111027 wessanen q3 2011 final

TRANSCRIPT

press release

Q3 2011: Wessanen’s next consecutive quarter with progression

Q3 autonomous revenue growth +8.0% (5.2% volume)

Grocery continues to perform well

ABC showing very strong performance in third quarter

Press release 27 October 2011

Page 2 of 15

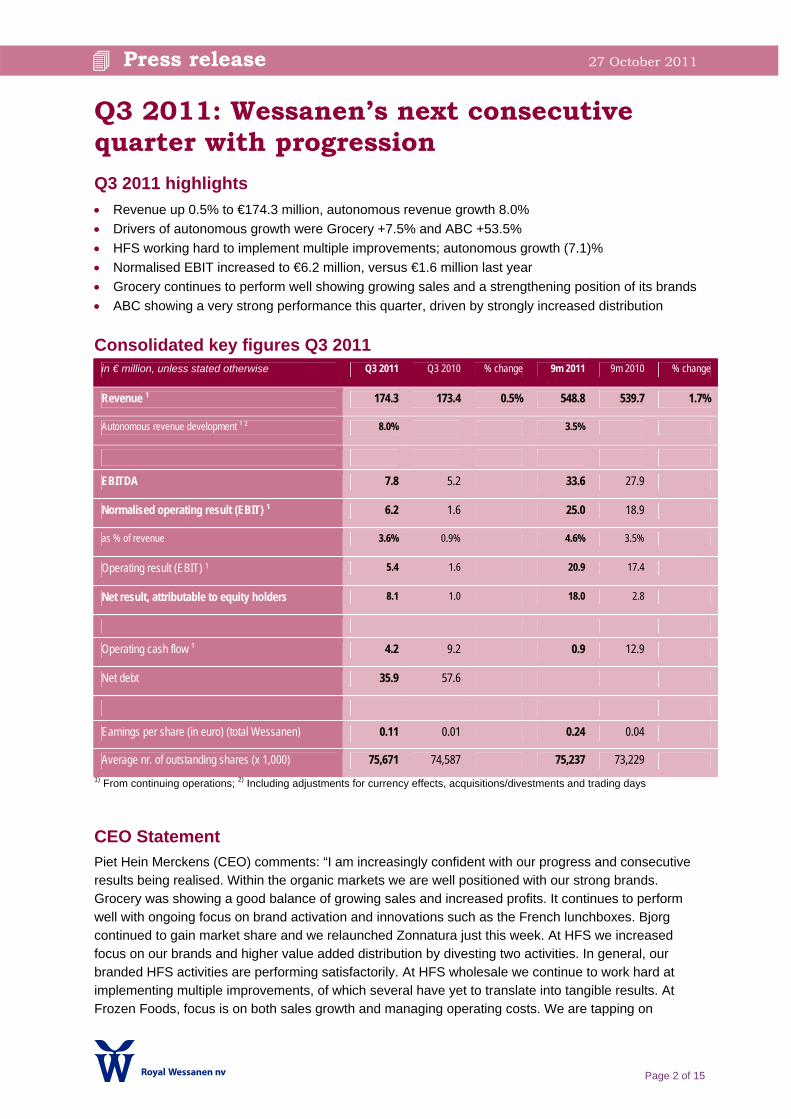

Q3 2011: Wessanen’s next consecutive quarter with progression Q3 2011 highlights • Revenue up 0.5% to €174.3 million, autonomous revenue growth 8.0% • Drivers of autonomous growth were Grocery +7.5% and ABC +53.5% • HFS working hard to implement multiple improvements; autonomous growth (7.1)% • Normalised EBIT increased to €6.2 million, versus €1.6 million last year • Grocery continues to perform well showing growing sales and a strengthening position of its brands • ABC showing a very strong performance this quarter, driven by strongly increased distribution

Consolidated key figures Q3 2011 in € million, unless stated otherwise Q3 2011 Q3 2010 % change 9m 2011 9m 2010 % change

Revenue ¹ 174.3 173.4 0.5% 548.8 539.7 1.7%

Autonomous revenue development ¹ ² 8.0% 3.5%

EBITDA 7.8 5.2 33.6 27.9

Normalised operating result (EBIT) ¹ 6.2 1.6 25.0 18.9

as % of revenue 3.6% 0.9% 4.6% 3.5%

Operating result (EBIT) 1 5.4 1.6 20.9 17.4

Net result, attributable to equity holders 8.1 1.0 18.0 2.8

Operating cash flow ¹ 4.2 9.2 0.9 12.9

Net debt 35.9 57.6

Earnings per share (in euro) (total Wessanen) 0.11 0.01 0.24 0.04

Average nr. of outstanding shares (x 1,000) 75,671 74,587 75,237 73,229 1) From continuing operations; 2) Including adjustments for currency effects, acquisitions/divestments and trading days

CEO Statement Piet Hein Merckens (CEO) comments: “I am increasingly confident with our progress and consecutive results being realised. Within the organic markets we are well positioned with our strong brands. Grocery was showing a good balance of growing sales and increased profits. It continues to perform well with ongoing focus on brand activation and innovations such as the French lunchboxes. Bjorg continued to gain market share and we relaunched Zonnatura just this week. At HFS we increased focus on our brands and higher value added distribution by divesting two activities. In general, our branded HFS activities are performing satisfactorily. At HFS wholesale we continue to work hard at implementing multiple improvements, of which several have yet to translate into tangible results. At Frozen Foods, focus is on both sales growth and managing operating costs. We are tapping on

Press release 27 October 2011

Page 3 of 15

improvement initiatives to grow the top line and bottom line. ABC realised a very strong quarter driven by the success of gaining additional distribution for ready-to-drink pouches and production efficiencies. Going forward, we are cautiously optimistic. We have a strong team in place and the execution of our strategy is progressing. Some signs of improvement are already showing in different areas, for example at Grocery, whereas in some other areas improvements are yet to be seen and remain the focus of our efforts. We also have to deal with an element of uncertainty due to persistently subdued European economic environment and pressured consumer confidence. Despite these macro-economic challenges we are firmly determined to improve our performance step-by-step and further solidify our positions and brands in the European organic markets.”

Financial guidance FY 2011 • Net financing costs expected to reach €3-4 million • The effective tax rate expected to be 25-30% (excluding the recognition of deferred tax assets) • Capital expenditures expected to be €10-11 million • Depreciation and amortisation (excl. impairments) expected to be about €14 million • Non-allocated expenses (including corporate expenses) expected to be around €10 million

Financial summary Q3 2011 In Europe, the weak economic environment persisted and is characterised by pressured consumer confidence. However, consumer spend on food however continues to trend positively. Growth of the organic food markets clearly outpaces this trend with awareness and appreciation for organic food continuing to grow.

Autonomous revenue growth 8.0% Revenue increased 0.5% to €174.3 million. Autonomous growth amounted to 8.0% with price/mix effects contributing 2.8% and volume effects 5.2%. This was driven by strong growth at Grocery of 7.5% and ABC of 53.5%. Frozen Foods showed autonomous growth of 0.8% reversing several quarters of decline, while HFS was down 7.1%. More than 2% of the decline at HFS was due to a weak performance of Kalisterra (which was divested as of 1 October). The divestment of Tree of Life UK per mid-July had a negative impact of 4.8%, while there was a negative currency effect of 1.9% due to a weaker British pound and US dollar.

Breakdown sales Q3 2011

ABC21%

Grocery33%

HFS31%

Frozen Foods15%

Normalised EBIT €6.2 million (Q3 2010: €1.6 million) Normalised EBIT increased by €4.6 million to €6.2 million, up strongly versus last year’s €1.6 million due to strong performances at Grocery and ABC. EBIT increased to €5.4 million impacted by the recycling of a (non-cash) exchange loss deferred in equity following divestment of Tree of Life UK, a positive impact of €0.8 million of the net reversal of impairment losses at ABC and some positive exceptional costs of €0.4 million. Net financing costs were stable at €(1.1) million (Q3 2010: €(1.0) million). Although interest expenses decreased due to a decrease in drawn amounts, the defined benefit interest expenses increased. Total income taxes amounted to €3.8 million positive versus (Q3 2010: €0.3 million positive). This income tax gain is mainly caused by the recognition of unrecognised tax carry forward losses in the United States resulting in a deferred tax asset of €4.7 million at quarter-end.

Press release 27 October 2011

Page 4 of 15

In € million Normalised EBIT → EBIT (incl. exceptionals and impairments)

6.2 Normalised EBIT

0.2 Grocery Release of restructuring provisions

(2.0) HFS Mainly exchange loss deferred in equity (divestment Tree of Life UK per 18 July)

0.2 ABC Minor asset adjustments

0.8 ABC Net reversal of impairment losses

5.4 EBIT

Net result attributable to equity holders amounted to €8.1 million (Q3 2010: €1.0 million). Earnings per share amounted to €0.11 (Q3 2010: €0.01). Operating cash flow from continuing operations (after interest and income tax paid) was €4.2 million, mainly as a result of the operational profits generated. Working capital increased €8.9 million versus the previous quarter, mainly driven by factoring. Due to the ongoing improved financial position of the company, factoring of debtors (at 30 June: €9.2 million) was ended per this quarter resulting in an increase of trade receivables.

Net debt decreased to €35.9 million; debtor factoring ended Net debt fell to €35.9 million (Q2 2011: €39.1 million) despite the discontinuation of debtor factoring in France. The net debt to EBITDA ratio amounted to 0.9x as at 30 September (Q2 2011: 1.1x).

0

50

100

150

200

Q3 09 Q4 09 Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 110.00

1.25

2.50

3.75

5.00

Net debt (in € mln) Leverage ratio

Grocery HFS Frozen Foods ABC Non-allocated Wessanen in € million, unless

stated otherwise Q3 2011

Q3 2010

Q3 2011

Q3 2010

Q3 2011

Q3 2010

Q3 2011

Q3 2010

Q3 2011

Q3 2010

Q3 2011

Q3 2010

Revenue 57.5 54.6 54.7 68.3 27.3 27.1 37.7 26.5 (2.9) (3.1) 174.3 173.4

Normalised EBIT 3.8 2.2 (0.5) 1.4 0.2 1.1 5.2 (0.7) (2.5) (2.4) 6.2 1.6

As % of revenue 6.6% 4.0% (0.9)% 2.0% 0.7% 4.1% 13.8% (2.6)% - - 3.6% 0.9%

Exceptionals 0.2 - (2.0) - - - 0.2 - - - (1.6) -

Impairments - - - - - - 0.8 - - - 0.8 -

EBIT 4.0 2.2 (2.5) 1.4 0.2 1.1 6.2 (0.7) (2.5) (2.4) 5.4 1.6

Press release 27 October 2011

Page 5 of 15

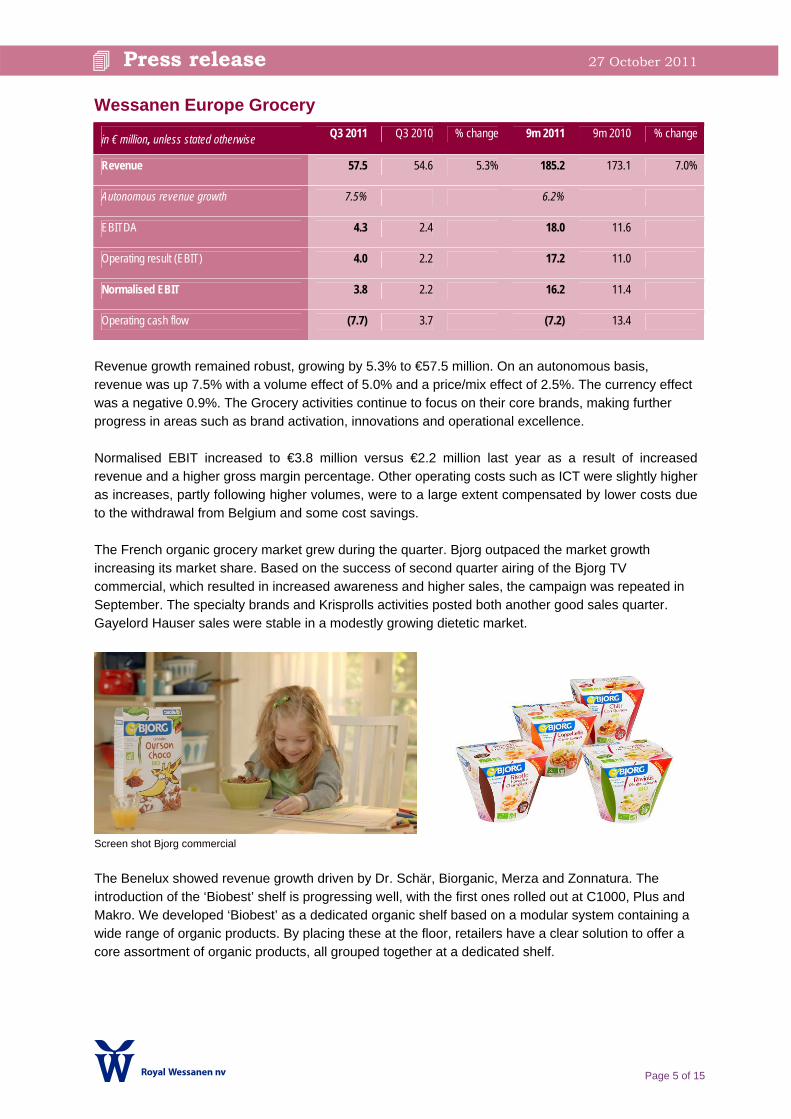

Wessanen Europe Grocery

in € million, unless stated otherwise Q3 2011 Q3 2010 % change 9m 2011 9m 2010 % change

Revenue 57.5 54.6 5.3% 185.2 173.1 7.0%

Autonomous revenue growth 7.5% 6.2%

EBITDA 4.3 2.4 18.0 11.6

Operating result (EBIT) 4.0 2.2 17.2 11.0

Normalised EBIT 3.8 2.2 16.2 11.4

Operating cash flow (7.7) 3.7 (7.2) 13.4

Revenue growth remained robust, growing by 5.3% to €57.5 million. On an autonomous basis, revenue was up 7.5% with a volume effect of 5.0% and a price/mix effect of 2.5%. The currency effect was a negative 0.9%. The Grocery activities continue to focus on their core brands, making further progress in areas such as brand activation, innovations and operational excellence. Normalised EBIT increased to €3.8 million versus €2.2 million last year as a result of increased revenue and a higher gross margin percentage. Other operating costs such as ICT were slightly higher as increases, partly following higher volumes, were to a large extent compensated by lower costs due to the withdrawal from Belgium and some cost savings. The French organic grocery market grew during the quarter. Bjorg outpaced the market growth increasing its market share. Based on the success of second quarter airing of the Bjorg TV commercial, which resulted in increased awareness and higher sales, the campaign was repeated in September. The specialty brands and Krisprolls activities posted both another good sales quarter. Gayelord Hauser sales were stable in a modestly growing dietetic market.

Screen shot Bjorg commercial The Benelux showed revenue growth driven by Dr. Schär, Biorganic, Merza and Zonnatura. The introduction of the ‘Biobest’ shelf is progressing well, with the first ones rolled out at C1000, Plus and Makro. We developed ‘Biobest’ as a dedicated organic shelf based on a modular system containing a wide range of organic products. By placing these at the floor, retailers have a clear solution to offer a core assortment of organic products, all grouped together at a dedicated shelf.

Press release 27 October 2011

Page 6 of 15

At the end of October, Zonnatura launched a sizeable activation campaign focusing on organic teas and its natural taste. The 360º activation campaign consists of multimedia and in-store promotions such as radio commercials, outdoor posters, television ‘bumpers’ around the most popular Dutch sitcom, social media, in-store tasting and second placement displays. The new packaging is available in all stores. The UK grocery environment continues to be tough. Our revenue was impacted by the focus on further de-emphasising private labels and ‘cutting the tail’, a programme we are executing to delist low margin, low volume products.

Dairy alternatives are one of our European core categories. In the UK we opted for one strong brand and therefore we phased out So Good. A range of soy milks was relaunched under the Kallo brand at the end of the quarter.

This rebranding has been supported by a programme of posters, press and digital support. Within savoury biscuits the new packaging is filtering through on the shelf.

In Italy, we continue to work on expanding our distribution coverage, resulting in growing volumes. In Germany, the grocery market is modestly up. However, our sales continue to grow strongly, albeit from a low base, driven by higher volumes of Whole Earth and Culinessa. In the quarter, Bjorg was launched on the German market. Bjorg with its nutritional positioning is complementary to the indulgence positioning of Whole Earth. Overall distribution gains were realised due to additional listings. Marketing spending increased to enhance support for Whole Earth and the launch of a second meter of organic shelf (with Bjorg) at retailers. Our range of Whole Earth Inka Taler Amaranth cookies won an award as one of the top 2012 organic brands by the magazine ‘Lebensmittel Praxis’.

Press release 27 October 2011

Page 7 of 15

Wessanen Europe Health Food Stores (HFS) in € million, unless stated otherwise Q3 2011 Q3 2010 % change 9m 2011 9m 2010 % change

Revenue 54.7 68.3 (19.9)% 194.2 212.5 (8.6)%

Autonomous revenue growth (7.1)% (6.5)%

EBITDA (2.0) 1.9 2.6 8.3

Operating result (EBIT) (2.5) 1.4 (2.3) 6.6

Normalised EBIT (0.5) 1.4 3.8 7.3

Operating cash flow 0.5 (2.8) 2.1 (0.6)

The HFS segment consists of two activities: branded and wholesale. In general, our branded activities are performing satisfactorily with brands such as Ekoland, De Rit, Bonneterre, Evernat, Allos and Tartex. The challenge is to further increase brand activation - requiring a higher level of in-store activation versus Grocery - and introduce meaningful innovations on an ongoing basis. At wholesale we continue to work hard at implementing multiple improvements, of which several have yet to translate into tangible results. Focus is amongst others on operational excellence, such as implementing and better employing ICT systems and improving service levels, and expanding the Dutch own format store footprint (GooodyFooods and Natuurwinkel). We divested both our lower added value UK wholesale activities (Tree of Life UK) and French distributor of pharmacies (Kalisterra). We aim to focus on higher added value wholesale activities such as Natudis in the Netherlands and Bonneterre in France. Revenue decreased to €54.7 million, of which the divestment of Tree of Life UK accounted for €8.3 million (12.2)%. Autonomous revenue growth amounted to (7.1)% with volumes down (8.0)% and the price/mix effect contributing 0.9%. Furthermore Kalisterra - which was divested as of 1 October - had a weak quarter, contributing over 2% to the organic decline in the quarter. Normalised EBIT decreased to €(0.5) million (Q2 2011: €1.4 million), mainly due to lower volumes in France and the Benelux. Operating result amounted to €(2.5) million, impacted by the recycling of an exchange loss deferred in equity of €(2.1) million following divestment of Tree of Life UK.

A new GooodyFooods opened in Zaandam early October. The Benelux market is growing whereas our sales are lower as a result of stores exiting the Natuurwinkel formula in previous quarters. At our existing own-format stores, we see revenue trending up. Our fresh supplier Kroon continues to grow, partly driven by new customer gains and benefiting from the cooperation with dedicated fresh distributor Vroegop-Windig.

Press release 27 October 2011

Page 8 of 15

The French market was down modestly. Kalisterra showed a weak performance, reducing total HFS revenue by over 2%-point. Bonneterre, our branded business, showed some growth while the wholesale activities declined in both dry groceries and fruits and vegetables. The German market showed sound growth with our German revenues trending in line with the overall organic market, driven by growth at the HFS stores (‘Naturkost’). Sales to the more specialised stores (‘Reformhauses’) were stable. Innovations included amongst others a new range of Allos cookies.

Frozen Foods In € million, unless stated otherwise Q3 2011 Q3 2010 % change 9m 2011 9m 2010 % change

Revenue 27.3 27.1 0.7% 84.0 86.5 (2.9)%

Autonomous revenue growth 0.8% (4.4)%

EBITDA 1.4 2.3 5.6 7.5

Operating result (EBIT) 0.2 1.1 2.1 3.9

Operating cash flow 1.5 1.7 5.0 5.1

Revenue increased 0.7% to €27.3 million. Autonomous revenue showed growth of 0.8% with price/mix effects contributing 3.8%, while volumes were 3.0% lower. Branded volumes increased as a result of higher sales in Belgian out-of-home and exports, despite somewhat lower volumes in Dutch retail and out-of-home markets. Private label sales were about stable. In general, competition in our markets remained fierce with customers continuing to focus on price. Our focus is on both sales growth and managing operating costs. We are tapping on improvement initiatives to grow the top and bottom line. EBIT decreased to €0.2 million mainly as a result of increased raw material prices. Marketing spending was in line with last year. Revitalising the Beckers brand and clearly distinguishing it from private label offerings remains key. In October, we introduced the Bicky Double Chicken in the Belgian out-of home channel, including a newly designed carton box. Initial response by the trade has been favourable. With this innovation we further extended our Bicky range as we did last year with the launch of the still very successful Bicky Royal. The introduction of the Bicky Double Chicken has been supported by TV commercials and an online campaign.

Press release 27 October 2011

Page 9 of 15

ABC in € million, unless stated otherwise Q3 2011 Q3 2010 % change 9m 2011 9m 2010 % change

Revenue 37.7 26.5 42.3% 94.6 76.9 23.0%

Autonomous revenue growth 53.5% 33.7%

EBITDA 6.2 0.6 13.6 7.7

Operating result (EBIT) 6.2 (0.7) 11.4 4.1

Normalised EBIT 5.2 (0.7) 10.4 4.2

Operating cash flow 10.4 4.6 12.9 2.8

in US$ million, unless stated otherwise Q3 2011 Q3 2010 % change 9m 2011 9m 2010 % change

Revenue 53.2 34.6 53.8% 134.0 100.8 32.9%

Operating result (EBIT) 8.7 (0.8) 16.1 5.4

Operating cash flow 14.8 6.1 18.3 3.7

ABC showed a very strong third quarter performance. Autonomous revenue was up 53.5% to US$53.2 million, based on 46.6% volume growth and price/mix effect contributing 6.9%. In euro terms, revenue was up 42.3% to €37.7 million. A weaker US dollar resulted in a negative currency effect of 10.8%.

The strong results are mostly attributable to Daily’s - ABC’s cocktail mixers brand - and in particular the ready-to-drink (RTD) pouches which are showing very strong growth. In addition, other Daily’s products such as the bag-in-a-box and premixes are also performing well. Drivers were the development of the right packaging concepts for all channels, a change in the distribution strategy to also serve grocery chains, consistent execution and its attractive price-value positioning. The expansion of distribution was achieved by adding numerous new customers for who RTD pouches and other Daily’s products were new to their assortment. The existing RTD capacity has been further expanded, while we also realised further production efficiencies.

Page 10 of 15

Little Hug - our juice drink brand - was stable during the quarter. On the one hand our sales were affected by continued competitive activity and the impact of active pruning and de-emphasising of lower margin products. On the other hand, our 20-count variety pack continued to perform well, benefiting from new packaging and some new distribution. The process of revitalising Little Hug continues with amongst others print advertising highlighting the new brand identity and the message ‘75% less sugar’ among other initiatives.

EBIT of US$8.7 million was clearly up versus a year ago (Q3 2010: $0.9 million loss) representing an operating margin of 16.4% (normalised margin of 13.8%). A favourable volume and product mix and higher absorption of direct production costs both contributed to this strong increase. For full year 2011, the operating result is expected to be in the range of US$17-19 million. Autonomous revenue is expected to show continued strong year on year growth, although the fourth quarter is traditionally its seasonally weakest. In 2012, we expect further revenue and earnings growth, based on the strong increase in demand this year, the increased distribution of Daily’s and ongoing expansion of our production capacity. In addition, we expect to conduct to start promotional activities to further support and activate Daily’s as a brand.

Non-allocated and eliminations (including corporate expenses)

In € million, unless stated otherwise Q3 2011 Q3 2010 9m 2011 9m 2010

Revenue (2.9) (3.1) (9.2) (9.3)

EBITDA (2.0) (2.0) (6.1) (7.2)

Operating result (EBIT) (2.5) (2.4) (7.5) (8.2)

Inter-segment revenue between Grocery and HFS amounted to €(2.9) million. Non-allocated expenses, reflecting corporate costs not charged to operating segments, were €(2.5) million which is in line with last year.

Press release 27 October 2011

Page 11 of 15

Important dates Thursday 23 February 2012 Q4 2011 results (7h15 CET) Friday 2 March 2012 Publication Annual Report 2011 (online) Tuesday 17 April 2012 Annual Meeting of Shareholders (Amsterdam (14h00 CET)) Friday 27 April 2012 Q1 2012 results (7h15 CET) Wednesday 25 July 2012 Q2 2012 results (7h15 CET) Thursday 25 October 2012 Q3 2012 results (7h15 CET)

Analyst & investor conference call An analyst, investor and media conference call will be hosted by Ronald Merckx (CFO) at 11h00 CET. The dial-in number is: +3120 794 8485. The call will be live audio webcasted via www.wessanen.com. The presentation and press release can be downloaded from our website.

Press, investor and analyst enquiries Carl Hoyer (VP Corporate Communications) Phone +31 20 3122 140 / +316 1235 5658 Twitter @RoyalWessanen

Company profile Royal Wessanen is a leading company in the European organic food market. In 2010, Wessanen generated revenue of €712 million with over 2,200 employees. Operating mainly in France, the Benelux, the UK, Germany and Italy, we manage and develop our brands and products in the grocery and health food channels. Our vision is to make our organic brands most desired in Europe. Our brands, such as Bjorg, Whole Earth, Zonnatura, Bonneterre, Ekoland, Allos and Tartex, are pioneering brands in the organic food markets. Next to our leading position in organic food businesses, we also produce and market branded (Beckers, Bicky) and private label frozen snack products in the Benelux (Frozen Foods) and fruit drinks (Little Hug) and cocktail mixers (Daily’s) in the US (ABC).

Note on forward-looking statements This press release includes forward looking statements. Other than reported financial results and historical information, all statements included in this press release, including, without limitation, those regarding our financial position, business strategy and plans and objectives of management for future operations, are forward-looking statements. These forward-looking statements are based on our current expectations and projections about future events and are subject to risks and uncertainties that could cause actual results to differ materially from those expressed in the forward-looking statements. Many of these risks and uncertainties relate to factors that are beyond Wessanen's ability to control or estimate precisely, such as future market conditions, the behaviour of other market participants and the actions of governmental regulators. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this press release and are subject to change without notice. Other than as required by applicable law or the applicable rules of any exchange on which our securities may be traded, we have no intention or obligation to update forward-looking statements.

Press release 27 October 2011

Page 12 of 15

Condensed consolidated income statement

Q3 2011 Q3 2010 In EUR millions, unless stated otherwise 9 months 2011 9 months 2010(unaudited) (unaudited) (unaudited) (unaudited)

Continuing operations174.3 173.4 Revenue 548.8 539.7

(110.0) (111.1) Raw materials and supplies (345.7) (340.6) (27.8) (28.3) Personnel expenses (85.2) (86.3) (2.4) (3.6) Depreciation, amortisation and impairments (12.7) (10.5)

(28.7) (28.8) Other operating expenses (84.3) (84.9) (168.9) (171.8) Operating expenses (527.9) (522.3)

5.4 1.6 Operating result 20.9 17.4

(1.1) (1.0) Net financing costs (2.6) (7.4) - - Share in results of associates - -

4.3 0.6 Profit/(loss) before income tax 18.3 10.0 3.8 0.3 Income tax expense (0.2) (2.0)

8.1 0.9 Profit/(loss) after income tax from continuing operations 18.1 8.0

Discontinued operations

- 0.3 Profit/(loss) from discontinued operations, net of income tax - (4.7)

8.1 1.2 Profit/(loss) for the period 18.1 3.3

Attributable to: 8.1 0.7 Total attributable from continuing operations 18.0 7.5

- 0.3 Total attributable from discontinued operations - (4.7)

8.1 1.0 Equity holders of Wessanen 18.0 2.8

- 0.2 Non-controlling interests 0.1 0.5

8.1 1.2 Profit/(loss) for the period 18.1 3.3

Earnings per share attributable to equity holders of Wessanen (in EUR)

0.11 0.01 Basic 0.24 0.04 0.11 0.01 Diluted 0.24 0.04

Earnings per share from continuing operations (in EUR)

0.11 0.01 Basic 0.24 0.10 0.11 0.01 Diluted 0.24 0.10

Average number of shares (in thousands)75,671 74,587 Basic 75,237 73,229

0.7096 0.7777 Average USD exchange rate (Euro per USD) 0.7062 0.7624 1.1420 1.2030 Average GBP exchange rate (Euro per GBP) 1.1415 1.1714

Press release 27 October 2011

Page 13 of 15

Condensed statement of comprehensive income Q3 2011 Q3 2010 In EUR millions 9 months 2011 9 months 2010

(unaudited) (unaudited) (unaudited) (unaudited)

8.1 1.2 Profit/(loss) for the period 18.1 3.3

Other comprehensive income

6.8 (8.7) Foreign currency translation differences, net of income tax 1.6 11.2

(0.3) 0.2 Effective portion of changes in fair value of cash flow hedges, net of income tax (0.1) 0.6

6.5 (8.5) 1.5 11.8

14.6 (7.3) Total comprehensive income for the period 19.6 15.1

Attributable to: 14.6 (7.5) Equity holders of Wessanen 19.5 14.6 - 0.2 Non-controlling interests 0.1 0.5

14.6 (7.3) Total comprehensive income for the period 19.6 15.1

Condensed consolidated statement of changes in equity

In EUR millions 30 September 2011

30 September 2010

(unaudited) (unaudited)

Balance at beginning of year 183.8 155.6

Profit/(loss) for the period 18.1 3.3

Other comprehensive income 1.6 11.2

(0.1) 0.6 Total other comprehensive income 1.5 11.8

Total comprehensive income for the period 19.6 15.1

Transactions with owners, recorded directly in equity

Contributions by and distributions to ownersDividends to shareholders (1.3) - Sale of own shares - 0.8 Share capital increase - 17.9 Share-based payment transactions 0.3 0.2 Change in non-controlling interests 0.1 - Total contributions by and distributions to owners (0.9) 18.9

Total transactions with owners (0.9) 18.9

Balance at end of period 202.5 189.6

Equity attributable to equity holders of Wessanen 195.6 183.4 Non-controlling interests 6.9 6.2 Total equity at the end of the period 202.5 189.6

Effective portion of changes in fair value of cash flow hedges, net of income tax

Foreign exchange translation differences, net of income tax

Press release 27 October 2011

Page 14 of 15

Consolidated statement of financial position

In EUR millions, unless stated otherwise30 September

201131 December

2010(unaudited) (audited)

AssetsProperty, plant and equipment 84.5 85.8 Intangible assets 126.1 126.1 Investments in associates and other investments 0.9 1.6 Deferred tax assets 7.9 3.7 Total non-current assets 219.4 217.2

Inventories 66.5 63.4 Income tax receivables 3.3 3.0 Trade receivables 83.6 66.4 Other receivables and prepayments 24.5 20.1 Cash and cash equivalents 12.5 8.7 Assets classified as held for sale - 13.5 Total current assets 190.4 175.1

Total assets 409.8 392.3

EquityShare capital 76.0 75.2 Share premium 102.9 105.0 Reserves and retained earnings 16.7 (3.2) Total equity attributable to equityholders of Wessanen 195.6 177.0 Non-controlling interests 6.9 6.8 Total equity 202.5 183.8

LiabilitiesInterest-bearing loans and borrowings 45.7 35.9 Employee benefits 23.5 22.7 Provisions 2.5 2.5 Deferred tax liabilities 1.3 1.3 Total non-current liabilities 73.0 62.4

Bank overdrafts 2.5 1.1 Interest-bearing loans and borrowings 0.2 0.6 Provisions 2.2 7.2 Income tax payables 1.5 2.3 Trade payables 70.6 74.6 Non-trade payables and accrued expenses 57.3 54.0 Liabilities classified as held for sale - 6.3 Total current liabilities 134.3 146.1

Total equity and liabilities 409.8 392.3

End of period USD exchange rate (Euro per USD) 0.7406 0.7493 End of period GBP exchange rate (Euro per GBP) 1.1539 1.1609

Press release 27 October 2011

Page 15 of 15

Consolidated statement of cash flows Q3 2011 Q3 2010 In EUR millions, unless stated otherwise 9 months 2011 9 months 2010

(unaudited) (unaudited) (unaudited) (unaudited)Cash flows from operating activities

5.4 1.6 Operating result 20.9 17.4

Adjustments for:2.5 3.6 Depreciation, amortisation and impairments 12.8 10.5 2.3 0.8 Other non-cash and non-operating items 2.3 3.0

10.2 6.0 Cash generated from operations before changes in working capital and provisions 36.0 30.9

(4.3) 5.6 Changes in working capital (23.5) (13.4) (0.3) (1.0) Payments from provisions and changes in employee benefits (4.9) (4.9)

5.6 10.6 Cash generated from operations 7.6 12.6

(0.6) (0.7) Interest received/(paid) (1.2) (3.6) (0.8) (0.7) Income tax received/(paid) (5.5) 3.9

4.2 9.2 Operating cash flow from continuing operations 0.9 12.9 - 0.3 Operating cash flow from discontinued operations - (21.9) 4.2 9.5 Net cash from operating activities 0.9 (9.0)

Cash flows from/(used in) investing activities(2.6) (2.5) Acquisition of property, plant and equipment (6.9) (9.1) - 0.2 Proceeds from sale of property, plant and equipment 0.1 0.4 0.1 0.5 Proceeds from sale of other investments 0.7 1.3 1.7 - Proceeds from sale of business 1.7 -

(0.7) (0.8) Acquisition of intangible assets, excluding goodwill (1.8) (1.8) - - Acquisition of subsidiaries - (2.8)

(1.5) (2.6) Investing cash flow from continuing operations (6.2) (12.0) - (1.6) Investing cash flow from discontinued operations - 125.4 (1.5) (4.2) Net cash from/(used in) investing activities (6.2) 113.4

2.7 5.3 Net cash flow before financing activities (5.3) 104.4

Cash flows from/(used in) financing activities(0.2) (1.5) Proceeds from/(repayments of) interest bearing loans and borrowings 9.6 (127.0) (0.1) (0.1) Net payments of finance lease liabilities (0.3) (0.3) 0.4 (0.3) Cash payments derivatives (0.3) (8.7) - - Share capital increase - 17.9 - 0.8 Sale of own shares - 0.8 - - Dividends paid (1.3) -

0.1 (1.1) Financing cash flow from continuing operations 7.7 (117.3) - - Financing cash flow from discontinued operations - - 0.1 (1.1) Net cash from/(used in) financing activities 7.7 (117.3)

2.8 4.2 Net cash flow 2.4 (12.9)

7.0 26.0 Cash and cash equivalents at beginning of period 7.7 41.7 2.8 4.2 Net cash from operating, investing and financing activities 2.4 (12.9) 0.2 (0.4) Effect of exchange rate differences on cash and cash equivalents (0.1) 0.9 - - Acquired cash 0.1

- (0.9) Cash and cash equivalents related to discontinued operations at end of period - (0.9)

10.0 28.9 Cash and cash equivalents of continuing operations at end of period 10.0 28.9