2009 annual meeting ● assemblée annuelle 2009 halifax, nova scotia ● halifax (nouvelle-...

DESCRIPTION

Canadian Institute of Actuaries. L’Institut canadien des actuaires. 2009 Annual Meeting ● Assemblée annuelle 2009 Halifax, Nova Scotia ● Halifax (Nouvelle- Écosse ). Denise Lang Overview of the GMWB product, need it fills and impact of the economic crisis Pierre Vincent - PowerPoint PPT PresentationTRANSCRIPT

2009 Annual Meeting ● Assemblée annuelle 2009Halifax, Nova Scotia ● Halifax (Nouvelle-Écosse)

2009 Annual Meeting ● Assemblée annuelle 2009Halifax, Nova Scotia ● Halifax (Nouvelle-Écosse)

Canadian Institute

of Actuaries

Canadian Institute

of Actuaries

L’Institut canadien desactuaires

L’Institut canadien desactuaires

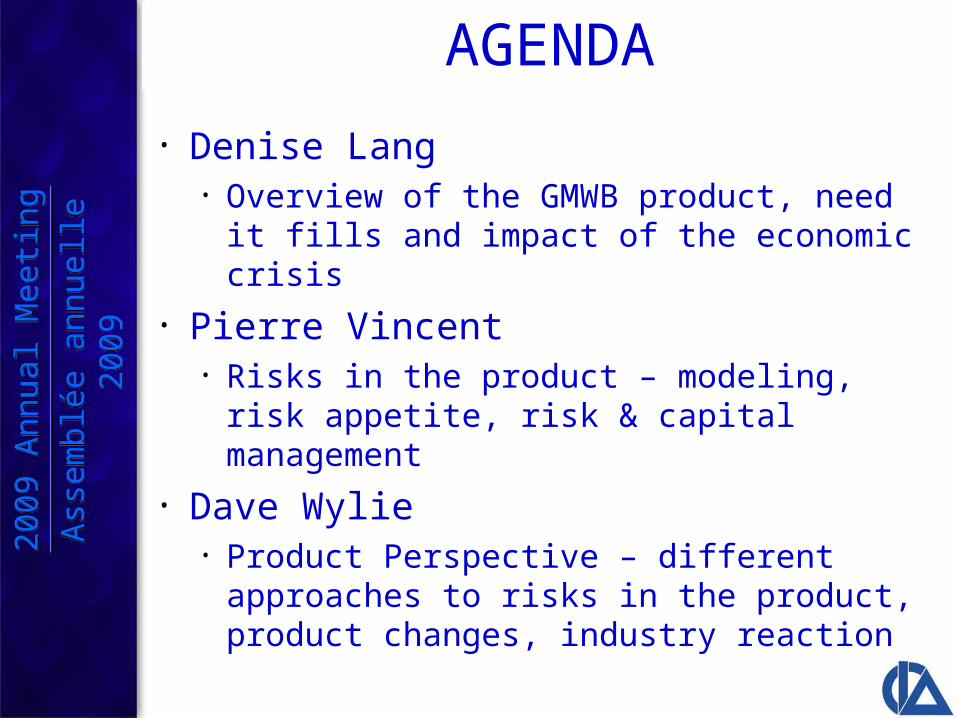

AGENDA

• Denise Lang• Overview of the GMWB product, need it

fills and impact of the economic crisis

• Pierre Vincent• Risks in the product – modeling, risk

appetite, risk & capital management

• Dave Wylie• Product Perspective – different

approaches to risks in the product, product changes, industry reaction

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

AGENDA

• Background - Demographic changes

• Retirement Challenges

• Needs in Retirement

• Typical GMWB (Guaranteed Minimum

Withdrawal Benefit) product features

• Impact of the economic crisis

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

Some headlines & research findings• Boomers age 47 to 60 make up roughly 22% of Canadian

population – Boomers & retirees in Canada Secondary research – July /06

• In under 10 years Canadians 55 years of age and older will control over 70% of investment assets – Investor Economics, household balance sheet report 2005

• Of leading edge boomers only 15% feel prepared for retirement, 45% feel they need same or more income – Strategic Guidance Consulting

• 50% of Canadians expect to live into their 90’s – BMO Retirement study findings quoted in Investment Executive article Jun 1 /06

• 48% of 50-something boomers are unsure of the best choices for retirement savings, 32% are worried their standard of living will drop once they reach retirement – Jonathan Chevreau, National post articles “Boomer gender battle in retirement?”, Jul 17/06 and “Stressed Boomers”, Jul 13/06

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

Changing Demographics in Canada

• Canadian population is aging

• Life expectancy continues to increase

• Implications

Consumer focus will shift from wealth accumulation to management and payout of accumulated wealth

Savings must fund a longer retirement period

Product allocation increasingly important as more baby boomers approach and enter retirement years

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

New Challenges in Retirement

• Longevity

• Interest Rates and Inflation

• Market Volatility

• Inflation

• Control and Access

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

Challenge: Market Volatility

• Investors will face their greatest risks and challenges in the few years just before and after retirement

• Choosing the right investment products is critical

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

Accumulation Phase Same Average Return = Same Accumulation Result

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009 Accumulation

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

Average return is key during accumulation

Payout PhaseSequence of returns makes a big difference

in the distribution phase

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

Distribution

$793,304

$0

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

$1,600,000

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

Strong Early ReturnsReversed: Poor Early Returns

What do Canadians want?• The majority of Canadians prefer a

monthly income stream in retirement

• Many are concerned that they may outlive their savings

• Canadians will have a strong preference for products that provide

• risk management

• income management

• tax efficiency

• GMWB products designed for these needs

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

GMWB Products• Income is predictable, sustainable and

potentially increasing

• Products allow investments in a variety of funds – usually a limit on equity exposure

• Initially a 20 year guarantee - now ‘for life’

• Upside potential in guarantees

– resets - lock in market gains

– Annual bonus (on guarantee withdrawal balance) if no withdrawal taken

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

How do guarantees work?

Product example:• Lifetime guarantee 5% p.a. if start at age 65

• 5% bonus on WB annually if no withdrawals

• Guaranteed value resets every 3rd anniversary

• 100% Death benefit

• Client deposits $500,000

At issue:

• Guaranteed Withdrawal Benefit = $500,000

• Death Benefit Guarantee = $500,000

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

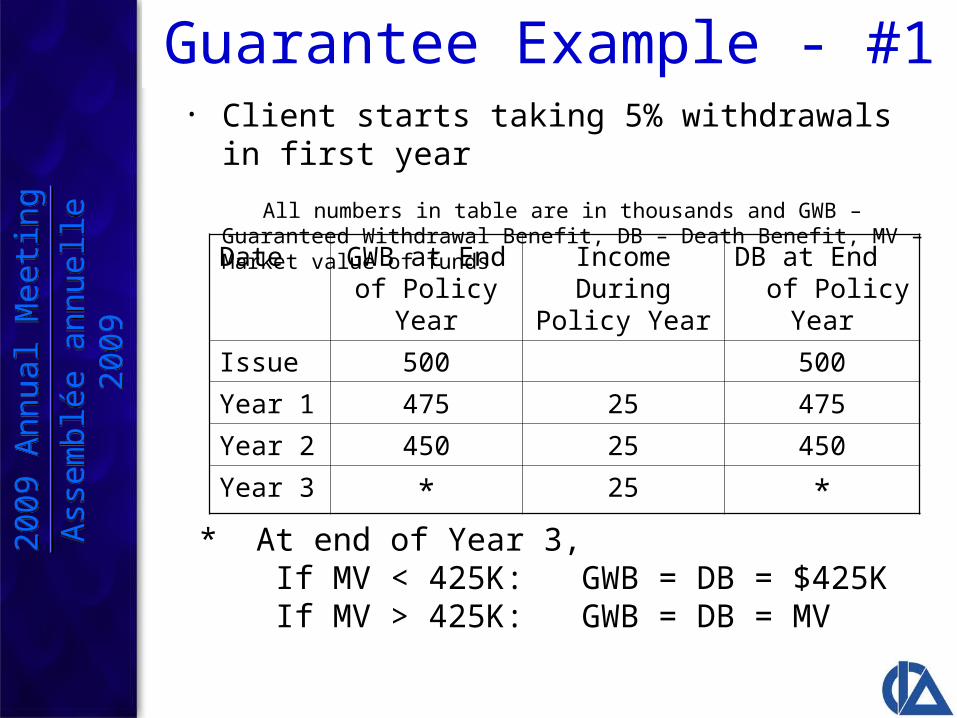

Guarantee Example - #1• Client starts taking 5% withdrawals in first year All numbers in table are in thousands and GWB – Guaranteed Withdrawal

Benefit, DB – Death Benefit, MV – Market value of funds

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

* At end of Year 3, If MV < 425K: GWB = DB = $425K If MV > 425K: GWB = DB = MV

Date GWB at End of Policy Year

Income During Policy Year

DB at End of Policy Year

Issue 500 500

Year 1 475 25 475

Year 2 450 25 450

Year 3 * 25 *

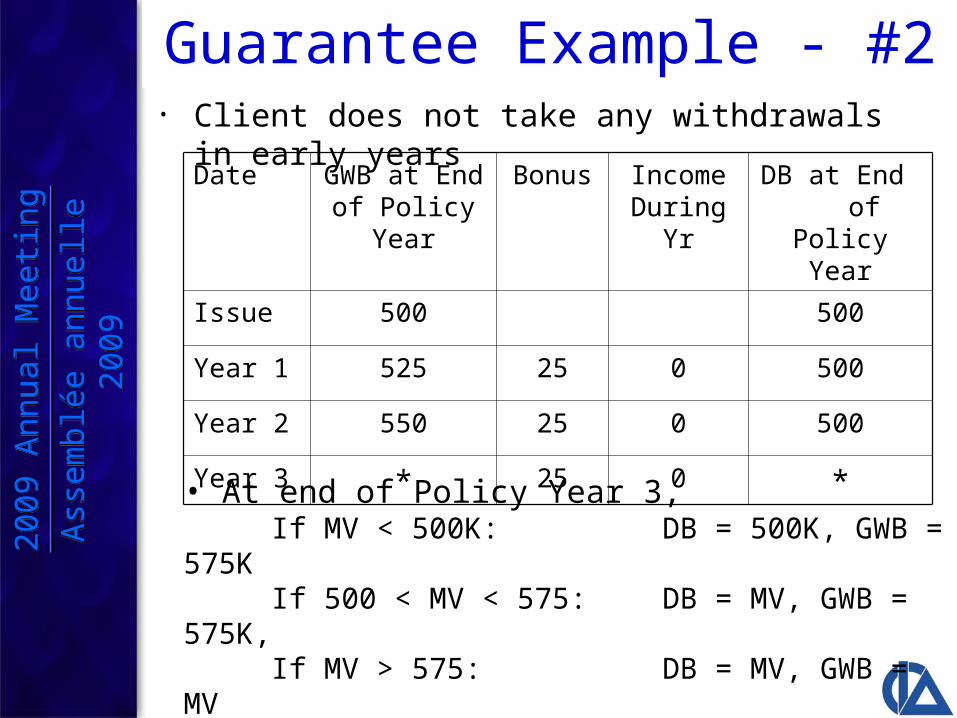

Guarantee Example - #2• Client does not take any withdrawals in early years

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

• At end of Policy Year 3, If MV < 500K: DB = 500K, GWB = 575K If 500 < MV < 575: DB = MV, GWB = 575K, If MV > 575: DB = MV, GWB = MV• If MV > 500K at 3rd anniversary, the annual bonus amount will typically be reset to 5% of that MV going forward

Date GWB at End of Policy Year

Bonus Income During Yr

DB at End of Policy Year

Issue 500 500

Year 1 525 25 0 500

Year 2 550 25 0 500

Year 3 * 25 0 *

Impact of the Economic Crisis• Reserves and required capital are typically very small at

issue for GMWB products

• When equity market declines occur, actuarial liabilities and capital increase considerably even though

– benefits are very long dated with guarantees stretching many years into the future

– guaranteed benefits cannot be accelerated by the policyholder

– the best estimate liability for the guarantees is typically very small compared to the liability required

• Reserves and capital can also be very sensitive to interest rate changes

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

Impact of the Economic Crisis

The increases in reserves and capital have

caused companies to take a number of

actions, including:

– Raising capital

– Increasing risk management activities

(e.g. hedging, reinsurance)

– Product design and pricing changes to

reduce risks

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009

2009

Ann

ual M

eetin

g

Ass

embl

ée a

nnue

lle 2

009