11 loan recovery policy kerala financial … recovery policy kerala financial corporation 2010 -11...

TRANSCRIPT

KE

RA

LA

FIN

AN

CIA

L C

OR

PO

RA

TIO

N

LOA

N R

EC

OV

ER

Y P

OLI

CY

20

10

- 1

1

KERALA FINANCIAL CORPORATION Vellayambalam, Thiruvananthapuram - 33

Loan Recovery Policy 2010 - 11

2 Kerala Financial Corporation

1. OBJECTIVE The basic objective of the Loan Recovery Policy (LRP) of the Corporation is to maximize recovery of dues under the credit portfolio and out of Non-Performing Assets (NPAs), by proper application of appropriate recovery tools. The other allied objectives are :

a. To initiate time-bound action for recovery.

b. To bring about uniformity in approach while dealing with defaulting borrowers.

c. To ensure that all the NPAs are duly attended to and an appropriate recovery tool is applied expeditiously.

2. GUIDING PRINCIPLES

a. The basic approach for recovery would be practical, non prejudiced and result oriented.

b. Coercive action would be resorted only as a last resort.

c. The focus would be on initiating quick action without losing time.

d. Identified Trigger Points, as given in Appendix I, would help the concerned officers to initiate time-bound action.

e. Selection of an appropriate recovery tool would depend on comparative analysis of all the

options available.

f. While specific recovery action in each case would depend upon the facts of the case and attendant circumstances, general consistency in approach would be maintained while dealing with the defaulting borrowers.

g. More considerate treatment would be given to such borrowers who continue to make

payments even after being classified as NPAs.

h. The cases of willful default/suspected fraud/malfeasance would generally be legally pursued to its logical end. Consideration of CSS offer in such cases would be only with the approval of EC/ Board.

Loan Recovery Policy 2010 - 11

3 Kerala Financial Corporation

3. ORIENTATION AND APPROACH

a. The LRP emphasizes that all the Branch Offices would have the recovery orientation right from the stage of sanction / disbursement of assistance.

b. Efforts should be made to ensure timely documentation and disbursements which would

help create a healthy relationship with the borrower.

c. It would be important to stipulate only practical and meaningful terms and conditions at the time of sanction of assistance so that timely compliance therewith can be made by the borrower unit / company.

d. Success of the borrower in implementing the assisted project / activity, without time and cost

overrun as far as possible, would be of paramount importance for hassle-free recovery in most of the cases. Verification of end-use of funds would indicate whether the project is being implemented in the right earnest. Besides, verification of documents and progress reports, site visits would also play a crucial role in ensuring close monitoring at the project implementation / completion phases.

e. Creation of primary security under the project would not have any meaning unless the

assets are created out of the Corporation’s assistance disbursed to the borrower. This would call for periodical site visits and verification of assets installed at the unit.

f. Proper and timely communication of dues payable by the borrower would also help in

ensuring a smooth recovery channel.

g. In case of continued default, the dues would get compounded quickly and after sometime, it would become difficult for the borrower to honour them. Remedial measures would, therefore, be initiated right from the first instance of delayed payments/ defaults.

h. The guidelines for KYC/AML would be strictly followed before considering any application

from the borrowers. 4. MONITORING OF NPAs The key objectives of monitoring include: � Monitoring of asset quality, application of recovery tools and progress thereunder, etc. � Continuous monitoring and intervention from HO/ZO/BO once asset comes under stress

category (arrears of principal and / or interest exceeds 30 days).

Loan Recovery Policy 2010 - 11

4 Kerala Financial Corporation

a. Multi-tier monitoring

While the primary responsibility to monitor the individual NPA accounts would continue to rest with BO concerned, for the overall monitoring purpose multi tier monitoring structure would be followed for collective review of all standard assets. For loans upto Rs.100 lakhs - BM/CM For loans between Rs.101 – Rs.300 lakhs - ZM For loans between Rs.301 lakhs – Rs. 500 lakhs - DGM For loans from Rs. 501 lakhs and above - GM

b. Failure Cause Analysis and Knowledge Sharing � As part of the Corporation’s policy regarding prevention of fresh slippages into NPAs, analysis of

failure of accounts would be carried out by the FO and reports submitted to BM/CM within a month of an account turning into a NPA, and the finding thereof would be used towards mitigating the risk of slippages of new accounts into NPAs.

� An indicative list of reasons which could cause failure of cases is given as Annexure to Appendix I.

c. Review of Legal/RR Cases BMs/ZMs shall review all Court/RR cases and wherever the balance outstanding is above Rs.100 lakhs they shall be reviewed by AGM(L)/DGM/GM. These reviews will be conducted once in a quarter. d. Review of wilful default / fraud cases RBI has recently in FY 09 redefined the term “willful default” in supersession of its earlier definition. The modified definition of the term “willful default” is furnished below: A willful default would be deemed to have occurred if any of the following events is noted:-

a. The unit has defaulted in meeting its payment/repayment obligations to the lender even when it has the capacity to honour the said obligations.

b. The unit has defaulted in meeting its payment/repayment obligations to the lender and has

not utilized the finance from the lender for the specific purposes for which finance was availed of but has diverted the funds for other purposes.

c. The unit has defaulted in meeting its payment/repayment obligations to the lender and has

siphoned of the funds so that the funds have not been utilized for the specific purpose for

Loan Recovery Policy 2010 - 11

5 Kerala Financial Corporation

which finance was availed of, nor are the funds available with the unit in the form of other assets.

d. The unit has defaulted in meeting its payment/repayment obligations to the lender and has

also disposed of or removed the movable fixed assets or immovable property given by him or it for the purpose of securing a term loan without the knowledge of the Corporation/lender.

Further, RBI has also reiterated that no additional facilities should be granted by any Corporation/FI to the listed willful defaulters. The objective of identification of willful defaulters is to:

a. alert banks and FIs and to put them on guard against borrowers who had willfully defaulted in their dues to lending institutions, and

b. to make public the names of the borrowers who had willfully defaulted.

As soon as an account is identified as a willful defaulter by the F.O. the BM/CM may after verification inform the matter to ZM, who in turn will put up the facts before DGM/GM for inclusion in the consolidated list to be maintained at HO and sent to Credit Information Bureau Limited (CIBIL) on quarterly basis. A review of wilful default/fraud cases shall be done periodically and the status submitted to the Board. As per RBI guidelines, a Grievance Redressal Committee (GRC) is being constituted to look into the representation received from the borrowers. Recovery related matters would also be examined from the staff accountability point of view. e. Review of Sn.29 cases CM/BM shall conduct monthly review. ZM shall conduct quarterly review of all cases under Section 29. DGM/GM shall review all such cases which are in the custody of the Corporation for more than an year. f. Review of RR cases CM/BM shall conduct monthly review. ZM shall conduct quarterly review of all RR cases. DGM/GM shall review all such cases which are not settled even after lapse of 1 year from the date of RRR. g. Restructuring of NPAs

i. The general framework of the restructuring policy of the Corporation would be aligned in line with the policy guidelines issued by RBI/SIDBI from time to time.

ii. From the point of view of portfolio retention and continuing to earn even from irregular

accounts, restructuring of impaired accounts would be pursued as one of the primary tools of NPA management. In order to have a focused attention on the restructuring of nascent NPAs, FOs should visit such units within a month of the account turning into NPA so as to initiate timely action.

Loan Recovery Policy 2010 - 11

6 Kerala Financial Corporation

iii. Having regard to the safety of collateral properties mortgaged, all immovable properties

mortgaged as collateral security should also be inspected by the FOs. iv. Further, repeat visits should invariably be made to those assets within one month of an

account becoming NPA. v. Notwithstanding the above, visits may also be carried out by the Officers preferably when an

account shows any signs of default or slips to the stressed asset category. vi. Restructuring would include one or more forms of relief/concessions such as

reschedulement of principal instalments, funding of interest, reduction in interest rate and granting need based additional finance would be targeted at the following segments:

� NPAs which are not classified as sick SSI units, where grant of relief/concessions may

help the units to tide over their temporary problems.

� Potentially viable sick SSI units, where grant of rehabilitation package may be helpful to turnaround such units.

vii. Coordination with other lenders to the borrower in finalizing a workable restructuring

package would be important so that the unit’s long term viability is assured and the projections are realistically drawn.

viii. Since timely restructuring would help in preventing further deterioration of the account, a

decision on the restructuring proposal would be taken within one month of receipt of such proposal along with complete information.

ix. Monitoring of restructuring package would be done on regular basis to check whether the

desired impact of restructuring is being achieved. If not, alternative course of action would be contemplated.

h. Rehabilitation In deserving cases rehabilitation of sick units can be done after conducting detailed inspection and study by teams consisting of Technical Officers. Based on the recommendation of the team suitable package of assistance can be extended to the units. Close follow-up and monitoring of these units to be carried out by F.Os. during their periodic visits. Separate Register is to be maintained. As per RBI guidelines an SSI unit should be considered 'Sick' if : any of the borrowal accounts of the unit remains substandard for more than six months.

or

Loan Recovery Policy 2010 - 11

7 Kerala Financial Corporation

there is erosion in the net worth due to accumulated cash losses to the extent of 50 per cent of its net worth during the previous accounting year;

and

the unit has been in commercial production for at least two years. i. Delegation All decisions on rehabilitation, revival, reschedulement/restructuring packages will be exercised by the next higher authority so as to form an unbiased opinion. In all BIFR cases and for loans above Rs.500 lakhs the sanctioning authority shall be the M.D. 5. VALUATION OF ASSETS

a. Valuation of assets (primary & collateral) charged to the Corporation would be carried out in all NPAs. Valuation of primary or collateral security should be carried out as prescribed in the Valuation Policy of the Corporation .

b. Valuation would be carried out for evaluation of CSS proposals, and would be preferably

dated within 6 months of the proposal of CSS but in any case not more than one year. 6. INSURANCE OF ASSETS

Insurance cover would continue to be obtained in all NPA cases, including recalled and suit filed cases as per the operational guidelines issued by the Corporation from time to time. These guidelines relate, inter alia, to the issues of insurance with regard to NPAs with nil assets value, taken over assets, closed units, units with multiple lenders, where CSS has been granted, non-creation of final security, uncooperative borrowers, etc. It will be the responsibility of the concerned Field Officers to ensure the renewal of insurance.

7. IDENTIFICATION OF NPAs

The primary guiding factor for recognising a non-performing asset will be the Asset classification norms prescribed by RBI/SIDBI. As per the norms, among other conditions, if interest and / or principal instalments remain unpaid in a loan account for a period of 90 days or more on the relevant date, the loan account concerned will be classified as NPA.

8. UPGRADATION OF NPAs a. Corporation would follow the guidelines on prudential norms and asset classification issued by

the RBI/SIDBI from time to time. Upgradation of NPAs would also be governed by the said guidelines in force. The major guidelines in this regard are given at Appendix-III.

Loan Recovery Policy 2010 - 11

8 Kerala Financial Corporation

b. NPAs not subjected to restructuring will be upgraded immediately on clearance of defaults, if

the account does not otherwise show any inherent deficiencies. c. The restructured NPA accounts would be upgraded after satisfactory debt servicing

performance for the specified period in terms of the extant RBI/SIDBI guidelines. Field Officers should take maximum efforts in reducing NPA level.

9. FRESH ASSISTANCE IN NPA CASES a. Sanction of fresh loans/limits would be considered in NPA cases, if it is found absolutely

desirable for better prospects of the borrower unit/company and in the process would also ensure clearance of the outstanding dues to the Corporation.

b. In case of restructured NPA accounts, if the post-restructuring performance is satisfactory,

as envisaged in the package, any request for fresh finance/limits could be considered on merits, even before upgradation of the asset to performing category.

c. Sanction of fresh assistance under (a) and (b) above shall be done only with the permission

of Managing Director. 10. TRIGGER POINTS A system of triggers would be adopted for post-NPA management with a view to

automatically triggering off the desired action. Trigger Points would be updated from time to time. A list of Trigger Points, along with desirable actions, which would constitute an indicative Trigger System is given at Appendix I.

11. COMPROMISE SETTLEMENT SCHEME

The Compromise Settlement application can be processed by BOs if it satisfies the norms / guidelines already approved by the Board. Any deviation can be considered only with the prior permission of Managing Director.

(a) Eligibility Where asset classification is Doubtful and loss assets as at the end of the immediately preceding FY (March 31st). (b) Conditions to be followed:

i. All Doubtful cases and loss asset cases as on beginning of the FY and continuing in the same category as on date of approaching for Compromise Settlement and all loss assets are eligible for Compromise Settlement.

Loan Recovery Policy 2010 - 11

9 Kerala Financial Corporation

ii. The default shall not be willful. iii. Borrowers who have involved in fraudulent practices will not be eligible for Compromise

Settlement. iv. Generally no other cases other than those mentioned above will be considered for CS.

However in case of any deviations such matters will be referred to Board with the prior approval of Managing Director.

(c) Compromise Settlement Formula:

It is observed that though major portion of advances are secured by collateral, past experience of the Corporation shows that recovery of dues through realisation of such collateral (mostly residential houses of low income group) is very low. Hence a liberal Compromise Settlement scheme as below is proposed.

i. D3 Loans upto Rs. 2 lakhs: D3 Loans upto Rs.2 lakhs (Rupees Two lakhs only)

disbursed can be settled for Principal outstanding plus other expenses irrespective of the Security position of the assets.

ii. D3 loans above Rs.2 lakhs but below Rs.10 lakhs: Loans where 1st disbursement has

taken place prior to 10 years from date of application for Compromise Settlement can be settled at Principal outstanding + O.E. subject to the following conditions:

(a) Coercive steps either under RR or Section 29 should have been initiated. (b) Wherever a higher offer than the Principal outstanding + other expenses have been made by the loanee in the past, the C.S. shall not be less than the earlier offer. (c) Wherever a sale offer has been received for an amount higher than the Principal outstanding + O.E. the C.S. amount shall not be less than the sale offer. (d) In the case of a borrower / unit having multiple accounts, If one account is less than 10 years then the unit will not be eligible under this scheme and can be considered under the normal scheme. (e) The total amount remitted in the loan account including CS amount should be atleast 1.5 times of the amount disbursed and there should not be any write off of principal and other expenses.

To arrive at the minimum amount of C.S., a system of calculation of Net Simple Rate (NSR) shall be adopted.

Loan Recovery Policy 2010 - 11

10 Kerala Financial Corporation

iii. Definitions for NSR Calculation: NSR = NSR is the amount to be realized towards interest from the date the account

turning into NPA till the first of the month of registration of CSS proposal. P = Principal outstanding on the date of Calculation of Compromise Settlement. OE(1) = Other expenses incurred upto NPA date, but still outstanding. OE(2) = Other expenses incurred between NPA date and Compromise Settlement date, but

outstanding on the date of calculation of Compromise Settlement. OE = OE (1) + OE (2) I = Interest accrued as on NPA date. NSR amount is arrived by calculating the Simple Interest on P+I+OE (1) from the date of the account becoming NPA and not from the date of first disbursement and till first of the month in which the proposal for Compromise Settlement is registered by the Corporation. The interest paid after becoming NPA should be deducted from NSR to arrive at Net NSR. However, if net NSR is negative it shall not be credited to the Principal. In such cases the settlement should be at Principal + other expenses outstanding. There shall be no Principal Write off. Detailed procedure for calculation of NSR and minimum eligible Compromise Settlement amount is given in Appendix- II.

iv. Doubtful loans upto Rs. 10 lakhs.

Table I

Sl. No.

Amount Disbursed

Value of primary + Collateral security as % of P + OE + NSR is One or more Promoters/ Guarantors/ Co-obligants to get relieved of liability

Upto 100% Above 100% P+OE 1 Upto

Rs.10/- lacs P+I+ OE(2)+20%

NSR P+I+OE(2)+50% NSR.

Loan Recovery Policy 2010 - 11

11 Kerala Financial Corporation

v. Doubtful loans above Rs. 10 lakhs:

Table II

Sl. No

Amounts Disbursed

Value of Primary and Collateral Security as percentage to the P+OE+NSR is

More than 150%

Between 125% - 150%

Between 100% - 125%

Between 75 – 100% and

Between 50-75% and

Less than 50% and

Repaying Capacity worth &

standing of Promoters & Guarantors is

Repaying Capacity worth & standing of Promoters & Guarantors is

Repaying Capacity worth & standing of

Promoters & Guarantors is

High Mod & Low

High Mod & Low

High Mod & Low

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10) (11)

1 Above Rs.10 lakhs

General Package

P+I+ OE(2)+ 103% NSR

P+I+ OE(2)+ 102% NSR

P+I= OE(2)+ NSR

P+I+ OE(2)+ 90% NSR

P+I+OE(2)+ 80% NSR

P+I+ OE(2)+ 75% NSR

P+I+ OE(2)+ 65% NSR

P+I+ OE(2)+ 60% NSR

P+I+ OE(2)+

50% NSR

Under item IV and V calculation under yield method, NPV and yield percentage on loan also to be made.

In case of loans where the value of Primary and Collateral security is less than the Amount as per norms it is mandatory that the CMs/ BMs shall make thorough enquiry about the properties/ assets held by the promoters/ co-obligants/guarantors. Procedure for ascertaining the repaying capacity is mentioned below: Branch Offices may report the following along with the Compromise Settlement proposals:

a) The Field Officer shall make a thorough enquiry about the properties held by the borrower/guarantors and give reports.

b) Field Officer shall physically verify and report whether the unit is existing and/or working. In

case the unit is closed, the date/month in which it was closed and brief highlights of working results/financials at the time of closure shall be included in the report. Wherever the units are functioning, a brief working result of the unit shall be included in the report.

c) F.O. to report if RR proceedings against the unit/promoters/guarantors has been initiated by

any other authorities by verifying with the village/Taluks authorities.

d) Where borrowers have filed cases in Courts/ DRT, if Court cases can be withdrawn, then out of Court settlement can be preferred by Compromise Settlement.

Loan Recovery Policy 2010 - 11

12 Kerala Financial Corporation

vi. Loss Assets/No asset cases Compromise Settlement of D3 & no asset case: As on 01.10.2010 there are about 2754 D3 accounts with Rs.171.83 crores principal outstanding. Of this 849 units with principal outstanding of Rs. 50.20 crores are without any assets. To settle these accounts under Compromise Settlement Scheme a liberalized policy is required. Definition of Loss Assets/No asset cases – No asset cases are those where all the mortgaged assets were already sold by the Corporation under recovery action and credited the proceeds in the loan account. In such cases no mortgaged assets are available to be proceeded against for realizing the dues. Cases where the mortgaged properties were alienated or sold by the party or outside court/RR attachment made on the mortgaged property, do not fall under this category and are not eligible for consideration under this category. Under this category the minimum amount to be collected towards Compromise Settlement shall be normally P+OE. However, wherever the branch offices feel that it is difficult to collect the total P+OE outstanding, they can forward such proposals even for lesser amounts, taking into account the value of solvency, worth, social status, living conditions and repaying capacity of the promoters / co-obligants etc. The Field Officer of the Corporation and Dy.T (RR) shall make thorough enquiries about the properties held by the promoters, co-obligants and their parents, spouses, sons and unmarried daughters before forwarding such proposals. A. This policy is applicable to all those cases which satisfy the following eligibility criteria.

a) The cases should be 10 years or more old D3 cases/loss assets. b) All its mortgaged assets are already sold under any of our recovery action. c) RR proceedings are already initiated against its promoters and co-obligants. d) Absence of any personal assets in the name of promoters/co-obligants. e) Even if there is some personal assets there is no possibility of selling it and

realising the loan arrears due to legal or other problems. B. Compliance of the last two conditions above i.e., A(d) and A(e) are to be done in the following manner:

1) Letters to be sent to the Village Officers concerned (Village where the promoters/co-obligants resided, the Village where they are residing now and the Village where the

Loan Recovery Policy 2010 - 11

13 Kerala Financial Corporation

mortgaged assets / units located) for getting information about any properties in the name of the parties to our loans. 2) Field Officer along with Dy.Tahsildar may also contact the Village Officers concerned to expedite reply to our enquiry. Help of the loanee / co-obligant may also be sought to get the above information. 3) Loanee / Co-obligants are to be contacted by FO and persuade them for a Compromise Settlement. 4) Simultaneously Dy.T (RR) may be addressed to get a report on the availability of personal assets, if any, actions taken under RR and present stage of RR action. 5) Field Officer shall make thorough enquiry about the net-worth, living conditions and repaying capacity of the promoters/co-obligants and give a detailed report. 6) A notarized affidavit from the promoters / co-obligants shall also be obtained at the time of submitting the OTS proposal declaring nil property or the properties, if any, owned by them. 7) Field Officer to report if RR proceedings have been taken against the unit / promoters / co-obligants by any other authorities by verifying with the village/Taluk authorities. 8) To verify whether any case is pending in courts / DRT etc.

For settling hard core NPA cases below norms and without assets Board has constituted a

Task Force. Hence BMs/CMs/ZMs may identify suitable cases for placing before the Task Force. It may be ensured that maximum possible amount is collected in all the above cases and the proposals are to be submitted through BLSC and ZLSC.

vii) Policy for the write off of very old No Asset, D3 cases

There are a large number of very old D3 no asset cases in our loan portfolio. Some of them

can be settled as above. In the remaining no asset D3 cases, where there is no chance at all to realize any amount and the only solution possible is to write off the balance outstanding, such deserving cases can be separately identified by the branch office and can be forwarded to the Managing Director for a reference to the EC for write-off. Guidelines to be followed for write off D3 no asset cases It is not proper to write off any account simply due to the fact that there is no asset to be proceeded against. We have to enquire and ascertain about the availability of any asset in their name. It is not possible to conduct enquiries in all the Villages in the District or State. Hence we may restrict our enquiries to the Villages where the promoters/ co-obligants now residing or once resided and village where the security properties including the unit located.

Loan Recovery Policy 2010 - 11

14 Kerala Financial Corporation

This being the last resort to close the loan account, due seriousness should be given in recommending such cases. Hence the following guidelines are stipulated for the write off of D3 No asset cases which satisfy the following eligibility criteria.

a) Cases should be 20 years or more old D3 cases/Loss assets. b) All its mortgaged assets are already sold under any of our recovery action. c) RR proceedings are already initiated against its promoters and co-obligants and RRC

returned by the concerned District Collector. d) Absence of any personal assets in the name of promoters / co-obligants. e) Even if there is some personal assets there is no possibility of selling it and realising

the loan arrears due to legal or other problems. f) Thus there is no chance for realising any amount from the promoters / co-obligants /

legal heirs.

Method of compliance of above said Eligibility Criteria is already detailed under (vi -B) above.

(d) Mode of Payment:

Application for Compromise Settlement need be registered by B.O. only if Compromise Settlement advance computed at 10% of balance outstanding or 25% of principal outstanding (whichever is less) is remitted. The amount has to be kept in Compromise Settlement appropriation account. Generally no application should be processed without Compromise Settlement advance as above. However in deserving cases M.D. can give permission to process C.S. application without advance.

For No assets cases, Compromise Settlement advance can be waived, if required, by the

CM/BM. Normally 3 months time from the date of sanction by appropriate authority will be given for remittance. No interest will be charged during this period. In the event of rejection of CS proposal by the Corporation or failure of the applicant to remit the sanctioned CS amount within the stipulated period, the amount received as advance should be kept in CS appropriation account till it is settled and should not be adjusted towards normal dues. However, earnest efforts should be made by the Field Officer/Branch Office to settle the account at the earliest.

Loan Recovery Policy 2010 - 11

15 Kerala Financial Corporation

(e) Date of Compromise Settlement Calculation

The balance outstanding as on 1st of the month in which Compromise Settlement proposal is registered is taken for the purpose of calculating the sacrifice. NSR calculation will be upto the same date. Rate of interest to be charged for NSR calculation will be PLR of the Corporation as on date of registration of the CS proposal. 12. DELEGATION OF POWERS (a) Compromise Settlement

The revised delegation will be as follows: (i) ZLSC : Sacrifice upto Rs. 10 lakhs a per norms without principal

write off.

(ii) MD on recommendation : of HPC

Sacrifice above Rs.10 lakhs and upto Rs. 25 lakhs without principal write off.

(iii) E.C. : Sacrifice and principal write off of any amount. All such settlements will be regularly reported to the Board for information. (b) Waiver of Penal Interest

Occasions may arise when an account can be regularised or brought to standard assets with waiver of penal interest. There can also be genuine reasons like remittances made by borrower could not be accounted in time due to intervening holidays or fault in the computer system or any other unforeseen circumstances beyond the control of borrowers, such as accidents, calamities, etc. which, may result in delay in payment of dues to the Corporation by the borrowers. In such eventualities, waiver of penal interest can be considered for all loans in standard & NPA category as per the following limits.

Upto Rs.25,000 - Branch Level Settlement Committee Above Rs.25,000 to Rs.50,000 - Zonal Level Settlement Committee Above Rs.50,000 up to 10,00,000 - MD on recommendation of High Power Committee Above Rs.10,00,000/- - EC/Board (c) Belated Interest

Normally Compromise Settlement is allowed for 3 months only. Coercive action has to be initiated / continued in case the remittance is not made within 3 months. Some times the loanees are not able to pay the Compromise Settlement amount due to various constraints like selling of property which takes time, and mobilization of resources from friends and relatives, raising funds

Loan Recovery Policy 2010 - 11

16 Kerala Financial Corporation

from other institutions, etc. In such genuine cases the time for payment of Compromise Settlement amount can be extended by a period of 9 months by CM/BM/ZM. For extension of period above one year for payment of C.S. amount approval from M.D. should be obtained. No interest will be charged if Compromise Settlement amount is remitted within 3 months from the date of sanction of Compromise Settlement. Interest at 12% will be charged on the balance amount to be remitted out of the Compromise Settlement amount for the period exceeding three months and upto 12 months. Interest on delayed belated interest amounts pending will also attract 12% simple interest till date of settlement. (d) Waiver of belated interest on Compromise Settlement amount 1) Waiver of belated interest upto

Rs.50,000/-

: Branch Level Settlement Committee

2) Waiver of belated interest above Rs.50,000/- up to Rs. 1 lakh

: Zonal Level Settlement Committee

3) Waiver of belated interest above Rs. 1 lakh up to Rs.10.00 lakhs.

: MD on recommendation of HPC

4) Waiver of belated interest above Rs. 10 lakhs

: EC

5) For recommendation of waiver of belated interest of already sanctioned Compromise Settlement

cases, any one of the conditions (i to vii) may be satisfied. i. Borrower/ co-obligants are financially poor (to be specifically commented by Branch Level

Committee). ii. Borrower/ co-obligants have no other property other than residential property. iii. Borrower/ co-obligants are critically sick and being treated for terminal diseases. iv. Borrower/ co-obligants have absconded/ abandoned the assets. v. Borrower/ co-obligants are dead and legal heirs are coming to settle the debts. vi. Where primary or collateral assets have been seized and sold by the Corporation/ Revenue

Authorities before sanction of Compromise Settlement. vii. If the Branch Level Committee is of the opinion that the promoter has suffered heavy losses by

venturing into the project.

Loan Recovery Policy 2010 - 11

17 Kerala Financial Corporation

13. GENERAL GUIDELINES

The Branch Level and Zonal level officers will strive hard to settle the cases under Compromise Settlement as per the policy approved. If any of the proposals for Compromise Settlement cannot be settled as per general rules of the policy but the Branch Level Committee is of the opinion that settlement of the account is in the best interest of the Corporation it may be placed before the HPC for consideration.

1) Time frame for Processing Compromise Settlement of Applications:- B.O. - 15 days Z.O. - 10 days HPC - 10 days

2) Time frame for informing the Client for Compromise Settlement sanction. Within two days of receipt of orders/minutes of the appropriate authority. 3) The RR Commission if charged by the RR authorities has to be additionally paid by the

loanee. This should be communicated to the loanee. 4) In cases where CS applications are rejected, the promoters can apply afresh. 5) Under no circumstances shall Compromise Settlement result in refund of

remittances already received by the Corporation. 6) Principal Write Off shall be allowed only in exceptional cases with approval of the

EC/Board. 7) If for any reason it is felt that the interests of the Corporation will be best served by

settling the account under Compromise Settlement by allowing relaxation in norms, such cases have to be compulsorily referred to the Board/EC. The minutes of the Branch/Zonal/High Power Committees recommending such cases should clearly spell out the deviation from norms and justification/reasons for recommending Compromise Settlement despite the deviations and attached as Annexure to the CS note.

8) Any proposal for modification to the policy shall be placed before the Board and if

approved shall be circulated as substitution of/addition to the existing chapter/paragraph. 9) Compromise Settlement cases already sanctioned will not normally be re-opened.

However cases that may require special consideration on account of issues beyond the control of borrower can be reopened with the approval of MD.

10) Compromise Settlement be allowed for NEF loans as per guidelines prescribed by

SIDBI. 11) The Loan Recovery Policy will come into force with immediate effect and shall be

valid till a subsequent review of the same is carried out and advised.

Loan Recovery Policy 2010 - 11

18 Kerala Financial Corporation

12) If a CS proposal submitted is rejected by the next higher authority the CS amount as per

norms has to be reworked by the Branch Office if the period exceeds one month on re-submission.

13) Time limit for cancellation of Compromise Settlement: Compromise Settlement approved shall be normally cancelled if the default exceeds

90 days from the approved schedule at any stage. 14) a) BIFR/ AAIFR Cases: In respect of BIFR/ AAIFR cases the Compromise

Settlement packages shall be awarded in the light of decisions taken in the consortium meetings subject to final approval of the Board of Directors.

b) Consortium: In respect of Consortium cases the Compromise Settlement

packages shall be awarded in the light of decision taken in joint meetings with other lenders and after the approval of the Board of Directors.

15) Compromise Settlement amount prescribed are minimum. It is reiterated that

amount prescribed for settlement as above are only the minimum amount. All concerned shall negotiate for higher amounts depending on the value of available securities, solvency and repaying capacity of the borrower / guarantors / co-obligants / legal heirs.

16) Withdrawal of earlier Office Orders & Circulars on Compromise Settlement Scheme: The revised Compromise Settlement Guideline above supersedes all earlier

guidelines on Compromise Settlement issued earlier. 17) Clarifications and Interpretations: Clarifications if any, on the LRP shall be referred

to Managing Director for interpretation and approval. 18) Further loans for Promoters involved in Compromise Settlement cases: Any one who has obtained Compromise Settlement shall not be normally eligible for

future loans from the Corporation. However, where the promoters have settled their loan accounts under Compromise Settlement due to failure of units for reasons beyond their control application for further loans can be accepted only after obtaining approval from M.D.

19) Compromise Settlement proposals with CS amount as per norms of Rs. 25 lakhs or more

shall be pre-audited by the Internal Audit Section. Such proposals recommended by BLC should be forwarded to the Internal Audit representative in the zone by the concerned CM/BM under intimation to AGM (IA&IW). The Internal Audit Wing should visit the site and assess whether the asset value given is realistic. They should also verify whether the justification for Compromise Settlement given is as per norms. The Internal Audit Wing will finalise the report and submit the same to CM/BMs who will then forward it to HPC through ZLC. Pre-audit of CSS proposals have to be completed within seven day's time.

…....................

Loan Recovery Policy 2010 - 11

19 Kerala Financial Corporation

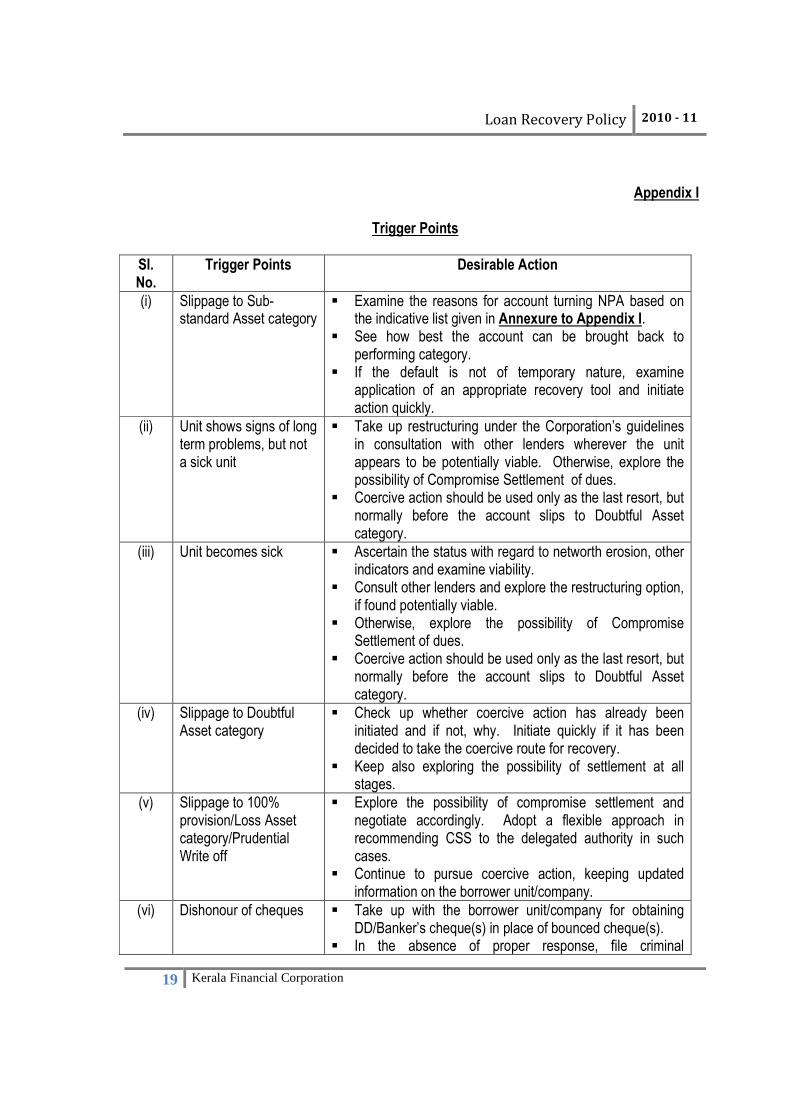

Appendix I

Trigger Points

Sl. No.

Trigger Points Desirable Action

(i) Slippage to Sub-standard Asset category

� Examine the reasons for account turning NPA based on the indicative list given in Annexure to Appendix I.

� See how best the account can be brought back to performing category.

� If the default is not of temporary nature, examine application of an appropriate recovery tool and initiate action quickly.

(ii) Unit shows signs of long term problems, but not a sick unit

� Take up restructuring under the Corporation’s guidelines in consultation with other lenders wherever the unit appears to be potentially viable. Otherwise, explore the possibility of Compromise Settlement of dues.

� Coercive action should be used only as the last resort, but normally before the account slips to Doubtful Asset category.

(iii) Unit becomes sick � Ascertain the status with regard to networth erosion, other indicators and examine viability.

� Consult other lenders and explore the restructuring option, if found potentially viable.

� Otherwise, explore the possibility of Compromise Settlement of dues.

� Coercive action should be used only as the last resort, but normally before the account slips to Doubtful Asset category.

(iv) Slippage to Doubtful Asset category

� Check up whether coercive action has already been initiated and if not, why. Initiate quickly if it has been decided to take the coercive route for recovery.

� Keep also exploring the possibility of settlement at all stages.

(v) Slippage to 100% provision/Loss Asset category/Prudential Write off

� Explore the possibility of compromise settlement and negotiate accordingly. Adopt a flexible approach in recommending CSS to the delegated authority in such cases.

� Continue to pursue coercive action, keeping updated information on the borrower unit/company.

(vi) Dishonour of cheques � Take up with the borrower unit/company for obtaining DD/Banker’s cheque(s) in place of bounced cheque(s).

� In the absence of proper response, file criminal

Loan Recovery Policy 2010 - 11

20 Kerala Financial Corporation

complaint(s) under Section 138 of the Negotiable Instruments Act against the Company/Directors.

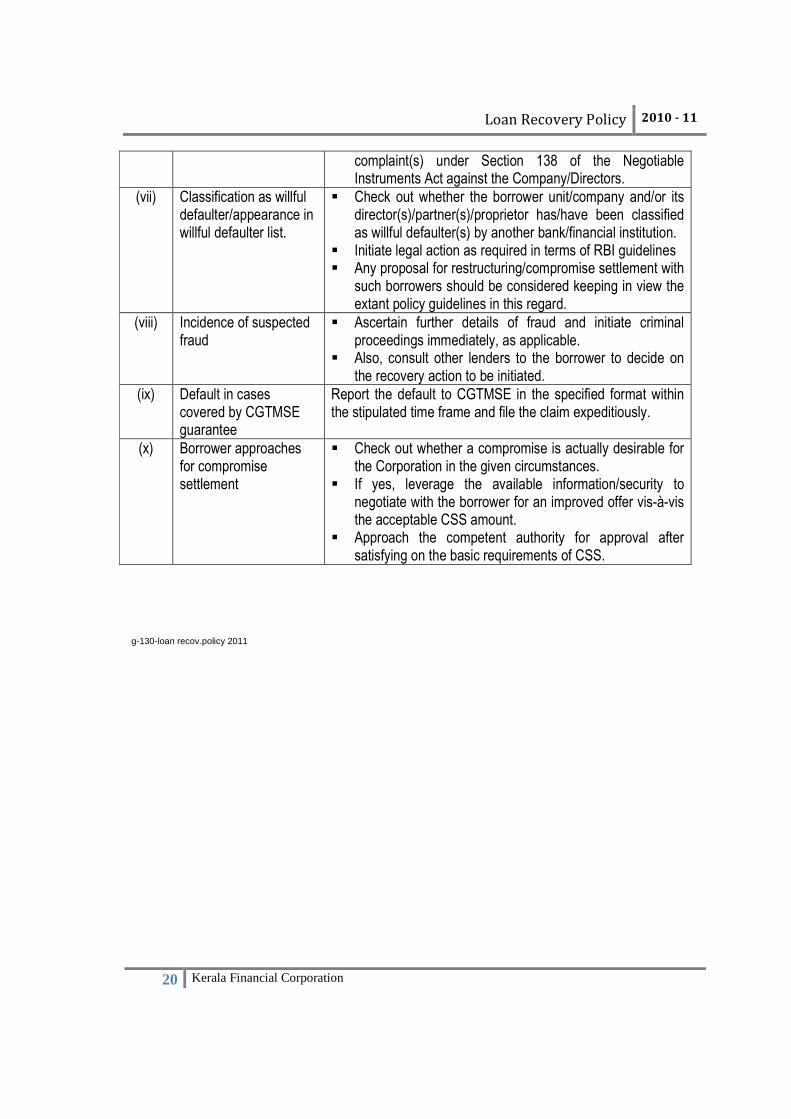

(vii) Classification as willful defaulter/appearance in willful defaulter list.

� Check out whether the borrower unit/company and/or its director(s)/partner(s)/proprietor has/have been classified as willful defaulter(s) by another bank/financial institution.

� Initiate legal action as required in terms of RBI guidelines � Any proposal for restructuring/compromise settlement with

such borrowers should be considered keeping in view the extant policy guidelines in this regard.

(viii) Incidence of suspected fraud

� Ascertain further details of fraud and initiate criminal proceedings immediately, as applicable.

� Also, consult other lenders to the borrower to decide on the recovery action to be initiated.

(ix) Default in cases covered by CGTMSE guarantee

Report the default to CGTMSE in the specified format within the stipulated time frame and file the claim expeditiously.

(x) Borrower approaches for compromise settlement

� Check out whether a compromise is actually desirable for the Corporation in the given circumstances.

� If yes, leverage the available information/security to negotiate with the borrower for an improved offer vis-à-vis the acceptable CSS amount.

� Approach the competent authority for approval after satisfying on the basic requirements of CSS.

g-130-loan recov.policy 2011

Loan Recovery Policy 2010 - 11

21 Kerala Financial Corporation

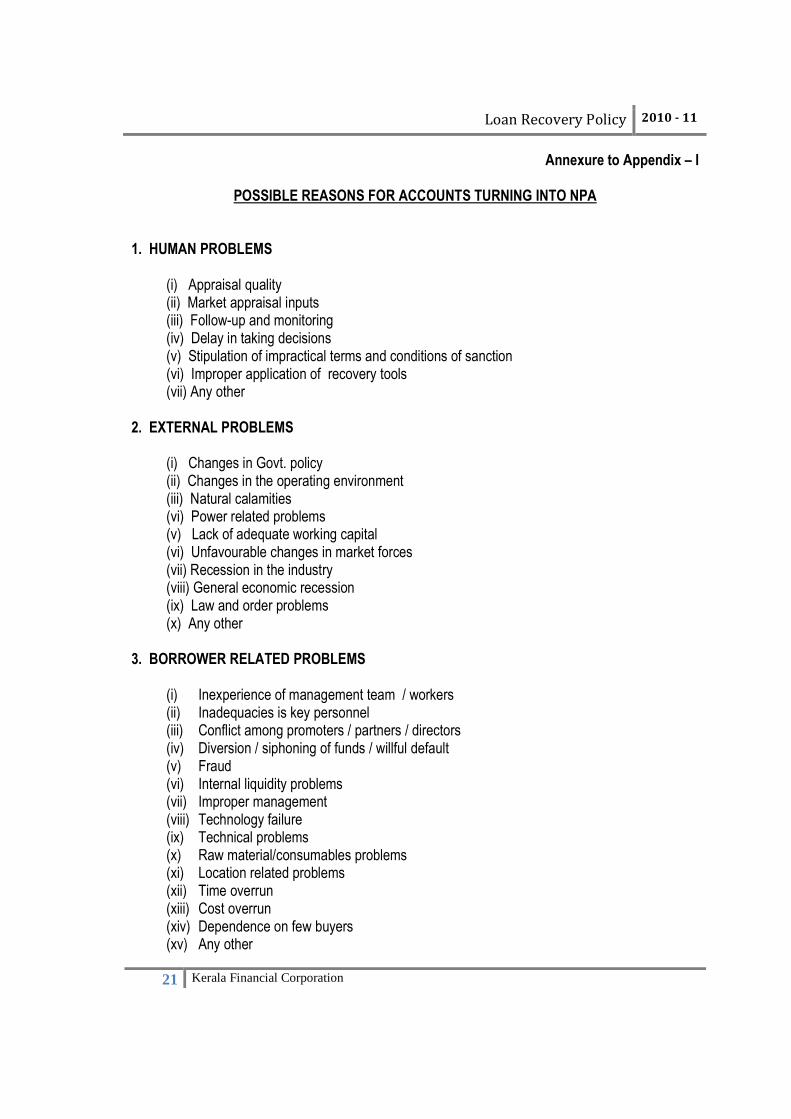

Annexure to Appendix – I

POSSIBLE REASONS FOR ACCOUNTS TURNING INTO NPA

1. HUMAN PROBLEMS

(i) Appraisal quality (ii) Market appraisal inputs (iii) Follow-up and monitoring (iv) Delay in taking decisions (v) Stipulation of impractical terms and conditions of sanction (vi) Improper application of recovery tools (vii) Any other

2. EXTERNAL PROBLEMS

(i) Changes in Govt. policy (ii) Changes in the operating environment (iii) Natural calamities (vi) Power related problems (v) Lack of adequate working capital (vi) Unfavourable changes in market forces (vii) Recession in the industry (viii) General economic recession (ix) Law and order problems (x) Any other

3. BORROWER RELATED PROBLEMS

(i) Inexperience of management team / workers (ii) Inadequacies is key personnel (iii) Conflict among promoters / partners / directors (iv) Diversion / siphoning of funds / willful default (v) Fraud (vi) Internal liquidity problems (vii) Improper management (viii) Technology failure (ix) Technical problems (x) Raw material/consumables problems (xi) Location related problems (xii) Time overrun (xiii) Cost overrun (xiv) Dependence on few buyers (xv) Any other

Loan Recovery Policy 2010 - 11

22 Kerala Financial Corporation

4. PROCEDURAL PROBLEMS

(i) Improper compliance of terms of sanction (ii) Inadequacies in examining proper end use of disbursed funds. (iii) Inadequacies in assessing need for funds (iv) Inadequate/Non-examination of No Lien accounts/stock statements, etc. (v) Pre-disbursement site visits not carried out. (vi) Inadequacies in periodical follow-up visits. (vii) Non-adherence to other procedural requirements. (viii) Any other.

5. LACK OF EXPERIENCE/TRAINING (OF THE OFFICERS OF THE CORPORATION)

(i) Project / Technical / Management appraisal. (ii) Analysis of financial statements. (iii) Follow up and monitoring. (iv) Coordination with working capital bankers/other lenders. (v) Market information (vi) Borrower related intelligence mechanism (vii) Any other.

g-130-loan recov.policy 2011

Loan Recovery Policy 2010 - 11

23 Kerala Financial Corporation

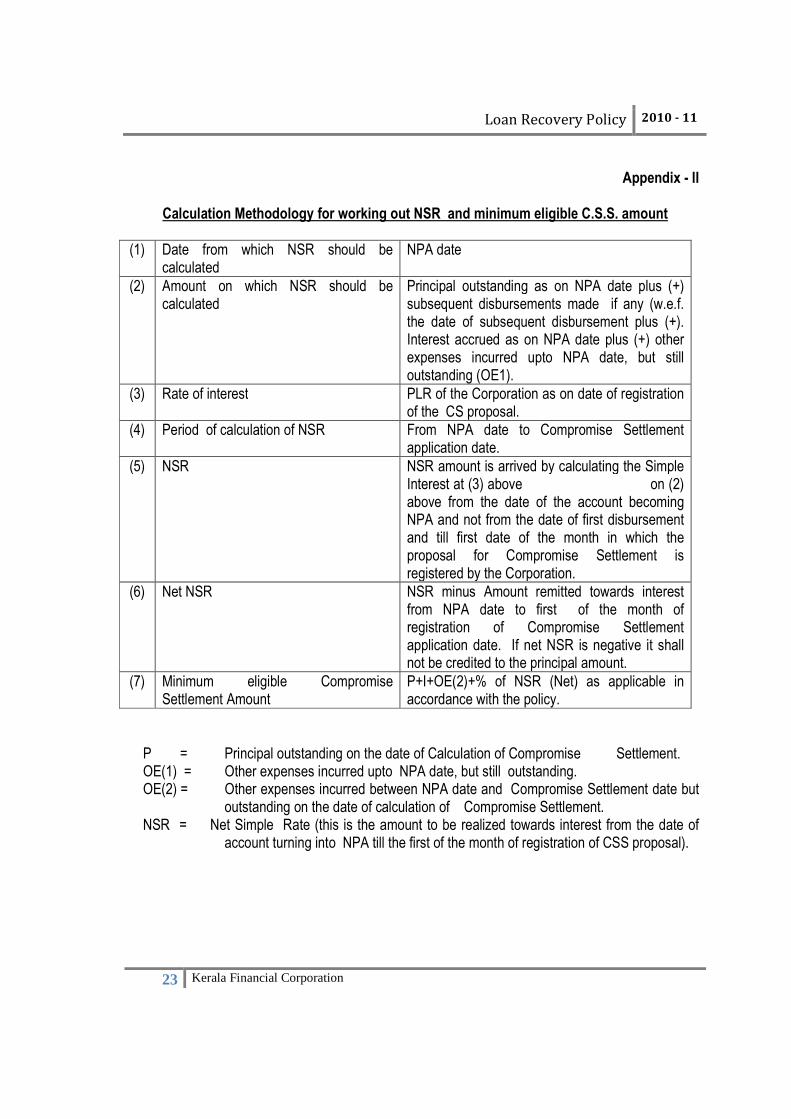

Appendix - II

Calculation Methodology for working out NSR and minimum eligible C.S.S. amount

(1) Date from which NSR should be calculated

NPA date

(2) Amount on which NSR should be calculated

Principal outstanding as on NPA date plus (+) subsequent disbursements made if any (w.e.f. the date of subsequent disbursement plus (+). Interest accrued as on NPA date plus (+) other expenses incurred upto NPA date, but still outstanding (OE1).

(3) Rate of interest PLR of the Corporation as on date of registration of the CS proposal.

(4) Period of calculation of NSR From NPA date to Compromise Settlement application date.

(5) NSR NSR amount is arrived by calculating the Simple Interest at (3) above on (2) above from the date of the account becoming NPA and not from the date of first disbursement and till first date of the month in which the proposal for Compromise Settlement is registered by the Corporation.

(6) Net NSR NSR minus Amount remitted towards interest from NPA date to first of the month of registration of Compromise Settlement application date. If net NSR is negative it shall not be credited to the principal amount.

(7) Minimum eligible Compromise Settlement Amount

P+I+OE(2)+% of NSR (Net) as applicable in accordance with the policy.

P = Principal outstanding on the date of Calculation of Compromise Settlement. OE(1) = Other expenses incurred upto NPA date, but still outstanding. OE(2) = Other expenses incurred between NPA date and Compromise Settlement date but

outstanding on the date of calculation of Compromise Settlement. NSR = Net Simple Rate (this is the amount to be realized towards interest from the date of

account turning into NPA till the first of the month of registration of CSS proposal).

Loan Recovery Policy 2010 - 11

24 Kerala Financial Corporation

Appendix III

Asset Classification and Income Recognition Norms

a) For classification of assets, Corporation would continue to follow the guidelines issued by RBI/SIDBI from time to time in this regard. In terms of the same, a Non-performing Asset (NPA) is a loan or an advance where

i. Interest and/or instalment of principal remain overdue for a period of more than 90 days in respect of a Term Loan; ii. The account remains 'out of order' for a period of more than 90 days, in respect of an Overdraft/Cash Credit (OD/CC); iii. The bill remains overdue for a period of more than 90 days in the case of bills purchased/discounted; iv. Any amount to be received remains overdue for a period of more than 90 days in respect of other accounts. • Non-performing assets would be further classified into the following three categories

based on the period for which the asset has remained non-performing and the realisability of the dues:

1. Sub-standard Assets 2. Doubtful Assets 3. Loss Assets

a. Sub-standard Assets A sub-standard asset would be one, which has remained NPA for a period less than or equal to 12 months. In such cases, the current net worth of the borrower/guarantor or the current market value of the security charged is not enough to ensure recovery of the dues to the Corporation in full. In other words, such an asset will have well defined credit weaknesses that jeopardise the liquidation of the debt and are characterised by the distinct possibility that the Corporation will sustain some loss, if deficiencies are not corrected. b. Doubtful Assets An asset would be classified as doubtful if it has remained in the substandard category for a period exceeding 12 months. A loan classified as doubtful has all the weaknesses inherent in assets that were classified as sub-standard, with the added characteristic that the weaknesses make collection or liquidation in full, on the basis of currently known facts, conditions and values – highly questionable and improbable. c. Loss Assets A loss asset is one where loss has been identified by the Corporation or internal or external auditors or the RBI/SIDBI/AG inspection team but the amount has not been written off wholly. In other words, such an asset is considered uncollectible and of such little value that its continuance as a bankable asset is not warranted although there may be some salvage or recovery value.

Loan Recovery Policy 2010 - 11

25 Kerala Financial Corporation

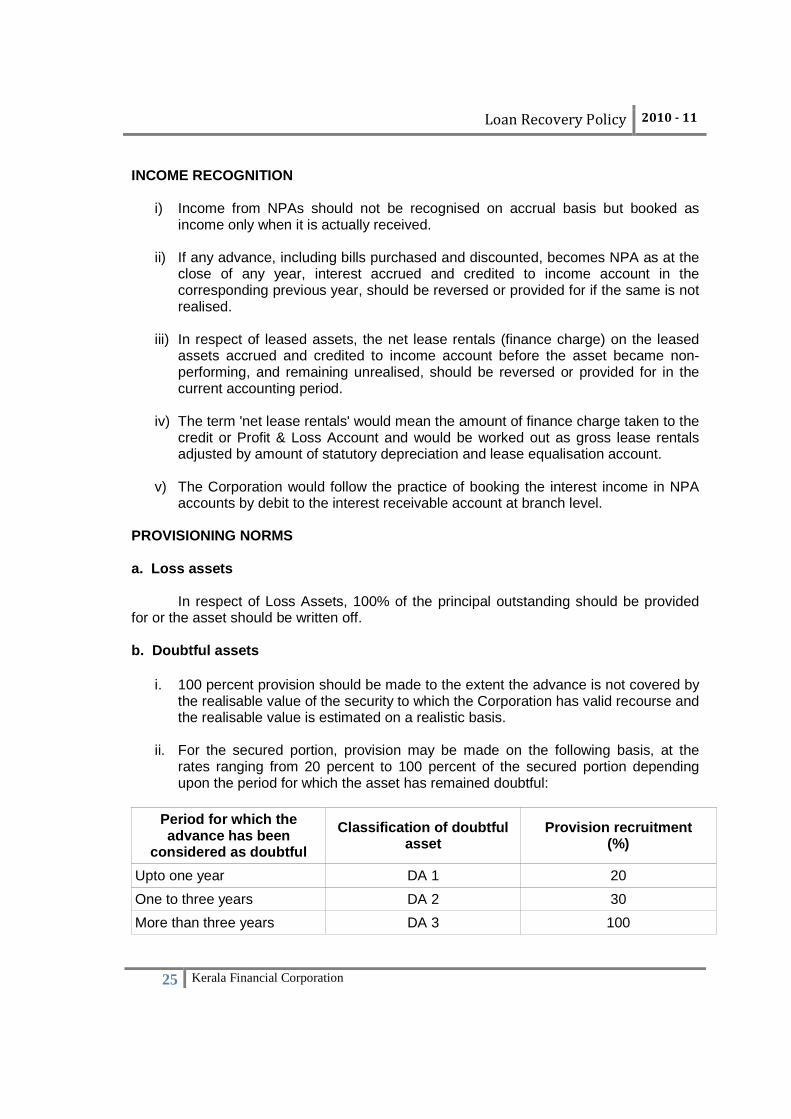

INCOME RECOGNITION

i) Income from NPAs should not be recognised on accrual basis but booked as income only when it is actually received.

ii) If any advance, including bills purchased and discounted, becomes NPA as at the

close of any year, interest accrued and credited to income account in the corresponding previous year, should be reversed or provided for if the same is not realised.

iii) In respect of leased assets, the net lease rentals (finance charge) on the leased

assets accrued and credited to income account before the asset became non-performing, and remaining unrealised, should be reversed or provided for in the current accounting period.

iv) The term 'net lease rentals' would mean the amount of finance charge taken to the

credit or Profit & Loss Account and would be worked out as gross lease rentals adjusted by amount of statutory depreciation and lease equalisation account.

v) The Corporation would follow the practice of booking the interest income in NPA

accounts by debit to the interest receivable account at branch level. PROVISIONING NORMS a. Loss assets In respect of Loss Assets, 100% of the principal outstanding should be provided for or the asset should be written off. b. Doubtful assets

i. 100 percent provision should be made to the extent the advance is not covered by the realisable value of the security to which the Corporation has valid recourse and the realisable value is estimated on a realistic basis.

ii. For the secured portion, provision may be made on the following basis, at the

rates ranging from 20 percent to 100 percent of the secured portion depending upon the period for which the asset has remained doubtful:

Period for which the advance has been

considered as doubtful

Classification of doubtful asset

Provision recruitment (%)

Upto one year DA 1 20

One to three years DA 2 30

More than three years DA 3 100

Loan Recovery Policy 2010 - 11

26 Kerala Financial Corporation

iii. The unsecured portion should be fully provided for. c. Sub-standard assets A general provision of 10 percent on total outstanding should be made without making any allowance for DICGC/ECGC/CGTMSE guarantee cover and securities available. d. Standard assets

i. Corporation would continue to follow the guidelines issued by RBI/SIDBI in this regard from time to time. Corporation is required to make a general provision for standard assets at the following rates for the funded outstanding on global loan portfolio basis:

(a) direct advance to agricultural and SME sectors at 0.25 per cent; (b) advances to Commercial Real Estate (CRE) Sector at 1.00 per cent; (c) all other loans and advances not included in (a) and (b) above at 0.40 per cent. ii. The provisions on standard assets should not be reckoned for arriving at net NPAs. iii. The provisions towards Standard Assets need not be netted from gross advances but shown separately as 'Contingent Provisions against Standard Assets' under 'Other Liabilities and Provisions – Others' in Schedule 5 of the balance sheet. UPGRADATION OF NPAs a. Corporation would continue to follow the guidelines on prudential norms and asset

classification issued by the RBI/SIDBI from time to time. Upgradation of NPAs should also be governed by the said guidelines in force.

b. NPAs not subjected to restructuring will be upgraded immediately on clearance of

defaults, if the account does not otherwise show any inherent deficiencies. c. The restructured sub-standard accounts would be upgraded after satisfactory debt

servicing performance for the specified period in terms of the extant RBI/SIDBI guidelines. Any excess provisions made against upgraded assets would be written back after the specified period.

d. As for Doubtful and Loss assets, where relief/concessions have been granted or the

terms of assistance have been renegotiated, the policy for upgradation of such accounts would be decided in consultation with RBI/SIDBI/Statutory Auditors.

g-130-loan recov.policy 2011