2016 software sector outlook - rbc insight

TRANSCRIPT

EQU

ITY

RESE

ARC

H RBC Global Equity TeamClick here for contributing analysts' contactinformation

December 18, 2015

2016 Software Sector OutlookWe remain optimistic and biased towards next-gen software withmargin expansionStay long the SPAWNS in 2016: Although our software universe as a whole was effectively flat vs themarket in 2015, large-cap software was dominated by names such as PANW +53%, CRM +33%, ADBE+31%, NOW +29% and MSFT +21%. Similar to 2015, a core tenet in picking our favorite names is next-generation/disruptive software or names that have reinvented themselves coupled with improvingmargins. We don't see a change to that thesis in 2016 and expect the SPAWNS (Salesforce, Palo Alto,Adobe, Workday, ServiceNow, Mr. Softy (Microsoft) and Splunk) to outperform again.

Sector view expectations for 2016: (1) Stay long SaaS applications: We remain bullish on the group asa disruptor of legacy tech and are modeling 24% growth driven by CRM, HCM, Financials, vertical SaaSsolutions and analytics. Consolidation through M&A and increased IPO activity are likely to remain afocus. (2) Still optimistic on Security, but stay selective: We are modeling 12% growth, and excludingCHKP and SYMC are modeling a more bullish 25% growth. We expect 2016 to be another good year forsecurity, with a greater focus on consolidation and endpoint security as increased regulation could helpthe sector. (3) Legacy Infrastructure feels the pain of the hybrid/public cloud as we remain cautious:We are bearish towards the legacy names in the group and are modeling 2% growth as concerns lingeraround the negative impact of the hybrid/public cloud to infrastructure software. We remain positive/optimistic on next-gen infrastructure names.

Top themes for software in 2016: (1) Margins matter more: Stock performance has depended onpositive margin out-performance in addition to revenue growth. (2) 2016 could be a tipping point forstrategic M&A: A number of factors are converging that could make 2016 a significant year for strategicM&A in software. (3) All apps to the cloud: The progression of apps to the cloud continues, thoughnot all at the same pace. (4) Data as a differentiator: The most innovative cloud application playersare differentiating offerings through unique data insight. (5) Amazon moves to the app layer: Amazonhas moved from compute and storage to database and could start to attack the app layer. (6) Shiftingpriorities for cyber-security: 2016 could see more vendor consolidation at the high end and focus ondifferentiated best-of-breed solutions, especially endpoint-based solutions. (7) Shift to the cloud shouldcontinue to be deflationary to legacy infrastructure vendors: Next generation software should continueto pull spending from legacy infrastructure vendors that face deflationary trends. (8) Value emergesas the IoT market starts to materialize: This attractive, but nascent market has begun to materialize,which could create real value for software companies and investors. (9) Focus on the next-generationdisruptors: In addition to public cousins, there are a number of emerging private companies that couldhelp shape the tech landscape.

Favorite large cap names: (1) ADBE: Strong growth and conservative cost expectations, (2) CRM:Consistent execution, expanding margins and still a large TAM, (3) MSFT: A reinvigorated juggernaut -the pivot to growth coming (4) NOW: ERP for IT and so much more, (5) PANW: Next-gen security couldconsolidate spend, (6) SPLK: Could see a reversion in 2016 with accelerating results and (7) WDAY: 2016the year for financials take off, margin upside potential.

Favorite SMID cap names: (1) DWRE: A reasonable guide to FY/16 sets the stage for a good year, (2)ELLI: a 2H16 re-acceleration story, (3) HDP: Once in a decade data replatforming opportunity, (4) MIME:Attractive opportunity and below-peer valuation, (5) PFPT: Best in class Security-as-a-Service, (6) QLIK:Early success of Qlik Sense and easy comps, (7) SHOP: Multi-quarter inflection for fundamentals and (8)ZEN: Rapid growth, CFFO improvement and expanding product set.

Priced as of prior trading day's market close, EST (unless otherwise noted).All values in USD unless otherwise noted.

For Required Conflicts Disclosures, see Page 79.

Table of contents

2015 in Review: Software ..................................................................................................... 3

Software slightly outperforms S&P 500 in 2015 ........................................................................ 3

2015 much like last year for large-cap software ........................................................................ 5

Balanced returns for growth vs. value/GARP software .............................................................. 7

2015 was again a tougher year for smid-cap software .............................................................. 7

Largest outperformers for 2015 across all market caps .......................................................... 10

Largest underperformers for 2015 across all market caps ...................................................... 12

Mixed performance from the IPO class of 2015 ...................................................................... 13

2016 Software Spending Outlook ....................................................................................... 15

Stay long Software-as-a-Service (SaaS): expect 24% growth or better .................................... 15

Still optimistic on Security software, but stay selective: expect 25% plus growth excluding CHKP and SYMC ........................................................................................................................ 16

We remain more bearish on legacy Infrastructure and more optimistic/bullish on next-gen names: overall expect low-to-mid single digit growth ............................................................. 17

Top Themes in 2016: Software ........................................................................................... 18

1) Stock theme: margins matter .............................................................................................. 18

2) Could 2016 be a tipping point for strategic M&A? .............................................................. 23

3) Tech theme: All apps to the cloud ....................................................................................... 27

4) Tech theme: Data as a differentiator ................................................................................... 31

5) Tech theme: Amazon to the app layer ................................................................................. 36

6) Tech theme: Shifting priorities for cyber-security ............................................................... 42

7) Tech theme: Shift to the cloud should continue to be deflationary to legacy infrastructure vendors ..................................................................................................................................... 45

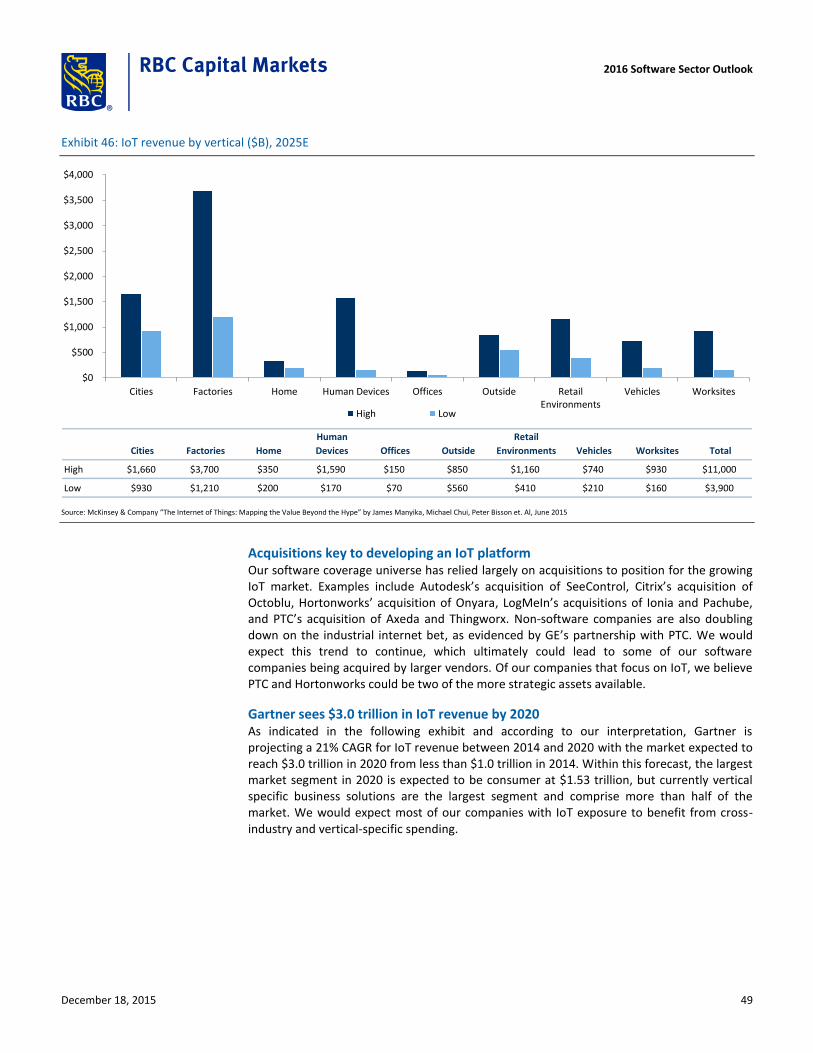

8) Tech theme: Value emerges as the IoT market starts to materialize .................................. 48

9) Tech theme: Focus on next-generation disruptors .............................................................. 53

Looking at 2017 estimates .................................................................................................. 58

Top Ideas for 2016 .............................................................................................................. 60

2016 Software Sector Outlook

December 18, 2015 2

2015 in Review: Software In a year where software was flat vs. the market, next-generation/disruptive names or those that reinvented themselves dominated Although our software universe as a whole was effectively flat vs the market in 2015, large-cap software was dominated by names such as PANW +53%, CRM +33%, ADBE +31%, NOW +29% and MSFT +21%. Similar to 2015, a core tenet in picking our favorite names is next-generation/disruptive software or names that have reinvented themselves coupled with improving margins. We don't see a change to that thesis in 2016 and expect the SPAWNS (Salesforce, Palo Alto, Adobe, Workday, ServiceNow, Mr. Softy (Microsoft) and Splunk) to outperform.

Software slightly outperforms S&P 500 in 2015

As of December 16, our coverage universe (+2.8%) outperformed the S&P 500 (+0.7%), but trailed the NASDAQ composite (+7.1%) on a market cap-weighted basis in 2015. Outperformance was more balanced across market cap in 2015 vs. 2014, when nine of 15 large-cap ($10B+) stocks were up more than 20%. In 2015, only six of 15 large-cap stocks were up more than 20% while seven of 31 small-to-midcap stocks were up more than 20%. In total, 11 of 15 large-cap stocks had positive returns while 15 of 31 small-to-midcap stocks had positive returns. In total, 20 of 46 stocks in our coverage universe outperformed the NASDAQ while 26 of 46 stocks outperformed the S&P 500.

In the mega-cap space, Microsoft and Oracle were up 24% and 18%, respectively, in 2014. In 2015, Microsoft was up 21% while Oracle was down 13%.

Elli Mae was the best-performing stock in our coverage universe, up 58% vs. +50% in 2014.

After Elli Mae, the best-performing stocks in our software coverage universe in 2015 were Palo Alto (+53%), Fleetmatics (+49%), Q2 Holdings (+47%) and Imperva (+39%). The worst-performing stock in our coverage universe in 2015 was Varonis (-48%), followed by Teradata (-37%), Interactive Intelligence (-33%), Verint (-29%) and NetSuite (-23%).

2016 Software Sector Outlook

December 18, 2015 3

Exhibit 1: Coverage universe vs. S&P 500 and NASDAQ, 2011-2015

2011 2012 2013 2014 2015 Market Cap ($M)

ELLI NA 391% -3% 50% 58% 1,904

PANW NA 1% 7% 113% 53% 16,087

FLTX NA 13% 72% -18% 49% 2,041

QTWO NA NA NA 24% 47% 1,070

IMPV 45% -9% 53% 3% 39% 2,153

LOGM -13% -42% 50% 47% 37% 1,692

PFPT NA -27% 169% 45% 36% 2,659

ULTI 34% 45% 62% -4% 36% 5,729

CRM -23% 66% 31% 7% 33% 52,383

ADBE -8% 33% 59% 21% 31% 47,665

NOW NA 22% 87% 21% 29% 13,816

CTXS -11% 8% -4% 1% 24% 12,440

MSFT -7% 3% 40% 24% 21% 448,361

NICE -1% -3% 22% 24% 16% 3,557

RHT -10% 28% 6% 23% 14% 14,399

SAP 5% 52% 8% -20% 13% 96,413

ANSS 10% 18% 29% -6% 12% 8,165

BNFT NA NA 8% -43% 11% 1,046

CHKP 14% -9% 35% 22% 10% 15,646

DATA NA NA 36% 23% 9% 6,739

INTU 7% 13% 28% 21% 7% 26,150

RP -18% -15% 8% -6% 7% 1,847

ZEN NA 0% 0% 81% 7% 2,315

NASDAQ -2% 16% 38% 13% 7%

FTNT 35% -4% -9% 60% 4% 5,508

ADSK -21% 17% 42% 19% 3% 13,954

SHOP NA NA NA NA 2% 1,985

S&P 500 0% 13% 30% 11% 1%

QLIK NA -10% 23% 16% 0% 2,884

WDAY NA 12% 53% -2% 0% 15,608

MIME NA NA NA NA -1% 541

CA -17% 9% 53% -10% -6% 11,917

PTC -19% 23% 57% 4% -6% 3,911

SPLK NA -18% 137% -14% -6% 7,188

QLYS NA 1% 56% 63% -7% 1,199

DWRE NA 16% 135% -10% -8% 1,998

ORCL -18% 30% 15% 18% -13% 165,937

BCOV NA -37% 56% -45% -14% 218

MKTO NA NA 60% -12% -20% 1,132

SYMC -7% 20% 25% 9% -20% 13,828

CVLT 49% 63% 7% -31% -22% 1,822

HDP NA NA NA NA -22% 978

LOCK NA -4% 102% 13% -23% 1,365

N 62% 66% 53% 6% -23% 6,716

VRNT -13% 7% 46% 36% -29% 2,577

ININ -12% 46% 101% -29% -33% 698

TDC 18% 28% -26% -4% -37% 3,665

VRNS NA NA NA -25% -48% 443

Source: FactSet, priced as of December 16, 2015

2016 Software Sector Outlook

December 18, 2015 4

2015 much like last year for large-cap software Large-cap software ($10B+ market cap) performance was much like last year across our coverage universe with essentially the same number of companies outperforming the S&P 500 and NASDAQ as in 2014. Of the 15 names under coverage with over $10B market cap, nine outperformed in 2015 and eight outperformed in 2014. This compares with seven names outperforming in the last three years and four in the last five years. With a few exceptions, 2015 was another good year to own mid-large cap software. Notable outperformers in 2015 included many of the top performers from the last three years: Palo Alto, Salesforce, Adobe and ServiceNow with increases of 53%, 33%, 21% and 29% in 2015 and 279%, 87%, 153% and 194% over the last three years, respectively. Adobe and Salesforce have also been the best performing large-cap stocks over the last five years at 210% and 139%, respectively. The worst performing large-cap stocks in 2015 included Symantec (-20%), Oracle (-13%) and CA (-6%) while over the last three years the worst performing large-cap stocks include SAP (-2%), Symantec (+5%) and Oracle (+13%). Over the last five years, the worst-performing stocks include Citrix (+16%), CA (+17%) and Symantec (+22%). The only large-cap stocks that have outperformed over the last one, three and five years are Adobe, Microsoft and Salesforce. The only large-cap stocks that have underperformed over the last one, three and five years are CA, Oracle and Symantec.

Exhibit 2: Large cap 2015, three-year and five-year stock performance

Large Cap Stocks (>$10B)

Ticker Price Market Cap ($M) 5-Year Return 3-Year Return 2015 Return

PANW $187 $16,087 NA 279% 53%

CRM $79 $52,383 139% 87% 33%

ADBE $96 $47,665 210% 153% 31%

NOW $87 $13,816 NA 194% 29%

CTXS $79 $12,440 16% 20% 24%

MSFT $56 $448,361 101% 106% 21%

RHT $79 $14,399 73% 46% 14%

SAP $78 $96,413 55% -2% 13%

CHKP $87 $15,646 87% 83% 10%

INTU $99 $26,150 101% 60% 7%

ADSK $62 $13,954 62% 70% 3%

WDAY $81 $15,608 NA 55% 0%

CA $29 $11,917 17% 26% -6%

ORCL $39 $165,937 24% 13% -13%

SYMC $20 $13,828 22% 5% -20%

S&P 500 2,073 65% 42% 1%

Nasdaq Composite 5,071 91% 64% 7% Source: FactSet, priced as of December 16, 2015

2016 Software Sector Outlook

December 18, 2015 5

Exhibit 3: Large cap stocks vs. S&P 500

Large Cap Stocks (>$10B) vs. S&P 500

Ticker Price Market Cap ($M) 5-Year 3-Year 2015

PANW $187 $16,087 NA 237% 52%

CRM $79 $52,383 74% 45% 32%

ADBE $96 $47,665 146% 111% 31%

NOW $87 $13,816 NA 152% 28%

CTXS $79 $12,440 -49% -22% 23%

MSFT $56 $448,361 36% 64% 20%

RHT $79 $14,399 8% 4% 13%

SAP $78 $96,413 -10% -45% 12%

CHKP $87 $15,646 22% 41% 9%

INTU $99 $26,150 36% 18% 7%

ADSK $62 $13,954 -3% 28% 2%

WDAY $81 $15,608 NA 13% -1%

CA $29 $11,917 -48% -16% -7%

ORCL $39 $165,937 -41% -29% -14%

SYMC $20 $13,828 -43% -37% -21%

Over/Under-Performance

Source: FactSet, priced as of December 16, 2015

Exhibit 4: Large cap stocks vs. NASDAQ

Large Cap Stocks (>$10B) vs. Nasdaq Composite

Ticker Price Market Cap ($M) 5-Year 3-Year 2015

PANW $187 $16,087 NA 216% 46%

CRM $79 $52,383 48% 23% 26%

ADBE $96 $47,665 119% 90% 24%

NOW $87 $13,816 NA 131% 22%

CTXS $79 $12,440 -75% -43% 17%

MSFT $56 $448,361 10% 42% 14%

RHT $79 $14,399 -19% -17% 7%

SAP $78 $96,413 -36% -66% 6%

CHKP $87 $15,646 -4% 20% 3%

INTU $99 $26,150 10% -3% 0%

ADSK $62 $13,954 -29% 7% -4%

WDAY $81 $15,608 NA -8% -7%

CA $29 $11,917 -74% -37% -13%

ORCL $39 $165,937 -67% -50% -21%

SYMC $20 $13,828 -69% -58% -27%

Over/Under-Performance

Source: FactSet, priced as of December 16, 2015

2016 Software Sector Outlook

December 18, 2015 6

Balanced returns for growth vs. value/GARP software Returns for growth vs. value/GARP software stocks were more balanced in 2015 following outperformance of value/GARP in 2014. In 2015, the total return for growth names was 8.1% while the total return for value/GARP names was also 6.6%. Of the 26 names that outperformed the S&P 500 in 2015, seven were value/GARP compared to eight in 2014. Growth names accounted for all five of the best-performing stocks (Ellie Mae, Palo Alto, Fleetmatics, Q2 Holdings and Imperva) and value/GARP names accounted for three of the five worst-performing stocks (Teradata, Interactive Intelligence and Verint). The best performing value/GARP name was Adobe while the worst performing growth name was Varonis.

Exhibit 5: Balanced growth and value returns in 2015

Growth vs. GARP/Value (2014)

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Growth GARP/Value

Growth vs. GARP/Value (2015)

Growth includes: CRM, DATA, DWRE, N, NOW, WDAY, ULTI, QLIK, PFPT and RHT; GARP/Value includes: MSFT, ORCL, ADBE, ADSK, INTU, PTC, CA, and CHKP Source: FactSet, RBC Capital Markets, priced as of December 16, 2015

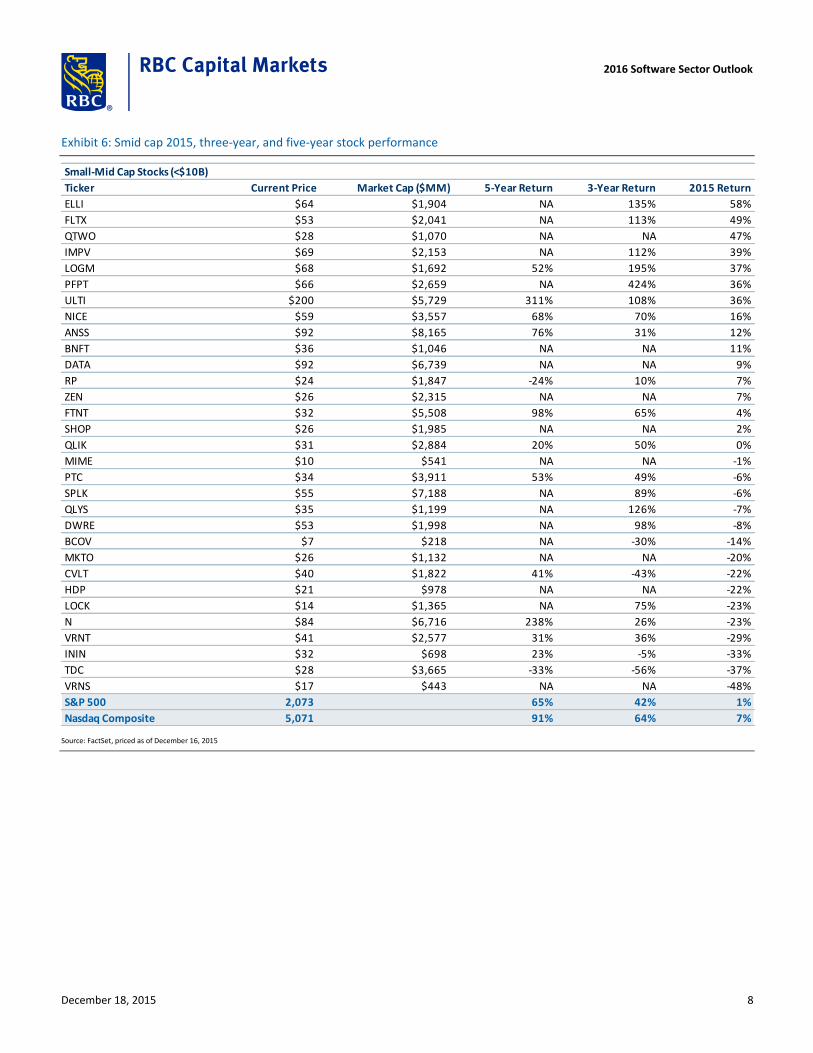

2015 was again a tougher year for smid-cap software Slightly fewer SMID cap software companies (under $10B market cap) in our coverage outperformed the S&P500 and NASDAQ in 2015 as in 2014. Of the 31 companies under coverage in this market cap range, 11 outperformed the major indexes vs. 14 last year while 18 underperformed. Compared to the three-year average, where only three companies had a negative return, 2015 again turned out to be a tougher year for smid-cap software with 15 companies having a negative return. The top-performing stocks in 2015 included Ellie Mae (+58%), Fleetmatics (+49%), Q2 Holdings (+47%), Imperva (+39%) and LogMeIn (+37%). Only Ellie Mae returned as one of the top-performing stocks (+56% in 2014). Security accounted for two of the six top-performing stocks compared to three in 2014, but with different companies: Imperva and Proofpoint in 2015 compared to Palo Alto (moved to large cap), Qualys (-7% vs. +68% in 2014) and Fortinet (+4% vs. +64% in 2014) in 2014. The only smid-cap company that outperformed over the last one, three and five years is Ultimate Software. The worst-performing stocks in 2015 included Netsuite (-23%), Verint (-29%), Interactive Intelligence (-33%), Teradata (-37%) and Varonis (-48%). The only smid-cap companies that underperformed over the last one, three and five years are CommVault, Interactive Intelligence, Teradata and Verint.

Returns for growth and value/GARP were more balanced in 2015 following outperformance of value/GARP in 2014.

2016 Software Sector Outlook

December 18, 2015 7

Exhibit 6: Smid cap 2015, three-year, and five-year stock performance

Small-Mid Cap Stocks (<$10B)

Ticker Current Price Market Cap ($MM) 5-Year Return 3-Year Return 2015 Return

ELLI $64 $1,904 NA 135% 58%

FLTX $53 $2,041 NA 113% 49%

QTWO $28 $1,070 NA NA 47%

IMPV $69 $2,153 NA 112% 39%

LOGM $68 $1,692 52% 195% 37%

PFPT $66 $2,659 NA 424% 36%

ULTI $200 $5,729 311% 108% 36%

NICE $59 $3,557 68% 70% 16%

ANSS $92 $8,165 76% 31% 12%

BNFT $36 $1,046 NA NA 11%

DATA $92 $6,739 NA NA 9%

RP $24 $1,847 -24% 10% 7%

ZEN $26 $2,315 NA NA 7%

FTNT $32 $5,508 98% 65% 4%

SHOP $26 $1,985 NA NA 2%

QLIK $31 $2,884 20% 50% 0%

MIME $10 $541 NA NA -1%

PTC $34 $3,911 53% 49% -6%

SPLK $55 $7,188 NA 89% -6%

QLYS $35 $1,199 NA 126% -7%

DWRE $53 $1,998 NA 98% -8%

BCOV $7 $218 NA -30% -14%

MKTO $26 $1,132 NA NA -20%

CVLT $40 $1,822 41% -43% -22%

HDP $21 $978 NA NA -22%

LOCK $14 $1,365 NA 75% -23%

N $84 $6,716 238% 26% -23%

VRNT $41 $2,577 31% 36% -29%

ININ $32 $698 23% -5% -33%

TDC $28 $3,665 -33% -56% -37%

VRNS $17 $443 NA NA -48%

S&P 500 2,073 65% 42% 1%

Nasdaq Composite 5,071 91% 64% 7%

Source: FactSet, priced as of December 16, 2015

2016 Software Sector Outlook

December 18, 2015 8

Exhibit 7: Smid cap stocks vs. S&P 500

Small-Mid Cap Stocks (<$10B) vs. S&P 500

Ticker Price Market Cap 5-Year 3-Year 2015

ELLI $64 $1,904 NA 93% 58%

FLTX $53 $2,041 NA 71% 48%

QTWO $28 $1,070 NA NA 46%

IMPV $69 $2,153 NA 70% 38%

LOGM $68 $1,692 -13% 152% 36%

PFPT $66 $2,659 NA 382% 36%

ULTI $200 $5,729 247% 66% 36%

NICE $59 $3,557 3% 28% 15%

ANSS $92 $8,165 11% -11% 11%

BNFT $36 $1,046 NA NA 10%

DATA $92 $6,739 NA NA 8%

RP $24 $1,847 -89% -32% 7%

ZEN $26 $2,315 NA NA 6%

FTNT $32 $5,508 33% 23% 4%

SHOP $26 $1,985 NA NA 1%

QLIK $31 $2,884 -45% 8% 0%

MIME $10 $541 NA NA -1%

PTC $34 $3,911 -12% 7% -7%

SPLK $55 $7,188 NA 47% -7%

QLYS $35 $1,199 NA 84% -8%

DWRE $53 $1,998 NA 56% -9%

BCOV $7 $218 NA -72% -15%

MKTO $26 $1,132 NA NA -21%

HDP $21 $978 NA NA -22%

CVLT $40 $1,822 -24% -85% -23%

LOCK $14 $1,365 NA 33% -23%

N $84 $6,716 173% -16% -23%

VRNT $41 $2,577 -34% -6% -30%

ININ $32 $698 -42% -47% -34%

TDC $28 $3,665 -98% -98% -38%

VRNS $17 $443 NA NA -48%

Over/Under-Performance

Source: FactSet, priced as of December 16, 2015

2016 Software Sector Outlook

December 18, 2015 9

Exhibit 8: SMid cap stocks vs. NASDAQ Composite

Small-Mid Cap Stocks (<$10B) vs. Nasdaq Composite

Ticker Price Market Cap 5-Year 3-Year 2015

ELLI $64 $1,904 NA 72% 51%

FLTX $53 $2,041 NA 50% 42%

QTWO $28 $1,070 NA NA 40%

IMPV $69 $2,153 NA 48% 32%

LOGM $68 $1,692 -39% 131% 30%

PFPT $66 $2,659 NA 360% 29%

ULTI $200 $5,729 220% 45% 29%

NICE $59 $3,557 -23% 6% 9%

ANSS $92 $8,165 -15% -32% 5%

BNFT $36 $1,046 NA NA 4%

DATA $92 $6,739 NA NA 2%

RP $24 $1,847 -115% -54% 0%

ZEN $26 $2,315 NA NA 0%

FTNT $32 $5,508 6% 2% -3%

SHOP $26 $1,985 NA NA -5%

QLIK $31 $2,884 -71% -14% -7%

MIME $10 $541 NA NA -8%

PTC $34 $3,911 -39% -14% -13%

SPLK $55 $7,188 NA 25% -13%

QLYS $35 $1,199 NA 63% -14%

DWRE $53 $1,998 NA 35% -15%

BCOV $7 $218 NA -94% -21%

MKTO $26 $1,132 NA NA -27%

CVLT $40 $1,822 -51% -106% -29%

HDP $21 $978 NA NA -29%

LOCK $14 $1,365 NA 12% -30%

N $84 $6,716 147% -38% -30%

VRNT $41 $2,577 -61% -28% -36%

ININ $32 $698 -68% -69% -40%

TDC $28 $3,665 -124% -119% -44%

VRNS $17 $443 NA NA -55%

Over/Under-Performance

Source: FactSet, priced as of December 16, 2015

Largest outperformers for 2015 across all market caps Ellie Mae (58%): Ellie Mae was the best performing stock in our coverage universe in 2015 and benefitted from strong fundamental outperformance. Consensus expectations for growth started the year at 26% and have since more than doubled, while expectations for EBIT margins have improved almost as much. This outperformance has come from a stronger mortgage market, as well as the company taking share and adding users faster than expected. Despite negative near-term mortgage origination volumes, we think growth expectations, valuation and the potential for growth surprises (especially in 2H16) leave the outlook biased to the upside.

Palo Alto (53%): The stock benefitted from another strong year in security and is well-positioned to continue its share gains, in our opinion. Billings and revenue accelerated Y/Y throughout the year, demonstrating the power of the hybrid-SaaS model while margins have consistently expanded Y/Y. Palo Alto's platform approach clearly is resonating with

2016 Software Sector Outlook

December 18, 2015 10

customers, as we feel the company is taking a disproportionate share of increased security spend while legacy providers and point solution vendors seem to be lagging behind.

Fleetmatics (49%): Fleetmatics rebounded following second-quarter guidance that was lowered due to FX and some conservatism around larger deals, to become the fourth best performing stock in our coverage universe. The company had an analyst day shortly following first-quarter results/second-quarter guidance that helped refocus investors on the long-term opportunity. From there the company continued to expand vehicles under subscription, made several acquisitions, entered new geographies and had success in mid-to-larger deals. The year was capped off with an OEM deal with GM, which was a positive surprise and while early, has been a focal point for investors to close the year.

Q2 Holdings (47%): Outperformance for the stock was driven largely by tier one deal signings, which should bode well for the future, as it will take several quarters for the deals to go live and the company to recognize revenue from them. Other positive events included the introduction of a new Treasury product and version 4.0 of the platform, the acquisition of Centrix, entry into the banking-rich northeastern part of the country and continued adoption of the platform by registered users.

Imperva (39%): Imperva reported strong results throughout 2015, outperforming the mid-point of revenue guidance by an average of $5.9 million. Similar to Palo Alto, what is even more impressive is expanding OM by 1,400 bps Y/Y to date. We feel this momentum should be sustainable as the company continues to take a disproportionate amount of the increased security spend as it displaces legacy providers such as IBM. The company is only 13% penetrated in the Fortune 1000 and has a long runway for expansion.

LogMeIn (37%): LogMeIn was again one of the top performing software names, up 36% in 2015 after being up 47% in 2014 and 50% in 2013. The stock really got moving following fourth-quarter and first-quarter results and followed through from there. The company executed consistently throughout the year, outperformed on leading metrics, steadily raised guidance and made a single-sign-on and password management acquisition. We remain impressed by an evolving strategy for relevance in collaboration, ITM and IoT, while join.me remains the overall growth driver. Cash flow remains strong while the stock continues to trade at a discount to peers.

Proofpoint (36%): Shares of Proofpoint benefitted from consistent quarterly outperformance through the year, a positive security backdrop and a competitive environment that continued to improve. We believe the threat landscape continues to move in the company’s favor, as we believe email/social should be a multiple-year opportunity with social more of a FY/16-to-FY/17 opportunity. TAP remains a robust opportunity and can double the ASP, as each of the 3,500+ customers could be a potential TAP customer. Most recently, McAfee announced it was going to end-of-life its email security suite, which should be a positive for Proofpoint and partially led management to guide to initial FY/16 revenue growth of 29-30%, which was above our initial expectations of 25%.

2016 Software Sector Outlook

December 18, 2015 11

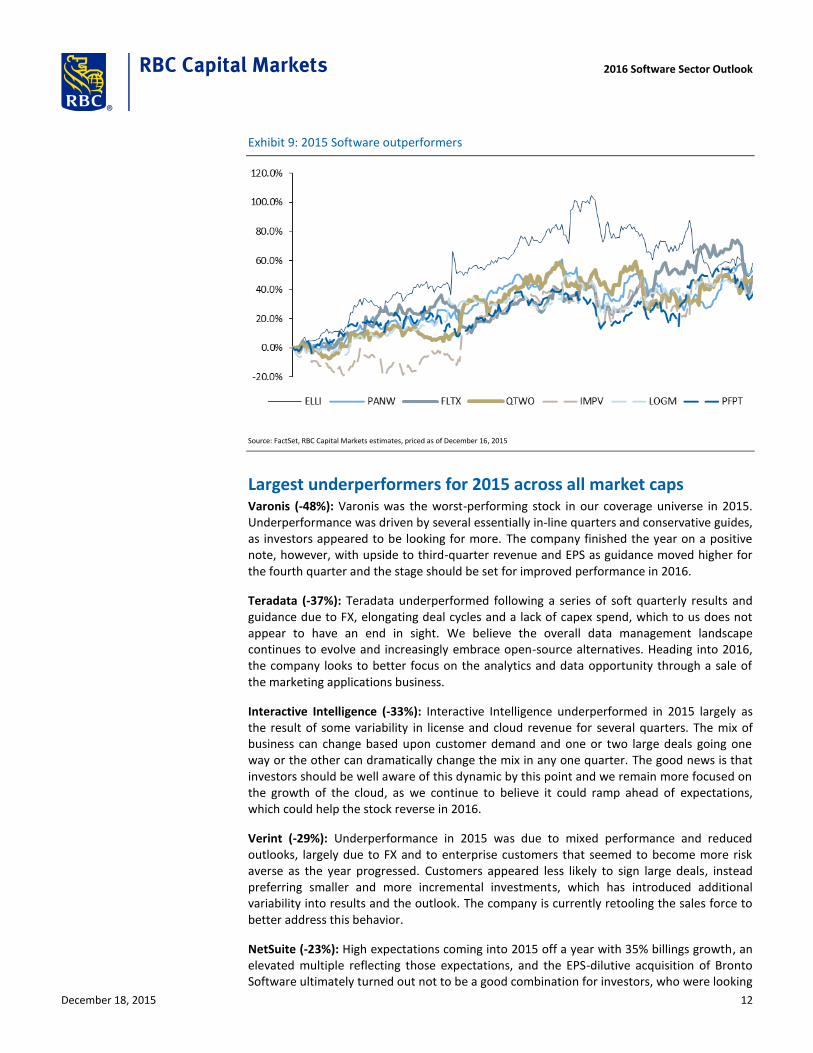

Exhibit 9: 2015 Software outperformers

Source: FactSet, RBC Capital Markets estimates, priced as of December 16, 2015

Largest underperformers for 2015 across all market caps Varonis (-48%): Varonis was the worst-performing stock in our coverage universe in 2015. Underperformance was driven by several essentially in-line quarters and conservative guides, as investors appeared to be looking for more. The company finished the year on a positive note, however, with upside to third-quarter revenue and EPS as guidance moved higher for the fourth quarter and the stage should be set for improved performance in 2016.

Teradata (-37%): Teradata underperformed following a series of soft quarterly results and guidance due to FX, elongating deal cycles and a lack of capex spend, which to us does not appear to have an end in sight. We believe the overall data management landscape continues to evolve and increasingly embrace open-source alternatives. Heading into 2016, the company looks to better focus on the analytics and data opportunity through a sale of the marketing applications business.

Interactive Intelligence (-33%): Interactive Intelligence underperformed in 2015 largely as the result of some variability in license and cloud revenue for several quarters. The mix of business can change based upon customer demand and one or two large deals going one way or the other can dramatically change the mix in any one quarter. The good news is that investors should be well aware of this dynamic by this point and we remain more focused on the growth of the cloud, as we continue to believe it could ramp ahead of expectations, which could help the stock reverse in 2016.

Verint (-29%): Underperformance in 2015 was due to mixed performance and reduced outlooks, largely due to FX and to enterprise customers that seemed to become more risk averse as the year progressed. Customers appeared less likely to sign large deals, instead preferring smaller and more incremental investments, which has introduced additional variability into results and the outlook. The company is currently retooling the sales force to better address this behavior.

NetSuite (-23%): High expectations coming into 2015 off a year with 35% billings growth, an elevated multiple reflecting those expectations, and the EPS-dilutive acquisition of Bronto Software ultimately turned out not to be a good combination for investors, who were looking

2016 Software Sector Outlook

December 18, 2015 12

for some operating leverage in the model. While the first two quarters were solid, cracks started to appear in Q3 as the Enterprise spending environment weakened. The company lowered annual guidance at the high end, a first for it since 3Q09, missed internal Enterprise expectations for Q3 due to volatility in ASPs, and declined to guide for 2016. We think the competitive environment needs to be watched, as others (including Oracle and Workday) begin to focus more on enterprise and upper-mid market Financials/ ERP.

Exhibit 10: 2015 Software Underperformers

Source: FactSet, RBC Capital Markets estimates, priced as of December 16, 2015

Mixed performance from the IPO class of 2015 We saw another full slate of issuance in 2015, with 12 software companies going public vs. 14 last year. IPO performance was mixed, with a couple of sizable outperformers, most notably Shopify, and also several stocks that were below issue price (Apigee, Box and Ooma).

Within our coverage universe, Shopify was up 54% from its pricing and Mimecast was flat from its pricing.

2016 Software Sector Outlook

December 18, 2015 13

Exhibit 11: 2015 IPOs and returns as of 12/16/15

Company Ticker Exchange IPO Date IPO Price Current Price Mkt Cap ($M) Return Since IPO

Box, Inc. BOX NYSE Jan-22-2015 14.00 $13.80 $1,595 -1%

Apigee Corporation APIC NASDAQ Apr-24-2015 17.00 $8.27 $238 -51%

Shopify, Inc. SHOP NYSE May-20-2015 17.00 $26.21 $2,238 54%

MINDBODY, Inc. MB NASDAQ Jun-24-2015 14.00 $15.04 $606 7%

Alarm.com Holdings, Inc. ALRM NASDAQ Jun-25-2015 14.00 $17.12 $761 22%

Xactly Corporation XTLY NYSE Jul-01-2015 8.00 $8.77 $267 10%

AppFolio, Inc. APPF NASDAQ Jun-25-2015 12.00 $15.41 $525 28%

Ooma, Inc. OOMA NYSE Jul-16-2015 13.00 $7.15 $119 -45%

Rapid7, Inc. RPD NASDAQ Jul-16-2015 16.00 $16.91 $637 6%

Instructure, Inc. INST NYSE Nov-12-2015 16.00 $19.98 $539 25%

Mimecast Limited MIME NASDAQ Nov-19-2015 10.00 $10.02 $576 0%

Atlassian Corporation Plc TEAM NASDAQ Dec-10-2015 21.00 $26.54 $5,529 26%

Unweighted Return: 7%

Weighted Return: 26%

Source: Company filings, FactSet

2016 Software Sector Outlook

December 18, 2015 14

2016 Software Spending Outlook Coming off a mixed year for software in 2015, we expect 2016 to remain more of a stock-picker’s market. Overall valuations have moved higher and tech spending continues to show signs of improvement. In the following sections, we analyze the forecasted revenue growth for various segments of software: SaaS, security and infrastructure. Company data is sorted by expected 2016 revenue growth.

Stay long Software-as-a-Service (SaaS): expect 24% growth or better For 2016, we are modeling 24.3% growth in actual SaaS dollar spending vs. 28.7% in 2015. From an absolute growth perspective (median growth expected across the 18 companies), we expect 24.0% for 2016 vs. 33.1% in 2015. In general, we expect incrementally more dollars to be allocated to CRM, social, HR, Human Capital Management (HCM), vertical SaaS solutions (health care, insurance, banking, wellness, etc.) and marketing automation software. In addition, we expect to see continued consolidation in the space, as many of the smaller vendors remain attractive acquisition candidates, in our opinion.

Exhibit 12: RBC SaaS spending forecast

2013A revenue

growth

2014A revenue

growth

2015E revenue

growth

2016E revenue

growth

SHOP 112.2% 108.7% 86.7% 56.6%

ZEN 88.5% 76.4% 62.2% 44.2%

NOW 74.2% 60.7% 46.8% 37.0%

WDAY 71.3% 68.1% 47.0% 35.2%

N 34.2% 34.1% 32.9% 31.4%

MKTO 64.2% 56.4% 39.3% 31.1%

QTWO 38.4% 39.1% 36.8% 30.3%

DWRE 34.1% 51.0% 46.0% 28.1%

BNFT 28.2% 31.1% 33.2% 24.9%

ULTI 23.5% 23.3% 21.7% 23.1%

CRM 33.5% 32.0% 23.7% 21.1%

FLTX 39.2% 30.6% 22.9% 20.7%

ELLI 26.2% 26.1% 54.3% 19.6%

LOGM 19.8% 33.5% 21.6% 19.3%

LOCK 33.7% 28.8% 23.0% 13.1%

ININ 34.1% 7.2% 14.0% 12.5%

RP 17.8% 6.6% 15.1% 11.8%

BCOV 24.9% 13.8% 6.8% 9.3%

Mean growth 44.3% 40.4% 35.2% 26.1%

Median growth 34.1% 32.8% 33.1% 24.0%

Mean dollar growth 36.1% 34.1% 28.7% 24.3%

Source: FactSet, RBC Capital Markets estimates

For 2016, we are modeling 24.3% growth in actual SaaS dollar spending vs. 28.7% in 2015.

2016 Software Sector Outlook

December 18, 2015 15

Still optimistic on Security software, but stay selective: expect 25% plus growth excluding CHKP and SYMC For 2016, we are modeling 11.5% growth in actual security software dollar spending vs. 7.0% in 2015 across the eight companies, though much of that is driven by larger firms, including CHKP and SYMC. Excluding CHKP and SYMC, we are modeling 25.1% in actual security software dollar spending vs. 32.9% in 2015 across the six companies, which we view as a better proxy for the potential in the more growth-oriented companies in the space. From an absolute growth perspective (median growth expected across the eight companies), we expect 23.9% for 2016 vs. 27.1% in 2015, though we expect an upward bias to estimates throughout the year. In general, we expect incrementally more dollars to be allocated to data security, Security-as-a-Service, advanced threat protection, passwords/authentication and endpoint security. In addition, we expect to see continued consolidation in the space, as many of the smaller vendors remain attractive acquisition candidates, in our opinion.

Exhibit 13: RBC security software spending forecast

2013A revenue

growth

2014A revenue

growth

2015E revenue

growth

2016E revenue

growth

PANW 49.2% 53.0% 53.4% 33.4%

PFPT 29.8% 41.8% 34.7% 29.3%

FTNT 15.3% 25.2% 31.2% 25.2%

IMPV 32.2% 19.1% 40.0% 25.0%

QLYS 18.1% 23.7% 23.0% 22.8%

MIME NA 33.5% 22.2% 19.2%

CHKP 3.8% 7.3% 9.1% 9.3%

SYMC NA -3.4% -10.4% -1.0%

Mean growth 24.7% 25.0% 25.4% 20.4%

Median growth 23.9% 24.5% 27.1% 23.9%

Mean dollar growth 186.9% 7.0% 7.0% 11.5%

Source: FactSet, RBC Capital Markets estimates

For 2016, we are modeling 11.5% growth in actual security software dollar spending vs. 7.0% in 2015, though much of that is driven by larger firms, including CHKP and SYMC. From an absolute growth perspective (median growth expected across the eight companies), we expect 23.9% for 2016.

2016 Software Sector Outlook

December 18, 2015 16

We remain more bearish on legacy Infrastructure and more optimistic/bullish on next-gen names: overall expect low-to-mid single digit growth For 2016, we are modeling 2.2% growth in actual infrastructure/application software dollar spending vs. -2.6% in 2015. From an absolute growth perspective (median growth expected across the 20 companies), we expect 6.4% for 2016 vs. 0.8% in 2015. Within the group, concerns linger around the impact of the hybrid cloud to classic infrastructure software (will be addressed further in the next section) as next-generation names thrive.

Exhibit 14: RBC infrastructure software and traditional applications spending forecast

2013A revenue

growth

2014A revenue

growth

2015E revenue

growth

2016E revenue

growth

HDP 670.9% 113.1% 131.3% 46.4%

DATA 82.0% 77.5% 57.7% 32.8%

SPLK 52.1% 49.0% 44.3% 30.7%

VRNS 39.7% 35.8% 23.6% 23.4%

ADBE -7.9% 2.3% 15.7% 19.4%

QLIK 21.1% 18.4% 11.4% 16.2%

RHT 16.0% 16.5% 14.3% 14.5%

ANSS 6.6% 9.3% 1.2% 7.2%

CVLT 20.4% 8.1% -5.5% 6.4%

NICE 6.5% -1.5% -1.2% 6.4%

SAP 14.3% 0.8% 16.8% 6.4%

INTU 7.2% 11.0% -1.7% 5.9%

VRNT 7.3% 27.3% 0.4% 5.3%

CA -2.8% -2.8% -7.1% 2.8%

CTXS 12.9% 7.7% 2.9% 0.9%

MSFT 14.4% 12.0% -8.1% 0.4%

ORCL 0.7% 3.3% -3.4% 0.2%

PTC 3.2% 4.6% -10.0% -2.0%

TDC 0.8% 1.5% -8.0% -3.2%

ADSK -1.7% 10.5% -1.1% -15.3%

Mean growth 48.2% 20.2% 13.7% 10.2%

Median growth 10.1% 9.6% 0.8% 6.4%

Mean dollar growth 9.2% 8.0% -2.6% 2.2%

Source: FactSet, RBC Capital Markets estimates

For 2016, we are modeling 2.2% growth in actual infrastructure software dollar spending vs. -2.6% in 2015. From an absolute growth perspective (median growth expected across the 20 companies), we expect 6.4% for 2016 vs. 0.8% in 2015.

2016 Software Sector Outlook

December 18, 2015 17

Top Themes in 2016: Software In this section, we highlight several themes we think will be most impactful for software in 2016. A number of these are consistent with what we have experienced over the last few years and center on the shift to the cloud, security, M&A and the importance of margin expansion, but we also call out several new themes.

Our software themes for 2016 include: margins matter; we could see a tipping point for strategic M&A; all apps to the cloud; data as a differentiator; Amazon to the apps layer; shifting priorities in cyber-security; a shift to the cloud should continue to be deflationary to legacy infrastructure vendors; value emerges as the IoT market starts to materialize; and a focus on next-generation disruptors.

These should all be important themes for 2016 so we provide a brief overview and details on which companies are affected by these trends.

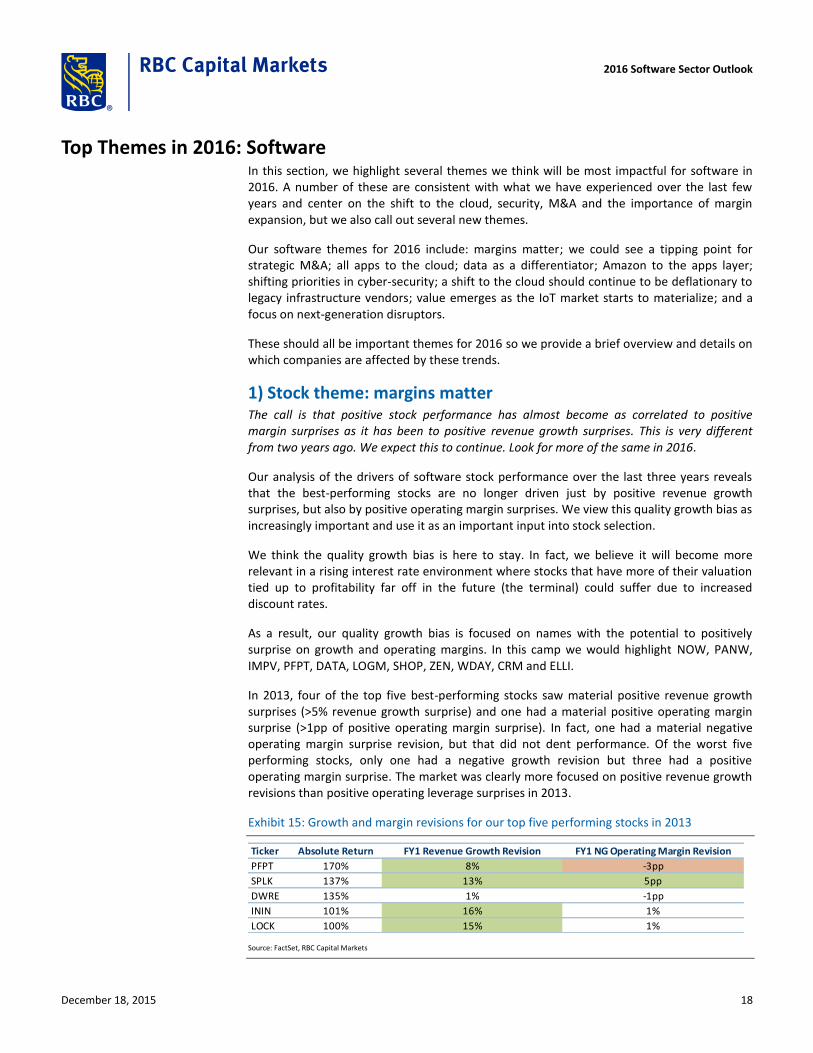

1) Stock theme: margins matter The call is that positive stock performance has almost become as correlated to positive margin surprises as it has been to positive revenue growth surprises. This is very different from two years ago. We expect this to continue. Look for more of the same in 2016.

Our analysis of the drivers of software stock performance over the last three years reveals that the best-performing stocks are no longer driven just by positive revenue growth surprises, but also by positive operating margin surprises. We view this quality growth bias as increasingly important and use it as an important input into stock selection.

We think the quality growth bias is here to stay. In fact, we believe it will become more relevant in a rising interest rate environment where stocks that have more of their valuation tied up to profitability far off in the future (the terminal) could suffer due to increased discount rates.

As a result, our quality growth bias is focused on names with the potential to positively surprise on growth and operating margins. In this camp we would highlight NOW, PANW, IMPV, PFPT, DATA, LOGM, SHOP, ZEN, WDAY, CRM and ELLI.

In 2013, four of the top five best-performing stocks saw material positive revenue growth surprises (>5% revenue growth surprise) and one had a material positive operating margin surprise (>1pp of positive operating margin surprise). In fact, one had a material negative operating margin surprise revision, but that did not dent performance. Of the worst five performing stocks, only one had a negative growth revision but three had a positive operating margin surprise. The market was clearly more focused on positive revenue growth revisions than positive operating leverage surprises in 2013.

Exhibit 15: Growth and margin revisions for our top five performing stocks in 2013

Ticker Absolute Return FY1 Revenue Growth Revision FY1 NG Operating Margin Revision

PFPT 170% 8% -3pp

SPLK 137% 13% 5pp

DWRE 135% 1% -1pp

ININ 101% 16% 1%

LOCK 100% 15% 1%

Source: FactSet, RBC Capital Markets

2016 Software Sector Outlook

December 18, 2015 18

Exhibit 16: Growth and margin revisions for our bottom five performing stocks in 2013

Ticker Absolute Return FY1 Revenue Growth Revision FY1 NG Operating Margin Revision

TDC -27% -11% 1pp

FTNT -9% -4% -2pp

CTXS -4% -1% 2pp

ELLI -3% 0% 3pp

RHT 6% -1% 3pp

Source: FactSet, RBC Capital Markets

In 2014, things started to change. Four of the top five best-performing stocks saw material positive growth revisions, but in addition, two of the top five saw material positive operating margin surprises. Even more telling is the fact that while three of the bottom five performing stocks had negative material revenue growth surprises, four of the bottom five had negative material operating margin surprises.

Exhibit 17: Growth and margin revisions for our top five performing stocks in 2014

Ticker Absolute Return FY1 Revenue Growth Revision FY1 NG Operating Margin Revision

PANW 113% 16% 1pp

QLYS 63% 4% 3pp

FTNT 60% 9% -5pp

ELLI 50% 6% 0pp

LOGM 47% 18% 3pp

Source: FactSet, RBC Capital Markets

Exhibit 18: Growth and margin revisions for our bottom five performing stocks in 2014

Ticker Absolute Return FY1 Revenue Growth Revision FY1 NG Operating Margin Revision

BCOV -45% -3% -5pp

BNFT -43% 4% -14pp

CVLT -31% -7% -3pp

ININ -29% -8% -8pp

SAP -20% -8% -1pp

Source: FactSet, RBC Capital Markets

In 2015 (YTD through December 16), four of the top five best performing stocks saw material positive revenue growth surprises and three of the top five saw material positive operating margin surprises. Not one of the top five stocks had a negative operating margin surprise, while two of the worst-performing stocks had negative revenue growth and operating margin surprises.

Exhibit 19: Growth and margin revisions for our top five performing stocks in 2015

Ticker Absolute Return FY1 Revenue Growth Revision FY1 NG Operating Margin Revision

ELLI 58% 29% 9pp

PANW 53% 19% 1pp

FLTX 49% -2% 0pp

QTWO 48% 7% 2pp

IMPV 39% 18% 7pp

Source: FactSet (priced as of December 16, 2015), RBC Capital Markets

2016 Software Sector Outlook

December 18, 2015 19

Exhibit 20: Growth and margin revisions for our bottom five performing stocks in 2015

Ticker Absolute Return FY1 Revenue Growth Revision FY1 NG Operating Margin Revision

VRNS -48% -4% 1pp

TDC -37% -12% -6pp

ININ -33% 3% 2pp

VRNT -29% -7% -1pp

N -23% 2% -3pp

Source: FactSet (priced as of December 16, 2015), RBC Capital Markets

Taking a broader view of the space, we see similar patterns emerge over the last three years. Revisions to 2013 growth expectations had a 59% correlation to 2013 returns, while margin revisions were essentially uncorrelated at (9%). This dipped to 43% for 2014 growth revisions and grew to 28% for margin revision. 2015 through December 16 has seen growth revisions 46% correlated to returns, while margin revisions are almost as high at 41% (excluding Hortonworks from both calculations).

Exhibit 21: Growth Revisions vs. Stock Outperformance in 2013 (59% Correlation)

NOW

ININLOCK

SPLK

FLTX

WDAY

PFPT

CRM

IMPV

CVLT

N

PANW

BCOV

DWRE

QLIK

ELLI

LOGMVRNT

RHT

ULTIQLYS

CTXS

ADBE

RP

MSFT

CA

CHKP

NICESYMC

FTNT

ANSS

ORCLSAP

ADSK

PTC

INTU

TDC

-100%

-50%

0%

50%

100%

150%

-15% -10% -5% 0% 5% 10% 15% 20%

Source: RBC Capital Markets, FactSet

2016 Software Sector Outlook

December 18, 2015 20

Exhibit 22: Margin Revisions vs. Stock Outperformance in 2013 (-9% correlation)

WDAY

FLTX

CVLT

BCOV

PANW

NOW

ULTI

SPLK

RP

PTC

ANSS

SAP

QLYS

CHKP

ELLI

RHT

NICEINTU

SYMCCRM

VRNT

CTXS

LOCKININ

TDC

LOGM

QLIK

ORCL

NCA

DWRE

FTNT

IMPV

PFPT

MSFT

ADBE

ADSK

-100%

-50%

0%

50%

100%

150%

-10% -5% 0% 5% 10% 15%

Source: RBC Capital Markets, FactSet

Exhibit 23: Growth Revisions vs. Stock Outperformance in 2015 (46% correlation)

Source: RBC Capital Markets, FactSet (priced as of December 16, 2015)

2016 Software Sector Outlook

December 18, 2015 21

Exhibit 24: Margin Revisions vs. Stock Outperformance in 2015 (41% correlation)

Source: RBC Capital Markets, FactSet (priced as of December 16, 2015).

Ways to play the theme Among our coverage universe, companies that we see as well-positioned to deliver upside on both growth and margin expectations include Ellie Mae, Hortonworks, Imperva, LogMeIn, Palo Alto Networks, Proofpoint, Salesforce, ServiceNow, Shopify, Tableau, Workday and Zendesk.

2016 Software Sector Outlook

December 18, 2015 22

2) Could 2016 be a tipping point for strategic M&A? The call is that we think a number of factors are converging that could make 2016 a significant year of strategic M&A in software – especially large cap SaaS and Security.

The transition of enterprise technology to the cloud is accelerating, creating a fundamental challenge for incumbent technology players that have sold to the corporate data center for the past 30 years.

There is a risk that cloud leaders are reaching escape velocity in terms of scale and pace of innovation that means the window of opportunity to catch up is closing.

The number of strategic assets that could make a difference is limited to a small number of SaaS/ PaaS companies that are growing rapidly and could accelerate the efforts of incumbents.

Some extraneous factors could also add a spark. In particular, we think the potential for tax relief on the repatriation of overseas cash driven by the outcome of the 2016 elections could be a factor in driving strategic M&A next year.

Time for strategic (rather than sponsor) M&A? The last 12-18 months has seen a dearth of strategic M&A but a relatively high volume of financial sponsor M&A. In fact, in 2015, $15B (58%) of the $26B of software M&A was done by private equity, a significantly higher amount than in 2014 when $8B (34%) of the $23B of software M&A was done by private equity.

We note that some of the largest financial sponsor acquisitions of the last year in software include Vista Partners’ acquisition of Solera Holdings for $6.5B, Silverlake’s/Thoma Bravo’s acquisition of SolarWinds (~$4.6B), Permira’s/CPP’s acquisition of Informatica (~$4.8B) and Bain Capital’s acquisition of Blue Coat Systems (~$2.4B). Raytheon’s purchase of Websense ($1.9B) and the firewall business (Secure Computing asset) of Intel/McAfee also highlights the potential for non-traditional acquirers for specific assets.

Meanwhile, the most prominent strategic M&A deal has probably been SS&C’s acquisition of Advent Software to further consolidate its position in portfolio accounting and fund administration.

In 2016, we think this could change with the potential for large, strategic deals.

The lack of growth ex cloud makes this an imperative We think the continued expansion of cloud-based applications, platforms and infrastructure is a significant driver of M&A in the software universe.

The first wave of SaaS applications M&A was driven by the need for incumbents to kick-start their cloud presence and compete more effectively around the edge of the application core. Examples include Oracle’s purchases of RightNow, Taleo, Eloqua and Responsys; SAP’s purchases of SuccessFactors and Ariba and IBM’s purchases of DemandTec and Kenexa.

The question we ask ourselves today is whether we could see a second wave of SaaS applications M&A, driven by the need for incumbents to increase their cloud scale, make them more relevant in the cloud discussion and potentially elevate their chances of attracting future cloud workloads.

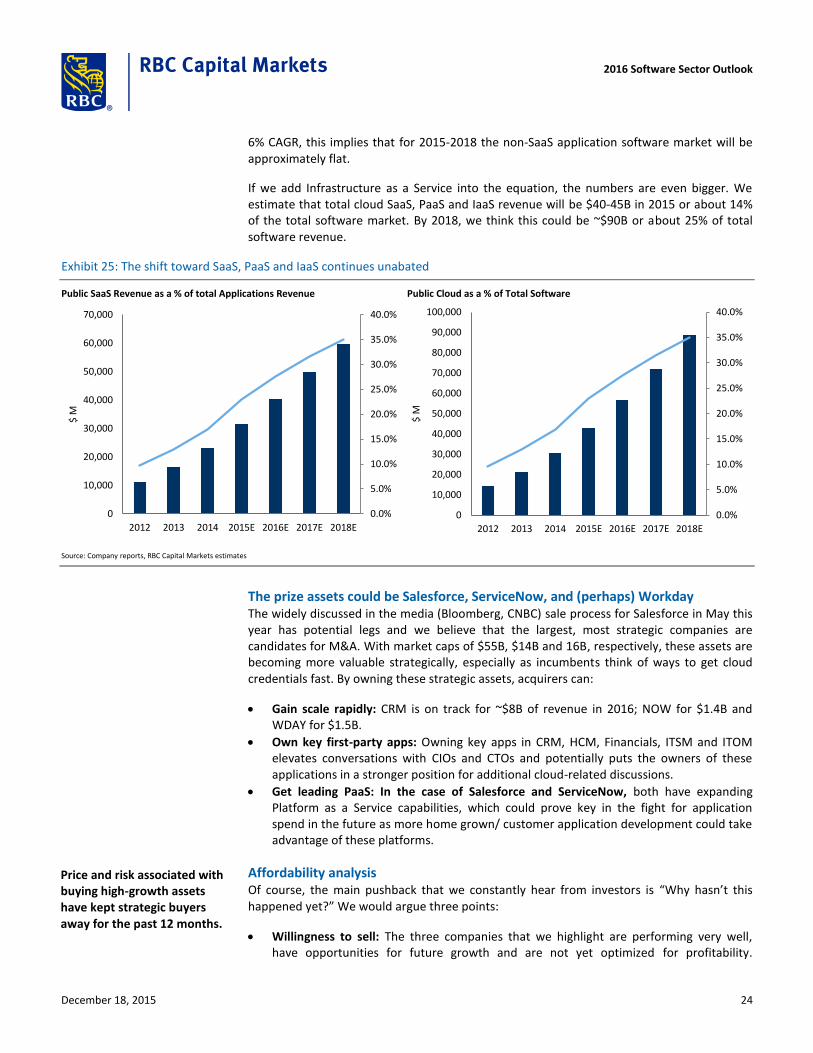

We think it is important to reflect that public SaaS revenue will be over $25B in 2015 (including SaaS revenues at SAP and Oracle) or about 17% of the total software application market. By 2018, we believe this could be ~$50B and in the range of 35% of the total software application market. Given that the software application market will grow at about

The accelerating shift to cloud and the need for incumbents to catch up fast could drive strategic M&A that has been absent over the last 12 months

2016 Software Sector Outlook

December 18, 2015 23

6% CAGR, this implies that for 2015-2018 the non-SaaS application software market will be approximately flat.

If we add Infrastructure as a Service into the equation, the numbers are even bigger. We estimate that total cloud SaaS, PaaS and IaaS revenue will be $40-45B in 2015 or about 14% of the total software market. By 2018, we think this could be ~$90B or about 25% of total software revenue.

Exhibit 25: The shift toward SaaS, PaaS and IaaS continues unabated

Public SaaS Revenue as a % of total Applications Revenue

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2012 2013 2014 2015E 2016E 2017E 2018E

$ M

Public Cloud as a % of Total Software

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

2012 2013 2014 2015E 2016E 2017E 2018E

$ M

Source: Company reports, RBC Capital Markets estimates

The prize assets could be Salesforce, ServiceNow, and (perhaps) Workday The widely discussed in the media (Bloomberg, CNBC) sale process for Salesforce in May this year has potential legs and we believe that the largest, most strategic companies are candidates for M&A. With market caps of $55B, $14B and 16B, respectively, these assets are becoming more valuable strategically, especially as incumbents think of ways to get cloud credentials fast. By owning these strategic assets, acquirers can:

Gain scale rapidly: CRM is on track for ~$8B of revenue in 2016; NOW for $1.4B and WDAY for $1.5B.

Own key first-party apps: Owning key apps in CRM, HCM, Financials, ITSM and ITOM elevates conversations with CIOs and CTOs and potentially puts the owners of these applications in a stronger position for additional cloud-related discussions.

Get leading PaaS: In the case of Salesforce and ServiceNow, both have expanding Platform as a Service capabilities, which could prove key in the fight for application spend in the future as more home grown/ customer application development could take advantage of these platforms.

Affordability analysis Of course, the main pushback that we constantly hear from investors is “Why hasn’t this happened yet?” We would argue three points:

Willingness to sell: The three companies that we highlight are performing very well, have opportunities for future growth and are not yet optimized for profitability.

Price and risk associated with buying high-growth assets have kept strategic buyers away for the past 12 months.

2016 Software Sector Outlook

December 18, 2015 24

Therefore, management and the board have less incentive to sell, unless a very significant premium can be realized.

Price: Salesforce and Microsoft unconfirmed discussions from 2015 are reported to have stalled due to a disagreement on price. We note that relative to current valuations, a 30% premium would put the three assets significantly above the median multiple of historical M&A deals (CRM currently trades at ~7x FY16 EV/Sales, while NOW and WDAY are at ~11x).

Risk: Acquisition of these assets would carry significant risk. First, an acquisition of Salesforce has the potential to be the largest technology acquisition of all time. Second, all of these companies have the classic founder/ owner deep involvement, which is notoriously difficult to maintain when no longer independent (Marc Benioff at Salesforce, Frank Luddy at ServiceNow and Dave Duffield/ Aneel Bhusri at Workday). Third, these companies have significant equity compensation incentives, which may be hard to replicate when no longer independent. Finally, the operational and execution risk surrounding buying growth assets is relatively high.

Affordability isn’t much of a gating factor: With large cash balances, we run illustrative affordability analyses to demonstrate that the potential universe of buyers remains robust. We haircut acquirers’ offshore cash balances by 35% where applicable to account for tax repatriation issues, and assume that strategic buyers could lever up to 3.0x Net Debt/2016 EBITDA to fund their purchases. The result is that Salesforce has a limited set of potential suitors (we think AAPL, GOOG and MSFT), but ServiceNow and Workday have a much wider set of potential suitors.

Exhibit 26: Illustrative affordability analysis

($ in M)

Potential Adj.

Acquirer Market Cap Net Debt EV EBITDA 2.0x Net Debt 3.0x Net Debt 4.0x Net Debt 2.0x Net Debt 3.0x Net Debt 4.0x Net Debt

2015E 2016E 2015E 2016E / '15 EBITDA /'15 EBITDA /'15 EBITDA / '15 EBITDA /'15 EBITDA /'15 EBITDA

Amazon $321,667 ($4,575) $317,092 $10,805 $14,218 -0.4x -0.3x $21,610 $32,416 $43,221 $26,185 $36,991 $47,796

Google 526,356 (52,836) 473,520 29,607 34,813 -1.8x -1.5x 59,214 88,821 118,428 112,050 141,657 171,264

IBM 136,365 30,092 166,457 21,333 21,551 1.4x 1.4x 42,667 64,000 85,334 12,575 33,908 55,242

HP Enterprise 26,872 4,345 31,217 7,962 7,983 0.5x 0.5x 15,925 23,887 31,850 11,580 19,542 27,505

Microsoft 453,773 (27,188) 426,585 32,235 32,648 -0.8x -0.8x 64,471 96,706 128,941 91,659 123,894 156,129

Apple 621,144 (75,784) 545,360 82,487 82,850 -0.9x -0.9x 164,974 247,461 329,948 240,758 323,245 405,732

Oracle 175,174 1,800 176,974 17,556 18,104 0.1x 0.1x 35,113 52,669 70,225 33,313 50,869 68,425

Cisco 138,408 (15,551) 122,857 16,218 16,423 -1.0x -0.9x 32,436 48,654 64,872 47,987 64,205 80,423

SAP 95,786 6,538 102,325 7,621 8,332 0.9x 0.8x 15,243 22,864 30,486 8,705 16,326 23,947

Debt Capacity at Capacity to purchase

Adj. Net Debt / EBITDA

Potential Target Market Cap 30% Premium Net Debt Adj. EV AMZN GOOG IBM HPE MSFT AAPL ORCL CSCO SAP

CRM salesforce.com, inc. $54,633 $71,022 ($269) $70,753 No Yes No No Yes Yes No No No

NOW ServiceNow, Inc. $14,730 $19,149 ($663) $18,486 Yes Yes Yes Yes Yes Yes Yes Yes No

WDAY Workday, Inc. Class A $17,494 $22,743 ($1,388) $21,354 Yes Yes Yes No Yes Yes Yes Yes No

Source: FactSet, Company reports and RBC Capital Markets estimates

2016 Software Sector Outlook

December 18, 2015 25

Some historical context Looking at large public-technology deals between 2001 and today, we screened over 150 transactions. In this universe, the smallest was the acquisition of Cytiva by Taleo for $8.7 million in early 2011 and the largest was the acquisition of VERITAS by Symantec for $13.0 billion in 2004. From an EV/S multiple, the mean of these transactions was 4.4x, the median was 3.5x, the high was 15.7x (HP’s 2011 acquisition of Autonomy), and the low was 0.5x (Oracle’s 2009 acquisition of Sun Microsystems). Exhibit 27 illustrates the multiples of the various transactions from 2001 to today, including the median and mean.

Exhibit 27: EV/S multiples for large, public, technology transactions 2001-2015

0.0x

2.5x

5.0x

7.5x

10.0x

12.5x

15.0x

Mean 4.4xMedian 3.5x

Source: FactSet, Company reports, RBC Capital Markets estimates

Exhibit 28: EV/S mean and median multiples for large public software transactions 2001-2015

Source: FactSet, RBC Capital Markets estimates

2016 Software Sector Outlook

December 18, 2015 26

3) Tech theme: All apps to the cloud The simple call is the progression of applications to the cloud continues. 2016 could be the tipping point for Financial Management, with WDAY the best way to play the theme.

However, it is clear that some application categories have moved faster than others. For example, when comparing Customer Relationship Management (CRM) to Enterprise Resource Planning (ERP), we can see that the former is already 50% in the cloud today given Salesforce’s dominance of the market, while ERP remains less than 20% converted to the cloud, with most of that shift being Human Capital Management (HCM) rather than Financial Management or others parts of the core backbone.

Exhibit 29: CRM is ~50% in the cloud, but ERP is less than 20% in the cloud

0%

10%

20%

30%

40%

50%

60%

70%

0

5,000

10,000

15,000

20,000

25,000

30,000

2013 2014 2015E 2016E 2017E 2018E 2019E

CRM ERP CRM ERP

Source: Gartner (Forecast: Public Cloud Services, Worldwide, 2013-2019, 3Q15 Update), RBC Capital Markets estimates

We think the shift of different application categories to the cloud is a function of one or more vendors forcing the agenda (Salesforce in the case of CRM), the state of the existing application environment (arguably the CRM market was littered with under-utilized CRM applications before Salesforce), and the pace of innovation and change in the underlying market. Recruiting applications in HCM, for example, have been largely replaced by next-generation versions that have tight integration to social networks such as Linkedin, as this is the way most recruiters now source candidates.

It is also interesting to note that two of the leading cloud SaaS vendors today, Salesforce and Netsuite, have had a very different path of growth. While there are many different reasons as to why Salesforce has >$6.5B of revenue today versus Netsuite’s <$1B, we fundamentally believe that the pace at which their respective end markets have adopted (Financial Management for Netsuite and Customer Relationship Management for Salesforce) has been an important input into this equation. In fact, overlaying the historical annual revenues of Salesforce against Netsuite, it is apparent that Financials adoption has lagged CRM adoption by an almost perfect factor of 10.

Salesforce and Netsuite were founded around the same time, but their respective markets have adopted at very different paces

2016 Software Sector Outlook

December 18, 2015 27

Exhibit 30: Salesforce vs. Netsuite tells the story of cloud adoption of CRM vs. financials

0

1,000

2,000

3,000

4,000

5,000

6,000

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14CRM Revenues N Revenues

0

1,000

2,000

3,000

4,000

5,000

6,000

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

CRM Revenues (N x 10) Revenues

Source: Company reports

Could 2016 be the year for financials to the cloud? We think a number of factors are in place that suggest 2016 could be a tipping point for financials moving to the cloud:

Functionality and scalability of cloud products continues to improve. We note that Workday is able to address companies with up to 200M annual journal lines (low end of F250) and continue to add functionality (such as professional service automation, internal inventory and financial planning).

More large companies are accepting that financials can move to the cloud. In 2015, we would highlight a number of wins, including HP’s deployment of Netsuite for its entire software division (15 counties and >$5B of revenue), and more recently, AON’s decision to move to Workday for Financial Management (AON is a F500 company with ~$12B in revenue, operations in over 60 counties and ~65K employees)

Incumbent vendors are stepping up their cloud game. Despite the risk of increased competition, we think the fact that Oracle is in the market selling Fusion ERP Cloud (Oracle claims more than 1,350 on Fusion ERP) and SAP with its Simple Finance for S4HANA solution, is actually an important catalyst for new cloud vendors.

Existing cloud applications are aging fast: We note that most existing applications continue to move through key support sunset dates, which usually triggers a customer need to look at upgrades and/or alternatives in the market. For example, Oracle Fusion Financials release in 2011 will see an end of Premier Support in 2016; Similarly Oracle Financials 12.1 released in 2009 will see an end of Premier Support in 2016.

Ways to play the theme Workday: Our recent meetings with management suggest the company remains confident in the Financial Management pipeline, product functionality, scalability and go to market. The pace of adoption appears to be the primary debate, but we think like CRM (50% cloud today) and HCM (35% cloud) before it, the shift of FM (15% cloud) is inevitable. The pace of adoption has actually accelerated, with signed customer count growing 40% in FY14, and 50% in FY16 through only three quarters. In addition, Workday continues to add ever larger customers, e.g., Unum (~20K employees) was the largest customer added in 2014 and AON (~65K employees).

2016 Software Sector Outlook

December 18, 2015 28

Exhibit 31: Workday’s financials customers are growing rapidly

0

20

40

60

80

100

120

140

160

180

200

FY13 FY14 FY15 FY16E

Financials Customers Live Financials Customers

Source: Company reports, RBC Capital Markets estimates

Other key business processes are being rapidly moved to the cloud While the largest core enterprise functions (CRM, HCM and ERP) are dominated by the key public players, other non-core processes that have long been the domain of in-house custom software, spreadsheets, or legacy ERP programs with limited functionality, are being attacked by fast-growing privates. We note the following areas:

Order to cash: Receiving and processing both B2B and B2C customer sales typically is categorized into different sub-processes such as Contracting, Pricing, Quoting (CPQ) and Revenue Management (especially in today’s increasingly subscription-focused economy). While these functions exist in the world of Enterprise Resource Planning (ERP), there are a number of emerging companies in this market. Zuora started as a subscription revenue management vendor; the company has evolved into a broader solution provider encompassing configure/ price/ quote, e-commerce and subscription revenue management. The company has an extensive customer list, which includes Dell, NCR, Informatica, Zendesk, Box and Tata Communications.

Spend management: Spend management encompasses the processes associated with direct and indirect spend by a company, including procurement, invoicing, travel and expense, sourcing, inventory management and contract management. SAP is the global leader in this market, given its strong position in core ERP and the acquisition of the market leaders in procurement (Ariba) and Travel and Expense (Concur). Other large competitors include Oracle (iProcurement) and IBM (Emptoris). However, we think there are companies to watch in this space that are addressing the market with easy to use cloud solutions that appear to be taking share.

Manufacturing: Long the domain of major ERP companies (SAP at the high end, Epicor and Infor in the mid-market), we are seeing a number of cloud first manufacturing process ERP companies emerge. Plex Systems, for example, provides cloud-based ERP exclusively focused on manufacturing. Its suite includes manufacturing execution systems, quality management systems, manufacturing specific customer relationship management, supply chain management and advanced planning and scheduling.

2016 Software Sector Outlook

December 18, 2015 29

Exhibit 32: Plex and its partner ecosystem

Source: Company reports

Vertical industry cloud software continues to create winners We have seen vertical-specific champions play for the winner-take-most nature of application software. Ellie Mae (ELLI) in mortgage compliance, quality and efficiency; Veeva Systems (VEEV) for life sciences; Fleetmatics (FLTX) for fleet management and vehicle tracking; and Q2 eBanking (QWTO) for online banking are just some of the public names that come to mind.

While the pace of adoption has differed, we note that once a vendor has achieved critical market share, it can usually outspend direct competitors and drive innovation that furthers its leading competitive position. In addition, we think by selling into discrete markets, vertical industry solution vendors can focus their sales spending more directly on a smaller set of customers and channels. This usually leads to achieving profitability earlier, which is evident across many of these names.

2016 Software Sector Outlook

December 18, 2015 30

4) Tech theme: Data as a differentiator The call is that the most innovative cloud application players are trying to differentiate their offerings through unique data insights – e.g., WDAY, CRM, ZEN, DWRE. This could be an important driver over time.

Cloud applications (SaaS) began in the 1990s with the formation of companies such as Salesforce and Netsuite, which brought the principles of the consumer internet to business applications. However, 15 years later it is hard to call the SaaS model a meaningful differentiator given that most applications that have been built since the early 2000s are SaaS and even incumbent vendors such as SAP and Oracle have acquired SaaS applications and (in the case of Oracle at least) tried to refactor their existing applications for the cloud.

Of course, the devil is in the details, and true cloud applications (multi-tenancy, single code base, high frequency of innovation) are quite a different beast from hosted applications (where instances are spun up on VMs) with the key determiner usually being gross margin profile (lower for hosted) and pace of innovation (slower for hosted).

However, we think true cloud applications have a durable competitive advantage based on the data that can be collected, analyzed and measured across users on the platform:

The use of the application is completely transparent to the application vendor. This has material advantages for the vendor, such as being able to tell when customers are at risk of leaving the platform (low usage) or which features development should focus on (those being used most often). This transparency was never available in the on-premise application world.

Aggregate data has significant value. Another advantage for cloud application vendors is the view on aggregate data across their customer base. While vendors don’t own their customers’ data, they still glean significant insights from it. This could be relatively simple (e.g., peak transaction times across a certain application) through to more sophisticated data (best practices that can be provided to other customers on the platform based on their characteristics).

Data network effects: In the cloud application world, there is greater opportunity to leverage networks from the data/ content. A simple example is Adobe’s use of the Behance Creative network alongside its creative tools. Creative professionals can post their portfolios of work on the network, which in turn can be seen by companies and agencies. This has driven new hiring and job features on the platform and so in some ways Behance has become a creative industry specific Linkedin tool used by professionals and recruiters alike.

Ways to play the theme Workday: We think Workday has always had a very strong focus on using data as a differentiator for its products and services. The Workday product is architected on an object-based, in-memory store, which is optimized for both transactions and analytic queries to run off the same data set at the same time. This provides the customer with real-time views of the business and negates the need for after the fact reports and analytics that are common amongst today’s enterprise applications.

Aneel Bhusri, co-CEO and founder of Workday, has made comments about how if the current generation of business applications were defined by cloud delivery, the next generation will be defined by their ability to leverage data for predictive means. Workday is therefore beginning to leverage data in a more significant way to differentiate its products. In late 2014, Workday announced Insight Applications (following the acquisitions of Identified and

Metadata can be used to both enhance existing features and drive additional revenue streams.

2016 Software Sector Outlook

December 18, 2015 31

Upshot earlier in the year), a new suite of applications for finance and human resources that harness the power of advanced data science and machine learning to equip customers to make better decisions. These applications are aimed at:

Predicting future outcomes: By pushing historic data from inside the Workday application and preconfigured third-party data through a machine learning algorithm, the company hopes to provide predictive insights for specific business scenarios.

Triggers and alerts: This same analysis can be run in the background of the application, such that triggers and alerts can be set, when the algorithm suggests a change in action to deliver against an outcome.

A new intelligent information engine: Workday SYMAN takes advantage of the latest technologies in data science and machine learning to map, classify and normalize definitions across multiple sources of data.

In 2015, Workday delivered Workday Talent Insights, the first insights application that predicts which employees are at risk of leaving based on historical data, job posting data and other third-party data. We expect further insight applications to be made available, especially in financial management as the company invests in planning functionality.

2016 Software Sector Outlook

December 18, 2015 32

Exhibit 33: Workday Talent Insights, which highlights retention risk

Source: Company reports

Salesforce: Salesforce has been increasing its focus on data across its platform in the last couple of years. First, the company launched Wave analytics in late 2014, a new cloud and mobile first business intelligence product. Second, the company has started to leverage assets from prior acquisitions into its sales cloud assets, such as Pardot for lead scoring and optimization in a B2B selling process. Finally, the company has made direct investments into analytics functional, including the acquisition of RelateIQ, to build new functionality into its core offering.

2016 Software Sector Outlook

December 18, 2015 33

SalesforceIQ is the result of the RelateIQ acquisition. The product is an overlay to Sales Cloud and provides data driven relationship intelligence to the deal process. The application collects communication data (such as emails and meetings) and allows users to add notes and comments to provide relevant information to other members of the team. The product provides alerts on suggested follow-ups to prospects and customers, so nothing in the sales pipeline is left to age without follow-up contact. The product also offers a close connections functionality, so that other relationships in an organization with the account can be found. Finally, the product is linked to other functionality in the platform so that events in SalesforceIQ are captured in areas like reports.

Exhibit 34: Suggested follow-ups and intelligence fields in SalesforceIQ

Source: Company reports

Zendesk: We think data services and predictive applications can be a durable differentiator for Zendesk. Today the company works with over 60K customers that collectively drive 4.6M communications a day and, on average, the company serves over 400 million daily web requests. Zendesk is building deeper capabilities in data analytics and machine learning on top of this rapidly growing data set.

Zendesk provides reporting and performance functionality. Within this, the company offers benchmarking capabilities. This allows customers to compare key stats like new ticket creation, first reply time and customer satisfaction to companies within the same industry, companies of the same size or companies with the same target audience. The benchmark is based on a 28-day rolling window of performance and uses average over mean (i.e., 50% of companies will be above and 50% below the benchmark).

In October, Zendesk launched a beta of Satisfaction Prediction, a machine learning and predictive capability for customer satisfaction. It uses historical data from satisfaction surveys to predict if an agent/ customer interaction is at risk of providing negative customer satisfaction. This solution examines the language used in the conversation, the latency between responses and the time to resolve the ticket in determining if the outcome will likely be viewed as positive or negative by a customer. This will also be used as an alternative to post-resolution surveys that have a very low participation rate. The service will be made generally available in early 2016.

2016 Software Sector Outlook

December 18, 2015 34

Exhibit 35: Benchmarking with Zendesk’s reporting functionality

Source: Company reports, RBC Capital Markets

Demandware: Like Salesforce, Demandware made an acquisition (CQuotient in 2014) to accelerate its predictive capabilities. Demandware is using advanced predictive science to help customers better understand the shopper journey, capturing online, offline customer and product data, promotions and content. This technology is being integrated into the core Demandware platform to provide two new products initially. Predictive email is an email personalization solution that tailors offers and promotions based on historic touch point data that a retailer has had with a customer. Predictive merchandising is a personalization solution to deliver product recommendations and personalize the online shopping experiences when a customer lands on a merchant's website.

Exhibit 36: Personalization of the shopping experience

Source: Company reports

2016 Software Sector Outlook

December 18, 2015 35

5) Tech theme: Amazon to the app layer The call is Amazon has moved from compute and storage, is attacking database and is now moving to the app layer (Workmail, Workdocs, etc). More business apps could be coming.

Amazon AWS continues to march forward as the disruptive technology force of our time. The business has grown from $4B run rate revenue at the end of CY13 to $8.3B in 3Q15. RBC expects this business to achieve >$25B run rate revenue exiting 2018. Amazon is covered by RBC Analyst, Mark Mahaney; Outperform; $670.65 priced as of market close 12/17/2015.

AWS was formed by Amazon taking the decade worth of experience in building out its e-commerce platform and exposing it to the outside world. At its heart is a set of dedicated software and operating procedures that allows Amazon to drive performance, reliability, operational quality and security at incredible scale. Amazon also allowed access to its catalogue of services and innovative developers started to leverage both the infrastructure and the services that Amazon was sharing with the outside community.

Exhibit 37: The shift toward SaaS, PaaS and IaaS continues unabated

AWS revenue growth has been accelerating . . .

3,1003,546 3,851

4,2304,644

5,1605,979

6,895

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Dec

-13

Mar

-14

Jun

-14

Sep

-14

Dec

-14

Mar

-15

Jun

-15

Sep

-15

4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15

0%

10%

20%

30%

40%

50%

60%

70%

LTM AWS Revenue Y/Y growth

. . . with price reductions as a driving force

Source: Company reports, RBC Capital Markets estimates

It starts with better economics . . . Superior economics has been the primary driver of AWS historically. The cost of building and maintaining reliable infrastructure in a multi-datacenter model could be as high as 70% of the total cost of provisioning IT for the enterprise. By exposing this infrastructure, Amazon can reduce the cost of provisioning IT for a normal company. Amazon also recognized that utilization of infrastructure resources at an individual company level is dramatically low. So Amazon provided a model where a company could achieve 100% utilization of the IT resources it was paying for. Pricing services in an on-demand fashion with a utility pricing model was key and in 2006 AWS delivered the first storage service (S3) and elastic compute (EC2).

Superior economics remains at the heart of everything Amazon does. The company’s mentality is one of building the best services and pricing them at a level that customers struggle to match elsewhere. However, we think there has been a subtle shift in the value proposition of AWS over the last three years to one where better economics has been augmented by more services that are allowing customers to innovate at a faster speed on AWS than they would elsewhere.

AWS started with superior economics . . . but is driving toward superior innovation

2016 Software Sector Outlook

December 18, 2015 36

Exhibit 38: The evolution of AWS

Infrastructure Applications

WorkDocs

Mobile Analytics WorkMail