2009100917 prezentacja lng terminal why at the baltic sea ... filepolish oil and gas companypolish...

TRANSCRIPT

Polish Oil and Gas CompanyPolish Oil and Gas CompanyLNG Terminal: Why at the Baltic Sea CoastLNG Terminal: Why at the Baltic Sea Coast??

24 November 2009, Strasburg

AgendaAgenda

1. Company Presentation

2. Gas market in Poland

3. LNG Project – LNG Terminal in Świnoujście

4. Polish and European Context

2

1. Company Presentation1. Company Presentation

33

PGNiG Capital Gro pPGNiG Capital GroupPoland’s leading integrated gas and oil companyPoland s leading integrated gas and oil company

Dominant gas and growing oil producer

Dominant gas importer to Poland and owner of gas

t

Robust domestic gas distribution businessp storages

Exploration and Production Trade and Storage Distribution

Well positioned for further growth in anenvironment of improving marketenvironment of improving market

fundamentals

44

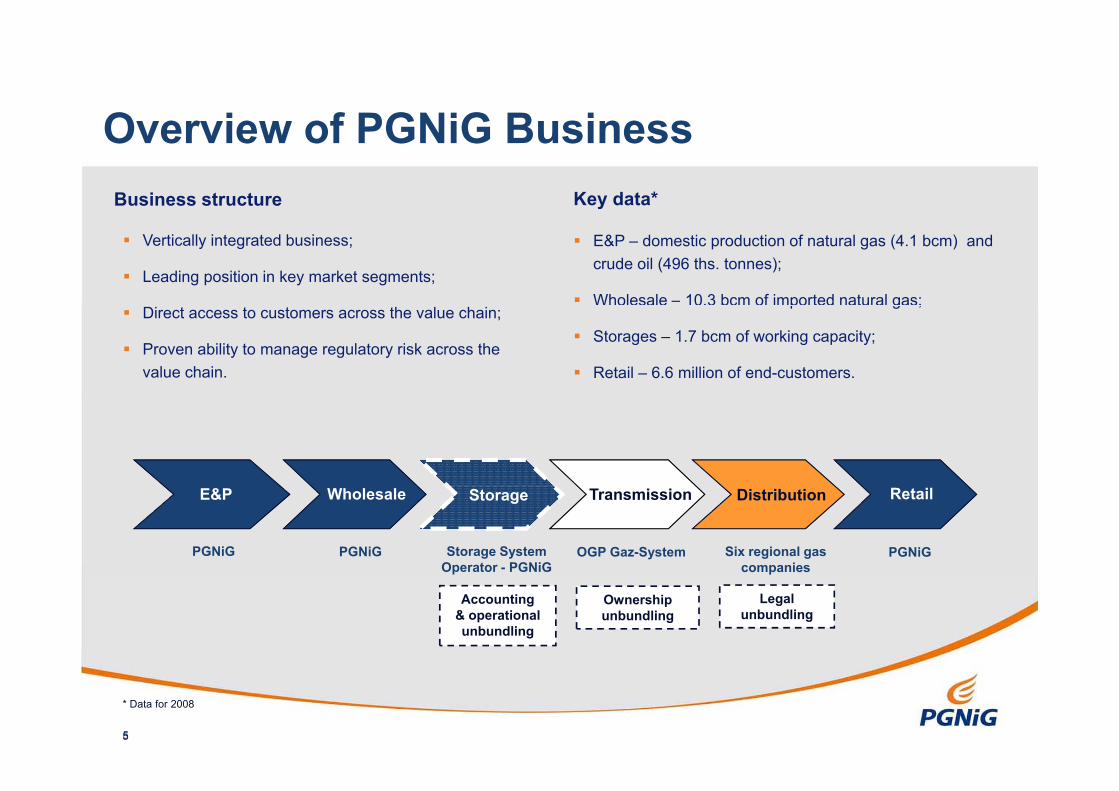

Overview of PGNiG BusinessOverview of PGNiG BusinessKey data*Business structure

E&P – domestic production of natural gas (4.1 bcm) and crude oil (496 ths. tonnes);

Wholesale – 10.3 bcm of imported natural gas;

Vertically integrated business;

Leading position in key market segments;p g ;

Storages – 1.7 bcm of working capacity;

Retail – 6.6 million of end-customers.

Direct access to customers across the value chain;

Proven ability to manage regulatory risk across the value chain.

WholesaleE&P Storage Transmission Distribution Retail

Six regional gas companies

PGNiG Storage System Operator - PGNiG

PGNiGPGNiG OGP Gaz-System

Ownership unbundling

Legal unbundling

Accounting& operationalunbundling

5

* Data for 2008

5

2. Gas Market in Poland2. Gas Market in Poland

66

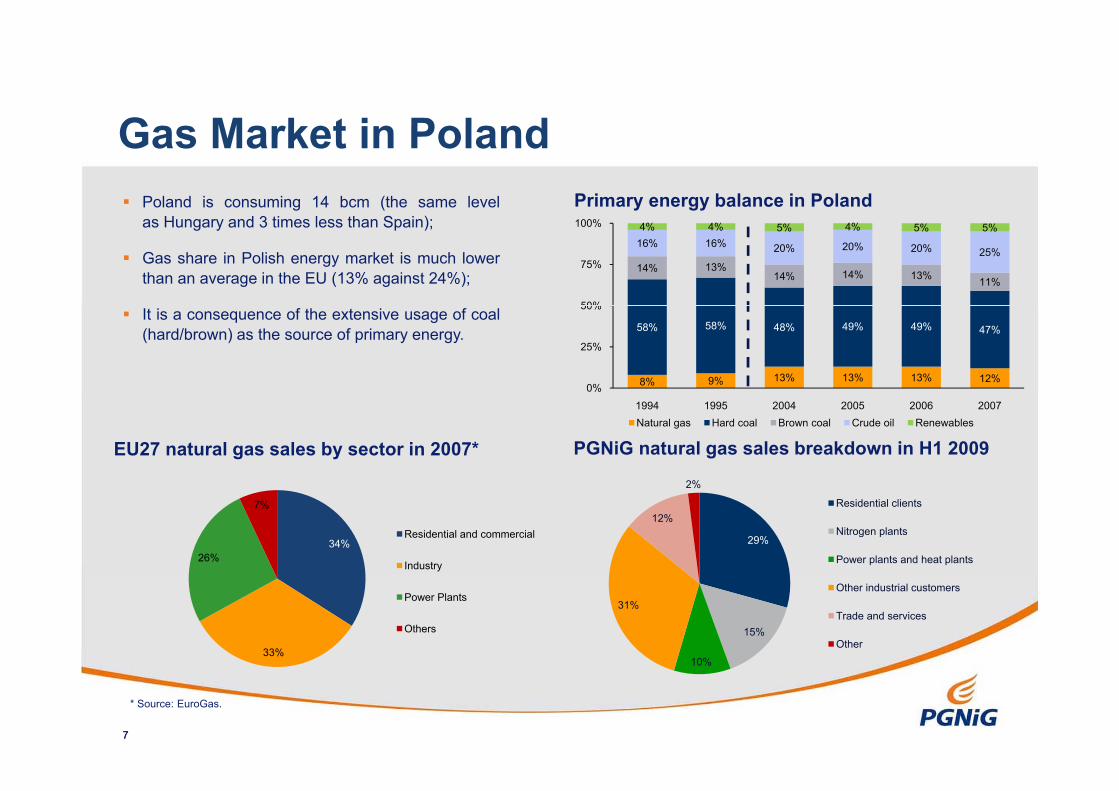

Gas Market in Poland Poland is consuming 14 bcm (the same level

H d 3 i l h S i )Primary energy balance in Poland

Gas Market in Poland

as Hungary and 3 times less than Spain);

Gas share in Polish energy market is much lowerthan an average in the EU (13% against 24%);

14% 13%14% 14% 13% 11%

16% 16% 20% 20% 20% 25%

4% 4% 5% 4% 5% 5%

50%

75%

100%

It is a consequence of the extensive usage of coal(hard/brown) as the source of primary energy.

8% 9% 13% 13% 13% 12%

58% 58% 48% 49% 49% 47%

0%

25%

50%

PGNiG natural gas sales breakdown in H1 2009EU27 natural gas sales by sector in 2007*

1994 1995 2004 2005 2006 2007Natural gas Hard coal Brown coal Crude oil Renewables

2%

34%26%

7%

Residential and commercial

Industry

29%

12%

2%

Residential clients

Nitrogen plants

Power plants and heat plants

33%

Power Plants

Others 15%

10%

31%Other industrial customers

Trade and services

Other

77

* Source: EuroGas.

10%

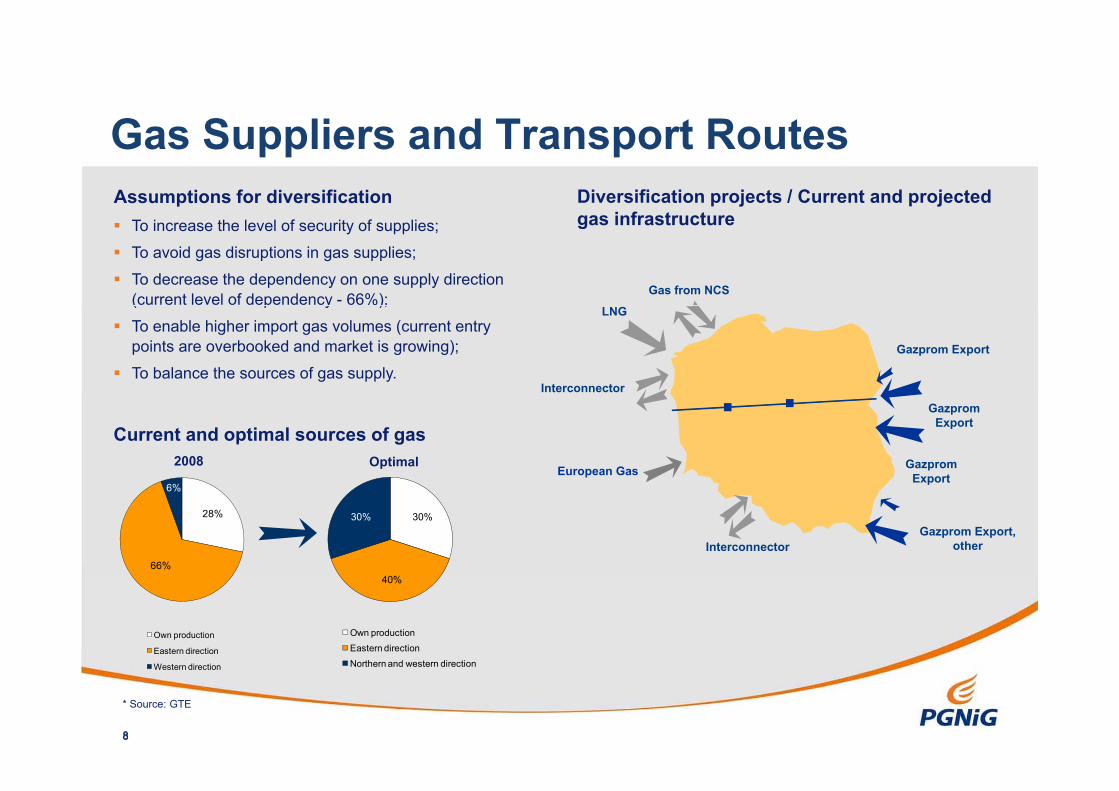

G S li d T t R tGas Suppliers and Transport RoutesDiversification projects / Current and projected gas infrastructure

Assumptions for diversification To increase the level of security of supplies;

To avoid gas disruptions in gas supplies;

To decrease the dependency on one supply direction (current level of dependency - 66%);

gas infrastructure

Gas from NCS( p y );

To enable higher import gas volumes (current entry points are overbooked and market is growing);

To balance the sources of gas supply.Gazprom Export

LNG

Interconnector

6%

Current and optimal sources of gas2008 Optimal

Gazprom Export

Gazprom ExportEuropean Gas

28%

66%

6%

30%30%Gazprom Export,

otherInterconnector

Own production

Eastern direction

W t di ti

40%

Own productionEastern directionNorthern and western direction

8

Western direction Northern and western direction

* Source: GTE

8

3. LNG Project – LNG Terminal in Świnoujściej j

99

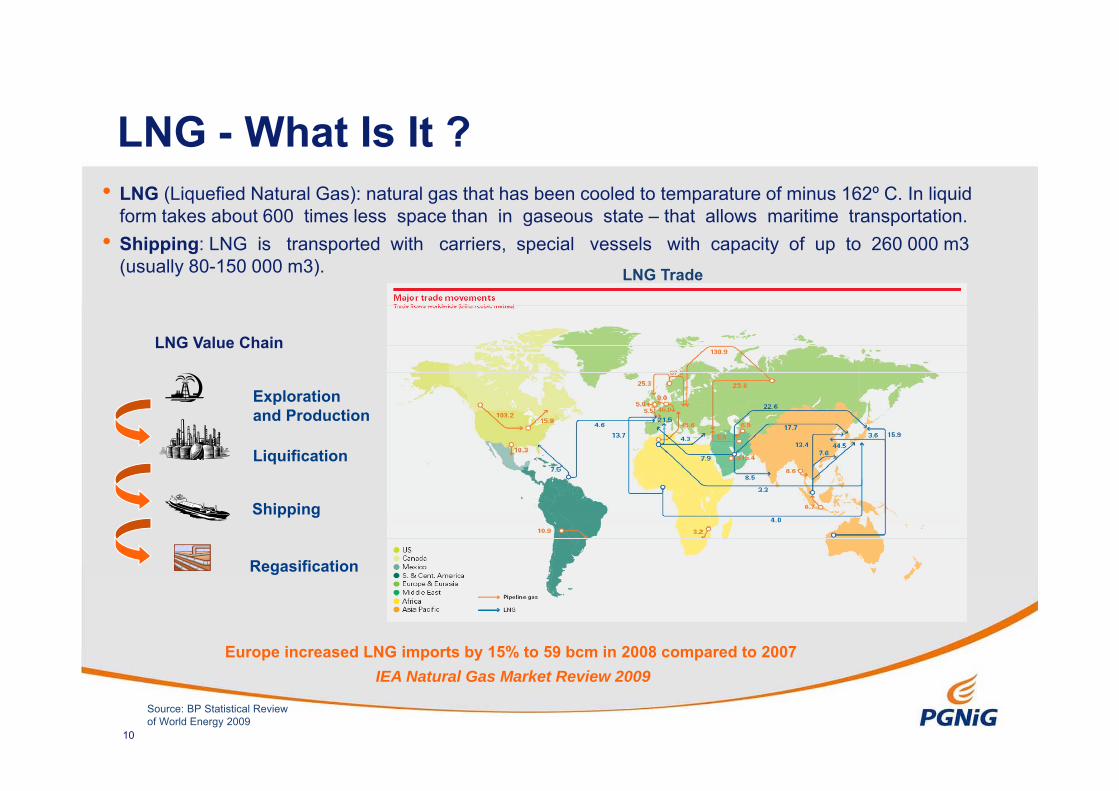

LNG What Is It ?LNG - What Is It ?• LNG (Liquefied Natural Gas): natural gas that has been cooled to temparature of minus 162º C. In liquid

form takes about 600 times less space than in gaseous state that allows maritime transportationform takes about 600 times less space than in gaseous state – that allows maritime transportation.• Shipping: LNG is transported with carriers, special vessels with capacity of up to 260 000 m3

(usually 80-150 000 m3). LNG Trade

Exploration

LNG Value Chain

Exploration and Production

Liquification

Shipping

Regasification

Europe increased LNG imports by 15% to 59 bcm in 2008 compared to 2007

10

Source: BP Statistical Review of World Energy 2009

IEA Natural Gas Market Review 2009

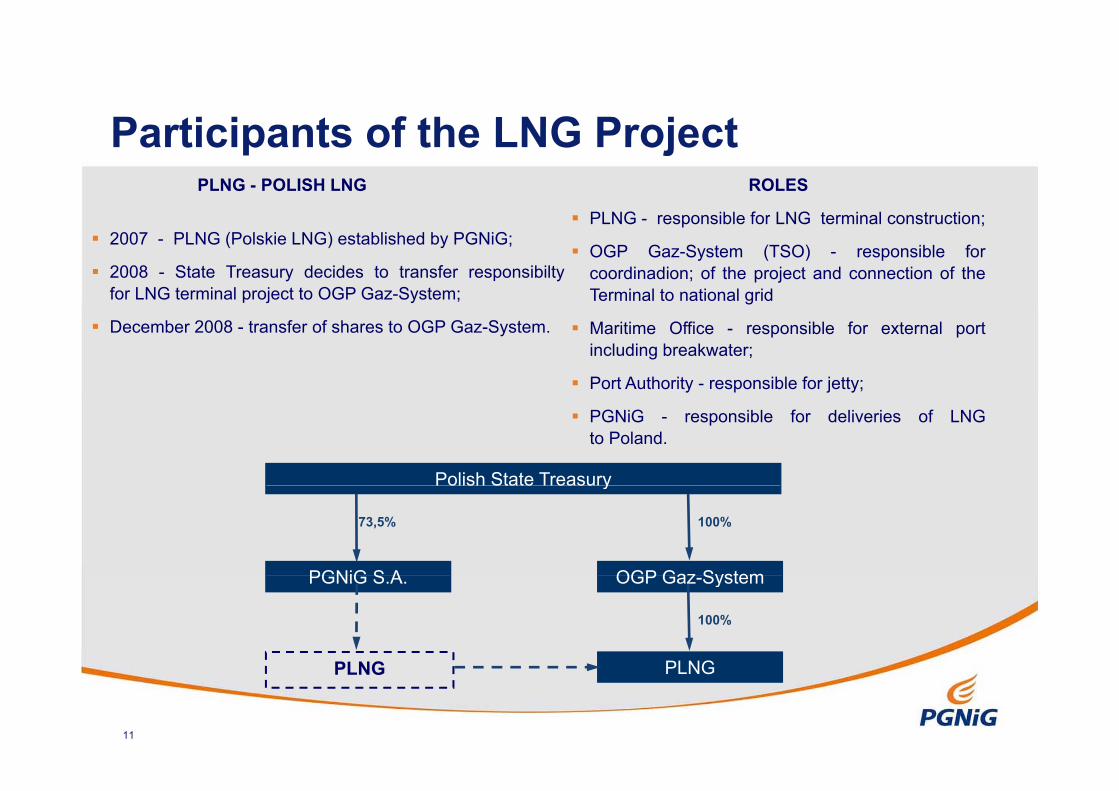

Participants of the LNG ProjectParticipants of the LNG ProjectPLNG - POLISH LNG ROLES

PLNG responsible for LNG terminal construction; 2007 - PLNG (Polskie LNG) established by PGNiG;

2008 - State Treasury decides to transfer responsibiltyfor LNG terminal project to OGP Gaz-System;

PLNG - responsible for LNG terminal construction;

OGP Gaz-System (TSO) - responsible forcoordinadion; of the project and connection of theTerminal to national grid

December 2008 - transfer of shares to OGP Gaz-System. Maritime Office - responsible for external portincluding breakwater;

Port Authority - responsible for jetty;

Polish State Treasury

PGNiG - responsible for deliveries of LNGto Poland.

Polish State Treasury

PGNiG S A OGP Gaz System

73,5% 100%

PLNG

PGNiG S.A. OGP Gaz-System

PLNG

100%

11

PLNG PLNG

LNG T i l b i d tBasic facts concerning LNG project

LNG Terminal – basic data

• Location of terminal: Świnoujście, Poland

Basic facts concerning LNG project

• Reloading capacity of terminal:

Phase I - 5.0 bcm/annually from H2 2014Phase II - 7.5 bcm/annually

• LNG tanks capacity: 2 x 160,000 m3

• Completion date:

• Estimated cost: ~

2014

600 M EUR

1212

LNG T i l ti h d lLNG Terminal – time schedule2006 - Feasibility Study Phase

• Terminal localisation in Świnoujście• Terminal localisation in Świnoujście

2007 - 2009 - Implementation Phase

• Selection of FEED and EPC contractors• Licenses and permits• Legal procedures and obtaining of concessions• Financing of the investment• LNG purchase agreements• Final investment decision

2010 - 2014 - Investment Phase2010 - 2014 - Investment Phase

• Construction of the LNG Regasification Terminal• Terminal connection to the National Transmission System• E i f th N ti l T i i S t d• Expansion of the National Transmission System managed by Transmission System Operator (TSO)

2014 - End of Construction/Commissioning & first LNG deliveries

1313

LNG deliveries supply contractsLNG deliveries - supply contractsContract between PGNiG and Qatargas

• In April 2009 PGNiG and Qatargas Operating Company signed the Head of Agreement in which Qatargas agreed that approx. 1 million tonnes of LNG (1,45 bcm of natural gas) will be suppliedof LNG (1,45 bcm of natural gas) will be supplied annually to LNG terminal in Świnoujście fora period of twenty years, starting from 2014.

• In June 2009 PGNiG and Qatargas signeda Sales and Purchase Agreement (SPA). LNG price in the SPA is based on crude oil prices.

• Deliveries will be executed on the Ex-Ship basis.Transportation wil be carried out with Q-flexvessels, that is, allowing for the transportation of

PGNiG plans to further diversify its portfolio. Depending on market situation Qatari contract will be supplemented with mid

approx 217 000 m3 of natural gas at a time.pp

or spot term LNG contracts.

14

LNG Terminal-Environmental and Technical Security IssuesSecurity IssuesEnvironment & Surroundings

LNG T i l i Ś i jś i h ll t h ti i t i t d iti• LNG Terminal in Świnoujście shall not have any negative impact on environment and citizens of Pomeranian Region. Moreover to protect historic landmarks and unique sand dunes the Terminal will be located aprox. 750 m away from the coast line.

• All air quality standards required by the provisions of the law will be met.

• There will be no negative impact for the integrity of the areas covered by NATURA 2000by NATURA 2000.

• Project will have positive influence on life conditions due to creation of new job oportunities in the region.

Technical Security

• In case of LNG leak out from the tank it would evapourate into the atmosphere without any consequences for h b i i i bi dihuman beings or ramaining biosurrounding.

• New technologies used in containers construction (so-called full-contaiment), dedicated proceedures and security systems guaratee the highest level of security.

15

y y g g y

4. Polish and European context4. Polish and European context

1616

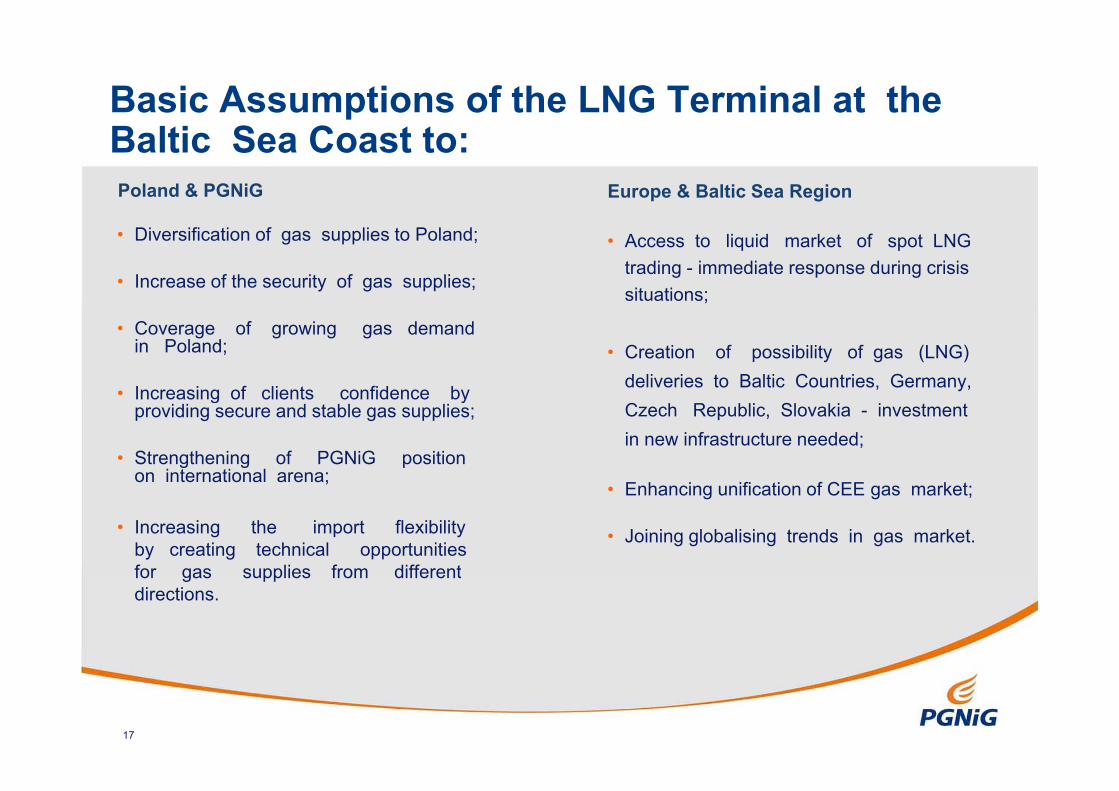

Basic Assumptions of the LNG Terminal at the B l i S CBaltic Sea Coast to:Poland & PGNiG Europe & Baltic Sea Region

• Diversification of gas supplies to Poland;

• Increase of the security of gas supplies;

• Access to liquid market of spot LNG trading - immediate response during crisis situations;

• Coverage of growing gas demandin Poland;

• Increasing of clients confidence by

• Creation of possibility of gas (LNG) deliveries to Baltic Countries, Germany, Increasing of clients confidence by

providing secure and stable gas supplies;

• Strengthening of PGNiG position on international arena;

Czech Republic, Slovakia - investment in new infrastructure needed;

E h i ifi ti f CEE k t

• Increasing the import flexibilityby creating technical opportunities for gas supplies from different

• Enhancing unification of CEE gas market;

• Joining globalising trends in gas market.

for gas supplies from differentdirections.

17

LNG Terminal in Świnoujście as a remedium for gas crisis and security of gas supply (SoS)

I POLISH CONTEXTI. POLISH CONTEXT

• January 2009 - Gas supply crisis in Europe.

• April 2009 - Skanled project suspended. As a consequence LNG Terminal in Świnoujście becomes

the most important diversification project.

• April/August 2009 - Polish Government issued special legal act dedicated to LNG

Terminal in Świnoujście as a guarantee of most eficient and efective realisation of this strategic

project.

• June 2009 - After solid and intensive negotiations PGNiG SA and Qatargas signed g Q g g

a long-term contract (for 20 years) for LNG deliveries of 1,45 bcm starting from the year 2014.

18

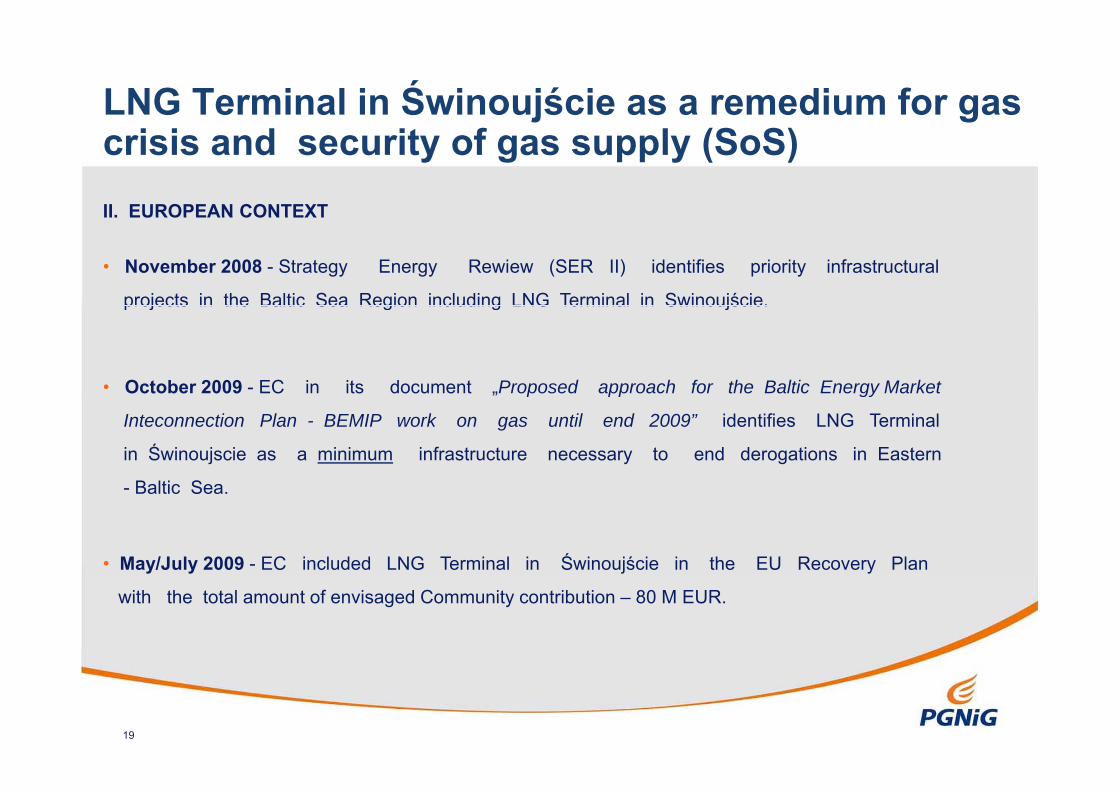

LNG Terminal in Świnoujście as a remedium for gas crisis and security of gas supply (SoS)II. EUROPEAN CONTEXTII. EUROPEAN CONTEXT

• November 2008 - Strategy Energy Rewiew (SER II) identifies priority infrastructural

projects in the Baltic Sea Region including LNG Terminal in Swinoujście.projects in the Baltic Sea Region including LNG Terminal in Swinoujście.

• October 2009 - EC in its document „Proposed approach for the Baltic Energy Market „ p pp gy

Inteconnection Plan - BEMIP work on gas until end 2009” identifies LNG Terminal

in Świnoujscie as a minimum infrastructure necessary to end derogations in Eastern

Baltic Sea- Baltic Sea.

• May/July 2009 - EC included LNG Terminal in Świnoujście in the EU Recovery Plan

with the total amount of envisaged Community contribution – 80 M EUR.

19

LNG Terminal in Świnoujście as a remedium for gas crisis and security of gas supply (SoS)III. OPEN SEASON

• June 2009 - PLNG commenced the 2009 procedure of offering an LNG Terminal in Świnoujście

on an open season basis.

• October 2009 - Polskie LNG launched public consultations of relevant documents

(draft Instruction as well as draft Model agreement for provision of regasification services).

20

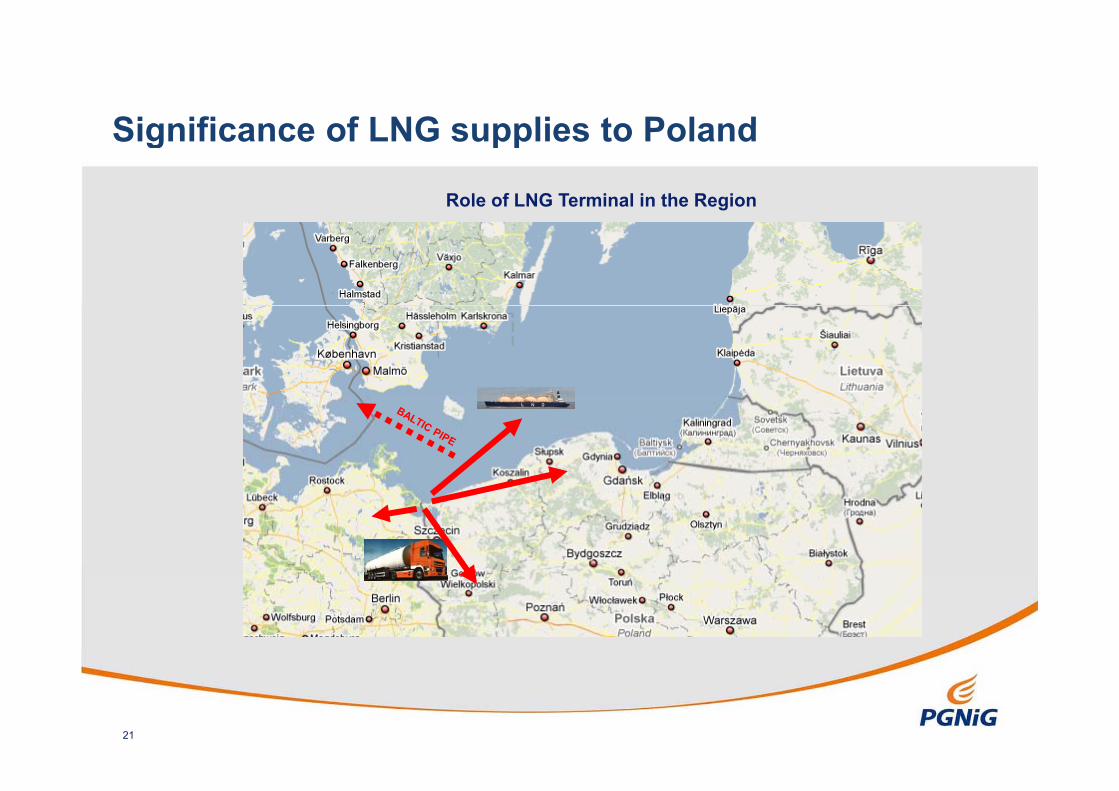

Significance of LNG supplies to PolandSignificance of LNG supplies to Poland

Role of LNG Terminal in the Region

21

Thank You For Your Attention !

22