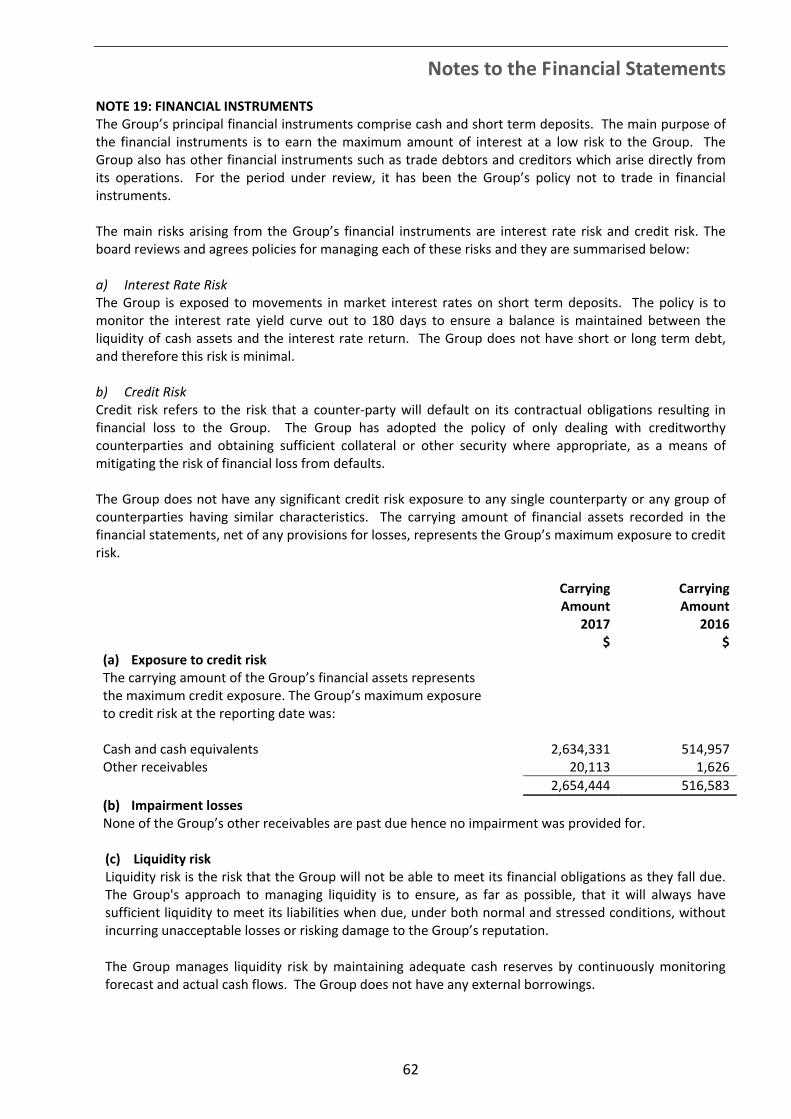

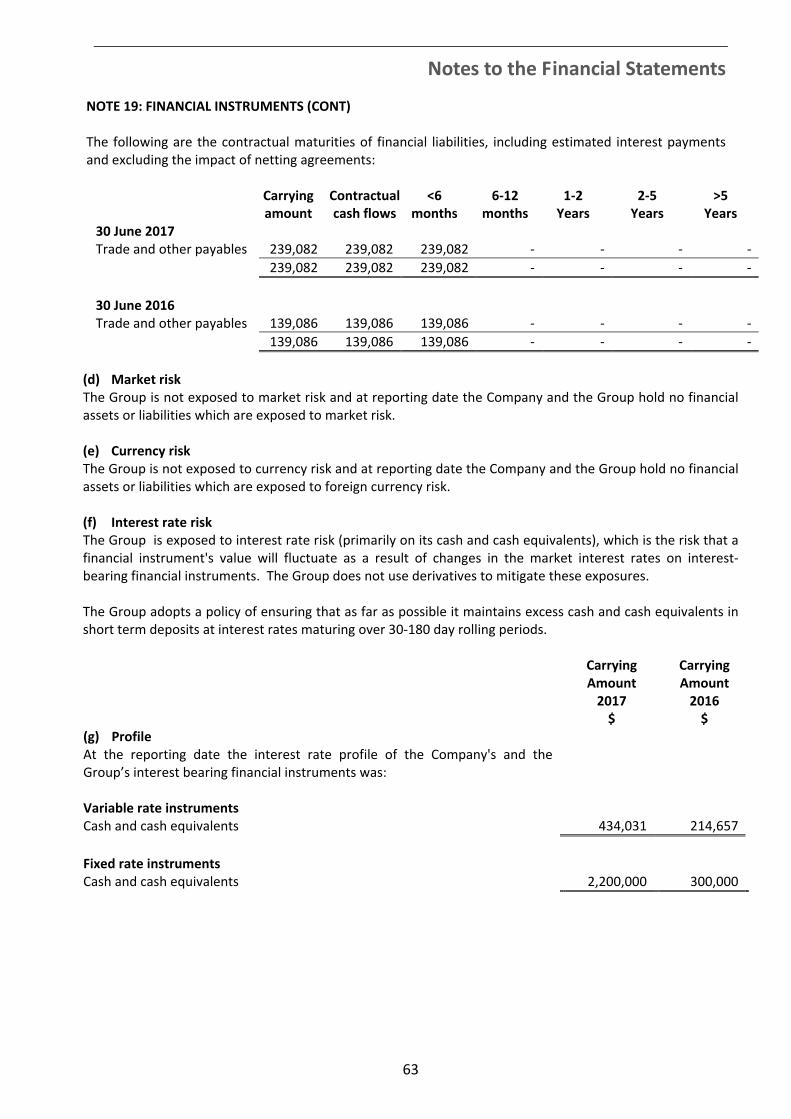

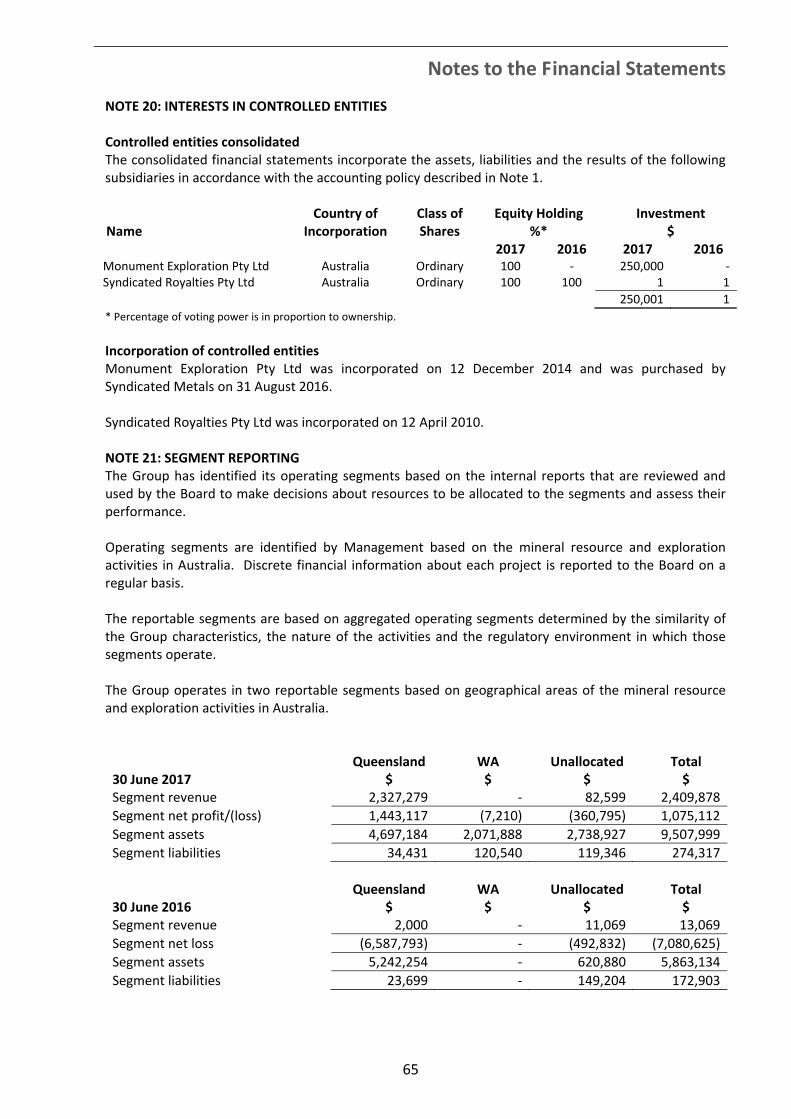

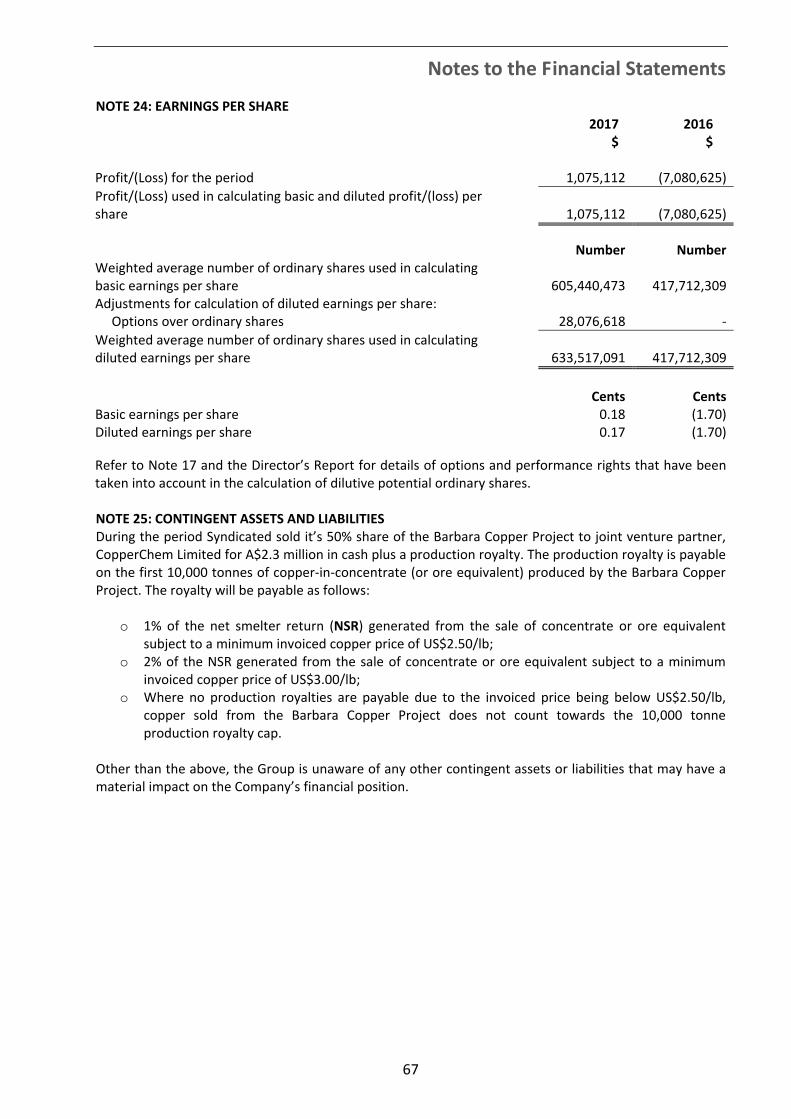

2017 annual report - syndicated metals · 2 chairman’s report dear shareholders, over the past 12...

TRANSCRIPT

2017 ANNUAL REPORT

ABN 61 115 768 986

CONTENTS

CORPORATE DIRECTORY ....................................................................................................................... 1

CHAIRMAN’S REPORT ........................................................................................................................... 2

DIRECTORS’ REPORT ............................................................................................................................. 3

AUDITOR’S INDEPENDENCE DECLARATION ......................................................................................... 33

CORPORATE GOVERNANCE STATEMENT ............................................................................................. 34

CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME ................. 35

CONSOLIDATED STATEMENT OF FINANCIAL POSITION ....................................................................... 36

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY ........................................................................ 37

CONSOLIDATED STATEMENT OF CASHFLOWS ..................................................................................... 38

NOTES TO THE FINANCIAL STATEMENTS ............................................................................................. 39

DIRECTORS’ DECLARATION ................................................................................................................. 70

INDEPENDENT AUDITOR’S REPORT ..................................................................................................... 71

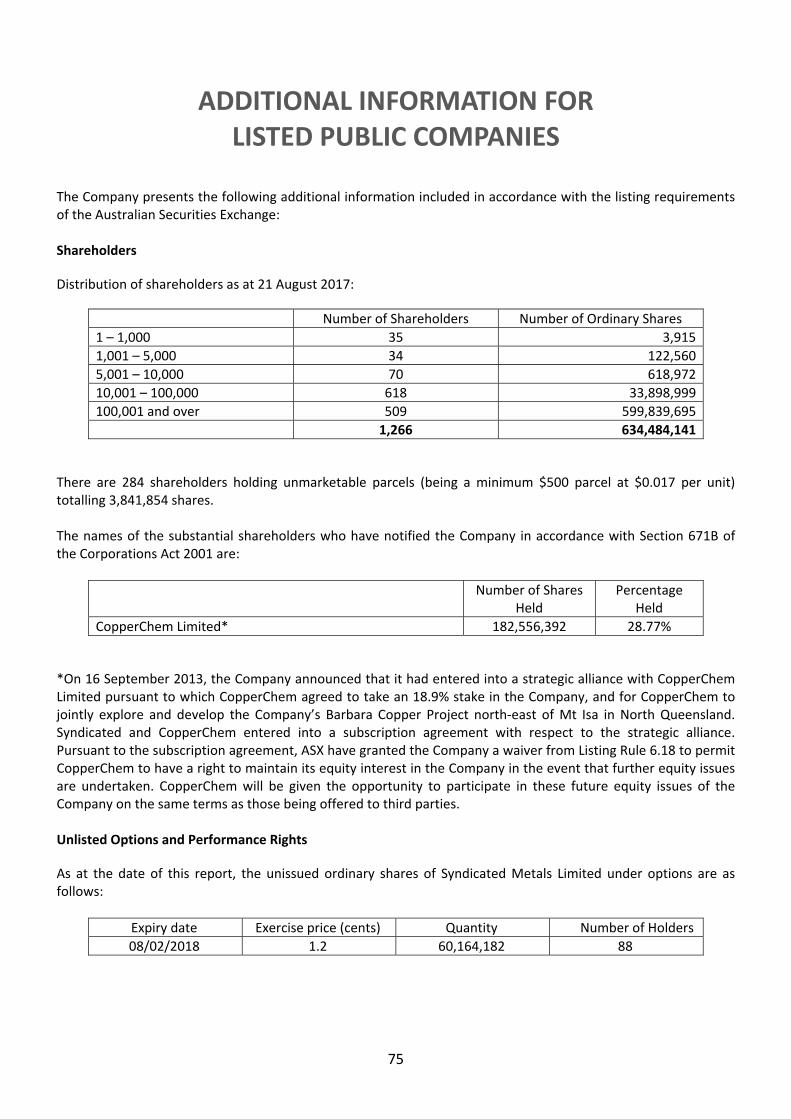

ADDITIONAL INFORMATION FOR LISTED PUBLIC COMPANIES ........................................................... 75

SCHEDULE OF INTERESTS IN MINING TENEMENTS .............................................................................. 78

1

CORPORATE DIRECTORY

DIRECTORS Peter Langworthy (Non‐executive Chairman) Andrew Munckton (Managing Director) David Morgan (Non‐executive Director) Robert Cooper (Non‐executive Director) REGISTERED OFFICE 68A Hay St Subiaco, WA 6008 Telephone: (08) 9380 9440 SOLICITORS Gilbert + Tobin Level 16, Brookfield Place Tower 2 123 St Georges Terrace Perth, WA 6000 AUDITORS PKF Mack Level 5, 35 Havelock Street West Perth, WA 6005 SHARE REGISTRY Computershare Investor Services Pty Limited Level 11, 172 St Georges Terrace Perth, WA 6000 Telephone: (08) 9323 2000 Facsimile: (08) 9323 2033 STOCK EXCHANGE LISTING Australian Securities Exchange (Home Exchange: Perth, Western Australia) Code: SMD BANK Westpac Banking Corporation 1257 Hay Street West Perth, WA 6005

2

CHAIRMAN’S REPORT

Dear Shareholders, Over the past 12 months, Syndicated Metals has shifted its focus to gold exploration within one of Australia’s premier gold districts with the acquisition of the highly prospective Monument Gold Project in Western Australia. The Monument Project is located in the world‐class Laverton district and lies directly along strike from the 3.3Moz Mt Morgans Gold Project, currently being developed by Dacian Gold Limited, and in close proximity to several other multi‐million ounce gold deposits. The project was acquired from private vendors for $250,000 cash and shares – a relatively low entry price for a project of its quality and location. Our exploration teams have been diligently working through the project and its historical data, while observing the progress being made by others in the district. We have confirmed the geological setting at the most advanced prospect, Korong, as being analogous to Dacian Gold’s 1.6Moz Westralia deposit at Mt Morgans, confirmed the source of historical geophysical anomalies at A1 North, and completed extensive regional soil sampling programs to generate additional drilling targets across the project. Our geological team now has a solid understanding of the styles of gold mineralisation present in the area and is now applying a systematic exploration philosophy to the assessment of the historical prospects and new areas of surface mineralisation. We intend to build on these solid foundations during the year ahead with the commencement of aircore drilling programs which we believe will assist us to vector into potential new discoveries. In order to significantly advance activities at the Monument Project, we have recently divested our 50% ownership of the Barbara Copper Project in Queensland to our joint venture partner at the project, CopperChem Limited. This transaction has provided us with sufficient funding to underpin ongoing quality, systematic exploration programs at the Monument Project. We are committed to our approach and we are confident that it will be rewarded with a breakthrough discovery over the next year. The Board and management team remain strongly motivated and committed to delivering quality, long‐term results to all our shareholders. In conclusion, I would like to take the opportunity once again to thank all our shareholders for their support, and look forward to delivering some exciting news over the coming year. Yours sincerely

Peter Langworthy Chairman

3

DIRECTORS’ REPORT

Your directors present the following report on Syndicated Metals Limited (the Company) and the entities it controlled (Group) during or at the end of the financial year ended 30 June 2017. INFORMATION ON DIRECTORS The directors of the company at any time during or since the end of the financial year are; Peter Langworthy Non‐Executive Chairman (Appointed 20 March 2012)

Mr Langworthy is a geologist with a career spanning more than 30 years in mineral exploration and project development in Australia and Indonesia. He has specific expertise in building successful teams that have been responsible for significant mineral discoveries and in integrating technically sound exploration and resource development strategies into corporate planning. His industry experience includes 12 years in senior management roles with WMC Resources, four years with PacMin Mining as Exploration Manager, five years with Jubilee Mines where he built the team responsible for numerous discoveries at the Cosmos Nickel Mine and the Sinclair Nickel Project, and three years with Talisman Mining as Technical Director. At Jubilee he was part of the corporate team responsible for the growth of the company until it was taken over by Xstrata. He has also held non‐executive directorships with other ASX‐listed companies namely Northern Star Resources, Falcon Minerals and Pioneer Resources. Mr Langworthy was previously a Non‐Executive and is now an Executive Director of Capricorn Metals Ltd (formerly Malagasy Minerals Limited) since July 2013 and has been a Non‐Executive Director of Silver Mines Limited since June 2016. Mr Langworthy holds an interest in 24,148,240 shares of the Company and 7,915,351 unlisted options. Andrew Munckton Managing Director (Appointed 20 March 2012)

Mr Munckton has a career spanning more than 30 years in senior roles in mineral exploration and project development in Australia and Sweden including 15 years in gold project exploration, development and operations as Chief Geologist with Pancontinental and General Manager Operations at Paddington, Kundana and Kanowna Belle gold mines. He was General Manager Operations for Gindalbie Metals where he oversaw the development of the Karara Iron Ore Project including securing major Joint Venture partner, Ansteel, of China and completion of a Bankable Feasibility Study on Direct Shipping Ore and Magnetite concentrate projects valued at $2.7 billion. He was Managing Director of ASX listed Avalon Minerals Ltd where he was involved in securing the Viscaria Copper Project in Sweden, building an exploration team and taking the project to Bankable Feasibility Study stage. Mr Munckton holds an interest in 6,306,306 shares of the Company and 5,182,682 performance rights. David Morgan Non‐Executive Director (Executive Director from 20 March 2012 to 31 August 2013.

Non‐Executive Director since 1 September 2013) Mr Morgan is a mining engineer and mechanical engineer with more than 30 years experience in the mining industry in Australia and Africa. He has previously held a number of executive development and mine operations roles involving project engineering, maintenance and contract earthmoving for companies such as Rio Tinto, Macmahon and WMC Resources. He was General Manager Operations for Equigold in Queensland where he was responsible for the building, commissioning and management of the Mt Rawdon Gold Mine. He was General Manager Mining and Metallurgy for Sundance Resources' Mbalam Iron Ore Project in Cameroon where he oversaw the completion of a PFS on a $3.3 billion Direct Shipping Ore and Itabirite project for that company, including the delivery of 10 years of JORC compliant, high grade Ore Reserves and the establishment of project metallurgical and processing parameters. Mr Morgan was CEO of ASX‐listed RNI NL between 2 November 2015 and 1 September 2016. Mr Morgan holds an interest in 13,966,677 shares of the Company and 2,000,000 unlisted options.

Directors’ Report

4

INFORMATION ON DIRECTORS (CONT) Robert Cooper Non‐Executive Director (Appointed 4 May 2015) Mr Cooper is a mining engineer with more than 25 years’ industry experience, having held leadership roles across a diverse range of metalliferous commodities, both in Australia and overseas. He has a broad foundation of operating and technical experience in both underground and open pit operations. His career has been defined by a very strong health and safety improvement focus combined with a track record in delivering successful volume and cost outcomes through improvements in operational efficiency. He has previously held leadership positions with BHP Billiton as General Manager of Leinster Nickel Operations within Nickel West, Project Manager of a BHP Billiton‐wide organisation design project, and as Asset President of Ekati Diamonds in Canada. He more recently held positions with Discovery Metals as General Manager ‐ Operations in Botswana and as General Manager ‐ Development in their Brisbane office. Mr Cooper is currently the CEO of CopperChem Limited and Exco Resources Limited, both of which are 100% owned subsidiaries of the Washington H Soul Pattinson Group of companies. CopperChem holds 28.77% of the Company’s shares. Mr Cooper was appointed as a Non‐Executive Director of ASX‐listed Verdant Minerals Limited (formerly Rum Jungle Resources Limited) in July 2016, and as a Non‐Executive Director of Novonix Limited (formerly Graphitecorp Limited) in October 2016. Mr Cooper holds an interest in 1,580,000 shares of the Company. The directors have been in office to the date of this report unless otherwise stated. COMPANY SECRETARY Mr Paul Bridson is a Chartered Accountant and Chartered Secretary with more than 25 years accounting and finance experience, including more than 20 years in the resources industry. He was formerly Chief Financial Officer and Company Secretary for an unlisted public gold exploration company and prior to that role fulfilled the same role with ASX listed exploration company Avalon Minerals Ltd. Prior to these roles he was Financial Controller for Gindalbie Metals Ltd and has also held site based finance positions with various other WA based mining and mine service companies. Mr Bridson is a Member of the Institute of Chartered Accountants and Governance Institute of Australia. He holds a Bachelor of Commerce degree from the University of Western Australia. PRINCIPAL ACTIVITIES AND SIGNIFICANT CHANGES IN NATURE OF ACTIVITIES During the year the principal activity of the Group consisted of mineral exploration and evaluation in relation to its gold, base metals and copper mineral resources in WA and Queensland. During the year, following shareholder approval, the Company sold its interest in the Barbara Copper Project in Queensland. Apart from this sale and the acquisition of the WA‐based Monument Gold Project, there were no significant changes in the nature of the activities of the Group during the year.

Directors’ Report

5

OPERATING AND FINANCIAL REVIEW Operating Results The net profit of the Group for the financial year after provision for income tax was $1,075,112 (2016: loss $7,080,625) which includes mineral exploration expenditure impaired and written off of $891,372 (2016: $6,740,665). Financial Performance During the year ended 30 June 2017 the Group’s net cash position increased. This increase was predominantly influenced by cash inflows from sale of the Barbara Copper Project of $2,300,000, capital raisings totalling $2,317,038 and receipt of a Research and Development tax incentive totalling $292,606. These inflows were offset by outflows for exploration and evaluation costs of $2,053,740, administrative costs of $622,274 and capital raising costs of $148,127. Financial Position At the end of the year the Group had a cash balance of $2,634,331 (2016: $514,957). The Company has no corporate debt and minimal non‐discretionary long‐term commitments. The net assets of the Group increased from $5,690,231 at 30 June 2016 to $9,233,682 at 30 June 2017 predominantly as a result of the receipt of proceeds of $2.3 million from the sale of the Barbara Project and the capitalisation of exploration and evaluation expenditure of approximately $1.7 million in relation to the newly acquired Monument Gold Project in WA. Total liabilities amounted to $274,317 (2016: $172,903) and were limited to trade and other payables and employee benefit provisions. Strategy The focus of the Group during the financial year was the commencement of drilling and other exploration activities at its recently acquired Monument Gold Project in the Laverton region of WA and exploration and asset maintenance activities associated with the Company’s Queensland copper‐gold projects to ensure the tenement holding is kept in good standing. The Company also negotiated the sale of the Barbara Copper Project to joint venture partner, CopperChem Limited. For the year ended 30 June 2018 the Group plans to continue exploration of the Monument Gold Project and continue to undertake asset maintenance activities associated with the Queensland copper‐gold projects to ensure the tenement holding is kept in good standing whilst avenues are investigated to extract value from these projects via joint venture or outright sales. Operational Overview During the year, the Company’s assessment of potential new gold and base metal resource assets culminated in the acquisition of the Monument Gold Project in the Laverton region of Western Australia. Syndicated immediately commenced a systematic exploration and evaluation program at the project utilizing $2.1 million in funding raised via a share placement at 2.1 cents per share completed in August 2016 on the back of the Monument Project acquisition. The Company completed its maiden RC and diamond drilling program at the Korong prospect, a follow‐up RC drilling program at the A1 North prospect, and extensive regional soil sampling programs during the reporting period to confirm its geological, geophysical and geochemical interpretation of the extensive historical dataset purchased with the project. Results from these programs have been encouraging, indicating the potential for the discovery of a large, high‐quality gold system. Planning for follow‐up exploration programs is now well underway with further drilling planned during the second half of 2017 and 2018.

Directors’ Report

6

OPERATING AND FINANCIAL REVIEW (CONT) During the year, the Company sold its 50% ownership of the Barbara Copper Project to it joint venture partner, CopperChem, for $2.3 million cash plus a production royalty. It has maintained its Mt Isa‐based copper exploration tenure while seeking earn‐in joint venture partners for both the Mt Remarkable and Fountain Range projects.

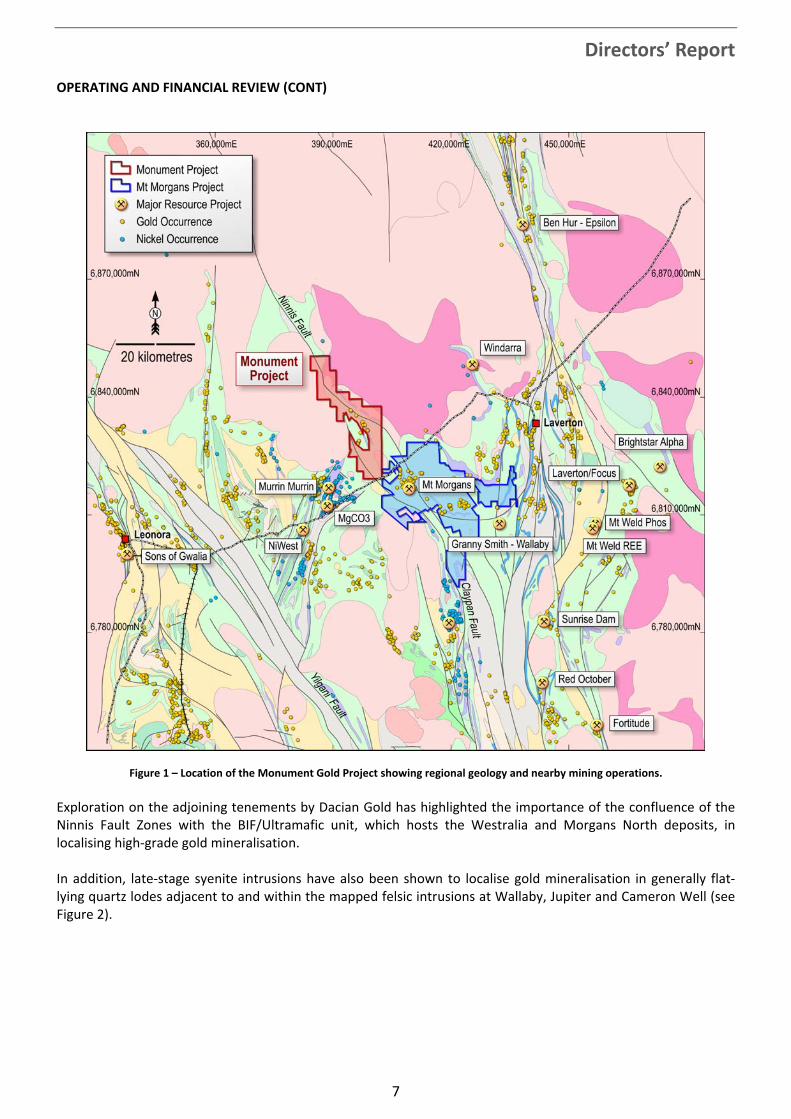

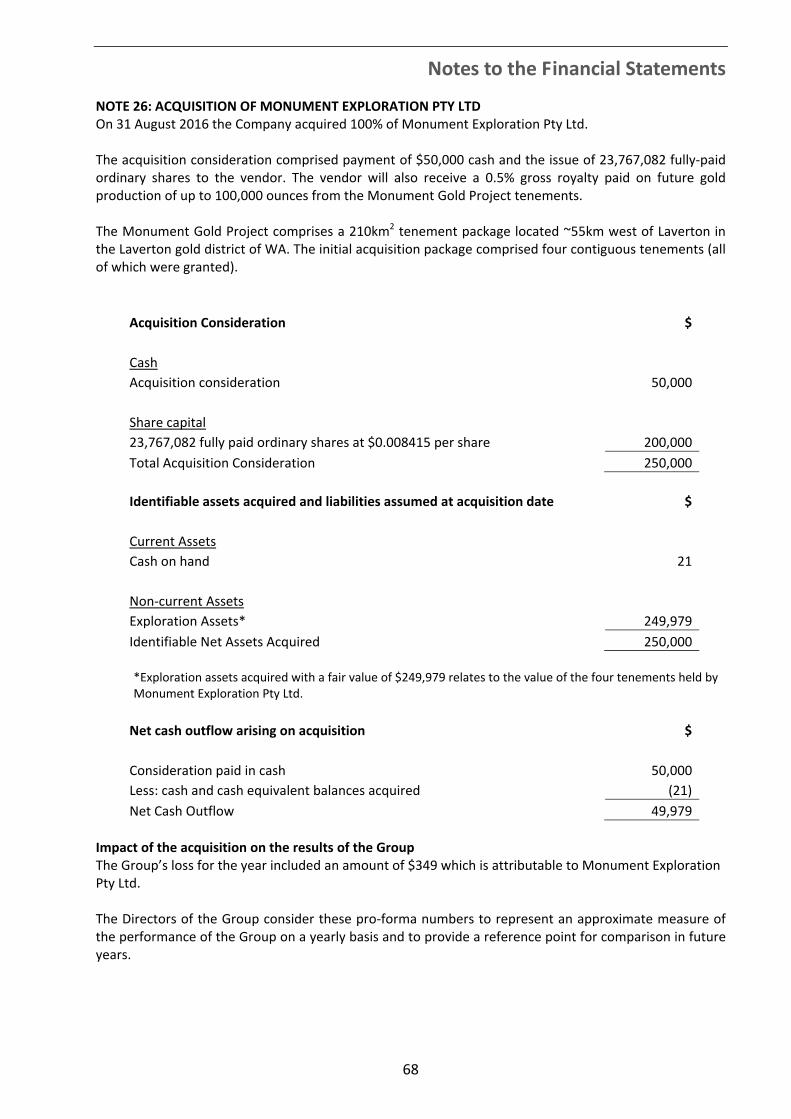

Exploration and Evaluation Monument Gold Project (WA) In August 2016, Syndicated acquired the highly prospective Monument Gold Project in WA’s Laverton gold province, through the purchase of private company Monument Exploration Pty Ltd (“Monument”). Syndicated acquired Monument for $50,000 in cash and 23,767,082 fully‐paid ordinary Syndicated shares ($200,000 total share consideration). The Vendor will also receive a 0.5% gross royalty paid on future gold production of up to 100,000 ounces from the tenements. Since the initial purchase, the Company has also acquired four additional tenements from other vendors and applied for an additional three tenements to complement the ground‐holding. The Monument Gold Project comprises a 210km2 tenement package (eight granted and four pending tenements) located ~55km west of Laverton and immediately to the north‐west of the 3.3Moz Mount Morgans Gold Project, currently being explored and developed by Dacian Gold Limited (ASX: DCN) (refer Dacian Gold announcement 25 July 2016) (see Figure 1). The Project lies in the world‐class Laverton gold district of WA, which hosts numerous multi‐million ounce gold mines such as Sunrise Dam (+10Moz), Wallaby (+8Moz), Granny Smith (+2Moz) and Lancefield (+2Moz). This area is a well‐established mining district with excellent infrastructure and access including the sealed Leonora‐to‐Laverton road (which runs through the project), a new gas pipeline and sealed airstrips at Laverton and Leonora. The Monument Gold Project tenements cover an approximate 25km strike length of the Ninnis and Claypan Fault Zones, the two significant regional geological structures which control gold and nickel mineralisation identified further to the south, particularly at the Mount Morgans Gold Project (see Figure 1). The last concerted phase of exploration on the Monument tenements was undertaken by Carpentaria Exploration and Western Mining Corporation in the late 1980s and early 1990s. Carpentaria Exploration drilled the Waihi and Korong prospects, both of which contain near‐surface historical gold workings, some dating back to the last century. The Korong mine produced some 2,875 tonnes of ore at an average grade of 35.6g/t Au while the Waihi mine produced 424 tonnes of ore at an average grade of 67.9g/t Au. Most of these workings were abandoned by 1910. Historical workings are to a maximum depth of approximately 20m below surface. A total of 142 historical drill holes have been recorded on the tenements, most of which were drilled under and immediately along strike of the historical workings at the Waihi and Korong prospects. Drilling rarely penetrated the oxidised zone, which ranges from 20m to 80m depth in the area. The last recorded drill hole was completed in 2003.

Directors’ Report

7

OPERATING AND FINANCIAL REVIEW (CONT)

Figure 1 – Location of the Monument Gold Project showing regional geology and nearby mining operations. Exploration on the adjoining tenements by Dacian Gold has highlighted the importance of the confluence of the Ninnis Fault Zones with the BIF/Ultramafic unit, which hosts the Westralia and Morgans North deposits, in localising high‐grade gold mineralisation. In addition, late‐stage syenite intrusions have also been shown to localise gold mineralisation in generally flat‐lying quartz lodes adjacent to and within the mapped felsic intrusions at Wallaby, Jupiter and Cameron Well (see Figure 2).

Directors’ Report

8

OPERATING AND FINANCIAL REVIEW (CONT)

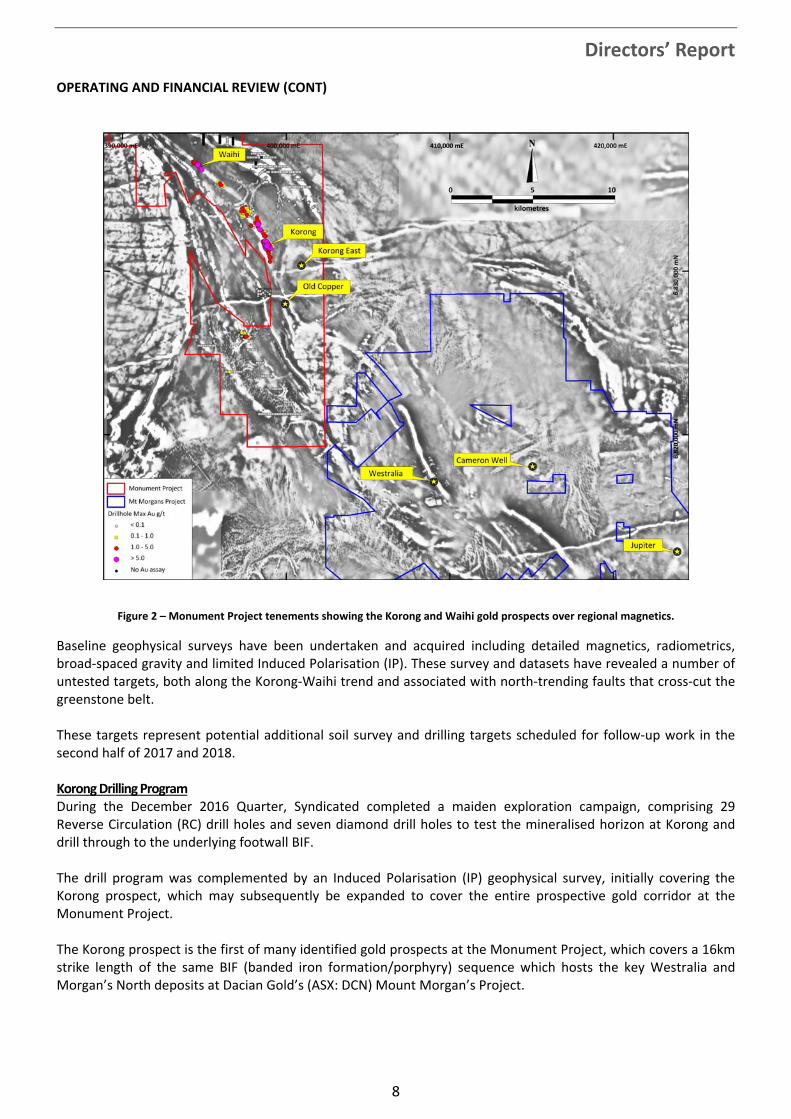

Figure 2 – Monument Project tenements showing the Korong and Waihi gold prospects over regional magnetics.

Baseline geophysical surveys have been undertaken and acquired including detailed magnetics, radiometrics, broad‐spaced gravity and limited Induced Polarisation (IP). These survey and datasets have revealed a number of untested targets, both along the Korong‐Waihi trend and associated with north‐trending faults that cross‐cut the greenstone belt. These targets represent potential additional soil survey and drilling targets scheduled for follow‐up work in the second half of 2017 and 2018. Korong Drilling Program During the December 2016 Quarter, Syndicated completed a maiden exploration campaign, comprising 29 Reverse Circulation (RC) drill holes and seven diamond drill holes to test the mineralised horizon at Korong and drill through to the underlying footwall BIF. The drill program was complemented by an Induced Polarisation (IP) geophysical survey, initially covering the Korong prospect, which may subsequently be expanded to cover the entire prospective gold corridor at the Monument Project. The Korong prospect is the first of many identified gold prospects at the Monument Project, which covers a 16km strike length of the same BIF (banded iron formation/porphyry) sequence which hosts the key Westralia and Morgan’s North deposits at Dacian Gold’s (ASX: DCN) Mount Morgan’s Project.

Directors’ Report

9

OPERATING AND FINANCIAL REVIEW (CONT) Significant assay results from the RC drilling program undertaken at the Korong Prospect included (for full details refer to ASX Announcements dated 28 November and 9 December 2016):

MRC003 6m @ 7.28g/t from 79m

MRC004 9m @ 1.92g/t from 88m

MRC005 8m @ 1.54g/t from 111m

MRC008 10m @ 1.21g/t from 63m

MRC011 4m @ 2.18g/t from 18m

MRC028 3m @ 5.41g/t from 112m

MRC029 6m @ 1.86g/t from 39m

MRC023 3m @ 3.27g/t from 84m

MRC024 1m @ 7.86g/t from 31m

MRC025 8m @ 1.61g/t from 75m

MRC026 7m @ 1.1g/t from 53m

MRC027 5m @ 1.35g/t from 137m and 2m @ 2.11g/t from 160m. Results from the diamond drilling included several intercepts in the Korong BIF/chert, such as:

MRCD001 10.0m @ 1.42g/t from 49m

MRCD004 3.0m @ 3.51g/t from 139m

MRCD006 5.0m @ 2.38g/t from 120m

MRCD007 5.8m @ 1.61g/t from 132m

The Korong Prospect mineralisation has so far been delineated by drilling over a strike length of approximately 500m, a down‐dip extent of 200m and an average thickness of 5m (see Figures 3 and 4). The recent drilling confirms the earlier interpretation of an east‐dipping and north‐plunging zone of gold mineralisation associated with the Korong BIF unit containing several shoots of higher grade mineralisation also plunging to the north. Representative cross‐sections of the mineralisation are shown in Figure 3. High‐grade intersections (3m @ 3.27g/t in MRC023) returned from the 1350mN line (see Figure 4) highlight the potential for further high‐grade zones at depth to the north (Target A). In addition, on the 1050mN line, near‐surface, high‐grade mineralisation (3m @ 5.41g/t in MRC028) has also been identified at Target C. These results highlight the outstanding potential to further expand the high‐grade zones of mineralisation along strike. Deeper diamond drilling was also completed to test new targets in the Korong Ultramafic stratigraphy. Four deep drill holes (MRCD001, MRCD004, MRCD005 and MRCD007) tested the ultramafic unit below Korong to a depth of approximately 300m below surface (see Figure 3). Geological logging of the drill holes indicates the presence of a suite of felsic porphyry intrusions and the intersection of a major sulphide‐rich shear zone near the lower contact with the underlying basalt unit. The shear zone contains pyrite alteration with minor gold mineralisation (see Figure 3). The targeted stratigraphy is interpreted to have been offset by the shear zone.

Directors’ Report

10

OPERATING AND FINANCIAL REVIEW (CONT)

Figure 3 – Korong cross‐section 1050N (left) and 1250N (right) (Local Grid) represent Korong BIF/Chert mineralisation generally 2 to 6 metres thick at the upper contact of the Korong Ultramafic unit. The lower contact is characterised by a pyrite rich alteration zone and

represents a priority target along strike from Korong.

Figure 4 – Korong Prospect Plan: Projection of BIF hosted mineralisation.

Directors’ Report

11

OPERATING AND FINANCIAL REVIEW (CONT) Geological Interpretation An updated geological interpretation of the Korong area is shown in Figure 5. A number of cross‐cutting faults have been identified that intersect the Korong stratigraphy and are associated with the regionally significant Celia Fault. These cross‐cutting faults are interpreted to be long‐lived structures that have been activated and reactivated during the extensive deformation of the greenstone belt, including the intrusion of a number of late‐stage granites and syenites which have been identified on the property. High‐grade gold mineralisation has been discovered at Dacian Gold’s neighbouring Mt Morgans Project, where BIF, ultramafic and felsic porphyry stratigraphy is intersected by north‐east trending faults that reactivate pre‐existing shear zones, intrusions and faults during later gold mineralising events, e.g. the Westralia footwall mineralisation. A number of deposits and prospects at Mt Morgans are associated with syenite intrusions (e.g. Jupiter and Cameron Well). Syndicated believes that the presence of gold mineralisation associated with sulphide alteration, in several orientations, at a number of geological settings on the Monument Project (including the Korong BIF deposit) are all associated with, and controlled by, the reactivation of the cross‐cutting faults by late‐stage granite and syenite intrusions. The varied and widespread nature of the mineralisation encountered to date is indicative of a large mineralised system. The Korong Prospect is the first target to be tested along a 16km strike length of favourable stratigraphy and major gold‐bearing structures which make up the Korong‐Waihi trend.

Figure 5 – Updated geological interpretation of Korong‐Waihi Trend, with key targets highlighted at the

intersection of the cross‐cutting faults with prospective stratigraphy.

Directors’ Report

12

OPERATING AND FINANCIAL REVIEW (CONT) Geological, Structural, Geophysical & Geochemical Review During the first half of 2017, Syndicated completed a comprehensive geological, structural, geophysical and geochemical review of the Monument Project area. The review was undertaken by Southern Geoscience Consultants and culminated in the development of a new geological and structural interpretation, which is illustrated in Figure 6. The review has highlighted new target positions along the Korong‐Waihi Trend and several conceptual targets outside of this Trend which warrant initial geochemical assessment through soil sampling and ground‐based validation of the geological interpretation. A comprehensive review was also undertaken of the broader exploration potential of the Monument Gold Project, including the 16km long Korong‐Waihi Trend which has been the main focus of the Company’s exploration activity since acquiring the project. Following this review, regional soil sampling programs commenced over conceptual targets to the north‐west of Waihi, in the far northern section of the tenement holding, and to the east of Korong, to establish the presence of gold mineralisation. The objective of the program is to identify accumulations of higher grade gold mineralisation for initial follow‐up with aircore drilling. If confirmed, these targets would rank alongside previously identified targets within the Korong‐Waihi Trend for drill testing later in 2017 (see Figure 6).

Figure 6 – Updated Geological and Structural interpretation of the Monument Gold Project. Advanced Targets lie

along the Korong‐Waihi Trend. Conceptual Targets have been initially tested with soil sampling.

Directors’ Report

13

OPERATING AND FINANCIAL REVIEW (CONT) At Korong, detailed analysis by WMC of the Korong mineralisation indicated two distinct stages of gold mineralisation associated with pyrite:

Early, fine‐grained pyrite associated with low grade gold and anomalous silver‐lead‐zinc; and

Later, coarse‐grained pyrite associated with high grade gold, copper and sericite alteration.

At Waihi, historical RC drilling under old workings intersected pyrite and iron‐rich (in the oxide zone) gold mineralisation associated with the BIF/Shale unit. The unit has been mapped over 4km either side of Waihi. Better assay results from the historical programs at Waihi included results such as (refer ASX announcement dated 27 July 2016):

MK32 2m @ 8.80g/t from 38m

MK33 1m @ 10.8g/t from 91m

MK34 2m @ 6.07g/t from 36m A1 North Drilling Program During the March 2017 Quarter, Syndicated completed modelling and interpretation of the Induced Polarisation (IP) geophysical survey completed earlier in the year. This revealed a new drilling target at A1 North, located 1.2km north of the previously drilled Korong prospect. The known gold (and associated pyrite) mineralisation at the Korong prospect, which was targeted by Syndicated in 2016 in its maiden drilling program, demonstrated a weak IP and resistivity response which is well correlated with the strength and position of the mineralisation encountered in the drilling. The A1 North IP target is located down‐dip from the surface expression of the mapped continuation of the Korong BIF/Shale unit. The strong IP anomaly was targeted because of the clear correlation between gold, pyrite and IP geophysics encountered at Korong.

Figure 7 – Korong and A1 North Prospects. Drill hole locations and mapped BIF/Chert outcrop over IP‐3D slice image.

Directors’ Report

14

OPERATING AND FINANCIAL REVIEW (CONT) The Company completed a program of reverse circulation (RC) drilling to test the A1 North target. The program comprised six holes drilled in three fences at 200m spacings, but was curtailed by the heavy rainfall experienced in March. The A1 North drilling intersected the BIF/Shale unit in all six completed holes. Narrow zones of high‐grade gold mineralisation were intersected associated with the pyrite‐rich shales and shear zones in the expected BIF/chert positions. Gold mineralisation is also present down‐dip of the Marionette and Pot Boiler surface workings, located to the east of the A1 North Target (Figure 7). Zones of banded pyrite mineralisation with low‐grade (0.2ppm to 0.9ppm) gold in BIF/shales are interpreted to be the source of the IP anomaly. The mineralisation in these positions is similar in appearance to the Korong prospect mineralisation. Intercepts included (for full details refer to the ASX announcement dated 26 April 2017):

MRC033 3m at 3.76g/t Au from 212m

MRC034 1m at 1.65g/t Au from 207m

MRC035 6m at 0.86g/t Au from 179m The pyrite mineralisation associated with the BIF/shale unit(s) at A1 North is anomalous in silver and base metals. The A1 North drilling is considered to contain the early stage mineralisation, as encountered at Korong. Ongoing exploration activities at Monument will be focused on identifying accumulations of later stage, high grade gold mineralisation. Regional Soil Sampling A regional soil sampling program was completed in the June 2017 Quarter at three areas within the tenement package. Each area was sampled on a 400m by 100m spacing with samples submitted to Intertek laboratories for multi‐element assay. Further more detailed soil sampling is planned. As at the date of this Report assay results are pending. The sampling targeted new exploration targets, including:

Perseverance, associated with Waihi‐style narrow high‐grade mineralisation;

Old Copper and Korong East, associated with the confluence of a major N‐S oriented fault; and

The circular magnetic feature postulated to contain a late‐stage felsic intrusion. New Exploration Program The recent exploration activities have given Syndicated a clear understanding of the geological controls and distribution of gold mineralisation on the Monument Project, highlighting two distinct phases of gold mineralisation and their associated structural controls and alteration indicators across the project. This understanding, coupled with the updated geological and structural interpretation work, will be tested with exploration programs over the coming months, and includes:

Follow‐up close‐spaced soil sampling programs over new and established mineralised trends highlighted along the Korong‐Waihi Trend and conceptual targets confirmed by the regional soil sampling programs detailed above; and

A targeted aircore drilling program over prospects highlighted at:

o The Korong‐Waihi Trend, where close‐spaced soil sampling has highlighted several areas of anomalous gold mineralisation where little or no drill testing has occurred; and

o New regional prospects highlighted by the regional and follow‐up soil sampling programs associated with late stage felsic intrusions.

Directors’ Report

15

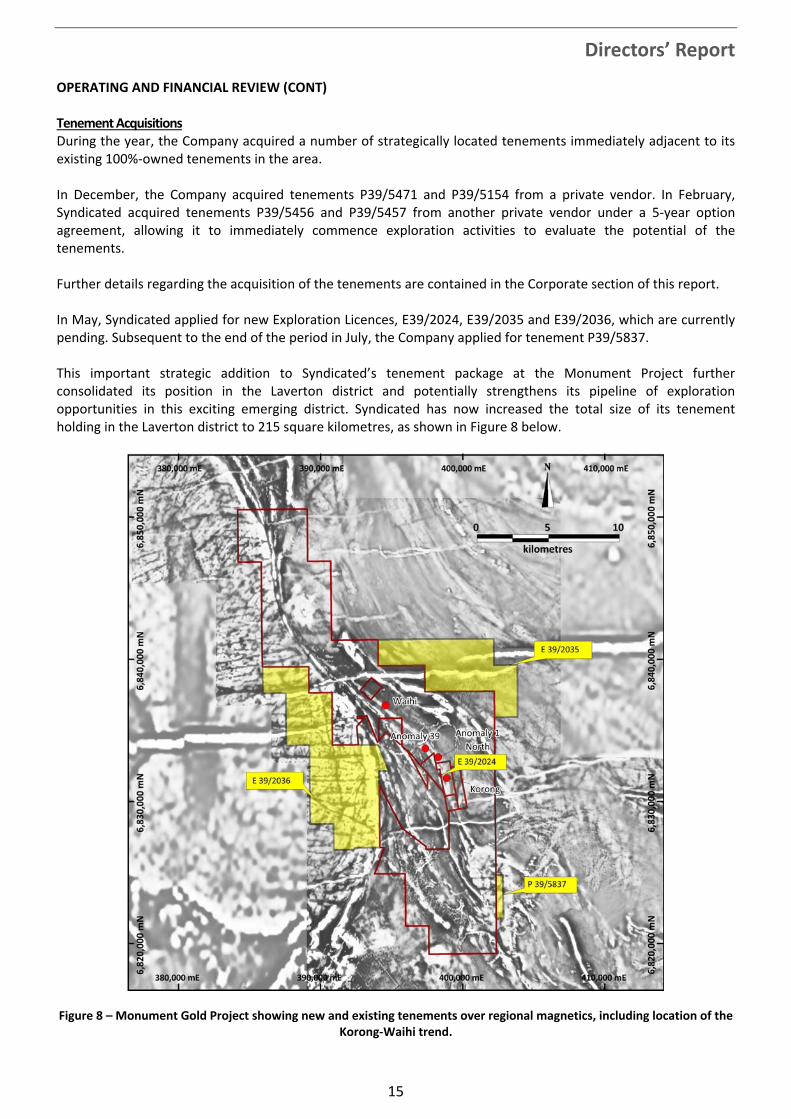

OPERATING AND FINANCIAL REVIEW (CONT) Tenement Acquisitions During the year, the Company acquired a number of strategically located tenements immediately adjacent to its existing 100%‐owned tenements in the area. In December, the Company acquired tenements P39/5471 and P39/5154 from a private vendor. In February, Syndicated acquired tenements P39/5456 and P39/5457 from another private vendor under a 5‐year option agreement, allowing it to immediately commence exploration activities to evaluate the potential of the tenements. Further details regarding the acquisition of the tenements are contained in the Corporate section of this report. In May, Syndicated applied for new Exploration Licences, E39/2024, E39/2035 and E39/2036, which are currently pending. Subsequent to the end of the period in July, the Company applied for tenement P39/5837. This important strategic addition to Syndicated’s tenement package at the Monument Project further consolidated its position in the Laverton district and potentially strengthens its pipeline of exploration opportunities in this exciting emerging district. Syndicated has now increased the total size of its tenement holding in the Laverton district to 215 square kilometres, as shown in Figure 8 below.

Figure 8 – Monument Gold Project showing new and existing tenements over regional magnetics, including location of the Korong‐Waihi trend.

Directors’ Report

16

OPERATING AND FINANCIAL REVIEW (CONT) Sale of Barbara Copper Project (Qld) The Barbara Copper Project is located 60km north‐east of Mt Isa in North Queensland. The Barbara Copper Project was part of the Barbara Joint Venture, which covered approximately 100km2 of tenure within the Mt Remarkable Project area. The Barbara JV was a 50/50 joint venture between CopperChem Limited (CopperChem) and Syndicated with CopperChem being the Manager of the Project. Syndicated was in joint venture with CopperChem at the Barbara Copper Project from September 2013 until June 2017. During the June Quarter, Syndicated entered into an agreement to sell its 50% share of the Barbara Copper Project to CopperChem for A$2.3 million in cash plus a production royalty. Following the satisfaction of all conditions precedent, including shareholder approval obtained at a shareholders meeting held on 7 June, and the receipt of indicative approval from the Queensland Minister of Mines for the transfer of Syndicated’s interest in the Project, the transaction was completed and funds were received from CopperChem in mid‐June. Funds raised from the sale of the Company’s interest in the Barbara Copper Project will be predominantly used to underpin the next phase of exploration programs at the Monument Gold Project. Agreement Terms and Consideration The consideration payable by CopperChem for the acquisition of Syndicated’s 50% share of the Barbara Copper Project was as follows:

A$2.3 million in cash payable in one instalment upon completion of the Sale and Purchase Agreement; and

A production royalty payable on the first 10,000 tonnes of copper‐in‐concentrate (or ore equivalent) produced by the Barbara Copper Project. The royalty will be payable as follows:

o 1% of the net smelter return (NSR) generated from the sale of concentrate or ore equivalent subject to a minimum invoiced copper price of US$2.50/lb;

o 2% of the NSR generated from the sale of concentrate or ore equivalent subject to a minimum invoiced copper price of US$3.00/lb;

o Where no production royalties are payable due to the invoiced price being below US$2.50/lb, copper sold from the Barbara Copper Project does not count towards the 10,000 tonne production royalty cap;

o NSR in relation to copper concentrate is defined as net revenue received from the sale of the products, excluding credits from other metals; and

o NSR in relation to ore sales is defined as net revenue received from the sale of the products, excluding credits from other metals and less processing costs.

Syndicated retains 100% ownership of its Northern and Southern Hub Projects in North Queensland, comprising a ground package of 1,542km2 containing numerous high‐grade copper‐gold targets plus multiple IOCG and SEDEX‐style targets.

Directors’ Report

17

OPERATING AND FINANCIAL REVIEW (CONT) Mt Remarkable/Northern Hub (Syndicated 100%) (Qld) The Mt Remarkable Project consists of eleven EPM tenements covering 1,082km2 of tenure and straddles the Mt Remarkable Fault from the Barkley Hwy to Kajabbi. The project has reverted to an exploration based assessment of potential new discoveries following the divestment of the Barbara Copper Project to CopperChem. During the year, the Company sought expressions of interest for joint venture partners to undertake exploration for IOCG and SEDEX lead‐zinc‐silver style mineralisation given the project’s prospectivity for these metals. Syndicated is seeking to partially divest the project via an exploration earn‐in joint venture.

Figure 9 – Mt Remarkable Base Metal/Gold Project showing existing tenements over regional magnetics, including location

of the divested Barbara Project.

Directors’ Report

18

OPERATING AND FINANCIAL REVIEW (CONT) Fountain Range/Southern Hub (Syndicated 100%) (Qld) The Fountain Range Project consists of sixteen EPM tenements covering approximately 460km2 of tenure 100km south‐east of Mt Isa. During the year, the Company sought expressions of interest for JV partners to undertake exploration for IOCG and high‐grade lode style gold mineralisation, given the project’s prospectivity for this style of mineralisation. Syndicated is seeking to divest the project via an exploration earn‐in joint venture or outright sale.

Figure 10 – Southern Hub Base Metal/Gold Project showing existing tenements over regional magnetics, including location

of the Duchess Project.

Directors’ Report

19

OPERATING AND FINANCIAL REVIEW (CONT) Other Projects Syndicated Royalties Pty Ltd (a 100% owned subsidiary of Syndicated Metals) holds a 2% NSR royalty over metals extracted from tenement EPM13870 now held by Hammer Metals Limited (ASX: HMX). Mineral Resources Barbara Copper Project (formerly owned 50% by Syndicated Metals) During the year the Barbara Copper Project was sold to the Company’s joint venture partner, CopperChem Limited. The Mineral Resource estimate for the Barbara Copper Project is therefore no longer reported. Lillymay Deposit (formerly owned 50% by Syndicated Metals) Lillymay is located 4km south‐west of Barbara and formed part of the Barbara Copper Project in partnership with CopperChem. During the year the Barbara Copper Project was sold to the Company’s joint venture partner, CopperChem Limited. The Mineral Resource estimate for Lillymay is therefore no longer reported. Comparison with previous Mineral Resource Estimates The Barbara Mineral Resource was announced in July 2014 and included in the 2014 Annual Report. The Lillymay Mineral Resource was announced in December 2014 and included in the 2015 Annual Report. Both Mineral Resources were sold to CopperChem Limited during the current reporting period. Mineral Resource Governance Arrangements The Company ensures that all Mineral Resource estimates are subject to appropriate levels of governance and internal controls. Exploration results are collected and managed by competent qualified geologists and overseen by the Exploration Manager. All data collection activities are conducted to industry standards based on a framework of quality assurance and quality control protocols covering all aspects of sample collection, topographical and geophysical surveys, drilling, sample preparation, physical and chemical analysis and data and sample management. Mineral Resource estimates are prepared by qualified Competent Persons and further verified by the Company’s technical staff. If there is a material change in the estimate of a Mineral Resource the estimate and supporting documentation is reviewed by a suitably qualified independent Competent Person. Joint Ventures Barbara Joint Venture – CopperChem Limited Syndicated was in Joint Venture with CopperChem Limited over portions of tenements EPM19733 and EPM18492 and all of EPM16112 and ML90241. CopperChem had earned a 50% interest in these tenements by funding and managing a feasibility study over the Barbara Copper Project. During the period, Syndicated sold its 50% share of the Barbara Copper Project to CopperChem for A$2.3 million in cash plus a production royalty. The Barbara Joint Venture was terminated with tenements EPM16112 and ML90241 being retained by CopperChem and tenements EPM19733 and EPM18492 retained by Syndicated. CopperChem has exploration rights over portions of the tenements retained by Syndicated.

Directors’ Report

20

OPERATING AND FINANCIAL REVIEW (CONT) Tenements Queensland The Company’s Queensland tenement holding covers 1,542 km2. Exploration on the Company’s tenements is managed by Syndicated Metals. The Company’s current tenement holdings consist of 100% ownership in 27 granted EPMs in the Northern and Southern Hubs. During the year tenement EPM26026 was granted to the Company. Tenements EPM16112 and ML90241 were sold by the Company. Western Australia The Company’s Western Australian tenement holding covers approximately 215 km2. The tenements are held by 100% owned subsidiary, Monument Exploration Pty Ltd. Exploration on the tenements is managed by Syndicated Metals. The Company’s current tenement holdings consist of 100% ownership in 12 tenements, 8 of which are granted and 4 applications. All tenements are located at the Monument Gold Project near Laverton. All tenements were acquired during the year. During the year tenement E39/1866 was granted to the Company. Competent Person’s Statement The information in this report that relates to Exploration Targets and Exploration Results is based on information compiled by Mr Andrew Munckton who is a Member of The Australasian Institute of Mining and Metallurgy (MAusIMM) and who has sufficient experience relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person as defined in the 2012 Edition of the Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves (the “JORC Code”). Mr Munckton is a full‐time employee of Syndicated Metals Limited and consents to the inclusion in the report of the Exploration Targets and Exploration Results in the form and context in which they appear.

Exploration Targets This report comments on and discusses Syndicated Metals Limited’s exploration in terms of target size and type. The information relating to Exploration Targets should not be misunderstood or misconstrued as an estimate of Mineral Resources or Ore Reserves. The potential quantity and quality of material discussed as Exploration Targets is conceptual in nature since there has been insufficient work completed to define them as Mineral Resources or Ore Reserves. It is uncertain if further exploration work will result in the determination of a Mineral Resource or Ore Reserve.

Corporate Share Placement In August, Syndicated successfully raised a total of $2.1 million to fast‐track its maiden drilling program at the Monument Gold Project. The capital raising, which was undertaken at an issue price of 2.1 cents per share, comprised a heavily oversubscribed share placement to sophisticated and professional clients of Sydney‐based Blue Ocean Equities, as well as some long‐standing shareholders of the Company, and an additional $110,000 share placement to companies associated with its Directors. A total of 95,000,000 fully paid ordinary shares were issued in Tranche 1 raising $1,995,000. The balance of the Placement Shares (5,238,095 Shares) were issued to companies associated with directors also at an issue price of 2.1 cents per Share (Tranche 2) to raise $110,000. Shareholder approval was required to issue the Tranche 2 shares and this was obtained at the Company’s AGM held on 27 October 2016.

Directors’ Report

21

OPERATING AND FINANCIAL REVIEW (CONT) CopperChem Anti‐dilution Right The issue of the placement shares triggered the CopperChem anti‐dilution right. CopperChem waived its anti‐dilution right in regard to the issue of the 95,000,000 Tranche 1 shares and accepted its right in regard to the Tranche 2 shares, subject to shareholder approval of the issue of the Tranche 2 shares and the issue of the CopperChem anti‐dilution shares. Details of the additional share and options issued to CopperChem under its anti‐dilution right are contained in the next section. Issue of Shares and Options Following shareholder approval obtained at the AGM held on 27 October 2016, the Company issued the following securities:

5,000,000 Shortfall Offer Shares;

5,238,095 Placement Shares;

10,355,000 Top‐Up Offer 1 and 2 Shares to CopperChem;

12,184,000 Top‐Up Offer 3 Shares to CopperChem;

2,685,000 Top‐Up Offer 4 Shares to CopperChem; and

7,677,500 unlisted Options comprising 2,500,000 Options attached to the Shortfall Offer Shares and 5,177,500 Options attached to the Top‐Up Offer 1 and 2 Shares.

Issue of Shortfall Offer Shares The Company issued 5,000,000 fully paid ordinary shares at 0.5 cents per share to raise $25,000 under the same terms and conditions of the Shortfall Offer as announced on 7 December 2015. The shares were issued to a company associated with a director, Mr Peter Langworthy. Issue of Placement Shares The Company issued 5,238,095 Shares at 2.1 cents per share to raise $110,000 under the second tranche of the share placement announced on 9 August 2016. The shares were issued to companies associated with two directors, Mr Langworthy and Mr Morgan. Issue of CopperChem Top‐Up Shares Pursuant to CopperChem’s anti‐dilution right granted under the Placement Agreement signed between Syndicated and CopperChem in September 2013, to the maximum extent permitted by law, Syndicated is required to offer to CopperChem new Shares in order for CopperChem to maintain the same percentage interest in the capital of Syndicated as was held prior to the issue of the new Shares. CopperChem exercised its right to subscribe for the following new Shares:

Issue of CopperChem Top‐Up Offer 1 and 2 Shares

On 4 April 2016, Syndicated issued 15,200,000 Shares at 0.5 cents per Share under the Shortfall Offer to unrelated parties of the Company. The Company further issued 5,000,000 Shares at 0.5 cents per Share under its Shortfall Offer to a company associated with a director, Mr Langworthy, as detailed above. The Company issued 10,355,000 fully paid ordinary shares to CopperChem. The Shares were issued at 0.5 cents per Share in line with the pricing of the Shortfall Offer and raised $51,775.

Directors’ Report

22

OPERATING AND FINANCIAL REVIEW (CONT)

Issue of CopperChem Top‐Up Offer 3 Shares On 31 August 2016, Syndicated issued 23,767,082 Shares at 0.8415 cents per Share pursuant to the acquisition of unlisted company Monument Exploration Pty Ltd. The Company issued 12,184,000 fully paid ordinary shares to CopperChem. The Shares were issued at 0.8415 cents per Share in line with the pricing of the Monument acquisition and raised $102,528.

Issue of CopperChem Top‐Up Offer 4 Shares On 9 August 2016, the Company announced that it had raised $2.1 million pursuant to a share placement. A total of 95,000,000 Shares at 2.1 cents per Share to raise $1.995 million were issued to sophisticated and professional investors with the balance of the Shares (5,238,095 Shares) issued to companies associated with Directors, as noted above. CopperChem waived its top‐up right in regard to the issue of the 95,000,000 Shares and accepted its right in regard to the Shares issued to director related entities. The Company issued 2,685,000 fully paid ordinary shares to CopperChem. The Shares were issued at 2.1 cents per Share in line with the pricing of the share placement and raised $56,385.

Issue of Unlisted Options Subscribers under the Shortfall Offer were offered the opportunity to subscribe for 1 free attaching unlisted option for every 2 Shares issued, with each option having an exercise price of 1.2 cents and expiring on 8 February 2018 (Options). This offer was made under the prospectus for the Entitlement Offer dated 10 December 2015. Following its election to exercise its anti‐dilution right following the Shortfall Offer, CopperChem was also offered the opportunity to subscribe for Options. This offer was also made under the prospectus for the Entitlement Offer dated 10 December 2015. Following shareholder approval for the above Option issues obtained at the Annual General Meeting held on 27 October 2016, Syndicated issued the following Options:

2,500,000 Options attaching to the 5,000,000 Shortfall Offer Shares issued to a company associated with a director, Mr Langworthy; and

5,177,500 Options attaching to the Top‐Up Offer 1 and 2 Shares to CopperChem. Issue of Shares for Tenement Acquisition In December the Company issued 600,000 Shares at 2.5 cents per share to the vendor of tenements P39/5471 and P39/5154 as consideration for the purchase of these tenements which adjoin Syndicated’s existing Monument Gold Project tenements ($15,000 total share consideration plus $10,000 cash). In February the Company issued 100,000 Shares at 2.3 cents per share to the vendor of tenements P39/5456 and P39/5457 as consideration for the purchase of these tenements which adjoin Syndicated’s existing Monument Gold Project tenements ($2,300 total share consideration plus $10,000 cash). The consideration for the acquisition comprised a combination of cash and shares, payable in two tranches:

Tranche 1 (paid in February) – $10,000 in cash and 100,000 fully‐paid ordinary shares in the Company at a deemed issue price of 2.3c per share; and

Tranche 2 (payable on a Decision to Mine on the tenements) – $250,000 in cash and 200,000 fully‐paid ordinary shares in the Company at a deemed issue price of 2.3c per share.

A 2% royalty on gross revenue on production from the tenements will also be payable.

Directors’ Report

23

OPERATING AND FINANCIAL REVIEW (CONT) Issue of Shares upon Exercise of Options In December Syndicated issued 87,500 Shares upon the exercise of unlisted options with an exercise price of 1.2 cents, expiring 8 February 2018. The Options were issued under Syndicated’s Prospectus dated 10 December 2015. Issue and Expiry of Performance Rights Following shareholder approval obtained at the AGM held on 27 October 2016, Syndicated issued a total of 2,384,473 performance rights to the Managing Director. The Tranche A rights (1,142,560) vest when the Company’s VWAP per share for 10 trading days exceeds $0.047 and the Tranche B rights (1,241,913) vest when the Company’s VWAP per share for 10 trading days exceeds $0.078. Both tranches of rights will expire on 27 October 2020. During the period the following performance rights did not meet the vesting conditions and expired:

Number Vesting when the Company’s 10 day VWAP exceeds Expiry Date

150,000 $0.30 30 November 2016

150,000 $0.45 30 November 2016

150,000 $0.60 30 November 2016

1,099,837 $0.06675 30 November 2016

1,556,692 $0.11125 30 November 2016

150,000 $0.30 8 November 2016

150,000 $0.45 8 November 2016

150,000 $0.60 8 November 2016

100,000 $0.30 31 October 2016

100,000 $0.45 31 October 2016

100,000 $0.60 31 October 2016

194,158 $0.06675 31 October 2016

274,808 $0.11125 31 October 2016

Expiry of Options On 9 January 2017, 5,000,000 unlisted options exercisable at $0.064 expired. Annual General Meeting The Company’s 2016 Annual General Meeting was held on 27 October 2016. All resolutions received strong support and were passed on a show of hands. Shareholders Meeting The Company held a General Meeting of shareholders on 7 June. All three resolutions, which included the approval to dispose of the Barbara Joint Venture interest to CopperChem, received strong support and were passed on a show of hands. Factors and Business Risks Affecting Future Business Performance The following factors and business risks could have a material impact on the Company’s ability to deliver its strategy: Access to funding The Company’s ability to continue to explore and evaluate its projects is contingent upon its ability to source timely access to additional equity funding as it is required.

Directors’ Report

24

OPERATING AND FINANCIAL REVIEW (CONT) Commodity demand and pricing The Company is exposed to adverse global demand for commodities and/or adverse commodity price movements. This could affect the Company’s ability to raise equity to fund its activities. Tenure risks The Company is exposed to loss of its tenure holding if it is unable to meet its tenement commitments due to lack of funding to do so. Operational risks The Company is exposed to several operational risks including unsuccessful exploration efforts, environmental issues and health and safety issues. Significant Changes in the State of Affairs During the reporting period the Company issued 130,574,595 shares at prices ranging between $0.005 and $0.021 raising $2,342,038 and a further 24,467,082 shares at prices ranging between $0.008415 and $0.025 in regard to the acquisition of assets and tenements. The Company also sold its interest in the Barbara Copper Project to its joint venture partner, CopperChem Limited for $2.3 million. In the opinion of the directors, other than as outlined in this report, there were no other significant changes in the state of affairs of the Group that occurred during the 2017 financial year. DIVIDENDS PAID OR RECOMMENDED No dividend has been paid or declared since the start of the financial year and no dividend is recommended.

EVENTS SUBSEQUENT TO REPORTING DATE There are no matters or circumstances that have arisen since the end of the financial year that have significantly affected or may significantly affect the operations of the entity, the results of those operations or the state of affairs of the entity, in future years. LIKELY DEVELOPMENTS AND EXPECTED RESULTS OF OPERATIONS Other than likely developments contained in the Operating and Financial Review, further information on likely developments in the operations of the Group and the expected results of those operations in future financial years have not been included in this report, as the directors believe that inclusion of such information is likely to result in unreasonable prejudice to the Company. ENVIRONMENTAL REGULATION The Group’s operations are regulated by the requirements of the Queensland Department of Natural Resources and Mines and the WA Department of Mines, Industry Regulation and Safety environmental regulations. The Company has complied with all of these requirements. MEETINGS OF DIRECTORS During the financial year five meetings of directors were held and the number of meetings attended by each director during the year is shown below:

Board Meetings Audit & Risk Committee

Remuneration Committee

Eligible to Attend

Attended Eligible to Attend

Attended Eligible to Attend

Attended

P J Langworthy 5 5 1 1 2 2

A T Munckton 5 5 1 1 ‐ ‐

D B Morgan 5 5 1 1 2 2

R J Cooper 5 5 1 1 ‐ ‐

Directors’ Report

25

INDEMNIFYING OFFICERS During the financial year, the Group paid insurance premiums (inclusive of fees and charges) in respect of Directors’ and Officers’ liability insurance. The liabilities insured are legal costs that may be incurred in defending civil or criminal proceedings that may be brought against Officers in their capacity as Officers of the Group, and any other payments arising from liabilities incurred by the officers in connection with such proceedings. This does not include such liabilities that arise from conduct involving a wilful breach of duty by the Officers or the improper use by the Officers of their position or of information to gain advantage for themselves or someone else or to cause detriment to the Company. It is not possible to apportion the premium between amounts relating to the insurance against legal costs and those relating to other liabilities. SHARE OPTIONS Unissued shares under options As at the reporting date, the unissued ordinary shares of the Company under unlisted options are as follows:

Grant date

Expiry date Exercise price (cents) Quantity

08/02/2016 08/02/2018 1.2 60,164,182

60,164,182

Each option entitles the holder to one fully paid ordinary share in the Company at any time up to expiry date. As at the reporting date 112,500 shares had been issued as a result of the exercise of options.

PROCEEDINGS ON BEHALF OF THE COMPANY No person has applied for leave of Court to bring proceedings on behalf of the Company or to intervene in any proceedings to which the Company is a party for the purpose of taking responsibility on behalf of the Company for all or any part of those proceedings. The Company was not a party to any such proceedings during the year. NON AUDIT SERVICES The board of directors is satisfied that the provision of non‐audit services during the year is compatible with the general standard of independence for auditors imposed by the Corporations Act 2001. The directors are satisfied that the services disclosed below did not compromise the external auditors’ independence for the following reasons: All non‐audit services are reviewed and approved by directors prior to commencement to ensure they do

not adversely affect the integrity and objectivity of the audit; and The nature of the services provided do not compromise the general principles relating to auditor

independence in accordance with APES 110: Code of Ethics for Professional Accountants set by the Accounting Professional and Ethical Standards Board.

The following fees were paid to PKF Mack for non‐audit services provided during the year ended 30 June 2017:

Taxation Services $ 2,550

AUDITOR’S INDEPENDENCE DECLARATION The auditor’s independence declaration for the year ended 30 June 2017 has been received and is included in the financial report.

Directors’ Report

26

REMUNERATION REPORT ‐ AUDITED This report details the nature and amount of remuneration for each key management person of Syndicated Metals Limited and its controlled entities, and for the executives receiving the highest remuneration. Remuneration policy The remuneration policy of Syndicated Metals Limited has been designed to align key management personnel objectives with shareholder and business objectives by providing a fixed remuneration component and offering specific long‐term incentives. The board of Syndicated Metals Limited believes the remuneration policy to be appropriate and effective in its ability to attract and retain the best key management personnel to run and manage the company, as well as create congruence between directors, executives and shareholders. The board’s policy for determining the nature and amount of remuneration for key management personnel of the Company is as follows:

The remuneration policy, setting the terms and conditions for the key management personnel, was developed by the board.

All key management personnel receive a base salary (which is based on industry experience and comparable rates for similar industry roles), superannuation and share based payments.

The board of directors review key management personnel packages annually by reference to the Company’s performance, executive performance and comparable information from industry sectors.

The performance of key management personnel is measured against criteria agreed with each executive. The board may, however, exercise its discretion in relation to approving incentives and share based payments. The policy is designed to attract the highest calibre of executives and reward them for performance that results in long‐term growth in shareholder wealth. Under the Company’s Performance Rights Plan, if in the opinion of the Board a participant acts fraudulently or dishonestly or is in material breach of his or her obligations to the Company or any of its subsidiaries, then the Board may, in its absolute discretion determine that:

‐ all of the participant’s performance rights have lapsed; or ‐ all shares held by the participant (or their nominee), as a result of the exercise of a performance right as

of the date of such determination will be bought back and cancelled by the Company (subject to the passage of a special resolution of shareholders), and until then will be subject to a transfer restriction.

The key management personnel receive a superannuation contribution, which for the year ended 30 June 2017 was 9.50%, and do not receive any other retirement benefits. All remuneration paid to key management personnel is valued at the cost to the Company and either expensed through the statement of profit or loss or capitalised to exploration and evaluation costs on the statement of financial position as appropriate. Share based payments are valued using the Black‐Scholes or binomial methodologies. The board policy is to remunerate non‐executive directors at market rates for time, commitment and responsibilities. The board determines payments to the non‐executive directors and reviews their remuneration annually, based on market practice, duties and accountability. Independent external advice is sought when required. The maximum aggregate amount of fees that can be paid to non‐executive directors is subject to approval by shareholders. Fees for non‐executive directors are not linked to the performance of the Company. However, to align directors’ interests with shareholder interests, the directors are encouraged to hold shares in the Company.

Directors’ Report

27

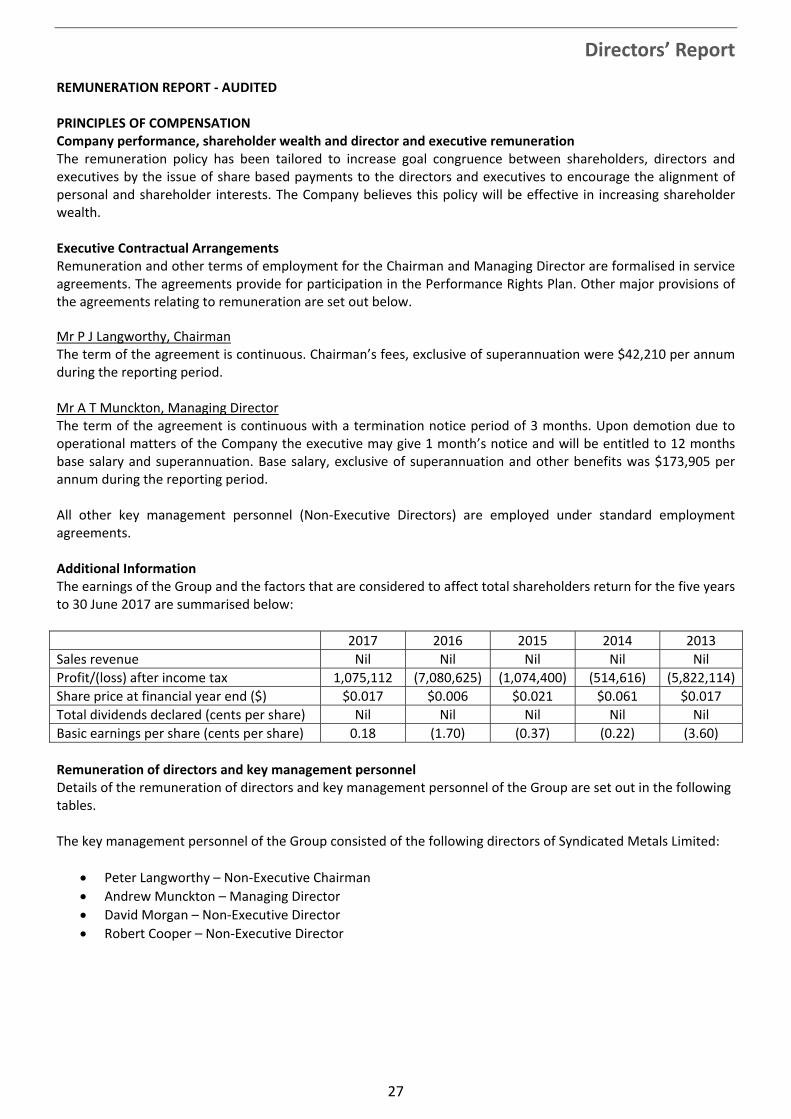

REMUNERATION REPORT ‐ AUDITED PRINCIPLES OF COMPENSATION Company performance, shareholder wealth and director and executive remuneration The remuneration policy has been tailored to increase goal congruence between shareholders, directors and executives by the issue of share based payments to the directors and executives to encourage the alignment of personal and shareholder interests. The Company believes this policy will be effective in increasing shareholder wealth. Executive Contractual Arrangements Remuneration and other terms of employment for the Chairman and Managing Director are formalised in service agreements. The agreements provide for participation in the Performance Rights Plan. Other major provisions of the agreements relating to remuneration are set out below. Mr P J Langworthy, Chairman The term of the agreement is continuous. Chairman’s fees, exclusive of superannuation were $42,210 per annum during the reporting period. Mr A T Munckton, Managing Director The term of the agreement is continuous with a termination notice period of 3 months. Upon demotion due to operational matters of the Company the executive may give 1 month’s notice and will be entitled to 12 months base salary and superannuation. Base salary, exclusive of superannuation and other benefits was $173,905 per annum during the reporting period. All other key management personnel (Non‐Executive Directors) are employed under standard employment agreements. Additional Information The earnings of the Group and the factors that are considered to affect total shareholders return for the five years to 30 June 2017 are summarised below:

2017 2016 2015 2014 2013

Sales revenue Nil Nil Nil Nil Nil

Profit/(loss) after income tax 1,075,112 (7,080,625) (1,074,400) (514,616) (5,822,114)

Share price at financial year end ($) $0.017 $0.006 $0.021 $0.061 $0.017

Total dividends declared (cents per share) Nil Nil Nil Nil Nil

Basic earnings per share (cents per share) 0.18 (1.70) (0.37) (0.22) (3.60)

Remuneration of directors and key management personnel Details of the remuneration of directors and key management personnel of the Group are set out in the following tables. The key management personnel of the Group consisted of the following directors of Syndicated Metals Limited:

Peter Langworthy – Non‐Executive Chairman

Andrew Munckton – Managing Director

David Morgan – Non‐Executive Director

Robert Cooper – Non‐Executive Director

Directors’ Report

28

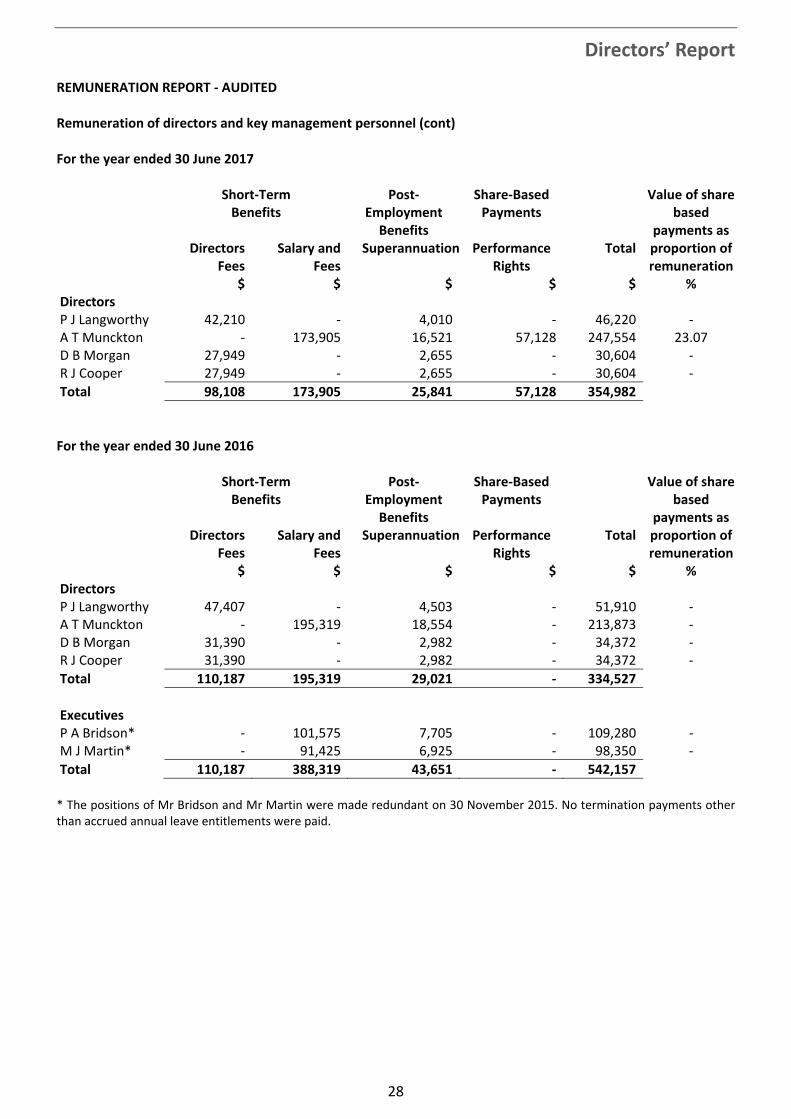

REMUNERATION REPORT ‐ AUDITED Remuneration of directors and key management personnel (cont) For the year ended 30 June 2017 Short‐Term

Benefits Post‐

Employment Benefits

Share‐Based Payments

Value of share based

payments as proportion of remuneration

Directors Fees

Salary and Fees

Superannuation Performance Rights

Total

$ $ $ $ $ % Directors P J Langworthy 42,210 ‐ 4,010 ‐ 46,220 ‐ A T Munckton ‐ 173,905 16,521 57,128 247,554 23.07 D B Morgan 27,949 ‐ 2,655 ‐ 30,604 ‐ R J Cooper 27,949 ‐ 2,655 ‐ 30,604 ‐

Total 98,108 173,905 25,841 57,128 354,982

For the year ended 30 June 2016 Short‐Term

Benefits Post‐

Employment Benefits

Share‐Based Payments

Value of share based

payments as proportion of remuneration

Directors Fees

Salary and Fees

Superannuation Performance Rights

Total

$ $ $ $ $ % Directors P J Langworthy 47,407 ‐ 4,503 ‐ 51,910 ‐ A T Munckton ‐ 195,319 18,554 ‐ 213,873 ‐ D B Morgan 31,390 ‐ 2,982 ‐ 34,372 ‐ R J Cooper 31,390 ‐ 2,982 ‐ 34,372 ‐

Total 110,187 195,319 29,021 ‐ 334,527

Executives P A Bridson* ‐ 101,575 7,705 ‐ 109,280 ‐ M J Martin* ‐ 91,425 6,925 ‐ 98,350 ‐

Total 110,187 388,319 43,651 ‐ 542,157

* The positions of Mr Bridson and Mr Martin were made redundant on 30 November 2015. No termination payments other than accrued annual leave entitlements were paid.

Directors’ Report

29

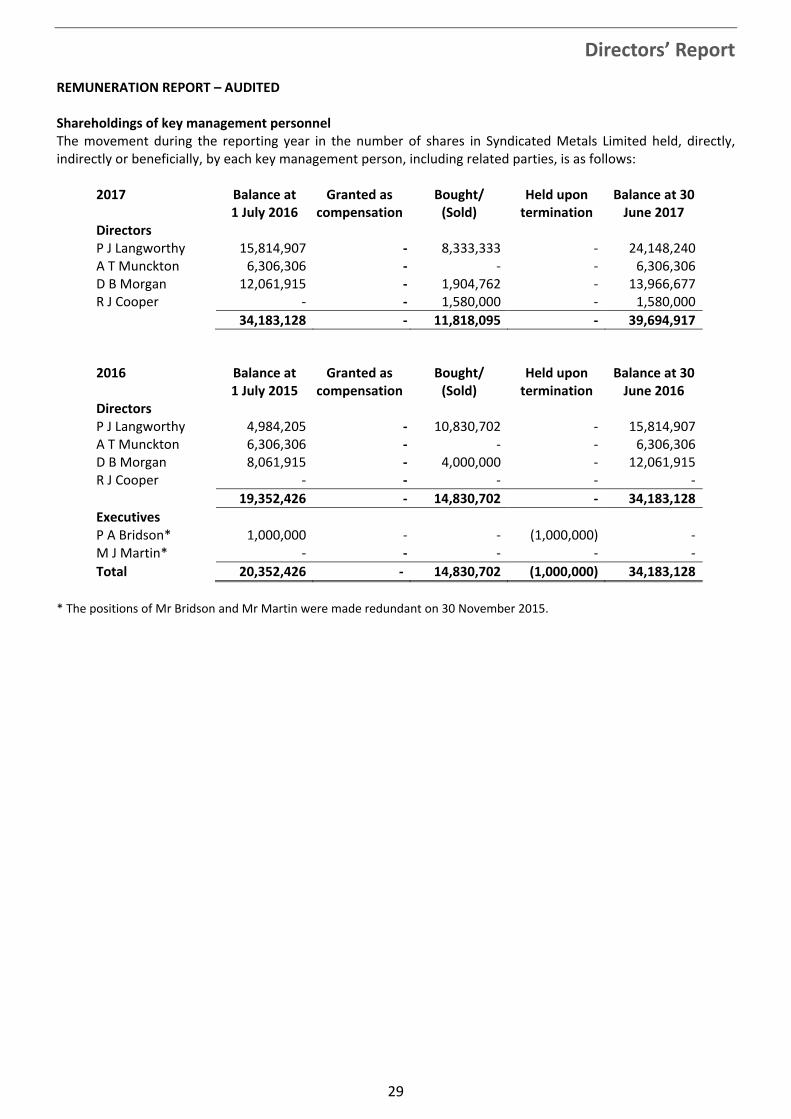

REMUNERATION REPORT – AUDITED Shareholdings of key management personnel The movement during the reporting year in the number of shares in Syndicated Metals Limited held, directly, indirectly or beneficially, by each key management person, including related parties, is as follows:

2017 Balance at 1 July 2016

Granted as compensation

Bought/ (Sold)

Held upon termination

Balance at 30 June 2017

Directors P J Langworthy 15,814,907 ‐ 8,333,333 ‐ 24,148,240A T Munckton 6,306,306 ‐ ‐ ‐ 6,306,306D B Morgan 12,061,915 ‐ 1,904,762 ‐ 13,966,677R J Cooper ‐ ‐ 1,580,000 ‐ 1,580,000

34,183,128 ‐ 11,818,095 ‐ 39,694,917

2016 Balance at 1 July 2015

Granted as compensation

Bought/ (Sold)

Held upon termination

Balance at 30 June 2016

Directors P J Langworthy 4,984,205 ‐ 10,830,702 ‐ 15,814,907A T Munckton 6,306,306 ‐ ‐ ‐ 6,306,306D B Morgan 8,061,915 ‐ 4,000,000 ‐ 12,061,915R J Cooper ‐ ‐ ‐ ‐ ‐

19,352,426 ‐ 14,830,702 ‐ 34,183,128

Executives P A Bridson* 1,000,000 ‐ ‐ (1,000,000) ‐M J Martin* ‐ ‐ ‐ ‐ ‐

Total 20,352,426 ‐ 14,830,702 (1,000,000) 34,183,128

* The positions of Mr Bridson and Mr Martin were made redundant on 30 November 2015.

Directors’ Report

30

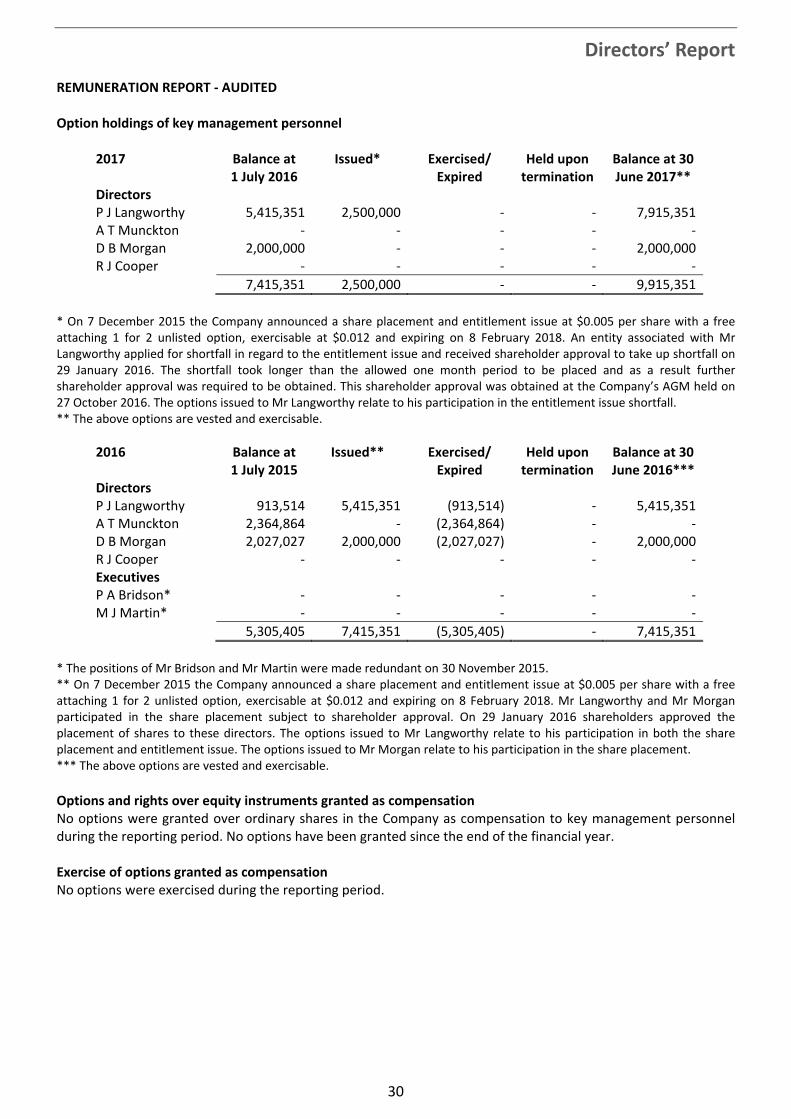

REMUNERATION REPORT ‐ AUDITED Option holdings of key management personnel

2017 Balance at 1 July 2016

Issued* Exercised/ Expired

Held upon termination

Balance at 30 June 2017**

Directors P J Langworthy 5,415,351 2,500,000 ‐ ‐ 7,915,351A T Munckton ‐ ‐ ‐ ‐ ‐D B Morgan 2,000,000 ‐ ‐ ‐ 2,000,000R J Cooper ‐ ‐ ‐ ‐ ‐

7,415,351 2,500,000 ‐ ‐ 9,915,351

* On 7 December 2015 the Company announced a share placement and entitlement issue at $0.005 per share with a free attaching 1 for 2 unlisted option, exercisable at $0.012 and expiring on 8 February 2018. An entity associated with Mr Langworthy applied for shortfall in regard to the entitlement issue and received shareholder approval to take up shortfall on 29 January 2016. The shortfall took longer than the allowed one month period to be placed and as a result further shareholder approval was required to be obtained. This shareholder approval was obtained at the Company’s AGM held on 27 October 2016. The options issued to Mr Langworthy relate to his participation in the entitlement issue shortfall. ** The above options are vested and exercisable.

2016 Balance at 1 July 2015

Issued** Exercised/ Expired

Held upon termination

Balance at 30 June 2016***

Directors P J Langworthy 913,514 5,415,351 (913,514) ‐ 5,415,351A T Munckton 2,364,864 ‐ (2,364,864) ‐ ‐D B Morgan 2,027,027 2,000,000 (2,027,027) ‐ 2,000,000R J Cooper ‐ ‐ ‐ ‐ ‐Executives P A Bridson* ‐ ‐ ‐ ‐ ‐M J Martin* ‐ ‐ ‐ ‐ ‐

5,305,405 7,415,351 (5,305,405) ‐ 7,415,351

* The positions of Mr Bridson and Mr Martin were made redundant on 30 November 2015. ** On 7 December 2015 the Company announced a share placement and entitlement issue at $0.005 per share with a free attaching 1 for 2 unlisted option, exercisable at $0.012 and expiring on 8 February 2018. Mr Langworthy and Mr Morgan participated in the share placement subject to shareholder approval. On 29 January 2016 shareholders approved the placement of shares to these directors. The options issued to Mr Langworthy relate to his participation in both the share placement and entitlement issue. The options issued to Mr Morgan relate to his participation in the share placement. *** The above options are vested and exercisable. Options and rights over equity instruments granted as compensation No options were granted over ordinary shares in the Company as compensation to key management personnel during the reporting period. No options have been granted since the end of the financial year. Exercise of options granted as compensation No options were exercised during the reporting period.

Directors’ Report

31

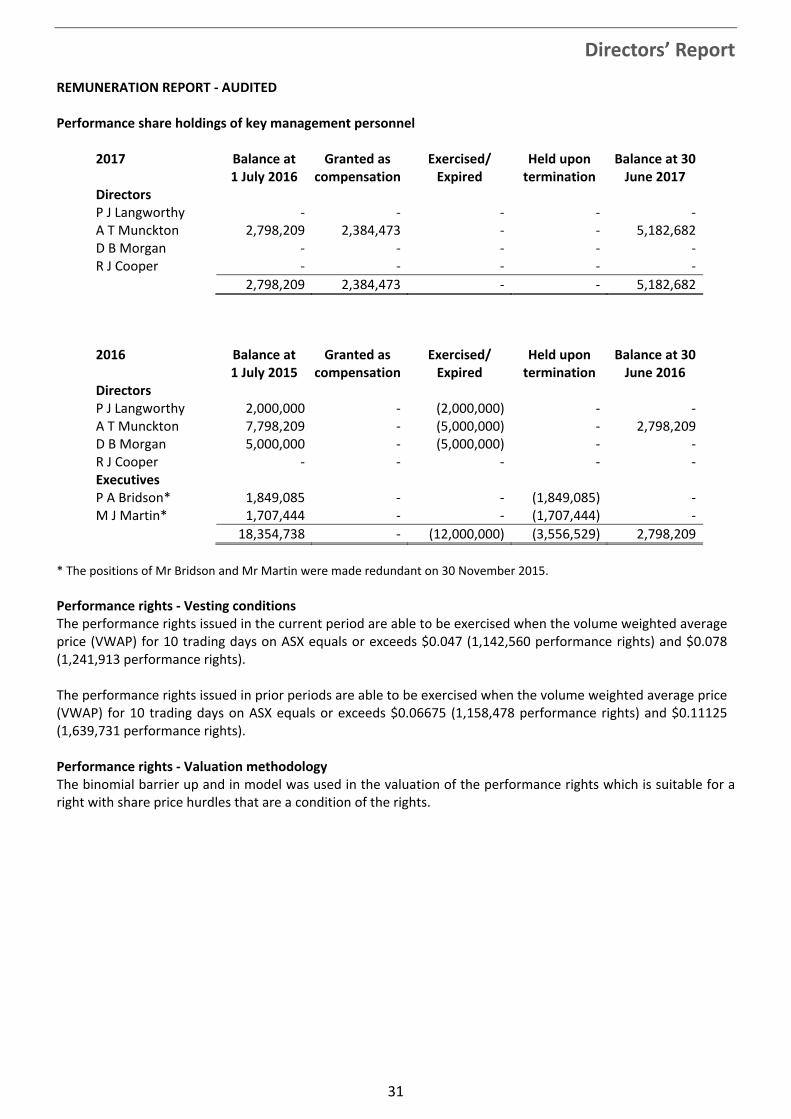

REMUNERATION REPORT ‐ AUDITED Performance share holdings of key management personnel

2017 Balance at 1 July 2016

Granted as compensation

Exercised/ Expired

Held upon termination

Balance at 30 June 2017

Directors P J Langworthy ‐ ‐ ‐ ‐ ‐A T Munckton 2,798,209 2,384,473 ‐ ‐ 5,182,682D B Morgan ‐ ‐ ‐ ‐ ‐R J Cooper ‐ ‐ ‐ ‐ ‐

2,798,209 2,384,473 ‐ ‐ 5,182,682

2016 Balance at

1 July 2015 Granted as

compensationExercised/ Expired

Held upon termination

Balance at 30 June 2016

Directors P J Langworthy 2,000,000 ‐ (2,000,000) ‐ ‐A T Munckton 7,798,209 ‐ (5,000,000) ‐ 2,798,209D B Morgan 5,000,000 ‐ (5,000,000) ‐ ‐R J Cooper ‐ ‐ ‐ ‐ ‐Executives P A Bridson* 1,849,085 ‐ ‐ (1,849,085) ‐M J Martin* 1,707,444 ‐ ‐ (1,707,444) ‐

18,354,738 ‐ (12,000,000) (3,556,529) 2,798,209

* The positions of Mr Bridson and Mr Martin were made redundant on 30 November 2015. Performance rights ‐ Vesting conditions The performance rights issued in the current period are able to be exercised when the volume weighted average price (VWAP) for 10 trading days on ASX equals or exceeds $0.047 (1,142,560 performance rights) and $0.078 (1,241,913 performance rights). The performance rights issued in prior periods are able to be exercised when the volume weighted average price (VWAP) for 10 trading days on ASX equals or exceeds $0.06675 (1,158,478 performance rights) and $0.11125 (1,639,731 performance rights). Performance rights ‐ Valuation methodology The binomial barrier up and in model was used in the valuation of the performance rights which is suitable for a right with share price hurdles that are a condition of the rights.

Directors’ Report

32

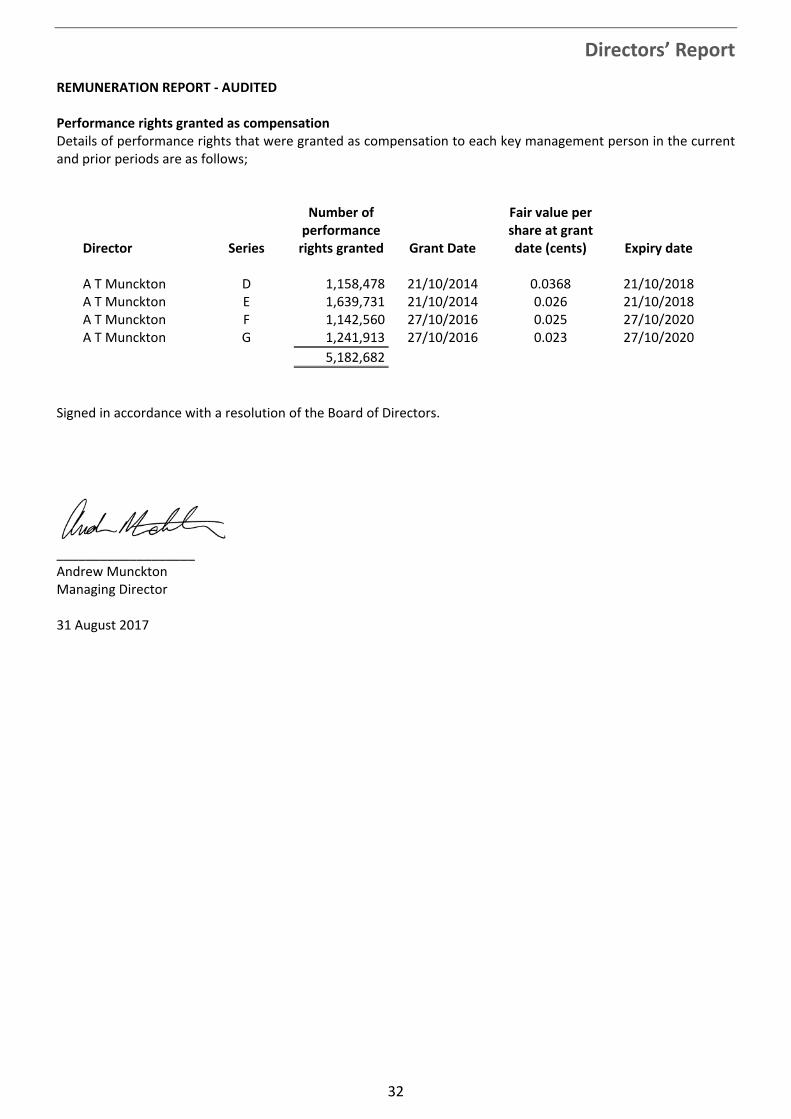

REMUNERATION REPORT ‐ AUDITED Performance rights granted as compensation Details of performance rights that were granted as compensation to each key management person in the current and prior periods are as follows;

Director

Series

Number of performance rights granted

Grant Date

Fair value per share at grant date (cents)

Expiry date A T Munckton D 1,158,478 21/10/2014 0.0368 21/10/2018 A T Munckton E 1,639,731 21/10/2014 0.026 21/10/2018 A T Munckton F 1,142,560 27/10/2016 0.025 27/10/2020 A T Munckton G 1,241,913 27/10/2016 0.023 27/10/2020

5,182,682

Signed in accordance with a resolution of the Board of Directors.

___________________ Andrew Munckton Managing Director 31 August 2017

33

AUDITOR’S INDEPENDENCE DECLARATION

TO THE DIRECTORS OF SYNDICATED METALS LIMITED

In relation to our audit of the financial report of Syndicated Metals Limited for the year ended 30 June 2017, to the best of my knowledge and belief, there have been no contraventions of the auditor independence requirements of the Corporations Act 2001 or any applicable code of professional conduct.

PKF MACK

SHANE CROSS PARTNER 31 AUGUST 2017 WEST PERTH, WESTERN AUSTRALIA

34

CORPORATE GOVERNANCE STATEMENT

The Company’s Corporate Governance Statement can be found on the Company’s website at http://www.syndicatedmetals.com.au/corporate‐governance.php, under the section marked "Corporate Governance Statements". The following governance‐related documents can also be found on the Company's website at the Corporate Governance page:

Charters Board Nomination Committee Audit and Risk Committee Remuneration Committee

Policies and Procedures Process for Performance Evaluation Policy and Procedure for Selection and (Re) Appointment of Directors Induction Program Procedure for the Selection, Appointment and Rotation of External Auditor Code of Conduct (summary) Diversity Policy (summary) Policy on Continuous Disclosure (summary) Compliance Procedures (summary) Shareholder Communication and Investor Relations Policy Securities Trading Policy

35

CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME

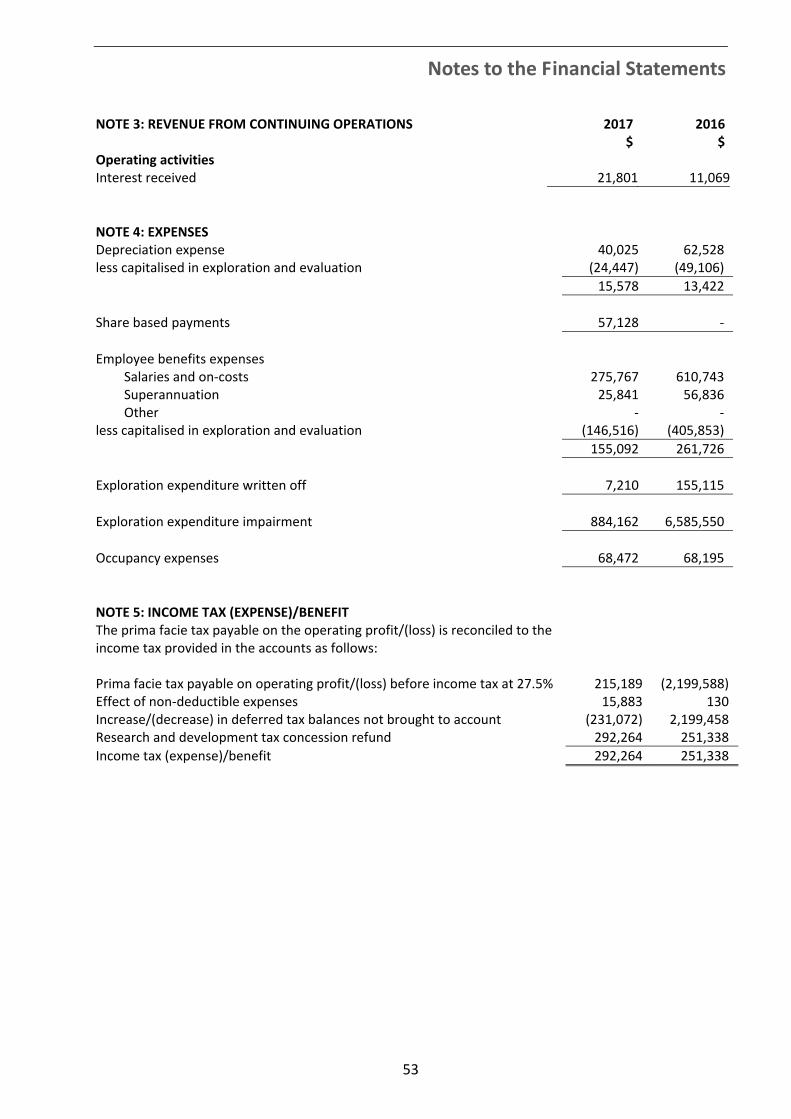

FOR THE YEAR ENDED 30 JUNE 2017

Note 2017 2016 $ $ Revenue Interest income 3 21,801 11,069 Proceeds on disposal of Barbara Copper Project 2,300,000 ‐ Sundry income 88,077 2,000

2,409,878 13,069 Expenses Administration expenses (439,730) (261,024) Occupancy expenses 4 (68,472) (68,195) Depreciation expense 4 (15,578) (13,422) Employee benefits expense 4 (155,092) (261,726) Exploration expenditure written off 4 (7,210) (155,115) Exploration expenditure impairment 4 (884,162) (6,585,550) Share based payments 4 (57,128) ‐

(1,627,372) (7,345,032) Profit/(Loss) before income tax expense 782,506 (7,331,963) Income tax benefit 5 292,606 251,338

Profit/(Loss) for the period 1,075,112 (7,080,625) Other comprehensive income ‐ ‐

Total comprehensive profit/(loss) for the year 1,075,112 (7,080,625)

Basic profit/(loss) per share (cents) 24 0.18 (1.70) Diluted profit/(loss) per share (cents) 24 0.17 (1.70)

The accompanying notes form part of these financial statements.

36

CONSOLIDATED STATEMENT OF FINANCIAL POSITION

AS AT 30 JUNE 2017

Note 2017 2016 $ $ CURRENT ASSETS

Cash and cash equivalents 6 2,634,331 514,957 Trade and other receivables 7 110,578 87,829

TOTAL CURRENT ASSETS 2,744,909 602,786

NON CURRENT ASSETS Property, plant and equipment 8 56,198 91,922 Exploration and evaluation costs 9 6,706,892 5,168,426

TOTAL NON CURRENT ASSETS 6,763,090 5,260,348

TOTAL ASSETS 9,507,999 5,863,134

CURRENT LIABILITIES Trade and other payables 10 239,082 139,086 Provisions 11 22,605 26,992

TOTAL CURRENT LIABILITIES 261,687 166,078

NON CURRENT LIABILITIES Provisions 11 12,630 6,825

TOTAL NON CURRENT LIABILITIES 12,630 6,825

TOTAL LIABILITIES 274,317 172,903

NET ASSETS 9,233,682 5,690,231

EQUITY Issued capital 12 26,187,467 23,776,256 Share based payments reserve 13 142,393 317,273 Accumulated losses (17,096,178) (18,403,298)

TOTAL EQUITY 9,233,682 5,690,231

The accompanying notes form part of these financial statements.

37

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

FOR THE YEAR ENDED 30 JUNE 2017

Issued Capital Share Based

Payments Reserve

Accumulated Losses

Total

$ $ $ $ Balance at 1 July 2016

23,776,256 317,273 (18,403,298) 5,690,231

Profit for the period ‐ ‐ 1,075,112 1,075,112Other comprehensive income ‐ ‐ ‐ ‐

Total comprehensive profit for the period ‐ ‐ 1,075,112 1,075,112

Transactions with owners, recorded directly in equity

Issue of share capital 2,559,338 ‐ ‐ 2,559,338Share issue costs (148,127) ‐ ‐ (148,127)Options and performance rights expired ‐ (232,008) 232,008 ‐Fair value of performance rights issued ‐ 57,128 ‐ 57,128

2,411,211 (174,880) 232,008 2,468,339

Balance at 30 June 2017 26,187,467 142,393 (17,096,178) 9,233,682

Issued Capital Share Based Payments Reserve

Accumulated Losses

Total

$ $ $ $ Balance at 1 July 2015

23,294,933 1,075,125 (12,080,525) 12,289,533

Loss for the period ‐ ‐ (7,080,625) (7,080,625)Other comprehensive income ‐ ‐ ‐ ‐

Total comprehensive loss for the period ‐ ‐ (7,080,625) (7,080,625)

Transactions with owners, recorded directly in equity

Issue of share capital 525,992 ‐ ‐ 525,992Share issue costs (44,669) ‐ ‐ (44,669)Options expired ‐ (757,852) 757,852 ‐Fair value of performance rights issued ‐ ‐ ‐ ‐

481,323 (757,852) 757,852 481,323

Balance at 30 June 2016 23,776,256 317,273 (18,403,298) 5,690,231

The accompanying notes form part of these financial statements.

38

CONSOLIDATED STATEMENT OF CASHFLOWS

FOR THE YEAR ENDED 30 JUNE 2017

Note 2017 2016 $ $ Cash flows from operating activities Interest received 20,074 18,475Payments to suppliers and employees (622,274) (634,081)Payments for exploration and evaluation (2,053,740) (1,341,476)Sundry income 88,077 2,000R&D income tax benefit 292,606 251,338

Net cash used in operating activities 15 (2,275,257) (1,703,744)

Cash flows from investing activities Purchase of plant and equipment (4,301) (2,378)Proceeds from joint venture partner ‐ 10,442Purchase of tenements (20,000) ‐Purchase of Monument Exploration Pty Ltd 26 (49,979) ‐Proceeds from sale of Barbara Copper Project 2,300,000 ‐

Net cash from investing activities 2,225,720 8,064

Cash flows from financing activities Proceeds from issue of shares 2,317,038 525,992Funds held in trust for share issue requiring shareholder approval ‐ 25,000Capital raising costs (148,127) (45,885)Payments for security deposits ‐ (340)