues were of great concern to the Greek populace, the direct economic implications for the global economy and Australia were assessed by members to be relatively limited. They noted that the reaction of financial markets to these developments had been fairly muted. This was consistent with the economic and financial exposures to Greece – apart from the official sector's financial exposure – being quite low.

Members noted that spreads to 10-year German Bunds on comparable bonds issued by Italy, Spain and Portugal had not risen much, with the limited contagion from developments in Greece likely to have reflected a general view of markets that previous adjustment policies in those countries had been relatively successful.

Members then turned their discussion to developments in bond markets more generally. Yields on longer-maturity German Bunds and US Treasuries had risen sharply over the first half of June, with German 10-year yields reaching 1 per cent, compared with a historic low of 8 basis points in mid April. German yields declined somewhat following the announcement of the Greek referendum. Longer-term sovereign yields of most other developed countries, including Australia, tended to move in line with US Treasuries. Expectations about the timing of the US Federal Reserve's first increase in the federal funds rate were little changed over the past month. Market pricing continued to suggest that the first increase would occur around the end of 2015. Although commentary by Federal Reserve officials suggested that it could be a little sooner than that, they continued to emphasise that the exact timing of the first increase would be less important than the pace of subsequent increases, which were expected to be gradual.

Liverpool Final Report

__________________________________________________________________________________________________________________

_______________________________________________________________________________ Southern Alliance Valuation Services Pty Ltd – Liverpool Final Report – BD 1 July 2015 Page 29 of 63

4.0 IDENTIFIED SIGNIFICANT CHANGES IN USE OR DEVELOPMENTS OF PROPERTY AND OTHER FACTORS WHICH MAY AFFECT VALUATIONS (Cont.)