1 page mortice limited annual report & accounts 2009 · 2017-07-14 · 6 | page mortice limited...

TRANSCRIPT

1 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

Contents 02 Chairman’s statement

05 Chief Executive’s statement

10 Year in review:

Tenon Property Services

13 Peregrine Guarding

16 Tenon Project Services

18 Financial review

21 General information

23 Board of Directors

26 Financial contents

27 Directors’ report

32 Corporate governance report

35 Statement by Directors

36 Independent auditors’ report

38 Financial Statements

45 Notes to Financial Statements

2 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

Chairman’s Statement Manjit Rajain

Expanding our Horizons

The ‘India Story’ is well‐known. Over recent years, off‐

shoring and outsourcing have helped to fuel the Indian

economy and the facilities management and security

industries have benefited and grown in parallel. Watching

how these industries have developed in mature markets has

helped us to see the immense opportunity for Mortice

Limited ('Mortice' or the 'Company') in India today. With

increasing privatisation and a rapidly growing public private

partnership initiative programme, we remain confident that

the market for our Facilities Management ('FM') and security

services will grow beyond any published market projection.

In a year of increased extremist activity, Government, industry and the population at large have become

more security conscious. In turn, the demand for security services has not dropped as much during the

economic downturn as has been witnessed in many other industries. As reported in the Company's trading

update on 8 June 2009, various factors have adversely impacted the Company and its subsidiaries (together

the 'Group') financial performance during the year. Despite the impact that the downturn has had on

business generally, the Group revenues for the year have still grown by 15.3% since the close of financial

year 2007‐08, which we believe is a creditable performance.

Apart from reducing our ability to achieve our projected sales, the Company had also announced on 24

December 2008, that the Board had decided not to pursue the general contracting business as it was highly

likely to face a negative impact as a result of the economic slowdown and its direct impact on the real

estate and infrastructure sectors, which would have resulted in lower margins and also had a high working

capital requirement.

As announced in the Company's trading update on 8 June 2009, the overall impact of the global economic

slowdown including the weakening of the Indian Rupee against the US dollar, the charging of expenses

associated with the Company's listing process, the cost of establishing our new FM business, and

preliminary Mergers & Acquisitions (‘M&A’) activity and overseas market opportunity research, Mortice’s

first full year results reflect our investment in the business. Like many other businesses, we have reduced

our cost base wherever we can do so without negatively impacting our plans for growth and we are

extremely confident that the foundations we have laid will enable the Group to demonstrate superior

growth during financial year 2009‐10.

3 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

In a year in which the global economy took a severe downturn and many countries moved into recession,

India achieved a GDP of 7.1%. Post economic downturn, India originally projected GDP would fall to 5.7%

for FY2009‐10 but has now revised its GDP projections to 6.5% with the services sector expected to grow by

8.2 per cent1 and we are already seeing an increase in new business inquiries and new wins. Our model for

self‐performing our facilities management services has attracted new customers during the recession as

businesses have sought ways of reducing their costs. The track record we have now established has given

Tenon brand recognition within the marketplace a result of which we are seeing a growing number of new

business enquiries.

1 Centre for Monitoring Indian Economy (CMIE) – June 2009

Figure 1: 15 May 2008 ‐ Mortice Lists on AIM

4 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

With the establishment of a pan‐India footprint for Tenon Property Services Limited ('Tenon') to match that

of Peregrine Guarding Limited ('Peregrine'), we have achieved one of our key strategic objectives to fill a

gap in the market by developing a service delivery platform to service customers with large, dispersed

operations. In parallel, our team has developed a sophisticated technology platform to be able to monitor

and manage these operations for our customers providing superior management information enabling

timely, quality management decisions. This key achievement has given us the opportunity to bid for large

pan‐India contracts that will enable a step change in our revenue generation capability.

Many services businesses say that “People are their only asset.” As a self‐performing service provider, this is

particularly the case with Mortice. The platform that we have now established is the result of a huge team

effort during our first year of operation under very challenging market conditions and I thank them all.

We now, confidently, expect to see our investment come to fruition as we continue to expand our horizons.

Figure 2: Tenon Corporate Office, Gurgaon, Delhi, India

5 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

Chief Executive’s Statement Andrew Barker

EXPANDING OUR BUSINESS

The Company set out with certain primary objectives at the

start of the financial year, predominant amongst them to

establish a differentiated outsourced facilities services

corporation. This we aimed to do through the following five

key initiatives:

Expanding our services ‐ Establishing a platform for the

delivery of integrated facilities services through a model of

“self‐performance” by harnessing the spread and strength

of the pan‐India infrastructure of Peregrine Guarding to

offer superior service standards across the country

Expanding our markets ‐ Extending the reach of professional facilities services to address “non‐

traditional” sectors which have historically performed facilities services through own staff (“in‐

sourced”) or local sub‐contractor vendor bases (“out‐tasked”)

Expanding our talent base ‐ Developing top talent with expertise in the various diverse facets of FM

and guarding including engineering services and critical infrastructure management, soft services

delivery, quality, technology support and finance amongst others.

Expanding our Knowledge Base ‐ Developing a superior, customer focused, technology platform to

provide a single client view for all facilities‐related management information requirements to enable

our customers to make informed, timely, quality decisions.

Expanding our Geographies ‐ Developing a pan‐India capability for the delivery of our FM services.

We have made considerable progress during the year towards the achievement of these strategic

objectives. Leading Indian and multinational corporations have bought our services and our track record to

date has now established the Tenon brand as a quality, preferred alternative to the traditional facilities

management sub‐contracting model.

In anticipation of consolidation within the FM and security marketplace in India, considerable effort was

also spent in reviewing the existing facilities services supplier base in India to identify suitable, potential

acquisition targets. Surprisingly, we identified nearly 150 service providers covering every conceivable facet

of the facilities management product. Many of these are small to medium size, local companies. Not

surprisingly, industry consolidation has already started.

6 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

Since the close of the reporting period, Mortice has acquired Rotopower Projects Private Limited

('Rotopower'), a medium‐sized pan‐India Mechanical & Electrical (‘M&E’) turned facilities management

service provider, which has given us strength and depth in this field and helped us to expand our geographic

footprint into East India and strengthened our position in North India.

We are very excited about the acquisition of Rotopower as there are significant synergies across the Group

most notably in cross‐sales opportunities. In the short time since the acquisition took place, we have seen a

number of new sales leads passing between the Group companies. Our expanded infrastructure has also

given us the capacity to be able to manage a significantly larger business with a reduced incremental

overhead. We are now also bidding into new geographies without the need to establish new offices in

those areas where Rotopower already have a presence. The acquisition also provides us with an entry

strategy for those Indian corporate who may not yet be ready for a full FM service but are used to

outsourcing their M&E, housekeeping and security services. Once again, this underlines Tenon’s strategy of

providing “Services That Fit”.

At a strategic level, the acquisition also helps us to adapt as a Group to the changing strategies of our

different customer market sectors. In the interests of generating productivity, we have various customers

who have been moving from discrete services such as manned guarding, M&E and housekeeping to a

“caretaker model” with multi‐tasked employees. In the fast‐growing telecommunications market in India,

Rotopower is currently providing both discrete M&E services and “caretaker” services. Peregrine also has a

significant presence in this market providing security services. As the market matures and we see more

customers seeking similar cost‐efficiency, the combined Tenon and Rotopower platform will enable us to

respond to these changing demands.

Figure 3: Tenon acquisition of

Rotopower ‐ 30th June 2009

7 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

A significant feature of our growing success has been the development of 'TeNet', a single client view, web‐

based suite of applications that support our service delivery and provide our clients and our management

team with transparent, in depth management information. Our technology platform combined with our

ability to deliver mandates in hinterland markets has opened up a much wider potential customer base for

the many companies that have large, dispersed retail portfolios.

During the year, we have continued to attract top industry talent in all our subsidiaries. Our key resources

come with many years of industry experience and qualifications in specialist facilities and security services

fields. This has provided us with the ability to offer enhanced service standards and helped us to gain

recognition for a refreshing and innovative approach to the delivery of our services.

WHY INDIA NEEDS MORTICE?

Over the past 10 years since the recognition of FM services in India, the evolving industry has polarised into

2 distinct sets of service providers; international real estate ('RE') service providers and local vendors.

Whereas the RE service providers are offering higher value solutions, the cost of the service is prohibitive

for many companies in India. By contrast, the low‐cost, local vendor base does not provide the

sophistication or quality of the RE service providers. Tenon was established to provide higher quality FM

services at a cost that is attractive to a much wider customer base.

‘Higher value at lower cost’ ‐ Tenon’s vertically integrated service delivery model unlocks value lost in the RE

service provider model where service delivery is sub‐contracted.

8 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

Going forward, the Company’s focus is to develop Tenon into a truly integrated outsourced management

services corporation and to ensure that Peregrine continues its strong growth by offering a high‐end,

differentiated security product to support our customers’ security needs in the face of increased extremist

activity.

The Public Private Partnership ('PPP') space in India is rapidly gathering momentum. India’s 11th plan has

projected an investment of nearly US$ 500 billion in infrastructure, of which 30% is expected to come from

private investment2. Recognizing the significant fillip that the Private Finance Initiative (‘PFI’) and then PPP

has given to the FM and security industries in other developed economies; we are seeking to establish

ourselves as a credible operating partner for PPP projects.

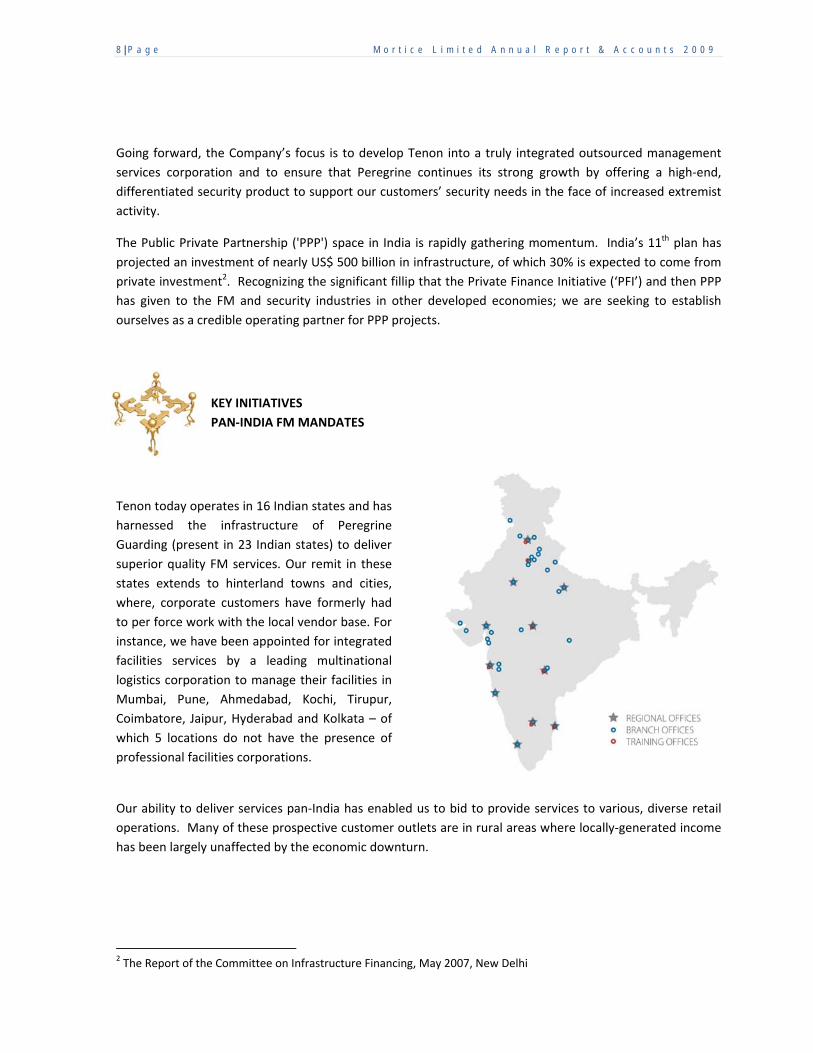

KEY INITIATIVES

PAN‐INDIA FM MANDATES

Tenon today operates in 16 Indian states and has

harnessed the infrastructure of Peregrine

Guarding (present in 23 Indian states) to deliver

superior quality FM services. Our remit in these

states extends to hinterland towns and cities,

where, corporate customers have formerly had

to per force work with the local vendor base. For

instance, we have been appointed for integrated

facilities services by a leading multinational

logistics corporation to manage their facilities in

Mumbai, Pune, Ahmedabad, Kochi, Tirupur,

Coimbatore, Jaipur, Hyderabad and Kolkata – of

which 5 locations do not have the presence of

professional facilities corporations.

Our ability to deliver services pan‐India has enabled us to bid to provide services to various, diverse retail

operations. Many of these prospective customer outlets are in rural areas where locally‐generated income

has been largely unaffected by the economic downturn.

2 The Report of the Committee on Infrastructure Financing, May 2007, New Delhi

9 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

KEY INITIATIVE

NON‐TRADITIONAL SECTORS

Our innovative approach to FM services has resulted in our acceptance by corporations in sectors such as

education and logistics, which have traditionally ‘in‐sourced’ or ‘out‐tasked’ FM services. We have also

designed and implemented innovative programs for sectors such as retail inducing efficiency and

professionalism into the management of logistics, personnel and monitoring compliance. Peregrine has

significantly enhanced its presence in the sectors which have found our services to be of high value – these

sectors include IT/ITeS, Telecom, Financial Services, Manufacturing, Retail and similar sectors where

guarding acts as a key enabler of business safety, security and continuity.

KEY INITIATIVE

PEOPLE

We are a solely, facilities‐focused Company and can

therefore offer exciting career paths and

opportunities for employees to grow within the

facilities management industry. This helps us

attract top industry talent. Examples of our ability

to draw such talent are visible across our

organization including in our support services

where we have been able to recruit seasoned

practice experts for functions such as finance &

accounting, corporate strategy, technology and HR.

These key appointments have helped us to

strengthen our position in the facilities

management and security services market.

Figure 4: "We are a solely, facilities‐focused Company..."

10 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

YEAR IN REVIEW

TENON ‐ EXPANDING OUR SERVICES

Vijayendra Babji – Group Chief Operating Officer

Integrated Facilities Management Services was launched as a

business line under the Tenon brand in January 2008 and

began contract operations in April 2008. The concept was to

introduce a superior service in the market – one that offered

global standards of service delivery in a locally relevant

manner. We have achieved this through our self‐

performance service delivery combined with the strength of

our senior management team.

Over the past year, we believe Tenon has exceeded its

objectives as we have established our pan‐India client base

winning many prestigious appointments with both

multinational and local corporations.

We have also developed customer‐specific, unique service delivery models in keeping with Tenon’s

strapline: “Services that Fit”

Figure 5: “Services That Fit” ‐ The advantages of Tenon's vertically integrated service delivery model

11 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

At the end of the reporting period, Tenon was managing a customer portfolio of over 5 million square feet.

Since this portfolio has been built in 18 months from the commencement of FM operations the Directors

believe it is a notable achievement and that it has surpassed the speed of growth of all other competitors in

the FM market in India to date. Our customer base comprises leading corporations from sectors such as IT /

ITeS / BPO, logistics, financial services, manufacturing, education, residential, real estate developers and

telecommunications. Several of our appointments are for pan‐India portfolios. Based on the level of new

business enquiries and order book the Board remains optimistic about its continued growth over the next

year with along with the expectations of improved market conditions in India.

Having built our base and infrastructure for service delivery, and a reputation for very high standards of

service, Tenon today stands well‐poised to add significant value to all stakeholders – customers and

investors alike.

IFM ADVANTAGE SHOWCASE

TENET – TENON’S SERVICE DELIVERY TECHNOLOGY PLATFORM

Technology is an essential element of our

ability to enhance service delivery

standards. TeNet is Tenon’s technology

platform comprising proprietary, highly‐

specialised, service delivery applications.

This suite of applications resides on ‘single

client view’ client‐specific extranet sites.

Our standard service delivery suite includes

tools for: facilities management and budget

planning, planning and tracking preventive

maintenance schedules, helpdesk

management, transport routing and

monitoring, inventory management,

training, management reporting and asset

management.

We also develop customized tools to meet client and industry‐specific needs; an example is SLATE, our

Satellite Location Activity Tracker, which enables us to monitor and manage service delivery achievement

across geographically dispersed portfolios and provides our customers with transparency and control.

Figure 6: TeNet ‐ Tenon's ‘single client view’ Technology Platform

12 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

TOTAL PRODUCTIVE MAINTENANCE

Tenon has adopted an industry‐leading

engineering practice called Total Productive

Maintenance ('TPM'). Originally a concept

employed in manufacturing, TPM

significantly enhances the quality of on‐

ground engineering service delivery through

a maintenance philosophy that logically

incorporates a combination of preventive,

predictive, and corrective maintenance

practices into a single, comprehensive

program. We are able to enhance the

effectiveness of TPM as a result of our

model of self performance, giving us the

control to train, develop and nurture

technical talent with a clear career path for

employees.

COMMUNICATIONS

Tenon today employs over 20,300 people across the sub‐

continent. The majority of these employees are located at

customer premises. Our ability to keep them informed

about the Company’s developments is essential. Where

our employees have access to e‐mail we send regular

updates on business related subjects and activities;

however, not all of our employees have access to

technology. With this in mind, this year also saw the

launch of “tenoCity”, our internal newsletter. This

magazine is also sent to customers to keep them in touch

with how we are developing our services to enhance our

support to them.

A well‐defined programme of senior management visits

also ensures that our site employees have the opportunity

to meet with senior representatives of the business on a

regular basis.

Figure 7: Total Productive Maintenance. Tenon's Technical

Advisory Group management inspecting our technician's

work at a customer site

Figure 8: tenoCity ‐ Tenon's internal

communication to employees and customers

13 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

PEREGRINE – EXPANDING OUR MARKETS

Rakesh Choudhary – Chief Operating Officer

Peregrine Guarding has been amongst the leaders in the field of

professional guarding services since we first established our

services in India in 1995. Today, Peregrine continues to be the

mainstay of the Group.

This year we have reinforced our position as one of the leading

security and guarding organizations in India and we have

continued to build our reputation as a committed and expert

services partner.

During the year, the heightened extremist activity in India and

many other countries has caused our customers to focus on how

they can enhance their security service within the cost

constraints of an economic downturn.

Despite this challenging backdrop, Peregrine has managed to grow its revenue by marginally over 40%

during the reporting period. Peregrine’s differentiators; a robust national service delivery platform, quality

of manpower, training regime and innovative solutions, are all cited as contributors towards our continued

success. In addition to enhancing its position in traditional market sectors such as financial services, IT /

ITeS, corporate offices and manufacturing, we also continued to strengthen our position in emerging

sectors including retail and telecommunications.

The business continues to focus on training

to respond to the changing needs of the

current security environment in India and

has recently opened a Training Institute to

provide a wide range of training courses to

help to develop the specialist skills that our

employees require and enhance their career

prospects. We have also continued to

attract top industry talent. Many of our

senior management today come from elite

backgrounds in the services industry and the

greater proportion of them having qualified

in business management from leading

business schools.

Figure 9: Training for Front of House Security Staff

14 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

SECURITY ADVANTAGE SHOWCASE

NATIONAL CUSTOMER RESPONSE CENTRE

Peregrine has established an initiative

unique to the security industry to

enhance its ability to collect direct

customer feedback which enhances

our responsiveness to customer

requests; and act as a strong

mechanism for quality and continuous

improvement initiatives. Our National

Customer Response Centre is a central

call centre manned by expert

customer response professionals who

have implemented a proven helpdesk

workflow methodology to log

requests, assign responsibilities and

track them to closure.

NEWS ALERTS

A service initiated by Peregrine in the previous year which has

earned significant popularity with customers is our news alerts

service. Twice a day at minimum, and immediately in the

event of a major development, our customers are sent alerts

on developments which have the potential to impact their

security situation. These alerts are sent through multiple

media such as SMS and emails; and are designed to help

customers stay in touch with latest developments and plan

mitigation programs proactively.

Figure 10: "Our National Customer Response Centre is a central

call centre manned by expert customer response professionals."

Figure 11: Peregrine's "Breaking News" and

"Headlines" Services help customers stay in

touch with latest security‐related

developments

15 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

RESEARCH SERVICE

During the year, we have also launched a research

service, published under the heading

“SecurCounsel”. These have included facts, advice

and guidance on counter‐terrorist measures and,

more recently facts and precautions in the face of

the H1N1 “swine flu” threat.

SCOPE OF SERVICE

Over the past year, we have recruited several new

senior managers to strengthen our service

delivery capability. We have also introduced

enhanced customer and business‐focused

management process and quality techniques.

Today, whatever our customers’

safety and security requirement,

Peregrine has a suite of services to

meet their needs. From a range

from standard services such as static

and mobile guarding to specialist

services such as event security,

executive protection, emergency

response planning, canine squads

and background investigations, we

are able to tailor our solutions to

meet our customer’s unique

requirements

Figure 13: Peregrine – Tailored solutions to meet customers’ needs

Figure 12: 'SecurCounsel ' ‐ Peregrine's research provides advice to customers on topical subjects

16 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

TENON PROJECT SERVICES – EXPANDING OUR PRODUCTS

Hemant Verma – Head Tenon Project Services

The physical security systems market in India is expected to

grow to at least $1.3 B by 2011, growing at a Compound

Annual Growth Rate (‘CAGR’) of 30% against an average 10%

growth rate in developed markets. IT/ITES companies, who

spend 30% on their security budgets, are currently the

biggest spenders on the installation of security devices,

followed by commercial institutions at 20% and the

hospitality industry at 15%. Retail and aviation sectors are

also expected to continue to be major contributors to

growth. PPP projects, such as airports and metro railways

are also expected to contribute to the growth of this

market3.

Against this backdrop, we have continued to develop Tenon

Project Services, our projects business line for the

installation and integration of security and safety systems.

Tenon Project Services offers consulting, design engineering, procurement, implementation and

maintenance services for a diverse range of the latest, state of the art safety and security systems including:

Intelligent and addressable fire detection and alarm

systems

Biometric/smart card/proximity technology based

access control systems

Analogue and IP technology based CCTV Systems

Analogue and digital technology based public address

and sound reinforcement systems

Water and gas based fire‐fighting systems

Equipment and building Integration systems.

3 Bostonanalytics report on Indian Security Systems Market dated December 2008.

17 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

During this financial year, Tenon Project Services,

a divison of Tenon has enhanced its customer

base by approximately 20%. Tenon Project

Services has also significantly increased its service

and product offering and implemented several

initiatives including the introduction of product‐

specific experts to help customers to assess their

needs and guide them by designing and

implementing customized and value added

solutions.

We are focused on continuously upgrading our

services by keeping abreast of the latest

technological advancements in the field of safety

and security equipments. Our team members’

skills are also regularly updated through internal

training sessions, on the job training modules,

and sessions and seminars conducted by our

strategic partners.

We have created strategic alliances with some of the

World’s most respected, established top of the line

equipment brands. Our key strategic partners include

Honeywell, Bosch, Rafiki, Pelco, Computar, Auric, HID,

Bioscript, Apollo, Kirloskar and Ingersoll Rand amongst

others.

The Directors believe that Tenon Project Services will become a significant contributor to the overall

revenues of the Group over the next two to three years.

Figure 14: Intelligent and addressable fire detection

and alarm systems

Figure 16: Home automation systems

18 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

Financial Review S. Krishnaswamy – Chief Financial Officer

The financial year 2008‐20094 was both a successful

and challenging period for the team. Mortice

engaged in various transactions during the year as a

part of it expansion plans, the most significant of

which was listing the Company on the Alternate

Investment Market of the London Stock Exchange.

We also significantly expanded both our customer

base and our geographic spread in India.

Significant investment has been made in the

development of our FM business and the Group

supporting management structure. This investment

is reflected in our results but, we are highly

confident, will yield significant returns over the

coming years.

Income statement

The Group revenue grew by 15.3 % Y‐O‐Y on an annualized basis after adjusting for extraordinary income in

the last year. The increase in both revenue and costs are due to an increase in the level of operations over

those in 2008.

Abridged Group consolidated Income statement for the year ended (in US$ M)

31 March 2009 31 March 2008 **

Revenue 23.46 4.04Cost of Sales -19.18 -2.71Operating expenses -6.95 -0.73EBITDA -2.67 0.60Depreciation & Finance costs -0.57 -0.08Profit/ (loss) before tax -3.24 0.52Tax 0.31 0.11Profit/ (loss) after tax -2.93 0.63Loss per share basic & diluted -0.06 0.07

** two months results.

4 Financial Year: 1 April 2008 to 31 March 2009.

19 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

The Group reported a US$ 2.9 m loss for the year. This included loss from certain non–recurring expenses

including IPO listing expenses of US$ 1.43 m and the loss incurred through closing down the general

contracting business little over US$ 0.1 m. The remaining loss was incurred through the investment in the

set‐up of the FM business, the establishment of the Group management structure, pre‐acquisition activity

and write offs/provisioning from the existing guarding business. It is important to note that for comparative

purposes the functional currency (Indian rupee) depreciation against the United States dollars also

contributes to about 12.5 % deflation in the reported results. Basic earnings per share reported a negative

US$ 0.06 per share, attributable to the loss for the year.

Balance sheet (in US$ M)

Abridged consolidated balance sheet position

Group Company

2009 2008 2009 2008

Tangible Assets 0.68 0.61 - -Interest in Subsidiaries - - 6.85 0.39Other non-current assets 0.82 0.62 - -Current assets 9.57 4.93 1.30 0.56Total assets 11.07 6.16 8.15 0.95Current liabilities 4.53 4.71 0.39 0.57Non-current liabilities 0.35 0.43 - -Net assets 6.19 1.02 7.76 0.38

The Group balance sheet strengthened with the infusion of fresh shareholder’s funds of US$ 9.15 m.

Correspondingly, the net assets of the Group increased to US$ 6.19 m (31 Mar 2008: US$ 1.02 m). Long

term borrowings and lease obligations were reduced and stood at US$ 0.23 m (31 Mar 2008: US$ 0.34 m).

The current assets ratio improved to 2.11 (31 Mar 2008: 1.05) showing marked improvement in the

performance in the management of this area. The ratio of net assets to total assets improved (31 Mar

2008: 0.17) to 0.56 in 2009. Reduction in Tangible assets is represented partly by realization of security

deposits and partly by movement into current assets as per required disclosures. Other non‐current assets

represent a deferred tax asset created in anticipation of the growth prospects of the business over the

coming years for adjustment against future Tenon business profits.

20 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

Equity

During the year, Mortice issued 7,700,000 ordinary shares to the public through IPO as a part of its initial

fund raising (Note 18 to the consolidated financial statements). The Company raised US$ 9.15 m, net of

issue costs. Total equity attributable to equity shareholders of the Company was US$ 7.77m (31 Mar 2008:

US$ 0.38 m).

Cash Flow (in US$ M)

Abridged Group cash flow (in US$ M) for the year ended

31 March 2009 31 March 2008

Net cash absorbed by operating activities

-5.47 -0.23Net cash (absorbed by)/generated from investing activities -0.34 0.06Net cash generated from financing activities 8.65 0.37Net increase in cash and cash equivalents 2.83 0.20Cash and cash equivalents at beginning of year 0.19 -Unrealised exchange differences -1.00 -0.01Cash and cash equivalents at end of year 2.01 0.19

Cash generation during the year has been negative as a result of the significant investments in setting up

the FM business with the deficit being made up from the freshly raised equity funds. Net cash absorbed by

operating activities (before taxation and interest) was –US$ 4.46 m (2008‐09: ‐US$ 0.17 m). During the year,

working capital utilized increased by US$ 1.9 m largely attributable to organic growth and the impact of the

recession year on speed of collections. Long term borrowings paid off amounted to US$ 0.19 m.

Post balance sheet events

The details of the Group’s material post balance sheet events are provided in note 36 to the consolidated

financial statements. The Group’s operating subsidiary Tenon acquired a 100% equity interest in Rotopower

Projects on 30 June 2009 for a cash consideration of INR 100 million (US$ 1.9m). As a direct result of this

transaction, the Group’s interest in the FM business has substantially increased and indirectly the Group’s

market presence has also increased in the FM segment.

Comparatives

The financial statements presented here for the year ended 31 March 2009 and 31 March 2008 are not

comparable as 2008‐09 represents 12 months of full operation and 2007‐08 covers the financial period of 9

January 2008 to 31 March 2008. The figures have been reclassified where necessary to be compatible with

current year’s financial statements.

21 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

General Information

Directors

Manjit Rajain – Executive Chairman

Andrew Michael Barker – Chief Executive Officer

Dr. Keith Hellawell QPM – Non‐executive Director

Arun Duggal – Non‐executive Director

Company Secretaries

Chia Luang Chew Hazel

Lim Keng San Shirley

KCS Corporate Services Pte Ltd

36 Robinson Road, #17‐01 City House

Singapore 068877

Registered Office

36 Robinson Road,

#17‐01 City House

Singapore 068877

Independent Auditors

Shanker Iyer & Co.

3 Phillip Street

#18‐00 Commerce Point

Singapore 048693

Nominated Adviser

Grant Thornton Corporate Finance

30 Finsbury Square

London EC2P 2YU

United Kingdom

22 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

AIM Broker

Jermyn Capital Partners Plc

Redwolf House, Ground Floor

5‐10 Bolton Street, Mayfair

London W1J 8BA

United Kingdom

Registrar

Computershare Investor Services (Channel Islands) Ltd

PO Box 83, Ordnance House

31 Pier Road, St. Helier

Jersey JE4 8PW

Channel Islands

Depositary

Computershare Investor Services PLC

PO Box 82, The Pavilions

Bridgwater Road, Bristol BS13 8AE

United Kingdom

ISIN Number : SG9999005326

SEDOL Number : B2NHWN8

AIM Symbol : MORT

Website : www.morticeGroup.com

Principal Banker

Standard Chartered Bank PLC

Jeewan Deep Building

10 Sansad Marg

New Delhi 110001

India

23 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

Board of Directors

Executive Directors

Manjit Rajain, aged 46, Executive Chairman

Major Manjit Rajain founded the Peregrine Group and through Mancom is the major shareholder of Mortice.

Major Rajain was commissioned in the Indian Army’s 11th Armoured Regiment in 1984. During his 7 years of

service, Major Rajain saw active service in Rajasthan and Jammu & Kashmir. Following his release from the

army, Major Rajain served in the police force where he attained the position of assistant commissioner stationed

in Jammu and Kashmir Using the security experience gained from his career in the military and the police force,

Major Rajain demonstrated his entrepreneurial capability to establish Peregrine which he has developed over the

last 13 years to become one of the top 4 security service providers across the sub continent of India. Following

the successful establishment of a transport management business to support the fast developing IT/ITeS sector,

Major Rajain seeded further facilities related companies to provide the foundation for Mortice with the vision of

creating the platform for Mortice.

On 14 October 2008, Major Rajain was recognized as ‘Entrepreneur of the Year’ at an awards function as part of

CAPSI’s 3rd National Conference, held in Bangalore in recognition of his proven skills as a business leader and

as a committed member of the security industry. Major Rajain is also an active member of Rotary

International.

Andrew Barker, aged 54, Executive Director

Mr. Barker has experience of delivering property and facilities management services across 27 countries whilst

working for and establishing many of the industry’s FM arms around the world. He has spent the last twelve

years working in Asia, six of which have been in India, during which time he has established three successful

property and facilities management companies. He was instrumental in developing MacLellan, the first FM

Company in India in 1998. Working in partnership with Ford India he led the MacLellan India team to win the UK

Premises and Facilities Management Partnership Award in 1999. He has been referred to within the FM industry

as ‘The Father of FM in India’ Mr. Barker was a founder member of the industry in the UK, where he worked

with Johnson Controls and MacLellan International. He is a Fellow of the British Institute of Facilities

Management and is an active Member of CoreNet Global as Vice Chair Learning on the Asia Regional Council. He

was formerly a member of the UK Competing for Quality and PFI Advisory Committees. He has a MSc in

facilities management and an MBA from Cranfield University. He has held board positions as sales & marketing

Director for MacLellan International in the UK and as operations Director for Serco Middle East in Dubai. He has

also held responsibility as vice president operations and general manager for MacLellan India and general

manager for Serco Gulf a joint venture with Dubai World’s Istithmar in Dubai. His other appointments have

included regional Director for asset services for Cushman & Wakefield Asia Pacific, national Director for

corporate property services for Jones Lang LaSalle for regional accounts in Asia Pacific and regional head of

property and facilities management services for ABN AMRO in Asia Pacific and the Middle East.

24 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

Non‐Executive Directors Arun Duggal, aged 63, Non-executive Director

Mr. Arun Duggal is a Senior Advisor to TPG Capital, a major Private Equity firm headquartered in San Francisco.

He is an experienced international Banker and has advised companies and financial institutions on Financial

Strategy, M&A and Capital Raising. He is Chairman of Board of Directors of Shriram Transport Finance

Company, Shriram Properties Pvt. Ltd, Shriram City Union Finance Ltd., and Shriram EPC Limited. He is the Vice

Chairman of International Asset Reconstruction Company.

He is on the Board of Directors of Jubilant Energy Ltd., Patni Computers (Chairman, Audit Committee), Fidelity

Fund Management, Manipal Acunova Limited, Zuari Industries, Info Edge (India), Dish TV India Ltd., Mundra

Port & SEZ Ltd., and IMA (formerly Economist Intelligence Unit, India), Hertz (India) and Mortice Limited

(Singapore). He is a member of the Investment Committee of Axis Private Equity.

He is Vice Chairman of Indian Venture Capital Association. He is a Board Member and erstwhile Chairman of the

American Chamber of Commerce, India He was on the Board of Governors of the National Institute of Bank

Management. Mr. Duggal is involved in several initiatives in social sector.

He is a founder Director of Bellwether Microfinance Fund which provides equity capital to promising Micro

Finance organizations and helps them in capacity building. He is a Trustee of Centre for Civil Society, New Delhi,

which focuses on improving the quality and access of education to students especially for the poor. He is Senior

Advisor (Asia Pacific) to Transparency International Berlin. Mr. Duggal had a 26 years career with Bank of

America, mostly in the U.S., Hong Kong and Japan. His last assignment was as Chief Executive of Bank of

America in India from 1998 to 2001.

He spent ten years (1981-1990) with the New York Corporate Office of Bank of America handling multinational

relationships. From 1991-’94 as Chief Executive of BA Asia Limited, Hong Kong he looked after Investment

Banking activities for the Bank in Asia. In 1995, he moved to Tokyo as the Regional Executive, managing Bank

of America’s business in Japan, Australia and Korea. From 2001 to 2003 he was Chief Financial Officer of HCL

Technologies, India.

A Mechanical Engineer from the prestigious Indian Institute of Technology, Delhi, Mr. Duggal holds an MBA from

the Indian Institute of Management, Ahmedabad. He teaches a course on Venture Capital & Private Equity at

the Indian Institute of Management, Ahmedabad as a visiting Professor.

25 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

Dr. Keith Hellawell QPM, aged 65, Non-executive Director

Dr. Keith Hellawell QPM is a highly renowned expert in the fields of security and facilities management and

brings significant professional experience and academic credentials with him. As a highly decorated police

officer, Dr. Hellawell has served as Chief Constable for the West Yorkshire Police and Cleveland Police; and has

advised senior government bodies and officials, including the Home Secretary and Prime Minister of the UK, the

European Union, former Soviet Bloc countries, Los Angeles Police Department, Government of Cyprus and the

FBI on diverse issues relating to combating crime.

In his professional capacity, Dr. Hellawell has served as a Director of Homework, a UK-based corporation

involved in manufacturing and installing security alarms. He has, and continues, to lend his professional advice

to several leading corporations as a Non-Executive Director – significantly, in the context of Mortice plc, to

Dalkia plc, a leading Facilities Management services provider.

Dr. Hellawell holds an LLB from London University and gained his MSc from Cranfield University. He has also

been awarded Honorary Doctorates from the Leeds/Bradford and Huddersfield Universities.

He has won several professional awards including “Communicator of the Year” (voted by PR industry), Top 50

most powerful men in Britain in a national newspaper survey and “Businessman of the Year” for the Yorkshire

and Humber Region.

Figure 17: Members of the Board of Mortice on the occasion of listing the Company on AIM – 15 May 2008

From the left: Dr. Keith Hellawell, Non‐Executive Director; Major Manjit Rajain, Chairman; Mr. Andrew Barker, CEO

26 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

Financial Contents

27 Directors’ report

32 Corporate governance report

35 Statement by Directors

36 Independent auditors’ report

38 Balance Sheets

39 Income Statement

40 Changes in Equity

42 Consolidated Cash Flow

45 Notes to the Financial Statements

27 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

Directors’ Report

For the year ended 31 March 2009

The Directors present their report to the members together with the audited financial statements of the Company and of the Group for the financial year ended 31 March 2009.

Principal activities of the business

Mortice is a diversified services Group that through its subsidiaries provides and delivers managed services

relating to guarding, facilities and property management and the execution of safety and security systems

project works.

A more detailed overview of the Group’s business during the year and indication of further development

may be found in the Chairman’s statement and CEO’s statement.

Going Concern

The Directors are confident that sufficient funding and adequate resources are available to enable the

Group to continue to meet its present obligations as they fall due for at least the next twelve months.

Accordingly, the Directors continue to adopt the going concern basis in preparing the financial statements.

Result and Dividend

The summary of results of the Group for the year ended 31 March 2009 are set out on pages 18 to 20 and

further details are presented in the appended financial statements. The Directors do not recommend

payment of a dividend for the year.

Directors

The names of individuals who served as Directors of the Company from the beginning of the year are as

follows:

Manjit Rajain Andrew Michael Barker Dr. Keith Hellawell QPM Arun Duggal

Brief biographies of each of the Directors are set out on pages 23 to 25.

Arrangements to enable Directors to acquire shares and debentures

Neither at the end of nor at any time during the financial year was the Company a party to any arrangement whose object is to enable the Directors of the Company to acquire benefits by means of the acquisition of shares in, or debentures of, the Company or any other body corporate. Directors’ contractual benefits

28 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

Since the end of the previous financial period, no Director has received or become entitled to receive a benefit by reason of a contract made by the Company or a related corporation with the Director or with a firm of which the Director is a member, or with a Company in which the Director has a substantial financial interest, except as disclosed in the financial statements.

Directors’ interests in shares and debentures

According to the register of Directors’ shareholdings kept by the Company for the purpose of Section 164 of

the Singapore Companies Act, Cap 50, none of the Directors holding office at the end of the financial period

had interest in shares of the Company and its related corporation except as follows:

Holdings registered in the

name of Director

Holdings in which a Director is deemed to have an interest

As at

1.4.2008

As at

31.3.2009

As at

1.4.2008

As at

31.3.2009

Mortice Limited

Ordinary shares

Manjit Rajain 1 1

‐ ‐

Mancom Holdings

Limited

Ordinary shares

Manjit Rajain

‐

‐

40,000,000

40,000,000

Tenon Property

Services Private Limited

Ordinary shares

Manjit Rajain

5,000

5,000

‐

‐

Directors’ remuneration

For the year ended 31 March 2009, the annual salary of each of the Directors was as follows: Director Annual salaries Manjit Rajain US$ 386,912 Andrew Barker US$ 305,718 Dr. Keith Hellawell QPM US$ 22,341 Arun Duggal US$ 22,363

29 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

Directors' Indemnities

The Company maintains Directors' and officers' liability insurance which gives adequate cover for legal

action brought against its Directors.

Related Party transactions

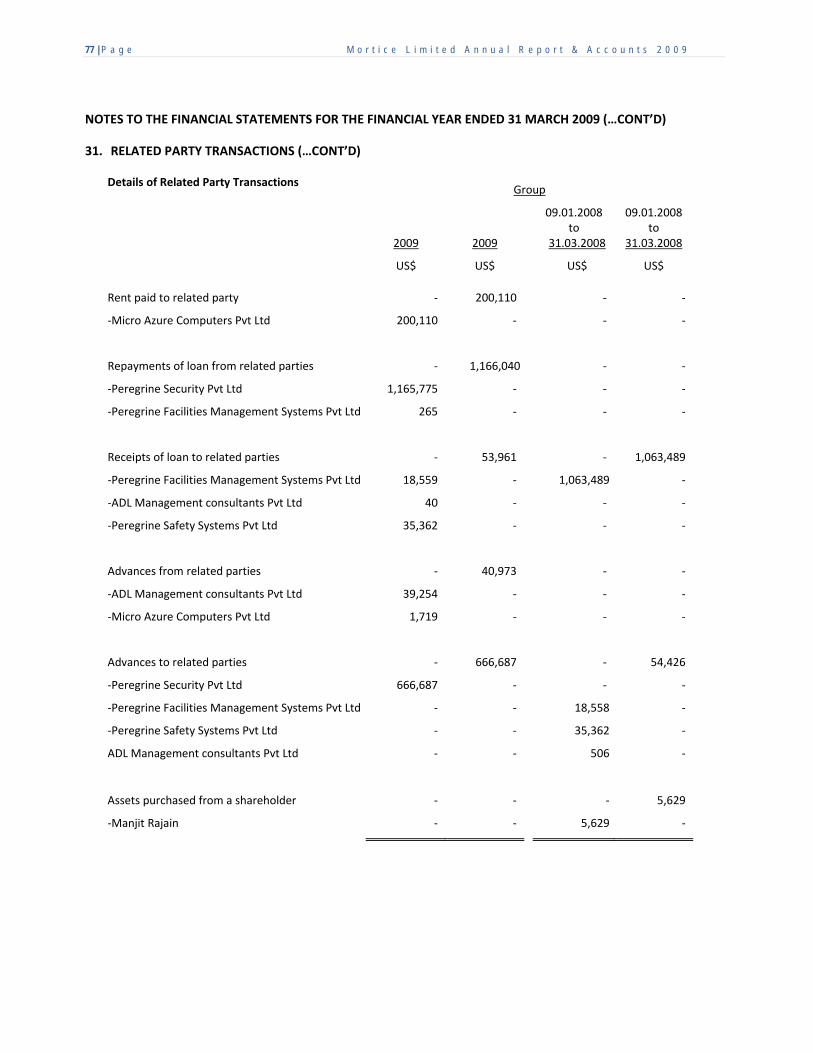

Details of related party transactions are contained in note 31 to the consolidated financial statements.

Credit payment policy

The Company has no formal code or standard which deals specifically with the payment of suppliers. It is

the Company's policy to settle the terms of payment with suppliers when agreeing the terms of the

transaction so as to ensure that suppliers and the Company are aware of those terms and abide by them;

however, the Company’s policy on the payment of all creditors is to ensure that the terms of payment, as

specified and agreed with the supplier, are not exceeded unreasonably. Our standard term of credit for

trade purchases is 30 days.

Principal risks and uncertainties

The activities of the Group are subject to a number of risks. If any of these risks were to materialise the

Group’s business, financial condition and results of future operations could be materially adversely affected

by, among other things, delays, increased costs and/or reduced revenues. The principal risks are detailed in

the Group’s admission document of 15 May 2008 and include risks relating to the proposed business model,

competitive risk, funding risk, dependence on key executives, political, regulatory and economic

uncertainty, and general risks such as general economic conditions.

Share Capital

On 15 May 2008, Mortice announced the successful placing of 7.7 million ordinary shares with institutional

investors, raising US$ 9.73 m before fees and expenses. Additional detail is provided in note 18 to the

consolidated financial statements.

Share Options There were no share options granted during the financial year to subscribe for unissued shares of the Company or its subsidiary companies. No shares have been issued during the financial year by virtue of the exercise of options to take up unissued shares of the Company or its subsidiary companies. There were no unissued shares of the Company or its subsidiary companies under option at the end of the financial year. The Board of Directors of the Company resolved on 14 July 2009 to cancel the share options scheme with retrospective effect.

30 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

Corporate Governance

A report on Corporate Governance is set out on pages 32 to 34.

Environmental Responsibility

The Company recognises that the nature of the Group's service delivery activities require it to have regard

to the potential impact that it and its subsidiary companies may have on the environment. The Company

has adopted an Environmental Policy for the Group and, wherever possible, the Company ensures that all

related companies are encouraged to comply with the local regulatory requirements with regard to the

environment.

Charitable and political donations

No charitable or political donations were made during the year.

Post balance sheet events

On 22 June 2009, Mortice announced the acquisition of Rotopower further details of which are set out in

note 36 to the consolidated financial statements.

Annual General Meeting

The Company will distribute a notice of Annual General Meeting to be held on 11 September 2009 to lay the

annual accounts before the shareholders and to deal with any other business for the consideration of the

shareholders. The notice of Annual General Meeting will be distributed with this Annual Report.

Disclosure of information to auditors

So far as each Director at the date of approval of this report is aware, there is no relevant audit information

of which the Company’s auditors are unaware and each Director has taken all steps that he ought to have

taken to make himself aware of any relevant audit information and to establish that the auditors are aware

of that information.

Independent auditors

The independent auditors, Messrs Shanker Iyer & Co., Certified Public Accountants, Singapore, have

expressed their willingness to accept re‐appointment and a resolution to re‐appoint them will be proposed

at the forthcoming Annual General Meeting.

31 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

Recommendation

The Board considers that the resolutions to be proposed at the Annual General Meeting are in the best

interests of the Company and it is their unanimous recommendation that shareholders support them.

On behalf of the Board Manjit Rajain Director Arun Duggal Director 25 August 2009

32 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

Corporate Governance Report

INTRODUCTION

The Board of Mortice Limited is committed to and is responsible for achieving high standards of corporate

governance, integrity and business ethics for all of its activities. Whilst the Group is not required under the

AIM Rules for Companies to comply with the Combined Code on Corporate Governance 2006 (the

Combined Code), the Board recognises the value of the Combined Code and has chosen to provide selected

disclosures which it believes are necessary or valuable to readers.

DIRECTORS

The Group Board has committed to meet not less than six times throughout the year and consists of an

Executive Chairman, one Executive Director and two Non‐Executive Directors. Details of the Board are set

out on pages 23‐25. The Board considers that both our Non‐Executive Directors are independent of the

Executive Directors and are free from any business or other relationships that might materially interfere

with their exercise of independent judgment. The Chairman and Directors bring experience at a senior level

of business operations and strategy and an expanse of knowledge and expertise gained from other areas of

business and public life. The Board has a schedule of matters reserved for its approval which includes Group

strategy, acquisitions and disposals of any subsidiary undertaking, review of any significant risks facing the

Group, appointment of key advisers, the consideration of major capital projects and significant financing

matters. The Board also reviews the strategic direction of each of the Group’s subsidiary operating divisions,

their annual budgets and progress towards the achievement of those budgets.

The Board has delegated authority to Audit and Remuneration Committees whose duties are summarised

below. Each Committee is chaired by one of our Non‐Executive Directors.

AUDIT COMMITTEE

The Audit Committee is chaired by Mr. Arun Duggal and its other member is our other Non‐Executive

Director, Dr. Keith Hellawell QMP.

The Committee met twice during the past financial year on 23 September 2008 and 23 December 2008. The

Committee operates within agreed terms of reference which include reviewing the effectiveness of financial

reporting and internal control procedures, monitoring the integrity of the financial statements of the Group

and any significant financial reporting judgments contained therein and reviewing the fees, independence

and objectivity of the external auditors.

33 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

The Group’s external auditors have unrestricted access to the Audit Committee and attended all Audit

Committee meetings held during the year. The Audit Committee has discussed matters with the external

auditors outside those meetings. The Executive Directors attend Audit Committee meetings through

invitation.

REMUNERATION COMMITTEE

The Remuneration Committee is chaired by Dr. Keith Hellawell QMP and its other member is our other Non‐

Executive Director, Mr. Arun Duggal. The Directors’ Remuneration is set out in the Directors’ Report at page

28.

MAIN BOARD MEETINGS AND ATTENDANCE

Directors are encouraged to attend all Board meetings and meetings of Committees of which they are

members. The Chairman and the CFO plan the programme for the meetings including attendance by senior

executives from within the Group. Detailed Board packs including financial results, operational issues and

notes on other matters reserved for the Board. The Company continues to maintain Directors’ and Officers’

liability insurance.

INTERNAL CONTROL

The Board has overall responsibility for the Group’s system of internal financial and operational controls

and the ongoing review of their effectiveness. These controls are design to safeguard the Group’s assets

and the investment of shareholders; however, any system of internal control can only manage rather than

eliminate risks and consequently such controls do not provide absolute assurance against misstatement or

loss. The main features of the Group’s internal systems include:

Allocation of responsibilities

The Board has considered and set terms of reference for its Chief Executive which includes the day

to day responsibility for the management and operations of the business. In addition, the Group has

clearly defined delegation of authority and authorization limits to Executive management. This is

clearly communicated to the employees of the business by the Executive Directors.

34 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

Risk identification

The Board is responsible for identifying the main business risks faced by the Group and for

determining the appropriate actions necessary to manage those risks.

Financial reporting and control

The Group has a comprehensive system for reporting financial results to the Board. Each subsidiary

prepares monthly management information which includes comparison against budget, forecast

and prior year. These results are considered by the management teams of each operating division.

Both operating and financial reports are prepared for the Group Board and actions arising from the

review of these reports are attributed as appropriate.

Investment appraisal

Capital expenditure is regulated by authorization limits. The acquisition of any business is subject to

appropriate due diligence being undertaken and conditional upon receiving Board approval.

Disaster recovery

The Group has established procedures over the security of data held on IT systems and has put in

place disaster recovery arrangements.

Internal audit

The Group does not currently have an internal audit function. However, the Board, and in particular

the Audit Committee, will continue to review the need to put in place and internal audit function

taking into account the size and nature of the Group.

INVESTOR RELATIONS

The Board places significant importance on maintaining good communication with shareholders. The

Chairman and Chief Executive Officer are available to meet with institutional shareholders and analysts

after the announcement of both the interim and final results and will undertake such meetings, whenever

reasonably requested by shareholders and analysts at other points during the course of the year. The

Annual Report is sent to all shareholders and all shareholders are invited to attend the Company’s Annual

General Meeting. The Group’s investor relations section on the corporate website contains information on

current activities (www.morticegroup.com).

35 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

STATEMENT BY DIRECTORS

In the opinion of the directors of MORTICE LIMITED,

(a) the accompanying balance sheets, income statements, statements of changes in equity and consolidated cash flow statement together with the notes thereto are drawn up so as to give a true and fair view of the state of affairs of the Company and of the Group as at 31 March 2009 and of the results, changes in equity of the Company and of the Group and cash flows of the Group for the financial year ended on that date; and

(b) at the date of this statement there are reasonable grounds to believe that the Company will be able to pay its debts as and when they fall due.

The board of directors authorised these financial statements for issue on 25 August 2009.

On behalf of the Board

Manjit Rajain

Director

Arun Duggal

Director

25 August 2009

36 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

INDEPENDENT AUDITORS’ REPORT TO THE MEMBERS OF

MORTICE LIMITED

(Incorporated in Singapore)

We have audited the accompanying financial statements of MORTICE LIMITED (the company) and its

subsidiaries (the group) as set out on pages 38 to 82, which comprise the balance sheets of the group and of

the company as at 31 March 2009, the income statements, statements of changes in equity of the group and

of the company and cash flow statement of the group for the year then ended, and a summary of significant

accounting policies and other explanatory notes.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in

accordance with the provisions of the Singapore Companies Act, Cap. 50 (the “Act”) and International

Financial Reporting Standards. This responsibility includes:

(a) devising and maintaining a system of internal accounting controls sufficient to provide a reasonable assurance that assets are safeguarded against loss from unauthorised use or disposition; and transactions are properly authorised and that they are recorded as necessary to permit the preparation of true and fair income statements and balance sheets and to maintain accountability of assets; (b) selecting and applying appropriate accounting policies; and (c) making accounting estimates that are reasonable in the circumstances. Auditors’ Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit.

We conducted our audit in accordance with International Standards on Auditing. Those standards require

that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance

whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain evidence about the amounts and disclosures in the

financial statements. The procedures selected depend on the auditors’ judgement, including the

assessment of the risks of material misstatement of the financial statements, whether due to fraud or error.

In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation

and fair presentation of the financial statements in order to design audit procedures that are appropriate in

the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s

internal control. An audit also includes evaluating the appropriateness of accounting policies used and the

reasonableness of accounting estimates made by management, as well as evaluating the overall

presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our

audit opinion.

37 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

INDEPENDENT AUDITORS’ REPORT TO THE MEMBERS OF

MORTICE LIMITED (…CONT’D)

(Incorporated in Singapore)

Opinion

In our opinion,

(a) the consolidated financial statements of the Group and the financial statements of the Company are properly drawn up in accordance with the provisions of the Singapore Companies Act, Cap. 50 (the “Act”) and International Financial Reporting Standards so as to give a true and fair view of the state of affairs of the Group and of the Company as at 31 March 2009 and of the results and changes in equity of the Group and of the Company and cash flows of the Group for the financial year then ended on that date; and

(b) the accounting and other records required by the Act to be kept by the Company have been properly

kept in accordance with the provisions of the Act.

SHANKER IYER & CO PUBLIC ACCOUNTANTS AND CERTIFIED PUBLIC ACCOUNTANTS

Singapore

25 August 2009

38 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

BALANCE SHEETS AS AT 31 MARCH 2009

Group

Company

Note 2009 2008 2009 2008

US$ US$ US$ US$

NON‐CURRENT ASSETS

Plant and equipment 4 677,163 609,147 ‐ ‐

Investment in subsidiary 5 ‐ ‐ 6,849,675 394,675

Deferred tax asset 6 618,853 165,870 ‐ ‐

Fixed deposits 7 111,933 14,589 ‐ ‐

Security deposits 8 88,897 439,329 ‐ ‐

1,496,846 1,228,935 6,849,675 394,675

CURRENT ASSETS

Cash and cash equivalents 9 3,253,140 390,420 1,294,212 5,028

Trade receivables 10 4,630,997 3,690,329 ‐ ‐

Other receivables 11 1,617,526 829,989 8,532 551,215

Inventories, at cost 12 67,262 20,481 ‐ ‐

9,568,925 4,931,219 1,302,744 556,243

CURRENT LIABILITIES

Trade payables 13 399,627 1,390,460 ‐ ‐

Other payables 14 2,733,403 2,709,298 386,965 568,542

Bank overdraft 9 1,241,451 200,389 ‐ ‐

Finance lease 15 60,760 43,029 ‐ ‐

Borrowings 16 90,218 369,052 ‐ ‐

4,525,459 4,712,228 386,965 568,542

NET CURRENT ASSETS/(LIABILITIES) 5,043,466 218,991 915,779 (12,299)

NON‐CURRENT LIABILITIES

Finance lease 15 (78,812) (97,271) ‐ ‐

Borrowings 16 (151,820) (237,883) ‐ ‐

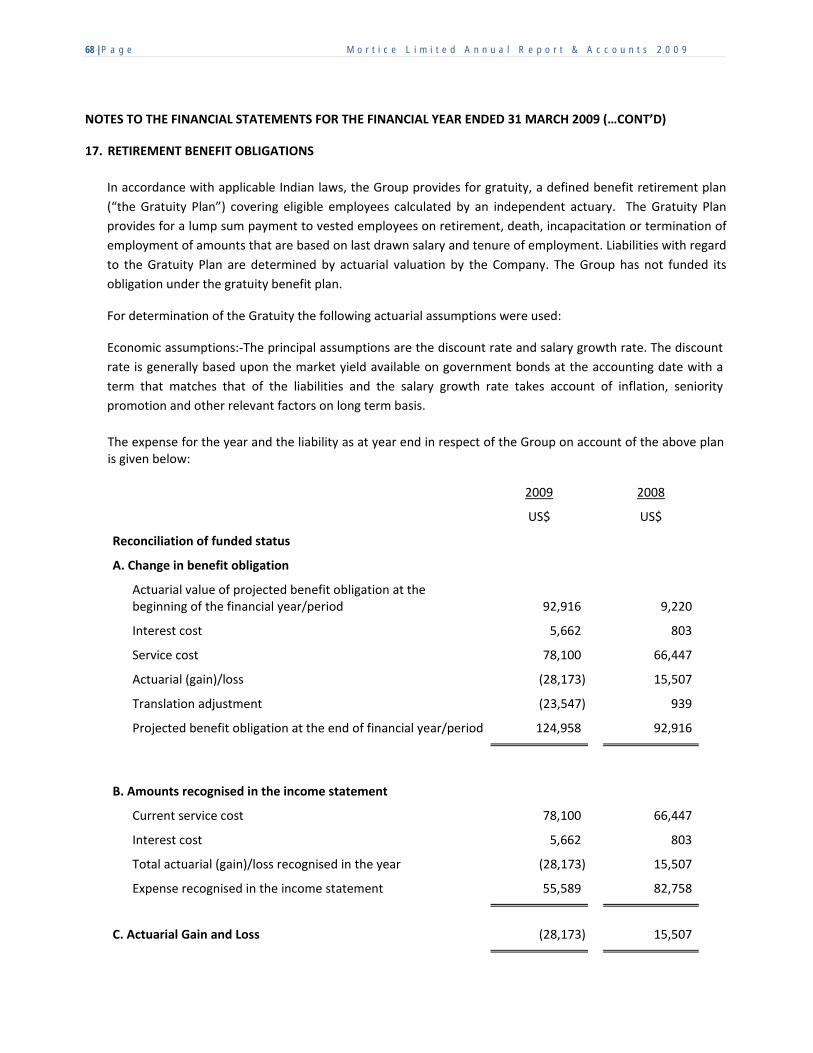

Retirement benefit obligations 17 (124,958) (92,916) ‐ ‐

NET ASSETS 6,184,722 1,019,856 7,765,454 382,376

SHAREHOLDERS’ EQUITY

Share capital 18 9,555,312 400,001 9,555,312 400,001

Reserves 19 (3,370,590) 617,361 (1,789,858) (17,625)

6,184,722 1,017,362 7,765,454 382,376

Minority interest 20 ‐ 2,494 ‐ ‐

TOTAL EQUITY 6,184,722 1,019,856 7,765,454 382,376

The annexed notes form an integral part of and should be read in conjunction with these financial statements.

39 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

INCOME STATEMENTS FOR THE YEAR ENDED 31 MARCH 2009

Group Company

Note 2009 09.01.2008

To

31.03.2008

2009 09.01.2008

To

31.03.2008

US$ US$ US$ US$

REVENUE

Services income 23,156,372 3,390,490 ‐ ‐

Other income 21 300,747 1,569 166,454 ‐

Negative goodwill written back 22 ‐ 651,478 ‐ ‐

Total revenue 23,457,119 4,043,537 166,454 ‐

COSTS AND EXPENSES

Services consumed 23 19,184,679 2,713,594 ‐ ‐

Depreciation of plant and equipment 4 161,653 20,401 ‐ ‐

Staff and related costs 2,860,657 471,020 306,762 ‐

Operating expenses 24 2,649,858 259,460 195,672 17,625

Initial Public Offering expenses 1,436,253 ‐ 1,436,253 ‐

Finance costs 25 407,880 60,333 ‐ ‐

Total costs and expenses 26,700,980 3,524,808 1,938,687 17,625

(LOSS)/PROFIT BEFORE TAXATION 26 (3,243,861) 518,729 (1,772,233) (17,625)

TAXATION 27 314,384 113,905 ‐ ‐

(LOSS)/PROFIT FOR THE YEAR/PERIOD (2,929,477) 632,634 (1,772,233) (17,625)

Attributable to:

Equity holders of the Company (2,926,983) 632,642

Minority interest (2,494) (8)

(2,929,477) 632,634

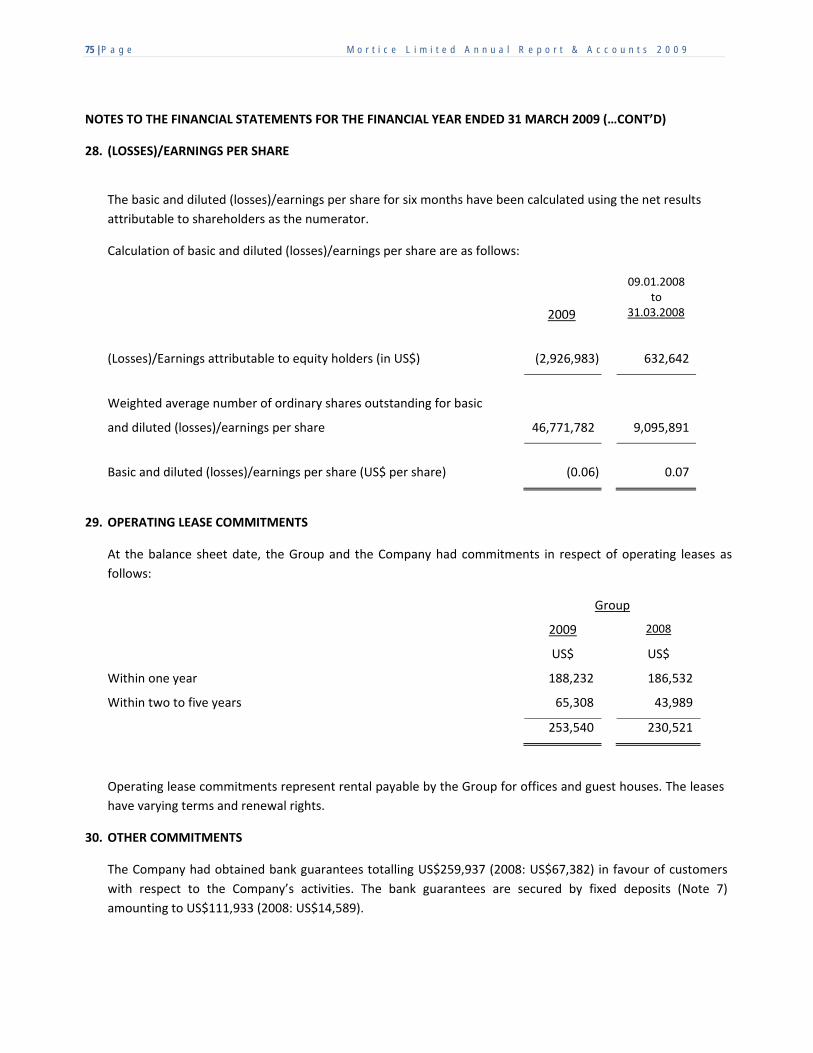

(Losses)/Earnings per share

‐ Basic and diluted 28 (0.06) 0.07

The annexed notes form an integral part of and should be read in conjunction with these financial statements.

40 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

STATEMENTS OF CHANGES IN EQUITY FOR THE YEAR ENDED 31 MARCH 2009

Attributable to equity holders of the group

Share

capital

(Accumulated losses)/Retained

profits

Currency translation reserve

Total Minority interest

Total

US$ US$ US$ US$ US$ US$

Group

2009

Balance as at 1 April 2008 400,001 632,642 (15,281) 1,017,362 2,494 1,019,856

Issuance of ordinary shares (Note 18) 9,730,120 ‐ ‐ 9,730,120 ‐ 9,730,120

Share issue expenses (Note 18) (574,809) ‐ ‐ (574,809) ‐ (574,809)

Loss for the year ‐ (2,926,983) ‐ (2,926,983) (2,494) (2,929,477)

Translation difference on consolidation ‐ ‐ (1,060,968) (1,060,968) ‐ (1,060,968)

Balance as at 31 March 2009 9,555,312 (2,294,341) (1,076,249) 6,184,722 ‐ 6,184,722

2008

Issuance of subscriber’s share 1 ‐ ‐ 1 ‐ 1

Issuance of ordinary shares (Note 18) 400,000 ‐ ‐ 400,000 ‐ 400,000

Acquisition of subsidiaries ‐ ‐ ‐ ‐ 2,502 2,502

Profit for the period ‐ 632,642 ‐ 632,642 (8) 632,634

Translation difference on consolidation ‐ ‐ (15,281) (15,281) ‐ (15,281)

Balance as at 31 March 2008 400,001 632,642 (15,281) 1,017,362 2,494 1,019,856

The annexed notes form an integral part of and should be read in conjunction with these financial statements.

41 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

STATEMENTS OF CHANGES IN EQUITY (…CONT’D) FOR THE YEAR ENDED 31 MARCH 2009

Attributable to equity holders of the group

Share

capital

(Accumulated

losses)/Retained

profits

Currency

translation

reserve

Total

Minority

interest

Total

US$ US$ US$ US$ US$ US$

Company

2009

Balance as at 1 April 2008 400,001 (17,625) ‐ 382,376 ‐ 382,376

Issuance of ordinary shares (Note 18) 9,730,120 ‐ ‐ 9,730,120 ‐ 9,730,120

Share issue expenses (Note 18) (574,809) ‐ ‐ (574,809) ‐ (574,809)

Loss for the year ‐ (1,772,233) ‐ (1,772,233) ‐ (1,772,233)

Balance as at 31 March 2009 9,555,312 (1,789,858) ‐ 7,765,454 ‐ 7,765,454

2008

Issuance of subscriber’s share (Note 18) 1 ‐ ‐ 1 ‐ 1

Issuance of ordinary shares 400,000 ‐ ‐ 400,000 ‐ 400,000

Loss for the period ‐ (17,625) ‐ (17,625) ‐ (17,625)

Balance as at 31 March 2008 400,001 (17,625) ‐ 382,376 ‐ 382,376

The annexed notes form an integral part of and should be read in conjunction with these financial statements

42 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

CONSOLIDATED CASH FLOW STATEMENT FOR THE YEAR ENDED 31 MARCH 2009

2009

09.01.2008to

31.03.2008

Note US$ US$

Cash Flows From Operating Activities

(Loss)/profit before taxation (3,243,861) 518,729

Adjustments for:

Depreciation of plant and equipment 4 161,653 20,401

Negative goodwill written back ‐ (651,478)

Bad debt written off 26 134,684 ‐

Interest expense 25 407,880 60,333

Interest income 21 (94,160) ‐

Provision for doubtful debts 24 199,023 ‐

Cash flows from operations before changes in working capital (2,434,781) (52,015)

Working capital changes, excluding changes relating to cash:

Trade receivables (1,254,696) (212,659)

Other receivables 241,954 87,136

Inventories, at cost (46,781) (20,481)

Trade payables (990,833) 80,885

Other payables 61,005 (67,573)

Retirement benefit obligations (32,042) 14,346

Cash absorbed by operations (4,456,174) (170,361)

Income tax paid (668,180) ‐

Interest paid (408,355) (60,333)

Interest received 66,733 ‐

Net cash absorbed by operating activities (5,465,976) (230,694)

Cash Flows From Investing Activities

Acquisition of plant and equipment 4 (372,169) (98,022)

Net cash outflow on acquisition of subsidiaries ‐ (394,675)

Proceeds from disposal of plant and equipment 27,203 557,562

Net cash (absorbed by)/generated from investing activities (344,966) 64,865

43 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

CONSOLIDATED CASH FLOW STATEMENT (…CONT’D) FOR THE YEAR ENDED 31 MARCH 2009

Cash Flows From Financing Activities

2009

US$

09.01.2008 to

31.03.2008

US$

Issuance of share capital 18 9,730,120 400,001

Payment for share issue expenses 18 (574,809) ‐

Proceeds from finance lease 72,463 140,300

Proceeds from borrowings ‐ 344,108

Advances to related parties (605,082) (62,070)

Repayment of finance lease obligation (36,273) ‐

Repayment of borrowings (192,771) ‐

Withdrawal/(placement) of security deposit 350,432 (439,329)

Placement of pledged fixed deposit (97,344) (14,589)

Net cash generated from financing activities 8,646,736 368,421

Net increase in cash and cash equivalents 2,835,794 202,592

Unrealised exchange difference (1,014,136) (12,561)

Cash and cash equivalents at the beginning of the year/period 190,031 ‐

Cash and cash equivalents at the end of the year/period 9 2,011,689 190,031

44 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

CONSOLIDATED CASH FLOW STATEMENT (…CONT’D) FOR THE YEAR ENDED 31 MARCH 2009 Note: In the previous financial period, the Company acquired a subsidiary Company. The effect of the above acquisition on the cash flows of the Group was as follows:

2008

US$

Summary of the effect of acquisition of a subsidiary

Cash and cash equivalents 557,562

Trade receivables 3,477,670

Other receivables 881,167

Deferred tax asset 2,499

Plant and equipment 539,352

Trade payables (1,309,575)

Retirement benefit obligations (78,570)

Other payables (2,758,686)

Long term borrowings (262,827)

Minority shareholders interest (2,539)

Currency translation adjustment 100

Net assets acquired 1,046,153

Negative goodwill on consolidation (651,478)

Amount paid in consideration of acquisition 394,675

Cash and cash equivalents of acquired entity 557,562

The annexed notes form an integral part of and should be read in conjunction with these financial statements

45 | P a g e M o r t i c e L i m i t e d A n n u a l R e p o r t & A c c o u n t s 2 0 0 9

NOTES TO THE FINANCIAL STATEMENTS

FOR THE FINANCIAL YEAR ENDED 31 MARCH 2009

1. CORPORATE INFORMATION

Mortice Limited (Company Registration No: 200800770W) is a public limited Company, domiciled in

Singapore. The Company’s registered office is at 36 Robinson Road, #17‐01 City House, Singapore

068877.

The Company was listed on Alternate Investment Market (AIM) of London Stock Exchange in United

Kingdom on 15 May 2008, issuing 7,700,000 ordinary shares with proceeds amounting to

US$9,730,120.

The principal activities of the Group are to provide guarding services, facilities management services,

property management, fleet management and sale of safety equipment and their installation. There

have been no significant changes in the nature of these activities during the financial year.

The financial statements of the Group and of the Company as at 31 March 2009 and for the year then

ended were authorised and approved by the Board of Directors for issuance on 25 August 2009.

2. SIGNIFICANT ACCOUNTING POLICIES

a) Basis of preparation

The consolidated financial statements are prepared in accordance with the provision of

Singapore Companies Act, Cap. 50 and International Financial Reporting Standards (“IFRS”).

The consolidated financial statements, which are expressed in United States dollars are prepared