130729 habibie center - thc aseanadmin.thcasean.org/assets/uploads/file/2014/11/mr. yoshifumi... ·...

TRANSCRIPT

Yoshifumi FukunagaYoshifumi Fukunagah f dh f dEconomic Research Institute for ASEAN and East AsiaEconomic Research Institute for ASEAN and East Asia

29 July 2013, Jakarta 1

What is RCEP? “New” FTA negotiation among the ASEAN+6 countries.

o ASEAN10 Australia China India Japan Korea and New Zealando ASEAN10, Australia, China, India, Japan, Korea and New Zealand

Negotiation starts in 2013.

Conclusion in 2015, as an ambitious goal. Conclusion in 2015, as an ambitious goal.

Three official documents have been issued:

o “ASEAN Framework for Regional Comprehensive Economic Partnership” (November 2011)

o “Guiding Principles and Objectives for Negotiating the Regional Comprehensive Economic Partnership” (August 2012)Comprehensive Economic Partnership (August 2012)

o “Joint Declaration on the Launch of Negotiations for the Regional Comprehensive Economic Partnership” (November 2012)

2

8 Principles of RCEPp1. WTO consistency

2 Significant improvements over the existing ASEAN+1 FTAs2. Significant improvements over the existing ASEAN+1 FTAs

3. Facilitation of trade and investment and transparency enhancement

4. Consideration of the different levels of development

(e.g., special and differential treatment)

5. Continued existence of the ASEAN+1 FTAs

6. Open accession

7 T h i l i d i b ildi7. Technical assistance and capacity building

8. Comprehensiveness (parallel negotiation of trade in goods, trade in services, investment and other areas))

3

RCEP Guiding Principles and ObjectiveRCEP Guiding Principles and Objective

“The objective of launching RCEP negotiations is to achieve a modern, comprehensive, high-quality and

t ll b fi i l i t hi tmutually beneficial economic partnership agreement among the ASEAN Member States and ASEAN’s FTA Partners.”

Principle 2:

“Significant improvements over the existing ASEAN+1 FTAs”

4

Why we want RCEP?yRCEP can…

Economic Reason1. Deepen the liberalization commitments (goods, services and ROO);2. Ease the “noodle-bowl” situation (not only in ROO but huge number of

tariff schedules, and different rules) and thus enhance the utilization of FTA;

3. Further ease the use of FTAs via “accumulation”;4. Deepen economic cooperation for facilitation measures; and,5 Prevent the potential loss from competing initiatives (e g CJK FTA)5. Prevent the potential loss from competing initiatives (e.g., CJK FTA).

+ Political Reason for ASEAN

51. Maintain and strengthen the “ASEAN Centrality” (politically) under the

pressure from TPP and CJK.

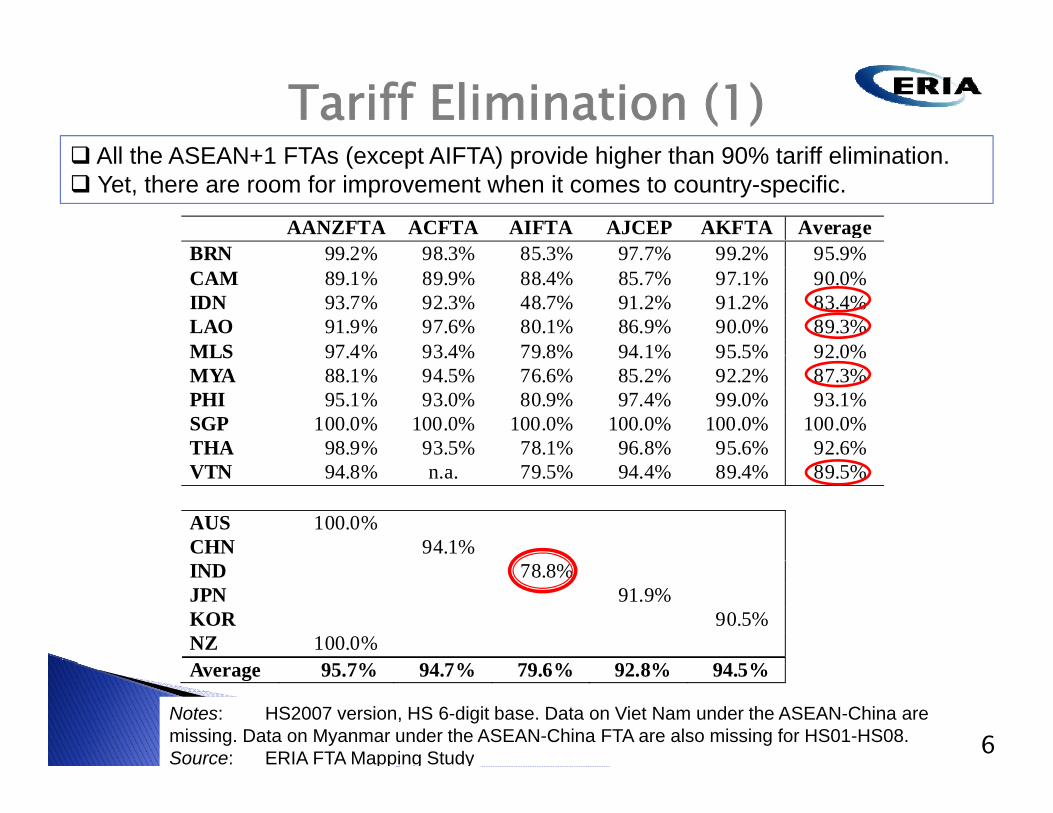

Tariff Elimination (1) All th ASEAN+1 FTA ( t AIFTA) id hi h th 90% t iff li i ti

AANZFTA ACFTA AIFTA AJCEP AKFTA AverageBRN 99 2% 98 3% 85 3% 97 7% 99 2% 95 9%

All the ASEAN+1 FTAs (except AIFTA) provide higher than 90% tariff elimination. Yet, there are room for improvement when it comes to country-specific.

BRN 99.2% 98.3% 85.3% 97.7% 99.2% 95.9%CAM 89.1% 89.9% 88.4% 85.7% 97.1% 90.0%IDN 93.7% 92.3% 48.7% 91.2% 91.2% 83.4%LAO 91.9% 97.6% 80.1% 86.9% 90.0% 89.3%MLS 97 4% 93 4% 79 8% 94 1% 95 5% 92 0%MLS 97.4% 93.4% 79.8% 94.1% 95.5% 92.0%MYA 88.1% 94.5% 76.6% 85.2% 92.2% 87.3% PHI 95.1% 93.0% 80.9% 97.4% 99.0% 93.1% SGP 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%THA 98.9% 93.5% 78.1% 96.8% 95.6% 92.6%VTN 94.8% n.a. 79.5% 94.4% 89.4% 89.5%

AUS 100.0% CHN 94.1% IND 78.8%JPN 91.9% KOR 90.5% NZ 100.0%A 95 7% 94 7% 79 6% 92 8% 94 5%Average 95.7% 94.7% 79.6% 92.8% 94.5%

Notes: HS2007 version, HS 6-digit base. Data on Viet Nam under the ASEAN-China are missing. Data on Myanmar under the ASEAN-China FTA are also missing for HS01-HS08.Source: ERIA FTA Mapping Study 6

Tariff Elimination (2)Common concession is a key feature in the ASEAN+1

FTAs.

(a) common concession --- e.g., Indonesia (or Korea) has single tariff schedules giving the same preferences to all the RCEP

bmembers.(b) non-common concession --- e.g., Indonesia (or Korea) gives

different preferences to RCEP members (max. 15 different tariff schedulesschedules.

Common concession will bring additional liberalization even if gthe level of ambition remains the same (e.g., 90%).

Thus ASEAN can gain additional liberalization even though it

7

Thus, ASEAN can gain additional liberalization even though it has FTAs with all the RCEP members .

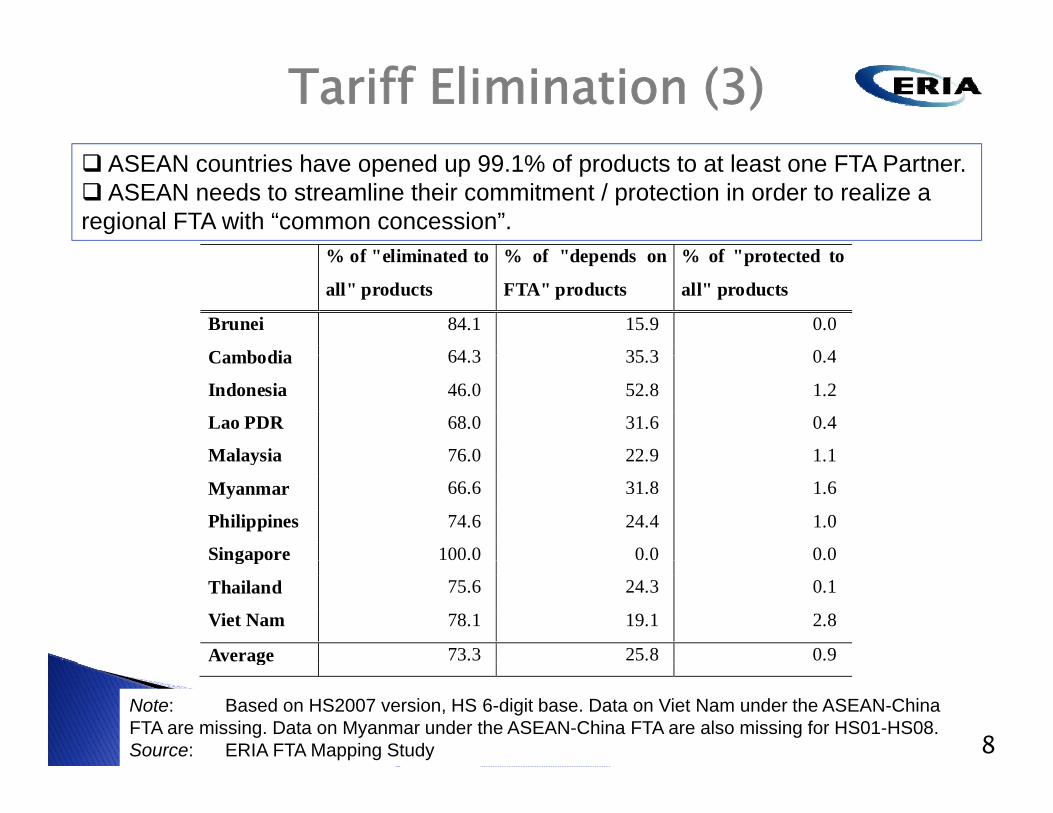

Tariff Elimination (3)

% f " li i t d t % f "d d % f " t t d t

ASEAN countries have opened up 99.1% of products to at least one FTA Partner. ASEAN needs to streamline their commitment / protection in order to realize a regional FTA with “common concession”.

% of "eliminated to

all" products

% of "depends on

FTA" products

% of "protected to

all" products

Brunei 84.1 15.9 0.0

Cambodia 64 3 35 3 0 4Cambodia 64.3 35.3 0.4

Indonesia 46.0 52.8 1.2

Lao PDR 68.0 31.6 0.4

Malaysia 76 0 22 9 1 1Malaysia 76.0 22.9 1.1

Myanmar 66.6 31.8 1.6

Philippines 74.6 24.4 1.0

Singapore 100.0 0.0 0.0g p

Thailand 75.6 24.3 0.1

Viet Nam 78.1 19.1 2.8

Average 73.3 25.8 0.9g

Note: Based on HS2007 version, HS 6-digit base. Data on Viet Nam under the ASEAN-China FTA are missing. Data on Myanmar under the ASEAN-China FTA are also missing for HS01-HS08.Source: ERIA FTA Mapping Study 8

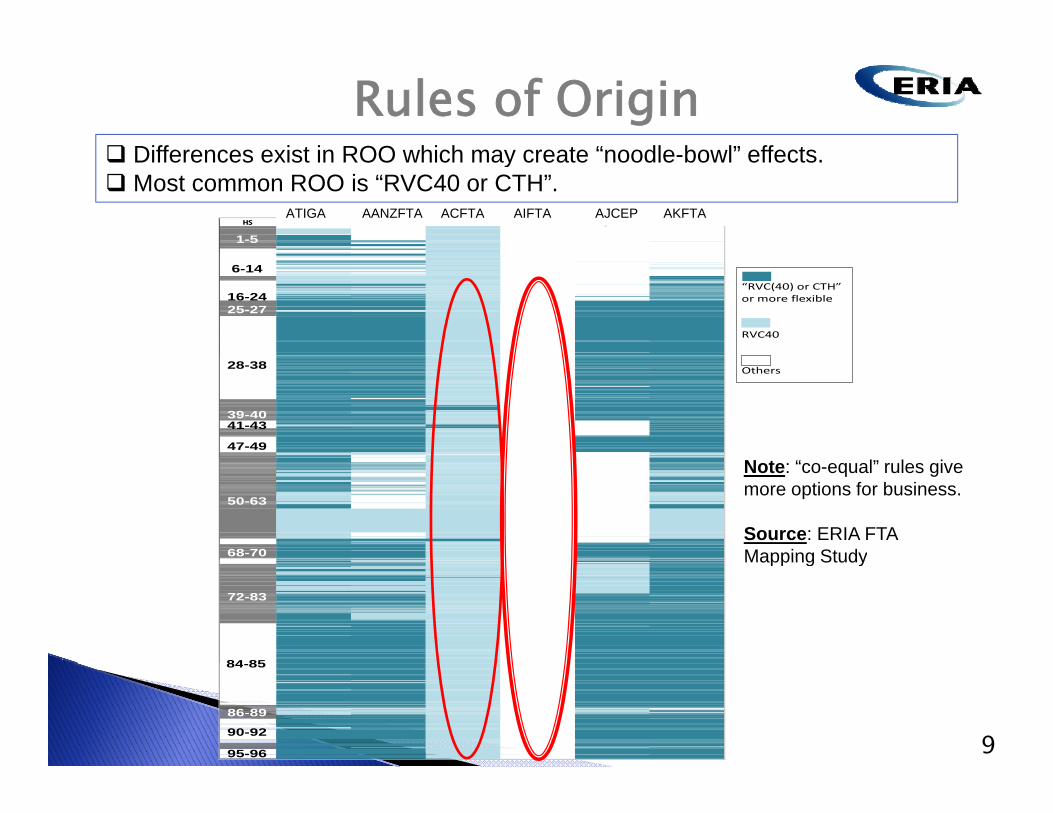

Rules of Origin Differences exist in ROO which may create “noodle bowl” effects

HS ATIGA AANZFTA ACFTA AIFTA AJCEP AKFTA

1-5

ATIGA AANZFTA ACFTA AIFTA AJCEP AKFTA

Differences exist in ROO which may create “noodle-bowl” effects. Most common ROO is “RVC40 or CTH”.

“RVC(40) or CTH”or more flexible RVC40

25-27

6-14

16-24

Others

39-40

28-38

41-43

47-49

50-63

68-70

Note: “co-equal” rules give more options for business.

Source: ERIA FTA Mapping Study

72-83

84 85

Mapping Study

986-89

84-85

90-92

95-96

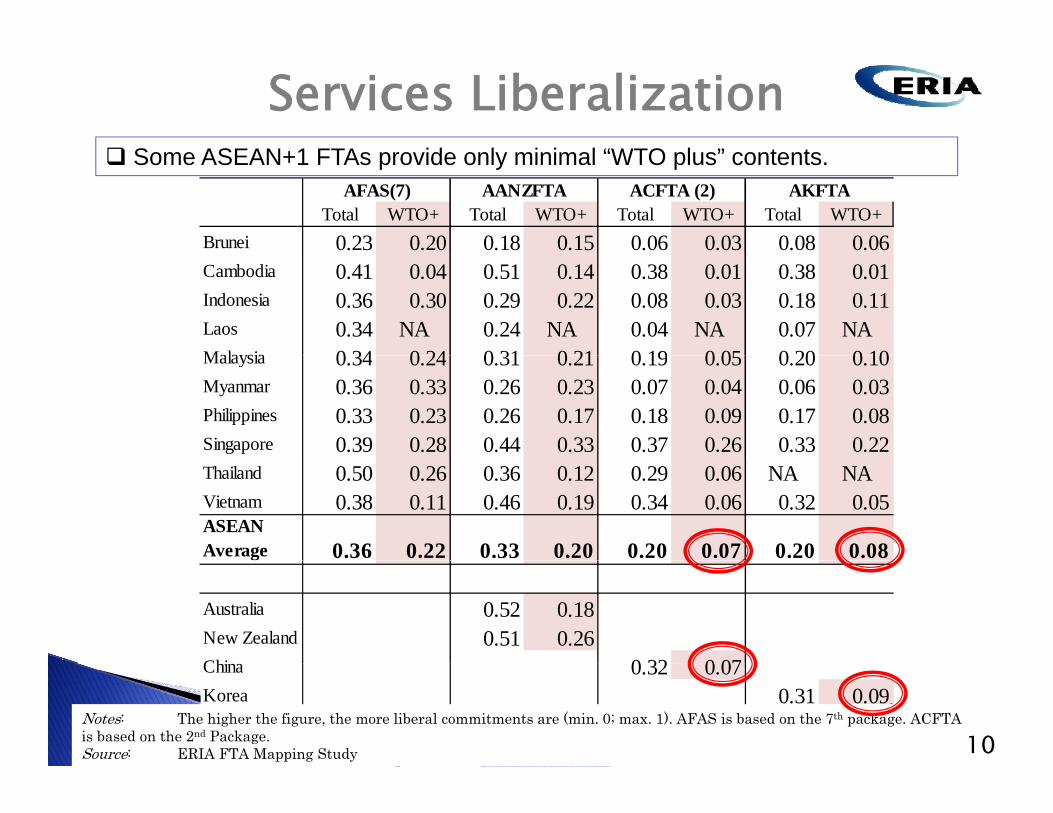

Services Liberalization S ASEAN 1 FTA id l i i l “WTO l ” t t

Total WTO+ Total WTO+ Total WTO+ Total WTO+Brunei 0.23 0.20 0.18 0.15 0.06 0.03 0.08 0.06

AFAS(7) AANZFTA ACFTA (2) AKFTA

Some ASEAN+1 FTAs provide only minimal “WTO plus” contents.

Cambodia 0.41 0.04 0.51 0.14 0.38 0.01 0.38 0.01Indonesia 0.36 0.30 0.29 0.22 0.08 0.03 0.18 0.11Laos 0.34 NA 0.24 NA 0.04 NA 0.07 NAMalaysia 0 34 0 24 0 31 0 21 0 19 0 05 0 20 0 10Malaysia 0.34 0.24 0.31 0.21 0.19 0.05 0.20 0.10Myanmar 0.36 0.33 0.26 0.23 0.07 0.04 0.06 0.03Philippines 0.33 0.23 0.26 0.17 0.18 0.09 0.17 0.08Singapore 0.39 0.28 0.44 0.33 0.37 0.26 0.33 0.22Thailand 0.50 0.26 0.36 0.12 0.29 0.06 NA NAVietnam 0.38 0.11 0.46 0.19 0.34 0.06 0.32 0.05ASEAN Average 0.36 0.22 0.33 0.20 0.20 0.07 0.20 0.08

Australia 0.52 0.18New Zealand 0.51 0.26Chi 0 32 0 07China 0.32 0.07Korea 0.31 0.09

Notes: The higher the figure, the more liberal commitments are (min. 0; max. 1). AFAS is based on the 7th package. ACFTA is based on the 2nd Package.Source: ERIA FTA Mapping Study 10

Potential Economic Impact on GDP of RCEP(Percentage Point, accumulated from 2011 to 2015) RCEP ill h th l t iti i i t ASEAN

13.414.0

16.0

RCEP will have the largest positive economic impacts on ASEAN.

9.58.3

8.0

10.0

12.0

2.3

5.8

3.0

5.0

3.3 2.9

2 0

4.0

6.0

0.0

2.0

ASEAN Coexistence of Five ASEAN+1 FTAsCoexistence of Five ASEAN+1 FTAs and CJK FTAASEAN+6 FTA (RCEP)

11

ASEAN+6 FTA (RCEP)

Note: Percentage Point, Accumulated from 2011 to 2015. Assumptions are: (a) complete elimination of the tariffs over the specified period of time, (b) reduction of ad valorem equivalents of service trade barriers, and (c) improvements in logistics cutting the ad valorem time.Source: Itakura for ERIA’s AEC Mid-term Review Study

How can we maximize the economic gains?gTrade in Goods “Common concession” in tariff schedules: common in A+1 FTA Consolidated ROOs with “co-equal” rules Cumulation rules: common in A+1 FTA Hi h l l f t iff li i ti Higher level of tariff elimination

Trade in Services Substantive “WTO Plus” components (more than A+1 FTAs)p ( )

Trade Facilitation Meaningful programs (many in ASEAN; but rare in A+1 FTAs)

Speed Speedy conclusion the key for “ASEAN Centrality”

12

“Open Accession Clause” (Principle 6)

1. “Any ASEAN FTA Partner that did not participate in the RCEP negotiations at the outset would be allowed to join the negotiations

p ( p )

negotiations at the outset would be allowed to join the negotiations, subject to terms and conditions that would be agreed with all other participating countries.”

AFPs can join during the negotiation --- but not the others.

2. “The RCEP agreement will also have an open accession clause to g penable the participation of any ASEAN FTA partner that did not participate in the RCEP negotiations and any other external economic partners after the completion of the RCEP negotiations.”

AFPs can join even after the conclusion of RCEP.

13 “Any other external economic partners” can also join the RCEP.

Condition for RCEP Accession?

1. “External economic partner” is a new terminology. We d ’t k h h th t ti ldon’t know who has the potential.

- ASEAN Charter Art. 44 uses “Dialogue Partner”, “Sectoral Dialogue Partner”, “Development Partner”, “Special Observer”, and “Guest”.

2 Th RCEP G idi P i i l i il t b t th2. The RCEP Guiding Principles is silent about the conditions that external economic partner should meet when acceding to RCEP. But, of course, there will be gsome conditions.“subject to terms and conditions that would be agreed with all other participating countries” (for AFPs to join the negotiation)

14

participating countries (for AFPs to join the negotiation)

ASEAN+1 FTA is a pre-condition?p

1. The biggest question is whether ASEAN+1 FTAs will be a condition to join the RCEPto join the RCEP.

2. The RCEP Guiding Principles explicitly distinguish the two wordings --- AFPs and EEPs.wordings AFPs and EEPs.(1) If “AFP” includes future AFP (e.g., HK), then EEP means somebody else --- no condition for A+1 FTA.(2) If “AFP” is fixed as the current 6 AFPs, then “EEP” may mean ( ) yfuture AFP --- A+1 FTA is still a condition.

3. If ASEAN+1 FTAs will become as a pre-condition…(1) It may enhance the “ASEAN Centrality” (cf. RCEP Guiding Principles; ASEAN Charter Art. 41.3);(2) The pace of expansion will be slower (maybe good, maybe bad for ASEAN); and

15

ASEAN); and,(3) Duplicate negotiation may take place.

Does Open Accession Work?p

1. We hope yes. But not quite sure.

2. TPP is originated from P4 (Singapore, Brunei, New Zealand and Chile). P4 had an open accession clause.

3. Does the current TPP negotiation utilize the P4 open accession clause? If not, why not? What was the , yproblem? Institutional design?

4 If a giant country (e g USA or EU) wishes to join4. If a giant country (e.g., USA or EU) wishes to join RCEP, can we use the RCEP open accession clause?(If China wants to join TPP, how does the open accession work?)

16 Further analysis is a necessary --- which requires

public access to the TPP negotiation process.

Some more potential implicationsp p

1. RCEP and TPP: Can we converge the two towards an FTAAP? Whi h i hi h lit ? ( t iffFTAAP? Which one is higher quality? (common tariff schedule and liberal ROOs?)

2. Expansion of ASEAN++ agreements in non-trade economic areas?

3. RCEP Secretariat? Implication to the ASEAN Secretariat?

4. Influence of RCEP on other regional initiatives. TPP and Alliance Pacifico?

17

Please Visit ERIA Webpage for more FTA studies: http://www eria org/research/ftaepa/http://www.eria.org/research/ftaepa/

18