magnumold.magnum.co.in/magazinepdf/may 2009.pdf · d e c e m b e r may 2009 magnum d e c e m b e r...

TRANSCRIPT

D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

PB 1

Magnum ConnectIssue No. IX May 2009

Monthly Magazine

Subscription :-Cover Price: Rs 30/-Annual Subscription (12 issues) : India Rs 300/-Overseas (Airmail) US$ 150(Cheque/D.D. drawn on Mumbai in favour of

Magnum Wealth Management Pvt. Ltd.Regd. Office :Mr. Piyush K. Upadhyay (Correspondent)Magnum ConnectD-13, Empire Mahal, 806, Dr. B. A. Road,Khodadad Circle, Dadar T.T.,Mumbai – 400 014.For General Enquiries Contact :+91-22-2415 8686E-mail : [email protected] : www.magnum.co.inPrinted at : HariOM Printers, Mumbai.

Dear Friends,Another good month for the market has passed, we would like to see the markets swaying in the same direction for some more time, but the turbulent phase cannot be avoided just by doing your part. Lots of things depend upon the external factors that are beyond our control and one such factor, which we are currently facing, is the ongoing general elections in the country. We are half-way through the mega event and still everything seems blurred with no clear conviction or clear consensus of any single party or group appearing on the forefront to form the government. Our today’s requirement is a stable government that can lead us to the path of growth amid this slowdown and guide the nation to stability.Friends, in the passing month India’s central bank – Reserve Bank of India – announced its annual review of monetary policy where the bank cut the repo and reverse repo rates by 25 basis points each, as a means to give signal to the markets that the apex bank will continue the aggressive stand. However, the apex bank left the cash reserve ratio (CRR) unchanged at 5%. While the banks considered it as meager, it has further given strength to the interest sensitive sectors like reality and auto .Though the rate cuts were more or less in line with market expectations, the most striking points that came from the policy was that the apex bank has pegged the GDP forecast for the FY10 at about 6%. This estimate though was on the optimistic side but has represented the fact that the current slowdown has seriously affected developing nations like, India, too. The results season is on, though the trends so far has been mixed with no any major setbacks barring few and further announcements will show how good or bad the final quarter was and the just-concluded fiscal for different companies. In this month, all the election formalities will get completed and the picture will get clear as to who will form the government at the Centre. A fractured mandate and a fragile government will definitely mar the sentiments of the market and can give a serious setback in coming months, on the same side if the mandate comes for a stable government, it will boost the sentiments.

VIJAY B. SHAH(Director)

Magnum Group

This document has been prepared by M/s Magnum Wealth Management Pvt Ltd and is being distributed in India byM/s. Magnum Wealth Management Pvt Ltd a registered broker dealer. The information in the document has been compiled by the research department.

Due care has been taken in preparing the above document. However, this document is not, and should not be construed, as an offer to sell or solicitation to buy anysecurities. Any act of buying, selling or otherwise dealing in any securities referred to in this document shall be at investor’s sole risk and responsibility.

This document may not be reproduced, distributed or published, in whole or in part, without prior permission from the CompanyM/s. Magnum Wealth Management Pvt Ltd

Subject only to Mumbai jurisdiction

IndexCover Story Cement ............................................................. 2Equity

Company Research........................................... 5 Stock Update..................................................... 7Corporate News................................................. 8Market Snapshot............................................... 10

EconomyQuick Review of Economy................................ 12Economy News................................................. 16

StatisticsScorecard : Banking......................................... 18 Dividend Yield..................................................20Sales............................................................... 21High PE ........................................................... 22Low PE ............................................................ 23 Price Trend...................................................... 24

Mutual FundSectoral Mutual Fund Analysis......................... 25MF Scorecard................................................... 26

StudyCurrency Futures............................................... 31FII Trends .......................................................... 33

InsuranceSystematics Investment Plan............................ 35ICICI Lombard - Car Insurance ........................ 36

D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

2 3D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

2 3

Cover Story - Cement

Cement: India’s construction story1. Introduction: The Indian cement industry with a total capacity of about 211.8 million tonne (MT) at the beginning of fiscal 2010 is the second largest market after China. Al-though consolidation has taken place in the Indian cement industry with the top five players controlling almost 50% of the capacity, the balance capacity still remains pretty fragmented.The industry had been on a roll for 4-5 years till second half of FY09. Driven by a booming housing sector, global de-mand and increased activity in infrastructure development such as state and national highways, the cement industry outpaced itself, ramping up production capacity, attracting the top cement companies of the world, and sparking off a spate of mergers and acquisitions to spur growth.2. A brief history of Indian cement industry: The attempt to produce cement in India dates back to 1889 when a Calcutta firm attempted to produce cement from argillaceous (kankar). But the first organized effort on mass scale to manufacture Portland cement commenced in Madras (now Chennai) in 1904, by South India Indus-tries. However, the effort did not succeed. It was in 1914 that the first cement manufacturing unit in India was set up and commissioned by India Cement Company at Porban-dar in Gujarat, with an installed capacity of 10,000 tonnes. Subsequently two plants; one at Katni (Madhya Pradesh) and another at Lakheri (Rajasthan) were set up. The industry grew rapidly in the pre-independence era with supply often off-stripping demand resulting in a price war. However, in the early years of independence, huge growth in infrastructure construction resulted in demand rising sharply and soon the supply side bottlenecks ap-peared. To ensure a smooth supply of cement and to bring in more regional balance, government controls were implemented through 1969 to 1982. Though this period witnessed increase in supply, significant disequilibrium in various aspects of industry forced the government to first partially (1982) and then fully (1989) deregulate the indus-try. Since then the industry has been growing rapidly in a competitive atmosphere. 3. Characteristic of Indian cement industry: The Indian cement industry is characterised by its regional and seasonal nature due to vast geography of the country and high energy intensity. 3.1 Regional nature: The viability of the location plays a major role in the economics of cement manufacturing. As such, a major defining feature of the Indian cement industry is the location of limestone reserves in select parts of country, which has resulted in it’s evolution in the form of clusters. The proximity to coal deposits constitutes another important factor in determining the location. As a result, the cement industry has strong regional character-istics. Further, since cement is a high bulk and low value

commodity, competition is also localized because the cost of transportation of cement to distant markets often results in the product being uncompetitive in those markets. 3.2 Energy Intensive: The cement industry is highly energy intensive and power costs form the most critical cost component in cement manufacturing, contributing about 35% to total cost of production. This also results in emphasis on technology and hence importance of scale economies. As a result, the market structure of cement has developed into typical oligopoly with small number of large firms in direct competition with each other along with large number of small companies playing role of atomistic producers*. 3.3 Seasonal Demand: Another distinguishing charac-teristic of the Indian cement industry is its cyclical nature, as the market and consumption is closely linked to climatic and agricultural cycles. In India, cement production nor-mally peaks in the month of March while it is at its lowest in the month of August and September (monsoon months). The cyclical nature of the industry has also helped the cause of consolidation in the industry as the large players are able to easily withstand the cyclic downturn in demand due to their economies of scale, operational efficiencies, centrally controlled distribution systems and geographical diversification etc. 4. Growth of the industry in liberalised period: The cement industry has been on a high growth path ever since liberalisation of the economy took place in early 1990s. In recent years, the infrastructure development de-rive of the government has also helped the industry pick up rapid pace.

Year Installed Capacity(Million Tonnes)

Production (MT)

Per Capital Consumption

1991-92 66.56 53.61 631995-96 97.25 69.57 721999-00 119.1 100.45 972003-04 157.48 123.5 1102007-08 198 168 150

*Small or atomistic producers are typically characterized by their lack in influencing either the industry supply or price and take these variables as given.

Fig 1 : Capacity and Production of Cement

0

50

100

150

200

250

1991-92 1995-96 1999-00 2003-04 2007-08

(millio

ns o

f to

nn

e)

Installed capacity

Production

Table 1: Growth of Cement Industry in Post-liberalisation Era

D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

2 3D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

2 3

Cover Story - Cement

Fig : 3 Region Wise Growth in Production

Fig 2 : Cement Production ( 2008-09)

All the performance metrics have shown tremendous growth over the period. Installed capacity increased from 63.9 MT to 193.8 MT by 2007-08, showing a CAGR of 7.3%. Production over the same period increase from 48.76 MT to 168.3 MT, showing a CAGR of 8.1%. Per capita consumption as a result increased from 56 kg to 150 kg, showing a CAGR of 6.3%. Figure 1 makes the things further clear. It reflects the con-sistency that the Indian cement industry has shown in the post liberalised era in terms of growth in both installed ca-pacity as well as production.

Current ScenarioAtmosphere in cement industry was very bullish till the first half of FY09. Riding on the real estate boom and infra-structural investment, the industry showed sharp growth in the proceeding 4-5 years. However, as the global finan-cial crisis and resulting downturn took the centre stage in affairs of economy, cement industry witnessed consider-able slowdown. Apprehensions of demand supply going forward too have come into light as the GDP growth slows down to a six year low. December quarter witnessed con-siderable slump in demand as well as prices. Nevertheless, in wake of the stimulus packages launched by the government and increased public expenditure to boost the slowing economy in the first few months of 2009, the industry has turned around the slowdown blues spec-tacularly. Demand for cement has been bullish throughout the March quarter, which helped the industry keep prices firm and margins high. In the following paragraphs we will trace the developments in the cement industry in the most recent period. 5.1 Demand rides on stimulus packages: Cement demand and production had slowed down towards the end of calendar year 2008. However, riding on the stimu-lus packages launched by the government and intensified public investment in infrastructural sector, cement demand recovered in early months of 2009. As a result, production during March 2009 stood at 18.10 MT, registering a growth of 10.43% as compared to 16.39 MT in the same month last year. Cement despatches, too, showed buoyancy and posted a growth of 10.35% at 18.12 MT against 16.42 MT last year.

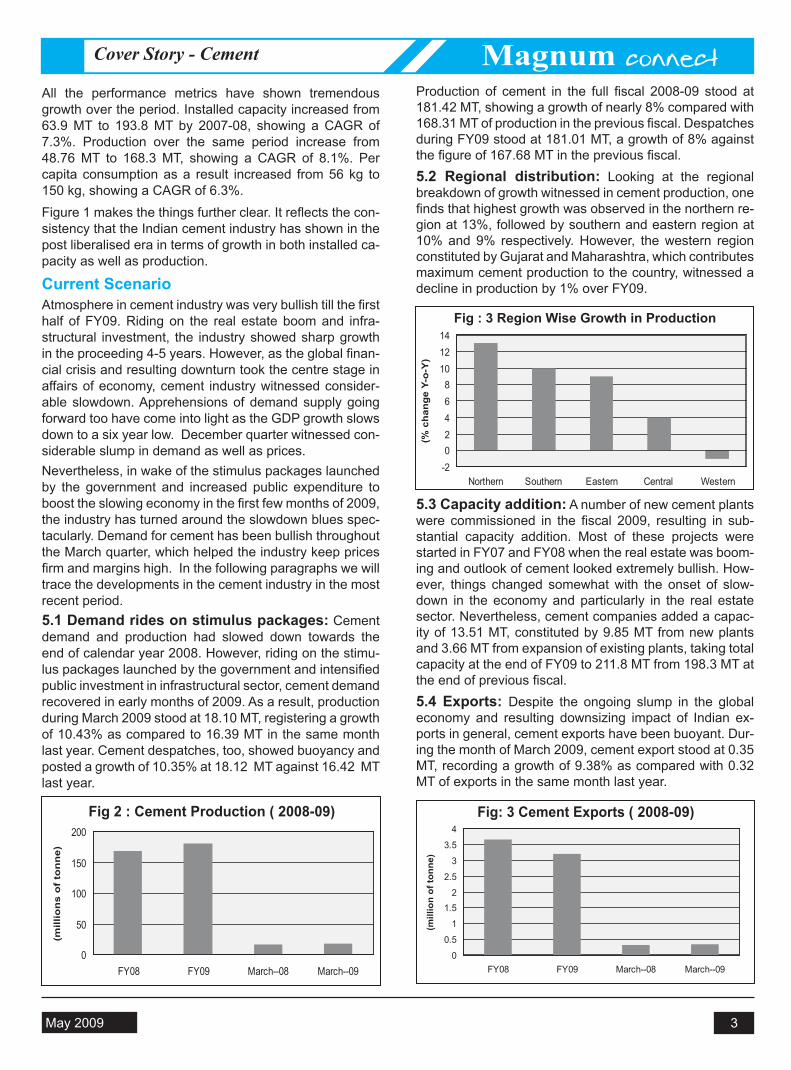

Production of cement in the full fiscal 2008-09 stood at 181.42 MT, showing a growth of nearly 8% compared with 168.31 MT of production in the previous fiscal. Despatches during FY09 stood at 181.01 MT, a growth of 8% against the figure of 167.68 MT in the previous fiscal. 5.2 Regional distribution: Looking at the regional breakdown of growth witnessed in cement production, one finds that highest growth was observed in the northern re-gion at 13%, followed by southern and eastern region at 10% and 9% respectively. However, the western region constituted by Gujarat and Maharashtra, which contributes maximum cement production to the country, witnessed a decline in production by 1% over FY09.

5.3 Capacity addition: A number of new cement plants were commissioned in the fiscal 2009, resulting in sub-stantial capacity addition. Most of these projects were started in FY07 and FY08 when the real estate was boom-ing and outlook of cement looked extremely bullish. How-ever, things changed somewhat with the onset of slow-down in the economy and particularly in the real estate sector. Nevertheless, cement companies added a capac-ity of 13.51 MT, constituted by 9.85 MT from new plants and 3.66 MT from expansion of existing plants, taking total capacity at the end of FY09 to 211.8 MT from 198.3 MT at the end of previous fiscal. 5.4 Exports: Despite the ongoing slump in the global economy and resulting downsizing impact of Indian ex-ports in general, cement exports have been buoyant. Dur-ing the month of March 2009, cement export stood at 0.35 MT, recording a growth of 9.38% as compared with 0.32 MT of exports in the same month last year.

Fig: 3 Cement Exports ( 2008-09)

0

50

100

150

200

FY08 FY09 March--08 March--09

(mill

ion

s o

f to

nn

e)

-202468

101214

Northern Southern Eastern Central Western

(% c

hang

e Y-

o-Y

)

0

0.5

1

1.52

2.5

3

3.5

4

FY08 FY09 March--08 March--09

(mill

ion

of to

nne)

D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

4 5D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

4 5

Cover Story - Cement

Total exports during the fiscal 2009 however have shown de-growth of 12.3%. India exported a total of 3.20 MT of cement in FY09 compared with 3.65 MT of cement export-ed in the previous fiscal. The decline primarily shows the impact of subdued exports in the first half of fiscal when commodity prices were soaring in India, local demand was surging.

5.5 Capacity utilisation shoots up in March: Buoy-ant cement demand during last few months, riding on higher demand from the infrastructure sector has pushed up capacity utilisation from poor levels witnessed towards end of calendar year 2008.

Further, increase in demand in March resulted in excep-tional rise in capacity utilisation to 103% from 92% in the month of February. Capacity utilisation in the full fiscal; however, has been lower at 88% compared with 94% in the previous fiscal, reflecting the impact of slowdown in cement industry during last quarter of 2008.

Outlook: After facing slowdown in last quarter of 2008, the cement industry has been performing very well in the first quarter of 2009. While demand from the real estate sector contin-ues to remain poor due to the ongoing severe downturn in the property market, increased investment in infrastruc-ture sector by the government has boosted the demand for cement from this segment.

As a result, there has been robust growth in both produc-tion and dispatches in the January-March quarter. Cement prices, which were facing a lot of downside pressure to-wards the end of 2008, have also stabilised in 2009, due to buoyant demand.

The country has witnessed cement dispatch growth of 9.98% at 18.06 million tonne (MT) during March this year, as against 16.42 MT during the corresponding month last year, according to Cement Manufacturers’ Associa-tion (CMA).The report says the total cement production in the country during March 2009 was 18.04 MT, up 10.06% over the figure of 16.39 MT reported during March 2008. The annual cement dispatch for fiscal 2008-09 posted a growth of 7.91% at 180.95 MT, compared to 167.68 MT

during 2007-08.

However, the upturn witnessed in the March quarter is rid-ing primarily in stimulus packages provided by the govern-ment and intensifying of public construction works in wake of the general elections. While the new government, which will take the office in June 2009 is expected to continue with measures to boost the economy, investment in the construction sector will come down from its exceptionally intense levels witnessed in January-March quarter.

As a result, the medium term prospects of cement do not look very strong at present. Demand supply mismatch, which was expected to hit the sector in early 2009, has only been delayed and as the demand softens in third quarter of current calendar, there may be significant over capacity, resulting in falling of capacity utilisation and hence margins.

The net effect of such demand-supply gap, however, will depend on nature and quantum of stimulus launched by the next government. Nevertheless, we expect the consump-tion growth in FY10 to slowdown by about 100-150 basis points compared with average of previous few years.

Talking of long term prospects with a time horizon of say more than couple of years, the cement industry possess-es excellent potential of returning to the high growth path witnessed over 4-5 years till FY09. Potential in growth of cement consumption is well reflected in the fact that even after recording around CAGR of 10% for last five years, per capita consumption of about 150 kg in India remains much below the world average of over 260 kg and more than 450 kg in China.

Further, as the global economy recovers and India moves back to growth rates of 8-9%, infrastructure investment too will grow at a rate in excess of 7-8%, thus providing ample scope of growth for the cement industry for many, many years to come. We may conclude the study by ob-serving that the cement industry has been one of the fast-est growing sectors in the liberalised history of India. Even though some doubts have been cast on the near term performance of the industry due the ongoing slowdown in global economy and its resulting downsizing impact on Indian economy, long run prospects of cement remains extremely healthy.

Capacity utilisation

80

85

90

95

100

105

FY08 FY09 March--08 March--09

(%)

D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

4 5D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

4 5

Company Research

UltraTech Cement SellUltraTech Cement was incorporated on August 24, 2000 as L&T Cement. Now, a $28 billion Aditya Birla Group company, it is the country’s largest exporter of cement clinker. The Aditya Birla Group that operates in 25 countries across the world is the 11th largest cement producer globally, the seventh largest in Asia and the second largest in India.UltraTech Cement has an annual capacity of 18.2 million tonnes. It manufactures and markets ordinary portland cement, portland blast furnace slag cement and portland pozzalana cement. It also manufactures ready mix concrete (RMC). The company has five integrated plants,

Stock Data (as on 29/04/09)

Current Mkt Price (Rs.) 567.60

52 week High (Rs.) 785

52 week low (Rs.) 250

Mkt Cap (Rs. Cr.) 7065.81

Return in last one Month (%) 6.93

Share Holding Pattern(as on Dec31,08) %

Total Promoter 54.78

Institutions 11.19

Non Institutions 33.88

Depository Receipt 0.15

Key Ratios

P/E 7.23

Price/Book(x) 3.60

Dividend Yield (%) 0.88

ROCE(%) 35.67

ROE(%) 37.37

Performance in the last year

six grinding units and three terminals – two in India and one in Sri Lanka.

ManagementThe management of the company is led by Kumar Mangalam Birla-Chairman, K C Birla is the Executive President & CFO, while other directors include Rajashree Birla, R C Bhargava, G M Dave, Y M Deosthalee, N J Jhaveri and few others. S Misra is the Managing Director of the company.

Business OverviewUltraTech Cement is the country’s largest exporter of cement clinker. The export markets span countries around the Indian Ocean, Africa, Europe and the Middle East. Individually it is the second biggest cement producer of the country, while together with Grasim it is the largest cement producer in India.The company’s products include ordinary portland cement, portland pozzolana cement and portland blast furnace slag cementThe company ensures a flawless operation in every stage, right from selecting raw materials to batching and mixing, transportation, placing of concrete till testing of concrete, putting together the right ingredients for perfect world class cement. The composite plants of the company are located at Tadipatri (Andhra Pradesh), Hirmi (Chhattisgarh), Jafrabad (Gujarat), Kovaya (Gujarat) and Awarpur (Maharashtra). The grinding units of the company are located at Magdalla (Gujarat), Ginigera (Karnataka), Ratnagiri (Maharashtra), Jharsuguda (Orissa), Arakkonam (Tamil Nadu) and Durgapur (West Bengal)

Investment Rationale The transport of concrete from its place of mixing to the delivery point is very critical, as there is possibility of the concrete drying out and losing its workability and plasticity. The company has got an edge on this point as the UltraTech Concrete transports concrete from its ready mix

0.00

100.00

200.00

300.00

400.00

500.00

600.00

700.00

800.00

30-Ap

r-08

30-M

ay-08

30-Ju

n-08

30-Ju

l-08

30-Au

g-08

30-Se

p-08

30-O

ct-08

30-No

v-08

30-De

c-08

30-Ja

n-09

28-Fe

b-09

30-M

ar-09

Date

Price

D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

6 7D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

6 7

Particulars March Qtr-09 March Qtr-08 Growth % FY08 FY07 Growth%Net Sales 1875.01 1601.66 17.07 6436.96 5508.78 16.85Total Income 1888.86 1628.69 15.97 6486.64 5609.07 15.64Other Income 13.85 27.03 -48.76 49.68 100.72 -50.68PBT 437.18 431.19 1.39 1361.46 1507.01 -9.66PAT 309.46 282.88 9.40 977.02 1007.61 -3.04OPM 29.96 27.56 -- 28.12 33.03 --NPM 16.50 14.56 -- 15.18 18.29 --EPS 24.86 45.40 -- 78.48 80.91 --

Company Research

concrete plants to the site through transit mixers. Further, the concrete is pumped to the actual point of concreting using high efficiency concrete pumps, Placing the concrete is expedited scientifically by specialised delivery trucks. Qualified and experienced engineers monitor the entire operation. UltraTech Concrete is equipped with computerised batching and mixing plants to strictly monitor the quality of the concrete. It uses a computerised recipe for the raw mix design and quantities of raw materials are weighed automatically as per the design mix.There has been a good appreciation in the cement dispatch figures for March keeping with growth trend seen in February, January, December and November. Industry observers expect the trend to continue in this quarter.

Latest result analysis F The company has posted a decline of 3.01% in its

consolidated net profit for the financial year ended March 31 at Rs 979.62 crore as compared to Rs 1,010.05 crore in the previous financial year.

F Net sales of the company during the year increased by 17.69% to Rs 6618.32 crore from Rs 5623.38 crore last year.

F The earning per share stood at Rs 78.57 against Rs 81.14 last year.

F The company reported a rise in its net profit after two consecutive quarters of decline.

F The net profit for the March quarter moved up by 9.39% to Rs 309.46 crore compared with Rs 282.88 crore in same quarter last year.

F Net sales during the three-month period improved by 17.06% to Rs 1,875.01 crore from Rs 1,601.66 crore in last year.

F The company reported a 230 basis points fall in operating margins at 29.2% in the fourth quarter.

F High input costs offset the company’s estimated 8.1% rise in cement realisations to Rs 4,166 per tonne in the fourth quarter of FY09.

INDUSTRY SCENARIOIndia is the world’s second largest producer of cement after China with industry capacity of over 200 million tonnes.

The Indian cement industry comprises of 134 large cement plants with an installed capacity of 173.08 million tonnes and more than 350 operating mini-cement plants across the country.Cement demand has a direct correlation with the GDP growth and had registered a growth of nearly 9% between FY06-FY08 driven primarily by strong demand from construction, infrastructure and real estate projects.

Latest developments Defending champions of IPL, Rajasthan Royals has signed a sponsorship deal with Ultratech Cement.Buoyed by improved demand, the Aditya Birla Group companies, Grasim Industries and UltraTech Cement, have recently raised prices by Rs 5-7 per bag.The Aditya Birla Group’s cement production for the period April-February 2009 has moved up by 5.23% at 290.09 lakh mt as against 275.67 lakh mt during April-February 2008. Dispatches grew by 5.25% at 289.71 lakh mt in April-February 2009 vis-a-vis 275.24 lakh mt in the corresponding period last year.

Recommendation FactorsIn its outlook, the company has said that a slow down in economic growth will aggravate the inevitable surplus in production capacity. The expected commissioning of an additional 50 million tonnes in FY10 and a further 15 million tonnes in the following year is likely to result in a reduction in capacity utilisation with adverse impact on margins.Additionally, the likely release of around 100 million tonnes capacity in a phased manner over the next two years coincides with slower economic growth. This will put pressure on sales realisation and margins in FY10.Volume increase to come up from commissioning of new capacities Cement prices currently ruling firm but likely to witness decline from Q1FY10.At current market price of Rs 569 (as on April 22, 2009), the stock is trading at a P/E of 7.3x and EV/EBITDA of 4.8x. We recommend a SELL on the stock as by the end of 2009-10 cement prices could start trending down as more capacity is commissioned and as new and smaller players look to establish themselves

(Rs. Cr.)

Standalone

D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

6 7D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

6 7

Stock Update

F ACC has posted Q4 pre-exceptional net profit at Rs4.08 bn owing to lower expenditure and lower power and fuel cost. Revenue for the quarter surged 14.4% to Rs20.5bn, mainly driven by 6.1% improvement in cement volumes (5.73mnt) and 7.9% increase in realizations to Rs3,587 per ton. It had a pre-exceptional EBIDTA for the quarter has spiked up 33.4% year-on-Year (y-o-y) basis to Rs6.28bn, while EBIDTA margins increased by 433 bps y-o-y to 30.5%,mainly on account of lower other expense.

F It has witnessed a reduction in power & fuel cost by 13.7% on quarter-on-quarter (Q-o-Q) basis on drop in international coal prices. ACC capacity expansion at Bargarh for 1.18 mtpa together with a 30 MW captive power plant is expected to be completed by mid CY2009.

F ACC remained firmed to keep its total cost per ton of cement to Rs2491, which is a meager 1.5% y-o-y increase thus clearly reflecting significant cost savings during the quarter. Further, the company continued to benefit on account of strong dispatch numbers and higher realizations on account of increase in cement prices on a pan India basis.

F Trading at a PE multiple of 10.1, the stock has an upside potential of 12% upsurges in near term, translating to the level of Rs 695-700. It is expected that ACC revenue to grow by a CAGR of 9.7% due to high fixed cost and low EBITDA per tonne, ACC’s earnings are highly sensitive to cement prices. It has been observed that for every 1% decline in cement prices, the EPS of the company reduces by 7.4%.

Last Traded Price (as on 29/04/09) Rs. 653.00

Price target Rs 695Market cap. in Rs cr. 12082.2152 Week H/L 790/369Free Float 53.79%BSE code 500410

ACC : Buy

F Shree Cements has reported Q4 FY09 net profit of Rs 235.6 crore from Rs 41 crore year-on-year. The company’s net sales spiked to Rs 806.2 crore as against Rs 662.5 crore YoY. Realization per bag is Rs 1 lower than last year’s overall realization. Volume growth is 28%. So, the realization is not per tonne, but the overall turnover is also higher by 28%. The cement prices have increased across the board and the rise has been undertaken on bagged cement.

F Excise duty relief has been given on the bulk cement and but the price increase is on the pack cement and in the pack cement no excise benefit has come. The price increase has been there on the retail sector. This maybe because of multiple things but the sector where the prices have not really increased, is the bulk cement, which is hardly 10% of the total production of the company.

F Due to the higher spending by the government in infrastructure projects, north India has successively posted a higher volume growth rate in the last quarter, compared to other regions and Shree Cement is expected to be the main beneficiary, as it has a strong presence in north India and also due to its relatively early expansion. On the back of strong demand, Shree Cement has raised cement prices by Rs4 to Rs6 per bag in the past couple of months (February-March).

F At the current market price of Rs776, the stock trades at 5.3 multiple and 8.8 multiple its FY2009 and FY2010 earnings estimate respectively, an enterprise value (EV)/earnings before interest, depreciation, tax and amortisation (EBIDTA) of 3.2x FY2010 and EV/tonne of $63 on expanded capacities of 10.1 million tonne. The stock has appreciated by over 45% since our last update on January 30, 2009. We maintain our Buy call on the stock with a revised 12-month price target of Rs825 (EV/tonne of $70 on expanded capacity).

Last Traded Price (as on 29/04/09) Rs. 776.00

Price target Rs 815Market cap. in Rs cr. 2702.8552 Week H/L 1045/330Free Float 53.79BSE code 500387

Shree Cements: Buy

PromoterInstNon Instt.

PromoterInst.Non InsttPublic

.

65.41%13.39%

10.13%

11.07%

46.21%

32.61%

21.18%

D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

8 9D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

8 9

Corporate News

GMR Group to exit non-core businesses The GMR Group, which has a strong presence in the infrastructure sector and has completed upgrading of domestic and international airports, is looking at exiting non-core business. The group has taken the decision in the wake of an overall cash crunch that has impacted infra projects in the country.The group has already hived off its ferro alloys business to Dubai-based Cronimet Mercon Invest for a consideration of around Rs 22 crore last year. It is currently in the process of offloading 30% stake in its sugar business to multinational Bunge, and plans to exit the sugar business in due time.The GMR Group has interests in agri business, ferro alloys, IPL, infrastructure and SEZ. Sahara takes Jet to court over non-payment of dues The Sahara Group, promoter of Air Sahara, which was acquired by Jet Airways in 2007, has taken the latter to court over default of dues worth Rs 1,450 crore that was part of the buyout deal.As per the deal, Jet was to pay Rs 900 crore to Sahara upfront, while Rs 137.5 crore was to be paid in yearly instalments over four years. Jet has reportedly defaulted on the annual instalments. Jet’s payout to Sahara in a single year’s default could be in the range of Rs 550 crore.Larsen & Toubro bags orders worth Rs 1100 crore in Q4 Turnkey engineering major Larsen & Toubro (L&T) has bagged a slew of large-value orders aggregating Rs 1100 crore in the electrical construction sector in the fourth quarter of 2008-09. The orders have come from leading public sector organizations like Power Grid Corporation of India (PGCIL) and the Rail Vikas Nigam and involve setting up high end transmission lines and substations as well as a project for the Indian Railways.RCom gets TDSAT nod for use of dual technology The Telecom Disputes Settlement and Appellate Tribunal (TDSAT), while hearing a petition filed by the Cellular Operators Association of India (COAI) that challenged the government’s decision to allow Reliance Communications to use dual technology (GSM and CDMA) for mobile services, cleared the latter’s use of dual technology.Criticising the COAI, the tribunal stated that GSM operators were not eligible for spectrum beyond 6.2 MHz. TDSAT also flayed the Telecom Regulatory Authority of India (TRAI) for mooting subscriber-linked criteria for allocating additional spectrum, which it claimed was not transparent.NMDC identifies potential partners for new coal blocks National Mineral Development Corporation (NMDC) has identified four prospective partners for developing new

coal blocks in India. The potential partners include Adani Power, KSK Power, Monnet Ispat and Sophia Power.NMDC had recently invited expression of interest’s (EoI) to develop the coal blocks jointly in the country. However, the company has not yet decided to take in multiple or single partners for the proposed joint venture. This depends on the allotment of fresh coal blocks.RIL begins gas production at KG-D6 block The Mukesh Ambani-led Reliance Industries (RIL) is reported to have started gas production at its Krishna-Godavari basin field creating a landmark in the history of oil and gas production in the country.The gas generated from the KG-D6 block is expected to boost the power supply from electricity generators starved of fuel and produce cheaper urea for agriculture.BHEL plans JV with foreign firm for Rs 1,200 cr Bharat Heavy Electricals (BHEL) is planning to invest around Rs 1,200 crore to form a joint venture with an international firm for manufacturing transmission equipment by June 2009.The company is currently in talks with a French equipment maker Areva and a Japan based Toshiba for forming a transmission joint venture by June 2009. The joint venture will manufacture transmission equipments having a capacity of 765 kilo volt (KV) and 1,200 KV.L&T to exit from infrastructure projects with minority stake Larsen & Toubro (L&T) is planning to exit from those infrastructure projects in which it holds minority stake (less than 50%). However, the company might bid in a consortium and take less than a 50% stake to diversify the risk in large and complex projects like urban metro.Bajaj Auto gets patent for its ExhausTEC technology Bajaj Auto has finally received a patent for its ‘ExhausTEC’ invention vide Patent No 231498 dated March 5, 2009 from the Indian Patent Office. The Pune-based company was involved in a controversy with TVS Motors as the two companies had clashed on issues related to technology infringement in 2007 when TVS developed the 125cc Flame using a technology similar to that of Bajaj.Videocon to mop up Rs 200 cr though preferential issue Videocon Industries has chalked out a plan to mop up Rs 200 crore through a preferential issue. The company’s has approved the issue of 1,17,65,000 crore warrants to Bennett, Coleman & Company (BCCL), which would be converted into equal number of equity shares, at a price of Rs 170 a piece.Upon conversion, BCCL’s holding in Videocon would rise to 6.13%. As on December 31, 2008 the former held 1.01% in Videocon, as per BSE data.

D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

8 9D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

8 9

Corporate News

Shareholders, creditors approve RIL-RPL merger The Mukesh Ambani-led Reliance Industries (RIL) has announced that the shareholders and the creditors of the company have approved the Scheme of Amalgamation of Reliance Petroleum (RPL) with RIL. Equity shareholders and secured and unsecured creditors of RIL took part in the meeting held on Saturday, April 4, 2009 and voted on the proposal. As per the media release by the company, 98.86% of the shareholders present in person/proxies, representing 99.9998% of the total value of the equity shares held by them, voted in favour of the Scheme of Amalgamation.Govt to finance Tata Motors’ Myanmar foray The government, which had signed an agreement with Myanmar offering the neighbouring country a $20 million line of credit, will finance Tata Motors’ plan of setting up a facility to assemble Tata Heavy Trucks in that country.The auto major is in the process of garnering a proper understanding of the project scope. The proposed plant will have an initial capacity of 1,500 trucks per year, with a provision for increasing the capacity as demand picks up.Govt appoints former AAI chief Ramalingam as Maytas Infra chairman The ministry of corporate affairs, on April 9, announced the appointment of K Ramalingam as the chairman of Maytas Infra, the company owned by the family of B Ramalinga Raju – the founder of the fraud-ridden Satyam Computer Services. Ramalingam is the former chief of the Airports Authority of India (AAI).The Centre has also appointed Anil K Agarwal on the board of Maytas Infra.Last month the Company Law Board had appointed noted tax lawyer O P Vaish and past president of Institute of Chartered Accountants of India Ved Jain on the board of Maytas Infra.Infosys Technologies reports 28.5% rise in consolidated profit IT services major Infosys Technologies, in its consolidated results for the year ended March 31, 2009, has posted a net profit after tax & minority interest rise of 28.52% to Rs 5,988 crore for the year ended March 31, 2009 as compared to Rs 4,659 crore in previous fiscal.Total income of the group has increased by 27.42% to Rs 22,166 crore from Rs 17,396 crore in the previous year.Infosys Technologies has also given a guidance for fiscal 2010, the revenues of the company is expected to grow by 1.7% to 5.7%; to decline by 6.7% to 3.1% in US dollar terms. Kingfisher again misses deadline to payback dues to IOC; seeks 10 days extension Kingfisher Airlines has missed deadlines of March 31 and April 10 to payback the dues to state-run Indian Oil Corporation (IOC) for jet fuel supplied by the refiner. The

airline has now sought a second extension of 10 days to settle the dues.The airline owes around Rs 1,000 crore to oil marketing companies like Hindustan Petroleum Corp (HPCL) and Bharat Petroleum Corp (BPCL) along with IOC. It has to settle dues amounting Rs 90 crore to IOC.L&T expects a 25-35% growth in order inflows for FY 2009-10 Larsen & Toubro (L&T) has come up with a strong order inflow outlook for 2009-10. The company recorded a healthy growth in order inflows during the fiscal 2008-09 and has bagged a number of prestigious orders, both domestic and international, from diverse sectors totalling approximately Rs 52,000 crore as compared to Rs 42,000 crore in the previous year.Wockhardt will finally sell minority stake in Wockhardt Hospitals The Wockhardt Group has finally decided to sell its minority stake in Wockhardt Hospitals, the hospital chain of the group, to reduce its debt burden of around Rs 3,700 crore.SBI to provide Rs 10,000 crore loan to Vodafone-Essar for 3G services State Bank of India (SBI) has decided to provide a loan of Rs 10,000 crore to Vodafone-Essar for financing the company’s foray into third generation (3G) telecom services, expansion of its broadband operations and various other business purposes. It will be a five-year loan carrying an interest rate of 13.25% for the first 2 years. Subsequently, the rate will be re-adjusted on the basis of the average prime lending rate of four public sector banks.Tech Mahindra completes the fund raising process for Satyam acquisition The new owner of scandal hit IT Company Satyam, Venturbay Consultants, a subsidiary of Tech Mahindra has informed that it has deposited Rs 2,910 crore in the escrow account. Venturbay is set to acquire total 51% stake in Satyam. It has raised the funds through non convertible debentures, commercial papers and borrowing from non-banking financial companies as well as partial funding from a special purpose vehicle and Rs 700 crore is raised internally.Tech Mahindra had agreed to buy Satyam for Rs 58 per share on April 13, 2009.GAIL among the 12 shortlisted for Nigeria gas field GAIL India has been shortlisted as prospective investors in Nigeria’s vast gas field. Besides GAIL, 11 foreign companies have also been short listed.The list of potential investors includes Russia’s Gazprom Oil and Gas, Germany’s E.ON Ruhrgas AG, UK based BG Group and Centrica Energy, Spain’s Gas Natural SDG SA and Union Fenosa and GAIL India.

D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

10 11D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

10 11

Indian equities markets ended on a positive note for the second consecutive month on the back of on the back of supportive global cues and continued buying interest shown by foreign institutional investors. This sudden ar-rival of foreign funds was perhaps a key reason for the strong rally witnessed by the local markets in the month. One thing evident was that there has been a considerable decrease of risk aversion, which was seen since last year. A fair amount of risk taking appetite was observed across all sections of investors.Indian markets also took heart as the world leaders reaching a $1.1-trillion deal to embark upon the global economic crisis at the G-20 summit added to optimism that the worst might be over for the world economy. Stock specific action was ob-served in the markets on account of announcement of profit numbers for the quarter and year ended March 2009.Though the benchmarks finally finished the month with positive gains, volatility did exist in the markets as inves-tors were seen booking profits after a rally in the past couple of weeks. Interestingly, there has been a sort of disconnect between the rally in the equities markets seen since past eight weeks and the continuing barrage of pes-simistic economic forecasts. Stock markets across the globe have seen an upmove, while the economic data shows that most economies continue to contract. Retail investors were seen cautious before making moves as they were aware that a sudden plunge in markets could be seen if the outcome of the general elections turns out to be something unexpected.Sensing a great opportunity from strong global cues, trad-ing on the local bourses have extended their gains fur-ther and substantiated by heavy buying in interest rate sensitive sectors like realty and banking in the mid of the month.

Domestic markets also took negative connotations amid rising uncertainties and gauged inflation figures adversely as heavy selling was witnessed in metal, realty, capital goods and power counters. Selling pressure was evident from dumping shares in hurry as the benchmark indices along with midcaps and smallcaps counters have taken a backseat and tweaked in tandem.The 30-share Bombay Stock Exchange’s (BSE) Sensex gained 1,694.75 points or 17.46% to 11,403.25, while the broader S&P CNX Nifty added 453 points or 15% to 3473.95 in the month of April 2009. Similarly, the BSE Mid-cap index surged 557.63 points or 18.86% to 3,513.86 and the BSE Small-cap index rose 694.27 points or 21.38% to 3,940.90.All sectoral indices on the BSE ended on a positive note in the month. Realty up 36.49%, Bankex up 26.59%, Capital Goods (CG) up 22.31%, Metal up 18.82% and TECk up 17.12% were the main gainers.Top gainers on the Sensex during the during the period be-tween March 31, 2009 and April 29, 2009 were Jaiprakash Associates 76.82%, ICICI Bank up 41.37%, Tata Motors up 40.66%, DLF up 39.47% and Rel Infra up 38.36%.Jaiprakash Associates has announced its result for the quarter and year ended March 31, 2009. The unaudited result for the quarter shows a net profit surge of 83% to Rs 385.32 crore against Rs 210.41 crore on Year on Year (YoY) basis. The total income stood at Rs 2,194.57 crore against Rs 1,345.28 crore showing a jump of 63% on YoY basis.ICICI Bank responded positively to the Reserve Bank of India’s (RBI) measure of reducing the benchmark repo and reverse repo rates by 25 basis points (bps). The bank has slashed its prime lending rate (PLR) by 50 bps to 16.25% effective April 22, 2009 and has also decided to reduce the deposit rates across various maturities by 25 to 50 bps, which will be applicable from April 24, 2009.On the other hand, Hindustan Unilever, down 2.03%, was the sole loser on the Sensex during the said period.For the third time with in two months, state-run oil market-ing companies (OMCs) on Wednesday raised prices of jet fuel, or ATF, this time by about 6.7%, in line with rising international rates. Indian Oil Corporation, Bharat Petroleum and Hindustan Petroleum hiked ATF prices by 10% on April 1 after a mar-ginal Rs 158 per kl increase two weeks earlier. ATF in Del-hi will now cost Rs 31,926 per kilo litre (kl) from April 16, as against Rs 29,925.97 per kl earlier. In Mumbai, ATF rates rose to Rs 32,855 per kl from Rs 30,784.81 per kl.The earnings and growth of the pharmaceutical sector is likely to take a hit in the last quarter of the just-concluded fiscal, as compared to the previous three quarters and is expected to be an underperformer during the fourth quar-ter of FY09.

Stocks in limelight on BSE Mid-cap index in AprilChange (%)

Jai Corp 115.99Anant Raj Inds 105.98BF Utilities 93.18HDIL 87.24Puravankara Projects 74.38

Sensex movement during April 2009

90009500

1000010500110001150012000

1-A

pr-0

9

2-A

pr-0

9

6-A

pr-0

9

8-A

pr-0

9

9-A

pr-0

9

13-A

pr-0

9

15-A

pr-0

9

16-A

pr-0

9

17-A

pr-0

9

20-A

pr-0

9

21-A

pr-0

9

22-A

pr-0

9

23-A

pr-0

9

24-A

pr-0

9

27-A

pr-0

9

28-A

pr-0

9

29-A

pr-0

9

Market Snapshot

D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

10 11D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

10 11

Market Snapshot

After the Reserve Bank of India (RBI) gave permission to domestic companies to buy back foreign currency con-vertible bonds (FCCBs) in December 2008, a dozen com-panies reacted in hurry to redeem such bonds worth $340 million at deep discounts to the conversion price in the melted markets, giving them a room for windfall gains.On one hand, buying back FCCBs companies pay off a loan at a discount, on the other hand they also earn a substantial windfall gain. To top it up, the deferment of AS11 mandate has relieved them from carrying the mark-to-market (MTM) losses for the redeemed FCCBs. Buying back FCCBs helps the domestic companies bring-ing down the liabilities on the company’s books as well as MTM losses provided for against the FCCBs. Hence, companies redeeming FCCBs are likely to gain from the practice and it will help them posting better results in the fourth quarter of the fiscal.As mentioned earlier, key reason of markets moving up at surprising speed in the month is that foreign institu-tional investors (FIIs) have been coming back in droves. The month saw of April saw a strong buying activity from FIIs, wherein the gross purchase of equities stood at Rs 38,871.55 crore against gross sales Rs 33,311.43 crore. As a result the FIIs emerged as net buyers of equities worth Rs 5,560.12 crore in the month.The world economy showed some mixed signals over last one month. There were good developments in US and China, suggesting the economy may be bottoming-out.

Close as on March 31 Close as on April 29 Change (points) Change (%)Sensex 9,708.50 11,403.25 1,694.75 17.46Nifty 3020.95 3473.95 453.00 15.00Mid-cap 2,956.23 3,513.86 557.63 18.86Small-cap 3,246.63 3,940.90 694.27 21.38

However, the good news was immediately followed by more bad news, raising serious doubts about any chances of an early recover. Adding to the woes of the policymakers, the country’s In-dex of Industrial Production (IIP) has again slipped in the negative zone to touch -1.2% vs 9.5% on a year-on-year (Y-o-Y) basis. February consumer durable goods also witnessed a negative growth at 3% as against 11.7% on Y-o-Y basis. The capital goods index, however, showed signs of strength posting a growth of 10.40% vs 10.70% on Y-o-Y basis, which is looking sustainable as the indus-try has a robust order book.India’s banking regulator Reserve Bank of India (RBI) has lowered its growth forecast for the current fiscal to 5.7%, down from 6% forecast of expansion that the bank had made three months ago.The RBI announced annual review of its monetary policy on April 21, 2009. The review came in back drop of sharp slowdown in economic activity in India, in line with the global economy suffering from severe slowdown. The bank cut the repo and reverse repo rates by 25 basis points (bps) each, primarily as a means to give signal to the markets that the apex bank will continue the aggres-sive stance it has taken since September last year to pro-tect growth and stimulating the slowing Indian economy. New repo and reverse repo rates will be 4.75% and 3.25% respectively. The bank however left the cash reserve ratio (CRR) unchanged at 5%.

Indices Close as on March 31 Close as on April 29 Change (points) Change (%)FMCG 2,036.24 2,095.00 58.76 2.89CD 1,625.45 1,757.58 132.13 8.13HC 2,830.11 3,067.98 237.87 8.40PSU 5,230.17 5,863.56 633.39 12.11Auto 3,061.67 3,498.24 436.57 14.26Power 1,847.10 2,112.76 265.66 14.38Oil & Gas 7,053.04 8,132.62 1,079.58 15.31IT 2,285.68 2,663.35 377.67 16.52TECk 1,846.83 2,163.00 316.17 17.12Metal 5,795.07 6,885.81 1,090.74 18.82CG 6,466.03 7,908.75 1,442.72 22.31Bankex 4,490.97 5,685.22 1,194.25 26.59Realty 1,560.83 2,130.41 569.58 36.49

D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

12 13D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

12 13

Quick Review of Economy

Monetary Policy India’s central bank Reserve Bank of India (RBI) announced the annual review of its monetary policy on April 21. The review came in the backdrop of a sharp slowdown in economic activity in India, in line with the global economy suffering from a severe slowdown. The Indian economy has slowed down to a six-year low with the quarterly expansion coming down to 5.3% for three months ending December 2008. In this wake, RBI was under a lot of pressure to take some further stimulus measures in its annual review, even if these come as a token of general stance. Before reviewing the monetary policy, it will be good to recall the conduct of monetary policy by the RBI since September 2008, when the US sub-prime problem officially turned into a global financial crisis impacting the world as well as the Indian economy. The fall of Lehmann Brothers resulted in freezing of global financial markets in the month of September last year. While Indian banks were not affected by the problem of toxic assets, the global deleveraging and resulting outflow of capital and frozen international markets resulted in acute cash crunch in Indian markets, too, forcing the RBI to loosen its monetary policy. Since September till the eve of annual review, the RBI had already cut the repo, the rate at which it infuses the short-term liquidity into markets and reverse repo, the rate at which it absorbs the excess liquidity from markets, by 400 and 250 basis points (bps) respectively. The bank had also cut the cash reserve ratio (CRR) by 400 basis points from 9% of net demand and time liabilities (NDTL) of banks to 5%. Together with CRR cut, increase in export credit refinance, special refinance Facility for banks and NBFCs etc, RBI had infused a total liquidity of Rs. 4,22,793 crore. As such, at the time release of monetary policy annual review the bank had already taken significant measures to keep the liquidity situation comfortable.

Annual Review for 2009-10The main thrust of the RBI’s policy was to ensure a policy regime that will enable credit expansion while preserving credit quality so as to support the return of the economy to a high growth path as well as preserve the price and financial stability of the system in wake of challenges being posed by the global financial crisis and its impact on the Indian economy. As such, the following are the main features of the annual review announced by the RBI on April 21. Major Policy Measures: The RBI cut the repo and reverse repo rates by 25 bps each, primarily as a means to give a signal to the markets that the apex bank will continue the aggressive stance it has taken since September last year to protect growth and stimulating the slowing the Indian economy. New repo and reverse repo rates stand at 4.75% and 3.25% respectively. The bank, however, left

the CRR unchanged at 5%. The bank rate was also left unchanged at 6%.

The special repo facility that the RBI introduced in September last year to provide financing to banks for meeting monetary needs of mutual funds arising out of excessive redemption pressure has been extended to March 31, 2010. The bank will conduct this repo on a weekly basis. The apex bank also extended a special refinance facility that was introduced on November 1, 2008 to provide funding to scheduled commercial banks up to 1% net demand and time liabilities (NDTL) as on October 24, 2008, to March 31, 2010.The RBI has also extended the relaxation on all-in-cost ceilings for external commercial borrowings (ECB) up to December 31, 2009. In view of the ongoing current global turmoil in the financial markets, the RBI has decided to continue, for the time being, with the current policy and procedures governing the presence of foreign banks in India. As per the ‘roadmap for presence of foreign banks in India’ which the apex bank has been following since beginning of FY065, the RBI was expected to review and expand the presence of foreign banks by allowing them to own controlling stakes in private Indian banks and enter into merger and acquisition with the latter. However, the review has been proposed and will be taken up after due consultation with all stakeholders once there is greater clarity regarding the stability of the global financial system and a shared understanding on the regulatory and supervisory architecture around the world.

Repo Rate since 2001

Reverse Repo Rate since 2001

0123456789

10

9/3/

2001

30-0

4-20

017/

6/20

0128

-03-

2002

12/1

1/20

027/

3/20

0319

-03-

2003

31-0

3-20

0426

-10-

2005

24-0

1-20

068/

6/20

0625

-07-

2006

30-1

0-20

0631

-01-

2007

30-0

3-20

0711

/6/2

008

24-0

6-20

0829

-07-

2008

20-1

0-20

083/

11/2

008

8/12

/200

82/

1/20

094/

3/20

0921

-04-

2009

(%)

012345678

2/2

0/20

01

3/2

/200

1

4/2

7/20

01

5/2

8/20

01

3/5

/200

2

6/2

7/20

02

10/

30/2

002

3/3

/200

3

8/2

5/20

03

10/

27/2

004

4/2

9/20

05

10/

26/2

005

1/2

4/20

06

6/8

/200

6

7/2

5/20

06

12/

8/20

08

1/2

/200

9

3/4

/200

9

(%)

D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

12 13D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

12 13

Quick Review of Economy

Monetary Projections: The RBI strongly mentioned its commitment to keep ample liquidity in the system in order the help the cause of growth. The bank observed that the liquidity overhang emanating from the surge in capital inflows witnessed during FY08 had substantially moderated in FY09. Further, the upside risks to inflation had declined substantially. As such, the bank placed money supply (M3) growth target for FY10 at 17.0%. Growth in non-food credit consistent with the monetary expansion has been targeted at 20%. The bank also projected the deposits of scheduled commercial banks to witness growth of 18% over FY10.

Growth Projection: Regarding the growth prospects of the Indian economy, the RBI observed that the fiscal and monetary stimulus measures initiated during 2008-09, coupled with lower commodity prices, could cushion the downturn in the growth momentum during 2009-10 by stabilising domestic economic activity to some extent. Nevertheless, it also added that any upturn in the growth momentum was unlikely in view of the projected contraction in global demand during 2009.

The bank in this wake placed its projection of GDP growth at 6% for the current fiscal. It may be mentioned that the median forecast in the survey of professional forecasts conducted by the RBI stood at 5.7% with respect to growth in FY10.

Government borrowing programme: RBI said in the annual policy review that one of the major challenges facing it was managing government borrowing. It mentioned that total borrowing need of the government during first half of FY10 was currently placed at Rs 2,07,364 crore.

However, the bank also signalled that ultimate supply of new securities into the market will be much less than the borrowing figure and also what was being expected by markets in recent months. The bank mentioned that after adjusting for MSS (market stabilisation scheme) unwinding and the Reserve Bank’s support by way of open market operations, net supply of fresh securities was expected to be of the order of Rs 85,364 crore. Although the fresh supply of securities would be higher than the first half of the last year, it would be of a much lower order as compared with the first half of 2007-08.

Inflation: With regard to inflation, the bank observed that the headline inflation measured by wholesale price index will remain negative during early part of the fiscal. However, RBI clearly said that the negative WPI inflation should not be interpreted as deflation and it had only statistical significance, not to be reflected in demand contraction in any way. RBI also observed that the sharp decline in WPI inflation had not been commensurately matched by a similar decline in inflation expectations, thus suggesting that RBI will have to continue to anchor inflationary expectation in the, particularly in the second

half of FY10. Union Finance: RBI expects the consolidated fiscal deficit of centre and state governments to reach the 9% mark, out of which 3% may be the contribution of states while the fiscal deficit of the Centre is expected around 6%. After including the off-budget and special securities issued by the central government outside the market borrowing programme, the total fiscal deficit may reach about 10.8% of GDP.

AssessmentOverall the credit policy was much in line with the market expectations. While the RBI avoided big ticket changes in policy stance in order to keep greater space with itself to manoeuvre the monetary policy once full budget for FY10 was out after the elections, it nevertheless did provided the signal markets were looking for through the 25 bps cut in both the policy rates. Further, RBI avoided placing any cap on deposits by commercial banks through the reverse repo window, a measure that was in talks among many quarters as means to check the yield on government securities. Such a measure could have proved overly distortionary and therefore it was probably in best interest that the RBI did not consider it. Another important detail in the policy was regarding the market borrowing programme of the government. The policy clearly specified that out of the total government borrowings in the first half of current fiscal, Rs 205,000 crore and Rs 120,000 crore was going to be through Open Market Operation (OMO) and Market Stabilisation Scheme (MSS) respectively, which leaves just Rs 85,000 crore to be raised incrementally through securities. While the announcement was aimed at calming the bond markets, it also reflected the commitment of RBI to keep the bond rates in check. Another important issue in the annual review is with regard to targeted (RBI however calls these indicators and not targets) monetary and credit expansions. The targets have been set at 17% and 20%, respectively, for growth in M3 and credit for FY10 against actual growth of 18.7% and 17.3% in FY09.Over past few years, there has been a wide deviation between targeted rates and the actual growth rates. For instance, target for of money supply expansion was at 14%, 15% and 17-17.5% for FY06, FY07 and FY08, respectively. However, riding on the bullish economy, the actual growth was above 20% in each of these years. Similarly, the growth for bank credit was anticipated around 20% in FY06 and FY07, whereas actual growth in credit was around 30% in both the fiscals. The target growth was revised upwards to 25% in FY09, bank credit grew merely 17%, suggesting the cautious

D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

14 15D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

14 15

behaviour of banks in view of slowing global economy. As such, it appears that monetary expansion has been overshooting or undershooting the RBI’s expectations depending on direction of trade cycle movement. As such, now that the economy is moving downwards, one may expect that the anticipated growth in money supply as well as credit delivery may fall short of targets or indicators set in the annual review. Finally, the bank has kept the economic growth projections and money supply and credit growth targets within reasonable reach. The bank has substantially lowered its growth target from 7% in previous review to 6% in the present one. This step indicates that the bank is keeping its feet on the ground and will approach the growth in a realistic way, which is a positive indication as far as RBI’s efforts to push the growth are concerned. On the whole we may observe that although the annual review might sound at some places a bit more bearish than expected, it nevertheless clearly outlines the fact that the bank will continue the aggressive stance to promote growth, a signal which the various players in economy desperately wanted.

Impact The major question facing the Indian economy at this stage is will and to what extent the policy rate cuts will lead to decline in banks’ retail rates. In this respect, the 25 bps rate cuts are not going to do much in terms of cutting the cost of funding for banks. Nevertheless, the RBI has by now cut the repo and reverse repo by 425 bps and 275 bps respectively and some substantial correction in the retail rates is due. What the rate cuts in policy review signify is that the RBI will uphold the aggressive policy stance it has been following to help the cause of growth. With regard top the retail rates being offered by commercial banks, most likely there will be a reduction going forward, although this may not be immediate. Banks have been parking a record daily average of Rs 1 lakh crore with the central bank through the reverse repo window, which fetch a return of 3.5% after the rate cut. While the decline of 25 bps in this rate is not large enough, it does give a signal to banks that his channel may not remain profitable in medium term and therefore may force them to enhance credit delivery in markets. The main reason why the rate cuts by the RBI have not transformed into the proportionate reduction in retail rate cuts by banks is that the financing costs of banks continue to remain relatively high. The fact is that banks have got locked into high cost medium-term deposits around the time of Lehman crisis and the average cost of deposits would go down as and when these high cost deposits run off. This is a process which will take place slowly and as the average cost of deposits comes down, there will certainly be more fall in prime lending rates (PLR) of banks

Reserve Bank of India (RBI) has said that slowdown was deepening in the Indian economy as the main indicators of growth showed significant moderation in a report prepared by the banking regulator. ‘Macroeconomic outlook of the Indian Economy’, based on various business expectations surveys, continues to exhibit the persistence of less than normal sentiments’, said the bank in its quarterly Macroeconomic and Monetary Developments report.

The professional forecasters’ survey conducted by the bank in December 2008 suggested further moderation in economic activity in 2008-09. ‘As reported by the respondents, the downside risks to growth seem to have amplified due to the projected global economic recession, deterioration in global financial markets and slowdown in domestic demand. The knock-on impact of the global downturn is visible as the main drivers of the growth process in the Indian economy have moderated during the third quarter of 2008-09’ said the bank.

The business expectations survey conducted by the central bank showed that the optimism for the quarters January-March 2009 and April-June 2009 based on major business sentiment indicators such as overall business situation, overall financial situation, production, order books, capacity utilisation, employment, exports, imports and profit margin significantly declined as compared to a year ago.

India’s growth trajectory has been hit hard by the ongoing economic slowdown and the capital outflows, sharp decline in exports and worsening sentiments have started telling on the actual economic expansion. Quarterly growth slowed down to lowest in more than five years in the three months ending December 2008 and most economists see the growth going further down for at least two more quarters before recovering.

India’s banking regulator Reserve Bank of India (RBI) said that there was more space with the monetary authority to further cut the policy rates even as it slashed key policy rates by 25 basis points (bps) in its annual review of monetary policy.

RBI Governor Duvvuri Subbarao said in an interview that there was more room for rate adjustments. “The room for adjustment has come down but that should not be read as a signal that there is no scope for further rate adjustment,’ he said.

However, he also added that this did not mean the RBI will necessarily cut rates in the near term. Earlier the apex bank cut its key lending rate for the sixth time in seven months on Tuesday and urged commercial banks to follow suit to promote the growth in a slowing economy that has taken a much bigger hit than was expected from the going global downturn.

Quick Review of Economy

D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

14 15D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

14 15

The RBI cut its repo rate, the rate at which it infuses short term liquidity into banks, to 4.75% from 5% and its reverse repo rate, at which it absorbs surplus cash from the banking system, to 3.25% from 3.50%.

India’s monetary authority Reserve Bank of India (RBI) said that short term prospects of growth of the Indian economy were expected to be mixed as it had taken a more than anticipated hit from the ongoing global economic crisis.

“India has sustained a greater than expected impact from the global economic crisis and has ‘mixed’ growth prospects for now,’ said D Subbarao, Governor of the central bank. He also added that GDP growth was slowing down, reflecting deceleration in production, negative export growth, shrinking corporate margins and slowing credit delivery growth.

Earlier the bank had lowered its projection of GDP growth at 6% for the current fiscal, in its annual review of monetary policy announced on April 21. While the RBI strongly mentioned its commitment to keep ample liquidity in the system in order the help the cause of growth, it accepted that there were signals of sharp slowdown in economy. The median forecast for growth in FY10 in the survey of professional forecasts conducted by the RBI stood at 5.7%, lowest in six years.

Mounting non-performing assets (NPAs) of the banks have led them to restructure loans worth Rs 80,000 crore in the last fiscal.

Tight liquidity conditions in the wake of the global financial crisis has prompted the Reserve Bank to give regulatory concession on restructuring to provide a breather to the corporate India.

Analysts believe that around 3% of the outstanding loans (Rs 80,000 crore) are to be restructured in the forth quarter of the last fiscal. It is believed that at over 3% of the outstanding credit, the incidence of restructuring is expected to be higher for PSU banks, as against 2% for private banks.

Inflation for the week ended April 18 stood up at 0.57% from 0.26%. Manufacturing index was up 0.3% and fuel index spiked up 0.1% (WoW), while primary articles index rose 1.7% (WoW).

The Reserve Bank of India has also announced to extend the concessional interest rate scheme for a further six months giving respite to exporters hit by shrinking global demand. The announcement came in wake of the deadline as the upper limit of interest on pre-shipment rupee export credit of up to 270 days and post-shipment credit of up to 180 days at BPLR minus 2.5% was due to terminate in the next few days.

In a memo to scheduled commercial banks the RBI said, ‘It has been decided to extend the validity of the scheme

to October 31, 2009’. However the announcement may fall short of exporters expectations who have been asking for credit at 7% without linking with the prime lending rate.

Majority of India’s export revenue comes from the US, Europe and the Middle East and exporters have been hit by a fall in demand in all these countries. For the first time in five years, India’s exports fell by 12.1% in October 2008 and have been unable to recover since.

The Reserve Bank of India has also announced to extend the concessional interest rate scheme for a further six months giving respite to exporters hit by shrinking global demand. The announcement came in wake of the deadline as the upper limit of interest on pre-shipment rupee export credit of up to 270 days and post-shipment credit of up to 180 days at BPLR minus 2.5% was due to terminate in the next few days.

In a memo to scheduled commercial banks the RBI said, ‘It has been decided to extend the validity of the scheme to October 31, 2009’. However the announcement may fall short of exporters expectations who have been asking for credit at 7% without linking with the prime lending rate.

Majority of India’s export revenue comes from the US, Europe and the Middle East and exporters have been hit by a fall in demand in all these countries. For the first time in five years, India’s exports fell by 12.1% in October 2008 and have been unable to recover since.

these things have been taken from Monthly Eco Review dated 20 April--

The outlook of the Indian economy continues to remain uncertain. India is getting increasingly coupled with the global economic downturn, through both the real as well as financial channels. However, the global scenario itself is uncertain and highly unpredictable at the moment. While some strength in expected in the near term to come from stimulus package being launched by the US government as well as some other developed countries, there remains doubts on how the governments will behave regarding foreign trade with some protectionism being already visible.

Further, any meaningful recovery in Indian economy, global economy will have to improve too. International Monetary Fund has already said that the year 2009 would be very difficult and recovery may be expected in 2010 if the global leaders pursue a coherent set of stimulus related policies while at the same time avoiding the protectionist tendencies.

Overall, we feel that outlook of Indian economy and the developing world in general has shown some improvement over the last one month. However, it is too early to reach any conclusion and one will have to wait for at least couple of quarters for some robust results to be discovered.

Quick Review of Economy

D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

16 17D e c e m b e r May 2009

Magnum

D e c e m b e r May 2009

Magnum

16 17

Economy News

RBI hints at regulating NBFC holding cos On instance of the report compiled by the tax authorities, it has been found that many of NBFCs have transferred surplus funds earned earlier to their holding companies, which are currently regulated under the Companies Act, in the form of loans or dividends, the Reserve Bank of India (RBI) has decided in principle to bring under its ambit NBFC holding companies floated by business groups and companies.The move was prompted by the fact that the NBFCs had been frequently complaining of an acute shortage of funds despite receiving liquidity support from the government in consultation with RBI.Govt defers AS 11 till FY 11 Conceding to the suggestions of the National Advisory Committee on Accounting Standard (NACAS), the government has decided to defer the accounting standard 11 (AS-11) mandate deals with foreign exchange losses.The government is expected to come up with a notification that will give relief to India Inc on AS 11 stipulating to recognize foreign exchange losses in the profit and loss accounts every year. AS 11 suggests for mark-to-market provisioning in profit and loss account for foreign exchange related gains and losses.S&P, Fin Min discuss outlook downgrade issue Global rating agency Standard & Poor’s and officials from the ministry of finance have held talks to discuss the grounds for the rating agency downgrading India’s outlook from stable to negative.Late last month, S&P had downgraded its outlook on India’s long-term sovereign credit rating to negative from stable. It claimed that worsening government finances could increase the overseas borrowing costs for companies and weaken the Indian rupee.Govt directs cement cos to roll back price hike Cement companies have come under the wrath of government for charging higher prices despite asking for stimulus package. The government has also warned these companies it will not allow stimulus package to the industry unless it reduces the price of the commodity.Recently, cement companies increased the price by up to Rs 7 per 50 kg bag. The department of industrial policy and promotion (DIPP), in a strongly worded message told the Cement Manufacturers’ Association (CMA) that their decision of price increase was uncalled for. ARCs to benefit from new NPA transfer norms Asset reconstruction companies (ARC) – companies that deal in buying non-performing assets (NPAs) from banks and turning them into earning assets – may get an automated route through which the transfer of ownership of distressed assets that these buy from banks will be recognized by registrar of companies (RoC).