20161215_innovation_lifecyle_funding_derek_henry_andrew_bourg_bdo

TRANSCRIPT

Innovation Lifecycle Funding

Derek Henry & Andrew Bourg

15 December 2016

2

Derek Henry

Tax Partner and Head of R&D Tax Services

Andrew Bourg

Partner- Corporate Investment and Business

Advisory

INTRODUCTION

Innovative Tax Incentives

EIIS PP EIIS Fund

ENTREPRENEUR/

RETIREMENT

RELIEFSTART UP EXEMPTION

SURE

TAX SUPPORTS AND THE CAPITAL LIFECYCLE

R&D

KDB

&

S.291 A

Focus of Presentation

R&D Success KDB

Research and Development Tax Credits –

Incentives for Innovation

BENEFITS

25%

12.5%

Effective tax saving of 37.5%

EXAMPLE CALCULATION

31 December 2015

Qualifying R&D Expenditure

€400,000

Credit @ 25%

= €100,000

USING THE CREDIT

Year Year 1 Year 2 Year 3

Prior year CT Current year CT

- Year 1 excess

Year 2 CT Year 3 CT

Year 1 excess

33.5%

Balance Refunded50% Refund

67% Balance

33% Refund

Year 1 excessYear 1 excess

R&D KEY EMPLOYEE

TWO TESTS

SCIENCE TEST

Qualifying Activity

Sci/Tech Uncertainty

Sci/Tech Advancement

Systematic

Investigative

Experimental

Field of Science

Basic Research Applied Research

Experimental Development

SCIENCE TEST

Types of Activities

SCIENCE TEST

In a Field of Science

1. Natural Sciences

2. Engineering and Technology

3. Medical Sciences

4. Agricultural Sciences

SCIENCE TEST

SYSTEMATIC, INVESTIGATIVE AND EXPERIMENTAL ACTIVITIES

1 • Planned

2 • Logical Sequence

3 • Records

4 • Dated

5 • Evidence of Activities

6

• Measures of Scientific/Technical Properties

SCIENCE TEST

Advancement

Existing

Technology

Base

SCIENCE TEST

Uncertainty

Can?

How?

Page 18

R&D Process (generally)

Routine Process (generally)

Page 19

R&D Process (generally)

Information focus should

be placed here!

UNCERTAINTY IN PRACTICE

R&D – FOOTPRINT REDUCTION

‘divide by’ and implement

R&D

POTENTIAL R&D – COMPUTER SCIENCE

NON-R&D – COMPUTER SCIENCE

ACCOUNTING TEST

Allocations

Records

Commencement and Termination

Project plan

Personnel

QUALIFYING COSTS

“The tax credit will be available in respect of expenditure incurred –

• In the carrying on

• By it

of research and development activities….”

Revenue

Capital

Plant and Machinery

Sub contracted activities (limited) –concessionary treatment

Interest not allowed

EXPENDITURE ON BUILDINGS AND STRUCTURES

35% of building must be used for R&D for 4 years

Clawback period 10 years

DOCUMENTATION

CLAIMS PROCESS

REVENUE REVIEW

COMMON MISTAKES

DocumentationQualifying Activity

Complete R&D

Claim

Qualifying Claim

Revenue Review

Tax Return

Qualifying Costs

Knowledge Development Box

DEREK HENRY

15 December 2016

BUDGET 2015

WHAT IT IS TO BE?

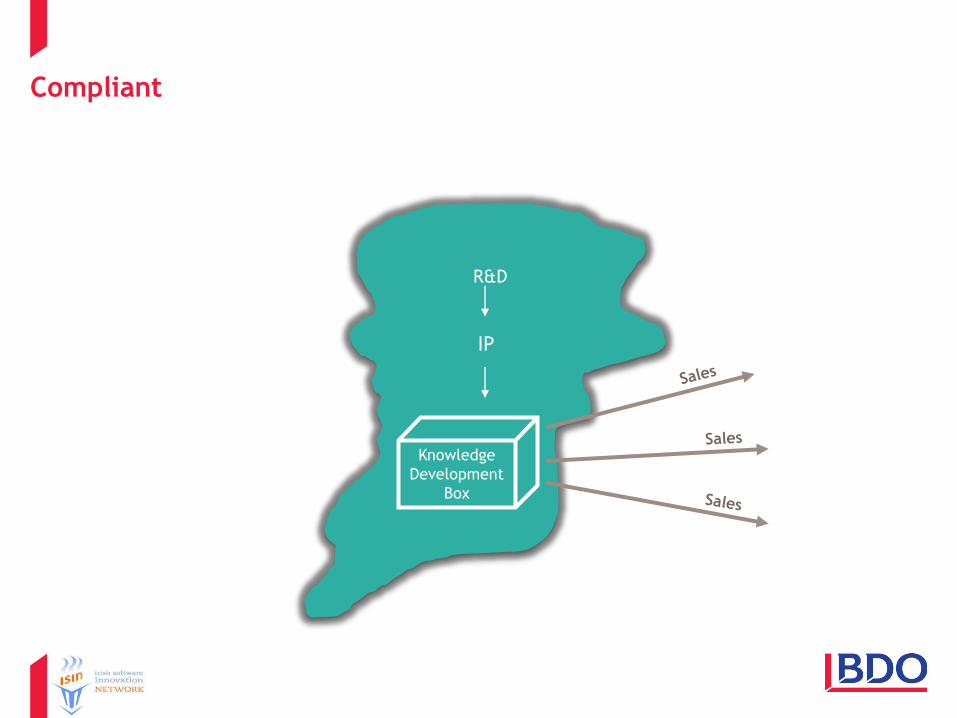

COMPLIANT

Non- Compliant

R&D

IP

Patent

Box

Low tax

COUNTRY A COUNTRY B

Compliant

R&D

IP

Knowledge

Development

Box

PUBLIC CONSULTATION

January 2015

FEEDBACK STATEMENT

July 2015

What is the relief?

Summary of Relief

Carry on R&D

Resulting in Qualifying Asset

Trading Income from Qualifying Asset

KDB Allowance

Corporation Tax on Profits 6.25%

Legislation

KDB Section 769G– Section 769R TCA 1997

• Section 32 Finance Act 2015

• Effective 1 January 2016

KDB ( Certificate of Inventions) Bill 2016

• Still Draft

New Patent Act re Examinations

What’s in the box?

KDB

2. Qualifying

Assets

4. Specified

Trade

5. Calculation of

Profits

6. KDB

Allowance

7. Tracking and

Tracing

1. Qualifying

Expenditure on

R&D activities

3. Qualifying

Income

What’s in the box?

Qualifying Patent cont’d

Registration versus substantive examination

Patent Granted Required System

Pre 1 January 2016 Registration if full

search carried out by

Patent Office

1 January 2016 – 31

December 2016

Registration if full

search carried out by

Patent Office

Patent Agent Cert

Post 1 January 2017 Substantive

Examination

Not A Qualifying Asset

Short-term Patents

Petty-patents

Utility models

Marketing Related IP

Computer Program

In section 769G(1) the definition of intellectual property, for the purposes of the KDB,

includes:

(a) a computer program, within the meaning of the Copyright and Related Rights Act

2000, but, where a computer program is a derivative work or adaptation, the portion

of

the computer program that represents the derivative work or the adaptation of the

original work and the original work shall be treated as two separate computer

programs,

Section (2) Copyright and Related Rights Act 2000 defines a computer program as:

…a program which is original in that it is the author's own intellectual creation and

includes any design materials used for the preparation of the program

IP for SMEs the 3rd Category

…inventions that are certified by the Controller of Patents, Designs and Trade

Marks as being novel, non-obvious and useful;

New Legislation

• Knowledge Development Box (Certificate of Inventions) Bill 2016

SME Definition

IP T/O < €7.5m (12 months)

Group T/O < €50m and

Micro, small or medium

Family of Products

• No. of Qualifying Assets

• Interlinked

• Reasonable to conclude not possible to id overall expenditure or income from

each QA

• Family of Assets = smallest grouping that can be identified

Family of Assets Example

• Family of assets based on sales (TV)

• Family of assets based on R&D (IT)

IP location

R&DLegal title

IP

Other Country

IP Held

Beneficial

Interest

Income

Qualifying Expenditure

Uplift Expenditure

Profits of Specified

Trade

Qualifying Profits

Overall

Expenditure

Modified Nexus Formula

managing, developing, maintaining,

protecting, enhancing or exploiting …

the researching, planning, … other similar

activity leading to ...

Sale of goods

or services

deriving

value…

•Direct income

•Embedded Royalty

Overall Income from

QA

Overall Income from

QA

Expense and Capital

Allowances of Specified Trade

•Just and reasonable allocation

Qualifying Profits

Modified Nexus Formula

Qualifying Expenditure

Uplift Expenditure

Profits of Specified

Trade

Qualifying Profits

Overall Expenditure

R&D Expenditure

• Creation

• Development or

improvement

• 3rd Party outsourcing

Acquisition cost &

related party

outsourcing

• 30% of QE

or

• acquisition costs &

group outsourcing

All of above plus

• total acquisition cost,

• total Group outsourcing

• other Non-Qualifying expenditure

The Relief

After capital

allowances,

before losses

INTERACTION WITH OTHER TAX RELIEFS

Section 766 TCA 1997

Tax Credit for Research and Development Expenditure

Section 291A TCA 1997Intangible Assets

Loss relief

Double Tax Relief

Collaborative Research

Knowledge Transfer Ireland

•Wholly industry-funded

•Partially industry-funded

•Assignment of Foreground IP

•Assignment of Non-several IP

•Licence of Foreground IP

•RPO Background IP

Enterprise Ireland’s Technology Centres

• Incurred by company in carrying out R&D = QE

•MV of licence payments = Acquisition costs

Documentation

Section 769L

• Have available all such records as may reasonably be required

• Records to cover tracking of:- Overall income

- Qualifying expenditure and

- Overall expenditure,

in relation to qualifying assets

• Family of assets - Commonality of science

- Consistency of methodology

- Nexus between expenditure and family of assets or

- Choice of family which creates the nexus

• Derivations

• Retain for 6 years after last year of claim

Sample Computation

KDB Co develops and sell a smart

TV. Within the TV is a computer

program which was developed a

number of years ago at the below

cost. It is estimated that this

program represent 20% of the

sales value of the TV.

Cost type €000

In house R&D 2,500

Purchased IP 500

Group outsourcing

cost

400

In the year ended 31 December 2016, KDB

company had the following results:

€000

Sales 10,000

Cost of Sales 3,000

Gross Profit 7,000

Administration 1,500

Net Profit 5,500

Sample Computation

Step 1- Work out specified trading profits

€000Specified

Trade

General

Trade

Sales 10,000 2,000 8,000

Cost of Sales 3,000 600 2,400

Gross Profit 7,000 1,400 5,600

Administration 1,500 300 1,200

Net Profit 5,500 1,100 4,400

Sample Computation

Step 2- Apply modified nexus formula to determine Qualifying Profits

Qualifying Expenditure

Uplift Expenditure

Profits of Specified

Trade

Qualifying Profits [QA]

Overall Expenditure

QE= €2,500,000

UE= €400,000 + €500,000 = €900,000

or €750,000

OE= €2,500,000 + €400,000 + €500,000 =

€3,400,000

Specified trade profits = €1,100,000

QA= (€2.5m+€0.75m)/€3.4m x €1.1m =

€1,051,470

Sample Computation

Step 3- Work out KDB allowance

• 50% of qualifying profits

• €1,051,470 * 50% = €525,735

Sample Computation

Step 4 - Complete Tax Computation

Specified

Trade

General

TradeTotal

Profits per

accounts 1,100,000 4,400,000

KDB allowance525,735 -

Taxable

profits 574,265 4,400,000

Tax at 12.5%71,783 550,000 621,783

Proof Taxable Tax

Taxable

profits1,100,000

6.25% 1,051,470 65,717

12.50% 161,766 20,221

12.50% 4,400,000 550,000

621,783

Transitional Measures

1 January 2016- 31 December 2019

• Acquisition costs pre 1 January 2016

• Group outsourcing pre 1 January 2016

• QE on QA = QE in the last 48 months

After 1 January 2020

• Acquisition costs pre 1 January 2016

• Group outsourcing pre 1 January 2016

• No QE on QA incurred pre 1 January 2016

Time Limits

24 Months

SMEs

• 10% Notional Royalty

• 3rd Category of Asset

• Documentation

Case Study

Case Study

ICT Limited

Trading for 5 years in high end software development/platform design.

The company has decided to develop a completely new payments platform, which is

compatible with internal legacy systems, cross browser compatible and provides high

processing efficiency (i.e. fast processing speed and high scalability).

It believes the development of this new platform will drive its business in the current

market.

ICT Limited has prepared a detailed business plan which is included below. It is

anticipated that the project will create 5 new jobs during the development phase.

The result of the R&D will be copyright software.

Case Study

Business plan

Year

R&D

expenditure

IP acquisition

costs Other costs Total Costs

Expected

Revenue

Gross Funding

Requirement Cumlative

1 650,000 100,000 50,000 800,000 0 800,000 800,000

2 200,000 150,000 350,000 -200,000 150,000 950,000

3 50,000 200,000 250,000 -500,000 -250,000 700,000

4 25,000 250,000 275,000 -1,000,000 -725,000 -25,000

5 25,000 250,000 275,000 -2,500,000 -2,225,000 -2,250,000

6 25,000 250,000 275,000 -2,750,000 -2,475,000 -4,725,000

975,000 100,000 1,150,000 2,225,000 -6,950,000 -4,725,000 -9,450,000

Case StudyStep 1

Work out Net funding requirement

R&D costs 975,000

EI R&D Grant -50,000

R&D tax credit -231,250

Real cost of R&D 693,750

IP Acquisition costs 100,000

100,000

Other costs 1,150,000

EI Feasibility Grant -25,000

1,125,000

Net Funding Requirement 1,918,750

Tax credits etc. need to be calculated annually. For illustrative purposes we have ignored this and

the implications of same.

Case StudyStep 2

Work out after Tax Repayment Capacity

Modified Nexus

Total Income -6,950,000

Total Expense 2,225,000 Specified profits (SP) -4,725,000

Net Profit -4,725,000 QE 975,000

OE 1,275,000

Addback Acq costs -100,000 UE 0

S 291A SIA 100,000

QA= SP x

(QE+UE)/OE -3,613,235

Taxable profits -4,725,000 KDB Allowance

50% of QA 1,806,618

KDB Allowance 1,806,618

Net Taxable profits -2,918,382

Tax at 12.5% 364,798

Net repayment capacity €4,360,202

Case Study

Tax Measures Effects

Reduction in funding requirement 231,250

Reduction in tax liability

S 291A 100,000

KDB 1,806,618

1,906,618

At 12.5% 238,327

Tax effect of Innovation Tax Measures 469,577

FUNDING OPTIONS

PRESENTATION TO

IRISH SOFTWARE INNOVATION

NETWORK

Andrew Bourg15th December 2015

OVERVIEW OF FUNDING MARKET

Currently manage the following Funds:

The BDO Development Capital Fund; and

Davy EIIS Fund.

Andrew Bourg

Investment Director

OVERVIEW OF FUNDING MARKET

1. Funding landscape

2. Financing options available

3. Accessing Funds

CHANGING FUNDING MARKET

What’s driving the change?

Irish SMEs reliant on banks

Disproportionately exposed to potential weaknesses in

the banking sector

Demand for alternative sources of Funding

SME growth increasing demand

SME Funding Requirement

Market Sentiment SMEs ICT Sector

Optimistic about the prospects for

their businesses in the coming year

82% 81%

Expecting revenue growth 85% 94%

Plan to hire more staff 60% 75%

Expect increase in growth in capital

/ R&D spend

51% 67%

GOVERNMENT

VENTURE CAPITAL

DEVELOPMENT

CAPITAL

EIIS & HNWI

PRIVATE EQUITY

SEED CAPITAL

LOAN GUARANTEE

SCHEME

TRADITIONAL

COMMERCIAL

FINANCE

SBCI

CREDIT FUNDS

EQUITY DEBT

NPRF / ISIF

ENTERPRISE IRELAND

R&D GRANTS

MICROFINANCE

IRELAND

COUNTY &

ENTERPRISE

BOARDS

FUNDING SOURCES

Bank Funding

• BOI - €12 billion to SMEs over the next 5 years

• AIB - Range of dedicated SME funds launched

over last 2 years

• Ulster Bank now “core” to RBS Group

• Strategic Banking Corporation of Ireland (“SBCI”)

What will SBCI do for SMEs?

• Lower cost of funding

• Provide loans of longer term

• More appropriate T&Cs

• Promote greater competition

IN SUMMARY – DEBT PROVIDERS

• Over reliance on Banks

• Re-capitalised & investment

• Key role

• Alternative funding sources

Size Fund Manager Investment/

Loan Amt

E350m

EQUITY/DEVELOPMENT CAPITAL FUNDS

Focus

SME Credit Fund

SME Equity Fund Carlyle Capital

E450m BlueBay Capital E5m-E45m Mid-Large Co’s

E2m-E50m

BDO Development Capital Fund

Development

CapitalE2m-E10mMid-Size Co’s

Mid-Large Co’s

E75m

MML E2m-E10mMid-Size Co’s E125mGrowth Capital Ireland Fund

NPRF BACKED GROWTH FUNDS

ENTERPRISE IRELAND BACKED

GROWTH FUNDS

Market Opportunity

Clear Strategy

Effective Management

Strong Governance

Risks Identified

Financial Model

Commercial risk adjusted

Return

What are funding providers

looking for?

Requirements for raising finance?

Typical requirements:

– Business plan / information memorandum

– Financial projections/assumptions

– Management team overview

Dealing with private equity providers:

Overview of the process

Prepare an information

memorandum

Contact private equity

providers / Teaser

Present

Receive

offers

Negotiate and

second round offers

Accept offer

Due diligence

Final negotiatio

ns and deal close

• RAISE FUNDS IN

ADVANCE

• AVOID SHORT TERM

FINANCING PRESSURES

• ENSURE YOU MATCH

FUNDING TO FUNDER

• SUSTAINABLE CAPITAL

STRUCTURE

• DEVELOP ROBUST

FINANCIAL PLAN & BE

REALISTIC

• DISCUSS IN DETAIL WITH

ADVISER IN ADVANCE

Key Challenges - & how to

overcome them?

ACCESSING

FINANCE

IDENTIFY RISKS

SLOW PROCESS

POOR

PREPARATION &

INFORMATION

IDENTIFY TYPE

FUNDING• IDENTIFY KEY

TRADING RISKS

• SHOW WHAT

ACTIONS COMPLETED

TO MITIGATE

PRESENTATION TO

IRISH SOFTWARE INNOVATION

NETWORK

THE FUND

• The BDO Development Capital Fund

• €75 million

• Development and growth capital

• Established and export focussed SME’s

• Managed by Development Capital

OUR APPROACH

Development Capital’s Smart Funding Model

Experience and support

INVESTMENT TEAM

Knowledge and understanding

ADVISORY PANEL

FUNDING PARTNERS

Funding and advice

TARGET COMPANIES

• Established and profitable companies

Revenues between €10m and €50m+ p.a.

Ambitious management teams

Significant growth opportunities

TARGET SECTORS

• Key Investment sectors

ICT & Software

Food & Agri

Industrial (including Engineering & traditional Manufacturing)

Life Sciences (including Medical Devices) and Clean Tech

FUND OFFERING

• Investment amounts between €2 - €10 million

• 5 year investment term

• Flexible transaction instruments; equity, equity/debt

mix

SUMMARY OF PROCESS

Information required for initial assessment

i. Latest management & audited accounts

ii. Summary of growth opportunity

iii. Overview of management team & credentials

Turnaround time: Between 5-10 days

INVESTMENTS COMPLETED TO DATE

INVESTMENT CASE STUDY

MAIN INVESTMENT TERMS

Terms

Investment amount €8 million

Investment instrument €8 million for Ordinary Shares

Use of funds Acquisition of complimentary

businesses in the UK market.

TIME LINE PROCESS

February/March

2014

April 2014 May 2014 June 2014 July 2014

Assessment & meetings

Signed

term sheet

- 30th April

Diligence

Financial, Legal, Tax & Commercial

SPA & Shareholder Agreement

Investment

Committee Approval

Completio

n – 30th

June

Advisory Panel input

― IT services company providing outsourced IT solutions including:

• Managed Services &

• Business Application Services

― Diversified & blue chip customer base

• c. 70% private sector

• c. 30% public sector

― Strong track record of organic growth• Customer retention &

• “Pull through” revenues

― UK acquisition strategy

• 2 acquisitions completed in 2013

KEY CHARACTERISTICS

Broad Criteria (/ X)

Revenues €10 million+ p.a.

Scaling companies (revenues €5m - €7m p.a.)

Profitable

Ambitious & capable management team

Export led growth opportunities

TARGET COMPANY PROFILES

(i) Mid-sized, high growth indigenous companies Substantial & rapidly growing revenues of €10m - €50m+ p.a. Profitable Export market opportunities

(ii) Scaling companies Turnover of c. €5 - €7 million p.a. (achieved in a short period

of time) Growth opportunities Financial alternative to premature early stage sell-out

(iii) Established businesses / possibly family owned Need for not only capital but also internal change MBO/MBI Generational change or key management team changes

TARGET COMPANY PROFILES

(iv) Internationalised businesses e.g. Successful track record Want to pursue export opportunities

(v) Expansionary companies e.g. Opportunities for strategic acquisition / mergers as routes to

new markets

OVERVIEW OF THE INVESTMENT

PROCESS

Indicative Timeframe minimum 8 weeks subject to #2

1. Proposed investment terms i.e. term sheet

2. Information request list

3. Commercial, legal, tax and financial due diligence

work programme

4. Investment proposal & presentation to Investment

Committee

p

A

R

A

L

E

L

L5. Investment legal agreements – shareholder

agreements etc.

The Davy BES & EII Tax Relief Fund

Irish Software Association

BACKGROUND - BUSINESS EXPANSION SCHEME

Introduced 1984

Incentive for private investors

Long term equity capital

Two methods to raise EII funds

1. Private Placing (friends and family); or

2. Designated Investment Fund e.g. The Davy EII Tax Relief Fund

What is the Employment & Investment Incentive Scheme (“EII

Scheme”)

The reformed and renamed Business Expansion Scheme (BES)

Government reviewed 2010 and 2014

Summary of main changes:

COMPANIES

Increased investment limits

Wider scope; available to the

majority of SME’s

Investment term

INVESTORS

More attractive return

Davy BES/EII Funds – Key Statistics

― Longest running BES/EII Fund manager in the Country

― Raised 23 BES/EII Funds (4) amounting to €140 million

since 1995.

― Invested in c. 146 qualifying SME’s- 26 Counties

― Investment range from €250,000 - €2 million.

― c. €40 million of Funds under management.

― c. 56 investee companies employing over 2,000

people.

― Co-invested with Banks, Enterprise Ireland & Private

investors.

― Funds invested in all industry sectors.

Investee Company Examples

Food & Agri

Traditional Manufacturing

Renewables

Millions of tons composted

ICT & Software

Investment Sector Analysis- Number of Companies

50

3823

2213

1. TraditionalManufacturing

2. ICT & Software

3. Food & Drink

4. RenewableEnergy/EnvironmentalServices

Advantages of EII finance

― Investment Limits

€15 million* limit per company (previously €10m)

€5 million* in any 12 month period (previously €2.5m)

Competitive fixed cost of finance for 4 years*

Investment is Equity and therefore reduces gearing levels

Existing owners retain control of the business

No capital repayment for 4 years*

May trigger additional funding e.g. Banks or other private investment

*Subject to EU Commission Approval of 2014 Budget changes

Assessment criteria for The Davy EII Funds

Funds Criteria/Investment mandate

Established companies with a 3-5 year strong trading record

Capable and experienced management team

Companies involved in growth sectors and/or with growth potential

Positive net asset value and low gearing levels

Ability to repay investment after 4 years

Typical timeframe 8-12 weeks.

Investment Process— Fact find/Management team meeting

— Proposed investment terms i.e. heads of terms/deal sheet

— Information request list

— Commercial, legal and financial due diligence work programme

— Revenue investment approval

— Investment proposal & presentation to Board of BES Management Ltd

— Investment legal agreements

Investment legal documents & Cost of funds

Investment Structure

1. New Ordinary shares

2. No preferential rights

3. 4 year investment term

4. Capped return

5. No guaranteed exit mechanism

Typical legal documents

1. New articles of association

2. Share subscription agreement

- Covenants

3. Put and call option agreement

Cost of funds – range between c.5% - c.8% fixed p.a.

The Davy BES & EII Tax Relief Fund

Investment Case Studies

Specialises in designing student management and recruitment software

systems for higher education institutes in UK and Ireland

Offers 3 licensed software solutions including

Admissions and Registrar

Student Information Systems

Analytics

Software integrates with existing student record system

Customers

“Leading US software unit spends €10m on CampusIT”

Leading provider of general practice and pharmacy software across the UK

and Ireland

Formed in 2006 following merger between Medicom and Systems Solutions

Software

Products include Dispensary Software, EPOS and Special Healthcare

Software

Customers include

Community and Hospital Pharmacies

Primary Care GPS and Private Consultants

“Helix Health raises €9m investment to expand its

business”

Q&A

Points of Contact

Andrew Bourg

Partner, Corporate Investment & Business Advisory

Tel: 01 4700470

Email: [email protected]

Derek Henry

Tax Partner, Head of R&D Tax Services

Tel: 01 4700211

Email: [email protected]