21st annual health sciences tax conference annual health sciences tax conference tax implications of...

TRANSCRIPT

21st Annual Health Sciences Tax Conference Tax implications of changing business models in life sciences 7 December 2011

Page 2 Tax implications of changing business models in life sciences

Disclaimer

Any US tax advice contained herein was not intended or written to be used, and cannot be used, for the purpose of avoiding penalties that may be imposed under the Internal Revenue Code or applicable state or local tax law provisions.

Page 3 Tax implications of changing business models in life sciences

Disclaimer

Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young LLP is a client serving member of EYGM in the US. For more information about our organization, please visit www.ey.com. This presentation is © 2011 Ernst & Young LLP. All rights reserved. No part of this document may be reproduced, transmitted or otherwise distributed in any form or by any means, electronic or mechanical, including by photocopying, facsimile transmission, recording, rekeying, or using any information storage and retrieval system, without written permission from Ernst & Young LLP. Any reproduction, transmission or distribution of this form or any of the material herein is prohibited and is in violation of US and international law. Ernst & Young LLP expressly disclaims any liability in connection with use of this presentation or its contents by any third party. Views expressed in this presentation are not necessarily those of Ernst & Young LLP.

Page 4 Tax implications of changing business models in life sciences

Presenters

Jeff Holtz Tax Director – Global Supply Chain Medical Devices and Diagnostics Global Services, LLC Johnson & Johnson Stijn Ehren Senior Director International Tax & Counsel Merck & Co

Karen Holden Ernst & Young LLP Philadelphia Cedric Bernardeau Ernst & Young LLP New York

Page 5 Tax implications of changing business models in life sciences

Changing business models – revisiting the value chain

► The pharmaceutical industry is currently facing unprecedented changes due to the impending blockbuster “patent cliff” of drugs with upcoming patent expirations, a decline in R&D productivity coupled with an increase in R&D costs, and pricing pressure.

► These pressures are refocusing companies on increasing R&D productivity and streamlining those costs in the value chain, including sales, marketing, R&D and manufacturing costs.

► The result is an industry in which specialty and niche pharmaceuticals (as opposed to large-volume blockbusters) are highly prized for their reimbursement potential. ► Functional activities such as marketing are streamlined and functions are

outsourced, although the ability to manage the substantial risks is retained.

► The exponential increase in M&A activity is a result of pharmaceutical companies’ continual assessment of their future business model(s).

Page 6 Tax implications of changing business models in life sciences

Agenda

► Changing R&D landscape ► Reliance on acquisitions and alliances ► Enhancing effectiveness and efficiency of R&D ► Impact on IP alignment

► From supply chain to value chain ► Change in manufacturing footprint ► Service principals ► Compensating value and risk

► Emerging markets

Page 7 Tax implications of changing business models in life sciences

Changing R&D landscape

► Reliance on acquisitions and alliances ► M&A activity ► Joint ventures

► Enhancing efficiency and effectiveness of R&D activity ► Increase in use of third-party service providers (contract research

organizations (CROs) and beyond) ► The US CRO market is forecast to almost double to $20b by 2017. ► An increasing number of drug makers are outsourcing trials to CROs

to keep costs and prices under control. ► Start-up and biotech companies are increasingly using CROs to take

pipeline beyond Phase I/II rather than out-license. ► Entrepreneurial R&D and other R&D models

► Impact on intellectual property (IP) alignment

Page 8 Tax implications of changing business models in life sciences

Acquisitions and alliances

► Reliance on acquisitions and alliances ► Does transaction create a comparable transaction?

► Acquisition of IP only ► Co-promotes and licenses

► Influence the terms of the deal to reflect economics

► Impact on deal structure ► Make transaction as tax-efficient as possible

► Keep deal data to create comparable ► Possibility of structuring post-acquisition IP ownership

► What is best structure when manufacturing is not being acquired? ► Work with third party on the supply chain structuring

Page 9 Tax implications of changing business models in life sciences

Increased use of third parties in R&D

► R&D service providers in the industry ► Information research and data analytics ► Medical communication and education ► Non-human testing ► CROs

► Funding the provider ► Ability to move ownership of IP by changing funding ► Supports compensating internal functions as service provider vs.

IP owner ► Structuring the relationship

Page 10 Tax implications of changing business models in life sciences

IP alignment in a changing business model

► Alignment of IP ownership in a changing business model ► Geographic alignment

► Market appropriate products ► Emerging market strategy

► Questions ► What is the IP? ► Who owns it today? ► Where should it be owned in the future?

► Alignment with business objectives ► Patent box regimes

Page 11 Tax implications of changing business models in life sciences

Ownership and nature of IP

► Understand relationship between transacting parties ► Identify role of value drivers and related intangibles ► Goodwill, going concern, workforce-in-place

► Value-adding synergies related to business activity that do not attach to any particular asset

► Common legal characteristics of an intangible asset: ► Specific identification and recognizable description ► Subject to legal existence and protection ► Subject to right of private ownership, and private ownership should be legally

transferable ► Tangible evidence of existence, e.g., contract or license ► Created or comes into existence at an identifiable time or as a result of

identifiable event ► Subject to being destroyed, existence terminated at an identifiable time or as

result of identifiable event

Page 12 Tax implications of changing business models in life sciences

Ownership and nature of IP

► Common tax categories of intangible assets (see IRC Sec. 936(h)(3)(B)(i)-(v))*: ► Marketing – trade name, trademark, brand name ► Technical – patent, invention, formula, process, design, pattern,

know-how, technical data ► Artistic – copyright, literary, musical, artistic composition ► Systems/processes – method, program, campaign, survey,

system, study, procedure, forecast, estimate ► Engineering applications – patent, invention, formula, process,

design, pattern, know-how, technical data ► Customer-related – customer list ► Contract-related – franchise, license, contract

*IRC Sec. 936(h)(3)(B)(v) includes any similar item that has substantial value independent of the services of an individual.

Page 13 Tax implications of changing business models in life sciences

Industry considerations

► IP – API, drug formulation, product design, manufacturing know-how, brand and other marketing intangibles ► IP often centralized – R&D talent, infrastructure, relationships, molecule library

typically in one location ► Contract content development – fee-based or profit split?

► IP migration ► Wide spectrum of options – franchising/full exploitation, local content

acquisition/licensing, co-development/financing; lots of third-party activity ► Product lifecycles/categories, “core” contributions, marketing IP and risk profile of

alternatives (cost sharing vs. other)

► Buy-in vs. licensing or co-development ► Buy-in – uncertainty around buy-in payments and administrative burdens ► Licensing has long history, is well understood, and likely to produce more modest

benefits (with muted downside risk vs. cost sharing) ► Co-development arrangements using profit splits must be distinguished from cost

sharing, but offer some attractive features

Page 14 Tax implications of changing business models in life sciences

Where to locate IP rights? Attributes and incentives

► Location assessment ► Alignment with commercial operations

► Alignment with existing or future supply chain

► IP protection ► Maximization of R&D and other tax incentives, including:

► Patent box planning ► R&D credit or investment deduction ► IP amortization ► Treaty network and withholding taxes ► Principal-type rulings ► Grants and subsidies ► Wage withholding tax exemptions for researchers ► Specific tax regime for expatriates

Page 15 Tax implications of changing business models in life sciences

Where to locate IP rights? Patent box regimes ► Multiple European countries offer patent boxes in various

forms, including: ► Belgium ► France ► Hungary ► Ireland ► Luxembourg ► Netherlands ► Spain ► Switzerland ► UK (still in consultation phase but expected to apply from

1 April 2013)

Page 16 Tax implications of changing business models in life sciences

From supply chain to value chain

Page 17 Tax implications of changing business models in life sciences

From supply chain to value chain

► Value chain vs. supply chain ► New product types ► Change in manufacturing footprint

► Increased use of CMOs ► Impact on substantial contribution

► Valuing risk ► Proliferation of service principals

► Change in business delivery ► Regional and pricing pressures ► Emerging markets

Page 18 Tax implications of changing business models in life sciences

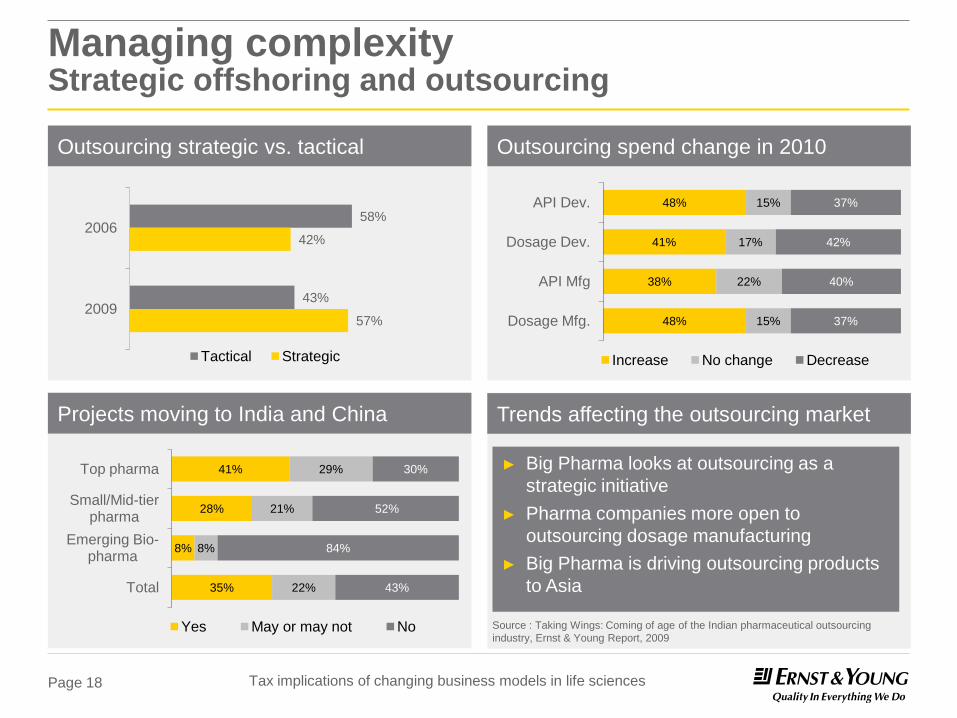

Managing complexity Strategic offshoring and outsourcing

Outsourcing spend change in 2010 Outsourcing strategic vs. tactical

Projects moving to India and China Trends affecting the outsourcing market

58%

43%

42%

57%

2006

2009

Tactical Strategic

48%

41%

38%

48%

15%

17%

22%

15%

37%

42%

40%

37%

API Dev.

Dosage Dev.

API Mfg

Dosage Mfg.

Increase No change Decrease

41%

28%

8%

35%

29%

21%

8%

22%

30%

52%

84%

43%

Top pharma

Small/Mid-tier pharma

Emerging Bio-pharma

Total

Yes May or may not No Source : Taking Wings: Coming of age of the Indian pharmaceutical outsourcing industry, Ernst & Young Report, 2009

► Big Pharma looks at outsourcing as a strategic initiative

► Pharma companies more open to outsourcing dosage manufacturing

► Big Pharma is driving outsourcing products to Asia

Page 19 Tax implications of changing business models in life sciences

Change in manufacturing footprint

► Change in manufacturing footprint ► New products

► By 2016, bioengineered vaccines and biologics will account for 23% of the global market (by volume), up from 17% in 2007. ► This will stress existing supply chains, which are not designed to handle

these types of products.

► Move from internal manufacturing to CMO ► Managing CMOs vs. internal manufacturing – difference in functions? ► Does this change the “principal as manufacturer” designation?

► Valuing risk ► Post-launch/commercialization risk ► R&D funding and execution ► Manufacturing quality

► Effect on substantial contribution

Page 20 Tax implications of changing business models in life sciences

Substantial contribution and CMs

► Oversight of manufacturing processes ► S&OP process ► Formulate policy for CMOs

Indicia of manufacturing Potential activities carried out by principal

Activities that are considered in, but are insufficient to satisfy, the substantial transformation

Material selection, vendor selection or control of raw materials, work-in-process or finished goods

Management manufacturing costs or capacities

Control of manufacturing-related logistics

Quality control

Developing, or directing the use or development of product design and design specifications, as well as trade secrets, technology or other intellectual property for the purpose of manufacturing or producing the product

Oversight and direction of the activities or process under which the product is manufactured

► Qualify, select and manage CMOs ► Ownership of inventory ► Manage supplier risk (capacity, obsolescence) ► Determine supplier capacity and continuity

► Identify and manage cost improvement initiatives ► Cost reduction (e.g., inventory reduction, price reduction)

► Direct the planning and production schedules for external partners ► Monitor production orders, schedules and output to ensure products

are manufactured and scheduled delivery dates are met.

1

2

3

4

5

6

7

► Evaluate supplier quality systems and share best practices ► Negotiate quality agreements ► Ultimate quality responsibility

► IP ownership ► Develop technology transfer process for new product introductions ► Transition design or process changes to external partners ► Partner with suppliers on supply chain development initiatives

► Finish and fill ► Sterilization

Page 21 Tax implications of changing business models in life sciences

Service principals

► Driven by a number of factors and trends, including: ► After-market repair and service vs. buy

► Medical devices ► Customer demand for global or regional contracting

► Procurement functions, contract R&D ► Changes in the way companies do business and deliver

► Make vs. buy decisions ► Centers of excellence and cost reduction initiatives

► Research centers, educational hubs, health outcomes analysis ► Migration and expansion to emerging markets ► Use of low-cost service providers/offshoring

Page 22 Tax implications of changing business models in life sciences

Services vs. products in pharma 3.0

► Human interaction may be face-to-face, remote or non-existent.

► “Boots on the ground,” “remote delivery,” “smart servers” ► Contracting models impact deferral alternatives. ► Value drivers:

► Technology vs. marketing intangibles ► Hardware/software (patents, copyrights, know-how) ► Brand/relationships (trademarks, KOLs, customer/patient lists)

► People versus assets ► R&D vs. sales and marketing ► Consultants vs. servers and other IT equipment

Page 23 Tax implications of changing business models in life sciences

Areas of tax controversy in services

► Withholding tax ► Character of revenue stream (royalty, services, sales) ► Emerging markets

► US Subpart F ► Location of the performance of services ► Substantial assistance and Notice 2007-13

► Indirect tax ► Minimizing irrecoverable VAT ► Mobile work force

► Transfer pricing ► Characterization and pricing of revenue stream ► IP creation and migration

Page 24 Tax implications of changing business models in life sciences

Emerging markets

Page 25 Tax implications of changing business models in life sciences

Emerging markets

► Life sciences companies are looking outside the US and Europe for market drivers and growth opportunities. ► IMS Health predicts that combined shares

of prescription spending in the US and Europe will shrink from 61% in 2005 to 44% in 2015.

► By 2020, revenues in emerging markets are expected to reach $487 billion (37% of total global sales).

► Specifically, IMS Health has coined 16 developing nations as “pharmerging”: ► China, Brazil, India, Russia, Turkey,

Poland, Venezuela, Argentina, Indonesia, South Africa, Thailand, Romania, Egypt, Ukraine, Pakistan and Vietnam

Pharmerging markets 5-year growth expectations 2008–2013

2008 2013(f)

7

10-20

15-25

15-25

15-25

12-22

22-32

65-75

10 10

11

11

19

19

160

140

120

100

80

60

40

20

0

$90B

$155–$185B

Russia* 14%–17%

CAGR 2008–2013: ~13-16%

South Korea 7%–10%

India 11%–14%

Turkey 11%–14%

Mexico 4%–7%

Brazil 7%–10%

China 20%–33%

Source: IMS Health, Market Prognosis, March 2009; Russia’s 2013 estimate based on September 2008 forecast

180

Page 26 Tax implications of changing business models in life sciences

Tax issues on entering emerging markets

► Market penetration strategy may create unfavorable precedents for transfer pricing ► Established products

► Partnering with local companies ► Pricing

Page 27 Tax implications of changing business models in life sciences

Tax efficient supply chain management (TESCM) structure issues in emerging markets

► Value-added tax (VAT) and indirect taxes ► Overseas company cannot register as a general VAT taxpayer ► Overseas company does not have tax attributes to hold inventory

locally ► Customs duties

► Potential duties on re-import of finished goods, if applicable ► Transfer pricing

► Statutory profit mark-up margins, irrespective of industry ► Does not follow Organisation for Economic Co-Development

(OECD) guidelines or different interpretation

Page 28 Tax implications of changing business models in life sciences

TESCM structure issues in emerging markets

► Permanent establishment (PE) ► PE concept not well-defined

► Withholding tax on certain cross-border payments ► Legal and regulatory consideration and foreign exchange

► Obtaining or amending the business scope ► Obtaining specific authorization for certain industries ► Exchange control restrictions on goods sold to non-residents but

not physically exported ► Cap on royalty payments

Page 29 Tax implications of changing business models in life sciences

Traditional transactional TESCM model

Sale of finished goods (resale minus)

Customers

Deliver finished

goods

Limited risk sales company

Sale of finished goods (market price)

Sale of materials

Sale of finished goods (cost +) or conversion fee (cost+)

Deliver materials

Sale of finished goods (market price)

Contractor toll

manufacturing

Principal trading company

(residual profits)

Suppliers

Typical tax considerations: ► CFC ► Withholding taxes ► Permanent establishment ► Transfer pricing ► Conversion and exit taxes ► Availability of double tax agreements ► Indirect taxes such as VAT, GST ► Duty relief ► Free trade agreement availability ► Customs valuation ► Importer and exporter of record ► Substance ► Non-tariff and other regulations (e.g., licences) ► Accounting, information technology and systems ► Currency remittance and exchange controls ► Legal structure ► Principal location ► Minority interest and joint ventures

Taxpayers are having to consider alternative transactional models to ensure that the operational reality is reflected in the transactional and tax model.

Page 30 Tax implications of changing business models in life sciences

Physical Flow

Alternative transactional models Local principal model

Local central company

Local country

Principal

Principal location

Local/Foreign Suppliers

Contract manufacturer

Raw materials

Limited risk distributor

Customers

Finished goods

Finished goods

Legal ownership

Legend:

Finished goods

Characterization of the fee? ► Royalty ► Service fee ► Franchise fee ► Inventory factoring fee

Considerations: ► Substance of the fee ► Transfer pricing ► Withholding tax ► Indirect taxes ► Deductibility of service fee ► Conversion

Use of a local principal entity? ► Is a local principal entity required or can

the fee be paid out of the manufacturer or distributor?

How is this characterized?

Fee

Page 31 Tax implications of changing business models in life sciences

Alternative transactional models China hybrid model

Local central company

China

Principal

Singapore

Local/Foreign Suppliers

Contract manufacturer

Raw materials

Limited risk distributor

Customers

Domestic Import and

domestic

Export – processing trade arrangement for finished goods

Use of a local principal entity? ► For local China sales, the China sub-principal

outsources manufacturing to the contract manufacturers and sells to the local distributors or directly to third-party customers.

► All export sales from China will be made directly from the contract manufacturer to the overseas principal; all of the manufacturers will be contract manufacturers for the principal for export sales.

► The China sub-principal will pay value-based service fees on the local sales portion to the principal.

Discussion points ► Characterization and deductibility of the fee?

► Royalty

► Service fee

► Other

► Indirect tax implications

► Conversion

Limited risk distributor

Imports

Value-based fee for domestic

Page 32 Tax implications of changing business models in life sciences

Procurement company How value is created in a central procurement organization

Suppliers Suppliers Suppliers

Framework agreement

Select and negotiate

Procurement support

services

Service fee

Commission

Physical product, invoice

Buy/call-off, payment

Service provider model

Suppliers Suppliers Suppliers

Invoice

Contract/payment

Procurement support

services

Service fee

Order/ payment

Physical product

Call-off

Sell/ invoice

Buy-sell model

Service provider

Shared service center

Local OpCo

Buy-sell

Shared service center

Local OpCo

Transfer price commission model Commission = X% of supplier price

Subject to demonstrable savings Applied and reviewed periodically on managed OpCo expenditure

Transfer price buy-sell model Price to OpCo = supplier price + margin

Subject to demonstrable savings Applied on a transactional basis and reviewed periodically

Higher functions risk =

Higher remuneration

SLA SLA

Page 33 Tax implications of changing business models in life sciences

US parent company tax issues

► Dealing with the Subpart F substantial contribution and branch rules

► Conversions on outbound transfer of intangibles ► Application of Section 909 and/or compulsory payment rules for

foreign tax credits in the case of audit adjustments ► Camp proposal – territorial taxation