2020 holiday sales forecast - icsc

TRANSCRIPT

2020 Holiday Sales Forecast

Holiday Intentions Survey 2020Despite the pandemic and economic downturn, we are forecasting an overall increase of 1.9% in holiday spending

+1.9% growth year-over-year

Expected Growth & Spend

Consumer Behaviors

$862.2B of total spending

73%Of all shoppers plan to spend more or about the same as in 2019

81% Will spend in a physical store 93%

Will embrace omnichannel and make purchases in a retailer’s physical store and their website

57%Plan to shop at discount department stores

43%Plan to make more purchases online due to COVID-19

$655 average spend on holiday-related items, which exceeds 2019 actual spend of $604 by 8%

ICSC Sales Forecast for Key Categories(Combined November and December)

Building Materials 7.5%

7.0%

4.4%

25%

$84.7 bil.

$143.8 bil.

$138.5 bil.

$190.3 bil.

Food & Beverage Stores

Sporting Goods, Hobby, Books & Music

Electronic Shopping & Mail Order

2020 Holiday Shopping Season Intentions

2020 Holiday Season Intentions Overview

94%

Plan to buy from omni-channel retailers

Top Shopping VenuesSpending Intentions by Generation

Discount Department Stores

57%1

Traditional Department Stores

34%2

Electronics Stores

31%3

Millennials

49%

Gen X

42%

Baby Boomers

20%

73%Will Spend the Same or More

Percent of Holiday Shoppers

Percent of Adults

Plan to participate inholiday shopping

94%

Will spend more

Will spend more

Will spend more

Consumer Shopping Channels

81%Will spend in a physical store

66%Will spend will with Amazon

49%Will spend online and

ship to home

53%Will spend

online and pick-up in a physical

store

Shoppers Buy Online and Pick Up In-Store

Shoppers picked up in store

2016-2019 Average

40%

Shoppers intend to pick-up in store

53%

2020 Intention

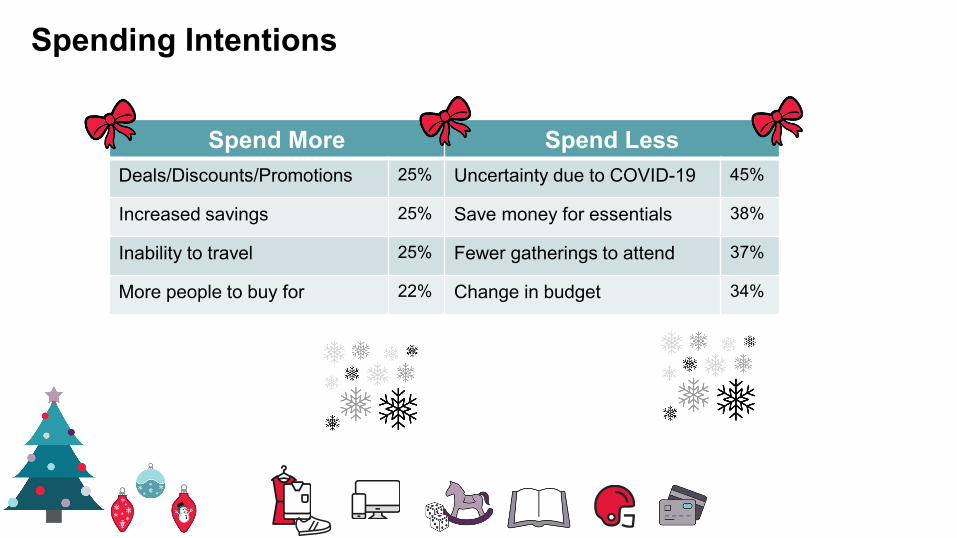

Spending Intentions

Spend More Spend LessDeals/Discounts/Promotions 25% Uncertainty due to COVID-19 45%

Increased savings 25% Save money for essentials 38%

Inability to travel 25% Fewer gatherings to attend 37%

More people to buy for 22% Change in budget 34%

Planned Shopping Start

12% 21%

9%

23%

24%

22%Thanksgiving weekend –

Cyber Monday

11%

Nov. 1 – Nov. 25

Holiday Shopping Timing

51%48%

47%46% 32%

Avoid crowds

Product Availability

Promotions

On-time delivery Health/Safety

Reasons

77% of holiday shoppers plan to start earlier than normal

The Impact of COVID-19

Consumer Behavior – Holiday Season

A surge in cases would negatively impact

holiday shopping plans

69%

More likely to visit stores with strict health protocols

66%

Promotions drive traffic to physical stores

49%

Shoppers will use click-and-collect more frequently this

holiday season

59%

74%

More patient and understanding of delivery delays

64%

Significantly scaled back plans this year

Plan to spend more with small businesses

due to COVID-19

54%

Discounts/Promotions result in additional

spending

65%

49%

Intend to be more charitable due to

pandemic

CO

NC

ERN

S

SHO

PPIN

G

GEN

ERAL

LY

PLAN

S

Coronavirus Consumer Survey

72%

Agree businesses should be open in

their state

72%

Will only shop in stores that have taken steps

to protect employees & customers

69%

Would support a lock down if cases in their

state surged

75%

Are concerned about a second major wave of

COVID-19 as fall approaches

53%

Dining indoors

52%

Shopping inside a mall

48%

Working out at a gym/ fitness center

30%

Believe the economy is better than it was 2

weeks ago

General Sentiment

Concern about COVID-19 still remains top of mind

In the next 2 weeks, people will do as much or more of the following

49%

Feel the economy will improve in the next 12 months

64%

Shopping inside a physical store for non-

essentials

66%

Feel prepared to handle a second major outbreak of COVID-19 in the fall

28%

Have no plans to cutback on spending, despite the pandemic

Questions?

Please type them in the Q&A pod

17