2011 european facility management - opportunities in a 98 billion euro market

TRANSCRIPT

2011 European Facility Management 2011 European Facility Management

Opportunities in a 98 Billion Euro MarketOpportunities in a 98 Billion Euro Market

Michael Meyer, Industry Analyst

30th November 2011

Today’s Presenter

Michael Meyer, Industry Analyst

Frost & Sullivan

2

Michael Meyer is an Industry Analyst with the Frost & Sullivan Europe Energy &

Environment Practice. He focuses on monitoring and analyzing emerging

trends, technologies and market dynamics in the Building Technologies markets

in Europe.

Michael has authored various research on the European Facility Management

Markets and completed several consulting assignments for some of the main

players in the industry.

Focus Points

Market Segmentation by End-user Contract Type

Definition of the Total FM Market

3

Focus Points

Competitive Landscape

Conclusions

Trends, Dynamics, and further Segmentations

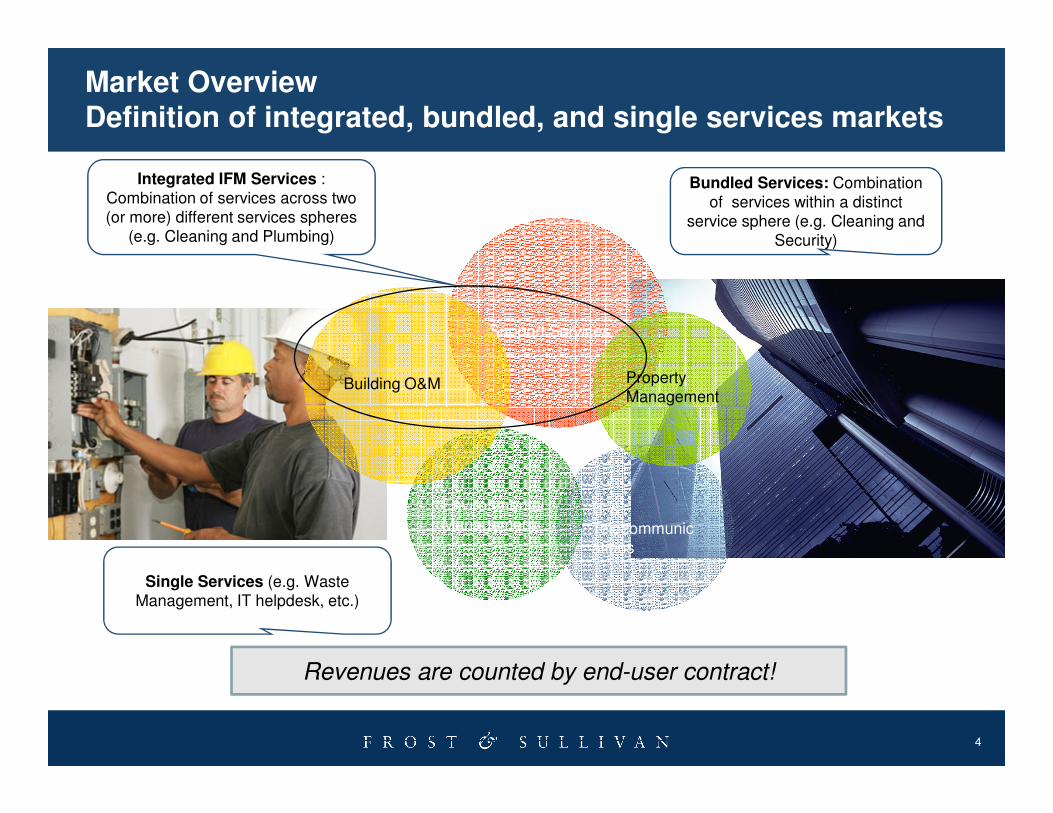

Market Overview Definition of integrated, bundled, and single services markets

Support Services

Property

ManagementBuilding O&M

Integrated IFM Services :

Combination of services across two

(or more) different services spheres

(e.g. Cleaning and Plumbing)

Bundled Services: Combination

of services within a distinct

service sphere (e.g. Cleaning and

Security)

4

IT &

Telecommunic

ations

Environmental

Management

Single Services (e.g. Waste

Management, IT helpdesk, etc.)

Revenues are counted by end-user contract!

Market Segmentation by End-user Contract Type Market

5

� Total Outsourced FM Market is 98.61 € Bn

� Single services is by far the largest market in Europe (60.56 € Bn)

� The outsourcing rate is 47.6%.

� The In-house market still accounts for the largest opportunity (108.76 €Bn)

47.6% Outsourcing Rate

Countries include: UK, Germany, France, Italy, Spain, Benelux, Scandinavia, Alpine

Market Growth

� Total additional opportunity to

2016 of 6.14 € Billion

� Fast growing markets for

integrated and bundled services

� Slight decline for single services

6

� Slight decline for single services

due to:

• Continuing price pressure

• Exclusion of revenues from sub-

contracting

• Service Integration (through

‘contract migration’)

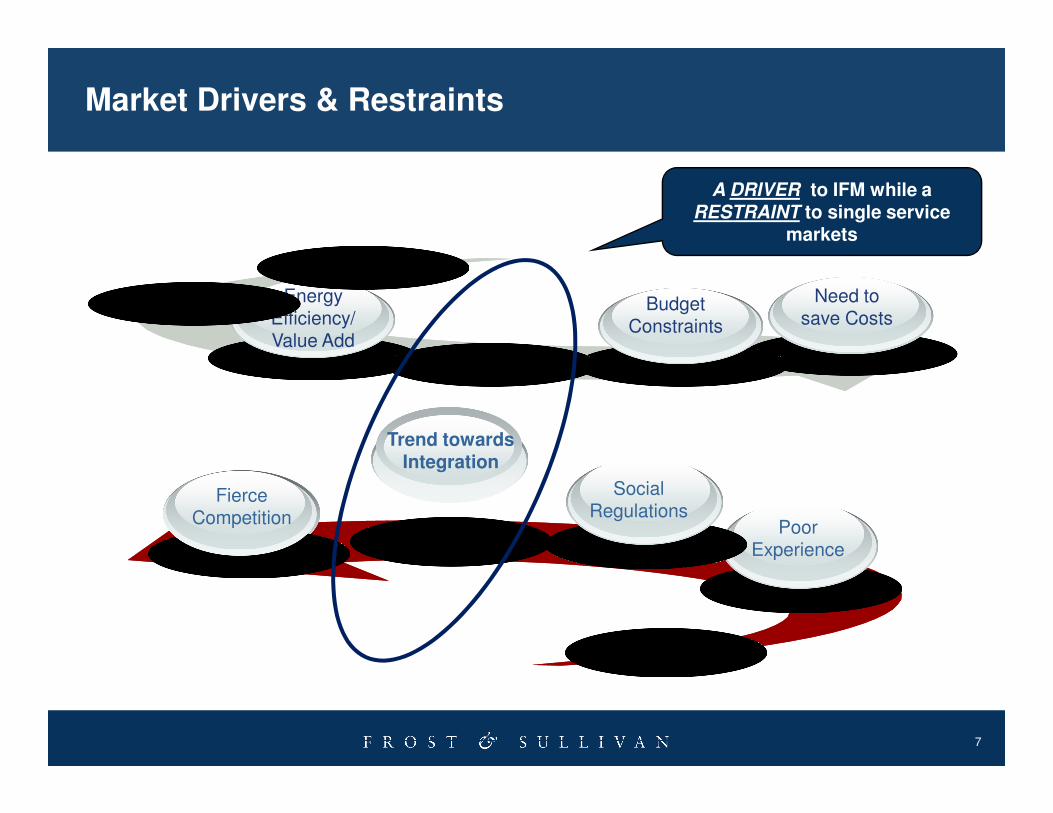

Market Drivers & Restraints

Need to save Costs

Energy Efficiency/ Value Add

Budget Constraints

A DRIVER to IFM while a RESTRAINT to single service

markets

7

Poor Experience

Fierce Competition

Trend towards Integration

Social Regulations

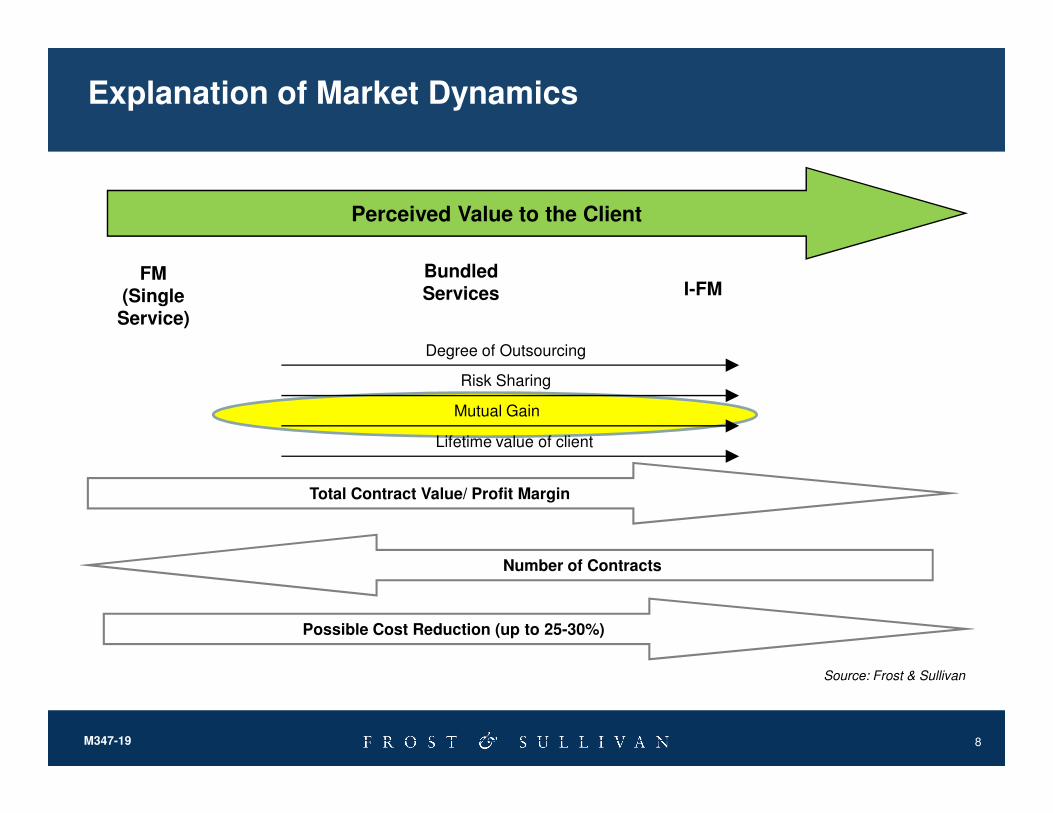

Explanation of Market Dynamics

Perceived Value to the Client

FM(SingleService)

I-FMBundledServices

Degree of Outsourcing

Risk Sharing

Mutual Gain

8M347-19

Source: Frost & Sullivan

Total Contract Value/ Profit Margin

Mutual Gain

Lifetime value of client

Number of Contracts

Possible Cost Reduction (up to 25-30%)

Geographical Split

9

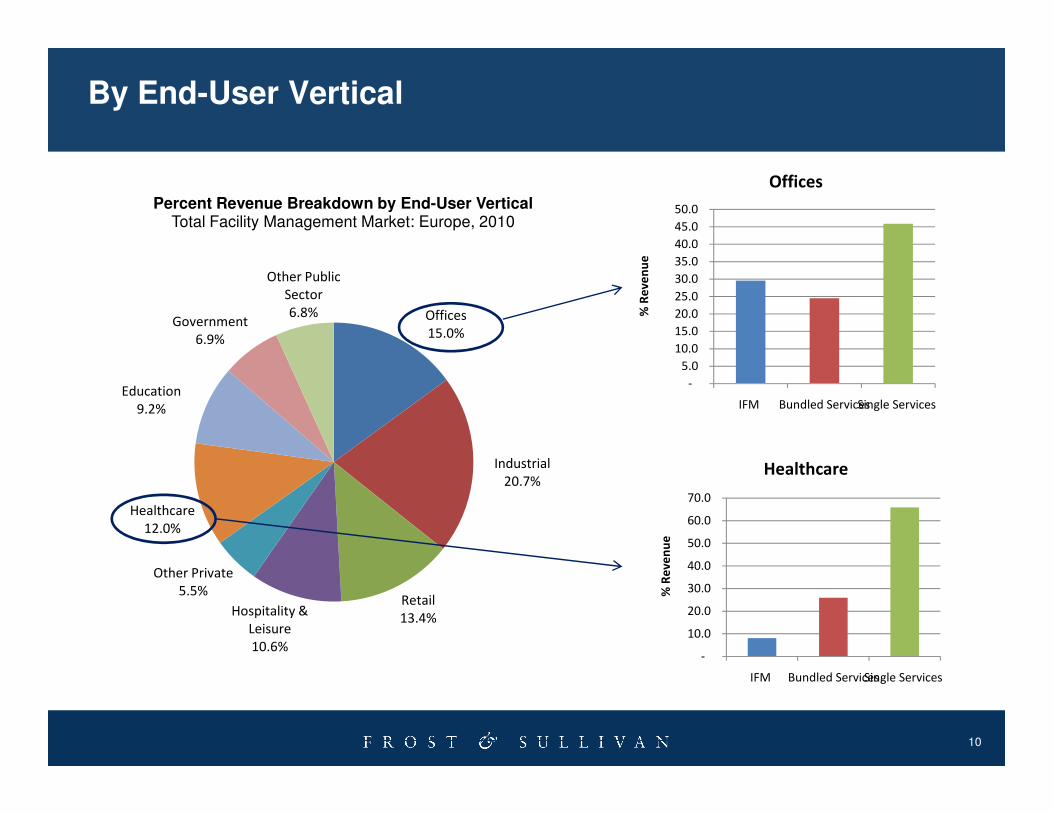

By End-User Vertical

Offices

15.0%

Education

9.2%

Government

6.9%

Other Public

Sector

6.8%

Percent Revenue Breakdown by End-User VerticalTotal Facility Management Market: Europe, 2010

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

IFM Bundled ServicesSingle Services

% R

ev

en

ue

Offices

10

Industrial

20.7%

Retail

13.4%Hospitality &

Leisure

10.6%

Other Private

5.5%

Healthcare

12.0%

9.2% IFM Bundled ServicesSingle Services

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

IFM Bundled ServicesSingle Services %

Re

ve

nu

e

Healthcare

By Service Type

50.0

60.0

70.0

80.0

90.0

100.0

% R

ev

en

ue

Revenues (2010): 52.8 € Billion

Revenues (2010): 13.1 € Billion

Catering

11

0.0

10.0

20.0

30.0

40.0

50.0

Support Services (incl. Cleaning, Security, etc.)Catering M&EOther (incl. Environmental, IT, etc.)

% R

ev

en

ue

Revenues (2010): 22.5 € Billion

Revenues (2010): 10.1 € Billion

Support Services

M & E Environmental, etc.

46.5% Share of

Bundled/ IFM

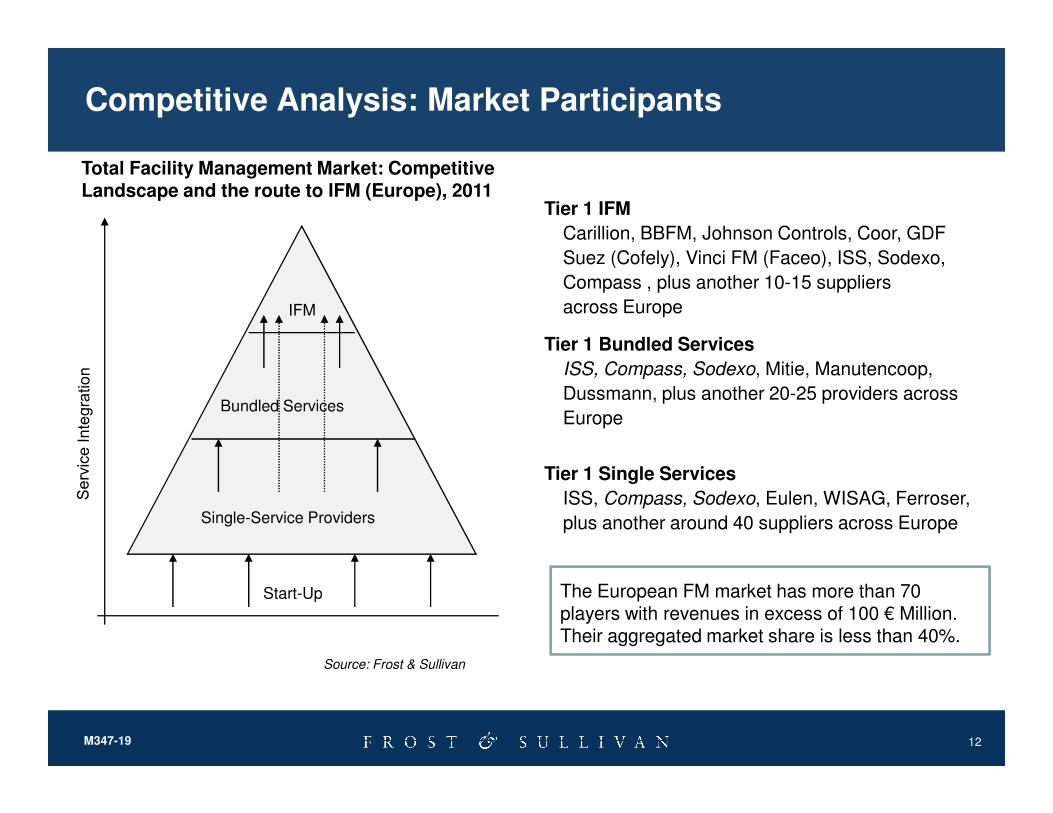

Tier 1 IFM

Carillion, BBFM, Johnson Controls, Coor, GDF

Suez (Cofely), Vinci FM (Faceo), ISS, Sodexo,

Compass , plus another 10-15 suppliers

across Europe

Tier 1 Bundled Services

ISS, Compass, Sodexo, Mitie, Manutencoop,

Dussmann, plus another 20-25 providers across

Competitive Analysis: Market Participants

Bundled Services

IFM

Total Facility Management Market: Competitive Landscape and the route to IFM (Europe), 2011

12M347-19

Europe

Start-Up

Single-Service Providers

Bundled Services

Source: Frost & Sullivan

Tier 1 Single Services

ISS, Compass, Sodexo, Eulen, WISAG, Ferroser,

plus another around 40 suppliers across Europe

The European FM market has more than 70 players with revenues in excess of 100 € Million. Their aggregated market share is less than 40%.

Conclusions

The FM Market has its own dynamics and ways of counting. Sub-contracting and cost saving effects from integration are important additional parameters

The in-house FM market still accounts for more than 50% of the total FM revenue opportunity, hinting at vast potential for market participants

Providers of integrated service concepts will continue to experience the highest growth rates

Source: Frost & Sullivan.

The share of IFM varies significantly by end-user vertical as well as by service type offering, significant long term potential exists in the public sector

Despite ongoing consolidation, the European FM will continue to experience a high degree of fragmentation

growth rates

The UK is most advanced in the adoption of integrated services concepts, however the substantial gap to other European markets will narrow

Next Steps

� Request a proposal for our Growth Partnership Services or Growth Consulting Services to support you and your team to accelerate the growth of

your company. ([email protected])

� Join us at our annual Growth, Innovation, and Leadership 2012: A Frost & Sullivan Global Congress on Corporate Growth (www.gil-global.com)

14

� Register for Frost & Sullivan’s Growth Opportunity Newsletter and keep

abreast of innovative growth opportunities

(www.frost.com/news)

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

What would you like to see from Frost & Sullivan?

15

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by “Rating” this presentation.

Follow Frost & Sullivan on Facebook, LinkedIn, SlideShare, and Twitter

http://www.facebook.com/FrostandSullivan

http://www.linkedin.com/companies/4506

16

http://twitter.com/frost_sullivan

http://www.linkedin.com/companies/4506

http://www.slideshare.net/FrostandSullivan

For Additional Information

Chiara Carella

Head of Corporate Communications

Europe, Israel, Africa

+44 (0) 207 343 8314

Michael Meyer

Industry Analyst

Environment and Building Technologies

+44 (0)20 7915 7826

17

John Raspin

DirectorEnergy and Environment +44 (0)20 7915 7814

Gerry Hill

Sales Manager

Environment and Building Technologies

0044 (0)207 915 7846