1 seminario de capacitación regional iais – assal – fides lima 2009 regulation, supervision and...

TRANSCRIPT

1

Seminario de Capacitación Regional IAIS – Seminario de Capacitación Regional IAIS – ASSAL – FIDES Lima 2009ASSAL – FIDES Lima 2009

Regulation, Supervision and

Policy Issuesfor

Microinsurance in Brazil

2

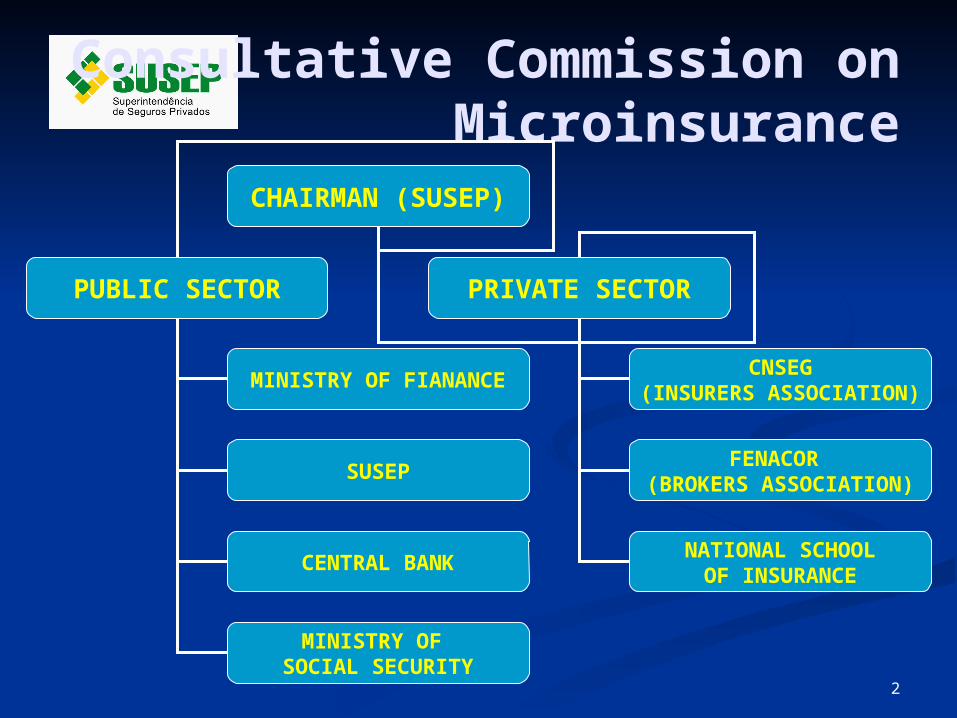

Consultative Commission on Microinsurance

CHAIRMAN (SUSEP)

PUBLIC SECTOR PRIVATE SECTOR

MINISTRY OF FIANANCECNSEG

(INSURERS ASSOCIATION)

SUSEP

CENTRAL BANK

FENACOR (BROKERS ASSOCIATION)

NATIONAL SCHOOLOF INSURANCE

MINISTRY OF SOCIAL SECURITY

3

SUSEP’s Working Groupon Microinsurance

COORDINATOR

STATISTICS DIVISION

LIFE INSURANCE DIVISION

P & C INSURANCE DIVISION

TAX DIVISION

ON-SITE SUPERVISON DEPARTMENT

GENERAL SECRETARIAT

4

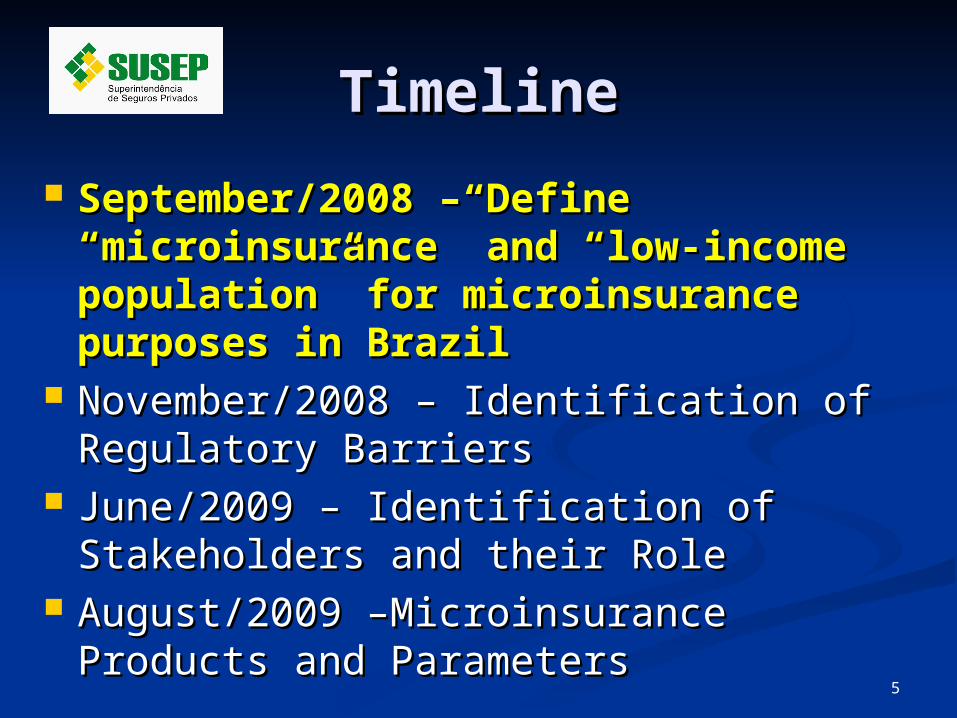

TimelineTimeline

September/2008 – Define September/2008 – Define “microinsurance” and “low-income “microinsurance” and “low-income population” for microinsurance population” for microinsurance purposes in Brazilpurposes in Brazil

November/2008 – Identification of November/2008 – Identification of Regulatory BarriersRegulatory Barriers

June/2009 – Identification of June/2009 – Identification of Stakeholders and their RoleStakeholders and their Role

August/2009 –Microinsurance August/2009 –Microinsurance Products and ParametersProducts and Parameters

5

TimelineTimeline

September/2008 – Define September/2008 – Define “microinsurance” and “low-income “microinsurance” and “low-income population” for microinsurance population” for microinsurance purposes in Brazilpurposes in Brazil

November/2008 – Identification of November/2008 – Identification of Regulatory BarriersRegulatory Barriers

June/2009 – Identification of June/2009 – Identification of Stakeholders and their RoleStakeholders and their Role

August/2009 –Microinsurance Products August/2009 –Microinsurance Products and Parametersand Parameters

6

“Microinsurance” Definition

“Microinsurance is the insurance protection provided by licensed entities within the country against specific risks which aims fundamentally to preserve the socio-economic and personal and family situation of the low-income population by means of premium payments which are proportional to the probability and cost of risks involved, in accordance with the legislation and globally accepted insurance principles.”

7

“Low Income Population”

Many variables influence the “poverty” concept

Brazil has continental dimensions and great contrasts among its different regions

Variables linked to income per capta jointly with educational variables and household variables, aiming to: 1. Preliminary investigation on the educational levels of potential microinsurance consumers2. Possible distribution channels and/or microinsurance premiums collection networks

8

Population: 184,388,620

52%

48%

Economically Active Population: 96,031,971Population not classified as EAP: 88,356,649

Source: IBGE - National Household Sample Survey 2005

9Source: IBGE - National Household Sample Survey 2005

Income Distribution (monthly per capta)

970 (0,6%)

2.557 (1,6%)

7.269 (4,7%)

9.036 (5,8%)

12.046 (7,7%)

32.075 (20,5%)

40.064 (25,6%)

50.758 (32,5%)Without income

Up to $208

$208 to $416

$416 to $624

$624 to $1040

$1040 to $2080

$2080 to $4160

Over $4160

Thousand persons

10Source: IBGE - National Household Sample Survey 2006

Functional illiteracy rate of persons aged 15 years and older

34,4

27,7

17,3

5,7

41,5

37,4

23,926,0

23,2

5,7

5,5

15,8

0,0

5,0

10,0

15,0

20,0

25,0

30,0

35,0

40,0

45,0

up to $104 >$104 to $208 >$208 to $416 > $416minimum wage = US$208

Brazil

North

Northeast

Southeast

South

Central East

Education X Income 1

11

Average years of schooling of persons aged 25 years and olderby montlhy income household per capta by fifth

0,0

2,0

4,0

6,0

8,0

10,0

12,0

poorest20%

2o. fifth 3o. Fifth 4o. Fifth richest20%

nationalaverage

years

of

stu

dy

Brazil

North

Northeast

Sotheast

South

Central East

Education X Income 2

Source: IBGE - National Household Sample Survey 2006

12

Urban Concentration

38.849.338

28.923.782

9.994.660

19.297.623

5.729.286

99.327.856

0 to 14 years-old

15 to 49 years-old

Over 49 years-old

Age

Urban Rural

Source: IBGE - National Household Sample Survey 2005

13

% urban households by monthly income per capita

20,6

27,525,3

9,6

7,0 6,9

39,0

30,5

16,5

4,93,5 3,5

12,5

25,6

30,8

12,7

9,17,7

0,0

5,0

10,0

15,0

20,0

25,0

30,0

35,0

40,0

45,0

up to $104 >$104 to $208 >$208 to $416 >$416 to $624 >$624 to $1040 >$1040

minimum wage = US$208

Brazil

North

Northeast

Southeast

South

Midle-East

Urban Households X Income

Source: IBGE - National Household Sample Survey 2006

14

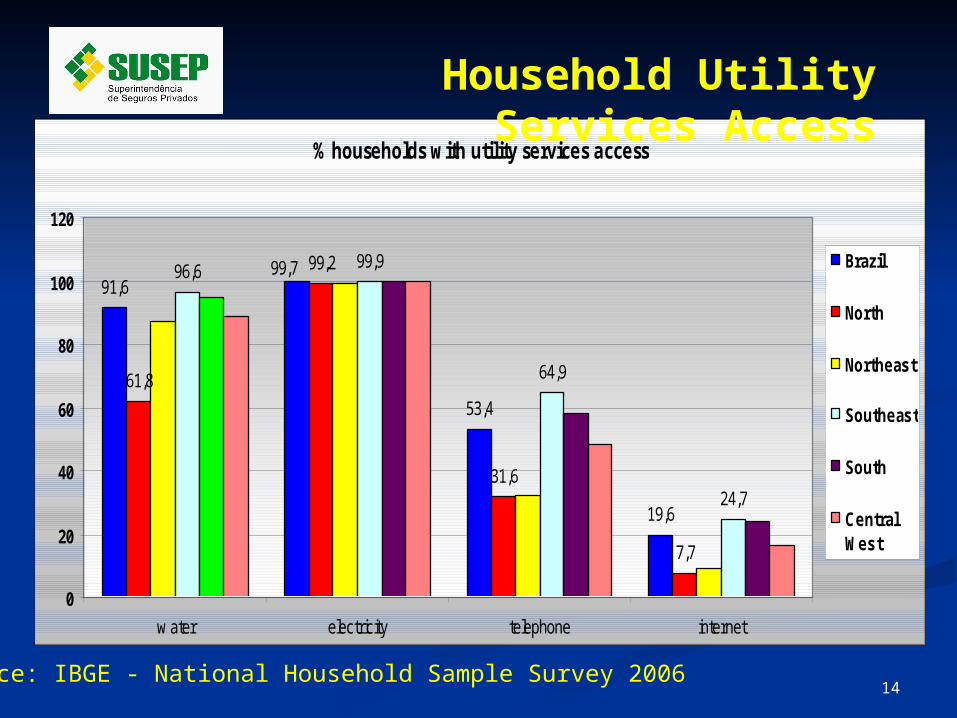

% households with utility services access

91,6

53,4

19,6

61,8

99,2

31,6

7,7

96,6 99,9

64,9

24,7

99,7

0

20

40

60

80

100

120

w ater electricity telephone internet

Brazil

North

Northeast

Southeast

South

CentralWest

Household Utility Services Access

Source: IBGE - National Household Sample Survey 2006

15

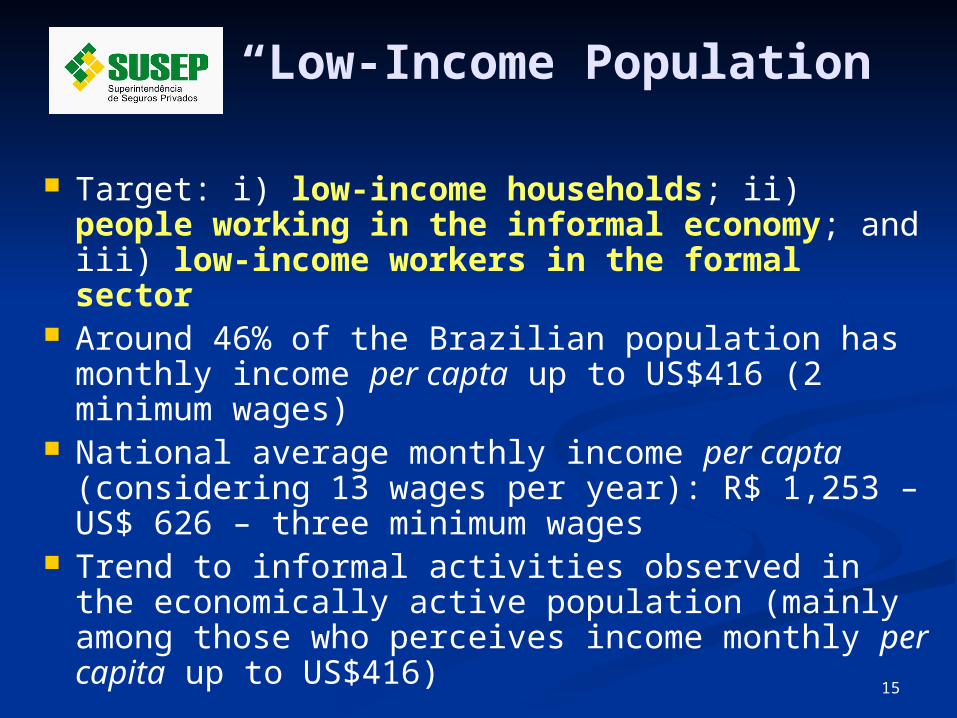

“Low-Income Population”

Target: i) low-income households; ii) people working in the informal economy; and iii) low-income workers in the formal sector

Around 46% of the Brazilian population has monthly income per capta up to US$416 (2 minimum wages)

National average monthly income per capta (considering 13 wages per year): R$ 1,253 – US$ 626 – three minimum wages

Trend to informal activities observed in the economically active population (mainly among those who perceives income monthly per capita up to US$416)

16

“Low-Income Population”Definition for Study

Purposes

“The low-income population in Brazil, for specific microinsurance purposes, is the segment of the population which monthly income per capta is up to three minimum wage national reference”. (US$624)

17

Survey Program MI Potential Market Mortality Table (Families up to 3 minimum wage per

capita) MI Experiences abroad (translation of the five-

country case studies) Identification of Regulatory Barriers Social Insurance within the Public Sphere Social Insurance supported or practiced by Private

Sphere Microcredit and MI Synergy Insurers perspectives Collection premiums models Distribution Channels, efficiency and costs Low Income Demand for Private Insurance MI Economic and Social Benefits

18

TimelineTimeline

September/2008 – Define September/2008 – Define “microinsurance” and “low-income “microinsurance” and “low-income population” for microinsurance population” for microinsurance purposes in Brazilpurposes in Brazil

November/2008 – Identification of November/2008 – Identification of Regulatory BarriersRegulatory Barriers

June/2009 – Identification of June/2009 – Identification of Stakeholders and their RoleStakeholders and their Role

August/2009 –Microinsurance August/2009 –Microinsurance Products and ParametersProducts and Parameters

19

Identification of Identification of Regulatory BarriersRegulatory Barriers

Assessment of the legislation which Assessment of the legislation which regulates the insurance sector – around regulates the insurance sector – around 90 rules (laws, resolutions and circulars)90 rules (laws, resolutions and circulars)

Evaluation of regulation impact – Evaluation of regulation impact – identification of identification of barriersbarriers, , opportunities and gapsopportunities and gaps in the in the legislation and also legislation and also risks and threats risks and threats due to lack of protection elements.due to lack of protection elements.

Meetings with private sector Meetings with private sector representatives – operational and representatives – operational and marketing experiencemarketing experience..

2020

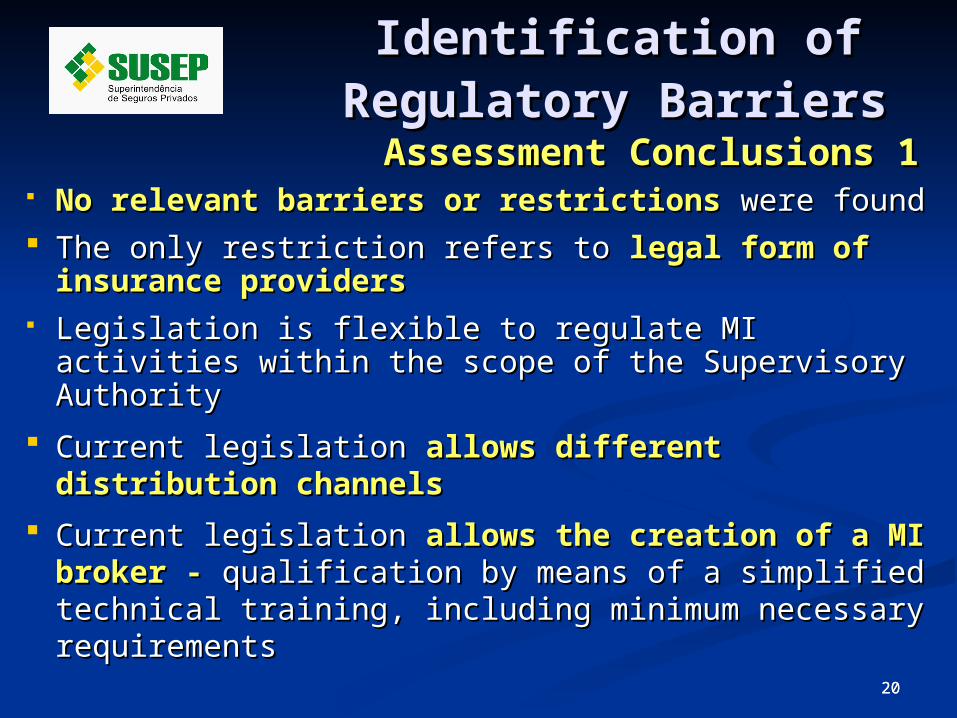

Identification of Identification of Regulatory BarriersRegulatory Barriers Assessment Conclusions 1Assessment Conclusions 1

No relevant barriers or restrictions No relevant barriers or restrictions were foundwere found The only restriction refers to The only restriction refers to legal form of legal form of

insurance providersinsurance providers Legislation is flexible to regulate MI activities Legislation is flexible to regulate MI activities

within the scope of the Supervisory Authoritywithin the scope of the Supervisory Authority

Current legislation Current legislation allows different distribution allows different distribution channelschannels

Current legislation Current legislation allows the creation of a MI allows the creation of a MI broker - broker - qualification by means of a simplified qualification by means of a simplified technical training, including minimum necessary technical training, including minimum necessary requirements requirements

2121

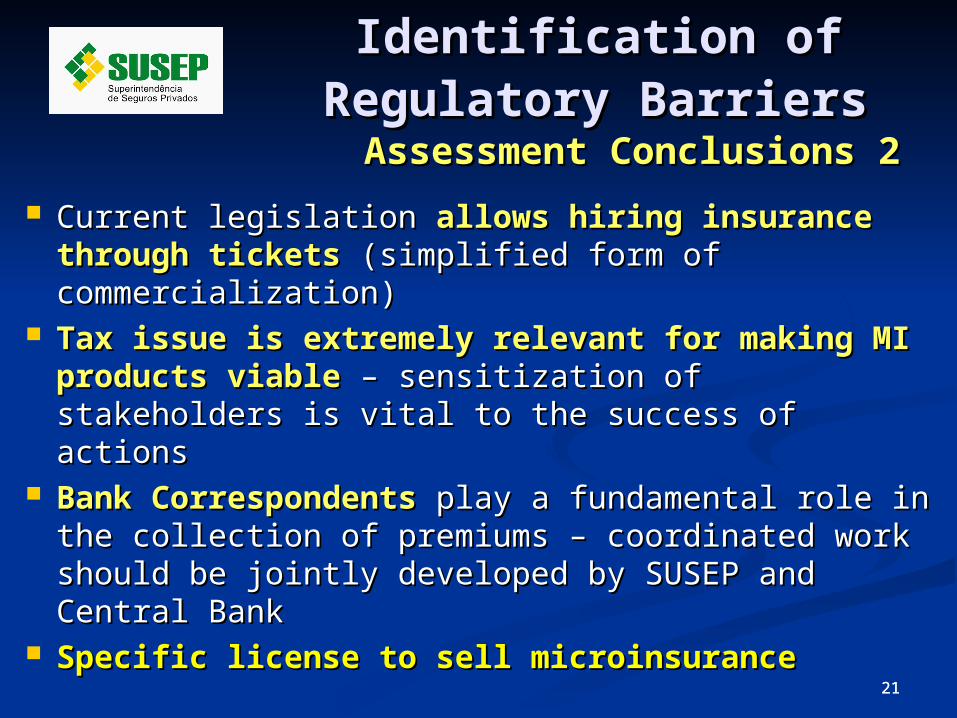

Identification of Identification of Regulatory BarriersRegulatory Barriers Assessment Conclusions 2Assessment Conclusions 2

Current legislation Current legislation allows hiring insurance allows hiring insurance through ticketsthrough tickets (simplified form of (simplified form of commercialization)commercialization)

Tax issue is extremely relevant for making Tax issue is extremely relevant for making MI products viableMI products viable – sensitization of – sensitization of stakeholders is vital to the success of actionsstakeholders is vital to the success of actions

Bank Correspondents Bank Correspondents play a fundamental role play a fundamental role in the collection of premiums – coordinated work in the collection of premiums – coordinated work should be jointly developed by SUSEP and should be jointly developed by SUSEP and Central BankCentral Bank

Specific license to sell microinsuranceSpecific license to sell microinsurance

22

TimelineTimeline

September/2008 – Define September/2008 – Define “microinsurance” and “low-income “microinsurance” and “low-income population” for microinsurance population” for microinsurance purposes in Brazilpurposes in Brazil

November/2008 – Identification of November/2008 – Identification of Regulatory Barriers.Regulatory Barriers.

June/2009 – Identification of June/2009 – Identification of Stakeholders and their RoleStakeholders and their Role

August/2009 –Microinsurance August/2009 –Microinsurance Products and ParametersProducts and Parameters

23

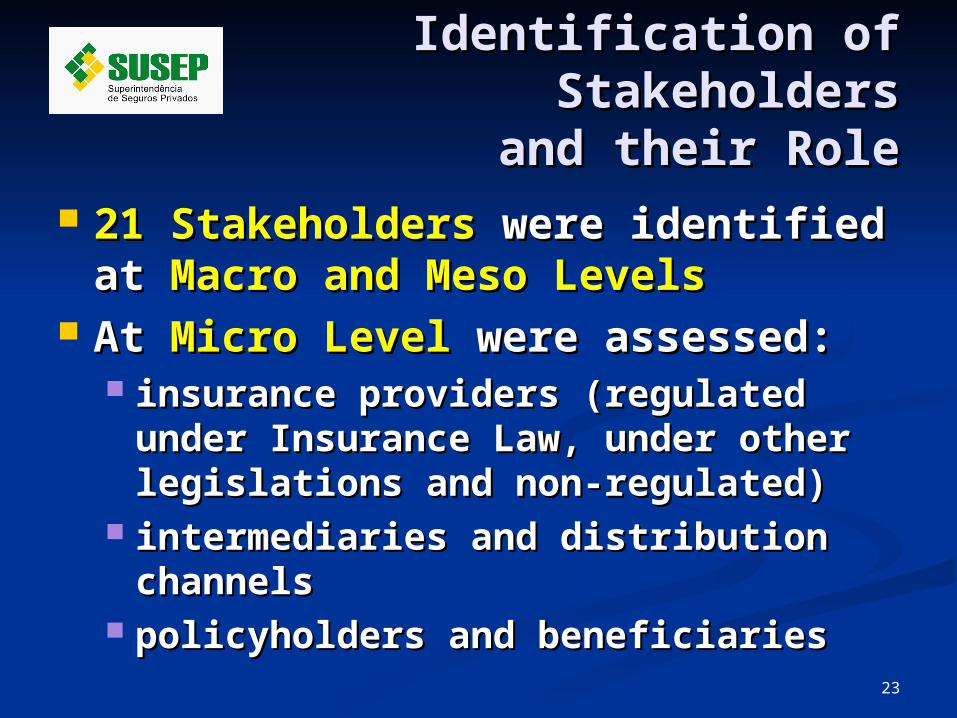

Identification of StakeholdersIdentification of Stakeholdersand their Roleand their Role

21 Stakeholders 21 Stakeholders were identified were identified at at Macro and Meso LevelsMacro and Meso Levels

At At Micro Level Micro Level were assessed:were assessed: insurance providers (regulated insurance providers (regulated

under Insurance Law, under other under Insurance Law, under other legislations and non-regulated)legislations and non-regulated)

intermediaries and distribution intermediaries and distribution channelschannels

policyholders and beneficiariespolicyholders and beneficiaries

24

Identification of StakeholdersIdentification of Stakeholdersand their Roleand their Role

At least 7 different distribution channels At least 7 different distribution channels were assessedwere assessed brokers, churches, coops, NGO´s, MFIs, Banks brokers, churches, coops, NGO´s, MFIs, Banks

and Bank Correspondents, Department Stores, and Bank Correspondents, Department Stores, Public Utility Providers, Capitalization Public Utility Providers, Capitalization Companies, among othersCompanies, among others

Role of Donors and Development Agencies Role of Donors and Development Agencies were evaluated were evaluated

Identification of key-divisions within the Identification of key-divisions within the Supervisory AuthoritySupervisory Authority

As a result, more stakeholders get As a result, more stakeholders get involvedinvolved

25

TimelineTimeline

September/2008 – Define September/2008 – Define “microinsurance” and “low-income “microinsurance” and “low-income population” for microinsurance population” for microinsurance purposes in Brazilpurposes in Brazil

November/2008 – Identification of November/2008 – Identification of Regulatory Barriers.Regulatory Barriers.

June/2009 – Identification of June/2009 – Identification of Stakeholders and their RoleStakeholders and their Role

August/2009 –Microinsurance August/2009 –Microinsurance Products and ParametersProducts and Parameters

26

MI Products

Potential ProductsPotential Products Credit Life (non compulsory)Credit Life (non compulsory) Group Life + Personal AccidentGroup Life + Personal Accident FuneralFuneral

Regulation should encourage new Regulation should encourage new products for low incomersproducts for low incomers

Products well designed will define the Products well designed will define the targettarget

Balance in the regulation: Innovation X Balance in the regulation: Innovation X Consumer Protection (product Consumer Protection (product regulation)regulation)

27

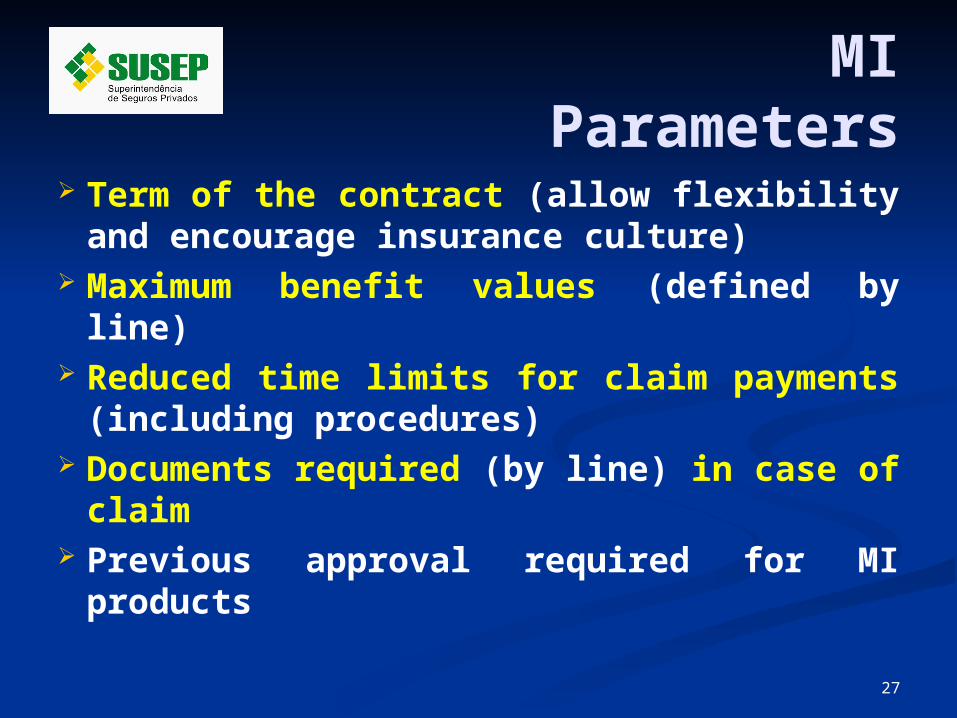

MI Parameters

Term of the contract (allow flexibility and encourage insurance culture)

Maximum benefit values (defined by line)

Reduced time limits for claim payments (including procedures)

Documents required (by line) in case of claim

Previous approval required for MI products

28

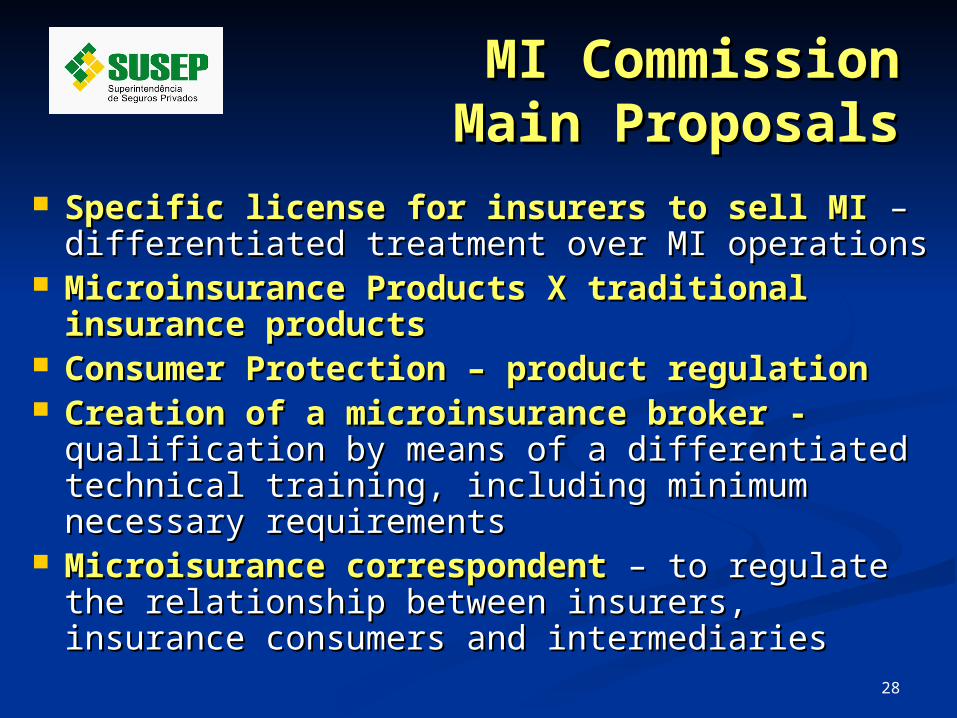

MI CommissionMI CommissionMain ProposalsMain Proposals

Specific license for insurers to sell MI Specific license for insurers to sell MI – – differentiated treatment over MI operationsdifferentiated treatment over MI operations

Microinsurance Products X traditional Microinsurance Products X traditional insurance productsinsurance products

Consumer Protection – product regulationConsumer Protection – product regulation Creation of a microinsurance broker - Creation of a microinsurance broker -

qualification by means of a differentiated qualification by means of a differentiated technical training, including minimum technical training, including minimum necessary requirements necessary requirements

Microisurance correspondentMicroisurance correspondent – to regulate – to regulate the relationship between insurers, insurance the relationship between insurers, insurance consumers and intermediariesconsumers and intermediaries

29

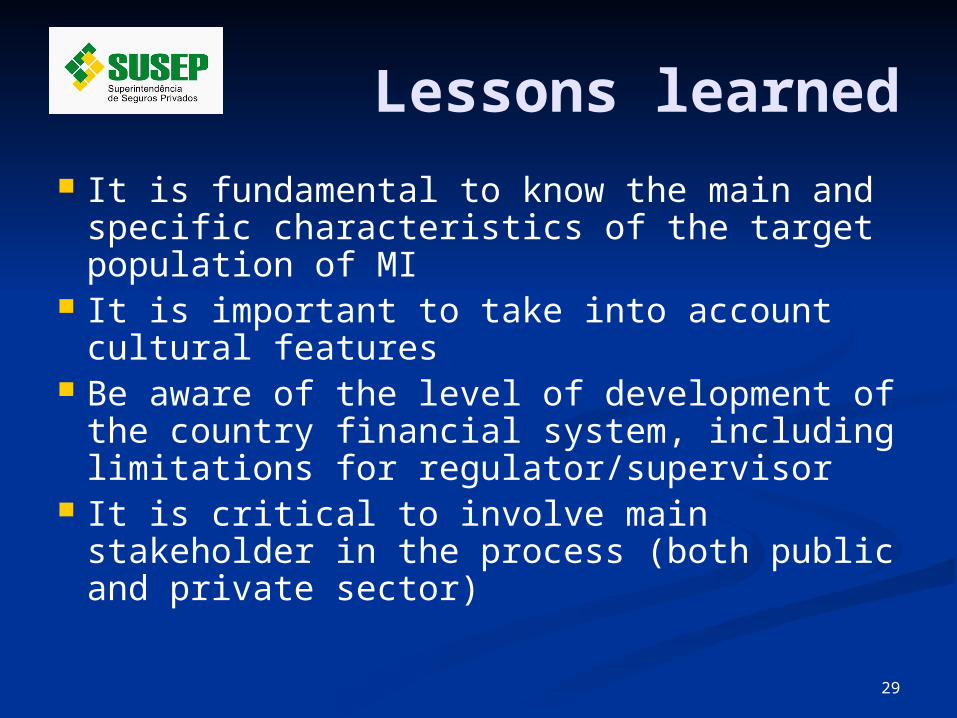

Lessons learned It is fundamental to know the main and

specific characteristics of the target population of MI

It is important to take into account cultural features

Be aware of the level of development of the country financial system, including limitations for regulator/supervisor

It is critical to involve main stakeholder in the process (both public and private sector)

30

THANK YOU!THANK YOU!

Christine de Faria ZettelChristine de Faria [email protected]

www.susep.gov.brwww.susep.gov.br