12 october 2004 pharma summit 2004 - kpmg pharma summit 2004.pdf · ranbaxy among the top 100 drug...

TRANSCRIPT

1©2004 KPMG Advisory Services Private Limited, an Indian body corporate, is the sub-licensee of KPMG, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved."

12 OCTOBER 2004

Pharma Summit 2004

India Pharma Inc- Leveraging Emerging Opportunities

Pharma Summit 2004

India Pharma Inc- Leveraging Emerging Opportunities

A D V I S O R Y

Opportunities and Projections

An Overview

2©2004 KPMG Advisory Services Private Limited, an Indian body corporate, is the sub-licensee of KPMG, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved."

Agenda Agenda

Global forces of change

Emerging opportunities

Projections and Imperatives

3©2004 KPMG Advisory Services Private Limited, an Indian body corporate, is the sub-licensee of KPMG, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved."

Global Global forces of changeforces of change

4©2004 KPMG Advisory Services Private Limited, an Indian body corporate, is the sub-licensee of KPMG, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved."

Global Global PharmaPharma Co profits are under pressure . . .Co profits are under pressure . . .

Higher cost of

drugs

Higher cost of

R & D Pressure to lower price/

discount

Profitability

Time to market

RegulatoryRequirements

Parallelimports Prescription of

generics

Government’scontrol over Prescription expenditure

Newtechnologies

Control overprice ofbranded

drugs

Higher cost for new product approval

Loss of marketshare

Lower sales(in value)

Higher cost of

healthcareMore

Demandingpatients

Health information over the net

. . . with simultaneous pressures from costs and prices

5©2004 KPMG Advisory Services Private Limited, an Indian body corporate, is the sub-licensee of KPMG, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved."

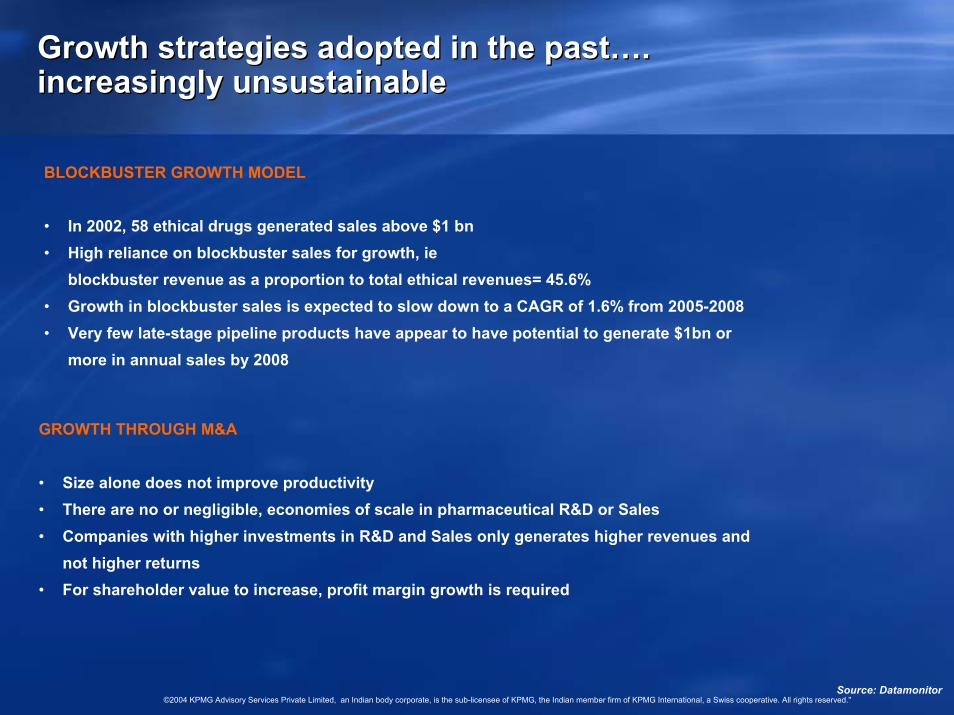

Growth strategies adopted in the pastGrowth strategies adopted in the past……..increasingly unsustainableincreasingly unsustainable

BLOCKBUSTER GROWTH MODEL

• In 2002, 58 ethical drugs generated sales above $1 bn • High reliance on blockbuster sales for growth, ie

blockbuster revenue as a proportion to total ethical revenues= 45.6%• Growth in blockbuster sales is expected to slow down to a CAGR of 1.6% from 2005-2008• Very few late-stage pipeline products have appear to have potential to generate $1bn or

more in annual sales by 2008

GROWTH THROUGH M&A

• Size alone does not improve productivity• There are no or negligible, economies of scale in pharmaceutical R&D or Sales• Companies with higher investments in R&D and Sales only generates higher revenues and

not higher returns• For shareholder value to increase, profit margin growth is required

Source: Datamonitor

6©2004 KPMG Advisory Services Private Limited, an Indian body corporate, is the sub-licensee of KPMG, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved."

Declining R&D and Sales productivityDeclining R&D and Sales productivity

No of Products

Low and declining:• 1 in every 5000- 10000

compounds approved• R&D/Sales rose from 9.3% to

16.3% from 1970-2002• US r&D spend to overtake

sales by 2015

True innovation is rare and therapy remains palliative

• Surge in generic competition• 40% of blockbusters in 2002 to

lose patent protection by 2008

X Revenue Potential

Long development timelines erode marketed patent life

• Up to 14 yrs for drug to reach market

• Admin delays launch for ~ 18 months

Time

High R&D costs• R&D/new molecular entity

approval ~ $802 m, projected to touch $1bn by 2005

• Expensive new enabling technologies

X Investment∝R&D PRODUCTIVITY

SALES PRODUCTIVITY ∝ No of Reps ↑Targeting small

group of Physicians

Decreasing detailing time &

less effective visitsROI ↓

Source: Datamonitor

7©2004 KPMG Advisory Services Private Limited, an Indian body corporate, is the sub-licensee of KPMG, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved."

Causing a deepening productivity crisisCausing a deepening productivity crisis

• Productivity drives shareholder value but productivity is declining

• Companies are investing more in current operations to maintain productivity, particularly via M&A

But, there are no scale economies in R&D or sales and marketingRevenues are directly proportional to S,G&A spend and rep headcountPipeline value is directly proportional to R&D spend and R&D headcountTherefore, size is not an advantage in increasing shareholder value

• Productivity drives shareholder value but productivity is declining

• Companies are investing more in current operations to maintain productivity, particularly via M&A

But, there are no scale economies in R&D or sales and marketingRevenues are directly proportional to S,G&A spend and rep headcountPipeline value is directly proportional to R&D spend and R&D headcountTherefore, size is not an advantage in increasing shareholder value

Operating profit

Revenue

HighCurrent degreeof company focus

returns, not revenues

Co

rrel

atio

n w

ith

SH

V

EVA

Net profit

LowLow

High

Growth strategies must focus on profits and

An alternative growth strategy is requiredCurrent position of metric

Ideal position of any metric

Recommended strategic shiftSource: Datamonitor

8©2004 KPMG Advisory Services Private Limited, an Indian body corporate, is the sub-licensee of KPMG, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved."

Networked Networked PharmaPharma……an emerging growth modelan emerging growth model

BASED ON PRINCIPLES OF INCREASED COLLABORATION AND OUTSOURCING

• Keep in-house only the intellectual capital that is core to competitive advantage and outsource the rest through strategic alliances and vendor contracts

• Leverage the resources, expertise and efficiencies of alliance partners/vendors thus enhancing portfolio at reduced costs

• Enable cost effective management of fluctuating and specialist resource demands, thus reducing overall costs and risk exposure

Discovery Product Development Manufacturing Sales Distribution

Benefits of collaborating/outsourcing

Global Pharmaceutical Industry- Networked Business Model

Broader technology base, hence higher synergies, greater productivity and reduces risks

Reduced timeReduced costs

Reduced costs

Increased efficiency through leveraging vendors expertise

Increased flexibility at lower costs

Reduced risks of lower RoI

Faster expansion

Increased flexibility at lower costs

Increased efficiency through leveraging vendors expertise

9©2004 KPMG Advisory Services Private Limited, an Indian body corporate, is the sub-licensee of KPMG, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved."

India Pharma IncIndia Pharma IncEmerging OpportunitiesEmerging Opportunities

10©2004 KPMG Advisory Services Private Limited, an Indian body corporate, is the sub-licensee of KPMG, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved."

How is India Pharma Inc positioned given the global landscape?

The Indian Pharmaceutical Industry

Strengths• Large untapped

domestic market• Fast changing

lifestyles• Low cost

manufacturing• High chemistry and

process reengineering skills

• Quick adoption of new technology

• Strong research talent pool

• Rich Biodiversity• Strong Marketing and

distribution network

Threats• 2005 IPR regime implies

drying up of product pipeline for Indian companies

• Lack of R&D enabling regulatory environment

• Pricing pressures imposed by DPCO

• China threat• Ambiguity on VAT• Loopholes in the Patent

Bill• EXIM policy

Domestic market perspective

Global market perspective

Weaknesses• Lack of product patents• Low Investments in

innovative R&D• Lack of pricing power

impacts growth• Characterised by low

margins• Low healthcare spends• Highly fragmented

industry• Inadequate regulatory

standards• Spurious drug sales

Opportunities• Potential to absorb high

priced products and Changing demographic and socio economic profile

• Opening up of the health insurance sector

• Product patent protection from 2005

• Escalating R&D costs across the world

• Pressure on global pharma to reduce costs

• Large number of drugs going off patent

• Low potential product pipeline

• Opening of OTC segment

11©2004 KPMG Advisory Services Private Limited, an Indian body corporate, is the sub-licensee of KPMG, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved."

Towards establishing a global footprint…

Products • Indian Companies accounted for over 30% of the DMFs filed in the US in 2003

• India’s share of ANDA filings has been rising and stood at around 23% in 2003

• Successful patent challenges• India recognised as a potential global manufacturing hub:

Highest number of USFDA approved plants outside the US• Production costs lower than the US by upto 50%

Geographies• Ranbaxy among the top 100 drug companies worldwide and ranked

the 15th fastest growing company in the world • Indian players together have covered close to 90% of the potential

generics pipeline• Increasing number of overseas acquisitions made by Indian

companies with different strategic objectives

Distribution and Manufacturing facilities

USCaraco Pharma

Sun Pharma

UKCP PharmaWockhardt

Marketing ConsolidationGermanyVeratideRanbaxy

Manufacturing expertiseUSSignatureRanbaxy

Market Entry StrategyUKBMSDr Reddy’s Labs

Market Entry StrategyFranceRPG AventisRanbaxy

Key DriverCountryTargetAcquirer

Illustrative, not exhaustiveIndustry sources

12©2004 KPMG Advisory Services Private Limited, an Indian body corporate, is the sub-licensee of KPMG, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved."

Towards establishing a global footprint…

Alliances• Increasing dependence on India:

Innovator companies for collaborative and contract research and manufacturing to capitalise on the low cost baseGenerics players to enhance their first-to-file position, expand product portfolio and reduce costs

Services• Indian Pharma companies have entered into licensing deals with

Global players like Bayer, Novartis and Novo Nordisk

• GSK –Ranbaxy collaborative research deal signed despite Ranbaxy having challenged it on its blockbuster product Ceftin

Global Pharmaceutical / Biotechnology organisations and leading R&D service providers targeting India as a resource base:

−Pfizer set up a Biometric Center in India in 1997

−J&J established the Jansen International stability center in 1999 for global analytical services

−Novartis set up the International Clinical Development Centerin 2002 to support the statistical needs of the global research team

13©2004 KPMG Advisory Services Private Limited, an Indian body corporate, is the sub-licensee of KPMG, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved."

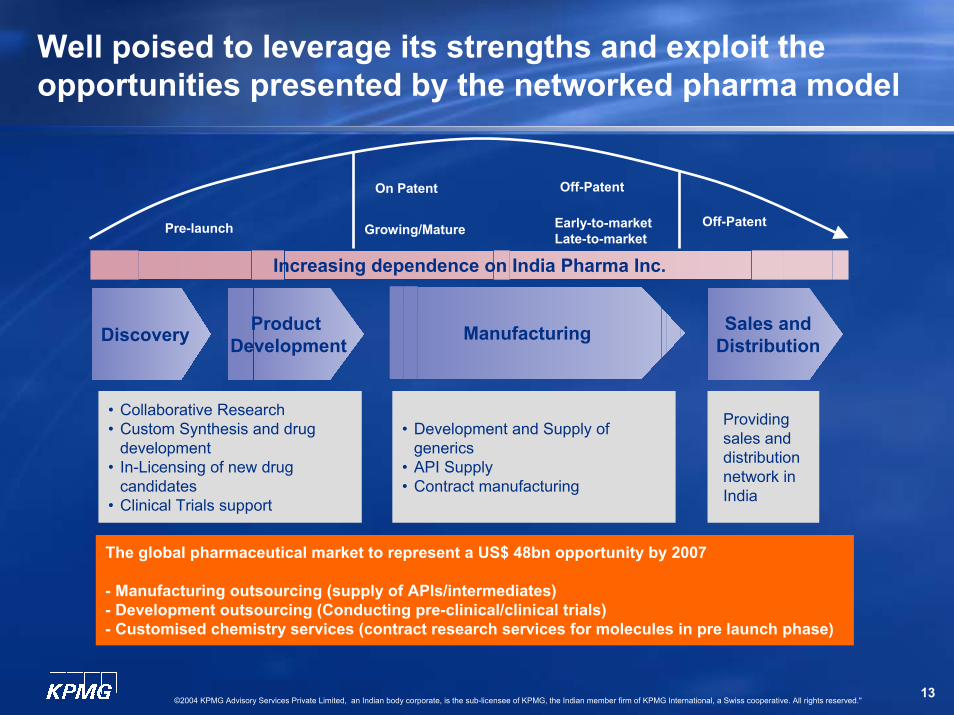

Well poised to leverage its strengths and exploit the opportunities presented by the networked pharma model

• Collaborative Research• Custom Synthesis and drug

development• In-Licensing of new drug

candidates• Clinical Trials support

• Development and Supply of generics

• API Supply• Contract manufacturing

Providing sales and distribution network in India

Discovery Product Development Manufacturing Sales and

Distribution

Increasing dependence on India Pharma Inc.

Pre-launch

On Patent Off-Patent

Growing/Mature Early-to-marketLate-to-market

Off-Patent

The global pharmaceutical market to represent a US$ 48bn opportunity by 2007

- Manufacturing outsourcing (supply of APIs/intermediates)- Development outsourcing (Conducting pre-clinical/clinical trials)- Customised chemistry services (contract research services for molecules in pre launch phase)

14©2004 KPMG Advisory Services Private Limited, an Indian body corporate, is the sub-licensee of KPMG, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved."

Drug discovery and product development

Enablers• World’s largest pool of trained

analytical and development chemists• Track record of innovation• Low cost advantages• Rapid time to market• Impending Patent regime forcing an

increased focus and hence investments in R&D

• Vast, diverse patient population

Opportunities• Research services like

bioinformatics, structure based drug design

• Development services including clinical trials and data management

• Support launch of NCEs through analog research, custom synthesis, NDDS and emerging therapies

Con

verte

d do

sage

form

Com

plex

ity

Inte

rmed

iate

s an

d B

ulk

Act

ives

Com

mod

ity g

ener

ic

Gen

eric

Mar

ket B

ulk

Dev

elop

ed c

ount

ries

Gen

eric

mar

ket A

ND

A

Valu

e ad

ded

and

bran

ded

gene

rics

ND

DS

NM

E/N

CE

s

Returns

Process Reengineering DMF & ANDA NDA

Low

High

High

Ranbaxy, DRL, Cipla, Lupin, Matrix, Divis, Neuland, Aurobindo, Orchid

Ranbaxy, DRL, Cipla

Ranbaxy. DRL

Potential going forward• Per Frost and Sullivan, the CRO industry is

expected to grow frm US$7.8bn in 2002 to US$14.4bn in 2007India can offer a savings of upto US$ 120-200mn on a drug development base of US$500-900mn”

Cost per patient - vast patient populationCost per investigator - highly trained medical professional poolCost and efficiency of analysis - strong data management capabilities

- emerging CRO infrastructurePreclinical development costs - strong synthesis capabilitiesShortening the cycle time - fast recruitment, accelerated approvals

- regulatory facilitation of parallel phase studies

Key Drivers

Cost per patient - vast patient populationCost per investigator - highly trained medical professional poolCost and efficiency of analysis - strong data management capabilities

- emerging CRO infrastructurePreclinical development costs - strong synthesis capabilitiesShortening the cycle time - fast recruitment, accelerated approvals

- regulatory facilitation of parallel phase studies

Key Drivers

15©2004 KPMG Advisory Services Private Limited, an Indian body corporate, is the sub-licensee of KPMG, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved."

Product sourcing

Enablers• Highest number of USFDA plants

outside the US• Vertical integration key to low cost

structure• Production costs lower than US by

upto 50%• Strong reverse engineering and

process improvement skills• Quick technology adaptation

Opportunities• Contract manufacturing- working

with innovators, especially in pre launch/early in life cycle

• Support unique needs of Specialty pharma- patent challenges, synthesising rare ingredients

• Sourcing base for generic players

Potential going forward• Over 2004-2008, ~US$ 70bn worth of branded

drugs to face patent expiration- more than doubling the patent cycle opportunity

• ANDA filings expected to double (~145 in 2004 against 66 in 2003)

• Global bulk manufacturing outsourcing space to grow to about US$17bn by 2007

NicholasOpthalmicsAllergan

MatrixShasun

AcyclovirRanitidine

GSK

JubilantAPI supplies, Intermediates

Novartis, Syngenta, Sanofi, Aventis, Lilly

Zydus CadilaPantoprazole Intermediates

Altana

Aventis IndiaShasun

GlibenclamideIbuprofen

AventisLupinCephalosporinsMerck GenericsLupinIntermediatesWyethLupinIntermediatesCyanamidWockhardtRange of APIsFerring

RanbaxyDoxycyline, amoxyccillin API

Bristol Myers Squibb

RanbaxyShasun

Range of APIsNizatidine

Eli LillySupplierProduct sourcedGlobal Pharmaco

Illustrative, not exhaustiveIndustry sources

16©2004 KPMG Advisory Services Private Limited, an Indian body corporate, is the sub-licensee of KPMG, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved."

Generic Biologics

Enablers• World’s largest pool of trained

analytical and development chemists• Expertise in recombinant

technologies, microbial fermentation as well as mammalian cell technology

• Low cost advantages

Opportunities• Set up capacity to develop biological

generics• Drug Discovery and development

opportunitiesPotential going forward• Global market estimated at US$35bn• Over the next five years, more than US$10bn

worth of biologics will lose patent protection• Widening supply-demand gap anticipated due to

severe production capacity constraints

• Wockhardt• launch of indigenously developed

Hepatitis B Vaccine• Recombinant human insulin

• Biocon• Established JV with Cuban company

CIMAB to manufacture and sell biologics produced by CIMAB in India

• Well underway in the monoclonal antibody space, working on an anti-cancer antibody undergoing clinical trials in Canada

• Suppliers contract agreement with Bristol Myers Squibb

• Bharat Biotech- contract manufacturing for Wyeth

17©2004 KPMG Advisory Services Private Limited, an Indian body corporate, is the sub-licensee of KPMG, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved."

Offshore support to other business processes

Enablers• Scalable, low cost workforce• 40-50% savings to be derived• Increased productivity• Time zone advantage• Strong technology capability

Data Entry

Analyticsand otherservices

Finance/ Accounts

Processing & Reporting

Call Centers• Collections• Cust.Serv.

• Technology Help Desk

• Research

Remote services in India

ILLUSTRATIVE

Opportunities• Data analytics supporting drug

development and clinical trials• Biometric and statistical analysis• Back office processing- Finance and

accounts, MIS, etc• IT support- application development

& maintenance, Infrastructure management, helpdesk, etc

Potential going forward• Estimated savings of upto 50% (of

the cost of the support function) to be derived by off-shoring to India

18©2004 KPMG Advisory Services Private Limited, an Indian body corporate, is the sub-licensee of KPMG, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved."

Projections andImperativesImperatives

19©2004 KPMG Advisory Services Private Limited, an Indian body corporate, is the sub-licensee of KPMG, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved."

Leveraging emerging opportunities – Key Challenges

Sustaining Growth and Profitability• Increasing investment requirements• Intensifying competition• Strained top line• Widening risk portfolio • Need to secure base cash flows as

companies move up the value chain

Volatility of earningsEmerging from• Evolving industry structure and fast

commoditisation of generics• Price erosion• Unsuccessful patent challenges• Skewed product / therapeutic segment

dependency

Intensifying competition among Indian players

• Domestic competition mandates low prices and low margins, thus affecting profitability

• On the Global front, multiple ANDA filings erode prices significantly thus shrinking the profit pie

• Players channeling resources in overlapping areas/segments

Evolving Global Landscape

• Emergence of authorised generics

• Shared exclusivity

Transitioning from strong Global position to true global leaders

• Ability to withstand shocks and consistently deliver profitable growth

• Secure domestic position• Focus on operational excellence• Prepare for globalisation

20©2004 KPMG Advisory Services Private Limited, an Indian body corporate, is the sub-licensee of KPMG, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved."

Success of players will hinge on…

Strength of existingproduct portfolio andpipeline of products

Focus on research and development with high success rates

Presence in growth markets andsegments

Access to proprietary technology Ability to manage costs

21©2004 KPMG Advisory Services Private Limited, an Indian body corporate, is the sub-licensee of KPMG, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved."

Adopting different growth strategies

Maintain the domestic competitive advantage• Upgrade facilities to comply with global

standards• Increase investments in R&D• Constantly monitor and trim the cost base• Sustain top line

Hence leveraging the domestic landscape to hone competitive advantage

Adopt a multi-dimensional stable business model

• Spanning across product/services offerings ranging from supplying API’s and formulations to providing research and development services

• Balanced portfolio- ie stable generic base with high risk- high reward patent challenges as well

• Diversify into new geographies , across regulated and unregulated markets

Focus on niche, technology intensive drugs

• Markets with fewer players• Offering higher margins and returns• Enable scaling up and gaining critical

mass early• Strengthen R&D base

Build Critical Mass• Key to the high volume generic model• Explore opportunities for inorganic growth• Consolidation within the domestic sector to

leverage of another’s expertise while consolidating own core competence

Differentiate• Focus on core competency to differentiate

and position product/service thus attracting collaboration/outsourcing opportunities

Partner of Choice• Leverage existing network and resources

and become partner of choice for product launches for MNCs that do not have presence in India

22©2004 KPMG Advisory Services Private Limited, an Indian body corporate, is the sub-licensee of KPMG, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved."

Thus realising a vision of becoming a global pharmaceutical powerhouse

Sourcing API’s

Intermediates Formulations

Drug Discovery

Contract Research

Bioinformatics

Custom Synthesis Business

Process Support

Drug Development

INDIA INDIA PHARMA PHARMA

INC.INC.

Licensing

Distribution in India

Technology Support

23©2004 KPMG Advisory Services Private Limited, an Indian body corporate, is the sub-licensee of KPMG, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved."

Presenter’s contact details

Shalini PillayAssociate DirectorKPMG Advisory Services Pvt Ltd+91 (080) 2 227 [email protected]

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.