1998 handbook - college of intensive care medicine

TRANSCRIPT

Prepared For:

Prepared By:

,

IMRB International

February, 2009

INVESTMENT POTENTIAL IN RETAIL

SECTOR OF INDIA

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 2

PREFACE

Thai-Indian business relations have improved considerably over the past decade.

Thailand and India are close to concluding a Free Trade Agreement (FTA) covering trade

in goods by 2010. The Free Trade Agreement between Thailand and India is expected to

improve trade relations between the two countries further. The FTA covering trade in

goods would lead to long term mutual benefits in trade and investment and the

partnership would be expanded further to cover technology knowledge and expertise

India's primary imports from Thailand are machinery, electronic appliances, textiles,

plastic material, transport equipment, vegetable oil and latex. The major items of imports

under FTA are polycarbonate, cathode-ray tubes, color-TVs, air conditioners and

Aluminum products. Thailand‘s main imports from India are jewelry, gemstones, steel,

pharmaceuticals and ferrous metal ores.

India's trade with Thailand could touch USD 7 billion by 2010-11 propelled by a

doubling in transaction under Free Trade Agreement (FTA). The EHS was implemented

on September 1, 2004, under which tariffs on 82 items were to be phased out by

September 1, 2006 by both the sides.

The trade between Thailand and India is estimated to be US $ 7 billion by 2010-11 from

US $ 2.2 billion in 2005-06.

The total trade of 82 items under Early Harvest Scheme (EHS) of the FTA was increased

by over 140 percent to about US $ 358.63 million in 2005-06 from US $ 149 million in

2003-04. The share of these 82 items in India-Thailand trade increased from 10.34

percent in 2003-04 to 15.68 percent in 2005-06.

Thailand‘s export to India of the identified 82 EHS items was increased from US $ 84.64

million to US $ 275 million during the period from 2003 – 04 to 2005 – 06. During the

same time, India‘s export to Thailand of these items increased from US $ 64.28 million to

US $ 83.03 million during the same period.

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 3

In 2007, Thailand‘s export for these 82 items was US $ 406.31 million. Due the FTA

between two countries, Thailand is able to manage the trade surplus of US $ 598 in 2007

in bilateral trade between Thailand and India.

With significant potential for growth of business between the two countries, the Ministry

of Commerce, Thailand and Royal Thai Embassy would like to understand the

investment potential in the following two sectors:-

1. Retail in India (with focus on Apparels & Fashion Accessories, Footwear, Food &

Grocery, Furniture & Furnishing, Personal Care, and Consumer Durables as

product verticals)

2. Logistics in India

In order to understand the trade potential across the above categories, the Ministry of

Commerce, Thailand and Royal Thai Embassy has commissioned Business and Industrial

Research Division (BIRD) of IMRB International to avail its research based consultancy

services.

Report for both the product categories are being submitted separately in two different

modules.

The following report ‘Investment Opportunities in Retail Sector of India’ is based on

the study conducted in Retail sector of India.

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 4

TABLE OF CONTENT

1. EXECUTIVE SUMMARY................................................................................................................. 8

2. RETAIL SECTOR IN INDIA ...........................................................................................................16

2.1. EMERGENCE OF MODERN (ORGANIZED) RETAIL IN INDIA ..........................................................16

2.2. INDIA: A PREFERRED RETAIL DESTINATION ...............................................................................17

2.3. KEY GROWTH DRIVERS FOR MODERN RETAIL IN INDIA .............................................................18

2.4. SIZE AND GROWTH OF RETAIL IN INDIA ......................................................................................21

2.4.1. Product Category-wise Break-up of Retail Market ...............................................................21

2.4.2. Organized Retail as Part of Total Retail ...............................................................................22

2.4.3. Product Category-wise Break-up of Organized Retail ..........................................................22

2.4.4. Category-wise Penetration of Organized Retail ....................................................................23

2.4.5. Food & Beverage based Servicing Retail in India ................................................................24

3. MODERN RETAIL STORE FORMATS ........................................................................................26

3.1. PREMIUM LIFESTYLE RETAILING ................................................................................................27

3.2. LIFESTYLE RETAILING ................................................................................................................28

3.2.1. Departmental Stores ..............................................................................................................28

3.2.2. Apparel and Fashion Stores ..................................................................................................28

3.3. VALUE RETAILING .......................................................................................................................29

3.3.1. Supermarkets .........................................................................................................................29

3.3.2. Hypermarkets.........................................................................................................................30

3.4. OTHER RETAIL FORMATS ............................................................................................................32

3.4.1. Specialty Stores......................................................................................................................32

3.4.2. Discount Stores/ factory outlets .............................................................................................33

3.4.3. Airport Retailing ....................................................................................................................34

3.4.4. Online, Telephone and Catalogue Buying .............................................................................34

3.4.5. Shopping Malls ......................................................................................................................34

3.4.6. Food Outlets as part of Modern Retail ..................................................................................36

4. CASH AND CARRY STORES .........................................................................................................38

4.1. GLOBAL RETAILERS ENTRY THROUGH CASH & CARRY FORMAT ...............................................38

4.2. DOMESTIC PLAYERS NOT FAR BEHIND .......................................................................................39

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 5

5. SUPPLY CHAIN INSIGHTS ...........................................................................................................40

5.1. SUPPLY CHAIN MODEL FOR MODERN RETAIL OUTLETS .............................................................40

5.1.1. Level 1: Product Sourcing .....................................................................................................41

5.1.2. Methods of Procurement........................................................................................................42

5.1.3. Level II: Storage and Distribution .........................................................................................46

5.1.4. Level III: Retail Stores ...........................................................................................................47

5.2. SUPPLY CHAIN FOR FOOD & BEVERAGE SERVICING RETAIL IN INDIA ........................................48

5.2.1. Level I: Suppliers ...................................................................................................................48

5.2.2. Level II: Distribution .............................................................................................................49

5.2.3. Level III: Outlets ....................................................................................................................50

5.3. LOGISTIC FACILITIES FOR RETAIL INDUSTRY IN INDIA ................................................................51

5.3.1. Cost of Logistics in Indian Retail ..........................................................................................52

6. RENT STRUCTURE IN RETAIL ...................................................................................................53

6.1. PREVALENT RENTAL MODELS IN INDIA ......................................................................................53

6.1.1. Fixed Lease Rental Model .....................................................................................................53

6.1.2. Revenue Sharing Model .........................................................................................................53

6.2. MAJOR COMPONENTS OF OCCUPANCY COSTS IN INDIA ..............................................................53

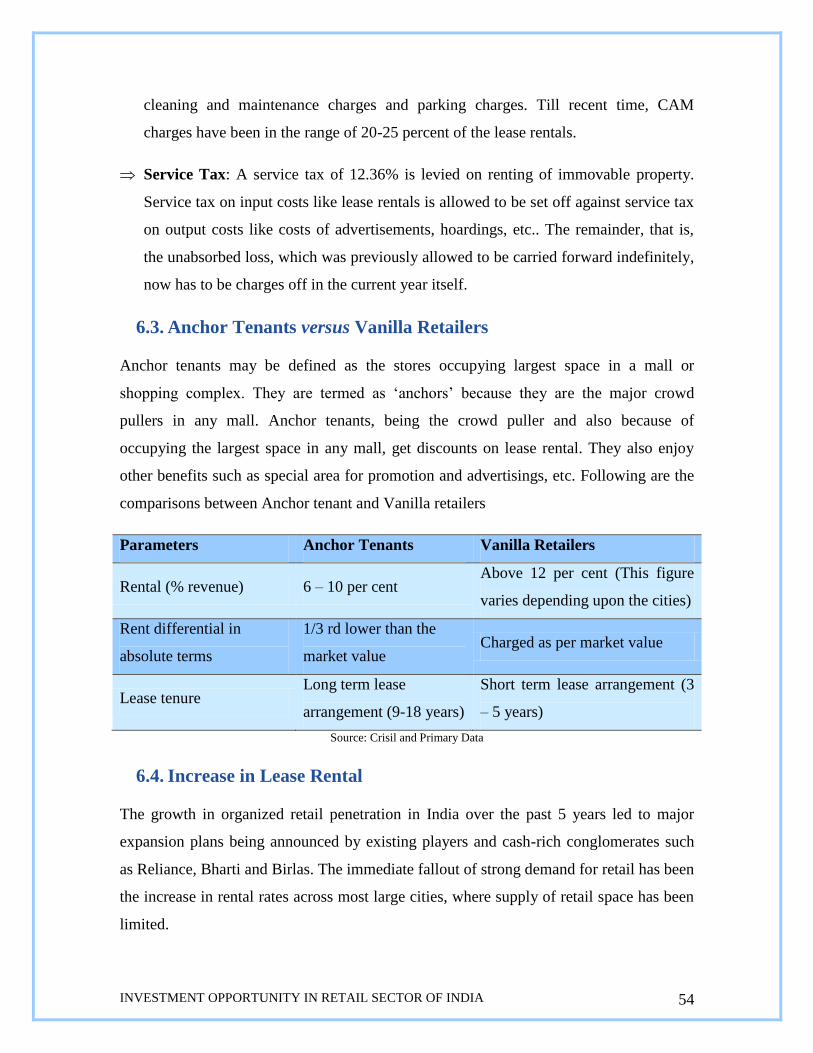

6.3. ANCHOR TENANTS VERSUS VANILLA RETAILERS ........................................................................54

6.4. INCREASE IN LEASE RENTAL .......................................................................................................54

6.5. ECONOMIC SLOWDOWN AND CHANGES IN STRATEGIES OF RETAILERS .......................................55

6.6. EXCESS SUPPLY OF RETAIL SPACE IN PIPELINE ...........................................................................56

6.7. CHANGING RENTAL MODELS ......................................................................................................56

6.8. THE ROAD AHEAD ......................................................................................................................57

7. PROFITABILITY ACROSS VERTICALS ....................................................................................58

7.1. A COMPARISON BETWEEN APPARELS, FOOD & GROCERY AND HOME APPLIANCES ....................58

8. LEADING RETAIL COMPANIES OF INDIA ..............................................................................61

8.1. STRENGTHS AND WEAKNESSES OF KEY ORGANIZED PLAYERS ...................................................62

9. INDIAN RETAIL INDUSTRY ANALYSIS ....................................................................................70

9.1. INDIAN RETAIL MARKET ANALYSIS BASED ON NINE FORCES MODEL ........................................70

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 6

9.1.1. Threat of New Entrants (High) ..............................................................................................70

9.1.2. Threat of Substitutes (High) ...................................................................................................74

9.1.3. Bargaining Power of Suppliers..............................................................................................74

9.1.4. Bargaining Power of Buyers (High) ......................................................................................76

9.1.5. Competitive Rivalry (Medium)...............................................................................................77

9.1.6. Government (Legal and Political Shifts) ...............................................................................78

9.1.7. Social Shifts ...........................................................................................................................79

9.1.8. Technological Shifts ..............................................................................................................80

9.1.9. Economic/ International Shifts ..............................................................................................80

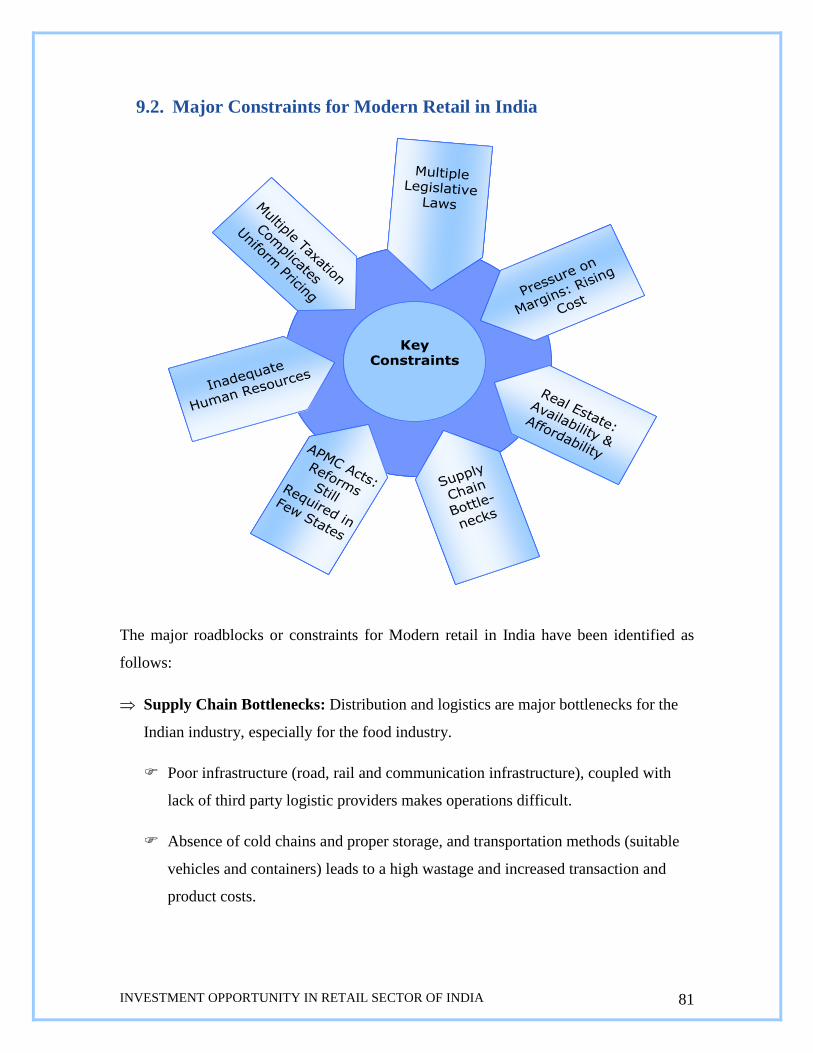

9.2. MAJOR CONSTRAINTS FOR MODERN RETAIL IN INDIA ................................................................81

9.3. EMERGING TRENDS IN THE INDIAN RETAIL INDUSTRY ................................................................85

9.4. CRITICAL SUCCESS FACTORS IN RETAIL .....................................................................................89

10. RETAILERS’ PERCEPTION ABOUT THAI IMPORTS........................................................92

10.1. APPARELS ...................................................................................................................................92

10.2. PLASTIC GOODS ..........................................................................................................................92

10.3. HOME DÉCOR ITEMS & ELECTRIC GOODS ..................................................................................93

10.4. FURNITURE..................................................................................................................................93

10.5. FOOTWEAR ..................................................................................................................................94

10.6. PROCESSED FOOD .......................................................................................................................94

10.7. PERSONAL CARE ITEMS...............................................................................................................96

10.8. OTHER FACTORS RELATED TO THAILAND....................................................................................96

11. POSSIBLE WAYS FOR ENTRY OF FOREIGN RETAILERS IN INDIA ............................97

11.1. MANUFACTURING AND SOURCING...............................................................................................97

11.2. CASH-AND-CARRY OPERATION....................................................................................................97

11.3. FRANCHISING ..............................................................................................................................97

11.4. TEST MARKETING .......................................................................................................................98

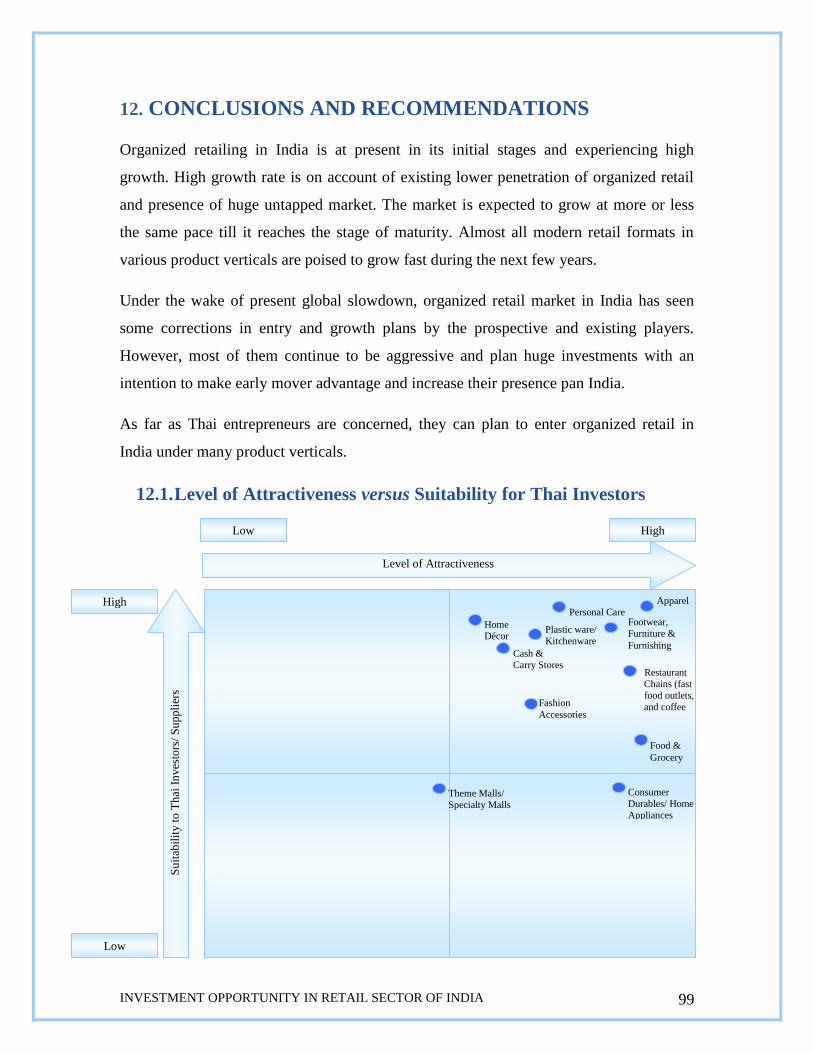

12. CONCLUSIONS AND RECOMMENDATIONS ......................................................................99

12.1. LEVEL OF ATTRACTIVENESS VERSUS SUITABILITY FOR THAI INVESTORS ....................................99

12.2. PROPOSED ENTRY STRATEGY ...................................................................................................101

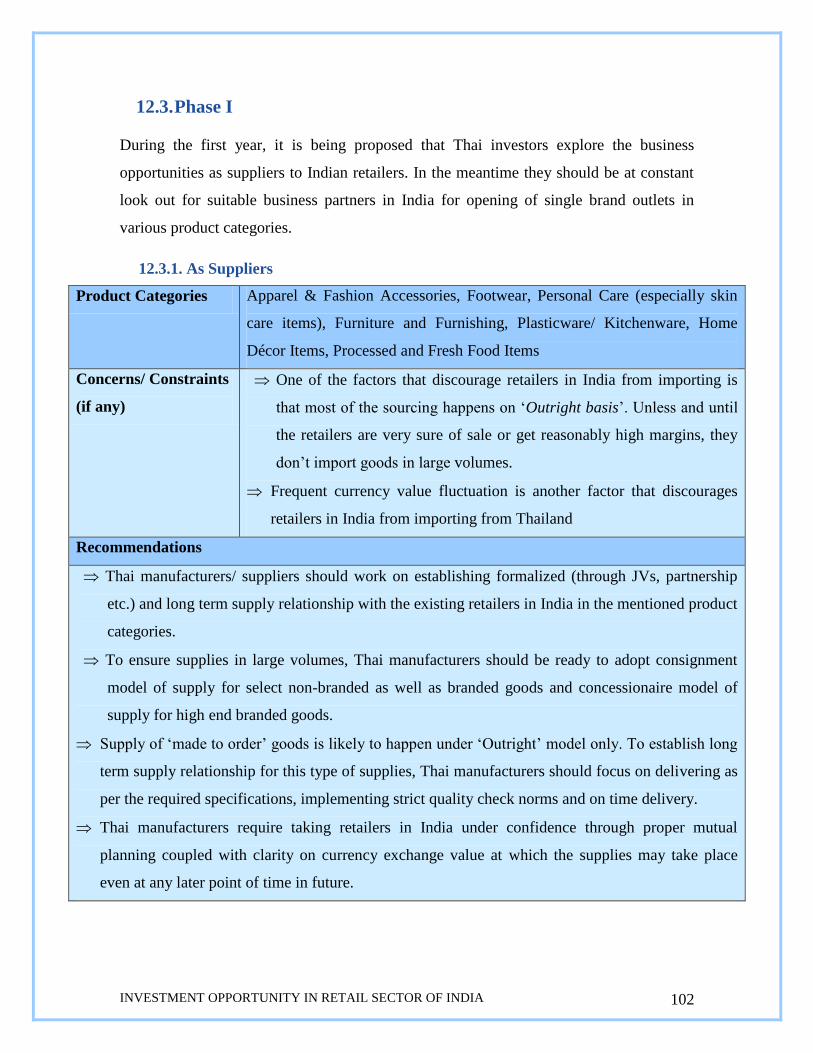

12.3. PHASE I .....................................................................................................................................102

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 7

12.3.1. As Suppliers ....................................................................................................................102

12.3.2. Look Out for Joint Ventures/ Franchisees/ 3 PL.............................................................103

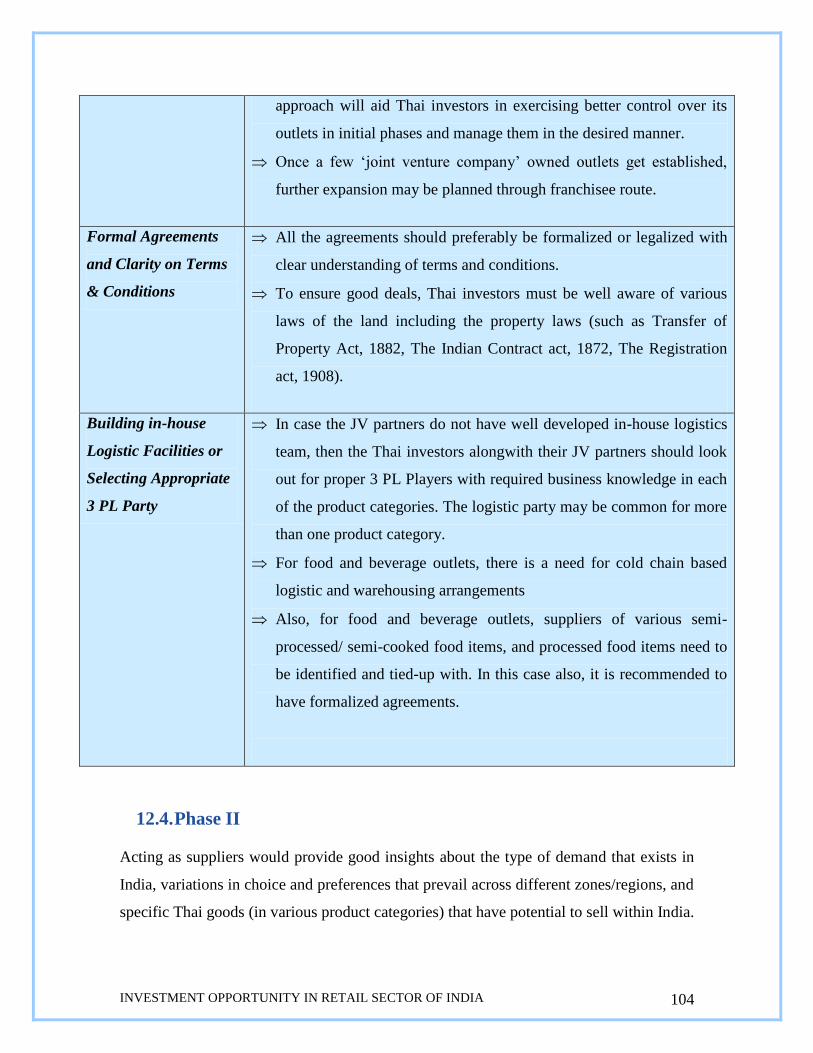

12.4. PHASE II ....................................................................................................................................104

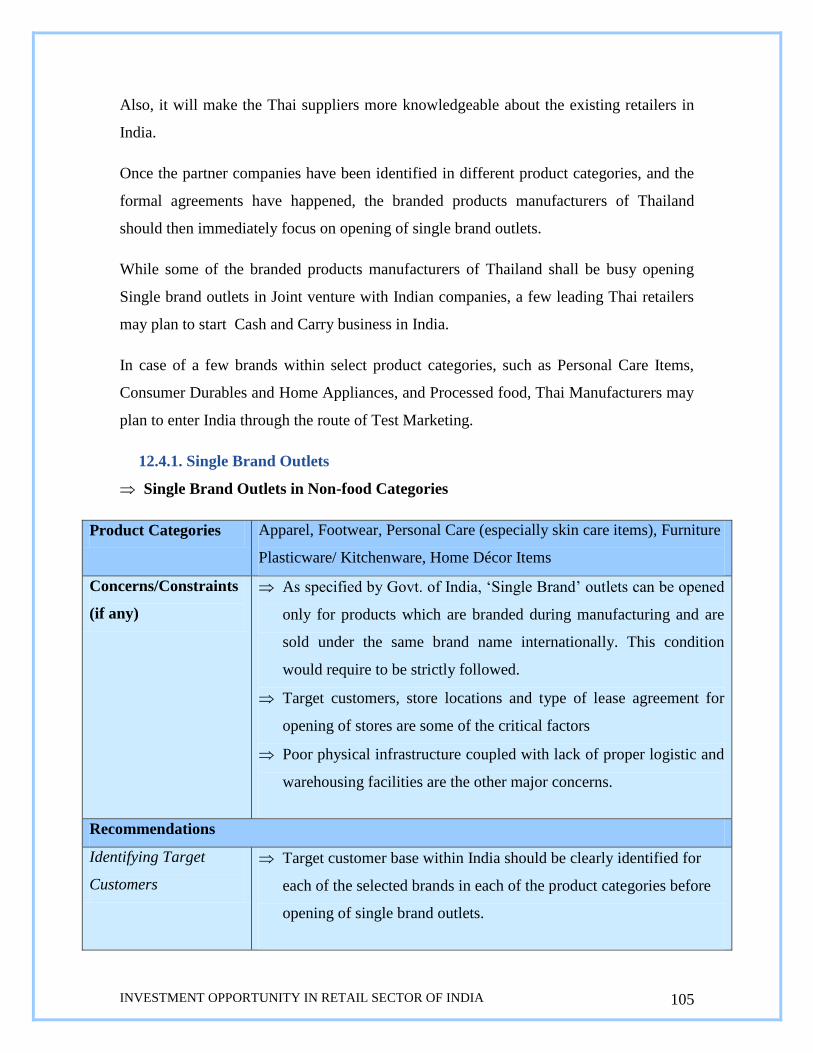

12.4.1. Single Brand Outlets .......................................................................................................105

12.4.2. Cash and Carry Stores ....................................................................................................108

12.4.3. Test Marketing ................................................................................................................109

12.5. PHASE III...................................................................................................................................110

12.5.1. Establishing Manufacturing Base in Select Product Categories ....................................111

12.5.2. Entering Theme / Specialty Malls ...................................................................................111

12.6. RECOMMENDATIONS ON FOCUS WITHIN EACH IDENTIFIED PRODUCT CATEGORY ....................112

1. ANNEXURE 1 ..................................................................................................................................113

1.1. COMPANY PROFILES IN RETAIL .................................................................................................113

2. ANNEXURE II .................................................................................................................................130

2.1. CITY-WISE RENTAL TRENDS .....................................................................................................130

3. REFERENCES .................................................................................................................................137

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 8

1. EXECUTIVE SUMMARY

1.1 Retail Sector in India

Retail business contributes around 11 percent of country‘s GDP and is the second largest

sector in India, only after agriculture. Retailing as a sector is witnessing revolution in

India. Modern retail has entered India as seen in sprawling shopping centres, multi-

storeyed malls and huge complexes that offer shopping, entertainment and food all under

one roof. Though at present, around 94-95% of India‘s retail market is unorganized, as

compared to unorganized retail, organized retail is experiencing much higher growth and

throwing open opportunities for new entrants to come and grow.

India: A Preferred Retail Destination

For three years in a row (2005-07), India has been ranked as the top retail destination

globally by a study from A T Kearney that measured retail investment attractiveness for

30 emerging markets in the world.

Key Growth Drivers for Modern Retail in India:

Higher disposable income coupled with favourable demographic changes (Increase in

working women population, rise in nuclear family, largest young population and higher

growth in urban and sub-urban population), changes in consumer needs, attitudes and

behaviour, and increased credit friendliness are some of the key growth drivers for

modern retail in India.

Size and Growth of Retail in India

Retail sales in India have grown from $US 230 billion in 2003-04 to $US 330 billion in

2007-08. Organized retail at present accounts for only around 5-6% of the total retailing

in India. However, growth experienced by organized retail (more than 35% against an

overall retail growth of around 11% in 2006-07) is much higher as compared to

unorganized retail within India. The graphs below depict the product category-wise

break-up of total and organized retail.

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 9

Coming to the category-wise share of organized retail out of total retail, timewear and

footwear are the categories with maximum organized retail (almost 50% of total retail in

each category). ‗Clothing & Textile‘ stands third with more than 20% of the trade in

organized retail.

1.2 Modern Retail Store Formats

Indian Retailers are experimenting with various modern retail formats customized to

customer categories and product mix. Following is a snapshot of various formats that

exist in India at present.

THE INDIAN RETAIL PIE (INDIA) 2007- 08 ( M a r k e t S i z e : $ US 3 3 0 bi l l i on)

Food &

Gr oc e r y

5 9 . 5 %

Foot wear

1.2%

Healt h & Beaut y

Services, 0.3%

Pharma

3.7%

Wat ches

0.3%

Jwellery

5.2%

Consumer

Durables

4.3%

Mobile&

Services

2.0%

Furnit ure &

Ut ensils

3.4%

Out -of -Home

Food Services

5.4%

Books, Music &

Gif t s

1.2%

Ent ert ainment

3.4%

Clot hing,

9.9%

THE ORGANIZED RETAIL PIE (INDIA) 2007-08 ( M arket Size: $U S 19 .4 2 b il i ion)

Food & Grocery

11.5%

Foot wear

9.9%

Beaut y Services

0.8%

Pharma

2.0%

Wat ches

2.7%

Jwellery

2.9%

Consumer

Durables

9.1%

Mobile, &

Services

3.5%

Furnit ure &

Ut ensils

6.4%

Out -of -Home

Food Services

7.3%

Books, Music &

Gif t s

2.8%

Ent ert ainment

3.1%

Clot hing,

38.1%

Source: F &R Research

Clothing Food & grocery Footwear

Pharmaceutical

Jwellery,

Accessories

Furniture &

Furnishing

Other Retail

Formats

Electrical &

Electronic

Equipments

Books & Stationery

Beauty &

Health Care Music &

Entertainment

Destination

Malls

Specialty

Stores

Modern Retail Store Formats

Discount stores

Airport retailing

Online/ telephonic &

catalogue buying

Key product

categories with

luxury brands:

Apparel

Jwellery

Time wear

Accessories

Furniture

Premium Lifestyle

based Retailing

Other Retail

Formats

Departmental

Stores

Apparel and

Fashion Stores

Lifestyle based

Retailing

Value based

Retailing

Supermarket

Hypermarket

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 10

This section discusses in details each of the above mentioned formats, average store

space under each format, preferred store locations and key players and their principal

fascia operating under these formats.

Cash and Carry Stores

As Government of India has allowed 100% FDI in cash and carry format, many foreign

companies are choosing to enter the market through this format. Amidst the increasing

interest from foreign players, domestic retailers have also been entering this format in

India.

1.3 Supply Chain of Modern Retail in India

Level I: Sourcing Level II: Storage

& Distribution

Level III: Retail Stores

Company-owned

outlets

Franchised Stores

Departmental stores

Specialty Stores

Hypermarket

Supermarket

Other formats

Products from other

countries

Local Manufacturers supplying to more

than one retailing company for selling

under private labels

Retail Company‘s own

procurement office in

other countries

Importer / Retail

company‘ Import

Partners

Companies Manufacturing Branded

Products

Local Manufacturers supplying to a

single retail company for selling under

private labels

Distribution Centres or Warehouses

owned by Retail Company or by its Logistic Partners

These may be central or regional distribution centres

depending upon the structure

adopted by the retailer

Retailer may have common or

separate warehousing

arrange-ments for its different

retail formats

Company‘s In-house

Inventory

Distribution Centre (Owned by Company‘s Franchisee or its

Logistic Partner)

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 11

The section discusses in details each of the three levels of supply chain alongwith details

on standard methods of procurement and margins enjoyed in case of select product

categories.

Logistic facilities for retail industry in India

While some of the modern retailers in India have been outsourcing their logistics needs to

specialist service providers, many large players with national footprint have opted to

develop in-house logistic systems. According to industry sources, level of satisfaction of

retailers with their logistic partners is mostly low in India and that speaks of the poor

level of logistic services.

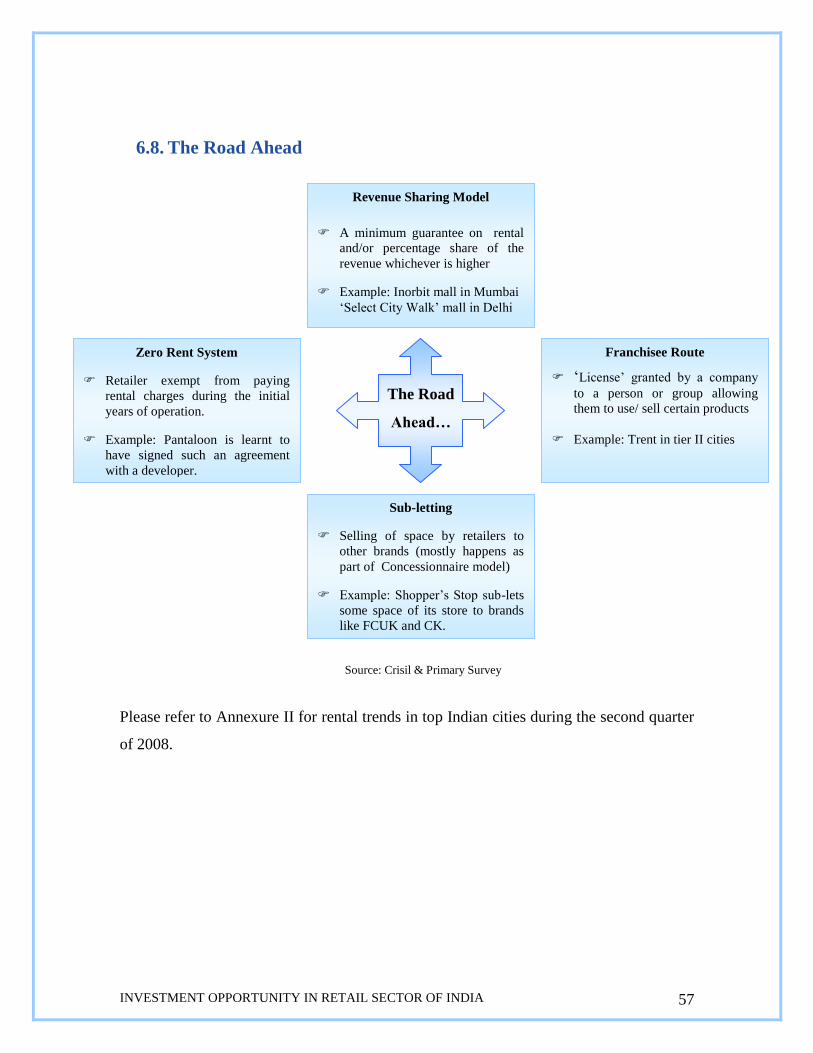

1.4 Rent Structure in Retail

Two types of rental models are prevalent in India – fixed lease rental model and revenue

sharing model. Though mall developers have been chasing for fixed lease rentals, of late

the retailers are bargaining hard for revenue sharing rental model. Given the increasing

competition in retail industry, high lease rentals and the sudden economic slowdown,

many retailers have changed their business strategies to mitigate the negative impacts and

consolidate their position. Slump in real estate sector and excess supply of mall space in

pipeline has also forced real estate developers to either cut down on rentals or adopt

‗revenue sharing based rental‘ or any other rental models. The diagram below depicts

the rental models that are likely to be used more frequently in Indian retail sector in

future.

Zero Rent System

Retailer exempt from paying

rental charges during the initial

years of operation.

E.g.: Pantaloon is learnt to have

signed such an agreement with a

developer.

The Road

Ahead…

Franchisee Route

‗License‘ granted by a company

to a person or group allowing

them to use/ sell certain products

E.g: Trent in tier II cities

Sub-letting

Selling of space by retailers to

other brands (mostly happens as

part of Concessionaire model)

E.g.: Shopper‘s Stop sub-lets

some space of its store to brands

like FCUK and CK.

Revenue Sharing Model

A minimum guarantee on rental

and/or percentage share of the

revenue whichever is higher

E.g: Inorbit mall in Mumbai

‗Select City Walk‘ mall in Delhi

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 12

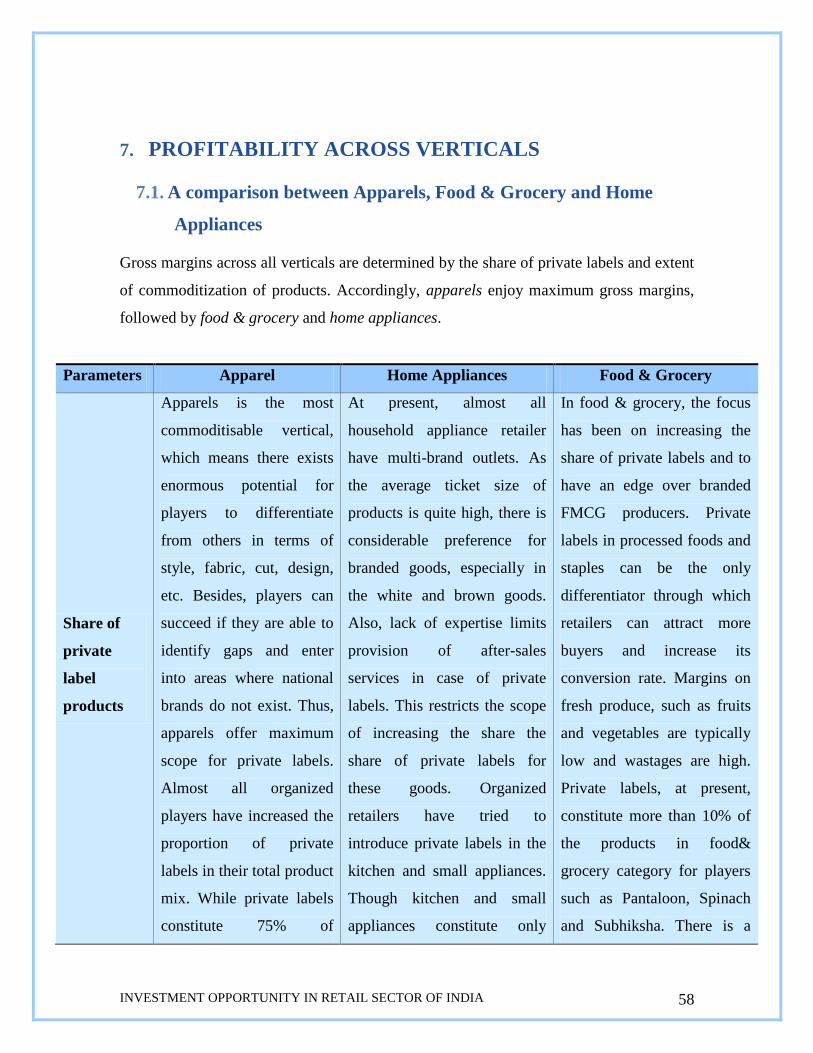

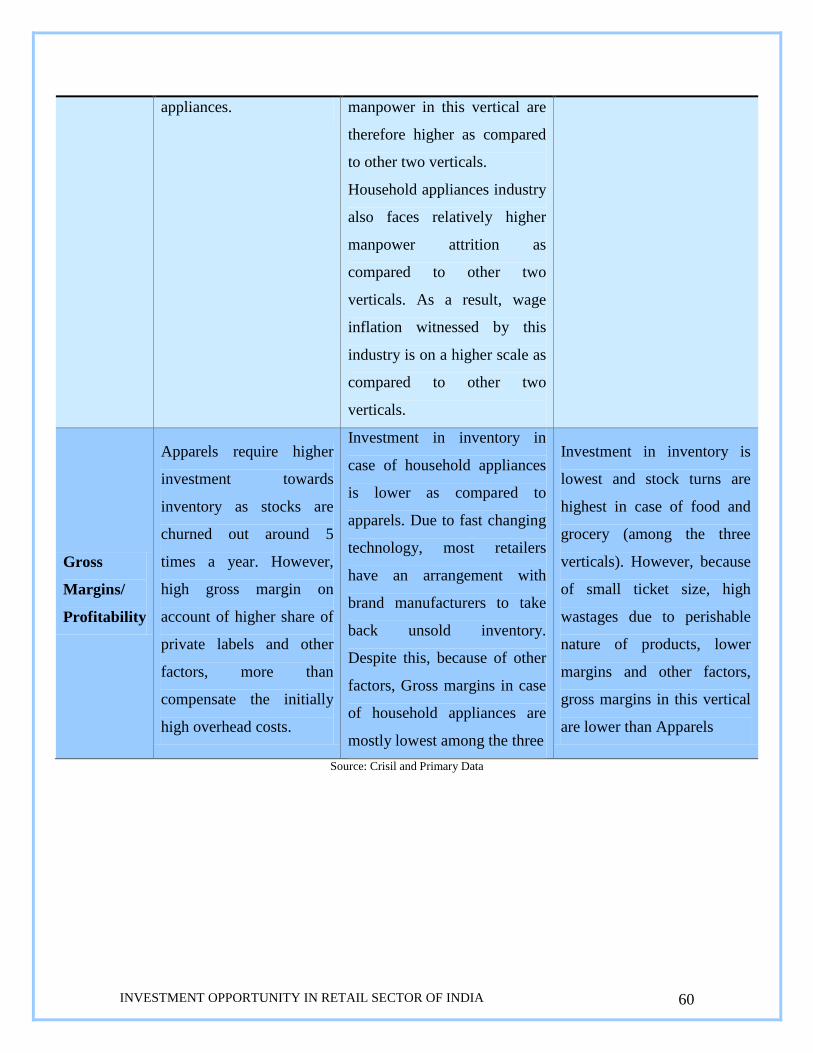

1.5 Profitability across Verticals

A comparison between Apparels, Food & Grocery and Home Appliances concludes that

apparels enjoy maximum gross margins, followed by food & grocery and home

appliances. Key reasons for higher gross margins in case of Apparels among the three

verticals are: Scope for higher share of private labels in case of Apparels, Cost of

developing & training manpower and wage inflation in case of Home Appliances higher

as compared to Apparels and Food & Grocery, Smaller ticket size in case of food &

grocery, and Store space largest in case of Home Appliances followed by Apparels and

then Food & Grocery

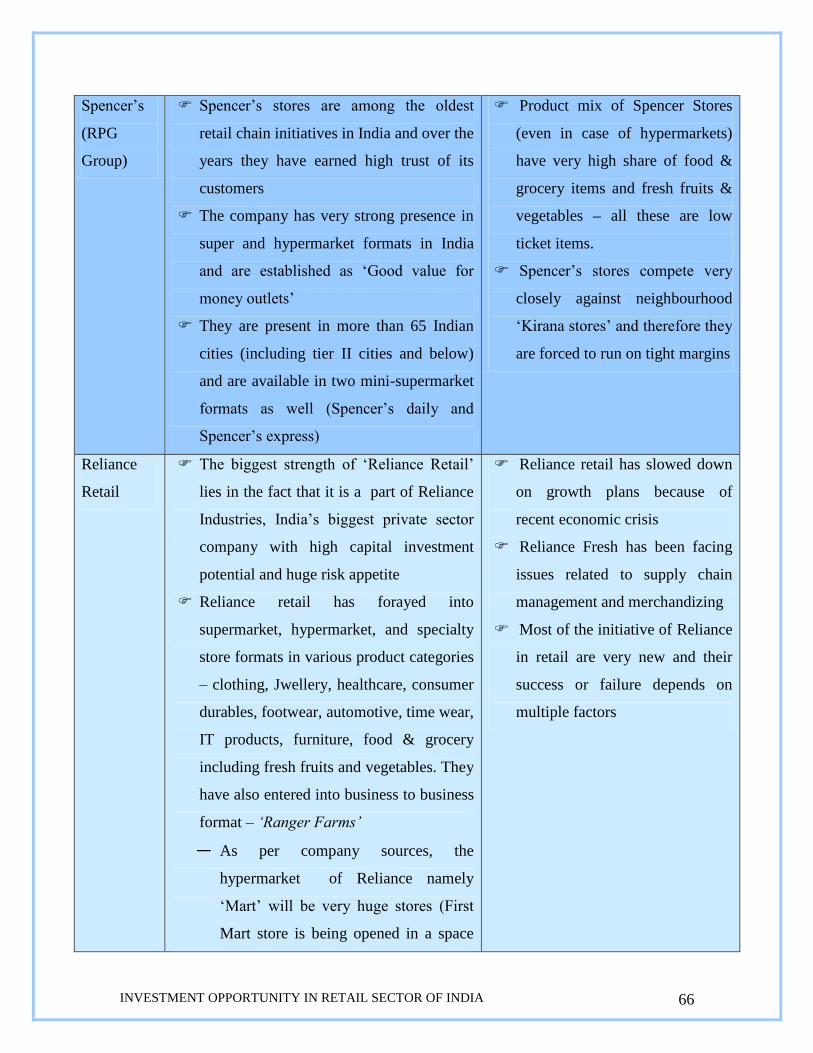

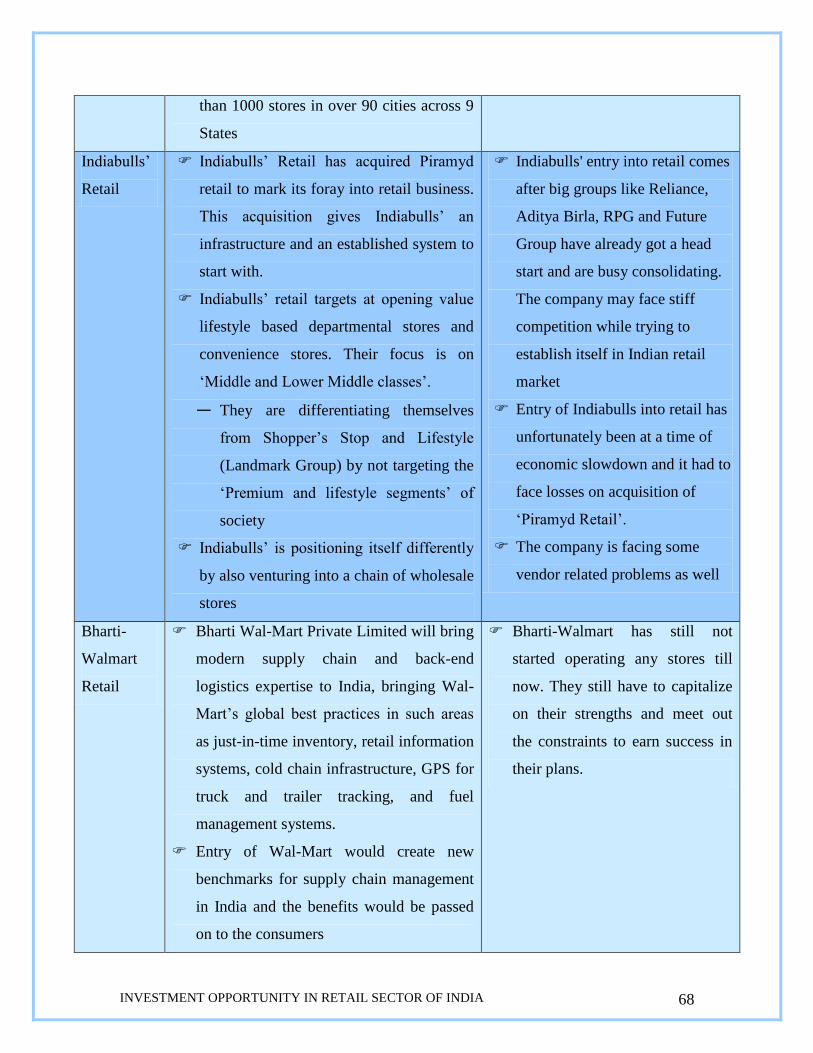

1.6 Leading Retail Companies of India

Pantaloon Retail is at present the largest retail company in terms of turnover, whereas

Vishal Retail leads in terms of presence and penetration across in India. Reliance and

Aditya Birla have forayed into the retail market only in 2006, however, they are poised to

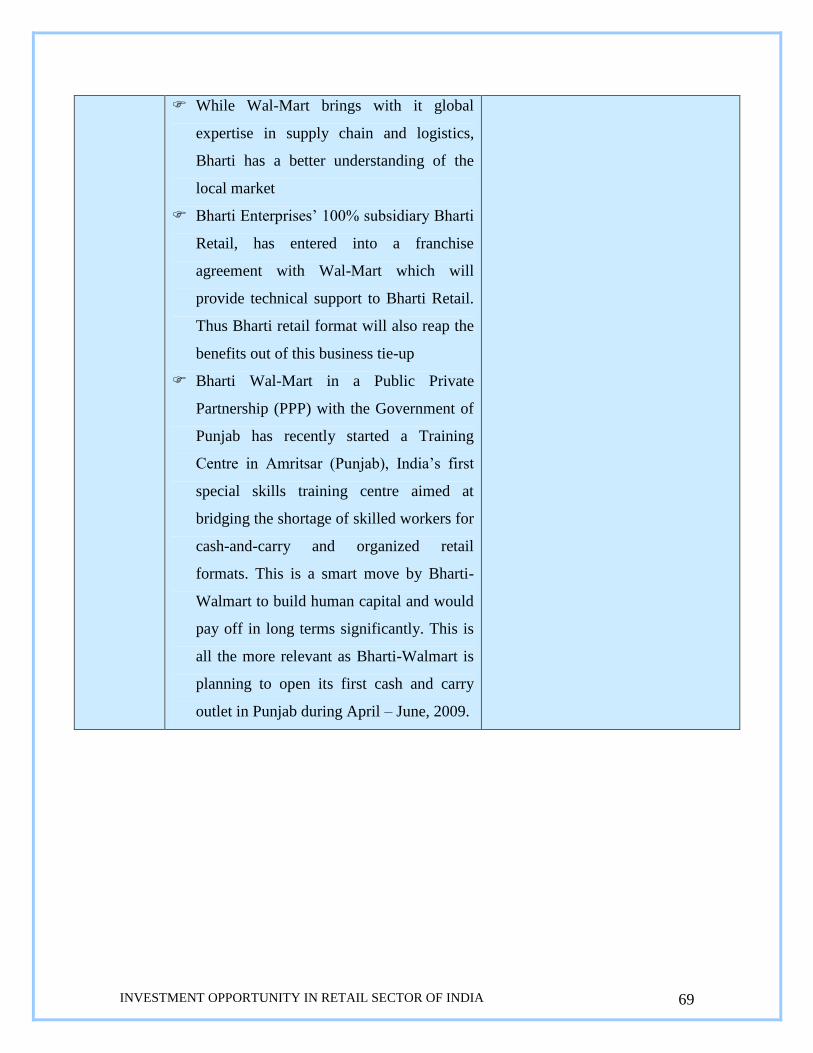

grow big and expand aggressively. Bharti-Walmart is expected to set new standards for

supply chain and back end logistics management and has aggressive growth plans in cash

and carry format. Subhiksha is India's largest supermarket, pharmacy and telecom retail

chain. In terms of turnover, Subhiksha is only next to Pantaloon Retail (figures from

2007-08). Shoppers‘ Stop and Lifestyle are leading in Departmental store format.

1.7 Indian Retail Industry Analysis

1.7.1 Indian Retail Market Analysis based on Nine Forces Model

Threat of New Entrants is high. Retailing doesn‘t require huge capital investments

into owning machineries and other assets; required technology can be obtained by any

new entrant; Specialist Knowledge requirement is addressable through right

recruitment, training and technology support; New entrants can differentiate

themselves in multiple ways; Distribution Channel are largely standardized and

replicable by new entrants; However, for a foreign player, there are FDI related

restrictions.

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 13

Threat of substitutes is high. Neighbourhood mom & pop stores, and other outlets

as part of unorganized retail, all are close substitutes of various Modern retail

formats. Cost of substitution is also not high in this case.

Bargaining power of real estate suppliers can be perceived as high to medium.

Recent real estate slowdown has given modern retailers power to bargain for lower

rentals or adoption of alternate lease models (e.g. revenue sharing). Bargaining power

of vendors varies from product to product and depends hugely upon whether a

product is branded or unbranded and whether the relationship with supplier is

formalized or not.

Bargaining power of buyers is high in case of modern retail largely because of

increased level of awareness among buyers on brands, quality, pricing etc., high price

sensitivity among Indian buyers and availability of close substitute in form of

unorganized retail.

Competitive rivalry can be perceived as medium because of medium to low

industry concentration ratio, concentration of players in few pockets, presence of

untapped market with room for new players to enter and grow, and low exit barriers

Government of India allows FDI in retail under two categories: Up to 100 per cent in

cash-and-carry (wholesale) retail and Up to 51 per cent in single brand retail.

Government regulations related to licenses, permits and taxation require further

simplification. Please refer to the section for further details on social, technological

and international/ economic shifts.

1.7.2 Major Constraints for Modern Retail in India

Poor physical infrastructure coupled with lack of 3 PL players, Absence of cold chain and

proper storage, High lease rentals, Inadequate Human Resources, and Stringent

Government Regulations are some of the key constraints faced by modern retail in India.

1.7.3 Emerging Trends in the Indian Retail Industry

Key emerging trends in the Indian retail industry are aggressive future plans of leading

retailers with higher focus on value retailing, more cases of market entry through

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 14

inorganic route, tie-up with global retailers, focus on tier II & lower cities, increased

share of goods under private labels and advent of self service outlets.

1.7.4 Critical Success Factors in Retail

Three most critical success factors for modern retail in India are: Location, Merchandize,

and Knowledge & Information. Knowledge & Information stands for Knowledge about

customers‘ tastes & preferences and Information is with regard to Efficient Supply Chain

and Inventory Management through Proper Information System.

1.8 Retailers’ Perception about Thai Imports

Apparels, plastic goods including kids‘ toys, home décor items, furniture, footwears, and

personal care items are some of the product categories in which Thai imports are being

preferred by retailers in India

1.9 Possible ways for entry of Foreign Retailers in India

Franchising, Cash and Carry Format, Test Marketing, and Manufacturing & Sourcing are

the possible routes through which International players can enter India

1.10 Conclusions and Recommendations

Among all product categories, Apparel comes out as the most attractive from Thai

Investors‘ point of view. Furniture, Footwear, Personal Care and Plasticware are the other

high potential categories for Thailand.

Recommendations on Focus within Each Identified Product Category

Product Categories Category-wise Focus

Apparel All types of denim based apparels for men, women and kids; Other fashion and casual

apparels for men, women and kids

Footwear Female footwear (specially the stiletto heel sandals); Thai manufacturers need to keep higher

quality standards for female footwears

Personal Care Various available range of products (skin care, cosmetics & health care products)

Plasticware All types of plasticwares (including plastic containers)

Furniture Rubber-wood/ Parawood based furniture

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 15

Home Décor Artificial flowers, vases, lamp shades, electric lamps, paintings, wall hangings etc.

Processed & Fresh Food

Sauces, Ketch-ups, Spices based pastes, and few ready to cook items (preferably vegetarian);

Supply of fresh items such as lettuce leaf

Thai manufacturers need to change the product packaging in following ways: no shrimps or

fishes drawn on the packets; cooking instructions and other details to be in clear font; Green

and red labels standing for vegetarian, and non-vegetarian items respectively to be put

clearly on the packets

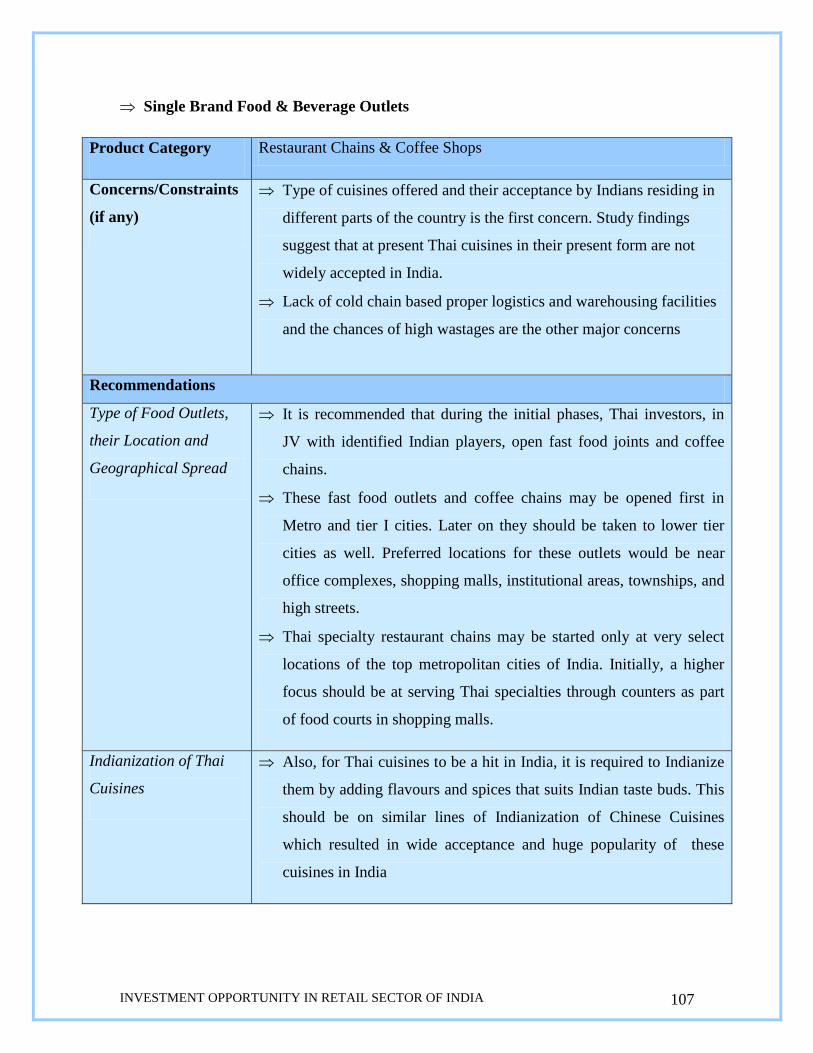

Food & Beverage Outlets Fast food Outlets and Coffee Chains

Proposed Entry Strategy : Thai Entrepreneurs should plan to invest in Indian Retail

Market in three phases that are briefed below:

Phase I: 1st Year

During the first year, it is being proposed that Thai investors explore the business

opportunities as suppliers to Indian retailers. In the meantime they should be at constant

look out for suitable business partners in India for opening of single brand outlets in

various product categories.

Phase II: 2nd

and 3rd

Year

Once the partner companies have been identified and the formal agreements have

happened, the branded products manufacturers of Thailand should then immediately

focus on opening of single brand outlets. Also, some of the leading Thai retailers,

preferably with past experience in the same categories, should plan to start Cash and

Carry business in India. In case of a few brands within select product categories, such

as Personal Care Items, Consumer Durables, and Processed food, Thai Manufacturers

may plan to enter India through the route of Test Marketing.

Phase III: 4th

Year onwards

To stay profitable in long term, establishing local manufacturing base, rather than

continuing to import, is a much desired step for select product categories. Also, this

would be the time to decide about putting up manufacturing facilities for the products that

were Test Marketed during Phase II. By the time phase III is entered, Theme malls

would have grown big on popularity. Thai Investors may plan to develop Thai Specialty

Malls.

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 16

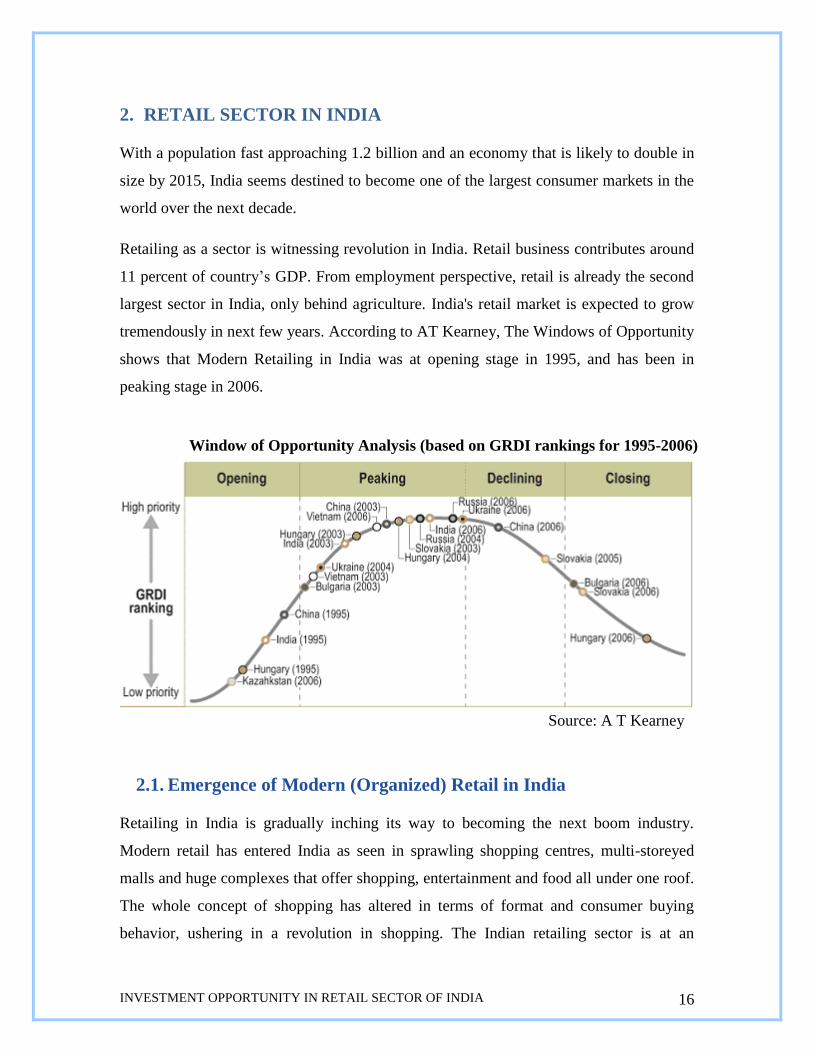

2. RETAIL SECTOR IN INDIA

With a population fast approaching 1.2 billion and an economy that is likely to double in

size by 2015, India seems destined to become one of the largest consumer markets in the

world over the next decade.

Retailing as a sector is witnessing revolution in India. Retail business contributes around

11 percent of country‘s GDP. From employment perspective, retail is already the second

largest sector in India, only behind agriculture. India's retail market is expected to grow

tremendously in next few years. According to AT Kearney, The Windows of Opportunity

shows that Modern Retailing in India was at opening stage in 1995, and has been in

peaking stage in 2006.

2.1. Emergence of Modern (Organized) Retail in India

Retailing in India is gradually inching its way to becoming the next boom industry.

Modern retail has entered India as seen in sprawling shopping centres, multi-storeyed

malls and huge complexes that offer shopping, entertainment and food all under one roof.

The whole concept of shopping has altered in terms of format and consumer buying

behavior, ushering in a revolution in shopping. The Indian retailing sector is at an

Window of Opportunity Analysis (based on GRDI rankings for 1995-2006)

Source: A T Kearney

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 17

inflexion point where the growth of organised retail and growth in the consumption by

Indians is going to adopt a higher growth trajectory.

Though at present, around 94-95% of India‘s retail market is unorganized, as compared

to unorganized retail, organized retail is experiencing much higher growth and throwing

open opportunities for new entrants to come and grow.

2.2. India: A Preferred Retail Destination

With markets in most of the developed countries reaching the stage of saturation, India

has emerged as one of the most preferred destination for global retailers. This is evident

from the number of retailers across the globe that have already forayed into India‘s retail

market or planning to do so soon.

For three years in a row (2005-07), India has been ranked as the top retail destination

globally, ahead of Russia and China by a study that measured retail investment

attractiveness for 30 emerging markets in the world.

2007 ranking Country 2006 ranking

1 India 1

2 Russia 2

3 China 5

4 Vietnam 3

5 Ukraine 4

6 Chile 6

7 Latvia 7

8 Malaysia 14

Source: A.T. Kearney, June, 2007

The same study, however, also identifies few key issues that stand in the way of India‘s

retail industry reaching its full potential. These issues have been discussed under ‗Major

Constraints for Modern Retail in India‘.

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 18

2.3. Key Growth Drivers for Modern Retail in India

2.3.1 Higher Disposable Income and Economic Prosperity

Disposable income of Indian consumers has increased steadily. The proportion of major

consuming class (with income above Rs 90,000 per annum) is expected to reach 48% by

2009-10 from 20% in 1995-96.

2.3.2 Demographic Changes

Higher Level of Working Women

According to census 2001, working women population has increased to 26% in 2001 as

compared to 22% in 1991. This would lead to a higher retail spending as the buying

behaviour of working women differs from that of housewives because of low availability

of time. Also, working women‘ propensity for spending is higher by 1.3 times as

compared to Indian housewives.

Rise in Nuclear Family

The per capita consumption increases in case of a nuclear family. During the last few

years in India, nuclear family as a percentage of total household population has increased.

The average household size has reduced to 5.36 in 2001 from 5.57 in 1991 and is

0%

100%

1995-96 2001-02 2005-06 2009-10*

CHANGING INCOME DISTRIBUTION

(Income figures in '000 per annum at 2001-02 prices, households in '000

numbers)

10000+

5001-10000

2001-5000

1001-2000

501-1000

201-500

91-200

< 90

Source: NCAER

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 19

expected to decline further to 5.02 by 2011. This would further increase the consumption

and in turn, the retail industry.

Baby Boomer Effect

India has the lowest median age of 24 as compared to developed countries like USA, UK,

Japan etc. The composition of the Indian population is shifting towards the age group of

20-49 i.e. the working population with purchasing power. Approximately 60% of the

Indian population is below 30 years of age. Thus, India has the largest ‗young‘ population

in terms of sheer size and this young segment is the major driver of consumption as they

have the ability (disposable income) and willingness to spend.

Higher Growth in Urban and Sub-Urban Population

Over the last 10 years (1990-2000), urbanization has increased at a rate of 2.7 percent.

Around urban centres, huge sub-urban agglomerates are developing and expanding at a

huge scale. This trend is expected to continue and urbanization is likely to grow at 2.4

percent between 2000 and 2015. Over the next 10 years, growth in organized retailing is

likely to be concentrated in urban and semi-urban areas.

2.3.3 Changes in Consumer Needs, Attitudes and Behaviour

The growth of modern retail is linked to consumer needs, attitudes and behaviour. Rising

income levels, education and global exposure have contributed to the evolution of the

Indian middle class. As a result, purchasing and shopping habits have been inculcated

and are increasing day by day.

Today, Indians are willing to try new things and look different, which has increased

spending on health and beauty products apart from apparels, food and grocery items.

Also, in the last 4-5 years, Indian markets have witnessed a strong shift towards

branded products.

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 20

2.3.4 Increased Credit Friendliness

The use of plastic money (credit and debit cards) has increased significantly in the last 3-

4 years. In fact the ease of payments (ability to spend without cash) due to the use of

credit and debit cards, has also led to an increase in total spending on shopping and eating

out. With the acceptance of and the increase in the number of electronic data converter

machines installed in retailing outlets, credit and debit cards will provide further fillip to

organised retail.

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 21

2.4. Size and Growth of Retail in India

Indian Retail Market has experienced enormous growth during the last few years. Retail

sales in India have grown from $US 230 billion in 2003-04 to $US 330 billion in 2007-

08.

2.4.1. Product Category-wise Break-up of Retail Market

Out of the total market size in retail, Food & Grocery is the dominant category (valued at

$US 196.47 billion in 2007-08) followed by Clothing, Textile & Fashion Accessories

(valued at $US 32.57 billion in 2007-08).

THE INDIAN RETAIL PIE (INDIA) 2007- 08

(Market Size: $ US 330 billion)

Food & Grocery

59.5%

Footwear

1.2%

Health & Beauty Services

0.3%

Pharmaceuticals

3.7%

Watches

0.3%

Jwellery

5.2%

Consumer Durables &

Home Appliances

4.3%

M obile, Accessories &

Services

2.0%

Furniture, Furnishings &

Utensils

3.4%

Out-of-Home Food

(Catering) Services

5.4%

Books, M usic & Gifts

1.2%

Entertainment

3.4% Clothing, Textile & Fashion

Accessories

9.9%

Source: F &R Research

Source: Images F & R Research

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 22

2.4.2. Organized Retail as Part of Total Retail

Organized retail happens to be a very small part of total retail market in India. At present,

it accounts for only around 5-6% of the

total retailing in India. However, growth

experienced by organized retail (more than

35% against an overall retail growth of

around 11% in 2006-07) is much higher as

compared to unorganized retail within

India. Owing to high growth rate,

organized retailing has finally emerged

from the shadows of unorganized retailing

and is contributing significantly to the growth of Indian retail sector.

2.4.3. Product Category-wise Break-up of Organized Retail

In the organized retail segment, the category-wise shares are very different from the

THE ORGANIZED RETAIL PIE (INDIA) 2007-08

(Market Size: $US 19.42 biliion)

F o o d & Gro cery

11.5%

F o o twear

9.9%

H ealth & B eauty

Services

0.8%

P harmaceuticals

2.0%

Watches

2.7%

Jwellery

2.9%C o nsumer D urables &

H o me A ppliances

9.1%

M o bile, A ccesso ries

& Services

3.5%

F urniture,

F urnishings &

Utensils

6.4%

Out-o f-H o me F o o d

(C atering) Services

7.3%

B o o ks, M usic & Gif ts

2.8%

Entertainment

3.1%

C lo thing, T extile &

F ashio n A ccesso ries

38.1%

Source: F &R Research

Source: F &R Research

Source: F &R Research

GROWTH OF TOTAL AND ORGANIZED

RETAIL MARKET IN INDIA

330298

256231

1914

97

0

500

2004 2005 2006 2007

Ret

ail M

arke

t

(Uno

rgan

ized

+ O

rgan

ized

)

(in

$ U

S b

illio

n)

0

40

Org

aniz

ed R

etai

l

(in $

US

bill

ion)

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 23

overall retail picture. Clothing, Textile & Fashion Accessories is the largest category

followed by Food & Grocery. Footwear and Consumer Durables happen to be the third

and fourth largest categories followed by Consumer Durables in organized retail at

present.

2.4.4. Category-wise Penetration of Organized Retail

Coming to the category-wise share of organized retail out of total retail, timewear and

footwear are the categories with maximum organized retail (almost 50% of total retail in

each category). ‗Clothing & Textile‘ stands third with more than 20% of the trade in

organized retail.

CATEGORY-WISE SHARE OF ORGANIZED RETAIL OUT OF TOTAL RETAIL IN INDIA

0%

10%

20%

30%

40%

50%

Clo

thin

g

Jwel

lery

Watc

hes

Foo

twea

r

Hea

lth &

Bea

uty

Ser

vice

sPhar

mac

eut

ical

s

Cons

um

er D

ura

ble

s

Mobile

, Acc

essor

ies

& S

ervi

ces

Fur

nitu

re, F

urn

ishi

ngs

& U

tensi

lsFoo

d &

Gro

cery

Out

-of-

Hom

e Food

Serv

ices

Book

s, M

usi

c &

Gift

sEnte

rtai

nm

ent

Ove

rall

2007 2006

2005 2004

100%

Source: F &R Research

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 24

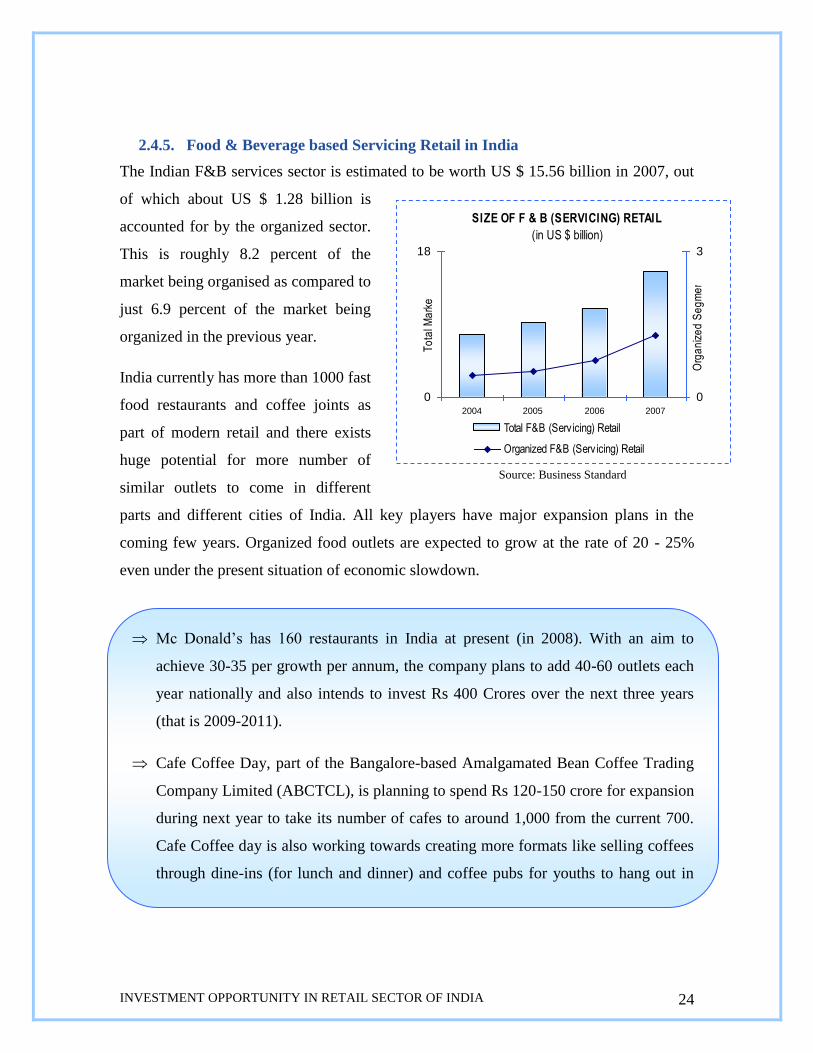

2.4.5. Food & Beverage based Servicing Retail in India

The Indian F&B services sector is estimated to be worth US $ 15.56 billion in 2007, out

of which about US $ 1.28 billion is

accounted for by the organized sector.

This is roughly 8.2 percent of the

market being organised as compared to

just 6.9 percent of the market being

organized in the previous year.

India currently has more than 1000 fast

food restaurants and coffee joints as

part of modern retail and there exists

huge potential for more number of

similar outlets to come in different

parts and different cities of India. All key players have major expansion plans in the

coming few years. Organized food outlets are expected to grow at the rate of 20 - 25%

even under the present situation of economic slowdown.

SIZE OF F & B (SERVICING) RETAIL (in US $ billion)

0

18

2004 2005 2006 2007

To

tal M

ark

et

0

3

Org

an

ize

d S

eg

me

nt

Total F&B (Serv icing) Retail

Organized F&B (Serv icing) Retail

Source: Business Standard

Mc Donald‘s has 160 restaurants in India at present (in 2008). With an aim to

achieve 30-35 per growth per annum, the company plans to add 40-60 outlets each

year nationally and also intends to invest Rs 400 Crores over the next three years

(that is 2009-2011).

Cafe Coffee Day, part of the Bangalore-based Amalgamated Bean Coffee Trading

Company Limited (ABCTCL), is planning to spend Rs 120-150 crore for expansion

during next year to take its number of cafes to around 1,000 from the current 700.

Cafe Coffee day is also working towards creating more formats like selling coffees

through dine-ins (for lunch and dinner) and coffee pubs for youths to hang out in

strategic locations. (Source: Business Standard, Dec 23, 2008)

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 25

Domino‘s intends to increase its outlets to 250 by March 2009 from the present

number of 230. The company has announced an investment of Rs220-230 crore in

India over the next three years for expanding its retail fast-food chain and

manufacturing capacities. (Company Sources, 17 Nov, 2008)

Over the past 10 years, Yum! has become the largest and fastest growing restaurant

company in India. As of the first quarter 2008 earnings, the company had 140 Pizza

Huts in 35 cities and 33 KFCs in nine cities. Yum plans to scale up Pizza Hut to 175

by 2010 and also add 15-20 new restaurants every year. (Source: Business Wire)

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 26

3. MODERN RETAIL STORE FORMATS

Indian Retailers are experimenting with various modern retail formats customized to

customer categories and product mix.

Key product

categories with

luxury brands:

Apparel

Jwellery

Timewear

Accessories

Furniture

Pharmaceutical

Food &

grocery

Clothing Footwear Jwellery,

Watches/

Accessories

Furniture &

Furnishing

Other Retail

Formats

Electrical & Electronic

Equipments

Books, Magazine

& Stationery

Beauty & Health

Care

Modern Retail Store Formats

Premium

Lifestyle based

Retailing

Lifestyle based

Retailing

Value based

Retailing

Departmental

Stores

Apparel and

Fashion

Stores

Specialty

Stores

Supermarket

Hypermarket

Other Retail

Formats

Discount

stores

Airport

retailing

Online/

telephonic

& catalogue

buying

Destination

Malls

Music & Entertainment

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 27

Following section deals in detail with these broad categories and sub-categories within

them:

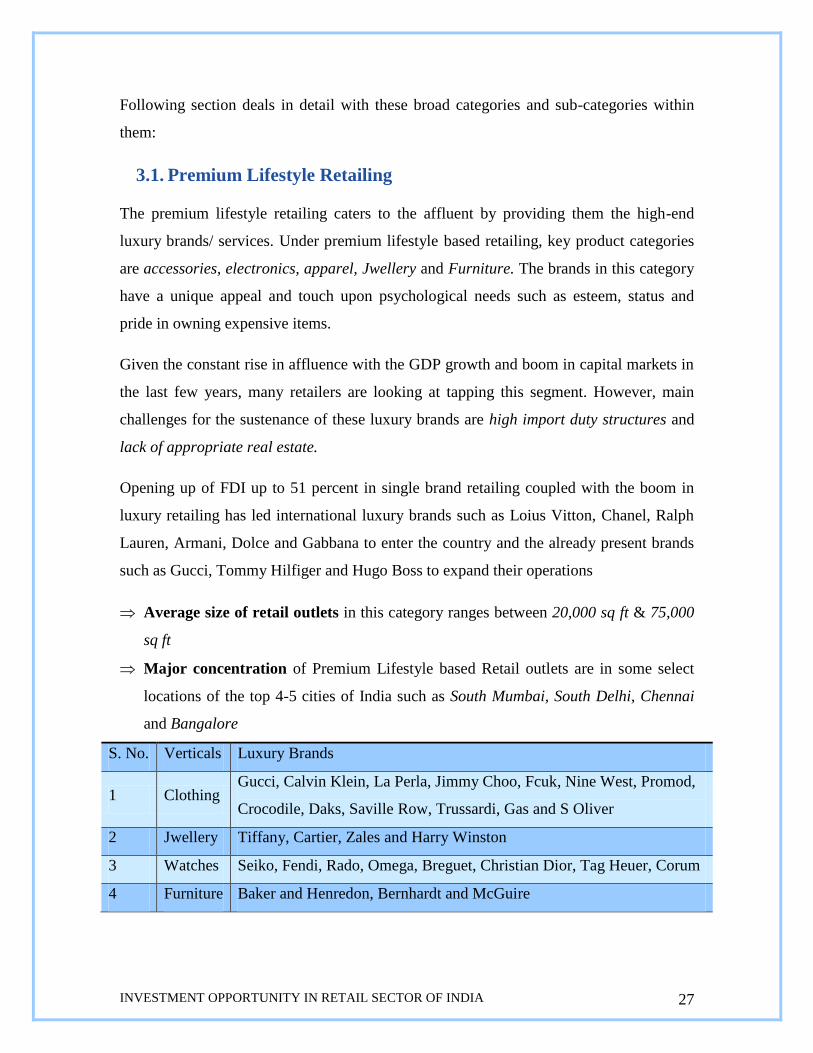

3.1. Premium Lifestyle Retailing

The premium lifestyle retailing caters to the affluent by providing them the high-end

luxury brands/ services. Under premium lifestyle based retailing, key product categories

are accessories, electronics, apparel, Jwellery and Furniture. The brands in this category

have a unique appeal and touch upon psychological needs such as esteem, status and

pride in owning expensive items.

Given the constant rise in affluence with the GDP growth and boom in capital markets in

the last few years, many retailers are looking at tapping this segment. However, main

challenges for the sustenance of these luxury brands are high import duty structures and

lack of appropriate real estate.

Opening up of FDI up to 51 percent in single brand retailing coupled with the boom in

luxury retailing has led international luxury brands such as Loius Vitton, Chanel, Ralph

Lauren, Armani, Dolce and Gabbana to enter the country and the already present brands

such as Gucci, Tommy Hilfiger and Hugo Boss to expand their operations

Average size of retail outlets in this category ranges between 20,000 sq ft & 75,000

sq ft

Major concentration of Premium Lifestyle based Retail outlets are in some select

locations of the top 4-5 cities of India such as South Mumbai, South Delhi, Chennai

and Bangalore

S. No. Verticals Luxury Brands

1 Clothing Gucci, Calvin Klein, La Perla, Jimmy Choo, Fcuk, Nine West, Promod,

Crocodile, Daks, Saville Row, Trussardi, Gas and S Oliver

2 Jwellery Tiffany, Cartier, Zales and Harry Winston

3 Watches Seiko, Fendi, Rado, Omega, Breguet, Christian Dior, Tag Heuer, Corum

4 Furniture Baker and Henredon, Bernhardt and McGuire

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 28

3.2. Lifestyle Retailing

Higher disposable income, increased level of awareness, international exposure, and

higher aspiration, all this has influenced the consumption pattern of the Indian

consumers. The Upper, Upper Middle and Middle class Indian customers are willing to

pay more for a brand or better product that keeps him/her up-to-date and in style. Major

growth drivers for Lifestyle retailing are: rising lifestyle aspirations, increasing

urbanization and changing mindset of Indian consumers

Two popular formats under this category are: Departmental stores and Apparel and

Fashion stores

3.2.1. Departmental Stores

Departmental stores are large stores having a wide variety of products, organized into

different departments such as clothing, houseware, furniture, appliances, toys, accessories

and cosmetics, among others. They offer value in terms of being a one-stop shop with

different brands in each category, catering to varied consumer needs. These stores target

primarily the SEC A, where the ticket size is larger in spite of a footfall lower than other

store types.

Major Players

Pantaloon, Shoppers‘ Stop, Lifestyle (Landmark Group), Ebony, Indiabulls Retail (Piramyd)

3.2.2. Apparel and Fashion Stores

These are stores with prime focus on apparel and will a small percentage of their mix

being fashion accessories, trinkets and home décor items. These may be multi-brand

stores or exclusive showrooms.

Average size of apparel and fashion stores in India is 20,000 sq ft

These stores are targeted primarily at high end consumers, primarily SEC A & B

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 29

Major Players

Pantaloon, Lifestyle (Max retail), Shoppers‘‘ stop, Westside, Globus, Provogue, Raymonds,

Madura Garments, Arvind brands, Guess, Fab India, and Koutons

The apparel segment, which is fairly organized, is profitable in comparison to other

product segments. This segment sees the presence of more international players than

most other retail segments.

3.3. Value retailing

Value retailing covers stores offering lower prices, better variety and a convenient and

improved shopping experience. It is based on the concepts of ‗Value for Money‘ and

‗Ways to Convenient Shopping‘.

The popular formats under this category are: Supermarkets and Hypermarkets

3.3.1. Supermarkets

A supermarket is a self-service one stop shopping store offering a wide variety of food

and household merchandise, organized into sections. It is larger in size and has a wider

selection than a traditional grocery store but is smaller than a hypermarket or superstore.

Supermarkets primarily cater to nearby residential areas and therefore throw a direct

competition to neighbourhood grocery stores and fresh fruits & vegetables retail mandis.

The basic appeal of supermarkets is the availability of broad selection of goods of

multiple brands as well as store‘s private labels under a single roof at relatively low

prices (possible on account of ‘Economy of Scale’ and ‘Efficient Warehousing and

Merchandizing’). Many of the superstores have discount and promotional offers on

various products at different points of time in a year. The concept of ‗Value retailing‘ is

catching up fast among middle class urban families.

Average size of supermarkets ranges from 3,000 to 10,000 sq ft and in some cases it

is upto 25,000 sq ft as well

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 30

Supermarkets of various Retail Companies are now present in many pockets of top

6-7 cities of India catering to the daily requirements of nearby residential areas. There

is an increasing focus on opening such outlets in Tier II cities (such as Ludhiana,

Patna, and Chandigarh etc.)

Key Players at National Level

Food Bazaar (Future Group), Reliance Fresh (Reliance), More (Aditya Birla Retail), Spencer

-Fresh, Daily and Super (RPG Group), Subhiksha , Indiabulls‘ Mart and Indiabulls‘

Megastore (Piramyd retail)

Modern Retail Players with presence in some specific regions and planning to grow big

Spinach (including Sabka Bazaar), Big Apple, Nilgiris, Marginfree, MK Retail, Namdhari‘s

Fresh, Easyday

3.3.2. Hypermarkets

Hypermarket is a large outlet which combines the format of a supermarket and a

department store. The result is a very large retail facility with an enormous range of

products catering to a spectrum of segments such as food and grocery, FMCG, apparel &

accessories, consumer durables, furniture & furnishing, entertainment & leisure, books

& stationery and other household items. Generally, they are located in the outskirts of

cities or as anchors in shopping malls. Hypermarkets offer lot of discount and

promotional offers to promote sales.

Margins depend on the product mix, volumes and supply chain management. A higher

share of food and grocery would mean lower margins. On the other hand, apparel and

furniture could increase margins.

Hypermarkets are becoming popular among consumers because products are available at

prices lower by 5% to upto 50% than the regular market price. Consumers are fine

traveling little far to shop in hypermarkets because of the price advantage they get.

Average size of hypermarkets ranges from 50,000 to 70,000 sq ft or more. Retail

outlets prefer to have their hypermarkets on one floor. However, in few cases the

space might be split into two or more floors as well.

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 31

There is an increasing focus on opening hypermarkets in Tier II cities. Retail

companies like Vishal Megamart and Big Bazaar are already operating their

hypermarkets in various tier II cities in India. Most of the Retail Outlets that are

present as supermarkets are now foraying into hypermarket format as well.

Key Players at National Level

Big Bazaar (Future Group), Reliance Hypermarket (Reliance), Spencer -Hyper (RPG Group), Star

Bazaar (Trent – Retail Arm of Tata) Subhiksha , Indiabulls‘ Mart & Megastore (Piramyd retail)

Business Break up of Big Bazaar (Pantaloon Retail)

F ruits &

Vegetables

2%

Live Kitchen

1%

F M C G_N o n-

fo o d

12%

F o o d B azaar

40%

Staples

12%

C lo thing

30%

General

M erchandise

16%

Electro nics,

F urniture,

F urnishing &

Others

14%

F M C G_F o o d

13%

Business break up of Vishalmart

Others, 1%

N o n-apparel

18%

A pparel

59%

F M C G

22%

Business break up of Aditya Retail in Staples

CategorySpices & Dry Fruits,

12%

Sugar & Salt, 8%

Edible Oil, 30%

Pulses, 20%

Cereals, 30%

Break up of General Merchandise

(Pantaloon Retail)

Utensils

& Steel

Items, 25%

P last ic

Items,

17%

F o o twear,

16%Luggage &

Other

Items, 42%

Source: Primary Data

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 32

3.4. Other Retail Formats

3.4.1. Specialty Stores

Specialty stores are category specific stores and are meant to cater to some specific needs

of consumers. A specialty store offers different brands of any specified category under

one roof. Specialty store can be dedicated to any of the following categories – Food &

grocery, Apparel, Footwear, Jwellery & Time wear & related accessories, Furniture &

Furnishing, Electrical & Electronic Equipments, Books & Stationery, Personal Care

(Beauty & Health Care), Consumer Durables (including home appliances),

Pharmaceuticals, Entertainment, Mobile Handsets & Accessories & Services, and

Others.

Average space for a Specialty Store ranges between 8,000 – 10,000 sq ft

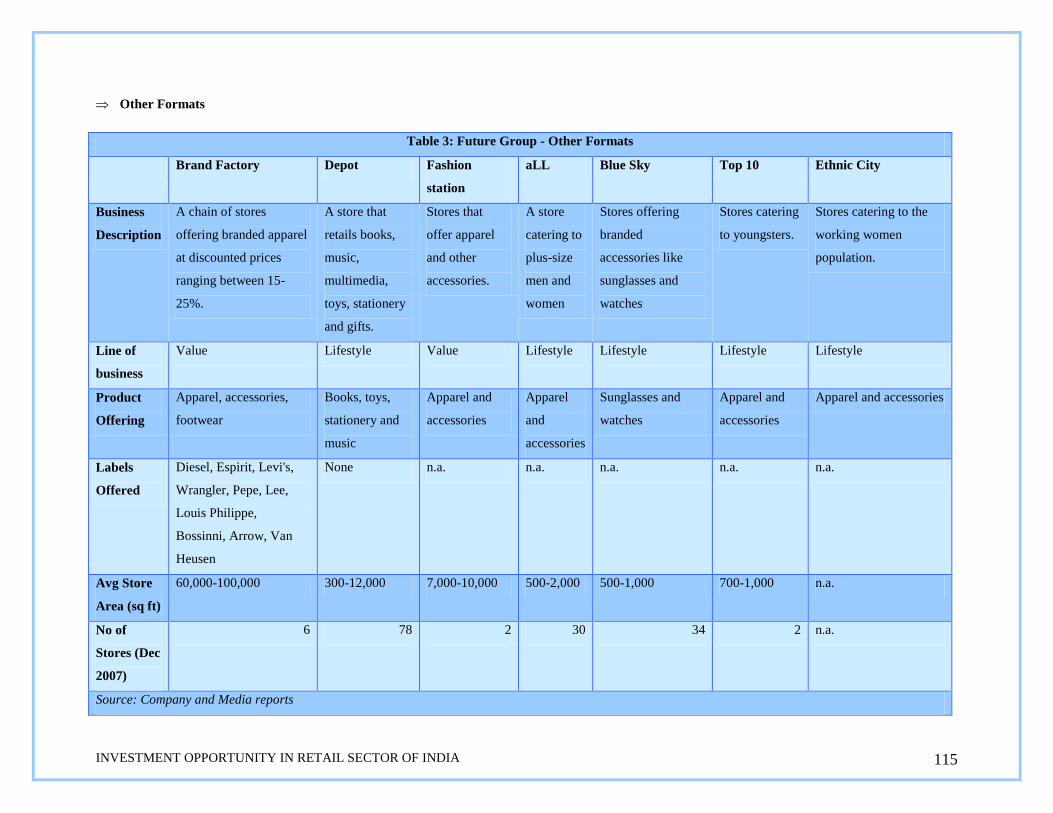

Verticals Key Players and their Principal Fascia

Food & Grocery Pantaloon (Brew bar, Café Bollywood, Chamosa)

Shoppers‘ Stop (Desi Café, Brio)

Clothing

Pantaloon (All, Brand Factory, Fashion Station, Top 10)

Shoppers‘ Stop (Mother Care)

Reliance Retail (Reliance Trendz)

Footwear Pantaloon (Shoe Factory)

Reliance Retail(Reliance Footprint)

Jwellery & Watches/

Accessories

Pantaloon (Blue Sky, Navaras)

Shoppers‘ Stop (Arcelia)

Furniture & Furnishing Pantaloon (Collection-i, Furniture Bazaar, Home Town)

Shoppers‘ Stop (Home Stop)

Electrical & Electronic

Equipments

Pantaloon (Electronics bazaar, e-zone, Got It)

Tata Trent (Croma)

Reliance Retail (Reliance Digital)

Videocon (Next)

Books, Magazine & Pantaloon (Depot)

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 33

Stationery Shoppers‘ Stop (Crossword)

Personal Care (Beauty &

Health Care)

Pantaloon (Health Village, Star Sitara, Tulsi, Turmeric)

Shoppers‘ Stop (MAC Cosmetics)

Reliance Retail (Reliance Wellness)

Music & Entertainment

Pantaloon (Bowling Co., F123, Sports Bar)

Shoppers‘ Stop (Time Zone)

Videocon (Planet M)

Mobile Handsets,

Accessories & Services

Pantaloon (Gen M, M Bazaar, M-port)

Spencer‘s Retail (RPG‘s Cellucom)

Subhiksha (Subhiksha Mobile)

Essar Group (Mobile Store)

3.4.2. Discount Stores/ factory outlets

These are sales outlets offering goods at a discounted price. Goods sold by discount

stores are generally the unsold or excess stock or slightly defective pieces. In general,

Manufacturers have their factory outlets. Discount outlets help manufacturers and

retailers to dispose of the excess or unsold stock while consumers get the benefit of

branded products at affordable prices.

Name of Store Key Players

The Loot Jay Retailing and Merchandizing Pvt. Ltd.

Megamart Arvind Brands

Shoe Factory Liberty Shoes and Pantaloon Retail (JV between two parties)

Globus Factory Outlet Globus

Maxretail Landmark group

Brand Factory JV of Pantaloon with Planet M, Globus, Staples and Dollar stores

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 34

3.4.3. Airport Retailing

Airport retailing is a new concept in India. Retailers are now capitalizing on the

increasing traffic at Indian airports. Domestic players are tying up with global retailers

having relevant experience in airport retailing in other countries.

However, the recent economic slowdown has impacted many of the retailers‘ plans in

Airport retailing.

3.4.4. Online, Telephone and Catalogue Buying

These are some other retail formats and are in their take off stage in India. There are

challenges in growth of these retail formats because of the ‗touch and feel‘ based buying

culture in India.

Indiatimes, rediff and ebay are some of the popular portals for online purchase

Pantaloons have ventured into e-tailing through their portal futurebazaar.com

Shopper‘s Stop has tied up with the UK based Home Retail group to develop the

Agros format of catalogue retailing in India

3.4.5. Shopping Malls

They are enclosures having different formats for retailers, both value and lifestyle based,

all under one roof. These are sophisticated versions of old shopping centres with huge

space, air-conditioned ambience, elevator and escalators. A variety of shops

(departmental stores, hypermarkets, and specialty stores), food court, parking space, and

entertainment (cine-multiplex and gaming zones) all together make it a One Stop

Shopper‘s Stop has tied up with Nuance from Switzerland whereas Tata‘s Consumer

Durable and Electronic Retail Company – Croma has tied up with Woolworth‘s to set up

retail stores at airports.

Pantaloon Retail had tied up with UK‘s Alpha Retail. However, because of major losses

faced by Alpha Retail, Pantaloon Retail has recently divested from the company and the

tie-up has ended.

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 35

destination. Mostly, shopping malls have anchor tenants, who cover large areas in the

mall and are important from the point of attracting footfalls.

In India, there is a new culture towards Specialty malls (also known as Theme Malls) –

catering to specific needs of customers. Specialty malls for luxury goods and premium

lifestyle segment is expected to catch up in India. At present, there are only few specialty

malls in India, but the Retailers Association of India (RAI) expects to push specialty

malls constituting nearly 10 per cent of the total malls in India.

The first specialty mall was the Gold Souk in Gurgaon. Dedicated entirely to the

Jwellery collection, the mall houses some of the big brands in the Jwellery business in

India as well as abroad.

‘Central’ is a first of its kind seamless mall in India. It is an initiative of Pantaloon

Retail. Pantaloon Retail (India), is expanding its retail chain ‘Central’ by setting up

new mall stores in metro cities like Mumbai and Bangalore and tier-II and tier-III

cities like Ahmedabad, Nashik, and Vashi.

There are divided opinions about success of specialty malls in India – while one

segment feels that Specialty malls are a step towards adding value to retailing in

India, the other segment feels that Indian market is still not mature enough and it is a

bit early to introduce this concept here.

DISTRIBUTION OF MALL SPACE

ACROSS ZONES IN INDIA (2011)*

(Total Supply: 236 mn sq ft)

East Zone, 9% South

Zone, 24%

West Zone, 28%

North Zone, 39%

DISTRIBUTION OF MALL SPACE

ACROSS ZONES IN INDIA (2007)

(Total Supply: 47.4 mn sq ft)

East Zone,

7%

South Zone, 14%

West Zone, 44%

North Zone, 35%

Source: Images F & R Research

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 36

3.4.6. Food Outlets as part of Modern Retail

Home-grown as well as international restaurant chains present in both high street

locations and malls represent the organised food and beverages (F&B) services retail

sector. Major categories in which modern food & beverage outlets can be put basis front

end formats are discussed below.

While some of the specialty restaurant chains are based only on take away or home

delivery format and don‘t have any seating arrangements, most of these modern

restaurant chains have both types of arrangements – home delivery as well as on the spot

consumption option.

Food Outlets as part of Modern Retail

Specialty

Restaurant Chains

Hot Beverage/

Coffee Chains

Food Courts Multi-cuisine

Restaurant Chains

These are restaurant

chains with wide range

of menu catering to

different cuisines.

Example:

- Ohri‘s

- Blue foods

- Indijoe

Some regional Indian

chains that are

growing fast:

- Nirula‘s

- Haldiram‘s

These are restaurant

chains with focus on a

single cuisine or with

some specialty to

offer. They may be

chains based on a

particular concept or

theme. Fast food

chains would also fall

in this category.

Example:

- Mc Donald‘s

- Pizza Hut

- KFC

- Subway

- Jumboking

- Yo! China

- Pizza Corner

- Papa John‘s

These are outlets with

coffee or other hot

beverage in different

flavours and varieties

as their major

offerings. Alongside,

they generally serve

some some snacks or

bakery items. In some

cases, there may be

more food items to

offer, however, coffee

or other hot beverage

remains at the core.

Example:

- Café Coffee Day

- Barista

- Mocha

- Costa Coffee

These are areas where

counters of multiple

food vendors are

present with a

common space for

self-serve dining. Food

courts are mostly

found as part of

shopping malls. In

some cases they may

be standalone

development as well.

Food courts may have

food stalls belonging

to various cuisines,

concepts and brands.

Coffee chains may

also present as part of

food courts.

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 37

Apart from the above mentioned categories, there are many traditional and regional

Indian restaurants that are now expanding their presence in different parts of India and

growing as Chain restaurants. However, their supply chain models are not exactly on

same lines as modern restaurant chains. Example: Sarvana Bhavan, Karim‘s, Hyderabadi

Biryani House, Vasanta Bhavan

Modern restaurant chains in India compete against the traditional vegetarian and non-

vegetarian restaurants and food stalls which constitute almost 92-93% of the total food &

beverage servicing segment in India. Some of the traditional cuisines of India are:

Kashmiri, Punjabi, Mughlai, Bengali, Gujarati, Rajasthani, and Hyderabadi.

Entry and Operating Format

Most of the modern food outlets are either franchised or company-owned. Most of the

global food chains have entered India either through franchise route or through JVs with

any existing Indian players. An international company can get into JVs with different

local players for opening and operating outlets in different parts of India.

Example: Mc Donald's India is a joint-venture company managed by Indians. In Western and

Southern India, Hardcastle Restaurants Private Limited owns and manages McDonald's

restaurants. In Northern and Eastern India, McDonald's Restaurants are owned and managed

by Vikram Bakshi‘s Connaught Plaza Restaurants Private Limited. Almost all the outlets of

Mc Donalds are company owned.

Pizza Hut has entered Indian market through Franchise route in 1996. The pizza franchise

soon expanded itself in India and now has the KFC brand beneath its umbrella.

Domino's entered India in 1996 through a franchise agreement with Vam Bhartia Corp. Vam

Bharti Corp. acts as master franchisee and in turn further extends franchises to different sub-

franchisees

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 38

4. CASH AND CARRY STORES

Targeted at and open only to business customers - cash and carry scheme focuses on

small-wholesale customers who buy in bulk and pay in cash. Unlike hypermarkets where

any consumer can walk-in and buy goods, cash-and-carry outlets allow only

authenticated bulk buyers to transact business. Medium-sized businesses such as retail

stores, hotels, restaurants, caterers, exporters etc can buy from cash-and-carry outlets at

prices much cheaper than market rate.

In its original form, owners of cash and carry outlets (i.e. large retail chains) buy from

producers directly at very high volume, dispensing with middlemen like wholesalers and

stockiest. They also establish their own brands - asking producers to manufacture as per

their product and packaging specifications. Volume purchase and removal of middlemen

result in substantial cost reduction - a part of which is passed on to b2b customers. So,

b2b customers get products of assured quality throughout the year at less than market

price.

Wholesale cash-and-carry operations would provide small retailers and business owners a

wide range of products at the wholesale prices.

4.1. Global Retailers Entry through Cash & Carry Format

As Government of India has allowed 100% FDI in cash and carry format, many foreign

companies are choosing to enter the market through this format. Global retailers plan to

use the opportunity to set up wholesale stores in India to understand the market. Opening

of 'Cash and Carry' stores throughout the country shall provide a golden opportunity to

these global retailers to make in-roads into India. When the restrictions on the retail

industry are lifted, international retailers will be in a prime position to easily convert their

'Cash and Carry' stores into highly profitable supermarkets and hypermarkets.

German wholesale major Metro Cash and Carry has already forayed into Indian

market and is taking its stores to Mumbai, Kolkatta, NCR and Punjab.

Bharti-Walmart is expected to roll out its first store in Punjab (One of the North

Indian States of India) between April and June, 2009.

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 39

French Retailer Carrefour has announced its entry in cash and carry segment of India

in 2009

Britain‘s largest retailer Tesco Plc announced its investment (in August, 2008) to

develop a wholesale cash-and-carry business in India. Also, Tesco has tied-up with

Trent Ltd, the retail arm of the Tata group, to help develop the Indian company‘s Star

Bazaar hypermarkets.

Costco, one of the largest retail chains of US has also shown interest in joining the

bandwagon

Australian retail giant Woolworths is in discussion with Future Group (Pantaloon

Retail) for an equal equity joint venture for entry into Cash and Carry format in India

4.2. Domestic Players Not Far Behind

Amidst the increasing interest from foreign players, domestic retailers have not been

left behind. Videocon Industries has floated a separate subsidiary company for its

cash and carry retailing business — Bolld Cash & Carry.

While Bharti has already stuck a deal with Wal-mart, Pantaloon is exploring the

options to foray into cash and carry business.

Wadhawan Food Retail, which owns Spinach, Sabka Bazaar and Home Store retail

formats, is also eyeing the cash and carry format.

Reliance is also planning to launch its B2B format

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 40

5. SUPPLY CHAIN INSIGHTS

5.1. Supply Chain Model for Modern Retail Outlets

The given supply chain model exists across various product verticals with slight

modifications

Level I:

Sourcing

Level II: Storage

& Distribution

Level III:

Retail Stores

Company-

owned outlets

Franchised

Stores

Departmental

Stores

Specialty

Stores

Hypermarket

Supermarket

Other formats

Products from

other countries

Local Manufacturers

supplying to more than one

retailing company for selling

under private labels

Retail

Company‘s own

procurement

office in other

countries

Importer / Retail

company‘ Import

Partners

Companies Manufacturing

Branded Products

Local Manufacturers

supplying to a single retail

company for selling under

private labels

Distribution Centres or

Warehouses owned by

Retail company or by its

Logistic Partners

These may be central

or regional distribution

centres depending

upon the structure

adopted by the retailer

Retailer may have

common or separate

warehousing arrange-

ments for its different

retail formats

Company‘s In-house

Inventory

Distribution Centre

(Owned by Company‘s

Franchisee or its Logistic

Partner)

INVESTMENT OPPORTUNITY IN RETAIL SECTOR OF INDIA 41

5.1.1. Level 1: Product Sourcing

Modern retailers in India largely procure branded products in various categories

(apparels, consumer durables, electrical & electronic equipments, furniture and furnishing

items, footwear etc.) directly from companies‘ factories and send the procured lots to

their distribution centres. Procurement is done centrally for all the retail outlets. In case of

private label items also sourcing is done directly from manufacturing points and the lots

are sent to distribution centres. From the distribution centres, the lots are further

distributed across various retail outlets.

There are two ways in which retailers usually import goods from other countries:

Maintaining their own offices in other countries: The offices act as procurement

points (from manufacturing units), quality check points and they take care of

shipment of procured goods to India. This method is mostly adopted for countries

from where large volume imports are happening on regular basis.

Sourcing from importers: In many cases, retailers don‘t import directly from

manufacturing points in other countries, rather source the products from already

existing importers present in India. This method is adopted if volume of procurement

is neither huge nor on regular basis.

India is a country of diverse culture, lifestyle and food habits. Taste and preferences of

buyers vary from region to region. Retailers in India need to maintain in their retail

outlets some products and brands that are locally popular in the regions where the retail