200101 past paper summary | university of western sydney

TRANSCRIPT

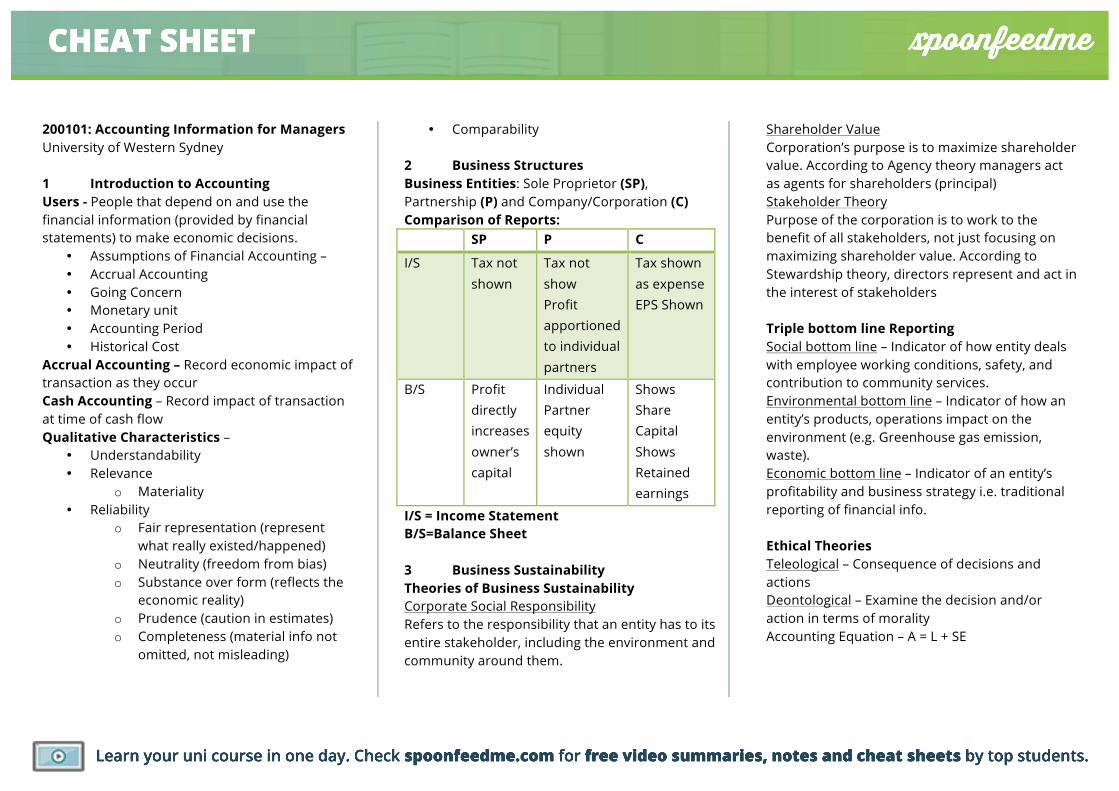

Learn your uni course in one day. Check spoonfeedme.com for free video summaries, notes and cheat sheets by top students.

CHEAT SHEET

200101: Accounting Information for Managers University of Western Sydney 1 Introduction to Accounting Users - People that depend on and use the financial information (provided by financial statements) to make economic decisions.

• Assumptions of Financial Accounting – • Accrual Accounting • Going Concern • Monetary unit • Accounting Period • Historical Cost

Accrual Accounting – Record economic impact of transaction as they occur Cash Accounting – Record impact of transaction at time of cash flow Qualitative Characteristics –

• Understandability • Relevance

o Materiality • Reliability

o Fair representation (represent what really existed/happened)

o Neutrality (freedom from bias) o Substance over form (reflects the

economic reality) o Prudence (caution in estimates) o Completeness (material info not

omitted, not misleading)

• Comparability 2 Business Structures Business Entities: Sole Proprietor (SP), Partnership (P) and Company/Corporation (C) Comparison of Reports: SP P C

I/S Tax not shown

Tax not show Profit apportioned to individual partners

Tax shown as expense EPS Shown

B/S Profit directly increases owner’s capital

Individual Partner equity shown

Shows Share Capital Shows Retained earnings

I/S = Income Statement B/S=Balance Sheet 3 Business Sustainability Theories of Business Sustainability Corporate Social Responsibility Refers to the responsibility that an entity has to its entire stakeholder, including the environment and community around them.

Shareholder Value Corporation’s purpose is to maximize shareholder value. According to Agency theory managers act as agents for shareholders (principal) Stakeholder Theory Purpose of the corporation is to work to the benefit of all stakeholders, not just focusing on maximizing shareholder value. According to Stewardship theory, directors represent and act in the interest of stakeholders Triple bottom line Reporting Social bottom line – Indicator of how entity deals with employee working conditions, safety, and contribution to community services. Environmental bottom line – Indicator of how an entity’s products, operations impact on the environment (e.g. Greenhouse gas emission, waste). Economic bottom line – Indicator of an entity’s profitability and business strategy i.e. traditional reporting of financial info. Ethical Theories Teleological – Consequence of decisions and actions Deontological – Examine the decision and/or action in terms of morality Accounting Equation – A = L + SE

Learn your uni course in one day. Check spoonfeedme.com for free video summaries, notes and cheat sheets by top students.

CHEAT SHEET

4 Business Transactions Accrual Accounting – Record economic impact of transaction as they occur Cash Accounting – Record impact of transaction at time of cash flow A L Rev. Exp. SE

Increase DR CR CR

Decrease CR DR DR

Balance DR CR CR DR CR The Accounting Cycle: 1) Source Document 2) Journal Entries 3) Post to Ledger 4) Pre-Closing Trial Balance 5) Adjusting Entries 6) Adjusted Trial balance 7) Closing Entries 8) Post-Closing Trial Balance 9) Financial Statements

5 Balance Sheet Asset: Definition: Resource controlled, Provide future economic benefit, Result of past event Recognition: Probable economic benefit, Reliably Measured Liability:

Definition: Present Obligation, Outflow of future economic benefit, Result of past event Recognition: Probable outflow of economic benefit, Reliably Measured Shareholders’ Equity: Definition: Residual Interest Measuring Assets - Historical Cost: Cost to initially acquire Market Value: Value you could sell for on the market Fair Value: Value it could be bought or sold for between willing parties, does not necessarily require a market place Contra Account - Are accounts that record any detraction from the historical cost of an asset or liability control account Allowance for Doubtful Debt Creating Allowance for Doubtful Debt DR Bad Debt Expense CR Allowance for Doubtful Debt Writing Off Bad Debt DR Allowance for Doubtful debt CR Accounts Receivable Depreciation DR Depreciation Expense CR Accumulated Depreciation

Perpetual Inventory System - Continually records the impact of transaction on COGS and Inventory control accounts. Purchase Returns and Allowances – DR Inventory CR Cash/ Accounts Payable OR DR Purchase Returns and Allowances CR Accounts Payable Sales Returns or Allowances – DR Sales Returns and Allowances CR Cash/ Accounts Receivables DR Inventory CR COGS Write –off: DR inventory write-down CR COGS Periodic Inventory System – Need to deduce COGS using the formula: COGS = O/B INVENTORY + PURCHASES - C/B INVENTORY (AFTER A END OF YEAR Stock take). Purchase Returns and Allowances - DR Cash/ Accounts payable CR Purchase Returns and Allowances Sales Returns and Allowances - Sales Returns or Allowance: DR Sales Returns and Allowances CR cash/ accounts receivable

Learn your uni course in one day. Check spoonfeedme.com for free video summaries, notes and cheat sheets by top students.

CHEAT SHEET

FIFO The value of COGS and ending inventory will be equal to the value of the oldest inventory purchased or held. LIFO The value of COGS and ending inventory will be equal to the value of the newest inventory purchased or held. Weighted Average Cost Method The value of COGS and ending inventory will be equal to the weighted average of all inventories. 6 Income Statement and Statement of Changes in Equity Income Statement – Revenue: Inflows of economic benefits (as a result of ordinary operating activities) that result in an increase in total equity (not attributed to owners contributions). Expenses: outflow of economic benefits (as a result of ordinary operating activities that result in a decrease in total equity (not attributed to owners’ distributions). Expiration of Assets - DR Insurance Expense CR Prepaid Insurance Unearned Revenue -

DR Unearned Revenue CR Service Revenue Accrual of Unrecorded Revenue - DR Accrued Revenue CR Service Revenue Accrual of Unrecorded Expenses - DR Wages expense CR Accrued Wages Depreciation DR Depreciation Expense CR Accumulated Depreciation

𝑆𝑡𝑟𝑎𝑖𝑔ℎ𝑡 − 𝑙𝑖𝑛𝑒 = 𝐶𝑜𝑠𝑡 − 𝑅𝑒𝑠𝑖𝑑𝑢𝑎𝑙 𝑉𝑎𝑙𝑢𝑒𝑈𝑠𝑒𝑓𝑢𝑙 𝐿𝑖𝑓𝑒(𝑖𝑛 𝑦𝑒𝑎𝑟𝑠)

𝑈𝑛𝑖𝑡𝑠 𝑜𝑓 𝑝𝑟𝑜𝑑𝑢𝑐𝑡𝑖𝑜𝑛

= 𝐶𝑜𝑠𝑡 − 𝑅𝑒𝑠𝑖𝑑𝑢𝑎𝑙 𝑉𝑎𝑙𝑢𝑒

𝑈𝑠𝑒𝑓𝑢𝑙 𝐿𝑖𝑓𝑒(𝑖𝑛 𝑢𝑛𝑖𝑡𝑠 𝑝𝑟𝑜𝑑𝑢𝑐𝑒𝑑)

𝑅𝑎𝑡𝑒 𝑓𝑜𝑟 𝑟𝑒𝑑𝑢𝑐𝑖𝑛𝑔 𝑏𝑎𝑙𝑎𝑛𝑐𝑒 = 1 − 𝑅𝑒𝑠𝑖𝑑𝑢𝑎𝑙 𝑣𝑎𝑙𝑢𝑒

𝐶𝑜𝑠𝑡!

𝑅𝑒𝑑𝑢𝑐𝑖𝑛𝑔 𝑏𝑎𝑙𝑎𝑛𝑐𝑒 𝑑𝑒𝑝𝑟𝑒𝑐𝑖𝑎𝑡𝑖𝑜𝑛= 𝐶𝑢𝑟𝑟𝑒𝑛𝑡 𝐶𝑎𝑟𝑟𝑦𝑖𝑛𝑔 𝑎𝑚𝑜𝑢𝑛𝑡 𝑋 𝐷𝑒𝑝𝑟𝑒𝑐𝑖𝑎𝑡𝑖𝑜𝑛 𝑟𝑎𝑡𝑒

7 Statement of Cash Flows Operating Activities – Involves income statement items Investing Activities: Involves cash flows from investment and non-current assets

Financing Activities: Involves cash flows from non-current liabilities and owner’s equity items Preparing the Statement of Cash Flows – Direct Method

1. Determine Cash Flows from Operating Activities

2. Determine Cash Flows from Investing Activities

3. Determine Cash Flows from Investing Activities

4. Calculate Net Cash Flows and Ending Cash Balance

Value/Purpose of the Statement of Cash Flows Helps to assess:

• Ability to generate future cash flows • Ability to pay dividends • Investing and financing transactions for

the period 8 Financial Statement Analysis Analytical Methods – Horizontal/ Trend Analysis: Evaluate series of financial statement data over period of time Vertical Analysis: Expressing each item in financial statement as % of base amount Ratio Analysis: Expresses Relationship among selected items of financial data Useful Ratios –

Learn your uni course in one day. Check spoonfeedme.com for free video summaries, notes and cheat sheets by top students.

CHEAT SHEET

Performance Ratios Return on Assets = !"#$%&'() !"#$%& !"#$%" !"#

!"#$% !""#$"

Activity Ratios Asset turnover rate = !"#$% !"#"$%"

!"#$% !""#$"

Liquidity Ratios Current ratio = !"##$%& !""#$

!"##$%& !"#$"%"&'

Financial Structure Ratios Debt to Equity Ratio = !"#$% !"#$"%"&"'(

!"#$% !!!"#!!"#$%& !"#$%&

Du Pont Analysis ROE =

𝑇𝑜𝑡𝑎𝑙 𝐴𝑠𝑠𝑒𝑡𝑠𝑇𝑜𝑡𝑎𝑙 𝑆ℎ𝑎𝑟𝑒ℎ𝑜𝑙𝑑𝑒𝑟𝑠 𝐸𝑞𝑢𝑖𝑡𝑦

𝑋𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑛𝑔 𝑝𝑟𝑜𝑓𝑖𝑡 𝑎𝑓𝑡𝑒𝑟 𝑡𝑎𝑥

𝑇𝑜𝑡𝑎𝑙 𝑆𝑎𝑙𝑒𝑠 𝑅𝑒𝑣𝑒𝑛𝑢𝑒𝑋𝑇𝑜𝑡𝑎𝑙 𝑆𝑎𝑙𝑒𝑠𝑇𝑜𝑡𝑎𝑙 𝐴𝑠𝑠𝑒𝑡𝑠

Limitations • Estimates • Atypical Data • Diversification of Entities

9 Budgeting The Budgeting Process

1. Setting business objectives. 2. Collecting data from company organisations. 3. Forecasting future conditions, including analysis of: a) Economic conditions b) Industry trends

c) Previous market share d) Changes in prices e) Anticipated advertising/promotion 4. Develop & prepare: a) Sales budget b) Cost of Sales budget (i.e. inventory required to meet sales forecast) c) Selling/administrative expense budget d) Budgeted income statement 5. Develop and prepare: a) Capital expenditure budget b) Cash forecasts and cash budget c) Budgeted Balance Sheet

6. Prepare Master Budget Behavioural Aspects of Budgeting – Bias: Tension between upper and lower management Participation: encourage participation by lower management when setting budgets Slack: Temptation to inflate costs or depress sales forecast

10 Cost and Costing Cost Behaviours – Variable Costs - Costs that vary directly, proportionately with changes in activity levels Fixed Costs - Costs that remain the same, regardless of changes in activity levels. CVP Analysis –

!"#$% !"#$!"#$ !"##$%& !"#$%!!"#$ !"#$"%&! !"#$

= Units needed

!"#$% !"#$#

!"#$%&%' !"#$%+ 𝑈𝑛𝑖𝑡 𝑉𝑎𝑟𝑖𝑎𝑏𝑙𝑒 𝐶𝑜s𝑡 = Unit Selling

Price

𝑝𝑟𝑜𝑓𝑖𝑡 𝑎𝑓𝑡𝑒𝑟 𝑡𝑎𝑥(1 − 𝑡𝑎𝑥 𝑟𝑎𝑡𝑒) + 𝐹𝑖𝑥𝑒𝑑 𝐶𝑜𝑠𝑡𝑠

𝑈𝑛𝑖𝑡 𝑆𝑒𝑙𝑙𝑖𝑛𝑔 𝑃𝑟𝑖𝑐𝑒 − 𝑈𝑛𝑖𝑡 𝑉𝑎𝑟𝑖𝑎𝑏l𝑒 𝐶𝑜𝑠𝑡= 𝑄𝑢𝑎𝑛𝑡𝑖𝑡𝑦 𝑛𝑒𝑒𝑑𝑒𝑑

Margin of Safety 𝑀𝑎𝑟𝑔𝑖𝑛 𝑜𝑓 𝑆𝑎𝑓𝑒𝑡𝑦 𝑎𝑠 𝑎 𝑃𝑒𝑟𝑐𝑒𝑛𝑡𝑎𝑔𝑒 =

𝑀𝑎𝑟𝑔𝑖𝑛 𝑜𝑓 𝑆𝑎𝑓𝑒𝑡𝑦 𝑖𝑛 𝑢𝑛𝑖𝑡𝑠𝐸𝑥𝑝𝑒𝑐𝑡𝑒𝑑 𝑆𝑎𝑙𝑒𝑠 𝑖𝑛 𝑢𝑛𝑖𝑡𝑠

𝑀𝑎𝑟𝑔𝑖𝑛 𝑜𝑓 𝑆𝑎𝑓𝑒𝑡𝑦 𝑎𝑠 𝑎 𝑃𝑒𝑟𝑐𝑒𝑛𝑡𝑎𝑔𝑒

= 𝑀𝑎𝑟𝑔𝑖𝑛 𝑜𝑓 𝑆𝑎𝑓𝑒𝑡𝑦 𝑖𝑛 𝑑𝑜𝑙𝑙𝑎𝑟𝑠𝐸𝑥𝑝𝑒𝑐𝑡𝑒𝑑 𝑆𝑎𝑙𝑒𝑠 𝑖𝑛 𝑑𝑜𝑙𝑙𝑎𝑟𝑠

Learn your uni course in one day. Check spoonfeedme.com for free video summaries, notes and cheat sheets by top students.

CHEAT SHEET