1intangiblesintangibles c hapter 11 an electronic presentation by douglas cloud pepperdine...

TRANSCRIPT

1

IntangiblesIntangiblesIntangiblesIntangibles

Chapter11

An electronic presentation by Douglas Cloud

Pepperdine University

An electronic presentation by Douglas Cloud

Pepperdine University

2

1. Explain the accounting alternatives for intangibles.2. Understand the amortization or impairment of

intangibles.3. Identify research and development costs.4. Explain the conceptual issues for research and

development costs.5. Account for identifiable intangible assets including

patents, copyrights, franchises, computer software costs, and trademarks and tradenames.

ObjectivesObjectivesObjectivesObjectives

ContinuedContinuedContinuedContinued

3

6. Account for unidentifiable intangibles including internally developed and purchased goodwill.

7. Understand the disclosure of intangibles.

8. Explain the conceptual issues regarding intangibles.

9. Estimate the value of goodwill. (Appendix)

ObjectivesObjectives

4

Characteristics that Characteristics that Distinguish IntangiblesDistinguish Intangibles

Characteristics that Characteristics that Distinguish IntangiblesDistinguish Intangibles

• There is generally a higher degree of uncertainty regarding the future benefits that may be derived.

• Their value is subject to wider fluctuations because it may depend to a considerable extent on competitive conditions.

• They may have value only to a particular company.

• Goodwill and intangible assets with indefinite lives are not expensed.

• There is generally a higher degree of uncertainty regarding the future benefits that may be derived.

• Their value is subject to wider fluctuations because it may depend to a considerable extent on competitive conditions.

• They may have value only to a particular company.

• Goodwill and intangible assets with indefinite lives are not expensed.

5

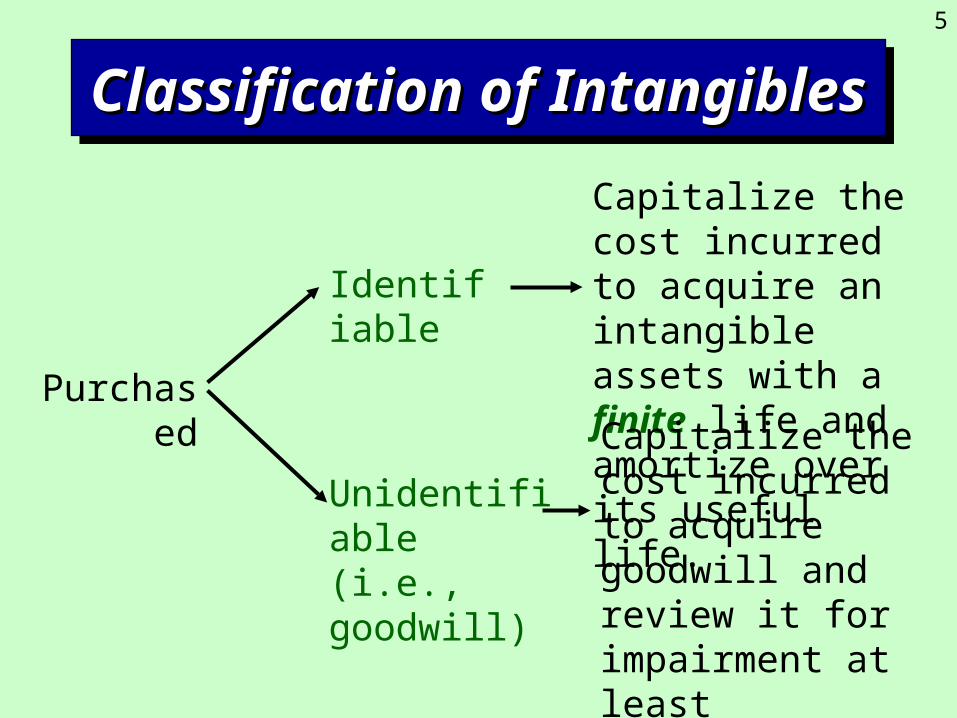

Classification of IntangiblesClassification of IntangiblesClassification of IntangiblesClassification of Intangibles

Purchased

Identifiable

Capitalize the cost incurred to acquire an intangible assets with a finite life and amortize over its useful life.

Unidentifiable (i.e., goodwill)

Capitalize the cost incurred to acquire goodwill and review it for impairment at least annually.

6

Classification of IntangiblesClassification of IntangiblesClassification of IntangiblesClassification of Intangibles

Internally Developed

Identifiable

Unidentifiable

Expense research and development costs as incurred

Capitalize certain costs incurred for an intangible asset with a finite life and amortize over its useful life

Capitalize certain costs incurred for an intangible asset with an infinite life and amortize over its useful life

Expense costs as incurred

7

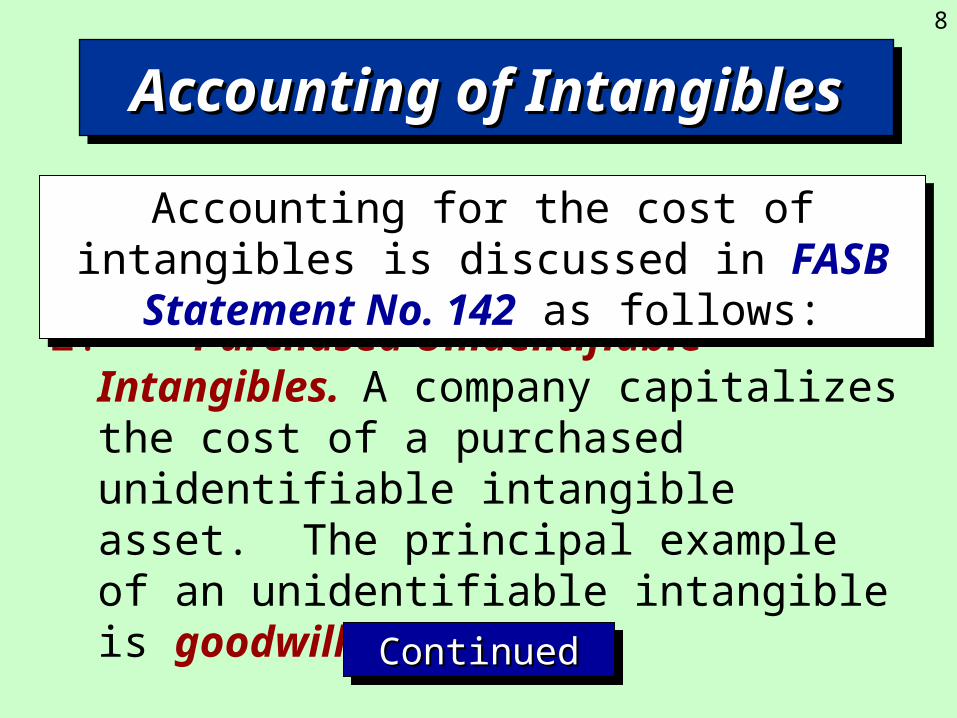

1. Purchased Identifiable Intangibles. A company may purchase an intangible asset from another company. The purchase is handled in the same manner as the acquisition of a single asset, in a group of assets, or in an exchange of similar or dissimilar assets.

Accounting for the cost of intangibles is discussed in FASB Statement No. 142 as follows:

Accounting for the cost of intangibles is discussed in FASB Statement No. 142 as follows:

ContinuedContinuedContinuedContinued

Accounting of IntangiblesAccounting of IntangiblesAccounting of IntangiblesAccounting of Intangibles

8

2. Purchased Unidentifiable Intangibles. A company capitalizes the cost of a purchased unidentifiable intangible asset. The principal example of an unidentifiable intangible is goodwill.

Accounting for the cost of intangibles is discussed in FASB Statement No. 142 as follows:

Accounting for the cost of intangibles is discussed in FASB Statement No. 142 as follows:

ContinuedContinuedContinuedContinued

Accounting of IntangiblesAccounting of IntangiblesAccounting of IntangiblesAccounting of Intangibles

9

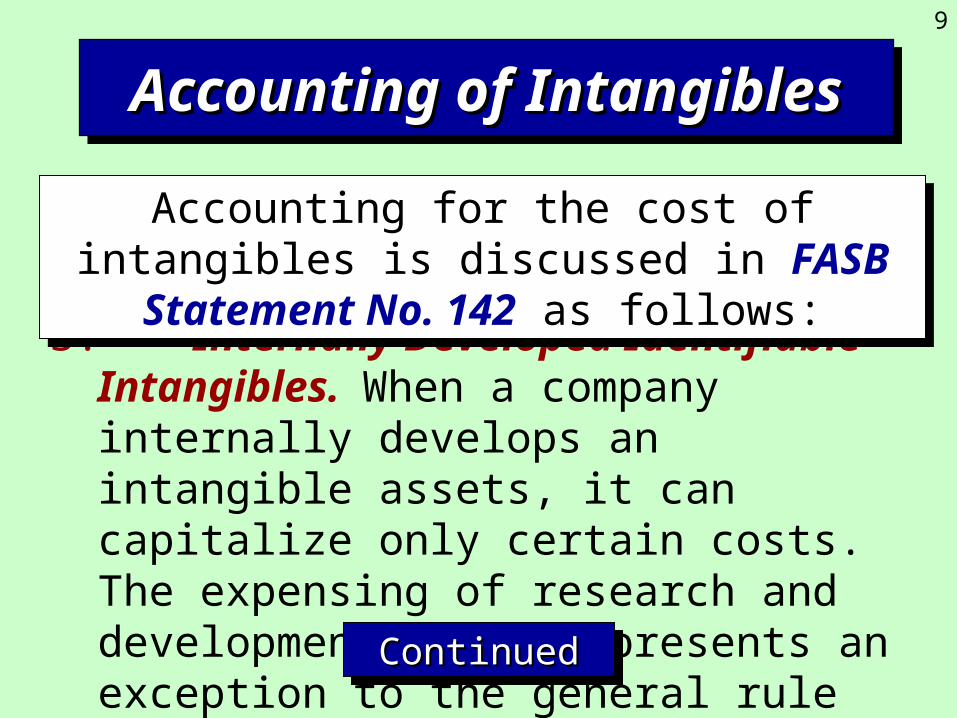

3. Internally Developed Identifiable Intangibles. When a company internally develops an intangible assets, it can capitalize only certain costs. The expensing of research and development costs represents an exception to the general rule of capitalizing of internally developed identifiable intangibles.

Accounting for the cost of intangibles is discussed in FASB Statement No. 142 as follows:

Accounting for the cost of intangibles is discussed in FASB Statement No. 142 as follows:

ContinuedContinuedContinuedContinued

Accounting of IntangiblesAccounting of IntangiblesAccounting of IntangiblesAccounting of Intangibles

10

Accounting of IntangiblesAccounting of IntangiblesAccounting of IntangiblesAccounting of Intangibles

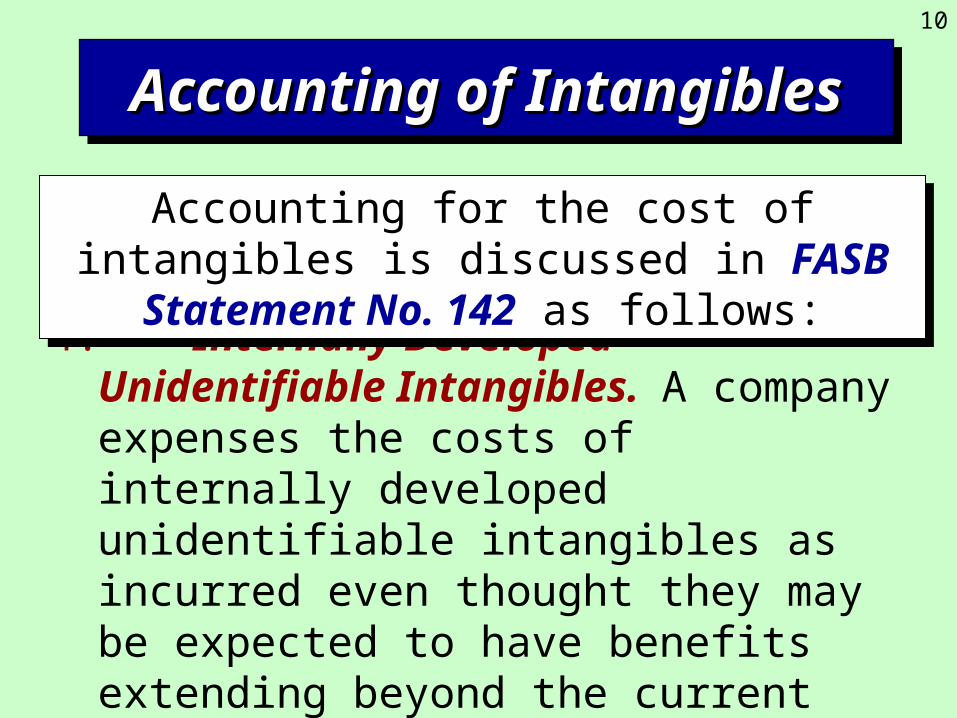

4. Internally Developed Unidentifiable Intangibles. A company expenses the costs of internally developed unidentifiable intangibles as incurred even thought they may be expected to have benefits extending beyond the current period.

Accounting for the cost of intangibles is discussed in FASB Statement No. 142 as follows:

Accounting for the cost of intangibles is discussed in FASB Statement No. 142 as follows:

11

Intangible Assets With a Finite Life Are Amortized.

Intangible Assets With a Finite Life Are Amortized.

The calculation of the amortization of intangible

assets follows the same principles as the depreciation

of tangible assets.

Amortization of IntangiblesAmortization of IntangiblesAmortization of IntangiblesAmortization of Intangibles

12

Amortization of IntangiblesAmortization of IntangiblesAmortization of IntangiblesAmortization of Intangibles

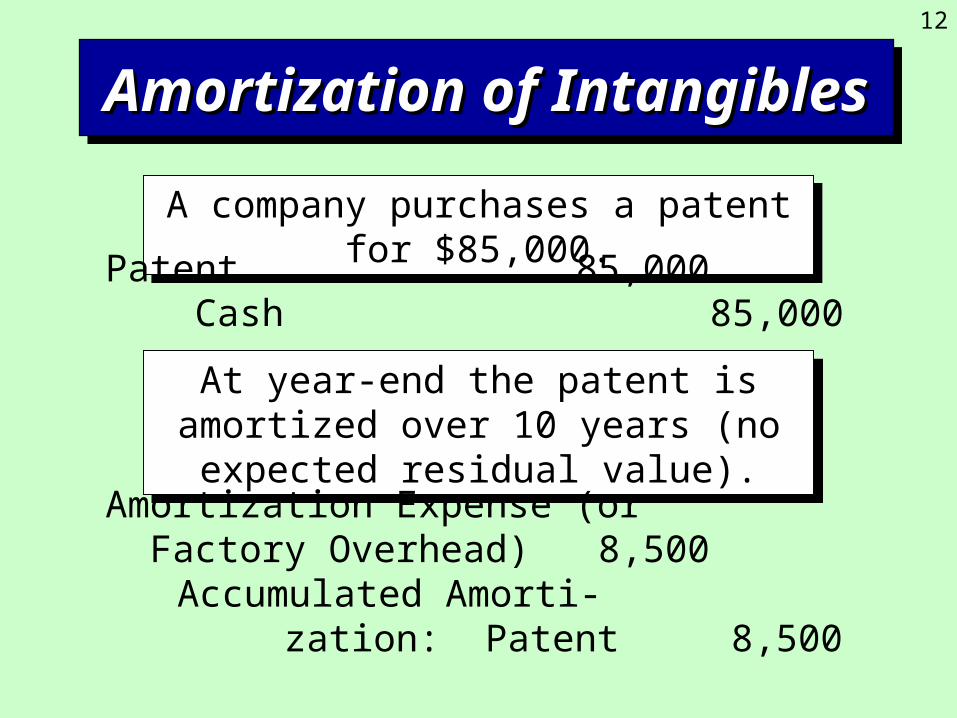

A company purchases a patent for $85,000.A company purchases a patent for $85,000.

Patent 85,000 Cash 85,000

At year-end the patent is amortized over 10 years (no expected residual value).

At year-end the patent is amortized over 10 years (no expected residual value).

Amortization Expense (or Factory Overhead) 8,500

Accumulated Amorti- zation: Patent 8,500

13

Impairment of an IntangibleImpairment of an IntangibleImpairment of an IntangibleImpairment of an Intangible

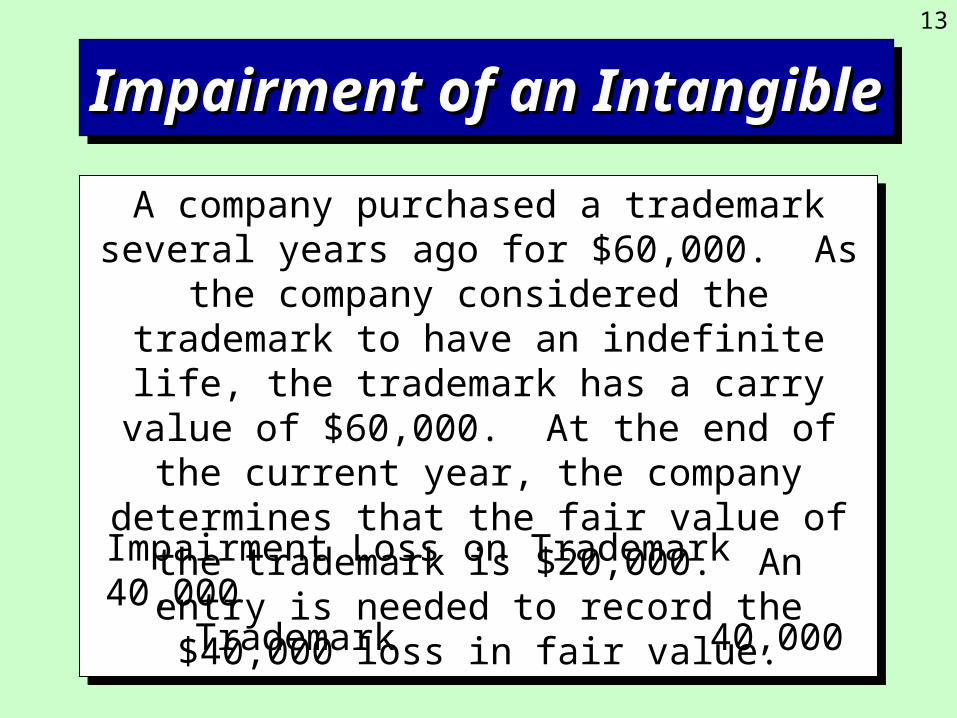

A company purchased a trademark several years ago for $60,000. As the company considered the trademark to have an indefinite life, the trademark

has a carry value of $60,000. At the end of the current year, the company determines that the fair

value of the trademark is $20,000. An entry is needed to record the $40,000 loss in fair value.

A company purchased a trademark several years ago for $60,000. As the company considered the trademark to have an indefinite life, the trademark

has a carry value of $60,000. At the end of the current year, the company determines that the fair

value of the trademark is $20,000. An entry is needed to record the $40,000 loss in fair value.

Impairment Loss on Trademark 40,000 Trademark 40,000

14

Research and Development CostsResearch and Development CostsResearch and Development CostsResearch and Development Costs

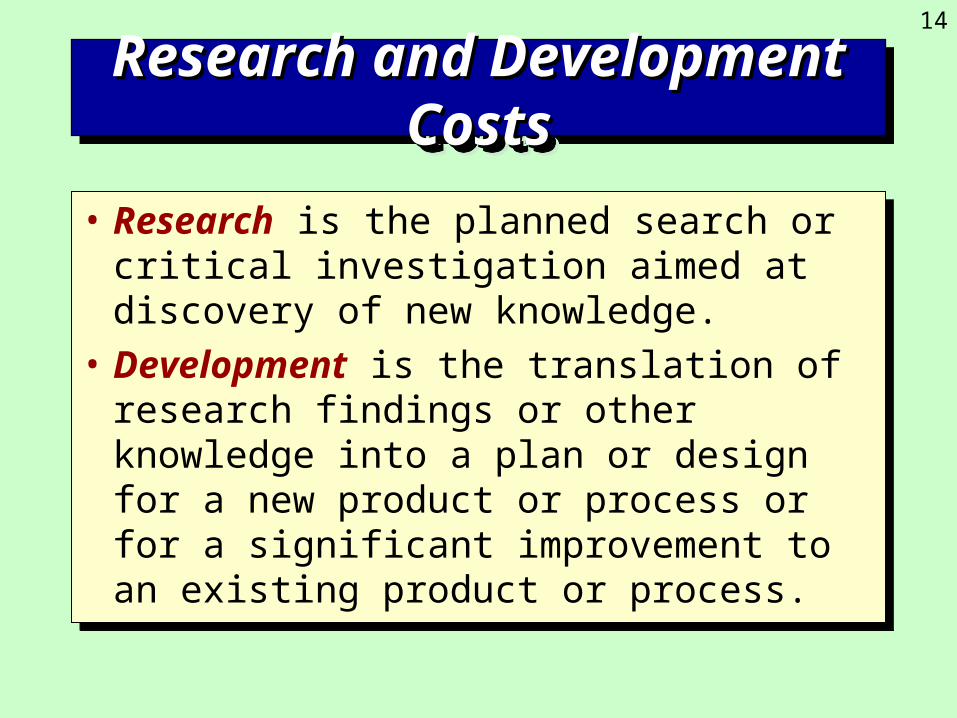

• Research is the planned search or critical investigation aimed at discovery of new knowledge.

• Development is the translation of research findings or other knowledge into a plan or design for a new product or process or for a significant improvement to an existing product or process.

• Research is the planned search or critical investigation aimed at discovery of new knowledge.

• Development is the translation of research findings or other knowledge into a plan or design for a new product or process or for a significant improvement to an existing product or process.

15

Research and Development CostsResearch and Development CostsResearch and Development CostsResearch and Development Costs

Costs associated with activities excluded

from R&D are either expensed or

capitalized according to normal

capitalization criteria.

Costs associated with activities excluded

from R&D are either expensed or

capitalized according to normal

capitalization criteria.

16

Materials, equipment, and facilities Personnel Intangibles purchased from others Contract services Indirect costs—R&D includes a

reasonable allocation of indirect costs.

Research and Development CostsResearch and Development CostsResearch and Development CostsResearch and Development Costs

Expenditures for the following elements of R&D activities are included in R&D costs and thus expensed as incurred:

17

Research and Development CostsResearch and Development CostsResearch and Development CostsResearch and Development Costs

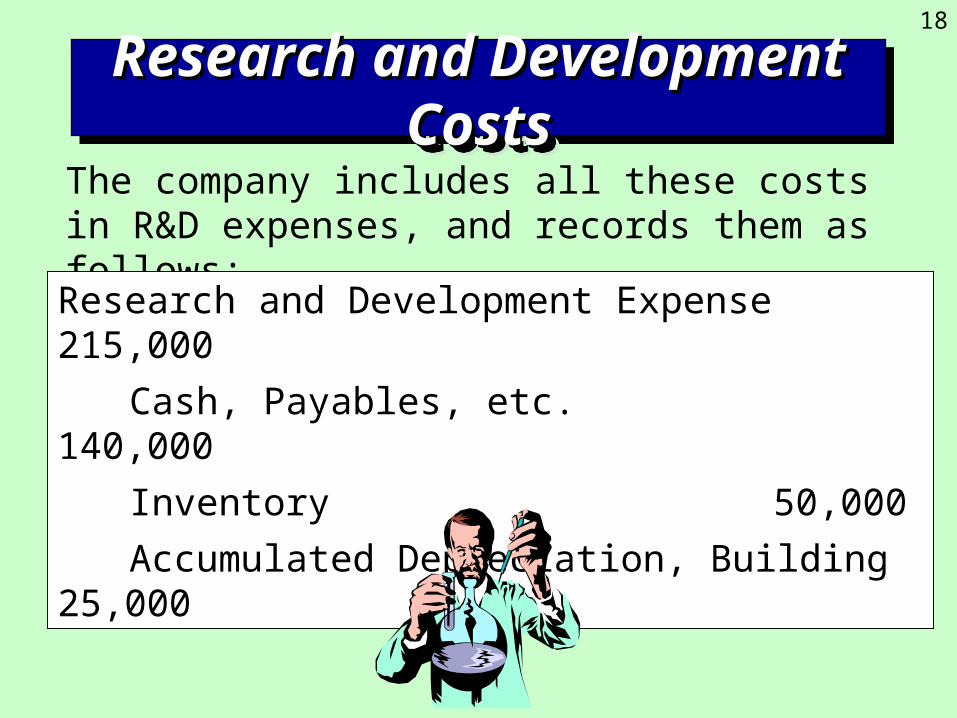

Kent Company incurred the following costs for R&D activities:

Materials used from inventory $50,000Wages and salaries 90,000Allocation of general and administrative

costs 20,000Depreciation on building housing R&D

activities 25,000Machine purchased for R&D project that

has no alternative future uses 30,000

ContinuedContinuedContinuedContinued

18

Research and Development CostsResearch and Development CostsResearch and Development CostsResearch and Development Costs

The company includes all these costs in R&D expenses, and records them as follows:

Research and Development Expense 215,000

Cash, Payables, etc. 140,000

Inventory 50,000

Accumulated Depreciation, Building 25,000

19

Identifiable Intangible AssetsIdentifiable Intangible AssetsIdentifiable Intangible AssetsIdentifiable Intangible Assets

Cost of Intangibles

Cost of Intangibles Expense

In period cost incurred Identifiable Intangible

Assets That Are Typically AmortizedPatentsCopyrightsFranchisesComputer Software CostsLeasehold Improvements

Amortize over service life

ContinuedContinuedContinuedContinued

R & DR & D

20

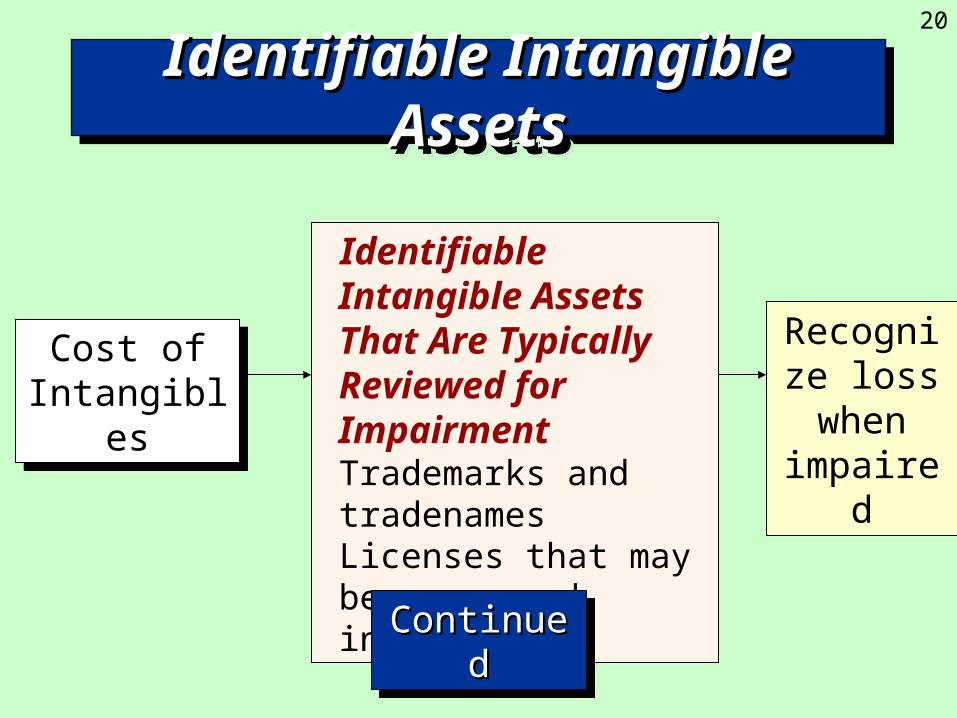

Identifiable Intangible AssetsIdentifiable Intangible AssetsIdentifiable Intangible AssetsIdentifiable Intangible Assets

Cost of Intangibles

Cost of Intangibles

Identifiable Intangible Assets That Are Typically Reviewed for ImpairmentTrademarks and tradenamesLicenses that may be

renewed indefinitely

Recognize loss when impaired

ContinuedContinuedContinuedContinued

21

Identifiable Intangible AssetsIdentifiable Intangible AssetsIdentifiable Intangible AssetsIdentifiable Intangible Assets

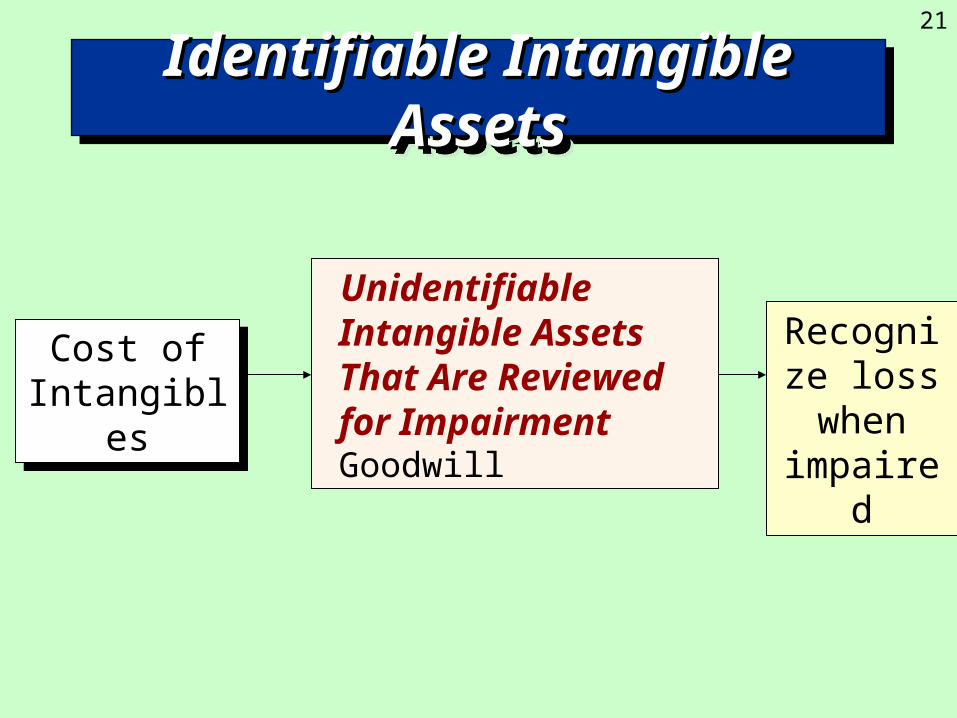

Cost of Intangibles

Cost of Intangibles

Unidentifiable Intangible Assets That Are Reviewed for ImpairmentGoodwill

Recognize loss when impaired

22

PatentsPatentsPatentsPatents

A patent is an exclusive right granted by the federal

government giving the owner control…

A patent is an exclusive right granted by the federal

government giving the owner control…

…of the manufacture, sale, or other use of an invention for 20 years from the date

of filing.

…of the manufacture, sale, or other use of an invention for 20 years from the date

of filing.

23

PatentsPatentsPatentsPatents

A company can capitalize the costs of successfully defending the legal validity of a patent. If the suit is lost, all legal costs are expensed.

A company can capitalize the costs of successfully defending the legal validity of a patent. If the suit is lost, all legal costs are expensed.

24

CopyrightsCopyrightsCopyrightsCopyrights

©

A copyright is a grant by the federal government to publish, sell or otherwise control literary or artistic products for

the life of the author plus 70 year.

A copyright is a grant by the federal government to publish, sell or otherwise control literary or artistic products for

the life of the author plus 70 year.

BooksMusic Films

25

FranchisesFranchisesFranchisesFranchises

Franchises are agreements entered into by two parties in which, for a fee, one party gives the

other party the right to perform certain functions or sell certain products or services.

Burger KingMcDonald’s

Midas MufflerKFC

26

Computer Software CostsComputer Software CostsComputer Software CostsComputer Software Costs

Technological Feasibility

General Release

R & D Expense Capitalize Expense

Technological feasibility is established either on the date the company completes a detail program design or, in its absence,

when it completes a working model of the product.

27

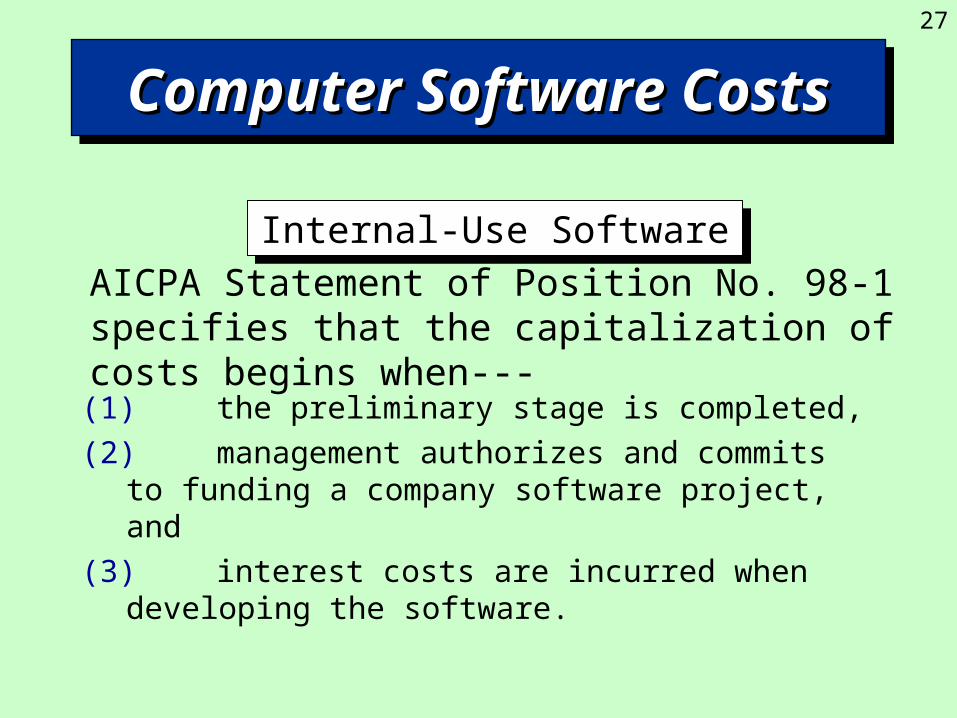

(1) the preliminary stage is completed,

(2) management authorizes and commits to funding a company software project, and

(3) interest costs are incurred when developing the software.

Computer Software CostsComputer Software CostsComputer Software CostsComputer Software Costs

Internal-Use SoftwareInternal-Use Software

AICPA Statement of Position No. 98-1 specifies that the capitalization of costs begins when---

28

Trademarks and TradenamesTrademarks and TradenamesTrademarks and TradenamesTrademarks and Tradenames

Registration of a trademark or tradename with the U.S. Patent Office establishes a right to exclusive use of a name, symbol, or other device used for product identification for 20 years. The right is renewable

indefinitely as long as it is used continuously.

29

• Deferred charges (a catch-all category in which several individually immaterial items are accumulated)

• Organization costs

Other IntangiblesOther IntangiblesOther IntangiblesOther Intangibles

Legal fees, stock certificate costs, underwriting fees, accounting fees, promotional fees

30

GoodwillGoodwillGoodwillGoodwill

Purchased goodwill arises when a company

is acquired. It is the difference between the purchase price of the

acquired company as a whole and the fair

value of the reported identifiable net assets.

Purchased goodwill arises when a company

is acquired. It is the difference between the purchase price of the

acquired company as a whole and the fair

value of the reported identifiable net assets.

31

GoodwillGoodwillGoodwillGoodwill

Sara Company purchases all the assets of Trevor Company for $790,000 cash and Trevor Company is dissolved.

Trevor Company’s identifiable assets had a fair value of $920,000 and its liabilities totaled $200,000.

Sara Company purchases all the assets of Trevor Company for $790,000 cash and Trevor Company is dissolved.

Trevor Company’s identifiable assets had a fair value of $920,000 and its liabilities totaled $200,000.

Assets 920,000Goodwill 70,000 Liabilities 200,000 Cash 790,000

Individual assets and liabilities Individual assets and liabilities actually would be debited or credited.actually would be debited or credited.

32

Impairment of GoodwillImpairment of GoodwillImpairment of GoodwillImpairment of Goodwill

A company must review its goodwill for

impairment annually at the reporting unit level.

A company must review its goodwill for

impairment annually at the reporting unit level.

33

Impairment of GoodwillImpairment of GoodwillImpairment of GoodwillImpairment of Goodwill

A company must also review its goodwill for impairment whenever events or changes in circumstances occur that would more-likely-than-

not reduce the fair value of the goodwill below its carrying value.

A company must also review its goodwill for impairment whenever events or changes in circumstances occur that would more-likely-than-

not reduce the fair value of the goodwill below its carrying value.

34

Impairment of GoodwillImpairment of GoodwillImpairment of GoodwillImpairment of Goodwill

The Kent Company acquired the Devon Company as a subsidiary several years ago. The Devon Company has a

book value of $3.6 million, including goodwill of $400,000. Kent Company estimates that its fair value is $3 million. If

Kent Company allocates $2.7 million of the fair market value to Devon Company’s identifiable assets and liabilities,

this means that $300,000 is implied for goodwill. Thus, there has been an impairment loss of $100,000.

Impairment Loss on Goodwill 100,000

Goodwill100,000

35

Disclosure of IntangiblesDisclosure of IntangiblesDisclosure of IntangiblesDisclosure of Intangibles

FASB Statement No. 142 requires a company to disclose certain information about its intangible assets, in either the financial statement or it notes, including:

FASB Statement No. 142 requires a company to disclose certain information about its intangible assets, in either the financial statement or it notes, including:

1. In the period it acquires intangible assets:a. The cost of any intangible asset acquired, separated

into categories.b. For assets subject to amortization, the residual

value and the weighted-average amortization expense for the next five years.

c. The cost of any R&D acquired and written off, and where it is included in the income statement.

ContinuedContinuedContinuedContinued

36

Disclosure of IntangiblesDisclosure of IntangiblesDisclosure of IntangiblesDisclosure of Intangibles

FASB Statement No. 142 requires a company to disclose certain information about its intangible assets, in either the financial statement or it notes, including:

FASB Statement No. 142 requires a company to disclose certain information about its intangible assets, in either the financial statement or it notes, including:

2. In each period for which it presents a balance sheet:a. For intangible assets that are amortized, the total

cost, the accumulated amortization, the amortization expense, and the estimated amortization expense for the next five years.

b. For intangible assets that are not amortized, the total cost and the cost of each major intangible asset class.

ContinuedContinuedContinuedContinued

37

Disclosure of IntangiblesDisclosure of IntangiblesDisclosure of IntangiblesDisclosure of Intangibles

FASB Statement No. 142 requires a company to disclose certain information about its intangible assets, in either the financial statement or it notes, including:

FASB Statement No. 142 requires a company to disclose certain information about its intangible assets, in either the financial statement or it notes, including:

2. In each period for which it presents a balance sheet:c. For goodwill, the amount of goodwill acquired, the

amount of any impairment losses recognized, and the amount of goodwill included in the disposal of a reporting unit.

d. For any intangible asset impairment, the facts and circumstances leading to the impairment, the amount of the loss, and the method used.

38

Conceptual IssuesConceptual IssuesConceptual IssuesConceptual Issues

Expensing internally generated goodwill is justified on the basis that measuring the cost of internally generated goodwill with a reasonable degree of

reliability is very difficult.

Expensing internally generated goodwill is justified on the basis that measuring the cost of internally generated goodwill with a reasonable degree of

reliability is very difficult.

Capitalization of internally generated goodwill would require amortization. It would be very

difficult to identify the revenues generated and therefore to decide over which periods, and by

which method, to match the amortization expenses against the benefits.

Capitalization of internally generated goodwill would require amortization. It would be very

difficult to identify the revenues generated and therefore to decide over which periods, and by

which method, to match the amortization expenses against the benefits.

39

Click here to skip Appendix material.

Appendix: Estimating the

Value of Goodwill

Appendix: Estimating the

Value of Goodwill

40

Steps Used In Estimating the Steps Used In Estimating the Value of Goodwill (AppendixValue of Goodwill (Appendix)Steps Used In Estimating the Steps Used In Estimating the Value of Goodwill (AppendixValue of Goodwill (Appendix)

1. Estimate the average future earnings from the identifiable net assets.

2. Estimate the rate of return that should be earned by the company on its identifiable net assets.

3. Estimate the current fair value of the identifiable net assets.

4. Compute the estimated excess annual earnings.

ContinuedContinuedContinuedContinued

41

Steps Used In Estimating the Steps Used In Estimating the Value of Goodwill (Appendix)Value of Goodwill (Appendix)Steps Used In Estimating the Steps Used In Estimating the Value of Goodwill (Appendix)Value of Goodwill (Appendix)

5. Estimate the expected life of the excess annual earnings.

6. Compute the present value of the estimated excess annual earnings.

7. Compute the total value of the company being considered for purchase.

8. Apply sensitivity analysis.

Two additional steps may follow the calculation of the value of goodwill:

Two additional steps may follow the calculation of the value of goodwill:

42

Steps Used In Estimating the Steps Used In Estimating the Value of Goodwill (Appendix)Value of Goodwill (Appendix)Steps Used In Estimating the Steps Used In Estimating the Value of Goodwill (Appendix)Value of Goodwill (Appendix)

STEP 1: Estimate the average future earnings.

1. Eliminate unusual gains or loss, extraordinary items, the results of discontinued operations, and the effects of changes in accounting principles.

2. Adjust for differences in accounting principles.

Select a number of years to determine the trend of the firm’s earnings.

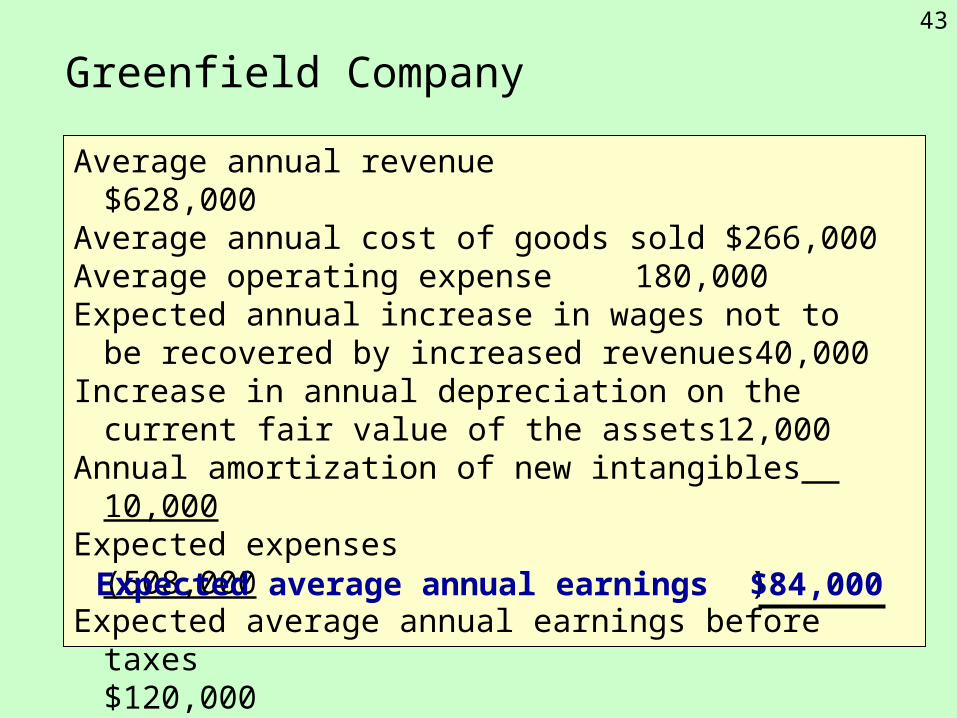

43

Average annual revenue $628,000 Average annual cost of goods sold $266,000Average operating expense 180,000Expected annual increase in wages not to

be recovered by increased revenues 40,000Increase in annual depreciation on the

current fair value of the assets 12,000Annual amortization of new intangibles 10,000Expected expenses (508,000

)Expected average annual earnings before taxes $120,000 Estimated income taxes (30%) (36,000

)

Greenfield Company

Expected average annual earnings $84,000

44

Steps Used In Estimating the Steps Used In Estimating the Value of Goodwill (Appendix)Value of Goodwill (Appendix)Steps Used In Estimating the Steps Used In Estimating the Value of Goodwill (Appendix)Value of Goodwill (Appendix)

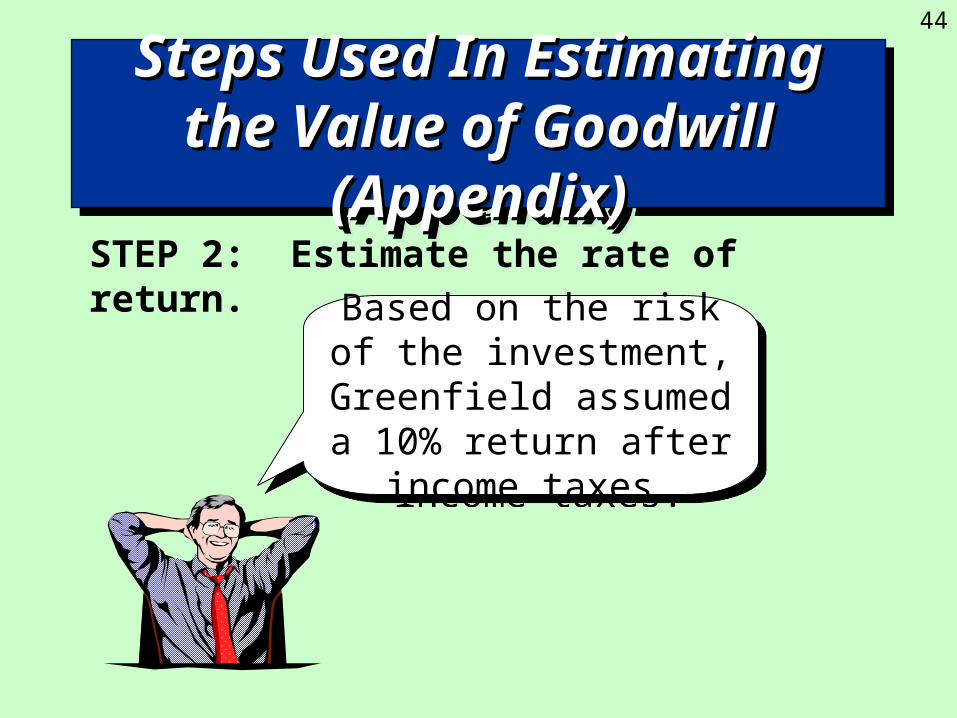

STEP 2: Estimate the rate of return.

Based on the risk of the investment, Greenfield assumed a 10% return

after income taxes.

Based on the risk of the investment, Greenfield assumed a 10% return

after income taxes.

45

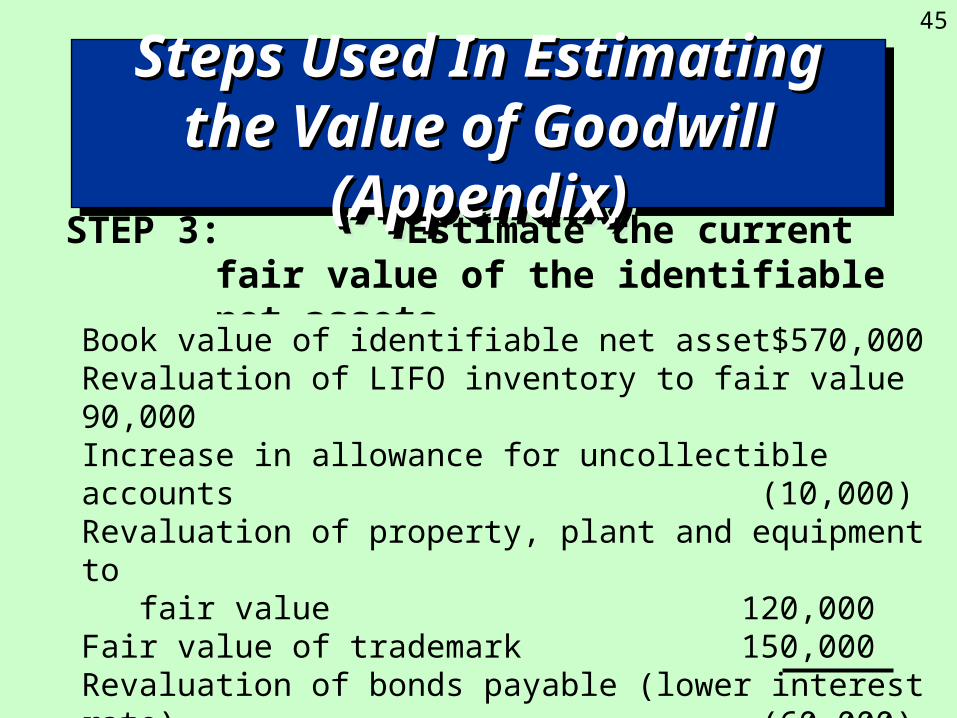

Steps Used In Estimating the Steps Used In Estimating the Value of Goodwill (Appendix)Value of Goodwill (Appendix)Steps Used In Estimating the Steps Used In Estimating the Value of Goodwill (Appendix)Value of Goodwill (Appendix)

STEP 3: Estimate the current fair value of the identifiable net assets.

Book value of identifiable net asset $570,000 Revaluation of LIFO inventory to fair value 90,000 Increase in allowance for uncollectible accounts (10,000)Revaluation of property, plant and equipment to fair value 120,000 Fair value of trademark 150,000 Revaluation of bonds payable (lower interest rate) (60,000)Unfunded projected benefit obligations of pension (140,000)Current fair value of identifiable net assets $720,000

46

Steps Used In Estimating the Steps Used In Estimating the Value of Goodwill (Appendix)Value of Goodwill (Appendix)Steps Used In Estimating the Steps Used In Estimating the Value of Goodwill (Appendix)Value of Goodwill (Appendix)

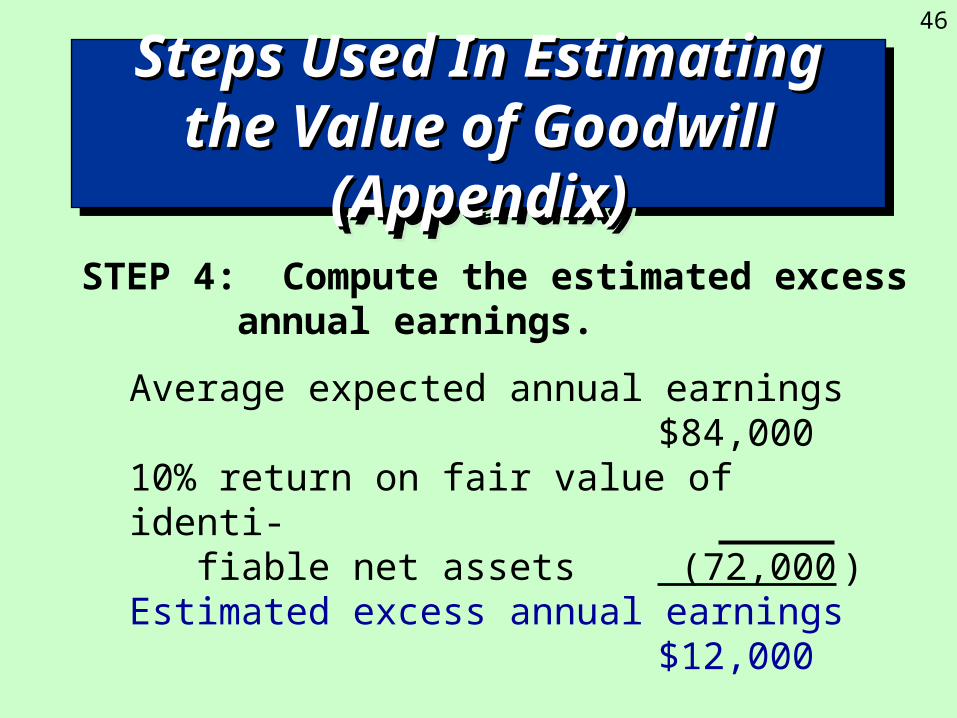

STEP 4: Compute the estimated excess annual earnings.

Average expected annual earnings $84,000 10% return on fair value of identi- fiable net assets (72,000 )Estimated excess annual earnings $12,000

47

Steps Used In Estimating the Steps Used In Estimating the Value of Goodwill (Appendix)Value of Goodwill (Appendix)Steps Used In Estimating the Steps Used In Estimating the Value of Goodwill (Appendix)Value of Goodwill (Appendix)

STEP 5: Estimate the expected life of excess annual earnings.

Greenfield Company estimates that the excess annual earnings

will last for ten years.

48

Steps Used In Estimating the Steps Used In Estimating the Value of Goodwill (Appendix)Value of Goodwill (Appendix)Steps Used In Estimating the Steps Used In Estimating the Value of Goodwill (Appendix)Value of Goodwill (Appendix)

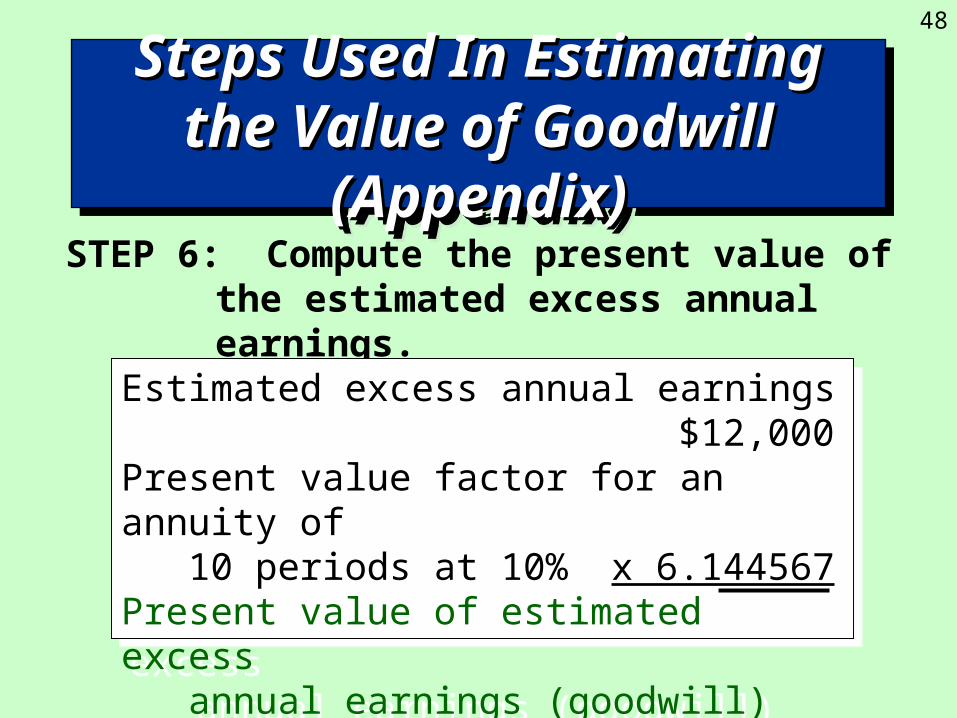

STEP 6: Compute the present value of the estimated excess annual earnings.

Estimated excess annual earnings $12,000Present value factor for an annuity of 10 periods at 10% x 6.144567Present value of estimated excess annual earnings (goodwill) $73,735

Estimated excess annual earnings $12,000Present value factor for an annuity of 10 periods at 10% x 6.144567Present value of estimated excess annual earnings (goodwill) $73,735

49

Steps Used In Estimating the Steps Used In Estimating the Value of Goodwill (Appendix)Value of Goodwill (Appendix)Steps Used In Estimating the Steps Used In Estimating the Value of Goodwill (Appendix)Value of Goodwill (Appendix)

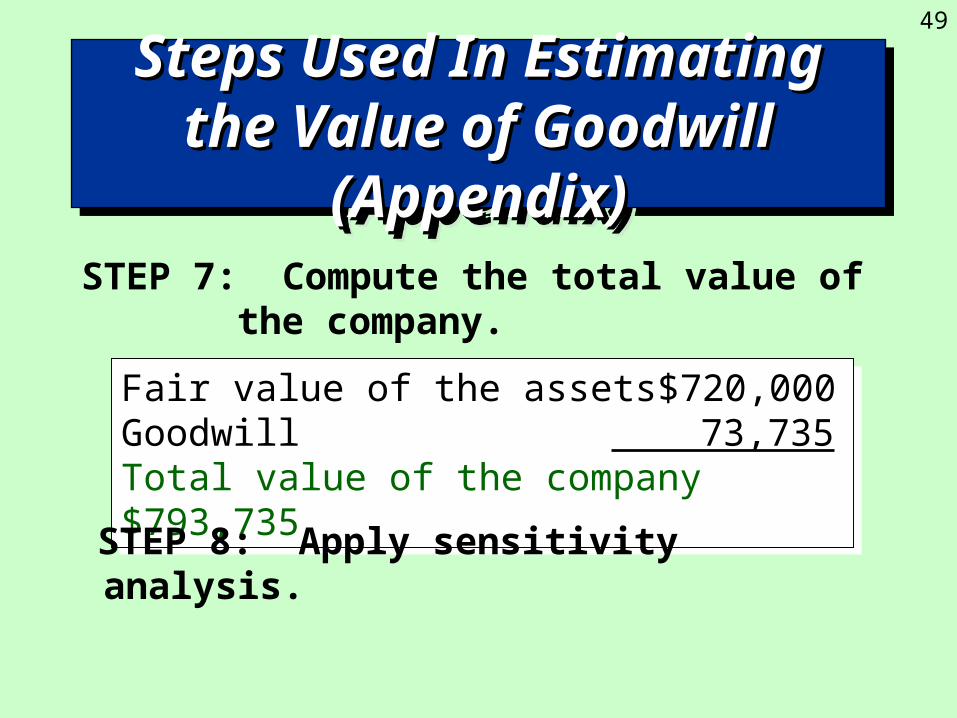

STEP 7: Compute the total value of the company.

Fair value of the assets $720,000Goodwill 73,735Total value of the company $793,735

Fair value of the assets $720,000Goodwill 73,735Total value of the company $793,735

STEP 8: Apply sensitivity analysis.

50

Chapter11

The EndThe EndThe EndThe End

51