10 key long term trends in the maritime business

TRANSCRIPT

► Demand

► Supply

► Markets

► The Future

► Demand

► Supply

► Markets

► The Future

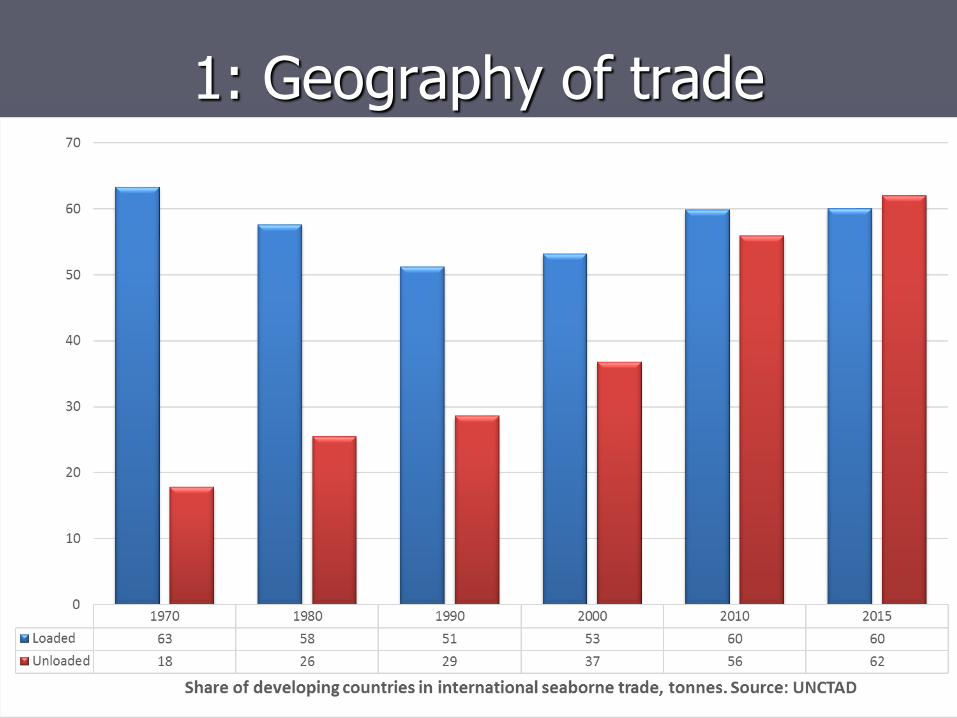

1: Geography of trade

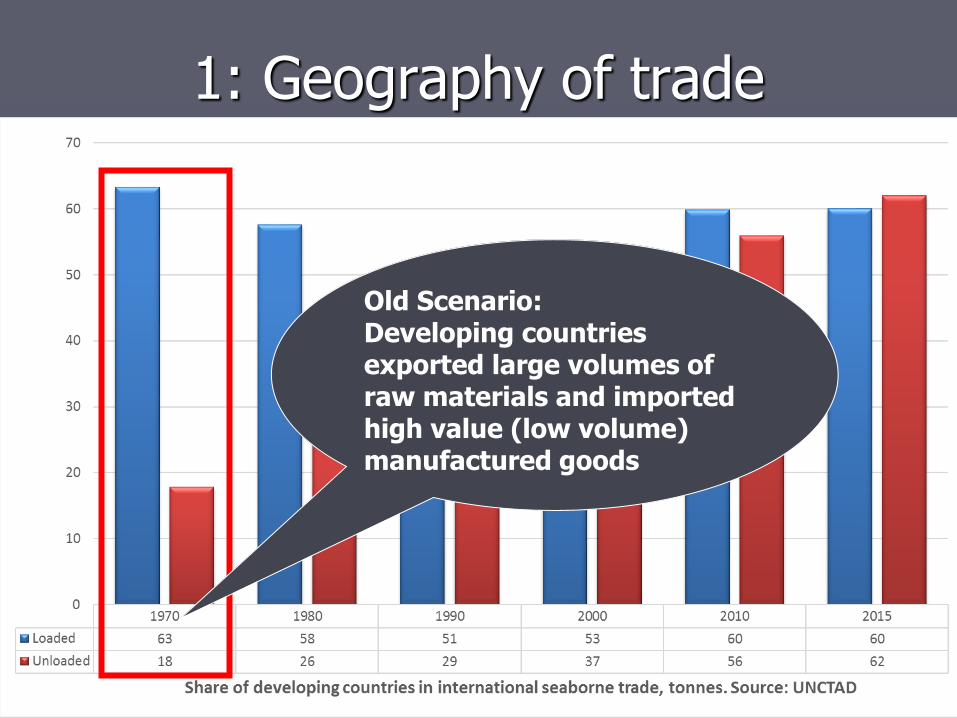

1: Geography of trade

Old Scenario: Developing countries exported large volumes of raw materials and imported high value (low volume) manufactured goods

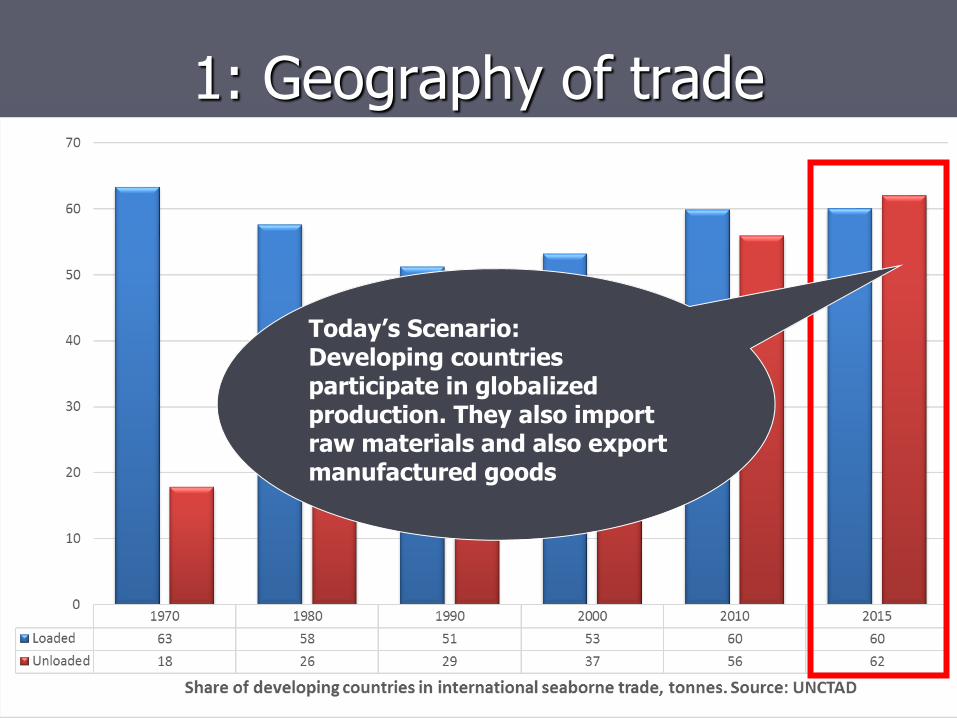

1: Geography of trade

Today’s Scenario: Developing countries participate in globalized production. They also import raw materials and also export manufactured goods

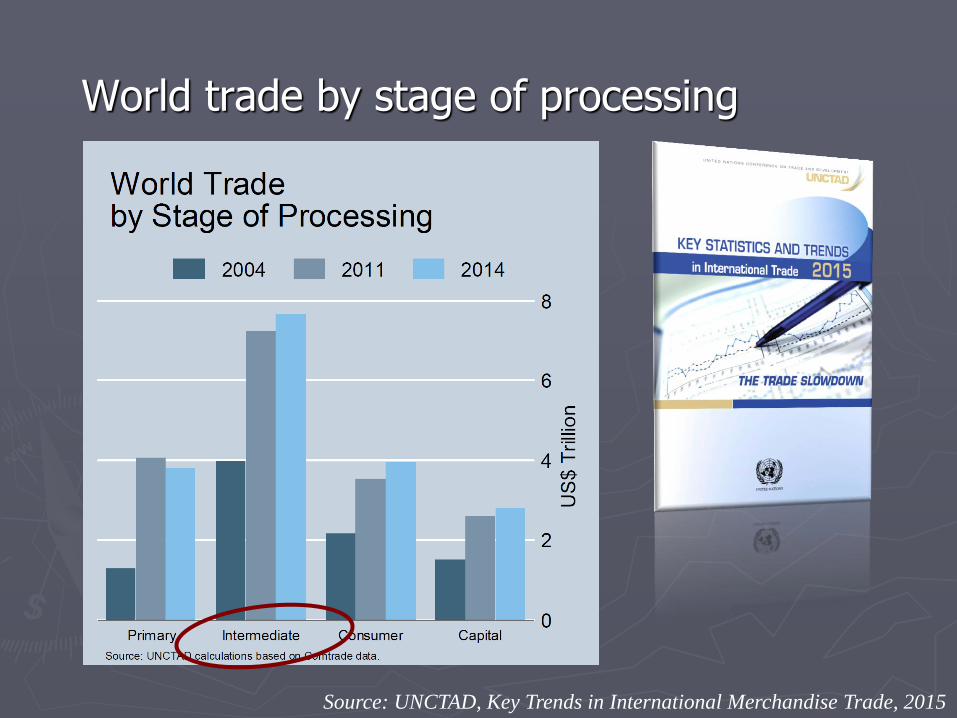

2: Maritime trade is part of globalized production

► More trade in intermediate goods (40%)

► More intra-company trade

► More door-to-door services

► Logistics is part of the production process

World trade by stage of processing

Source: UNCTAD, Key Trends in International Merchandise Trade, 2015

3: Containerization

(Bernhofen et al, 2013)

Demand

► Supply

► Markets

► The Future

Demand

► Supply

► Markets

► The Future

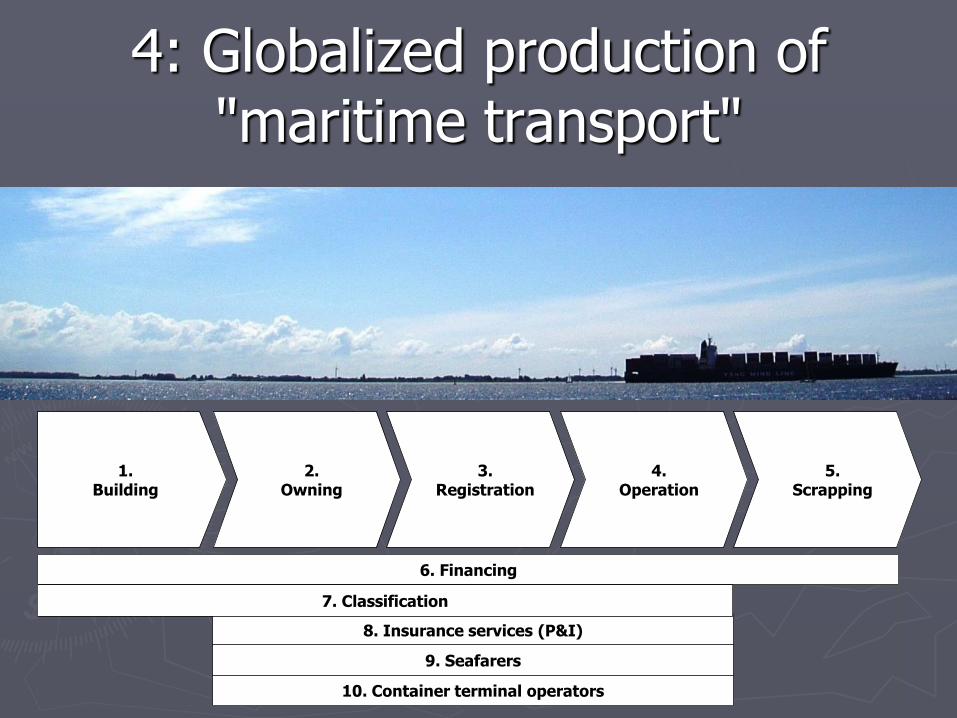

8. Insurance services (P&I)

10. Container terminal operators

9. Seafarers

6. Financing

7. Classification

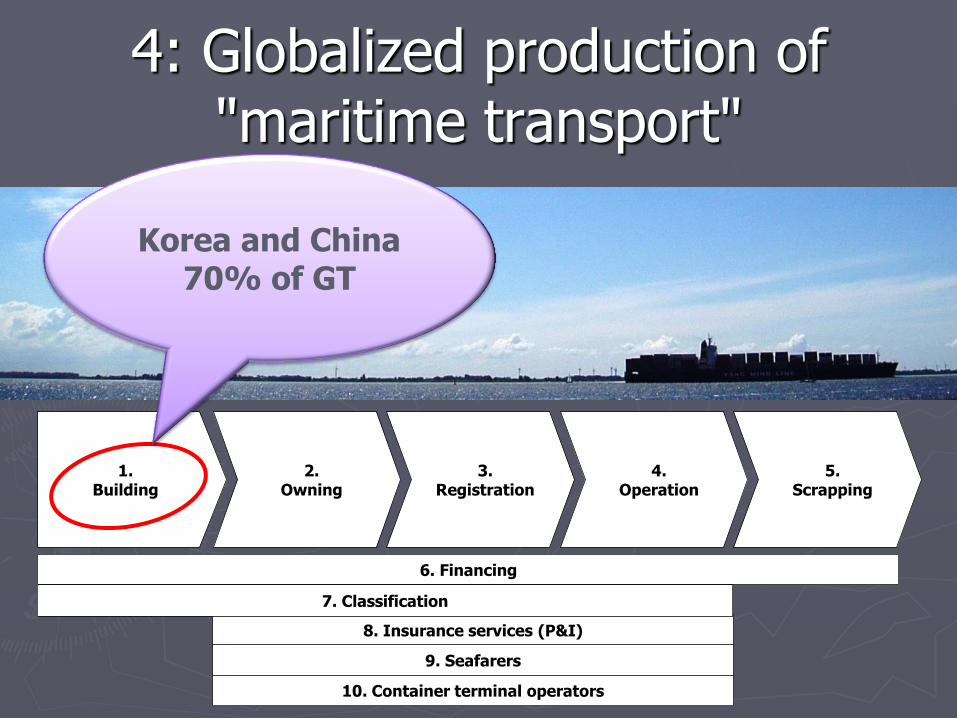

1. Building

5. Scrapping

2. Owning

3. Registration

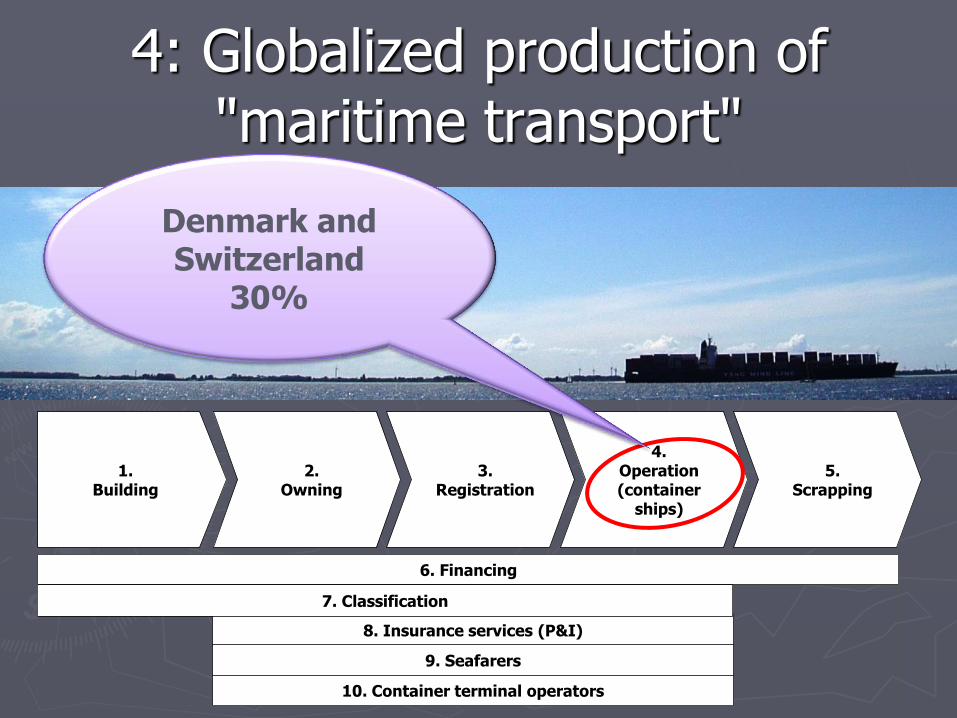

4. Operation

4: Globalized production of "maritime transport"

Example: “Hoffmann Shipping”: ►Owner: German ►Flag: Antigua and Barbuda ►Freight agent: Netherlands ►Seafarers: Poland ►Crewing agent: Cyprus ►Cargo: Turkey ► to Canada ►Fuel: Spain ►Insurance: United Kingdom ►Shipyard: Portugal

►Captains’ favourite drink: Ireland

8. Insurance services (P&I)

10. Container terminal operators

9. Seafarers

6. Financing

7. Classification

1. Building

5. Scrapping

2. Owning

3. Registration

4. Operation

4: Globalized production of "maritime transport"

8. Insurance services (P&I)

10. Container terminal operators

9. Seafarers

6. Financing

7. Classification

1. Building

5. Scrapping

2. Owning

3. Registration

4. Operation

4: Globalized production of "maritime transport"

Korea and China 70% of GT

8. Insurance services (P&I)

10. Container terminal operators

9. Seafarers

6. Financing

7. Classification

1. Building

5. Scrapping

2. Owning

3. Registration

4. Operation

4: Globalized production of "maritime transport"

Greece, Japan: 29%

8. Insurance services (P&I)

10. Container terminal operators

9. Seafarers

6. Financing

7. Classification

1. Building

5. Scrapping

2. Owning

3. Registration

4. Operation

4: Globalized production of "maritime transport"

Panama, Liberia, Marshall Islands:

41%

8. Insurance services (P&I)

10. Container terminal operators

9. Seafarers

6. Financing

7. Classification

1. Building

5. Scrapping

2. Owning

3. Registration

4. Operation (container

ships)

4: Globalized production of "maritime transport"

Denmark and Switzerland

30%

8. Insurance services (P&I)

10. Container terminal operators

9. Seafarers

6. Financing

7. Classification

1. Building

5. Scrapping

2. Owning

3. Registration

4. Operation (container

ships)

4: Globalized production of "maritime transport"

Denmark and Switzerland

30%

8. Insurance services (P&I)

10. Container terminal operators

9. Seafarers

6. Financing

7. Classification

1. Building

5. Scrapping

2. Owning

3. Registration

4. Operation

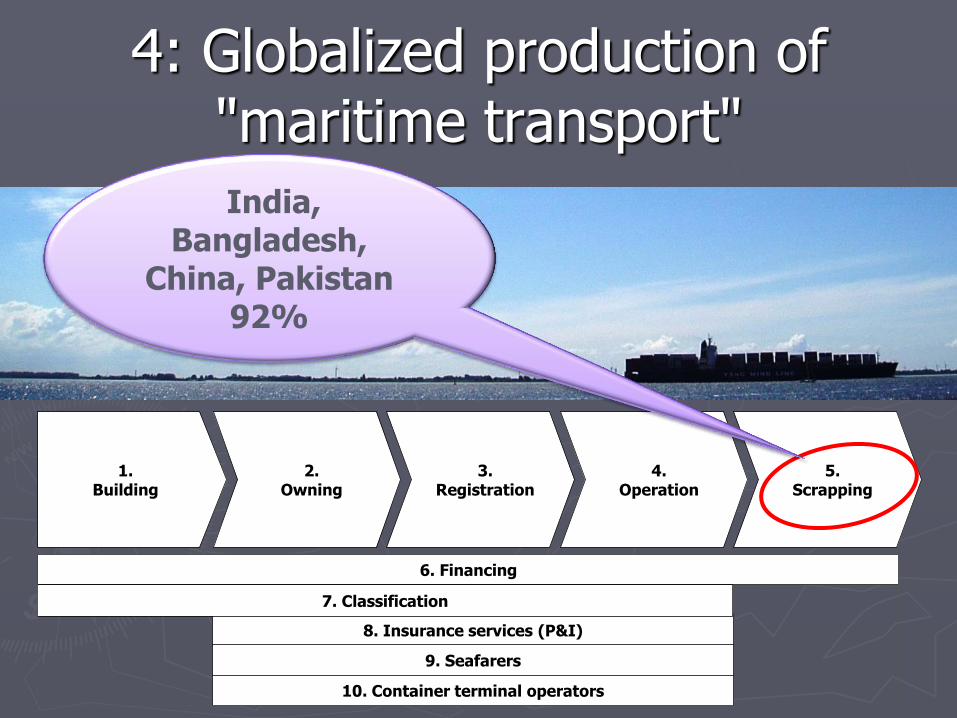

4: Globalized production of "maritime transport"

India, Bangladesh,

China, Pakistan 92%

8. Insurance services (P&I)

10. Container terminal operators

9. Seafarers

6. Financing

7. Classification

1. Building

5. Scrapping

2. Owning

3. Registration

4. Operation

4: Globalized production of "maritime transport"

Financial and other services:

UK, Scandinavia

8. Insurance services (P&I)

10. Container terminal operators

9. Seafarers

6. Financing

7. Classification

1. Building

5. Scrapping

2. Owning

3. Registration

4. Operation

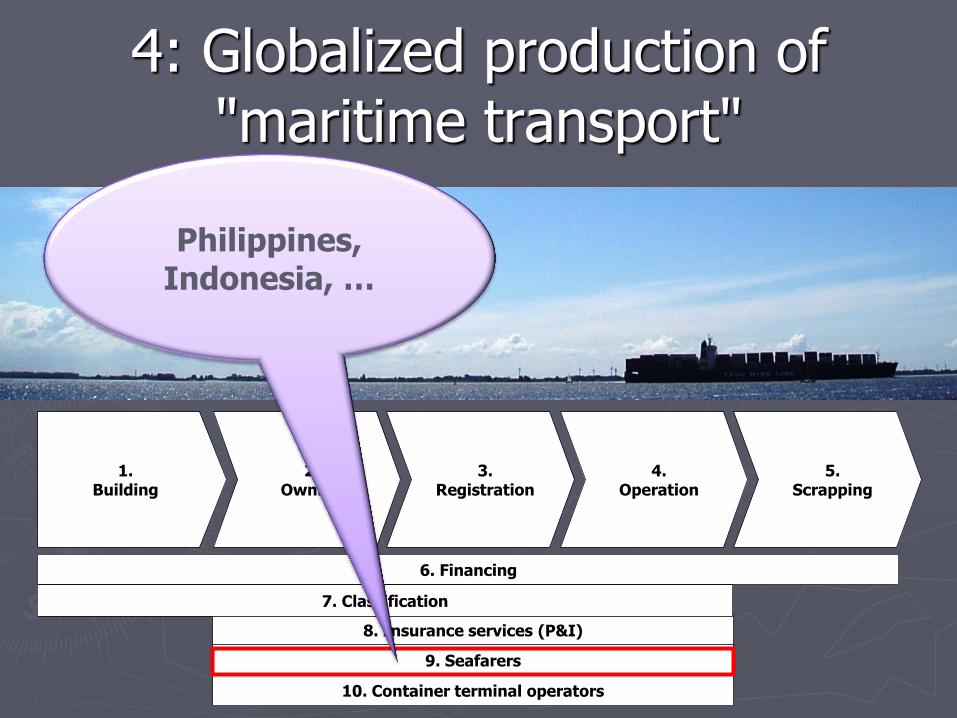

4: Globalized production of "maritime transport"

Philippines, Indonesia, …

8. Insurance services (P&I)

10. Container terminal operators

9. Seafarers

6. Financing

7. Classification

1. Building

5. Scrapping

2. Owning

3. Registration

4. Operation

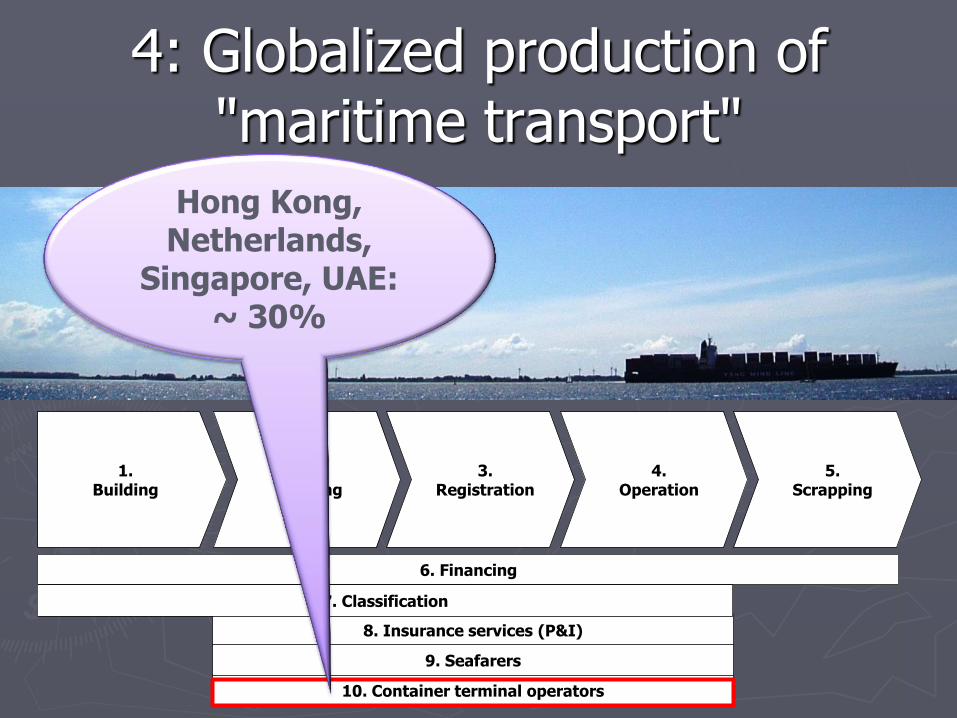

4: Globalized production of "maritime transport"

Hong Kong, Netherlands,

Singapore, UAE: ~ 30%

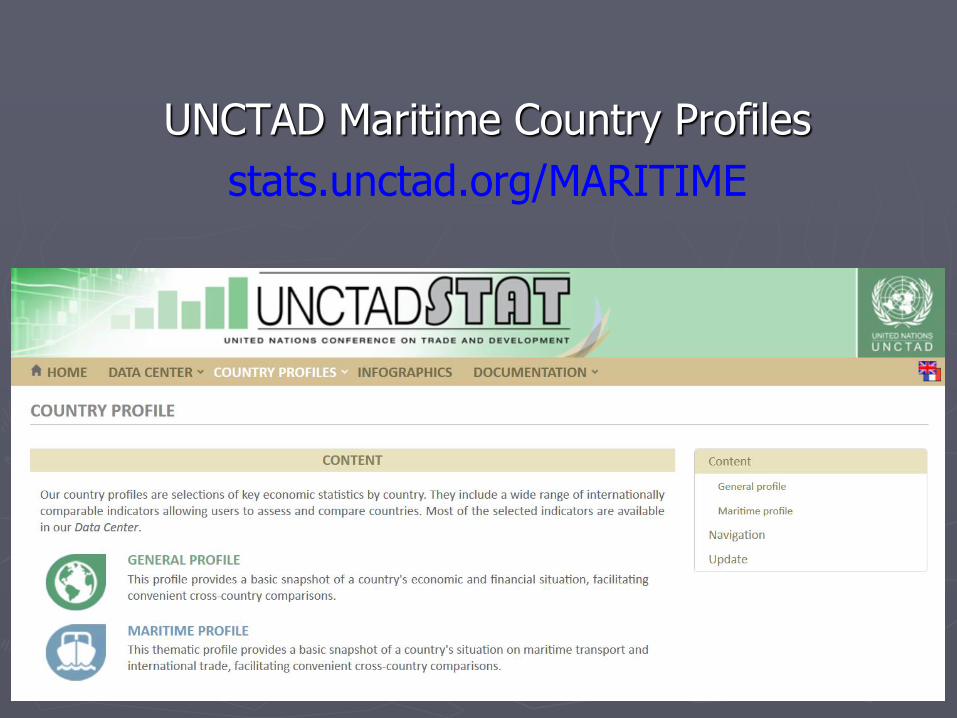

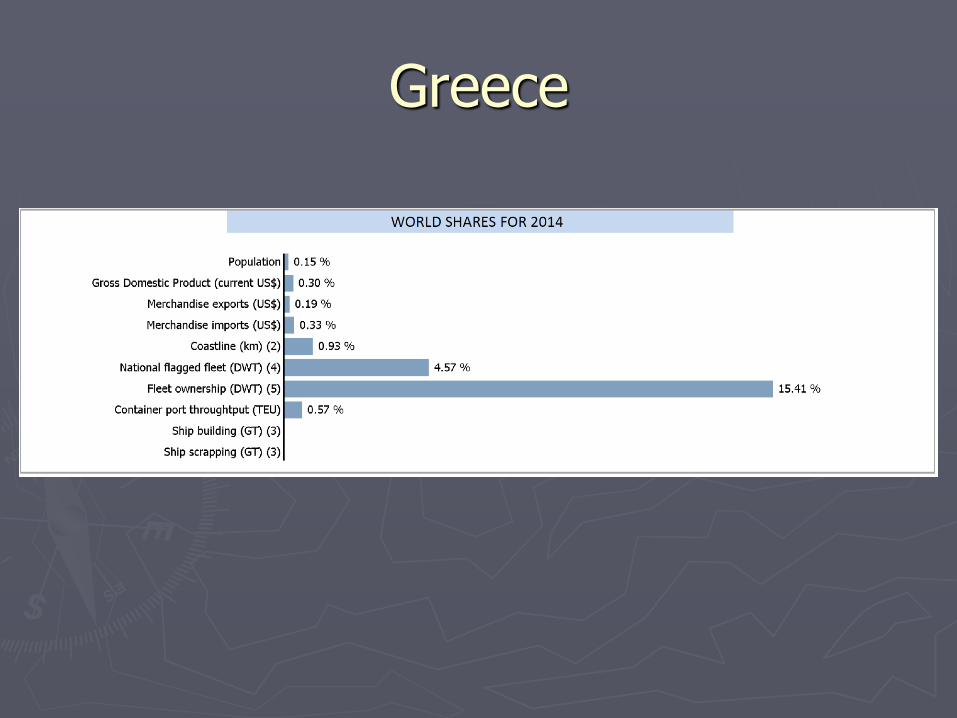

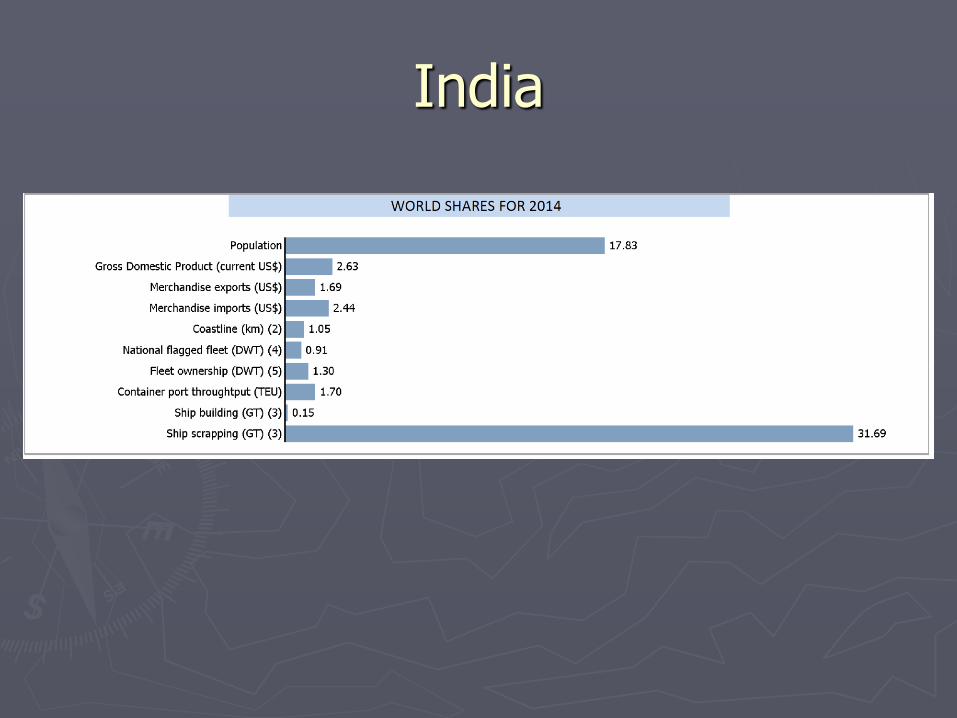

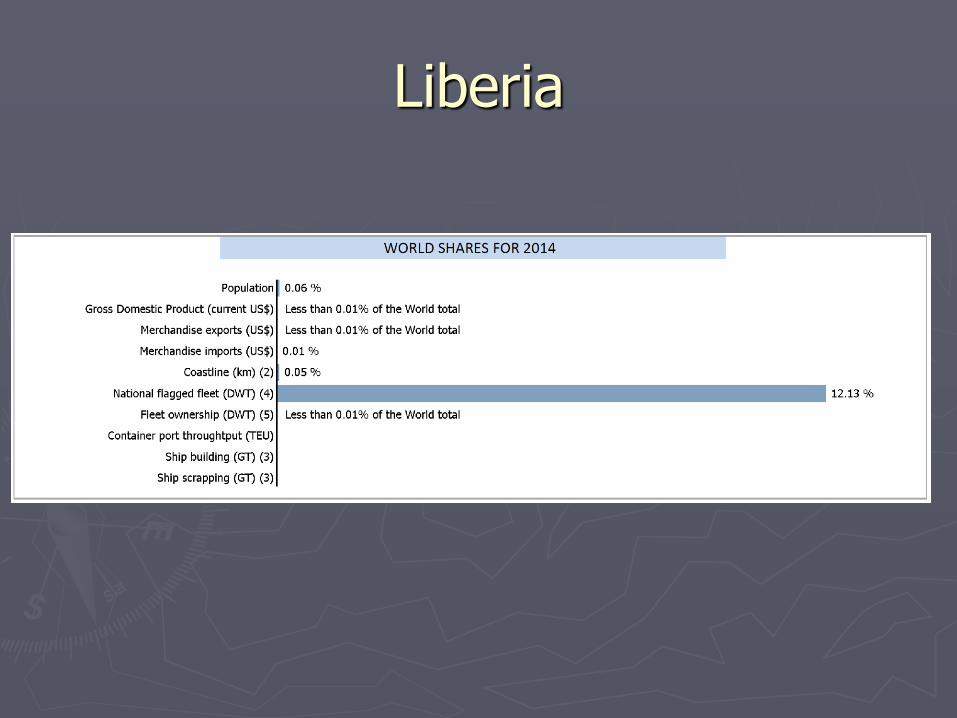

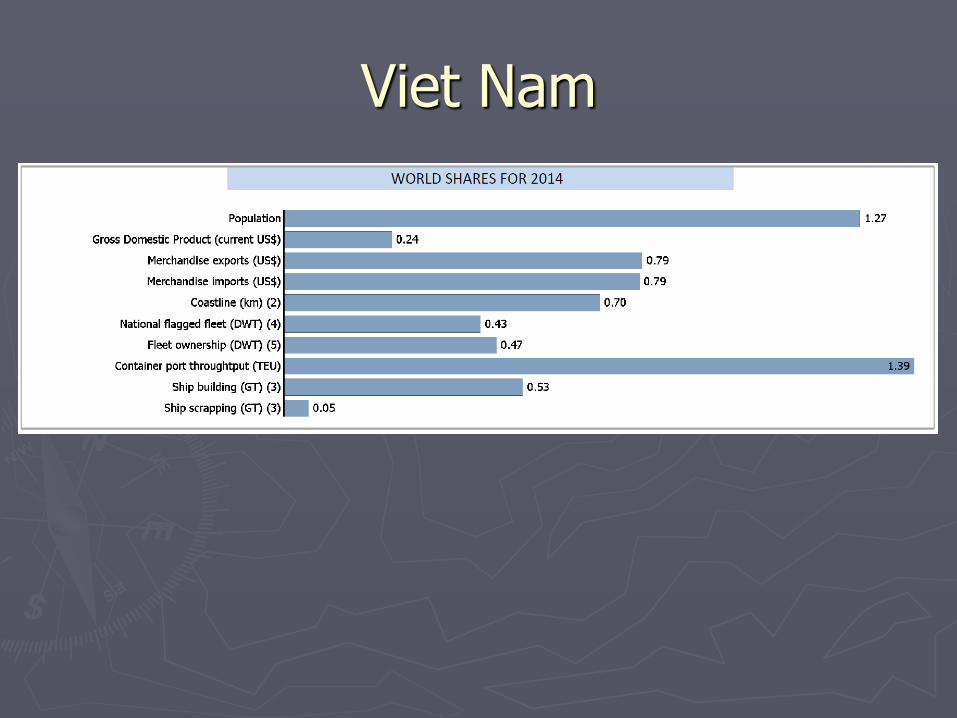

UNCTAD Maritime Country Profiles

stats.unctad.org/MARITIME

Greece

India

Liberia

Republic of Korea

Viet Nam

UNCTAD Maritime Country Profiles

stats.unctad.org/MARITIME

8. Insurance services (P&I)

10. Container terminal operators

9. Seafarers

6. Financing

7. Classification

1. Building

5. Scrapping

2. Owning

3. Registration

4. Operation

4: Globalized production of "maritime transport"

5: Industry consolidation (the other side of the same coin)

►As countries specialize…

►Industry

sees a process of concentration

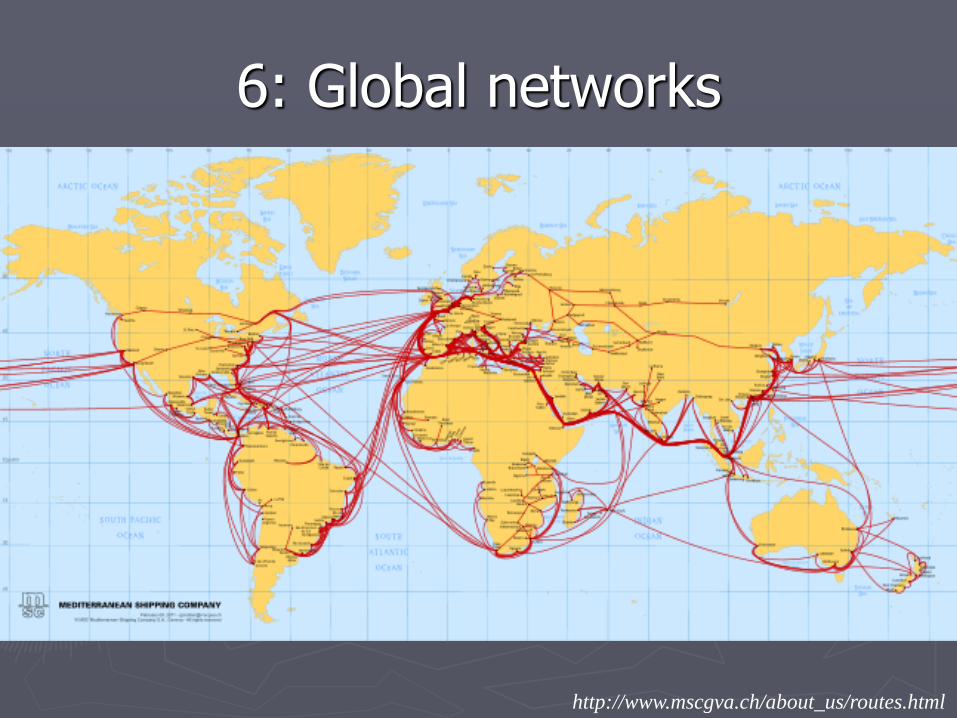

6: Global networks

http://www.mscgva.ch/about_us/routes.html

Networking

Out of 162 x 161 pairs of countries:

How many are connected by direct services?

Source: UNCTAD, based on data from Containerization International

Demand

Supply

► Markets

► The Future

Demand

Supply

► Markets

► The Future

7: Liberalized markets

► Less cargo reservation

► Fewer liner conferences (cartels)

► More private sector participation

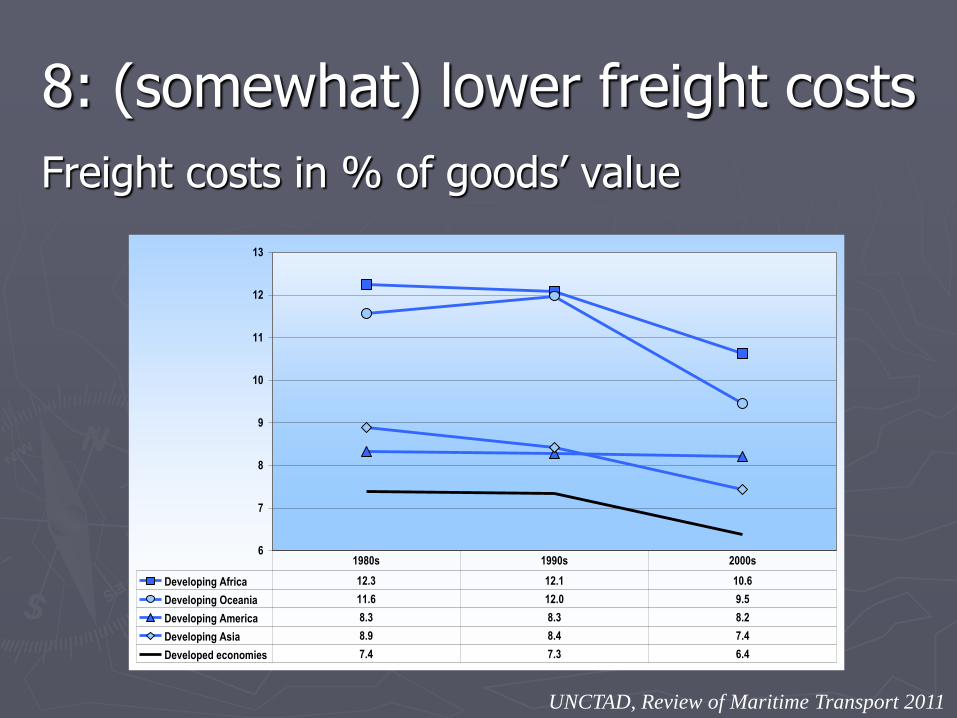

8: (somewhat) lower freight costs

UNCTAD, Review of Maritime Transport 2011

Freight costs in % of goods’ value

6

7

8

9

10

11

12

13

Developing Africa 12.3 12.1 10.6

Developing Oceania 11.6 12.0 9.5

Developing America 8.3 8.3 8.2

Developing Asia 8.9 8.4 7.4

Developed economies 7.4 7.3 6.4

1980s 1990s 2000s

9: More volatile freight rates

Today’s container shipping

►Ever larger ships

►Extremely low freight rates

►Idle fleet

Why is this a problem?

►Ever larger ships

►Extremely low freight rates

►Idle fleet

Why is this a problem?

a) Total logistics costs may actually go up

Why is this a problem?

b) It’s a game: Unless old ships are scrapped, the oversupply will remain, or rather, increase, as carriers build new and larger ships

Why is this a problem?

c) Potential oligopolies in small markets

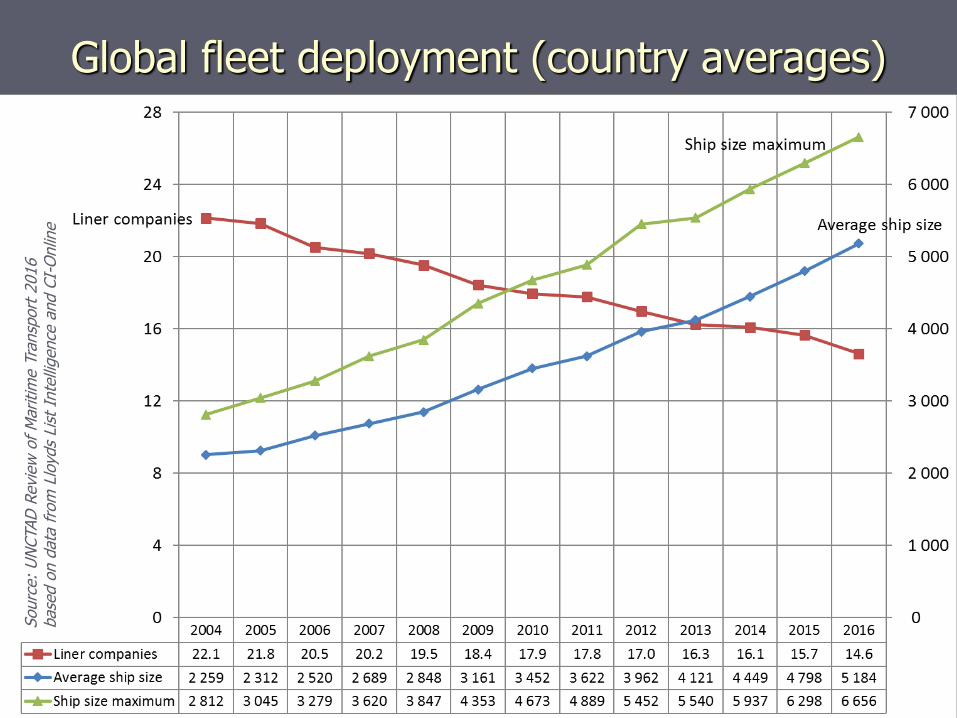

Global fleet deployment (country averages)

►Ever larger ships

►Extremely low freight rates

►Idle fleet

Sourc

e:

UN

CTAD

Revi

ew

of

Maritim

e T

ransp

ort

2016

base

d o

n d

ata

fro

m L

loyd

s Li

st I

nte

lligence

and C

I-O

nlin

e

Demand

Supply

Markets

► The Future

Demand

Supply

Markets

► The Future G

lob

ali

za

tio

n

Demand

Supply

Markets

► The Future

10: The Future

The future of today is different

Is the growth sustainable?

Where are we heading?

How much bigger can the ships get?

What will we do with our garbage

Building a new island

… out of garbage

How do we deal with changing weather patterns?

How do we deal with changing weather patterns?

How much more can the ports grow?

Will we run out of oil?

Can we beat the pirates?

Will we run out of marine resources?

Will the sea level rise?

What will be the impact of climate change?

What will be the questions

of The Future?

10 key long term trends in maritime supply chains

Geneva / Paris, 1 December 2016, [email protected]