2013 john gregg-navigate consult-trans cosmos-china mkt entry-call centre

TRANSCRIPT

-1-

ENTRY FOR PROFIT

TRANS-COSMOS INC. CHINA ENTRY STRATEGY PRESENTATION

February 8, 2013

John Gregg,

Principal, Navigate Consulting Pty Ltd

-2-

AGENDA

Executive Summary

Call Center Business

• Market Overview

• CC Customer Segmentation

- In-house users

- Outsourcers

• Demand

• Customer

• Economics

• Competition

• Recommendations

- Success business model

- Partnering strategy

E-Commerce Market Overview

TCI Tianjin

• Current Situation Analysis

• Recommendations

-3-

AGENDA

Executive Summary

Call Center Business

• Market Overview

• CC Customer Segmentation

- In-house users

- Outsourcers

• Demand

• Customer

• Economics

• Competition

• Recommendations

- Success business model

- Partnering strategy

E-Commerce Market Overview

TCI Tianjin

• Current Situation Analysis

• Recommendations

-4-

CHINA IS BECOMING A HIGHLY DYNAMIC CC MARKET

China’s call center market took off in 1998 with an annual growth rate over 100%

• Non-paging market size reached 364,000 seats in 2012

However past growth was largely driven by demands from administrative driven sector

• In 2011, over 60% CC demand comes from four pillar industries: Banking, Post Services, Fixed-line Telecom, and Insurance

• Distinctive purchasing behavior identified for these purchases

Future growth will be propelled by service oriented and call centres segments

• call centres market will grow at least 35% a year for the next few years

- However large variance exists for call centres segment growth

Overall, China Call Centres created over 360K seats in 2012 and 430K seats in 2015

-5-

AND IS GAINING GROUND ON KEY DECISION CRITERIA

Multiple call centres destinations around the world have sprung up as supplier bases.

• Besides India and China, popular locations include the Philippines, Malaysia, Romania, Ukraine, Brazil and Mexico.

Multiple surveys point to new location preferences and trends:

• Alternatives to India are being mixed in with greater frequency. Latin America and China ranked as the most popular alternatives to India in one recent survey.2

• According to a number of rankings, China is gaining ground on criteria such as financial attractiveness, people and skills, and business environment.

• Of 30 top destinations identified as best for offshore Call Centre operations, ten countries were from Asia (China, India, Thailand, Vietnam, Australia, New Zealand, Singapore, Malaysia, Pakistan, and the Philippines). Thailand was a newcomer to the list, as were a few other emerging markets such as Egypt, Morocco and Panama.

-6-

Currently, low-price/standard service vendors remain profitable

• Utilization, and therefore, long-term customers, is the key for profitability

• However, high-priced call centres solutions not widely accepted by the market

But high-end services will reach 65% of share off total market by 2014

• We are encouraged by recent positive news on clients’ long-term commitments to high-end outsourcers

High-end outsourcers can win the game by aggressively establishing long-term client base, and targeting various call centres opportunities along the value chain

• Five successful strategies identified for new customer development

• Telemarketing and value-added information service most likely to be outsourced

CC OURSOURCERS ARE STILL EXPLORING

-7-

TCI SHOULD PARTNER WITH RIGHT LOCAL CC OUTSOURCERS

A partnering strategy is essential for TCI to capture the great opportunities in China

• TCI lacks a bunch of local capabilities, while time is contingent

TCI should target both money making, and money losing tech advanced outsourcers during negotiation process, based on two plausible partnership strategies

• Money making ones: share profits and leverage local strength

• Money losing ones: control and negotiate for a bargain deal

Considering the limited number of candidates in China and TCI’s tight schedule, a broader search can strengthen TCI’s negotiation position

Five promising outsourcers identified during the interview process

• Money making ones: China Motion, 800 Teleservices, and Compaq-Star

• Money losing ones: TCY, ITS Shanghai

-8-

TCI-TJ: RSTRUCTURING AND BUILDING STRATEGIC ALLIANCES

TCI-TJ experienced difficulties due to both promotion and management issues

• Though improving, the firm is intrinsically uncompetitive in China market

It should restructure for better performance…

• Redefine corporate missions and strategies

• Restructure project arrangement, reporting, measurement and incentive systems

• Refocus its sales on Japanese companies in China and in Japan

… and find strategic alliance for TCI’s China expansion

• TCI should only partner with prestigious local software company or system integrators

• Wiseway screened all the potential candidates lists and funneled down 5 most promising companies for TCI’s further contact

- Longshine; Global eForce; eBIS; Modern Computer; Huateng Software

-9-

AGENDA

Executive Summary

Call Center Business

• Market Overview• CC Customer Segmentation

- In-house users

- Outsourcers

• Demand

• Customer

• Economics

• Competition

• Recommendations

- Success business model

- Partnering strategy

E-Commerce Market Overview

TCI Tianjin

• Current Situation Analysis

• Recommendations

-10-

CALL CENTRE INDUSTRY WILL REACH 380-400K SEATS IN 2014

Illustration

• Identify major driving factors to CC adoption- market competition and service awareness- telecom charges and phone penetration

• Quantify relationships between drivers and CC adoption- here we used US benchmark

• Project CC development by forecasting development of drivers

• Project CC penetration in major user’s industries- banking, telecom, insurance …

• Add up numbers of each industry to give a CC market overview

• Interview industry experts or knowledgeable industry practitioners for their opinion of CC market growth

- system integrators and experts

2009 (1)

(’000 seats)

158

132

145

2014 projection(1)

(’000 seats)

390

337

N.A.

Driving

factor

analysis

Bottom-up

analysis

Experts

opinions

(1) Without paging company

-11-

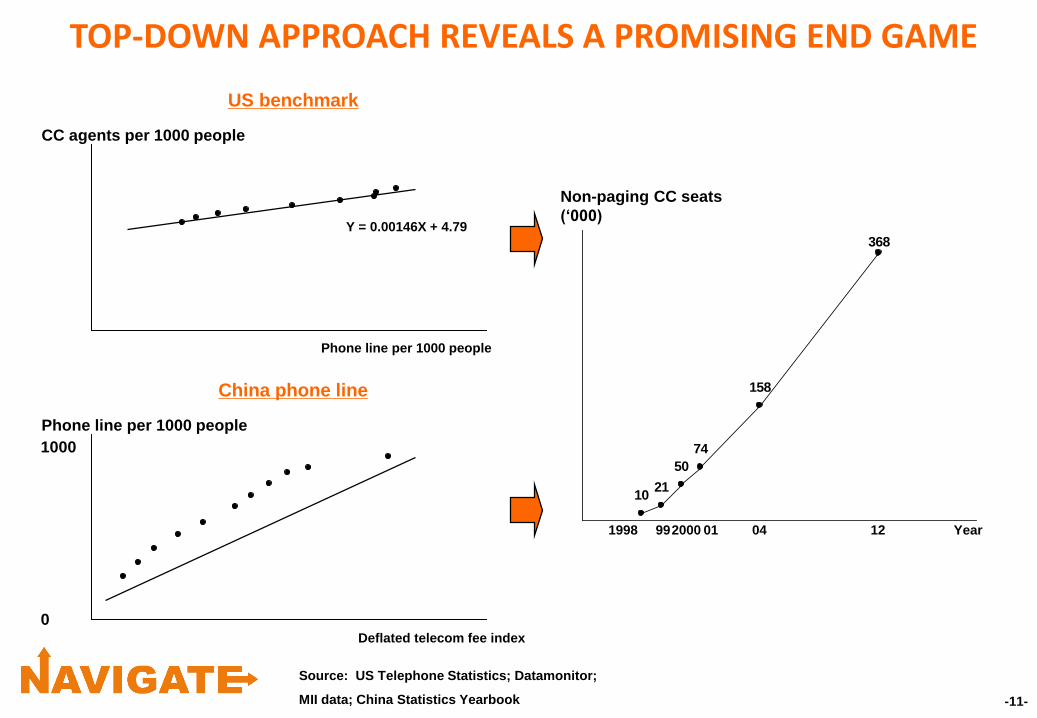

TOP-DOWN APPROACH REVEALS A PROMISING END GAME

Phone line per 1000 people

CC agents per 1000 people

US benchmark

Y = 0.00146X + 4.79

Deflated telecom fee index

Phone line per 1000 people

China phone line

1021

50

74

158

368

Year

Non-paging CC seats

(‘000)

Source: US Telephone Statistics; Datamonitor;

MII data; China Statistics Yearbook

1998 992000 01 04 12

1000

0

-12-

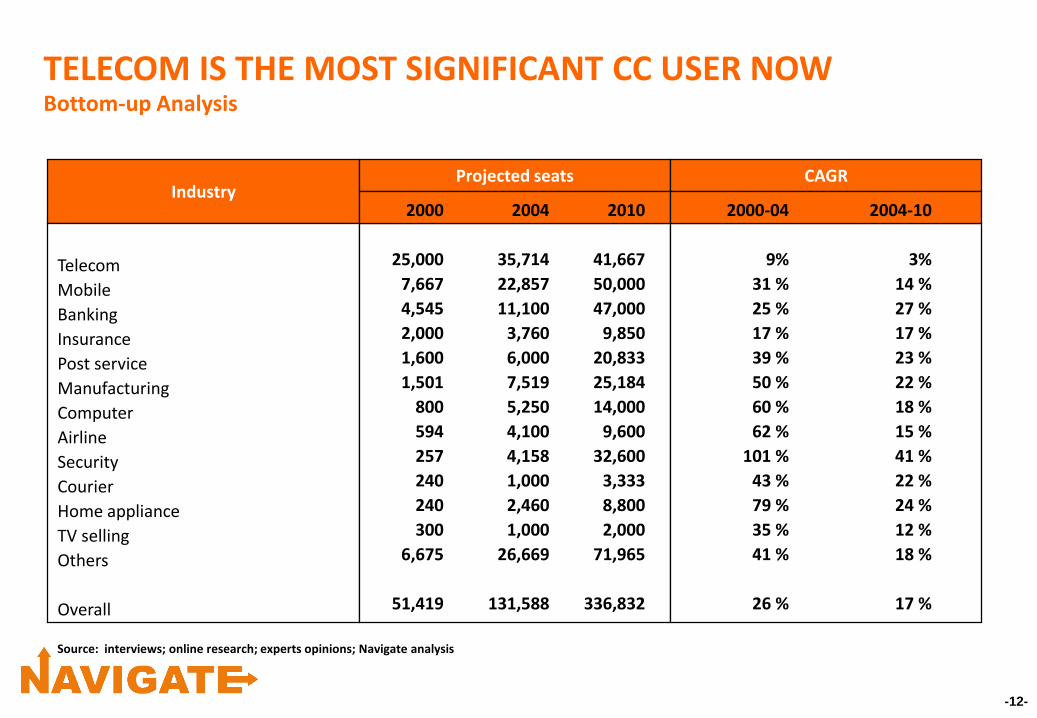

TELECOM IS THE MOST SIGNIFICANT CC USER NOWBottom-up Analysis

Industry

Telecom

Mobile

Banking

Insurance

Post service

Manufacturing

Computer

Airline

Security

Courier

Home appliance

TV selling

Others

Overall

Projected seats CAGR

2000

25,000

7,667

4,545

2,000

1,600

1,501

800

594

257

240

240

300

6,675

51,419

2004

35,714

22,857

11,100

3,760

6,000

7,519

5,250

4,100

4,158

1,000

2,460

1,000

26,669

131,588

2010

41,667

50,000

47,000

9,850

20,833

25,184

14,000

9,600

32,600

3,333

8,800

2,000

71,965

336,832

2000-04

9%

31 %

25 %

17 %

39 %

50 %

60 %

62 %

101 %

43 %

79 %

35 %

41 %

26 %

2004-10

3%

14 %

27 %

17 %

23 %

22 %

18 %

15 %

41 %

22 %

24 %

12 %

18 %

17 %

Source: interviews; online research; experts opinions; Navigate analysis

-13-

AGENDA

Executive Summary

Call Center Business

• Market Overview

• CC Customer Segmentation

- In-house users

- Outsourcers

• Demand

• Customer

• Economics

• Competition

• Recommendations

- Success business model

- Partnering strategy

E-Commerce Market Overview

TCI Tianjin

• Current Situation Analysis

• Recommendations

-14-

CC MARKET ROUGHLY SEGMENTED INTO FOUR CATEGORIESAccording to Area of CC Usage, and Willingness to Outsource

Selected industry examples

Willingness

to

outsource

High

Low

Service-oriented

call centres

Generic service

Admin-driven

Securities

Home appliance

Computer/technology

Courier service

Publication

TV selling

MessagingTravel

Simple order taking

Paging

Telecom

Insurance

Bank

Post service

Community service

Utility

Core area Non-core area

Area of CC usage

-15-

THREE CRITERIA TO DISTINGUISH CORE AND NON-CORE AREA

Industry

Core Area

• Securities• Courier service• Computer/technology

“Grey Area”

• Home appliance• Banking• Insurance• Publication• Telecom• Traveling

Non-core Area (generic)

• Paging service• Messaging• TV selling• Utilities

Functionality • Technical assistance• Aftersales service• Customer complaint

settlement

• Sourcing/supplier coordination

• Customer inquiry settlement• Telemarketing

• Message delivering• Simple order taking

Call Center’s impact to overall business- Core: When CC function is critical to the performance of the industry

Confidentiality requirement- Core: If the industry/functionality commands strict confidentiality

Call Center operational complexity- Core: If operating CC in this industry requires great sophistication

Criteria

Many industries have both core and non-core areas

-16-

AGENDA

Executive Summary

Call Center Business

• Market Overview

• CC Customer Segmentation

- In-house users

- Outsourcers

• Demand

• Customer

• Economics

• Competition

• Recommendations

- Success business model

- Partnering strategy

E-Commerce Market Overview

TCI Tianjin

• Current Situation Analysis

• Recommendations

-17-

ADMIN-DRIVEN SEGMENT: MOST IMPORTANT FOR NOW

High % in total new CC demand Driven by “Pillar industries”

Demand surged in a group of China’s important industries since 2004, aiming to improve service level

• Bank• Post service• Fixed-line telecom• Insurance

Required mostly mid-to-high end call center solutions (Nortel, Lucent, IBM, Huawei…)

• Big, monopolized, profitable corporations• High cost of failure• Budget approval from above• Often in conjunction with structural reform

1998 1999 2000

4.9

# of new CC seats (’000)

Year

Admin-driven

11.2

29.5 Total new demand

Admin-driven

66%

76%

62%

Source: Navigate Consulting modeling

-18-

UNIQUE THREE-TIER DECISION MAKING PROCESSSystem Integrators Should Put Efforts to All

Top-down initiatives

Advocate improving service standard

• Make “service facilities” an evaluation criteria

• May suggest call center as an option

Determine rolling out call centers in the corporation

Raise a list of recommended system integrators

• Present the list to branch companies

Set a budget for different branch companies

Decide call center size and sophistication based on corporate budget

Negotiate and select a system integrator mostly suitable to the branch’s requirements

SI should pay attention to Ministry’s recent

service improvement incentive

Ministry

SI should approach promising corporate

headquarters in advance to get the name on the

list

Corporate headquarter

SI should put most efforts to influence branch company’s

selection

Provincial/regional branches

Admin-driven

-19-

call centres ALMOST NEVER AN OPTION FOR ADMIN-DRIVEN COMPANIES

Call centres is not considered an option for CC adoption at corporate level

• Worried about unforeseeable consequences

• Money saving is not a priority for these big, monopolized SOEs

• Unable to distinguish different conditions in different geography

- some areas don’t have satisfactory outsourcers

Politically risky for branch managers to be “creative”

• If using outsourcers, branch managers have to bear all responsibilities

- potential for failure is considerable

• CC construction budget would be in vain if not used up

- while call centres budget needs to be reported for upper approval

Only exception is Guangzhou Mobile Company’s call centres of its “Mobile Secretary” service

• By nature a paging service: Ideal to be done by a paging company

• “Mobile Secretary” service is not planned and budgeted from the corporation (China Mobile)

• Guangzhou’s business practice is more liberal than rest of China

Admin-driven

-20-

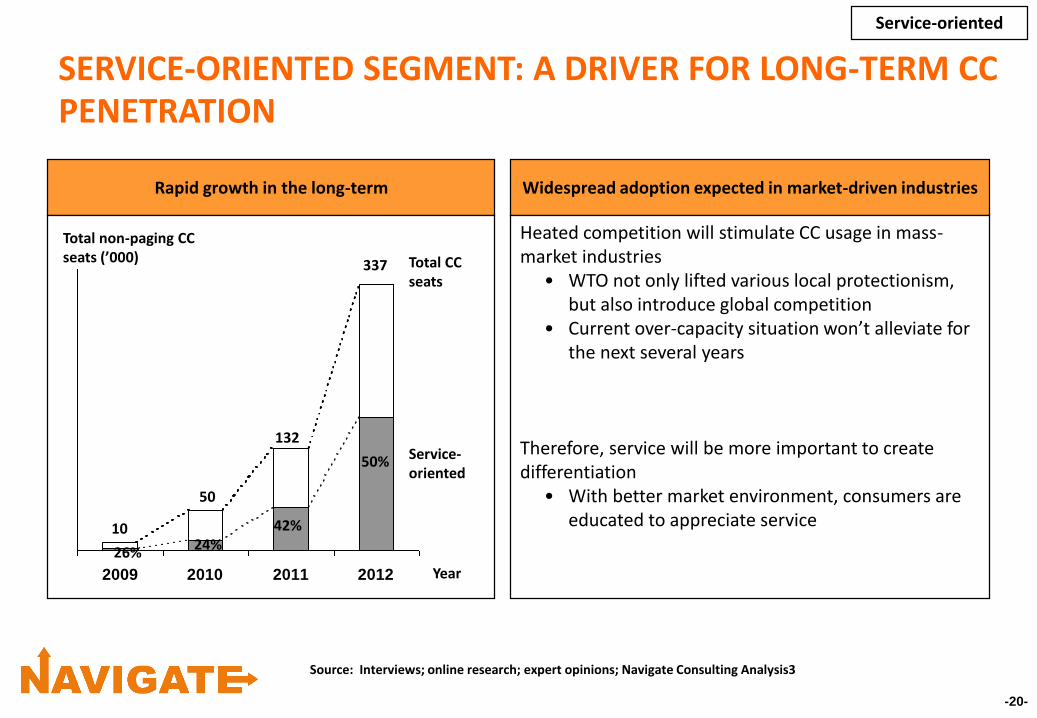

SERVICE-ORIENTED SEGMENT: A DRIVER FOR LONG-TERM CC PENETRATION

Rapid growth in the long-term Widespread adoption expected in market-driven industries

Heated competition will stimulate CC usage in mass-market industries

• WTO not only lifted various local protectionism, but also introduce global competition

• Current over-capacity situation won’t alleviate for the next several years

Therefore, service will be more important to create differentiation

• With better market environment, consumers are educated to appreciate service

Total non-paging CC seats (’000)

Service-oriented

2009 2010 2011 2012

10

Year

50

337 Total CC seats

Service-oriented

26% 24%

50%

132

42%

Source: Interviews; online research; expert opinions; Navigate Consulting Analysis3

-21-

MORE INDUSTRIES ARE LIKELY TO ADOPT CC OVERTIME

CC Adoption

AreaHome appliance

Automotive

Computer

Mobile

Securities

Retailing

Petrochemical

Distribution

FMCG(1)

Taxi

Textile

Machinery

Chemical

Publication

Health care

Government

Entertainment

Broadcasting/TV Aviation

General Technology

High

Moderate

Low

Competition

intensity

High

Horizontal will

extend overtime

Importance of service

(1) Fast-moving consumer goods

Source: Interviews; literature research summaries; Navigate Consulting Analysis

Horizontal will

extend overtime

Service-oriented

-22-

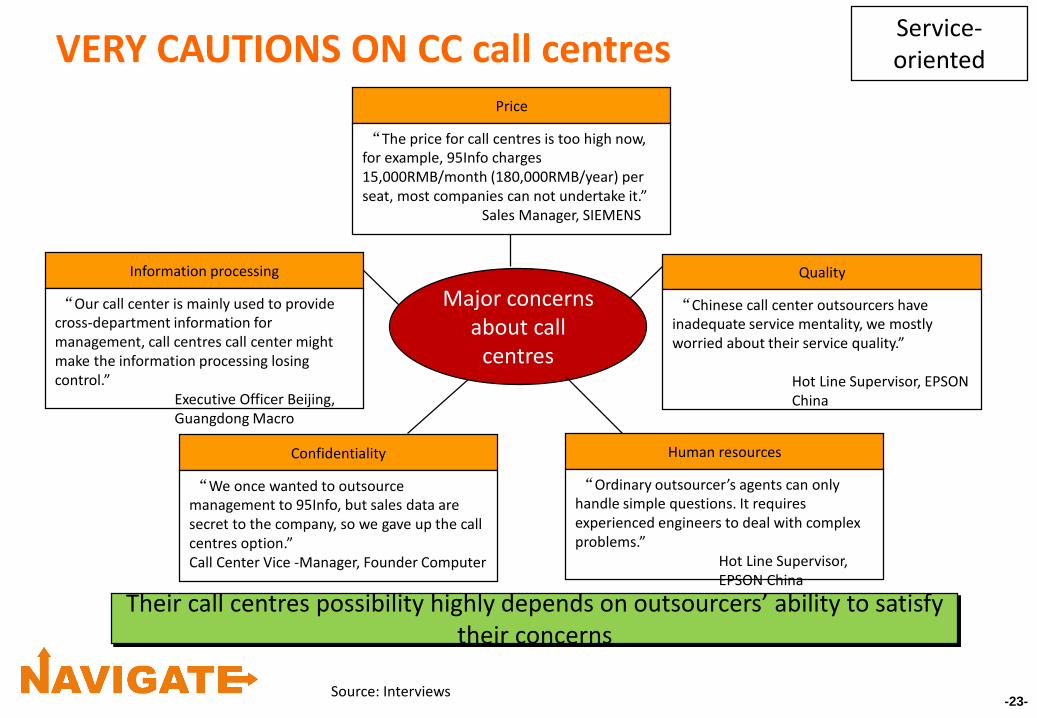

COMPANIES QUITE SELECTIVE ON CC USAGE

Not blindly chasing after high-end solutionsIntegrating call centers with its core business

practice

Interviews summary

Source: Interviews

%

Investment per seat (’000 RMB)

54%

31%

15%

0

0.1

0.2

0.3

0.4

0.5

0.6

Oct-70 70-150 150-250

Interviews summary%

Aftersales service

44%

31%

19%

6%

Order taking

Information service

Telemarketing10-70

Service-oriented

-23-

VERY CAUTIONS ON CC call centresPrice

“The price for call centres is too high now, for example, 95Info charges 15,000RMB/month (180,000RMB/year) per seat, most companies can not undertake it.”

Sales Manager, SIEMENS

Quality

“Chinese call center outsourcers have inadequate service mentality, we mostly worried about their service quality.”

Hot Line Supervisor, EPSON China

Human resources

“Ordinary outsourcer’s agents can only handle simple questions. It requires experienced engineers to deal with complex problems.”

Hot Line Supervisor, EPSON China

Confidentiality

“We once wanted to outsource management to 95Info, but sales data are secret to the company, so we gave up the call centres option.”Call Center Vice -Manager, Founder Computer

Information processing

“Our call center is mainly used to provide cross-department information for management, call centres call center might make the information processing losing control.”

Executive Officer Beijing, Guangdong Macro

Major concerns about call

centres

Their call centres possibility highly depends on outsourcers’ ability to satisfy their concerns

Source: Interviews

Service-oriented

-24-

AGENDA

Executive Summary

Call Center Business

• Market Overview

• CC Customer Segmentation

- In-house users

- Outsourcers

• Demand

• Customer

• Economics

• Competition

• Recommendations

- Success business model

- Partnering strategy

E-Commerce Market Overview

TCI Tianjin

• Current Situation Analysis

• Recommendations

-25-

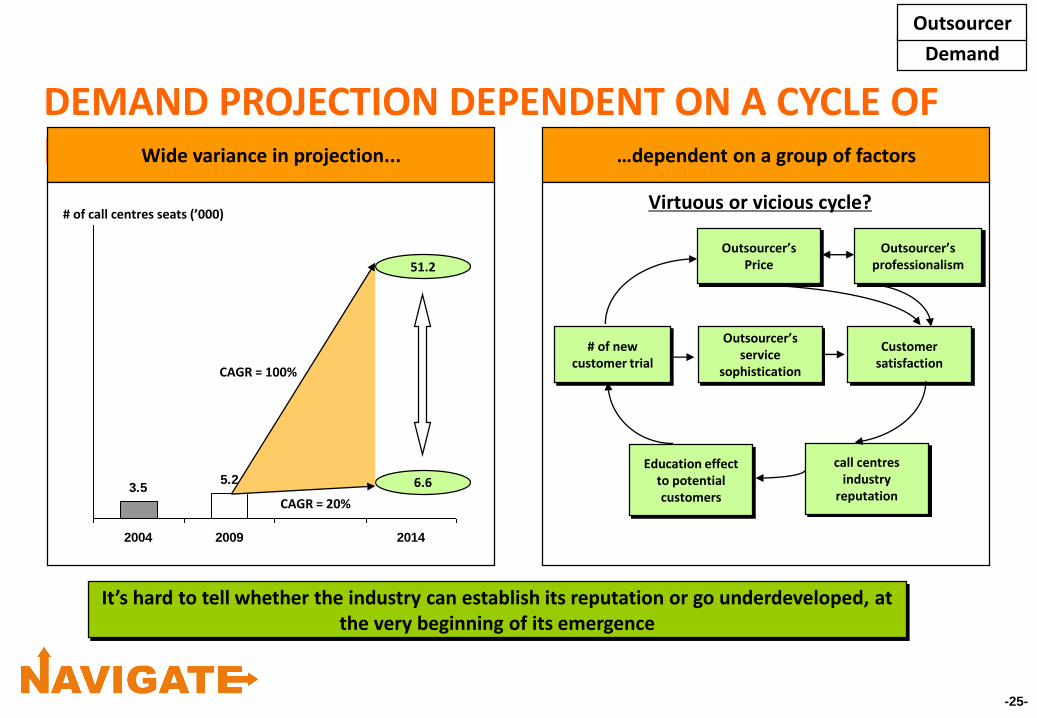

DEMAND PROJECTION DEPENDENT ON A CYCLE OF FACTORSWide variance in projection... …dependent on a group of factors

# of call centres seats (’000)

3.55.2

2004 2009 2014

Virtuous or vicious cycle?

Outsourcer’s Price

Outsourcer’s professionalism

Customer satisfaction

Outsourcer’s service

sophistication

# of new customer trial

Education effect to potential customers

call centres industry

reputation

It’s hard to tell whether the industry can establish its reputation or go underdeveloped, at the very beginning of its emergence

Demand

Outsourcer

51.2

6.6

CAGR = 100%

CAGR = 20%

CAGR = 20%

-26-

POSITIVE CUSTOMER EVOLUTION OBSERVED IN CHINA’S call centres BUSINESS

Positive projections for future

• Historical trends showed increasing penetration into high-end business

• China’s massive small-to-medium business constitutes good potential customer base

• Massive un-exploited geography: outside top 3 cities• Good outsourcer will emerge with increased business,

which will generate more business for the call centres industry

call centres service sophistication

TimeLow

High

Before Recent 2 years

We believe in the positive argument and project demand to grow at least 50% a year for the next 4 years

Paging service call centres for Hong Kong

“Secretary” service

Simple telemarketing

Order taking

After-sales service

Negative projections for future

• Customer’s negative thoughts about outsourcer’s quality haven’t changed

• Professionalism will continue to be a headache for China service industry, including call centres

• Low-end entry (paging companies) will ruin call centres industry’s pricing structure and make good outsourcer’s unprofitable

Demand

Outsourcer

-27-

BALANCE BETWEEN LONG-TERM CLIENTS AND PERIODIC ASSIGNMENTS IS CRITICAL

Customers

Outsourcer

Long-term clients

Long-term clients are most important to the profitability of an outsourcer

Job nature

Customer requirement

Compensation

• “Secretary” service

• Order-taking

• After-sales service

• Value-added information

• Trust between company and customer

• Training to agents

• Good understanding of clients’

business

• Smooth communication and feedback

of important information

• A monthly payment per agent seat

• Telemarketing

• Campaign/activity phone

reception

• Brand name in call centres

industry

• Trained agents and

effective management

• Information feedback

• Reasonable price

• Payment per call

Periodic assignments

-28-

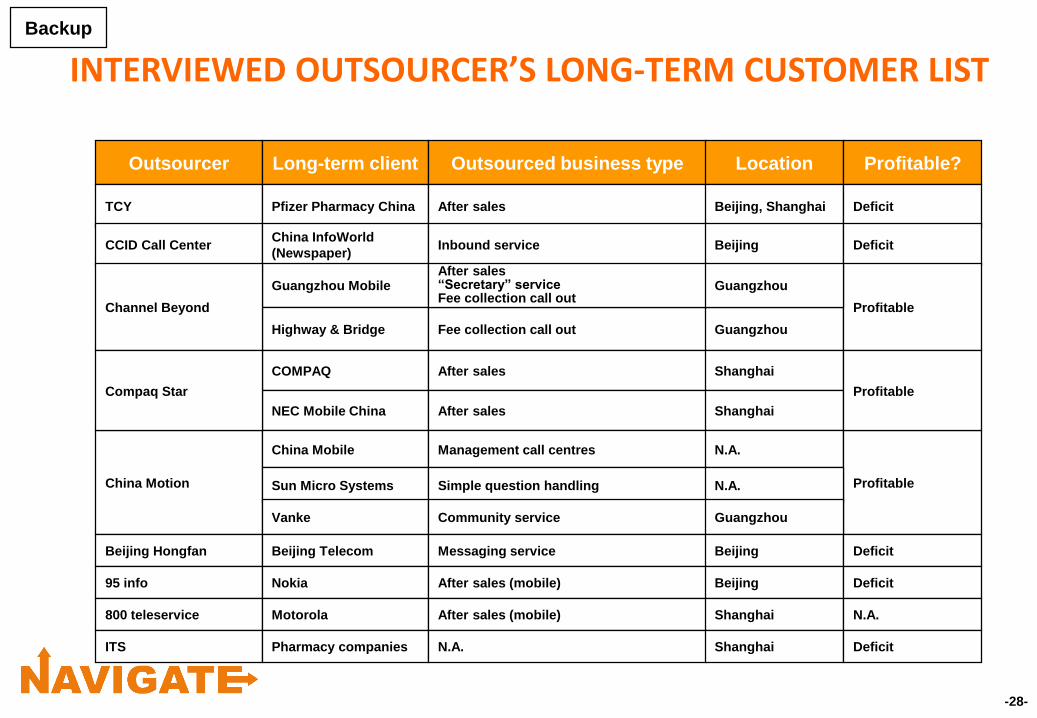

INTERVIEWED OUTSOURCER’S LONG-TERM CUSTOMER LIST

Outsourcer Long-term client Outsourced business type Location Profitable?

TCY Pfizer Pharmacy China After sales Beijing, Shanghai Deficit

CCID Call CenterChina InfoWorld

(Newspaper)Inbound service Beijing Deficit

Guangzhou Mobile

Highway & Bridge Fee collection call out Guangzhou

COMPAQ After sales Shanghai

NEC Mobile China After sales Shanghai

China Motion

China Mobile Management call centres N.A.

Profitable

Beijing Hongfan

Sun Micro Systems Simple question handling N.A.

Channel Beyond Profitable

Compaq Star Profitable

Backup

After sales“Secretary” serviceFee collection call out

Guangzhou

Vanke Community service Guangzhou

Beijing Telecom Messaging service Beijing Deficit

95 info Nokia After sales (mobile) Beijing Deficit

800 teleservice Motorola After sales (mobile) Shanghai N.A.

ITS Pharmacy companies N.A. Shanghai Deficit

-29-

call centres SALES AND SERVICE HELPS MULTINATIONALS TO FOCUS ON CORE CAPABILITIES

Advanced product design

Technology

Financial muscle

Operational management

Manufacturing

Distribution network

Customer relationships

Local marketing

Facilities (land, house…)

Regulatory knowhow

ServiceSourcing Manufacturing Sales

X

X

X

Multinational’s strengths

Local company’s strengths

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

Customers

OutsourcerBackup

-30-

HIGH-END OUTSOURCERS ARE STILL LOSING MONEY – CAPEX HIGH AND IRR BELOW ACCEPTED LEVELS

The key determinant: Utilization

Profitability

Economics

OutsourcerHi profits

Low

profits

Breakeven

Low

deficits

Hi deficits

Price/seat

(RMB/month)0 5000 10000 15000 20000 25000 30000 35000

China Motion

Shenghua

Cheng Bo

Compaq-Star

CCID

Hong Fan

TCY ITS

95Info

Source: Interviews; Navigate Consulting Analysis

-31-

AGENDA

Executive Summary

Call Center Business

• Market Overview

• CC Customer Segmentation

- In-house users

- Outsourcers

• Demand

• Customer

• Economics

• Competition

• Recommendations

- Success business model

- Partnering strategy

E-Commerce Market Overview

TCI Tianjin

• Current Situation Analysis

• Recommendations

-32-

PREVIOUSLY THE LOW-PRICE/STANDARD SERVICE MODEL PROVED SUCCESSFUL – Period 1998 - 2007Takeaway from Interviews

Not technically

feasible

Doomed failure

Possible

to be

successful

, too?

Several

successful

examples

observed

Customize/

High-end

Standard/

low-end

Low High

High-end outsourcers CAGR 2007-2012 14%

• Easier to persuade clients to accept a high price point

• Trust in big names

• Business not fully streamlined

- software and high-end customer support not available

• Most assignment periodic

Well-positioned, efficient low-end outsourcers WERE very profitable

• 70% or above business from long-term clients

• Both equipment and human resources are easy and cheap to source

Service

Level

Price

-33-

SUCCESSFUL HIGH-END MODEL HAS TAKEN 40% som Wiseway’s Belief

Long-term clients are most important for high-end CC outsourcer’s success

• Periodic assignment demand is inherently unstable, and demand fluctuation will worsen utility rate

- Current high-end CC outsourcers lack long-term clients

• Strong long-term client commitments give outsourcers credibility for other call center assignments

Prestigious long-term clients are beginning to commit to high-end outsourcers

• 95Info’s deal with Nokia in Beijing

• 800 Teleservices’s deal with Motorola in Shanghai

There are clear directions for high-end outsourcers to be profitable

• Establish long-term client base

- for a medium-sized call center, 1~2 long-term clients can turn it into profits

• Identify potential areas for CC call centres

-34-

HIGH-END OUTSOURCERS CAN DEVELOP BUSINESS ALONG TWO DIMENSIONS

Cu

sto

me

r p

en

etra

tio

n

Business penetration

Establish long-term client base

1. Build relationship through periodic assignments

2. Invite client’s equity investment

3. Provide “one-stop shopping”

4. Serve overseas market

5. Leverage existing relationship

Target various call centres opportunities along the value chain

Breakdown value chains to find out promising call centres opportunities

-35-

FIVE SUCCESSFUL STRATEGIES TO WIN LONG-TERM CLIENTS...

Building relationship through periodic

assignments

Outsourcers contact clients first for periodic

assignments, such as telemarketing or promotion

call reception, and sell long-term assignments when

trust and relationships are built

• Example: Guangzhou China Motion vs P&G

Provide “one-stop shopping”

Outsourcers also provide, or have alliances to

provide, other services that are compatible to

call center service. So customers can get all

they need from one company

• Example: Guangzhou Channel Beyond

Leverage existing relationship

Outsourcers develop domestic multinationals

clients leveraging overseas relationship

• Example: 800Teleservice v.s. Motorola

Serve overseas market

Outsourcers provide low-cost services to Hong

Kong, Taiwan or other overseas clients by

leveraging low-cost agents and language

ability in China

• Example: Guangzhou Shenghua

Invite client’s equity investment

Outsourcers ask an important client to make

equity investment, in order to lock in the

relationship and establish needed trust

• Example: Compaq-StarStrategies proved

successful

1

2 3

4 5

-36-

… EACH WITH ITS UNIQUE ADVANTAGES AND DISADVANTAGES

Cons

• Lowered entry barrier into potential clients

• Easier to build relationship and mutual trust

• Time consuming• Periodic assignments might not necessarily turn

to long-term commitment

• Lock-in relationships• Shared risks

• Controlled by clients• Limited opportunities for other clients

- restrained growth

• Increased customer satisfaction• Stronger advantages against all

competitors at “one-stop” area

• Strengths restrained in one particular area• Difficult to extend business to other areas

• Profitable business• Stable client relationship once

obtained

• Competition• Generally low-end services

- clients only pursue “low-cost”• Difficult to acquire overseas clients

• Monopolized client base• Familiar service standard• Leverageable software and

management

• Not a lot• Bad service in China might deteriorate

corporate’s relationship to the outsourcer

Building relationship through periodic assignments

Invite client’s equity investment

Provide “one-stop shopping”

Serve overseas market

Leverage existing relationship

1

2

3

4

5

Pros

-37-

call centres MOST PROMISING FOR TELEMARKETING AND VALUE-ADDED INFORMATION SERVICES

Potential Call Center Adoption Areas

After-sales service

Value-addedinformation

service

Trouble-shooting

Complaint handling

Concerns

Service

quality

Industry

knowledge

Information

processing

Confidentiality

Manu-

facturin

g

Sourcing

Ordering Suppliermgmt.

Sales

Tele-marketing

Inquiry handling

Order

taking

Most promising

Most promising

Not a concern

Significant concerns

-38-

call centres OPPORTUNITIES FOR SELECTED INDUSTRIES (I)Value Chain Breakdown for Sales and Services

Aft

ers

ale

s s

erv

ice

Tro

ub

le-

sh

oo

tin

gC

om

pla

int

han

dlin

gT

ele

-m

ark

eti

ng

Cu

sto

mer

inq

uir

y

han

dlin

g

Ord

er

takin

g

Valu

e-a

dd

ed

in

form

ati

on

serv

ice

Sale

s

IndustryTelecom

• Complaint reception

• Customer satisfaction survey

Mobile service

• Complaint reception

• Phone-line problem calling

• General trouble - shooting

• Mobile problem calling (lost, disconnected)

• Call dialing helpdesk

• Phone number inquiry (“114”)

• Phone bill information, etc.

• “Secretary” service

• Phone bill inquiry

• Fixed-line service application

• Other value-added service application

• Mobile service application

• Value-added service application

• Potential customer call-in reception • Potential customer call-in reception

• Long-distance service promotion

• General information of new products/services

• New service/products promotionLikely

Unlikely

-39-

call centres OPPORTUNITIES FOR SELECTED INDUSTRIES (II)Value Chain Breakdown for Sales and Services

Aft

ers

ale

s s

erv

ice

Tro

ub

le-

sh

oo

tin

gC

om

pla

int

han

dlin

gT

ele

-m

ark

eti

ng

Cu

sto

mer

inq

uir

y

han

dlin

g

Ord

er

takin

g

Valu

e-a

dd

ed

in

form

ati

on

serv

ice

Sale

s

IndustryBanking

• General complaint handling

Securities

• General complaint handling

• General trouble-shooting • General trouble-shooting

• Telephone banking

• Personal financialconsulting

• Investment analysis, suggestion,etc

• General marketinformation

• Deposit or other orders • Telephone transaction

• General question handling • General question handling

• New service promotion

• Corporate clientrelationship building

N.A.

Insurance

• General complaint handling

• General trouble-shooting

N.A.

• Telephone transaction

• General questionhandling

• Promotion of insurance policies

Likely

Unlikely

-40-

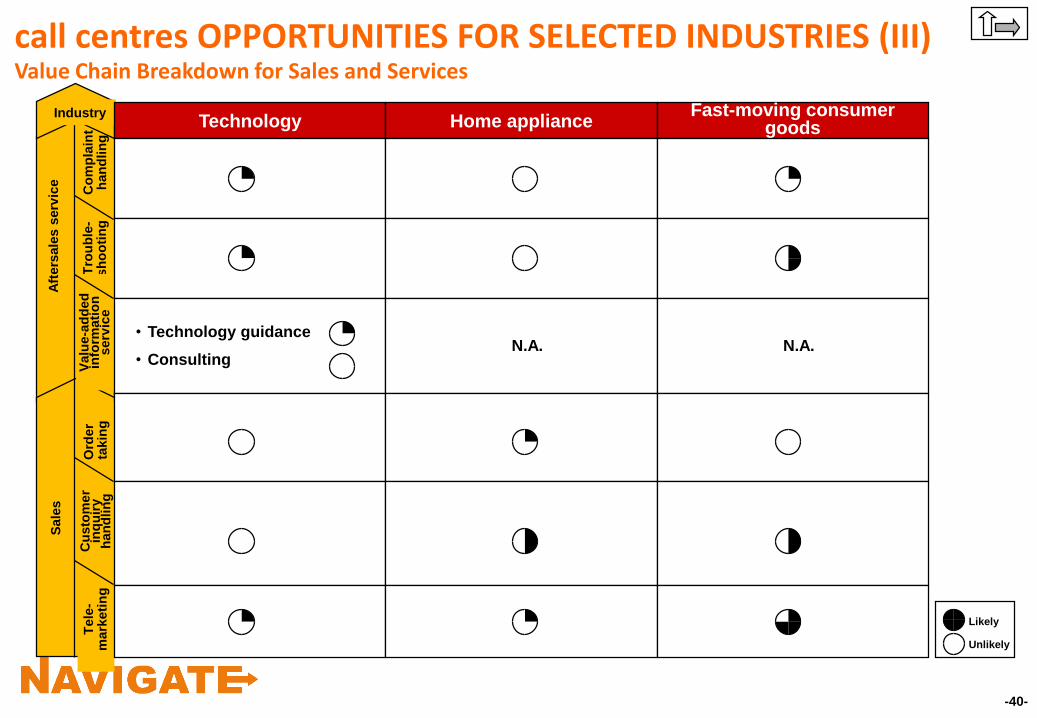

call centres OPPORTUNITIES FOR SELECTED INDUSTRIES (III)Value Chain Breakdown for Sales and Services

Aft

ers

ale

s s

erv

ice

Tro

ub

le-

sh

oo

tin

gC

om

pla

int

han

dlin

gT

ele

-m

ark

eti

ng

Cu

sto

mer

inq

uir

y

han

dlin

g

Ord

er

takin

g

Valu

e-a

dd

ed

in

form

ati

on

serv

ice

Sale

s

IndustryTechnology Home appliance

• Technology guidance

• ConsultingN.A.

Fast-moving consumer goods

N.A.

Likely

Unlikely

-41-

AGENDA

Executive Summary

Call Center Business

• Market Overview

• CC Customer Segmentation

- In-house users

- Outsourcers

• Demand

• Customer

• Economics

• Competition

• Recommendations

- Success business model

- Partnering strategy

E-Commerce Market Overview

TCI Tianjin

• Current Situation Analysis

• Recommendations

-42-

ONLY A PARTNERSHIP FITS INTO TCI’S SPECIFICATION

Self-construct a

call center

Partner with local

CC outsourcers

Provide CC call

centres training,

management and

consulting

• No China experience in call center

• No enough human resources to commit

• Little local client knowledge

• Time consuming

• Complement TCI’s local capabilities

• Satisfy time stringency concerns

• Commit little TCI resources

• Serve TCI’s potential clients well with

existing capacity

• Fit into TCI’s strengths well

• Demand less TCI’s commitment

However

• Need to establish local facilities and assign

knowledgeable people to China

• Profits will not be big

Maybe an

opportunity

-43-

TCI SHOULD ALLY WITH A LOCAL PARTNER TO ENTER INTO THE MARKET

Now is good to enter...

• Nevertheless, China CC call centres

segment is a fast growing market

• There are few high-profile CC call centres

companies in China

• Competition at high-end is not severe

• And…, TCI is in discussion with two

possible long-term clients

… But should ally with a local outsourcer

TCI lacks a lot of local capacities

• Local market understanding

• Local clients relationship

• Experienced agents

• Language

…

And time is tight

• A decision should be made very soon

A local partner with complementary capabilities is ideal for TCI’s fast

rollout in China

-44-

DIFFICULT TO FIND A PARTNER SATISFYING ALL CRITERIA

• Strong local market understanding

• Good local client relationship

Provide TCI with

most needed

capabilities

1 Be profitable Demand not too

much TCI’s

involvement

Allow TCI to

develop own brand

and share client

base

2 3 4

Partner’s

profile

• Mature, professional operations

• Experienced agents

• Sufficient long-term client base

• Strong, mature operations already

• Probably not strong self-brand and customer base

• Eagerly in need of TCI’s client, money, management

What TCI

might

face

• Command very high valuation for its shares

- TCI probably have to pay more under time pressure

• Stick to its right of control

- might agree in appearance, but suffocate in action TCI’s brand building efforts

• Persist on its own business practice

- TCI might feel difficult to configure to “Japanese standard”

• The outsourcer might be very bad

- no local client base

- losing money

- low morale

• TCI has to invest a lot

- money

- human resources

-45-

Partnership Strategy

Partner with strong,

money-making local

outsourcers

Partner with money-

losing, but high-end

equipped local

outsourcers

• Leverage partner’s

capabilities to

expand business

• Demand less TCI

investment

• Create synergy

more easily

• Leverage partner’s

advanced facilities

• Easy to control and

develop TCI’s own

brand

• Might be cheap

TWO POTENTIAL PARTNERSHIP STRATEGY SUGGESTEDReflecting Different Entry Focus

Advantages Disadvantage Entry Focus

• Expensive

• Hard to control

• Potential conflict

with TCI’s practice

• Profit sharing

• Fast rollout

• Synergy creation

• TCI might not benefit

too much from local

partner

• TCI has to invest a

lot

• High risk is entailed

• Control

• TCI brand and

practice

development

• A bargain deal

-46-

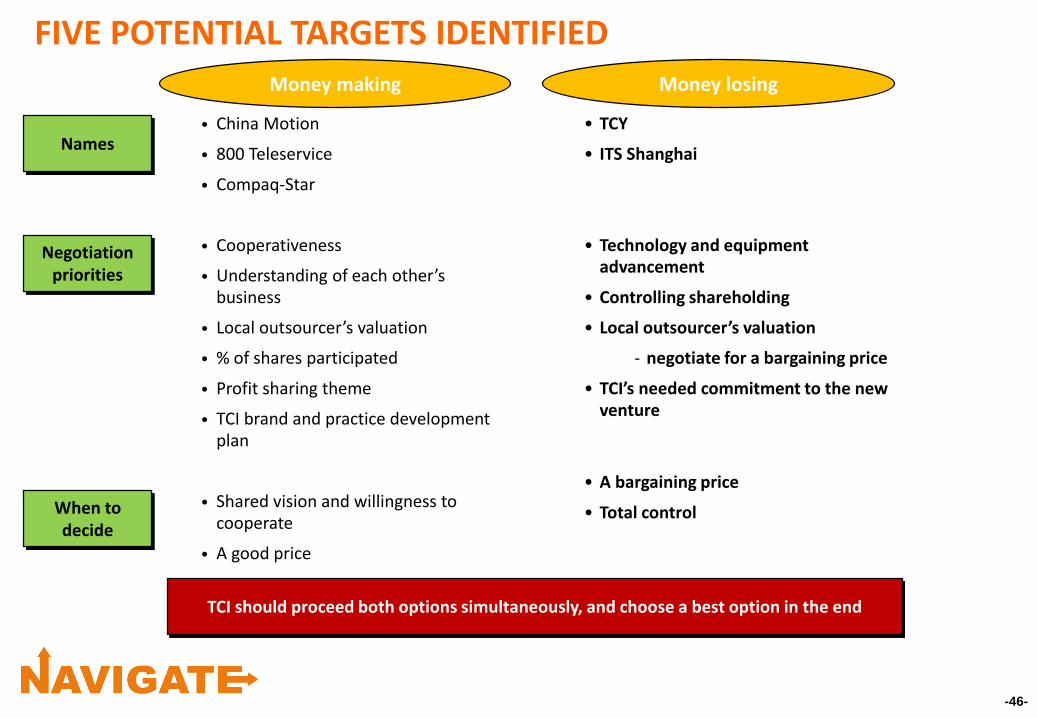

FIVE POTENTIAL TARGETS IDENTIFIED

• China Motion

• 800 Teleservice

• Compaq-Star

• Cooperativeness

• Understanding of each other’s business

• Local outsourcer’s valuation

• % of shares participated

• Profit sharing theme

• TCI brand and practice development plan

• Shared vision and willingness to cooperate

• A good price

Money making

• TCY

• ITS Shanghai

• Technology and equipment advancement

• Controlling shareholding

• Local outsourcer’s valuation

- negotiate for a bargaining price

• TCI’s needed commitment to the new venture

• A bargaining price

• Total control

Money losing

Names

Negotiation priorities

When to decide

TCI should proceed both options simultaneously, and choose a best option in the end

-47-

AGENDA

Executive Summary

Call Center Business

• Market Overview

• CC Customer Segmentation

- In-house users

- Outsourcers

• Demand

• Customer

• Economics

• Competition

• Recommendations

- Success business model

- Partnering strategy

E-Commerce Market Overview

TCI Tianjin

• Current Situation Analysis

• Recommendations

-48-

TCI-TJ EXPERIENCED TREMENDOUS DIFFICULTIES (I)

Most projects not profitable Overhead out of control

Rev.

Profit rate

-200%

-150%

-100%

-50%

0%

50%

100%

16%

-170%

35% 51%

61% 69% 98% 100%

2010

(’000 RMB)

508 997

2575

1758

1990

Gross profit

Salary

Management

fee

Depre.

Misc.

Source: TCI-TJ; Navigate Consulting Analysis

-49-

TCI-TJ EXPERIENCED TREMENDOUS DIFFICULTIES (II)

Programmer’s turnover is

worryingUtilization rate is low

Human resource

• From official statistics, on

average about 1/3 of

programmer’s working hours

were not staffed, real

situation can be worse

Real estate

• The whole second floor was

empty, while a depreciation

of RMB 2.4 million, 60% of

1999 revenue, is counted

each year as cost

Project schedule often out of

control

1996

1997

1998

1999

2000

Total recruited Left

Label

Programmers turnover

(7)

(1)

(20)

(5)

(4)

17

4

28

15

5

A 2011 project

People staffed

(4)

(1)

Time3 months

1 year

2 years

Planned

Actual

Source: TCI-TJ; Navigate Consulting Analysis

-50-

FIVE ROOT CAUSES IDENTIFIED FOR THESE PROBLEMS

Overhead out of

control

Over-invested

Project out of

control

Inadequate

programmer’s

training

Most projects not

profitable

Ineffective and not

disciplined sales

efforts

Low resources

utilization

Programmers not

motivated properly

Worrying

programmer’s

turnover

Compensation and

progression not

enough to retain

HR

-51-

TCI-TJ IS NOT COMPETITIVE IN DOMESTIC SOFTWARE MARKET

High fixed cost Ineffective domestic sales force

No sales department

Previous sales activities restrained in Tianjin

• And mainly through Japanese invested

companies

Targeting domestic customers means additional

investment on HR and spending

• With unforeseeable results

Equivalent domestic

company

TCI

Annual cost

(RMB ’000)

945

(1) With same actively-used office space, at a metropolitan location in Tianjin

Office cost example

83%

10%

7%

2926

Depreciation

Tax

Land

(1)

-52-

AGENDA

Executive Summary

Call Center Business

• Market Overview

• CC Customer Segmentation

- In-house users

- Outsourcers

• Demand

• Customer

• Economics

• Competition

• Recommendations

- Success business model

- Partnering strategy

E-Commerce Market Overview

TCI Tianjin

• Current Situation Analysis

• Recommendations

-53-

TCI-TJ CAN DEVELOP ALONG TWO PATHS

Restructure for better

performance

Questions are:

• What are advantages and potential risks entailed in different path?

• Which one to choose?

New business development

Introduce TCI Japan’s best-of-

breed technology to China through

TCI-TJ

Existing business penetration and

finance operation

Find strategic alliance for TCI-TJ

-54-

RESTRUCTURING FOR BETTER PERFORMANCE

• Transplant company’s vision to each employee’s mind

• Create better culture through informal interactive channels

• Mentor system

• Company activities

• “General Manager Day”

• Declare what should not be done

- Policies and rules

• Establish a scientific system to evaluate, incentivize, and promote staff

- Staff, evaluation, compensation and promotion

Customer strategy

• Focus on Japanese market and

Japanese companies around Tianjin

HR strategy

• Retain and promote the best people

in the company

• Create a programmer-centric

organization

Production strategy

• Adjust product and programming to

satisfy Japanese client

specifications

• Aspire to efficient production

• Improve HR utilization rate

Mission

• Turn into profitability in the next several years

• Develop TCI-TJ’s capability in software programming and service

• Retain best human resources

Belief system

Interactive

control

system

Boundary

system

Diagnostic

system

Control and

measurement system

-55-

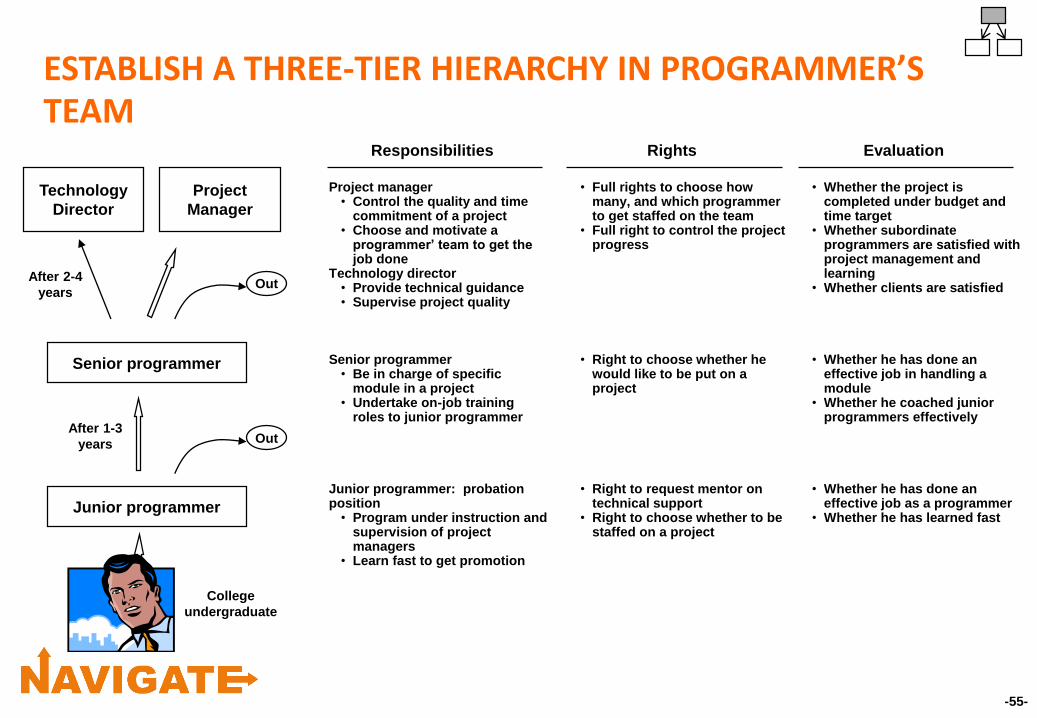

ESTABLISH A THREE-TIER HIERARCHY IN PROGRAMMER’S TEAM

Technology

Director

Project

Manager

Senior programmer

Junior programmer

After 2-4

years

After 1-3

years

College

undergraduate

Out

Out

Responsibilities

Project manager• Control the quality and time

commitment of a project• Choose and motivate a

programmer’ team to get the job done

Technology director• Provide technical guidance• Supervise project quality

Senior programmer• Be in charge of specific

module in a project• Undertake on-job training

roles to junior programmer

Junior programmer: probation position• Program under instruction and

supervision of project managers

• Learn fast to get promotion

Rights

• Full rights to choose how many, and which programmer to get staffed on the team

• Full right to control the project progress

• Right to choose whether he would like to be put on a project

• Right to request mentor on technical support

• Right to choose whether to be staffed on a project

Evaluation

• Whether the project is completed under budget and time target

• Whether subordinate programmers are satisfied with project management and learning

• Whether clients are satisfied

• Whether he has done an effective job in handling a module

• Whether he coached junior programmers effectively

• Whether he has done an effective job as a programmer

• Whether he has learned fast

-56-

HUGE BENEFITS OF BUILDING A THREE-TIER HIERARCHY

• Project managers are motivated to successfully compete the project as quickly as possible

- evaluated by customer satisfaction and time/budget consumed

• Project managers won’t abuse human resources

- better-off to select a small but capable programmer’s team

• Good programmers will be the king in the company: Strong incentive to be good

- treasured by every project manager: Enough good project to do

- compensated well and promoted fast

- incapable programmers will feel not well and have to leave the company

• Junior programmers will have enough training and opportunities to perform

• Senior management is disciplined to their sales efforts

- overly sold projects will be objected by project managers

Project management

HR development

Sales efforts

-57-

TWO TYPES OF STRATEGIC ALLIANCES PROPOSEDTCI-TJ

Advantages

• Use partner’s human

resources

• Benefit from partner’s

brand name

• Leverage partner’s client

base

• Introduce partner’s

management skills

• Retain huge potential

upside

- IPO process will boost

investment return

• Achieve potential

synergies between a

software company and an

E-commerce company

Disadvantages

• Very difficult to find such

a partner

- good companies

probably will find TCI-

TJ unattractive

• Lost control

• Potential risk of cultural

conflict

• Increasing risk of a

satisfactory IPO

• Partner’s experience of

working with a software

programmer

• Morale at TCI-TJ

Wiseway’s preference

Not

preferred

Preferred

Sell, or partner with

a local esteemed

software

programmer

Partner with a local

system integrator,

or E-commerce

company with IPO

potential

We will discuss partnership list in detail in the next part

-58-

Thank You?Questions

John Gregg,

Principal,

Navigate Consulting Pty Ltd

Ph: +61 402 493 278

Email: [email protected]

Web: www.navigatecoonsulting.com.au