2012 growth markets summit - goldman sachs · 2012 growth markets summit 7 10:40 am technology and...

TRANSCRIPT

2012 GROWTH MARKETS

SUMMIT

Growth Markets Insights: Shaping Global Investment Themes

2012 GROWTH MARKETS

SUMMIT

3This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. Please see additional disclosures.

Our annual Goldman Sachs Asset Management (GSAM) Growth Markets Summit, held on April 24th and 25th in New York City, featured a series of in-depth conversations on important themes and dynamics shaping the Growth Markets today. The event comprised 18 different sessions featuring over 40 leading CEOs, CIOs, policy makers, political scientists, industry experts, investment fund managers and senior Goldman Sachs professionals. We were honored to be joined by over 400 attendees representing over 275 organizations from 37 countries.

Speakers discussed a number of interesting questions throughout the Summit: Is Nigeria poised to be the next BRIC? Can the world fuel the rise of the Growth Markets from an energy perspective? What is the role of infrastructure development in growth and emerging economies? How will the power of social media effect change in China? What are the economic benefits of investing in women in the Growth Markets? These questions were debated during the Summit as we addressed many of the topics facing global investors today.

We look forward to continuing the dialogue around the Growth Markets and invite you to join us again at next year’s Summit. Please contact us at [email protected] anytime.

Timothy J. O’Neill and Eric S. LaneGlobal Co-Heads of the Investment Management Division, Goldman Sachs

4

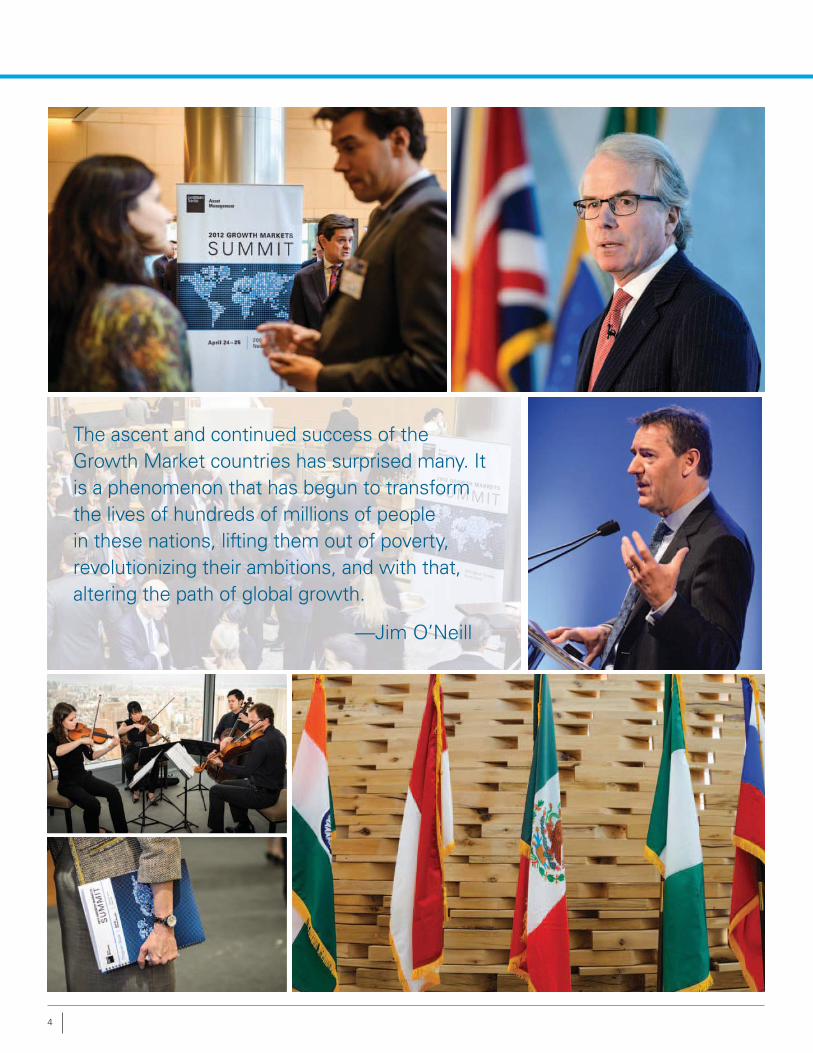

The ascent and continued success of the Growth Market countries has surprised many. It is a phenomenon that has begun to transform the lives of hundreds of millions of people in these nations, lifting them out of poverty, revolutionizing their ambitions, and with that, altering the path of global growth.

—Jim O’Neill

2012 GROWTH MARKETS

SUMMIT

5

6

April 24, 2012

5:30 pmCocktail ReceptionPerformances by musicians from The Juilliard School

6:30 pm Dinner and Welcome Remarks Timothy J. O’Neill, Global Co-Head of the Investment Management Division, Goldman Sachs

6:45 pmDiscussion with Sir Martin SorrellHosted by: Jim O’Neill, Chairman, Goldman Sachs Asset Management Sir Martin Sorrell, Group Chief Executive, WPP

7:45 pm Discussion with Alan Greenspan and Henrique de Campos MeirellesHosted by: Jim O’Neill, Chairman, Goldman Sachs Asset ManagementAlan Greenspan, Chairman, Federal Reserve System (1987-2006)Henrique de Campos Meirelles, Former Governor, Central Bank of Brazil

Agenda

April 25, 2012

7:45 amRegistration and Breakfast

8:00 am Living in a Growth Markets World Part IIJim O’Neill, Chairman, Goldman Sachs Asset Management

8:40 amThe Role of Healthcare and Education in Delivering Sustainable GrowthModerated by: Gabriella Antici, Chief Investment Officer and Head of Goldman Sachs Asset Management Brazil, Goldman SachsAmit Bhatia, Founder and CEO, Aspire Human Capital ManagementRicardo Leonel Scavazza, Chief Executive Officer, Anhanguera Educacional Participações S.A.Dinakar Singh, Founder and Chief Executive Officer, TPG-Axon CapitalShivinder M. Singh, Executive Vice Chairman,Fortis Healthcare Limited

9:10 amThe Paradox of Investor Short-Termism Knut N. Kjaer, Former Founding Chief Executive Officer of the Norwegian Sovereign Wealth Fund; Chairman, FSN Capital Partners and Trient Asset Management

9:25 amInfrastructure: Building the Growth Market DreamModerated by: Colin Coleman, Head of the Investment Banking Division for Sub-Saharan Africa, Goldman Sachs Dr. Daniel Alexander Jordaan, SAFA Vice President; Former Chief Executive Officer: 2010 FIFA World Cup Organising CommitteePrashant Khemka, Chief Investment Officer and Co-Chief Executive Officer of Goldman Sachs Asset Management (India) Private Limited, Goldman SachsEduarda La Rocque, Secretary of Finance, Municipal Government of Rio de JaneiroBabatunde Soyoye, Managing Partner, Helios Investment Partners LLP

9:55 amInternet: Unique Business ModelModerated by: J. Michael Evans, Vice Chairman, Chairman of Asia, Global Head of Growth Markets, Goldman SachsYuri Milner, Founder, DST Global

10:25 amBreak

2012 GROWTH MARKETS

SUMMIT

7

10:40 amTechnology and Venture Capital: What Are the Growth Market Opportunities?Moderated by: Ravi Viswanathan, General Partner, New Enterprise Associates Joe Lonsdale, Co-Founder, Palantir, Addepar, and Formation | 8Josh Wolfe, Co-Founder and Managing Partner, Lux Capital

11:00 amIs Nigeria the Next BRIC?Moderated by: Colin Coleman, Head of the Investment Banking Division for Sub-Saharan Africa, Goldman SachsTito Mboweni, Former Governor, South African Reserve Bank; International Advisor, Goldman SachsMansur Muhtar, Alternate Executive Director for Angola, Nigeria and South Africa, World BankBabatunde Soyoye, Managing Partner, Helios Investment Partners LLP

11:30 amSports and GlobalizationModerated by: Eric S. Lane, Global Co-Head of the Investment Management Division, Goldman SachsDavid J. Stern, Commissioner, National Basketball Association

11:55 amBreak for Working Lunch Session

12:15 pmChina: The Next Generation Mdm Yang Lan, Chairperson, Sun Media Group and Sun Culture Foundation

12:45 pmEnergy: Can the World Fuel the Rise of the Growth Markets?Moderated by: Arjun Murti, Co-Director of Americas Equity Research and Senior Energy Analyst,Goldman SachsWilliam Macaulay, Chairman and Chief Executive Officer, First Reserve CorporationAubrey K. McClendon, Chairman of the Board and Chief Executive Officer, Chesapeake Energy Corporation

1:15 pmThe Rise of the BRIC ConsumerModerated by: Kathryn A. Koch, Senior Portfolio Strategist and Chief of Staff, Office of the Chairman, Goldman Sachs Asset Management Govindraj Ethiraj, Former Founder-Editor in Chief, Bloomberg UTVIan Mukherjee, Chief Investment Officer, Amiya Capital LLP Harvey Sawikin, Principal, Firebird Management L.L.C.Juan Pablo Zucchini, Managing Director, Advent International

1:45 pmConnectivity Is Productivity: The Role of Innovation and Entrepreneurship in Low Income CountriesIqbal Z. Quadir, Founder and Director, Legatum Center at MIT; Professor of the Practice, MIT

2:00 pmMacroeconomic and Investment InsightsModerated by: Hugh Lawson, Co-Head of Alternative Capital Markets, Goldman SachsSam Finkelstein, Head of Macro Strategies, Global Fixed Income, Goldman Sachs Asset Management Tito Mboweni, Former Governor, South African Reserve Bank; International Advisor, Goldman SachsCecilia Reyes, Chief Investment Officer, Member of the Group Executive Committee, Zurich Insurance Group

2:30 pmBreak

3:00 pmInvesting in Women Is Smart EconomicsModerated by: Dina Habib Powell, President of the Goldman Sachs Foundation and Global Head of Corporate Engagement, Goldman Sachs Isobel Coleman, Senior Fellow and Director, Civil Society, Markets, and Democracy Initiative, Council on Foreign RelationsDivya Keshav, 10,000 Women Scholar; Owner, Krishna PrinternationalLuis Alberto Moreno, President, Inter-American Development Bank

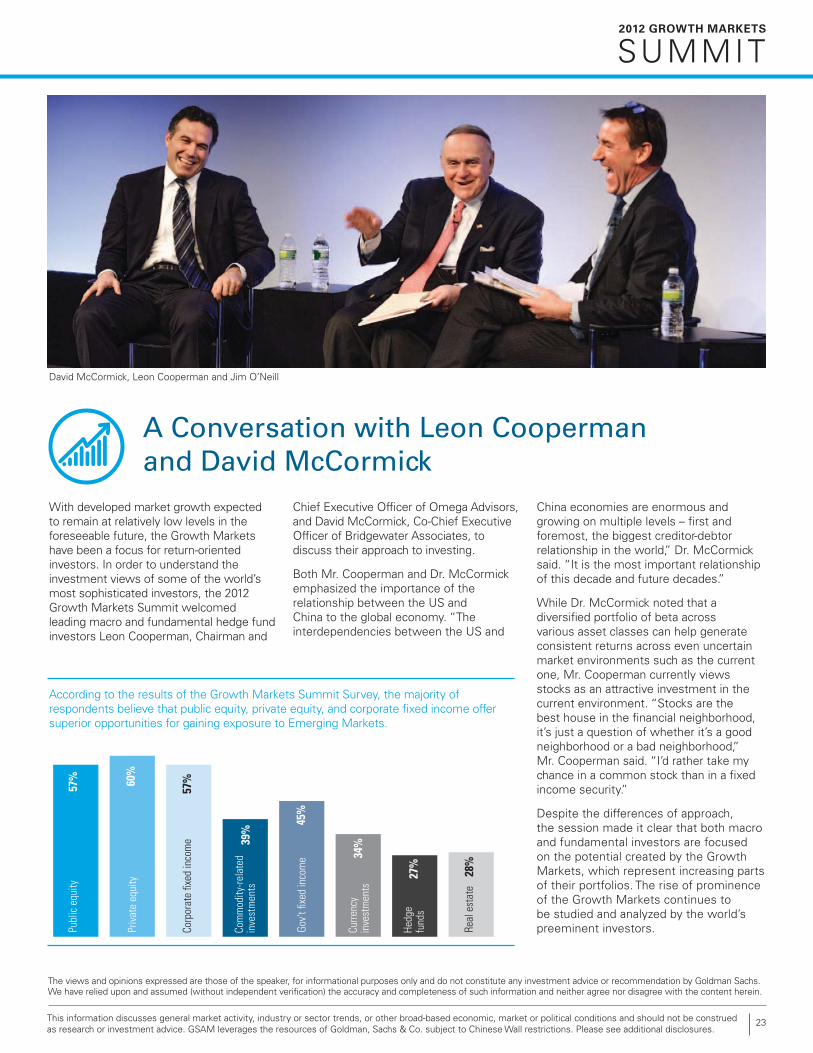

3:30 pmA Conversation with Leon Cooperman and David McCormickModerated by: Jim O’Neill, Chairman, Goldman Sachs Asset ManagementLeon G. Cooperman, Chairman and Chief Executive Officer, Omega Advisors, Inc.David H. McCormick, Co-Chief Executive Officer, Bridgewater Associates

4:10 pmEconomy and Security in the 21st CenturyModerated by: Sharmin Mossavar-Rahmani, Chief Investment Officer of the Private Wealth Management Group, Goldman Sachs Madeleine K. Albright, U.S. Secretary of State (1997-2001) Ian Bremmer, President, Eurasia Group

5:00 pmClosing Remarks and Cocktail Reception

8 This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. GSAM leverages the resources of Goldman, Sachs & Co. subject to Chinese Wall restrictions. Please see additional disclosures.

1. The N-11 is a term coined by Jim O’Neill in 2005 to describe the ‘next 11’ developing countries after the BRICs with the potential to rival the G-7 as a source of global demand and sustained growth and includes: Bangladesh, Egypt, Indonesia, Iran, South Korea, Mexico, Nigeria, Pakistan, the Philippines, Turkey and Vietnam.The views and opinions expressed are those of the speaker, for informational purposes only and do not constitute any investment advice or recommendation by Goldman Sachs. We have relied upon and assumed (without independent verification) the accuracy and completeness of such information and neither agree nor disagree with the content herein.

Perspectives on the Global Economy

Invite Sir Martin Sorrell, the CEO of the WPP Group, Alan Greenspan, the former Chairman of the Federal Reserve System and Henrique de Campos Meirelles, former governor of the Central Bank of Brazil to dinner and it is not surprising that the conversation bounces from China’s growing emphasis on domestic consumption to Brazil’s growth prospects to views on the Eurozone crisis. Jim O’Neill, Chairman of Goldman Sachs Asset Management, hosted the dinner conversation during which the speakers shared their views and personal experiences in the Growth Markets and the global economy.

Companies are investing in their brands in all markets, observed Sir Martin. In the slower-growing developed markets, it is to gain market share, while in the faster-growing markets such as the BRICs and N-111, it is accompanied by expanding capacity. Furthermore, he believes many local Growth Market brands may become global competitors, stating, “If anybody in this room is complacent or arrogant enough to believe that 1.3 bn Chinese or 1.2 bn Indians or 200 mn Brazilians or even 145 mn ageing Russians will not be able to produce competitive companies, think again.”

Sir Martin also shared a number of colorful anecdotes from his experience doing business all over the world. On China, he noted, “Look at the twelfth Five Year Plan. What does it emphasize? It emphasizes consumption. Good for us. It emphasizes healthcare, social security safety net, because they want to switch people from

savings to consumption.” Regarding Africa he noted, “I’m very bullish because – don’t tell anybody – Africa is growing – certainly none of our competition is aware of that fact, at least yet.” Furthermore, Sir Martin said, “You don’t get markets like Myanmar falling out of the sky opening up, I mean, there is a scrum, you can’t get a hotel room, you can’t get an airplane booking.”

The two former central bankers addressed several topics particularly relevant to the Growth Markets, including the role of China in the world economy and Brazil’s prospects. Dr. Greenspan has long suggested that a floating RMB would rebalance the system and make China more competitive and believes this is finally happening. China is clearly important to the Brazilian and world economies, Mr. Meirelles noted, though “there are also tradeoffs. The moment that China demands commodities and prices of commodities go up, that also leads to appreciation of the currency and that adds pressure on the manufacturing sector.” Fortunately, Brazil is more diversified that the typical export-driven economy, according to Mr. Meirelles. In addition, he expects Brazil to continue to grow above the international average because of advantageous demographics.

Finally, on the global economy, Dr. Greenspan opined, “The state of the world regrettably is being run by Europe,” and further suggested that “the most important thing President Obama should be worrying about (economically) is the potential of a rising Italian bond yield.”

Jim O’Neill with Alan Greenspan and Henrique de Campos Meirelles

Sir Martin Sorrell

63%Yes, but in morethan 5 yrs

29% Unlikely

5% Yes, within the next 5 yrs

2% Will never happen

The majority of Growth Markets Summit Survey respondents indicated that they thought the US dollar could be replaced as the dominant international reserve currency in more than 5 years.

2012 GROWTH MARKETS

SUMMIT

9This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. GSAM leverages the resources of Goldman, Sachs & Co. subject to Chinese Wall restrictions. Please see additional disclosures.

The economic and market forecasts presented herein for informational purposes as of the date of this presentation. There can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this presentationThe views and opinions expressed are those of the speaker, for informational purposes only and do not constitute any investment advice or recommendation by Goldman Sachs. We have relied upon and assumed (without independent verification) the accuracy and completeness of such information and neither agree nor disagree with the content herein.

Living in a Growth Markets World Part II

Jim O’Neill

Do you believe that the world can grow faster over the next 10 years than it has over the last 10? 59% of the attendees at the 2012 Growth Markets Summit said they did; GSAM’s Chairman Jim O’Neill dedicated his opening remarks to increasing that percentage.

“The world is changing at a speed that virtually none of us truly recognize,” stated Mr. O’Neill. The eight defined Growth Market countries (Brazil, Russia, India, China, South Korea, Mexico, Turkey and Indonesia) already contributed more to the world economy in the past decade than the G-7. In the coming decade, Mr. O’Neill expects them to contribute about $15 tn to global GDP, more than double what the US and Europe combined are expected to contribute. Therefore, while the world is worrying about the fate of Greece and Italy, “China creates the economic equivalent, hopefully a good one, of Greece every 11 and a half weeks…The four BRIC countries collectively, quite remarkably, created nearly the equivalent of another Italy in one year.”

“Consumer spending is increasingly being dominated by consumers in the so-called emerging world,” continued Mr. O’Neill, and may be the defining theme of the

decade. “By 2020, the dollar value of consumption in the four BRIC countries will be pretty much close to that of the US.”

Mr. O’Neill added that the Growth Markets offer more than just growth. Most have healthy and stable balance sheets at a time when many developed markets do not. To illustrate the point, he asked, which countries today would meet the European Monetary Union’s original Maastricht Criteria of inflation within 2% of the lowest country, a deficit of 3% of GDP or less and a debt-to-GDP ratio of 60% or less, or which are heading in that direction? Most of the EMU does not make the cut but six Growth Market countries do.

“This is really difficult for us all to understand because it’s like the world being turned upside-down from what we are familiar with,” concluded Mr. O’Neill. We are living in a Growth Markets world.

By 2020, the dollar value of consumption in the four BRIC countries will be pretty much close to that of the US. —Jim O’Neill

50%I agree

2% I strongly

disagree9% I strongly agree

40% I disagree

According to the Growth Markets Summit Survey, 59% of respondents believe the world can grow faster over the next 10 years than it has over the last 10 years.

10 This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. GSAM leverages the resources of Goldman, Sachs & Co. subject to Chinese Wall restrictions. Please see additional disclosures.

The views and opinions expressed are those of the speaker, for informational purposes only and do not constitute any investment advice or recommendation by Goldman Sachs. We have relied upon and assumed (without independent verification) the accuracy and completeness of such information and neither agree nor disagree with the content herein.

The rise of the Growth Markets has not occurred in isolation, but is partially the result of the growing economic interconnectedness between countries. The 2012 Growth Markets Summit welcomed former US Secretary of State Madeleine Albright, Ian Bremmer, President of the Eurasia Group and Sharmin Mossavar-Rahmani, Chief Investment Officer of the Goldman Sachs Private Wealth Management Group, to lend their unique perspectives on the world today.

Geopolitical issues took center stage, and the possibility and implications of a military engagement with Iran before the end of the year was a hotly debated topic. Dr. Albright put the chances of conflict at less than 25%, but cautioned that the “fallout effect” of any military engagement goes beyond oil export. “Some of the steps that the international community is taking are working,” she stated, though conceded that she is concerned about an accident. “There are a lot of small Iranian boats in the Gulf and you can never control every aspect of them. Accidents have a way of escalating.”

In a discussion on the path for China, Ms. Mossavar-Rahmani asked the panelists about the prospects for geopolitical tensions in the region and how they would affect investment in China. They noted a number of issues, discussing how territorial disputes with neighboring countries, such as disagreements over natural resources, shipping lanes and fishing rights in the South China Sea, as well as political infighting and the recent removal of Bo Xilai may

contribute to volatility in the country and drive uncertainty about China’s investment prospects despite its growth potential. Dr. Albright discussed the importance of disputes over territory and natural resources, arguing, “We ought to be looking at the Law of the Sea Treaty because in fact, we need some kind of governance procedures” to address competing claims over natural resources and trade routes in the South China Sea and the Arctic. “The Chinese are resource hungry. That’s what is dominating their foreign policy. I think it has the possibility of being volatile, which means there needs to be some rules of the road.” Dr. Bremmer discussed the importance of these issues in assessing the investment prospects of the country, saying, “I focus on an environment that is much more volatile than it used to be. You want to focus on BRICs because it’s growth, great. But the reality is that you can’t do growth in this environment. You have to do growth and resilience together. You have to bring the politics into your assessment here.”

Additionally, Ms. Mossavar-Rahmani led a discussion on Russia. Noting that the country’s contribution to global military spending had fallen significantly over the last two decades from 36% in 1985 to just 5% as of 2008, she initiated the conversation by asking both the audience and the panelists whether Russia matters to the global geopolitical landscape today. While the majority of the audience indicated yes, Dr. Albright and Dr. Bremmer discussed additional considerations indicating Russia’s declining relevance on the geopolitical stage.

Economy and Security in the 21st Century

Ian Bremmer, Madeleine Albright and Sharmin Mossavar-Rahmani

Dr. Bremmer noted that while the Russian president remains a powerful world leader in that he has few constraints on his individual power, Russia has been less involved in issues outside of the country, such as the six-party talks on North Korea. Nevertheless, both panelists highlighted Russia’s dangerous “spoiler role,” as the country still has the potential to influence many global issues, particularly in the Middle East.

In the final part of the discussion, in which Ms. Mossavar-Rahmani asked the panelists their views of US pre-eminence over the next 20 to 30 years, the conversation reflected increasing influence of the Growth Markets on the world. Dr. Albright discussed that while the US remains powerful, the increasing breadth of challenges facing the country including terrorism, nuclear proliferation and energy and environmentalism mean that the country cannot solve these challenges alone. She said, “I do believe the US is indispensable but there is nothing in the definition of the indispensable that says alone. It means the United States needs to be engaged.” Dr. Bremmer reflected that, “For the last 70 years we’ve been in an environment where if you got something done the US was driving it. We’ve had US led globalization. We’ve had US led global institutions. I think that’s over. I think we will now either have US led institutions that aren’t global. We will have global institutions that aren’t US led.” Based on the views and ideas presented by the speakers throughout the day, Dr. Bremmer was not the only one who shared this idea.

2012 GROWTH MARKETS

SUMMIT

11This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. GSAM leverages the resources of Goldman, Sachs & Co. subject to Chinese Wall restrictions. Please see additional disclosures.

The views and opinions expressed are those of the speaker, for informational purposes only and do not constitute any investment advice or recommendation by Goldman Sachs. We have relied upon and assumed (without independent verification) the accuracy and completeness of such information and neither agree nor disagree with the content herein.

Social MediaGrowth Market countries are rapidly harnessing the connectivity and global reach of social media. From Twitter’s role as a catalyst for the Arab Spring to Sino Weibo’s role as an outlet for the unfiltered views of Chinese citizens, social media users in Growth Markets are taking advantage of social media’s power to effect change. Global use of social media is ushering in an era where news and events can be shared with anyone, anytime and anywhere.

Facts

• 1.2 bn users worldwide now log onto social networks and 82% of the world’s internet users have social network accounts.1

• During the week before Egyptian president Mubarak’s resignation in 2011, the rate of tweets from Egypt and around the world about political change in Egypt grew from 2,300 a day to 230,000 a day.2

• $5.2 bn was spent on social media marketing globally in 2011, a number projected to reach $7.7 bn in 2012 and $10.2 bn in 2013.3

• Iran’s 33.2 mn internet users are more than all other Middle Eastern countries combined.4

Global Top 5 Social Media Sites by Number of Unique Visitors

ly obalal r’s role aass aa

Source: Google’s “Double Click Ad Planner” as of July 2011

1. Source: comScore, December 2011; 2. Source: Science Daily, September 2011; 3. Source: eMarketer, February 2012; 4. Source: Internet World Stats, March 2011

China: The Next Generation

Yang Lan

As the global use of social media increases, Growth Market countries are taking advantage of social media’s power to serve as an outlet for unfiltered views. Yang Lan, chairperson of Sun Media Group and Sun Culture Foundation, discussed China’s next generation and how they are transforming the future of the country, with a particular focus on how social media can serve as a powerful tool to effect change.

According to Ms. Yang, “Because the traditional media in China is still heavily controlled by the government, social media offers an opening to let the steam out a little bit.” Accusations of corruption or injustice can spread quickly through social media, which forces government accountability and a more inclusive process when developing public policy.

Ms. Yang also discussed the demographic trends that are emerging in this generation. Last year, the urban population in China surpassed the rural population for the first time. Of the country’s 200 mn migrant workers, 60% are young people, who are increasingly becoming an important consumer. Ms. Yang noted, “Migrant workers are becoming the vast and fastest growing market for manufactured goods. From clothes to detergent, from soda to shampoo, no corporation of fast consumption products can afford to lose this market.” Additionally, as many were born under China’s one-child policy, this generation now has 30 mn more young men than young women due to selective abortions by families who favored boys over girls, which his has led to empowerment of women.

Ms. Yang concluded her remarks with an optimistic outlook for China’s next generation: with high college graduation rates and illiteracy rates below 1%, the country’s youth are well-educated and poised to transform the country in the decades to come by taking advantage of social media’s power to demand government accountability and social justice.

12 This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. GSAM leverages the resources of Goldman, Sachs & Co. subject to Chinese Wall restrictions. Please see additional disclosures.

The views and opinions expressed are those of the speaker, for informational purposes only and do not constitute any investment advice or recommendation by Goldman Sachs. We have relied upon and assumed (without independent verification) the accuracy and completeness of such information and neither agree nor disagree with the content herein.

Technology and Venture Capital: What Are the Growth Market Opportunities?

Few would argue that technology has not been instrumental in the growth of business and opportunities in the Growth Markets. Unburdened by legacy infrastructure and systems, many new businesses have been able to leverage the latest technology to quickly access markets and information around the world. Joe Lonsdale, Co-Founder of Palantir, Addepar and Formation | 8 and Josh Wolfe, Co-Founder and Managing Partner of Lux Capital, a biotech and life science private equity firm, discussed the role of technology and venture capital in Growth Markets with Ravi Viswanathan, General Partner of the venture firm New Enterprise Associates.

Illustrating the increasing importance of the Growth Market consumer, South Korea leads the world in mobile phone penetration at 91%. Mr. Lonsdale observed that in his venture capital investments, the companies are often looking to the BRICs and other developing economies to fuel growth.

As Dr. Viswanathan inquired about how the panelists think about investing in international markets, Mr. Lonsdale noted that “having connections and partnerships in Growth Markets is a great way to help steward innovation and help de-risk your bets in innovation.”

Beyond consumers, Growth Markets are producing technology’s new great minds. According to Mr. Wolfe, “The biggest asset for most of our companies when we do these seed investments and spinning things out in physics and engineering and high tech, is the scientist. And 90% of our CTOs, VPs of engineering, CEOs are non-native US born scientists and engineers. And that’s a phenomenon that is well-known and talked about, but it’s something that is just frankly remarkable.”

As capital continues to follow the latest technological innovations, it seems that Growth Markets have the potential to be some of the largest beneficiaries and drivers of advances in technology.

Josh Wolfe, Joe Lonsdale and Ravi Viswanathan

82%Helpful

1% Nothelpful 15%

Marginally helpful

The majority of Growth Markets Summit Survey respondents believe a local presence is helpful in the pursuit of alpha generation in Emerging Market equities.

2012 GROWTH MARKETS

SUMMIT

13This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. GSAM leverages the resources of Goldman, Sachs & Co. subject to Chinese Wall restrictions. Please see additional disclosures.

The economic and market forecasts presented herein for informational purposes as of the date of this presentation. There can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this presentation.The views and opinions expressed are those of the speaker, for informational purposes only and do not constitute any investment advice or recommendation by Goldman Sachs. We have relied upon and assumed (without independent verification) the accuracy and completeness of such information and neither agree nor disagree with the content herein.

Internet: Unique Business ModelYuri Milner, founder of DST Global and the largest internet investor in the world, discussed how the internet differed from other investment sectors. In a conversation with J. Michael Evans, Vice Chairman of Goldman Sachs, Chairman of Goldman Sachs Asia and the first Global Head of Growth Markets at Goldman Sachs, Mr. Milner described the internet as an interrelated eco-system with unprecedented increases in efficiency and rates of growth. In the past 10 years, adoption has increased exponentially while the costs of storage and computation have decreased by a similar magnitude.

Mr. Milner highlighted five unique characteristics of the internet responsible for this dramatic trajectory. The first three, the cloud, the viral effect and the ability to offer services largely for free, enable companies to build a low-cost model. Mr. Milner then described the unique phenomenon of platform sites, where companies often pay 30% of revenue to use a platform site to generate business. Finally, Mr. Milner discussed the peer-to-peer capability that allows companies to build business without a central server at minimal cost. As a result, he estimates the costs to start an internet business have decreased 100 times in the past 10 years.

Looking ahead, Mr. Evans inquired about what challenges the internet may face over the coming years. Both Mr. Evans and Mr. Milner agreed that regulation presents a challenge, as governments become increasingly concerned about issues such as privacy rights. Additionally, the fast pace of internet adoption in developing countries has the potential to bring instability as people get access to information that they had not had before. Mr. Evans and Mr. Milner believe that the Growth Markets offer two important drivers of growth for internet companies: population growth and faster growth of online retail, which is gaining share from fragmented traditional retailers.

“By 2020, there will be at least 50 internet companies with at least a $10 bn market cap. Half will be in Emerging Markets,” Mr. Milner said. “At least 10 internet companies globally will be among the top 100 public companies.” With these trends in play, emerging economies are expected to be a major part of the internet’s continued growth.

J. Michael Evans and Yuri Milner

Technology & Venture CapitalContinuous technological evolution is positively impacting and transforming societies, individuals and businesses. The smartphone has started to replace the basic cell and home phone and sales of tablet devices are starting to surpass traditional computer sales. As increasing amounts of venture and corporate capital is directed towards technological innovation, Growth Markets will be some of the largest beneficiaries of advances in mobile technology.

Facts

• Over 2 bn people now use broadband internet, an almost 40-fold increase relative to a decade ago.1

• South Korea and Japan lead in mobile broadband penetration, with 91% and 88%, respectively.2

• Brazilians are still only using their mobile devices to talk and text. Online traffic generated from mobile phones and tablets represented only 1.5% of total web traffic in 2011.3

• In 2011 global smartphone shipments reached 452 mn units, surpassing PCs and desktops for the first time.4

• Apple’s market cap, $590 bn, is now larger than the rest of the US retail sector and twice the size of Microsoft’s.5

VC Spending by Sector

isng societtieiess

Source: PricewaterhouseCoopers & National Venture Capital Association

1. Source: WSJ Online Article referenced below AND ITU (stats page for global map) 2. Source: Mobithinking.com. 3. Source: Forbes.com 4. Source: IDC, Gartner 5. As of March 2012

14 This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. GSAM leverages the resources of Goldman, Sachs & Co. subject to Chinese Wall restrictions. Please see additional disclosures.

The views and opinions expressed are those of the speaker, for informational purposes only and do not constitute any investment advice or recommendation by Goldman Sachs. We have relied upon and assumed (without independent verification) the accuracy and completeness of such information and neither agree nor disagree with the content herein.

Without significant infrastructure build out, some Growth Markets risk never realizing their full potential. Daniel Alexander Jordaan, SAFA Vice President, Eduarda La Rocque, Secretary of Finance of the Municipal Government of Rio De Janeiro, Babatunde Soyoye, Managing Partner of Helios Investment Partners LLP and Prashant Khemka, CIO and Co-CEO of GSAM India discussed the current status of infrastructure and unique challenges facing Africa, India and Brazil during a panel moderated by Colin Coleman, Goldman Sachs’ Head of Investment Banking for Sub-Saharan Africa.

There is roughly a $50 bn per year shortfall in infrastructure investment in Africa. Dr. Jordaan stated boldly, “Africa must understand that it is about investment and infrastructure. If you want to be a player in the game, then this must be a central issue.”

Major sporting events, such as the World Cup and the Olympics, are huge drivers of important infrastructure spending, particularly in less advanced economies. Dr. Jordaan confirmed that the recent South African World Cup benefited the whole African continent while Ms. La Rocque described Brazil’s strategy ahead of hosting both events in the next several years: “The two more important words would be sustainability and legacy, which includes sanitation, the urbanization of a very important area, the seaport area, and transportation…I hope after the Olympic Games we would be one of the biggest tourism destinations in the world.” However, in the case of India, where the current state of infrastructure lags its BRIC peers, Mr. Khemka believes that the more efficient use of capital is for basic infrastructure like roads, electricity and sanitation rather than building stadiums.

Addressing the investment opportunity, Mr. Soyoye offered his perspective on accessing infrastructure through private equity. “There have been some amazing road projects…I think we’re looking to invest more in infrastructure in Africa but finding the right ones where we can get 30% returns and cycle that money within the 10-year timeframe is the thing we’re going to try to sort out.” Critical infrastructure build-out will not only provide a variety of investment opportunities but will literally lay the foundation for Growth Markets to pursue their ultimate potential.

Infrastructure: Building the Growth Market Dream

Babtunde Soyoye, Eduarda La Rocque, Prashant Khemka, Daniel Alexander Jordaan and Colin Coleman

InfrastructureInfrastructure development is critical to the growth trajectory of a country and its ability to realize its full economic potential. Improved infrastructure—be it a more reliable power supply, increased technological adaptation, better access to clean water and sanitation facilities or enhanced transport links—drives productivity gains, supports growth and increases the overall welfare of a country’s population.

Facts

• According to its twelfth Five Year Plan, China will invest $1 tn in infrastructure spending over the next five years. Brazil’s government committed to spending $900 bn on construction of railways, ports and power generation facilities. India is estimated to spend $500 bn on logistics infrastructure in the next decade.1

• Approximately one quarter of Nigeria’s population has access to adequate power, resulting in Nigeria being the world’s largest importer of diesel generators. Electricity from diesel generators costs on average five times more than when sourced from the grid.2

• Brazil, Russia and Korea will all host major sporting events over the next six years, heightening the need for infrastructure spending and improvements.3

Paved Roads

ll econommicic

1. Source: GSAM, McKinsey and Company, Building India: transforming the nation’s logistics infrastructure, as at July 2010; 2. Source: GSAM Strategy Series from the Office of the Chairman, The Rise of the BRICs and N-11 Consumer, December 2010; 3. Source: Global ECS Research, Global Economics Paper 166–Building the World: Mapping Infrastructure Demand, 24 April 2008

Source: World Bank, as at 2009

2012 GROWTH MARKETS

SUMMIT

15This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. GSAM leverages the resources of Goldman, Sachs & Co. subject to Chinese Wall restrictions. Please see additional disclosures.

Over the next decade, the $5 tn BRIC consumer could double and exceed the size of the US consumer. Govindraj Ethiraj, Former Founder-Editor in Chief of Bloomberg UTV, Juan Pablo Zucchini, Managing Director at Advent International, Ian Mukherjee, CIO of Amiya Capital LLP and Harvey Sawikin, Principal at Firebird Management LLC discussed specific drivers in Brazil, Russia, India and China that could fuel what might be the investment theme of the decade during a panel hosted by GSAM’s Kathryn Koch, Senior Portfolio Strategist and Chief of Staff for the Office of the Chairman.

The panelists described some of the unique opportunities and challenges to tapping the consumer in each country. “One big problem India has faced over the decades is a national portable ID for every Indian,” explained Mr. Ethiraj. Now, India’s unique identification (UID) program has a target of 600 mn unique identities that are biometrically linked by 2014. This achievement, combined with a legislative enablement, will allow hundreds of millions of potential consumers to open bank accounts and establish financial identities for the first time in their lives. Mr. Mukherjee suggested that in China, “The consumer had dropped from about 50% of the economy a decade ago to just above 30%. I think it might be quicker getting back to 50%.…It’s definitely going to increase and it’s going to be a big theme over the next decade. But it will be a

bumpy ride.” Addressing the concern that Brazil’s active consumer may be taking on too much debt, Mr. Zucchini stated, “All the metrics indicate that although the debt market is growing fast, it is still an under-penetrated market,” while Mr. Sawikin elaborated on the changing demographics in Russia, including life expectancy, birth rates and immigration. Importantly, he noted, there are “145 mn Russians, but half of them are middle class and the GDP per capita is already over $10,000, heading to $20,000, according to Jim O’Neill.”

The rise of the BRIC consumer is driving activity in both public and private equity markets and leading to a variety of investment opportunities. Mr. Zucchini noted that the Brazilian equity market is “becoming again more selective and more and more difficult for the entrepreneurs to do an IPO at a reasonable price. And that’s where I think private equity investors will find a place to play in that game.” Mr. Sawikin expressed optimism on the Russian market, suggesting there are “plenty of M&A deals going on, they’re trying to buy companies, merge, there’s an incredible amount of business activity among the Russians right now.” Mr. Mukherjee reflected on investing in Chinese consumer trends, which often change very quickly and sometimes reflect a preference for Western aspirational brands, saying, “It’s very fickle domestically, so we felt more comfortable looking at some of the big international

Consumption & DemographicsIn the next 40 years, over four billion people globally could cross over into the middle class. This could be one of the single most significant structural changes ever seen in the global economy and should create a significant number of investment opportunities. Fundamentally, it is demographics— the size and youthfulness of developing market populations—that will drive this shift.

Facts

• The BRIC and N-11 countries account for almost two-thirds of the global population.1

• The median age in Growth Markets is considerably lower than in developed markets, which face the challenges of an ageing population.1

• Over the next 15 years, over a billion people could enter the middle class within the Growth Markets.2

• China is the world’s largest market for autos, mobile telephones and flat screen televisions. In 10 years, it could become the largest aviation market, and, in 15 years, the largest luxury goods market.3

• The BRICs could together add up to $1 tn of additional real consumption each year to 2025.3

• The Growth Markets and BRIC consumer could overtake the US consumer inside the next 5 and 10 years respectively.3

Real Consumption % Change in 2009-2025

on to the miiddddlele

Source: International Monetary Fund

1. Source: GS Global ECS Research and GSAM; 2. Source: Goldman Sachs Global ECS Research, Four Demographic Trends that Will Shape the 21st Century by Jim O’Neill, June 24, 2009; 3. Source: UN data, as at 2010

Juan Pablo Zucchini, Ian Mukherjee, Harvey Sawikin, Govindraj Ethiraj and Kathryn Koch

The Rise of the BRIC Consumer

brands.” Mr. Ethiraj also reiterated the accelerated opportunity for consumer products and financial services companies presented by “the creation of another 300 mn consumers who were never in the `savings & payments’ pipelines.”

Rapidly growing economies, rising middle classes and increased focus on domestic spending are driving a consumption boom in the BRICs and proving to be a powerful investment theme.

The economic and market forecasts presented herein for informational purposes as of the date of this presentation. There can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this presentation.The views and opinions expressed are those of the speaker, for informational purposes only and do not constitute any investment advice or recommendation by Goldman Sachs. We have relied upon and assumed (without independent verification) the accuracy and completeness of such information and neither agree nor disagree with the content herein.

16 This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. GSAM leverages the resources of Goldman, Sachs & Co. subject to Chinese Wall restrictions. Please see additional disclosures.

The views and opinions expressed are those of the speaker, for informational purposes only and do not constitute any investment advice or recommendation by Goldman Sachs. We have relied upon and assumed (without independent verification) the accuracy and completeness of such information and neither agree nor disagree with the content herein.

The Role of Healthcare and Education in Delivering Sustainable Growth“Healthcare is probably one of the big demarcation points between what is a Growth Market country and what is not if you look at what is the defining characteristic. India, China and Brazil all have low expenditure of healthcare GDP. Education as well,” said Dinakar Singh, the founder and CEO of TPG-Axon Capital, in a conversation about improvements and challenges to healthcare and education in the Growth Markets. Gabriella Antici, CIO and Head of GSAM Brazil, hosted the panel which also featured Amit Bhatia, the founder and CEO of Aspire Human Capital Management, Ricardo Leonel Scavazza, the CEO of Anhanguera Educacional, Brazil’s largest publicly traded education company and Shivinder Singh, Executive Vice Chairman of Fortis Healthcare Limited.

The affordability and accessibility of healthcare and education was a key theme to emerge from the discussion. The panelists drew from their experiences, predominantly in India and Brazil. Discussing the quality of healthcare in India, Mr. Shivinder Singh noted that 80% of costs are paid out-of-pocket, which creates a need to control costs, and that the majority of healthcare services are provided by the private sector, in which over 84% of hospitals have fewer than 30 beds. This has created an opportunity for the private sector to develop high quality solutions for lower costs in India and then expand those solutions globally. In the process of extending these low-cost structures to international markets, healthcare companies in India can offer and learn new models and capabilities from these new countries. Mr. Shivinder Singh remarked, “What we realized over the last decade is that whereas we’ve managed to take care of the gap that existed in India, what we don’t have is experience in areas where India has not really developed yet such as newer models of healthcare delivery, like specialized ambulatory healthcare facilities, primary care networks and so on and so forth.”

As the discussion turned to education, Mr. Scavazza shared his opinion on the challenges of graduating more students from college in Brazil, where about 80% of education is private. He said, “The issue is funding, and I believe that the Brazilian government finally made the move to provide this funding basically through loans for private schools.” Mr. Bhatia reflected on a different path toward better education in India, saying “I think as the government starts shrinking their role in education, and public partnerships evolve, how entrepreneurs step up to accept their roles and grow the education market is going to be the other set of opportunities.”

From an investment standpoint, there is a lot of consolidation in Growth Markets’ healthcare and education companies, which should help investors better identify emerging winners.

Shivinder Singh, Dinakar Singh, Ricardo Leonel Scavazza, Amit Bhatia and Gabriella Antici

Healthcare & Education Poor health conditions and low levels of education hinder productivity and technological adoption, thereby worsening a country’s growth environment and inhibiting income growth. While human capital indicators have improved across Growth and Emerging Markets, they remain a long way from developed market levels, and require significant further development. Critically, this improvement must not solely be undertaken by the public sector, but can be expedited by the inclusion of private sector enterprises.

Facts

• Global poverty—as measured by those on incomes of $1.3 per day or less—has fallen to half its 1990 level, achieving the UN’s Millennium Development Goal 5 years earlier than the initial 2015 target.1

• Global spending on medicine is expected to reach $1.1 tn by 2015, with Growth and Emerging Markets’ share expected to increase from 12% in 2005 to 28% in 2015.2

• Higher education enrollment in Brazil and India has increased by 10% and 6% per annum, respectively, over the last decade. Developed world enrollment growth has been only 2%.1

• In Growth and Emerging Markets, 443 mn school days per year are lost due to water-related diseases.3

% Enrollment into Tertiary Education

ity worseneniningg a a

Source: World Bank, as at 2009

1. Source: World Bank, Economist; 2. Source: The Economist; 3. Source: The United Nations; 4. Gross enrollment % is the ratio of total enrollment, regardless of age, to the population of the age group that officially corresponds to the level of education shown (ages 18-24)

2012 GROWTH MARKETS

SUMMIT

17This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. GSAM leverages the resources of Goldman, Sachs & Co. subject to Chinese Wall restrictions. Please see additional disclosures.

AfricaFor decades, poverty, corruption, civil war and famine have been words associated with the African continent. Despite these challenges, we believe Africa is showing strong signs of economic growth. With some of the most attractive natural resource opportunities in the world and an entrepreneurial population of over a billion people, we believe Africa is poised to grow exponen-tially in the decades to come.

Facts

• Africa’s land mass equates to over 30 mn km2. This is 20% of the world’s land mass and equivalent in size to China, the United States, India, Western Europe and Argentina combined.1

• Africa is estimated to be home to over 60% of the world’s uncultivated arable land and responsible for half of the world’s diamond production.2

• Close to half a billion people across Africa could be lifted out of poverty and into the middle class by 2050.3

• The median age in Africa is under 20 years old. The median age in the United States, Western Europe and Japan is 37, 42 and 44 years old, respectively.4

Africa’s Land Mass Equals

continenentt. D Desespipitete

1. Source: Times Atlas; 2. Source: International Monetary Fund; 3. Source: GS Global ECS Research, as at February 2011; 4. Source: UN data, as at 2008

Is Nigeria the Next BRIC?

Babatunde Soyoye, Mansur Muhtar, Tito Mboweni and Colin Coleman

With GDP growth of about 7% in the last few years, a wealth of natural resources and a population of 160 mn, could Nigeria really surpass South Africa to become Africa’s biggest economy by 2050, as suggested by Jim O’Neill? Tito Mboweni, Former Governor of the South African Reserve Bank and International Advisor to Goldman Sachs, Mansur Muhtar, Alternate Executive Director for Angola, Nigeria and South Africa at the World Bank and Babatunde Soyoye, Managing Partner at Helios Investment Partners LLP, discussed Nigeria’s potential and challenges in a panel hosted by Colin Coleman, Head of Investment Banking for Sub-Saharan Africa at Goldman Sachs.

Nigeria’s serious power generation shortfall - its $250 bn economy operates on 3,000 megawatts of capacity but probably needs closer to 30,000 – is seen as a major hurdle to the country’s growth. Dr. Muhtar stated, “The key issue is really unlocking the potential of the economy in terms of infrastructure. Power sector reforms are key to this process, and there has been a lot of effort, first, in trying to complete ongoing power projects, but secondly, completing reforms, privatization, encouraging private sector participation through Independent Power

Producers so as to double the available power, among other things.”

What is the best way to access investment opportunities in Nigeria? Mr. Mboweni believes that with regards to development, the private sector has “a very important role to play. There are certain things that governments don’t seem to be able to do, or if they do them, do them very slowly and clumsily.”

Mr. Soyoye believes the public equity market faces two issues. “The problem I think is that the biggest companies in South Africa are listed, the mining companies, the telcos, power companies etc… in the rest of Africa including Nigeria, it’s still a very private equity-type environment, where the best performing companies in the most interesting sectors actually are all privately held. This will change with the right incentives.”

In summarizing his view on the current investment environment, Dr. Muhtar stated, “The attention is now focused on how to deepen and broaden the market, which has experienced some challenges in the past. There has been a lot of effort to strengthen regulation to build capacity and there has been a lot of discussion about

how you can get some of the oil companies and others listed on the stock exchange so they can broaden and enhance their liquidity and get more involvement.”

Population, power generation and private equity have the potential to drive Nigeria’s rise amongst the Growth Markets.

The economic and market forecasts presented herein for informational purposes as of the date of this presentation. There can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this presentation. The views and opinions expressed are those of the speaker, for informational purposes only and do not constitute any investment advice or recommendation by Goldman Sachs. We have relied upon and assumed (without independent verification) the accuracy and completeness of such information and neither agree nor disagree with the content herein.

18 This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. GSAM leverages the resources of Goldman, Sachs & Co. subject to Chinese Wall restrictions. Please see additional disclosures.

The views and opinions expressed are those of the speaker, for informational purposes only and do not constitute any investment advice or recommendation by Goldman Sachs. We have relied upon and assumed (without independent verification) the accuracy and completeness of such information and neither agree nor disagree with the content herein.

Sports & GlobalizationAcross the globe convergence between the sports and entertain- ment industries continues as both sectors strive to take advantage of new digital technologies and rising consumer demand for sporting events and sports merchandise. Concurrently, large scale sporting events like the World Cup and the Olympic Games are playing a significant role in the economic development of Growth Market countries, especially Brazil and China.

Facts

• The world’s most popular sport, soccer, generated total global revenue of $23 bn in 2011 compared to the National Football League’s $9 bn in revenue.1

• Manchester United, the world’s most valuable sports franchise, now boasts a total of 70 mn registered subscribers to its websites in China and Russia, an indication of how these Growth Markets have embraced the globalization of soccer.2

• In Q1 2012, viewership of live National Basketball Association games on CCTV5—China Central Television’s all-sports channel—is up 39% compared to Q1 2011 and is ranked as the No. 1 most followed sport in China.3

• The rise of foreign sports stars in Western markets is further globalizing the sports audience around the world. Jeremy Lin’s popularity has increased NBA ratings in Taiwan 16-fold to approx. 2.4 mn viewers per game.4

Summer Olympic Medal Counts

sectors s ststririveve

Source: International Olympic Committee

1. Source: Deloitte Football Money League Report, 2012; 2. Source: Jim O’Neill, The Growth Map; 3. Source: National Basketball Association; 4. Source: China Times

Sports and Globalization

Few mediums better reflect just how interconnected the world has become than the rapid globalization of sports. David Stern, Commissioner of the National Basketball Association for over 28 years, sat down with Eric Lane, Goldman Sachs Global Co-Head of the Investment Management Division, for a candid conversation about the relationship between sports and globalization.

Mr. Lane began the discussion by asking Mr. Stern to elaborate on the NBA’s strategy in the international markets, especially in China, where basketball is the most followed sport.

Mr. Stern explained that the NBA entered new markets by partnering with local media outlets in markets like China and finding ways to create win-win scenarios for both parties. “I made the first deal myself in late 1980s with China Central Television. We made a revenue-sharing deal,” Mr. Stern said, “They would run the games and we would share revenue. There was no revenue to share, but we sent the check religiously, so to speak, because we wanted the games to be there.” He added, “We have 20 regional deals, and we have just moved along. We’re slowly growing with offices in Shanghai and Beijing, and probably Guangzhou in the very near future.”

The conversation then turned to the increasingly global nature of sports ownership. Mr. Stern acknowledged this trend, highlighting Mikhail Prokhorov’s

ownership of the Brooklyn Nets and the Glazer family’s ownership of Manchester United as examples. He added that globalization continues to encourage the international flow of capital, and sports leagues are now, finally, benefiting from increased access.

Mr. Stern explained that one factor driving the expansion of the NBA is the fact that sports aligns with the increasing global concern over obesity and related health issues. Mr. Stern said, “One of the reasons we have a huge advantage is because basketball is this global sport that’s played all around the world and people are fans. We’re dealing with a lot of governments who are dealing with the obesity and diabetes problem. There is no question about it. Saudi Arabia has a huge problem. India has an increasing problem as our wonderful American lifestyle gets out there. And the Chinese government is particularly focused on exercise and the like. So we come in sort of two different ways. We come in on the business side or we go in on the, shall we say, social responsibility side. And invariably, there are either government departments or businesses that are quite concerned with the issue, and we manage to tie them together.”

Looking ahead to the next decade, Mr. Stern concluded his remarks with the hope that the NBA continues to contribute to the development of NBA-affiliated and sponsored leagues across various global markets, including Asia, Europe and Latin America.

David Stern and Eric Lane

2012 GROWTH MARKETS

SUMMIT

19This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. GSAM leverages the resources of Goldman, Sachs & Co. subject to Chinese Wall restrictions. Please see additional disclosures.

The economic and market forecasts presented herein for informational purposes as of the date of this presentation. There can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this presentation.

Energy: Can the World Fuel the Rise of the Growth Markets?

In 2010 China surpassed the US as the world’s largest consumer of energy, illustrating why the Growth Markets increasingly influence the dynamics in the global energy market. William Macaulay, Chairman and CEO of First Reserve Corporation and Aubrey McClendon, Chairman and CEO of Chesapeake Energy Corporation, shared their insights on this theme with Arjun Murti, Co-Director of Equity Research and Senior Energy Analyst at Goldman Sachs.

The new demand has pushed oil prices up dramatically over the last decade. Mr. Murti explained, “For the rate of growth that the world wants to have, there simply wasn’t enough ‘easy supply’ at $20 or $30 a barrel.” In non-OPEC (Organization for Economic Cooperation and Development) countries, demand is expected to dramatically outstrip supply. Energy consumption is expected to grow by over 75% in the non-OECD countries by 2030. Meanwhile, Mr. Murti observed, “One of the issues of the last decade has been how disappointing non-OPEC supply has been.” He noted, however, the US and offshore Angola in West Africa as bright spots in the oil supply outlook. Mr. Macaulay acknowledged the increased investment in the Southern Atlantic Basin in general, including the US Gulf of Mexico, Brazil and offshore West Africa

(for example, Angola). “You are seeing more and more oil activity in the Southern Atlantic Basin. This is a very important basin. But I think this is because the supply is needed and offshore is another big source of incremental oil. I think what offshore exploration discoveries will accomplish is they will enable the world to keep up with growing oil demand – in particular as it is needed for transportation fuel for non-OECD economies - but not necessarily overcome the expanding need that we have on a global basis.”

International investments in natural resources can be difficult. While the panelists noted opportunities in China, Russia and Eastern Europe in particular, they expect investment to be selective. Mr. Macaulay said, “You’re not going to see a revolution in terms of the geographies in which energy investments occur, but projected shale reserve potential will promote increased investment in select developing nations. However, when you put everything together on a risk reward basis, conducting successful business in some of these countries is not the easiest thing to do. There are a variety of challenging conditions. So, the question is not just whether or not shale oil and gas is present, it’s how we can realistically capture it.”

EnergyGrowth Market economies will be at the heart of the global energy market’s evolution over the next two decades. On the demand side, energy consumption is expected to grow by over 75% in the non-OECD countries by 2030. On the supply side, China, Russia and other developing economies will account for a significant share of the world’s energy production growth, particularly in alternative energy investment and innovation.

Facts

• In 2010, China surpassed the US as the world’s largest energy consumer, making up 20.3% of global energy consumption.1

• In 2010, Saudi Arabia was the largest producer of oil, at 10.5 mn barrels per day, followed by Russia at 10.1 mn barrels per day, and the US at 9.7 mn barrels per day.2

• The US is the world’s leading consumer of oil, at 19.2 mn barrels per day in 2010. The next largest consumer is China, at 9.4 mn barrels per day, and then Japan, at 4.5 mn barrels per day. These three countries are also the largest importers of oil.2

• The US Energy Information Administration estimates that the global supply of crude oil, other liquid hydrocarbons and biofuels is expected to be adequate to meet worldwide demand for liquid fuels for the next 25 years.

Share of fuel

o decaddeses OnOn tthehe

Source: BP Statistical Review of World Energy 2011

1. Source: BP Statistical Review of World Energy, 2011; 2. Source: U.S. Energy Information Administration*Includes biofuels

Growth may ease in Japan and Europe, even China and Russia as their populations age. But along with Brazil, India and the United States, which are likely to see ever growing populations, they will have a decisive impact on the growth of the world economy—and this will be critical for the demand for world energy. —Jim O’Neill

William Macaulay

20 This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. GSAM leverages the resources of Goldman, Sachs & Co. subject to Chinese Wall restrictions. Please see additional disclosures.

The views and opinions expressed are those of the speaker, for informational purposes only and do not constitute any investment advice or recommendation by Goldman Sachs. We have relied upon and assumed (without independent verification) the accuracy and completeness of such information and neither agree nor disagree with the content herein.

Connectivity Is Productivity: The Role of Innovation and Entrepreneurship in Low Income Countries

According to Iqbal Quadir, Founder and Director of the Legatum Center for Development and Entrepreneurship at MIT and Professor of the Practice at MIT, investing in local enterprises in general and enhancing connectivity in particular are the best solutions for driving growth in developing countries.

Dr. Quadir drew on two personal experiences in which his inability to connect with other people led to inefficiency and therefore to the conclusion that “connectivity is productivity. If you connect, it enables you to get things done. If you disconnect someone, you basically disable them.” To put this idea into practice, Dr. Quadir partnered with Grameen Bank to provide mobile phones throughout Bangladesh. Dr. Quadir’s view was that the cost of additional telephone service would be self-financed by the resulting increased productivity brought about by improved

connectivity. “If people become more productive, then they can use that increased productivity to pay for it.”

Prior to launching his efforts to create what is now Grameenphone nearly 20 years ago, only one out of every 500 people in Bangladesh had telephones. Now, the country has 80 mn cell phones, meaning one out of every two people has telephones.

What’s next for Bangladesh? According to Dr. Quadir, the country has similar characteristics to China and may be poised for additional growth in the coming years. Bangladesh’s GDP today is about the same size as China’s just 30 years ago and is growing at 6% annually with the country’s exports expected to triple in five years. According to Dr. Quadir, “The fact that Bangladesh is a country that has historically been prosperous, then slept for a while, and is coming up is another interesting parallel between China and Bangladesh.”

The Paradox of Investor Short-Termism

Investors globally have shifted their strategic asset allocation to accommodate the rise of the Growth Markets, particularly the BRICs. At the 2012 Growth Markets Summit, Knut N. Kjaer, Former Founding CEO of the Norwegian Sovereign Wealth Fund and Chairman of FSN Capital Partners and Trient Asset Management, presented his thoughts on the “paradox of investor short-termism.”

Mr. Kjaer began by pointing out that the emergence of the Growth Markets, particularly China and India, is actually part of a cycle that began roughly 2,000 years ago. He noted that he believes “a key issue for investors today is that we are too short sighted. Even long-horizon investors keep on chasing alpha in the crowded short-term space and are not exploiting their competitive edge. They often fail in the top down management of

risk factors, and their biggest mistake is herd-behavior and procyclical investments.” With current estimates showing the BRIC contribution to global GDP reaching close to 40% by 2050, this could be a time to rebalance portfolios to further incorporate the Growth Markets and generate value in a portfolio.

Mr. Kjaer emphasized the importance of maintaining a disciplined strategic asset allocation, even when it requires taking a contrarian or unpopular position. Additionally, Mr. Kjaer stressed being able to take a long-term view when implementing asset allocation decisions and working to identify long-term trends. The Growth Markets could have the underpinnings of a long-term trend that investors would not want to ignore in their portfolios.Knut Kjaer

Iqbal Quadir

2012 GROWTH MARKETS

SUMMIT

21This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. GSAM leverages the resources of Goldman, Sachs & Co. subject to Chinese Wall restrictions. Please see additional disclosures.

The views and opinions expressed are those of the speaker, for informational purposes only and do not constitute any investment advice or recommendation by Goldman Sachs. We have relied upon and assumed (without independent verification) the accuracy and completeness of such information and neither agree nor disagree with the content herein.

Macroeconomic and Investment Insights

As ongoing concerns over the European sovereign debt crisis and fiscal austerity in the developed world continue to present challenges for investors, Growth Markets offer a compelling investment opportunity. Sam Finkelstein, Head of Macro Strategies within the Global Fixed Income team in Goldman Sachs Asset Management, Tito Mboweni, Former Governor of the South African Reserve Bank and International Advisor to Goldman Sachs and Cecilia Reyes, member of the Group Executive Committee and Chief Investment Officer of Zurich Insurance Group (Zurich) discussed the current macroeconomic environment and potential investment opportunities in a conversation hosted by Hugh Lawson, Co-Head of Alternative Capital Markets at Goldman Sachs. Investing in the Growth Markets can offer higher yields and access to global growth. Mr. Finkelstein noted, “When you look towards the Growth Markets, you can generally pick up yield, in many cases ample yield, and improve the quality of the balance sheet and move towards where there is indeed global growth.”

Mr. Mboweni discussed the implications of this interest rate differential between growth and developed economies with a focus on how central banks are responding. Capital flows from developed markets to Emerging Markets strengthen the currency of the latter.

Resulting dislocations may prompt central bankers in Growth Markets to respond by lowering interest rates or intervening in the foreign exchange markets, leading to accumulation of reserves. According to Mr. Mboweni, this accumulation of reserves among developing countries is particularly concerning in light of the other risks present in the current global macroeconomic environment and in particular, “We should be concerned about the existence of these imbalances in the presence of this European debt crisis.”

Despite the challenging macroeconomic backdrop, the three panelists offered the audience several investment ideas. Mr. Mboweni discussed the opportunity to invest in infrastructure developments in Africa, including telecommunications, roads and bridges and hydropower. Dr. Reyes discussed opportunities in illiquid assets. In managing Zurich’s $200 bn balance sheet, Dr. Reyes applies an asset liability approach to investing, investing the assets to mitigate the risks from their liabilities. Zurich allocates capital on a risk factor base framework, looking at interest rate, term structure (or inflation), credit, liquidity and equity risk. Because illiquidity risk is a component of Zurich’s liability, investing in illiquid assets such as private equity, hedge funds, real estate and corporate bonds “affords us the ability to invest in illiquid assets and access the liquidity of

Cecilia Reyes, Tito Mboweni, Sam Finkelstein and Hugh Lawson

1. Source: The BRICs 10 Years On: Halfway Through the Great Transformation, GIR, December 2011; 2. Source: An Update on the Long-Term Outlook for the BRICs and Beyond, Jim O’Neill, January 2012

MacroeconomicsThe macroeconomic environment continues to present a complex set of challenges and considerations for both policy-makers and investors in 2012. Despite recent signs of improvement, there is continuing uncertainty about many aspects of the global economy, including the ongoing European sovereign debt crisis and fiscal austerity in the developed world. Despite this, growth has been resilient in many parts of the world.

Facts

• The BRICs have moved from 11% of global GDP (about 30% for broad Emerging Markets) in 1990 to around 25% (50% for broad Emerging Markets) currently. By 2050, we expect the BRICs to have reached close to 40% of global GDP and broad Emerging Markets to reach 73%.1

• The BRICs are still set to become the top five largest economies by 2050, together with the US. In 2050 the N-11 as a group is still projected to be larger than the US and almost twice the size of the Euro area.2

• The ten most populous African countries could, on aggregate, grow to over 15 times their current size by 2050, falling somewhere between Brazil and the Euro area.2

Global Market Consumption Could Drive Global Growth

Source: GS Global ECS Research, and GSAM calculations

r both popolilicycy-

risk premium and at the same time you’re actually reducing the risk on an asset liability basis.”

To capture the growth of developing economies, Mr. Finkelstein challenged investors to consider a GDP-weighted approach to asset allocation instead of the typical market cap-weighted approach. Mr. Finkelstein said, “If you own a market cap portfolio, you are likely to have the highest exposure to some of the most indebted countries and at least today, when you look at what you’re getting compensated for taking that risk, it is not very much indeed.”

22 This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. GSAM leverages the resources of Goldman, Sachs & Co. subject to Chinese Wall restrictions. Please see additional disclosures.

The views and opinions expressed are those of the speaker, for informational purposes only and do not constitute any investment advice or recommendation by Goldman Sachs. We have relied upon and assumed (without independent verification) the accuracy and completeness of such information and neither agree nor disagree with the content herein.

Divya Keshav, Isobel Coleman, Luis Alberto Moreno and Dina Habib Powell

Investing in Women Is Smart EconomicsOver the last several years, corporations, non-profits and government agencies have become increasingly aware of the critical role that women play in the global marketplace. Goldman Sachs similarly recognized the power of investing in women and in March 2008 launched 10,000 Women, a $100 mn initiative to provide business and management education to underserved female entrepreneurs in developing countries. Dina Powell, President of the Goldman Sachs Foundation and Global Head of Corporate Engagement, moderated a panel discussion with Isobel Coleman, Senior Fellow at the Council on Foreign Relations, Luis Alberto Moreno, President of the Inter-American Development Bank and Divya Keshav, a graduate of the 10,000 Women program.

President Moreno acknowledged the inconsistent integration of women in the Latin American economy and ongoing gender gaps in entrepreneurship development. He noted that women comprise half of Latin America’s population, and “more than 15% of the Latin American population of entrepreneurs. Yet, as entrepreneurs, women have the biggest amount of failure. This is why initiatives such as [10,000 Women] are so critical.”

Ms. Keshav, the owner of Krishna Printernational, a firm in India that

manufactures self-adhesive labels and provides customized labeling solutions, agreed with Mr. Moreno’s statement, adding that “Entrepreneurship was not a very popular option for women in India. But as the social and economic scenario changes in India, women are advancing more. I feel with better access to education, skill sets and knowledge, I think women can progress much more.”

Dr. Coleman discussed the economic benefits of achieving gender equality: “When you look at the large gender gaps that still exist around the world in terms of nutrition, education, access to credit - all these types of things present an opportunity. If you close those gaps, some have equated it to bringing online the equivalent of an Emerging Market the size of India or China.”

Speaking on a personal level, Ms. Keshav discussed the ways in which 10,000 Women helped her grow her business, “The mentoring that is provided helps us to know that yes, we are on the right track and also helps us measure and think in advance. The business plan that we made as part of the 10,000 Women program actually helped me realize where I could reach, and I could even reach beyond that in terms of my sales revenue and my profits.”

WomenomicsThe empowerment of women is one of the most effective means to reduce inequality and facilitate inclusive economic growth. Investing in women’s empowerment creates a significant multiplier effect leading not only to healthier and better educated families, but also to more prosperous communities. As Goldman Sachs CEO & Chairman, Lloyd Blankfein, has said, “…when you get to the topic of trying to invest and create GDP, there is no better or more efficient investment than the investment you make in women.”

Facts

• In 2010, women’s labor force participation rates remained below 30% in North Africa and Asia, and below 40% in Southern Asia. In Latin America, female labor force participation is above 50%.1

• Restricting job opportunities for women in the Asia and Pacific countries is costing the region between $42-46 bn each year.2

• The approximately 8 to 10 mn women-owned small-medium sized enterprises (SMEs) represent 31% of the total SMEs in developing countries.3

usive ecocononomim c

Source: Goldman Sachs Research—Japan Portfolio Strategy, Womenomics 3.0: The Time is Now, Oct 2010

1. Source: World Bank Report on Gender Parity, 2012 Inter-American Development Bank, Gender Equality by the Numbers, 2010 2. Source: World Economic Forum Global Gender Gap Report, 2011 3. Source: McKinsey-IFC SME Database; Enterprise Survey—Why Women Entrepre-neurs Matter; ILO, Human Development, October 2011

2012 GROWTH MARKETS

SUMMIT

23This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. GSAM leverages the resources of Goldman, Sachs & Co. subject to Chinese Wall restrictions. Please see additional disclosures.

The views and opinions expressed are those of the speaker, for informational purposes only and do not constitute any investment advice or recommendation by Goldman Sachs. We have relied upon and assumed (without independent verification) the accuracy and completeness of such information and neither agree nor disagree with the content herein.

A Conversation with Leon Cooperman and David McCormick

David McCormick, Leon Cooperman and Jim O’Neill