20150128 indogas gas natural...

TRANSCRIPT

Gas Natural Fenosa´s experience developing gas infrastructure

January 2015

experience in gas infrastructure

1

- Gas Natural Fenosa´s overview

Index

- Natural gas world consumption

- Infrastructure Planning

- Gas Natural Fenosa´s Experience

- Gas Infrastructure in Indonesia

- Conclusions- Conclusions

overview

Natural gas world consumption

Experience

Gas Infrastructure in Indonesia

2

Gas Natural

Fenosa

Gas Natural

Fenosa

3

Originsand history

1843 First gas company founded in Spain.

1969 Pioneer in distribution of natural gas in the Iberian Peninsula.

1991 Creation of Gas Natural SDG and integration of the gas distribution sector in Spain (merger of Catalana de Gas, Gas Madrid and Repsol Butano's gas pipeline assets).

1992 Start of international expansion in Latin America, entering Argentine market

2000 First electricity sales in

2009 Acquisition of Unión Fenosa concluded

2010 Launch of Gas Natural Fenosa brand.

1992 Start of international expansion in Latin America, entering Argentine market

First electricity sales in the liberalised Spanish market.

4

PortugalLNG/NG and electricity sales

SpainTransmission, distribution, gas and electricity sales, power generation, upstream, LNG/NG sales and infrastructure

The Group in the World

MexicoGas distribution,power generation

Puerto RicoLNG/NG infrastructure,power generation

and infrastructure

PanamaElectricity distribution, power generation

Dominican RepublicPower generation

Costa RicaPower generation

MoroccoLNG/NG Infrastructure

AngolaLNG/NG Infrastructure

AlgeriaGas supply, LNG/GN infrastructure

power generation

BrazilGas distribution

ArgentinaGas distribution

ColombiaGas and electricitydistribution

PeruGas distribution

ChileGas and electricitydistribution

United KingdomLNG/NG sales

FranceLNG/NG sales

ItalyGas distribution and sales, regasification projects,

BelgiumLNG/NG sales

NetherlandsLNG/NG sales

LuxembourgLNG/NG sales

MoldovaElectricity distribution

regasification projects, LNG/NG sales

JapanLNG/NG sales

IndiaLNG/NG sales

GermanyLNG/NG sales

South AfricaCoal mining

KenyaPower generation

AustraliaPower generation projects

LNG/NG sales

OmanGas supply, LNG/GN infrastructure

AngolaLNG/NG Infrastructure

EgyptGas supply, LNG/GN infrastructure

5

Natural Gas

World

Consumption

6

Primary Energy Natural Gas World Consumption

1973 1980 1990

1688 (19%)1688 (19%)

1234(17%

)

1234(17%

)

977(16%)977

(16%)

World NG Consumption (Mtoe)

Liquefaction Capacity (Mtpa)

1688 (19%)1688 (19%)

1234(17%)1234(17%)

2

146.556

LNG Carrierrs

Nº

m3

23

2.645.321

2 30 606

80RegasificationCapacity (Mtpa)

Source: IEA, WoodMackenzie, IHS

1990 2000 2012

2085(20%)2085(20%)

2848(21%)2848(21%)

1688 (19%)1688 (19%)

642

1688 (19%)1688 (19%)

7

44

4.051.301

92

7.523.440

417

32.447.957

60106

242206246

Infrastructure

Planning

8

Infrastructure Planning NG Value Chain

(DIRECT SUPPLY)

UPSTREAM LIQUEFACTION SHIPPING Gas

Reserves

Infrastructure planning must be done coherent and being coordinated in the all the value chain

(DIRECT SUPPLY)

SHIPPING REGASIFICATON TRANSPORT

AND DISTRIBUTION

Gas Sales

9

Infrastructure planning must be done coherent and being coordinated in the all the value chain

Security of supply

Infrastructure Planning The EnergyTrilemma

Sector Sustainability

Is the system sustainable in the long term ?

4

3

Is the infrastructure being

Cost Efficiency

Is the infrastructure being planned and implemented at low cost and high quality standards ?

Security of supply

Are we securing the supply in the long term ?

1

Sector Sustainability

2

Are we getting the fuel to the

10

Demand Orientation

Are we getting the fuel to the costumers at prices affordable by them?

Infrastructure Planning Key Questions to be Answered

Supply Demand

�Current sources of supply ?

�Status of the infrastructure ?

�Availability of domestic reserves to be developed in the future ?

�Agenda with potential suppliers ?

� Availability ofother alternatives as shale gas or CBM ?

�Demand structure ?

�Distribution model ?

�Economic growth pushing demand ?

�Potential for NG substitution to other fuels?

�Current consumer prices ?

�Business model for each agent in the value chain ?

�Price structure ?

�Current consumer prices ?

�Subsidies in the industry ?

Demand Others

Demand structure ?

Distribution model ?

Economic growth pushing demand ?

Potential for NG substitution to other fuels?

Current consumer prices ?

�Actual & potential infrastructure?

�Important players in the sector ?

�Technical capabilities to develop the industry ?

� Financing of the future investment needs ?

� Private sector participation in the

11

Current consumer prices ?

Subsidies in the industry ?

� Private sector participation in the industry ?

� Stability in the regulatory framework ?

GNF

ExperienceExperience

12

UPSTREAM MIDSTREAM

GNF ExperiencePresence in the value chain

LIQUEFACTION PLANTS LNG TRANSPORT

Plant Country Capacity

Damietta (40%) Egypt 5,5 Mtpa

Qalhat (7,4%) Qatar 3,3 Mtpa

≈ 2,5 Mtpy liquefaction capacity 8 LNG carriers + 4 under construction

Ship Name Since

Artic Spirit 1993

Cadiz Knutsen 2004

Castillo de Villalba 2003

Catalunya Spirit 2003

Iberica Knutsen 2006

LNG Libra 1979

Polar Spirit 1993

INTERNATIONAL CONECTIONS

Pipeline Country Capacity

≈ 20 bcmy of international conections

Plant Country

Reganosa (18%) Spain

Sagunto (42,5%) Spain

Ecoeléctrica (50%) P. Rico

Source: GNF Corporate Reports

≈ 8 bcm of regasification

Polar Spirit 1993

Ribera del Duero 2010

REGASIFICATION PLANTS

Pipeline Country Capacity

Medgaz (15%) Algeria 8 bcmy

MEG Algeria 12,5 bcmy

MIDSTREAM DOWNSTREAM

GN DISTRIBUTION PIPELINELNG TRANSPORT

Country Since km

Spain 1969 46.678

Italy 2001 6.958

Mexico 1997 18.874

Argentina 1992 24.496

Brasil 1997 6.661

Colombia 1997 20.293

Chile 2014 N.D

+125.000 km of pipelines worldwide 8 LNG carriers + 4 under construction

Since Capacity (m3)

1993 87.000

2004 135.000

2003 135.000

2003 135.000

2006 135.000

1979 126.000

1993 88.000

Country Capacity

Spain 3,5 bcm

Spain 12,3 bcm

Rico 4 bcm

13

Chile 2014 N.D

regasification capacity

1993 88.000

2010 173.000

REGASIFICATION PLANTS

+17 Tbtuy of LNG distribution by truck

LNG DISTRIBUTION TRUCK

Plant Country Capacity

Spain Spain 17 Tbtuy

France France 2,2 Tbtuy

Peru Peru 2,2 Tbtuy

GNF ExperienceContribution to the sector in Spain

Since the 70’s, strong contribution to the development of the Sector in Spain

40.000

50.000

60.000

70.000

80.000

90.000

NATURAL GAS NETWORK EVOLUTION1985-2013 (km)

0

10.000

20.000

30.000

1985 1990 1995 2000 2005 2010 2013

Total Spain GNF

Source: Sedigas, GNF Corporate Reports

Since the 70’s, strong contribution to the development of the Sector in Spain

15%

6%

6%

20%

Others

NG SALES 2012 (% MARKET SHARE)

Source: CNMC

54%

14

+5.000 M$ invest in the last two decades

GNF ExperienceLong term position in Latam.

200

250

300

350

400

450

500

GNF LATAM. GAS DISTRIBUTION CAPEX 1992-2012 (MILLION $)

0

50

100

150

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Mexico Colombia Argentina Brasil

Source: GNF Corporate Reports

+50.000 km of new pipelines in Latam. since 1995

69.054

64.132

56.7632005

2010

2013

GNF LATAM. PIPELINES LENGTH EVOLUTION 1995-2013 (km)

56.763

42.079

17.3391995

2000

2005

15

Market Characteristics

• Upstream and LNG infrastructure

GNF ExperienceKey factors in Latam. emerging markets

• Upstream and LNG infrastructure

•T&D sector with active private participation

• Tariffs and terms regulated by CRE

• Growth potential market

• Regular gas Consumption for power

• Upstream infrastructure

Mexico

•T&D sector with active mostly local participation

• Tariffs and terms regulated by CREG

• Mature Market

• Seasonal gas consumption for power

Colombia

Key factors in the short term

. emerging markets

• Absence of upstream investment

• Absence of a well interconnected high pressure grid

• Uncertain price policy of commodities

• Institutional Coordination

• Absence of upstream investment

16

• Absence of LNG infrastructure

• Absence of a well interconnected high pressure grid

• Power sector driven by availability of hydro generation affecting gas sector

Market Characteristics

•Upstream and LNG infrastructure

GNF ExperienceKey factors in Latam. emerging markets

•Upstream and LNG infrastructure

• Transport monopoly and private participation in Distribution

• Tariffs and terms regulated by state regulators

•Growth potential market

• Seasonal gas consumption for power

• Upstream and LNG Infrastructure

Brazil

• T&D sector with private and a few nationalised companies

• Tariffs and terms regulated by ENARGAS

•Mature market

• Regular gas consumption for power

Argentina

Key factors in the short term

• Uncertain price policy of commodities

. emerging markets

private participation in Distribution • Strong influence of Petrobras and local state owned companies

• Absence of a well interconnected high pressure grid

• Power sector driven by availability of hydro generation affecting gas sector

• Price policy affecting security of supply

17

T&D sector with private and a few nationalised companies• Price policy affecting security of supply

• Absence of investment in upstream and transport

• Unclear signals by regulator

• Absence of incentives to private investors

SPAIN

GNF ExperienceLNG supply by truck - “Virtual transport system”

Business Scheme

FRANCE

PERU

� GNF holds regas capactity in the 6 LNG plants operatingin Spain.

� 73 satellite plants to supply 227 large industrialcustomers (17 Tbtu/year).

� Strong development in the last 20 years as a temporarysolution until the arrival of gas pipeline

“Virtual transport system”

� LNG competiviness vs other fuels (40-50 %).

� Consolidated Technology and Logistics.

� First company in France in commissioning this kind ofplants.

� 15 new industrial customers addressed in the last twoyears with a total volume of 2,2 TBtu/year.

� Ambitious development plan just launched: 73 potentialclientes with a volume of 5 Tbtu/year.

18

� GNF was awarded the public concession for CGD inSouthwest Peru with deliveries through LNG by truck inJuly 2013.

� “Virtual transport system” using tanker trucks bringingliquefied natural gas from the Peru LNG liquefactionplant (950-1000 km) to the satellite plants in the 4 cities,and developing a distribution and sales network.

� 2,2 Tbtu/year to over 170.000 customers in 4 differentcities: Arequipa, Moquegua, Tacna and Ilo.

Gas

Infrastructure

Indonesia

19

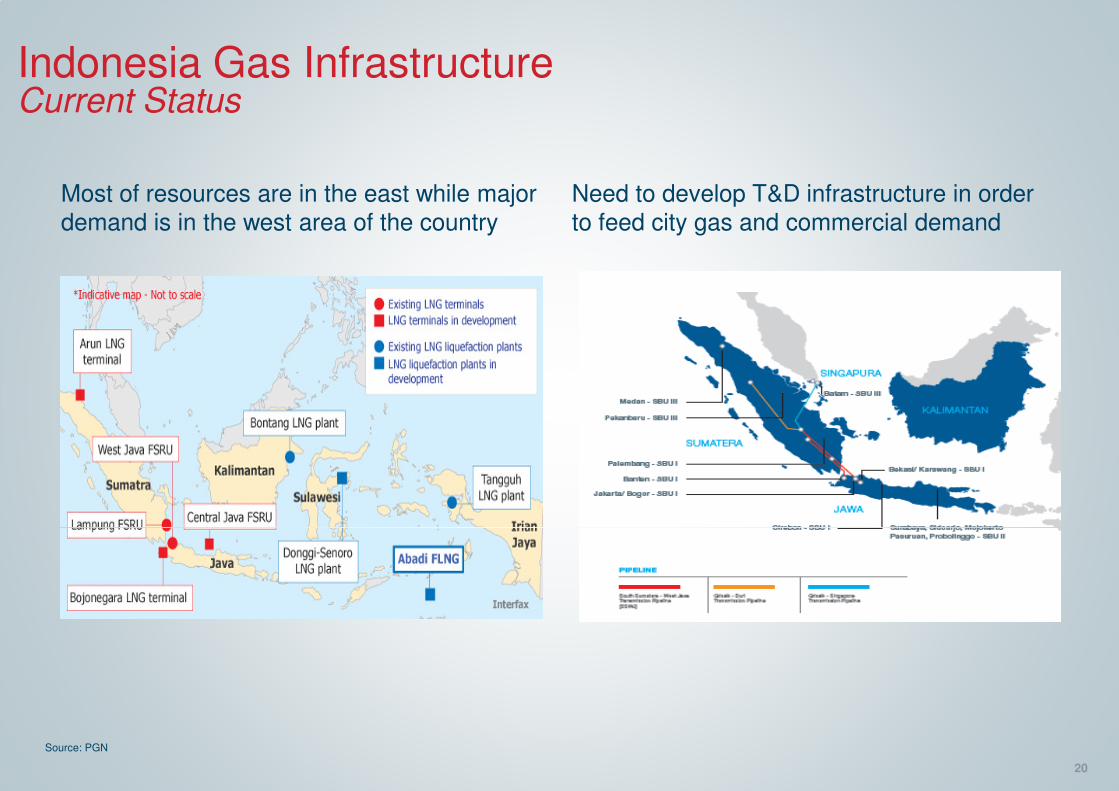

Most of resources are in the east while major demand is in the west area of the country

Indonesia Gas InfrastructureCurrent Status

Source: PGN

Need to develop T&D infrastructure in order to feed city gas and commercial demand

20

Indonesia Gas InfrastructureGas Market

4,81

Compound annual growth rate (CAGR02-12) of 5% in the last decade push by industrial and power sector

Natural Gas Consumption (bcm)

29,3633,15

6,15 7,02 10,37 12,377,56

11,05

14,1415,63

7,873,59

4,684,81

2002 2008 2010 2012

Power Industrial Transport Residential Commercial & Public Services Non Energy Use

Java and Sumatra concentrate 84% of the total consumption

21,65 21,76

29,36

Source: IEA

Sumatera

Java

Kalimantan

SalawesiPapua

0

18,3

9,5

4,7

Natural Gas Consumption by Geographic Area (bcm)

Source: IEA

Industrial and power sector concentrates the major consumption with more than 80% overt total natural gas demand

Natural Gas Demand 2012 (%)

Organic and fuel substitution growth is expected in the power and industrial sector

37%

47%

1% 15%Power

Industrial

Transport

Residential

Commercial & Public Services

Non Energy Use

Source: IEA

21

2012 2025

33,25

Organic Growth

+Fuel Sub.

50-60

Local Production Depleting

Indonesia Gas InfrastructureKey Issues for Future Planning

Island Chain configuration

Power Generation Power Generation & Industry Diesel Use

Consumer final price of Energy

LNG Import Facilities combined with E&P efforts

Potential for Small Scale LNG

NG Fuel

22

NG Fuel Substitution

Subsidies and price structure strategy

ConclusionsConclusions

23

Infrastructure Planning Infrastructure Planning

Industry Development Key Success Factors

Collaboration Collaboration Infrastructure Planning Infrastructure Planning Collaboration Collaboration

Authorities

Users

Private Sector

Collaboration Collaboration Stable Regulatory

Framework Stable Regulatory

Framework Collaboration Collaboration

Framework Framework

Authorities

Regulator

24

Financing Agencies

Thank you.

Terima Kasih

Thank you.

Kasih.

This presentation is the property of Gas Natural Fenosa. Both its subject matter and its graphic design is for the exclusive use of its staff.

©Copyright Gas Natural

This presentation is the property of Gas Natural Fenosa. Both its subject matter and its graphic design is for the exclusive use of its staff.

Copyright Gas Natural SDG, S.A.