1 in search for the right metric for corporate bond markets in argentina primer seminario...

TRANSCRIPT

1

IN SEARCH FOR THE RIGHT METRIC FOR CORPORATE BOND MARKETS

IN ARGENTINA

Primer Seminario LarrainVial de Renta Fija “Latinoamérica, Renta Fija Local – Una Nueva Clase de

Activos”Santiago, Chile.20 de Abril de 2007

Sergio Pernice, Universidad del CEMA

Roque Fernández and Jorge Streb, co-authors

2

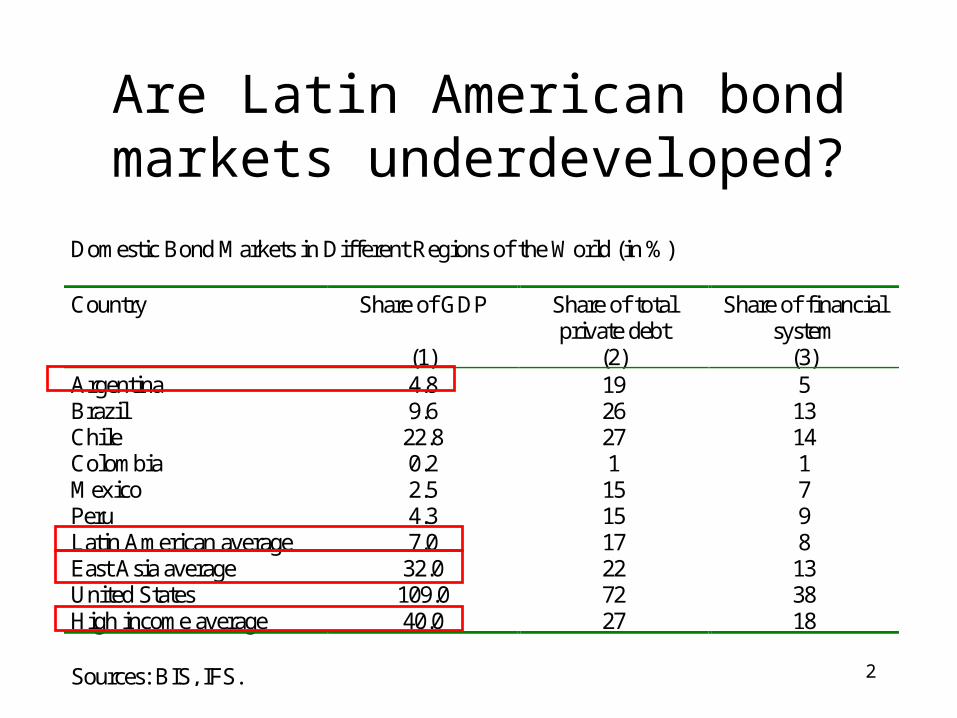

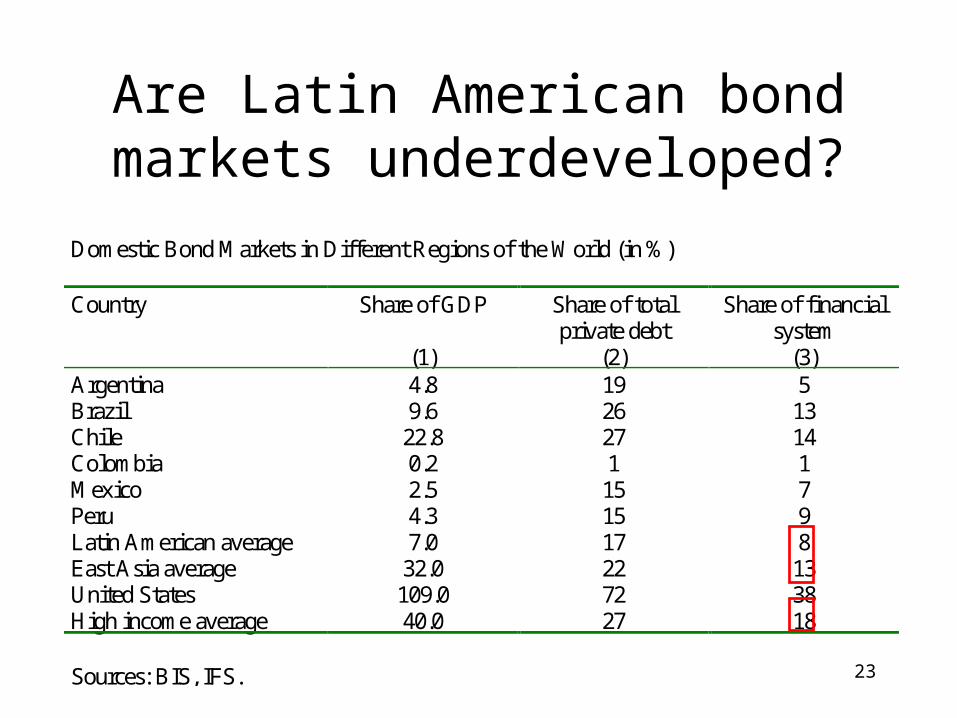

Are Latin American bond markets underdeveloped?

Domestic Bond Markets in Different Regions of the World (in %)

Country Share of GDP

(1)

Share of total private debt

(2)

Share of financial system

(3) Argentina 4.8 19 5 Brazil 9.6 26 13 Chile 22.8 27 14 Colombia 0.2 1 1 Mexico 2.5 15 7 Peru 4.3 15 9 Latin American average 7.0 17 8 East Asia average 32.0 22 13 United States 109.0 72 38 High income average 40.0 27 18 Sources: BIS, IFS.

3

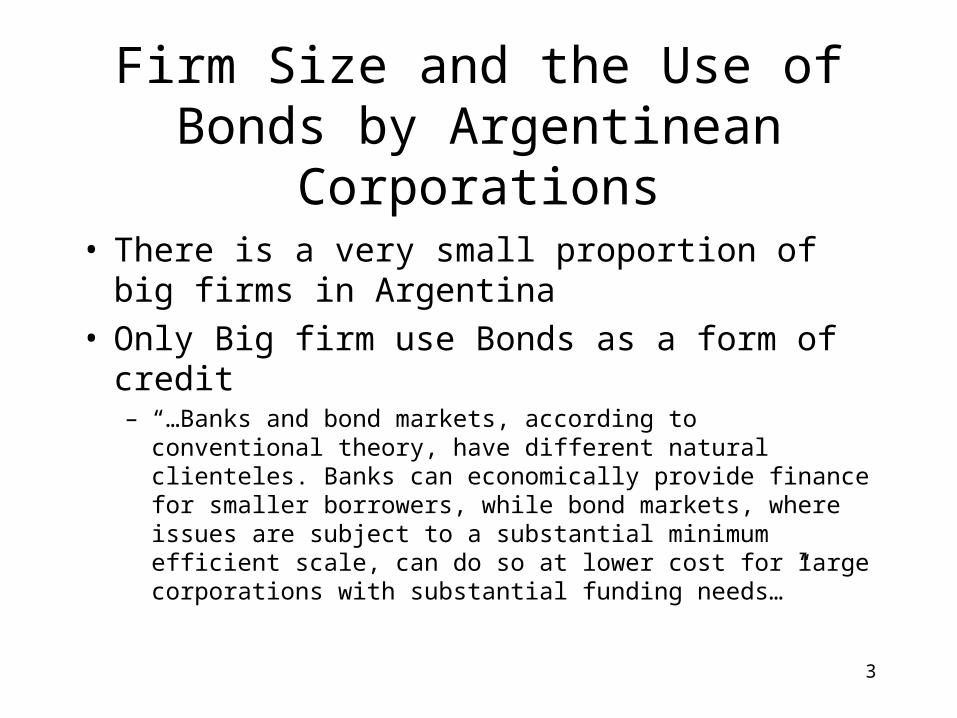

Firm Size and the Use of Bonds by Argentinean Corporations

• There is a very small proportion of big firms in Argentina

• Only Big firm use Bonds as a form of credit– “…Banks and bond markets, according to conventional

theory, have different natural clienteles. Banks can economically provide finance for smaller borrowers, while bond markets, where issues are subject to a substantial minimum efficient scale, can do so at lower cost for large corporations with substantial funding needs…”

4

Conceptual Framework:Modigliani-Miller (M&M) equivalent

proposition [(AB)(-B-A)]

• If the value of the firm is not independent of its financing policy (as is empirically the case), then it must be because the financing policy:

(i) Must affect taxes paid by issuers or investors, given the specificities of corporate and personal taxes, or

(ii) Must affect management’s incentives to follow the value-maximizing rule of investing in all positive NPV projects, or

(iii) Must affect contracting costs (this may include costs of issuing debt, the probability and costs associated to getting into financial difficulty or bankruptcy, etc.), or

(iv) Must provide a credible signal to investors of management’s confidence (or lack thereof) about the firm’s future earnings, in a context of information costs and asymmetric information

5

Evidence from US Firms

• The second reason --incentive problems-- is by far the most important determinant of leverage level (Barclay, Smith, and Watts 1999)

• Proxies: market-to-book ratio and tangibility of assets• The particular debt instrument chosen, which in turn affects the

maturity of the debt, is also affected strongly by the third reason --cost of issuing debt-- (Barclay and Smith 1999)

• Proxy: firm size• We conjecture the same for LA and in particular Argentinean

Firms

6

Taxes

• Taxes (first reason)– The market for bonds started to take off when

modified in 1991 by Law 23.962 to level field with bank loans, that had tax advantages

7

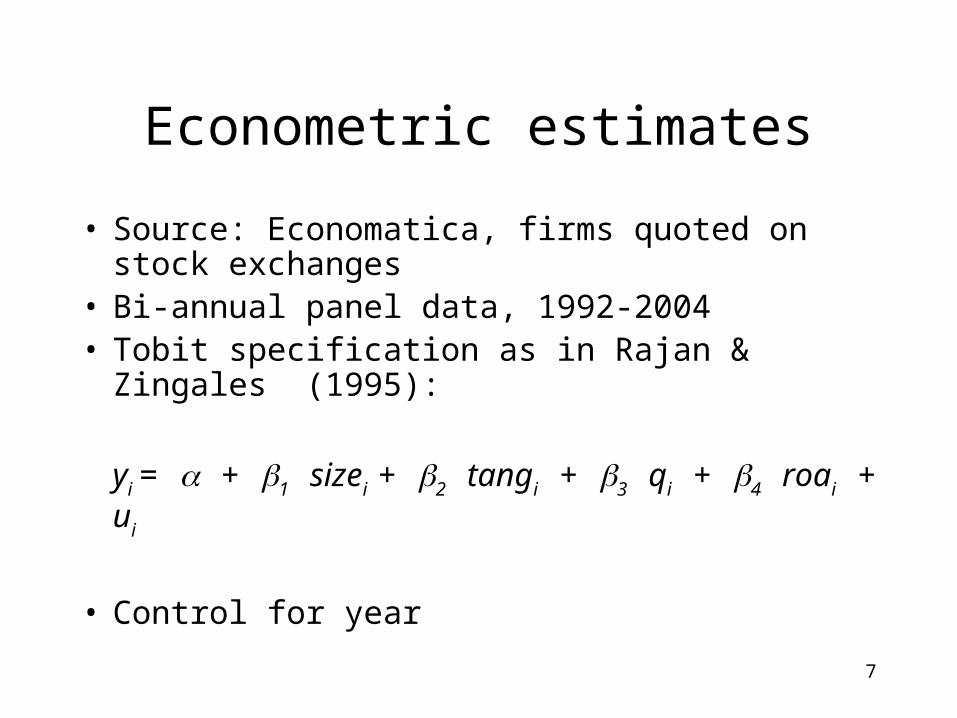

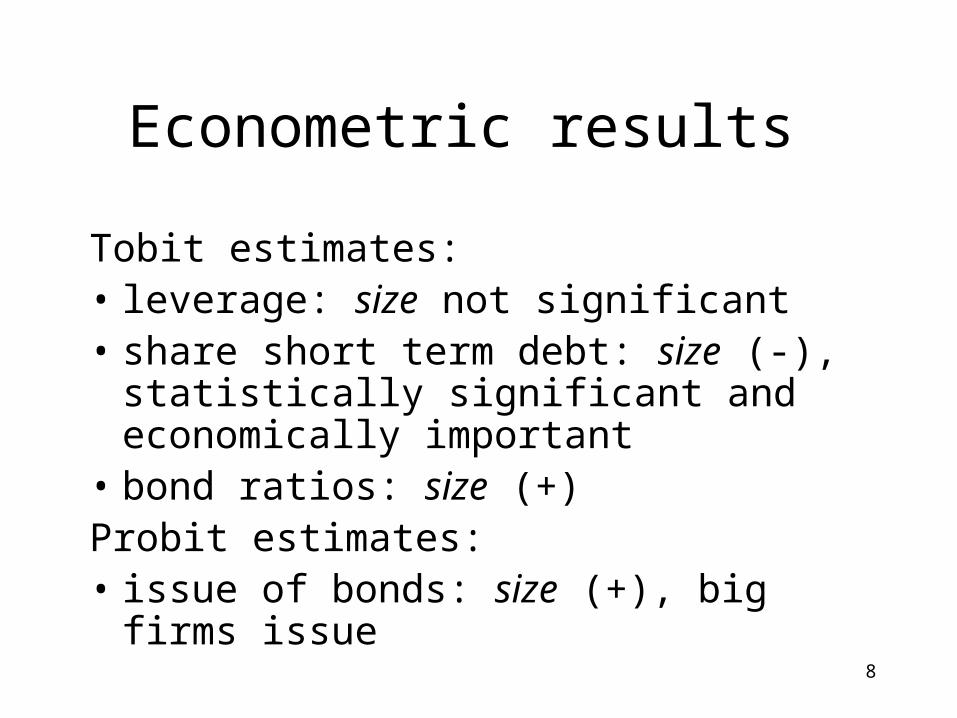

Econometric estimates

• Source: Economatica, firms quoted on stock exchanges

• Bi-annual panel data, 1992-2004• Tobit specification as in Rajan & Zingales

(1995):

yi = + 1 sizei + 2 tangi + 3 qi + 4 roai + ui

• Control for year

8

Econometric results

Tobit estimates:• leverage: size not significant • share short term debt: size (-),

statistically significant and economically important

• bond ratios: size (+) Probit estimates:• issue of bonds: size (+), big firms issue

9

Effect of size on bond ratios

Bond debt /firm value

Bond debt /assets

Bond debt /total debt

mean* parameter

1.69

1.22

2.64

(mean + 2 s.d.)* parameter

2.13 1.54 3.31

Effect of treatment (p.p.)

43.4 31.5 67.5

10

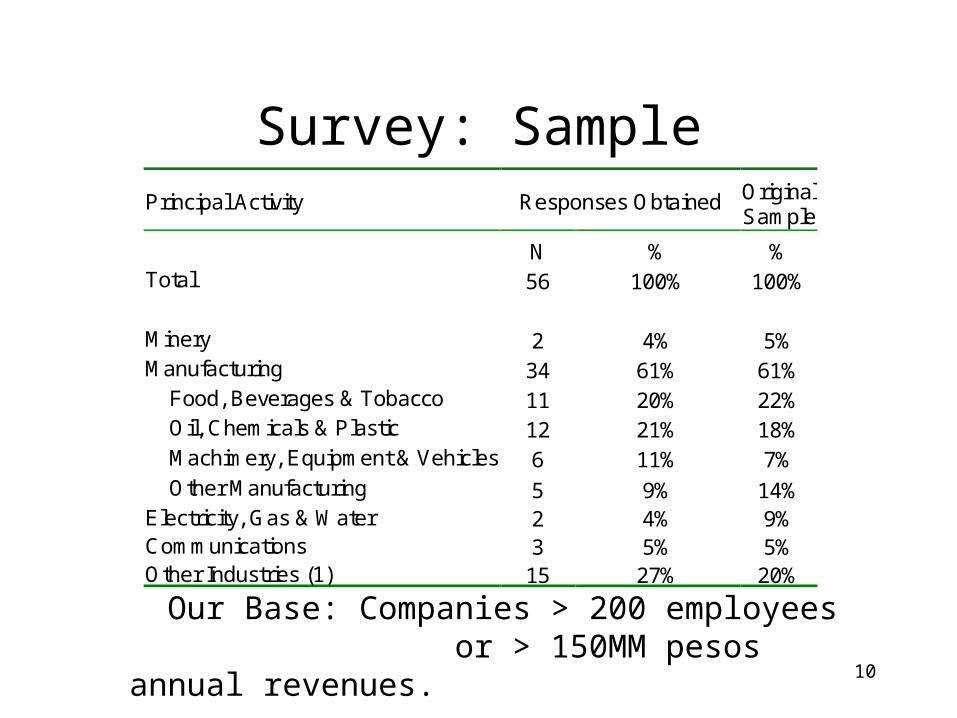

Survey: SamplePrincipal Activity Responses Obtained Original

Sample

N % % Total 56 100% 100% Minery 2 4% 5% Manufacturing 34 61% 61% Food, Beverages & Tobacco 11 20% 22% Oil, Chemicals & Plastic 12 21% 18% Machimery, Equipment & Vehicles 6 11% 7% Other Manufacturing 5 9% 14% Electricity, Gas & Water 2 4% 9% Communications 3 5% 5% Other Industries (1) 15 27% 20% Our Base: Companies > 200 employees

or > 150MM pesos annual revenues.

11

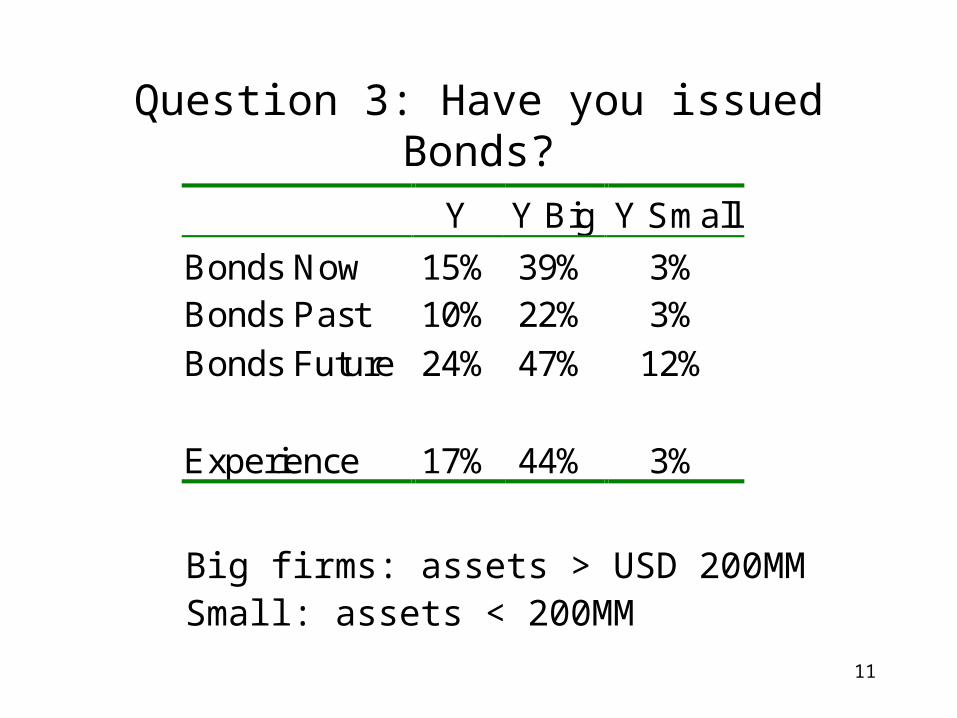

Question 3: Have you issued Bonds?

Y Y Big Y Small

Bonds Now 15% 39% 3% Bonds Past 10% 22% 3%

Bonds Future 24% 47% 12%

Experience 17% 44% 3%

Big firms: assets > USD 200MMSmall: assets < 200MM

12

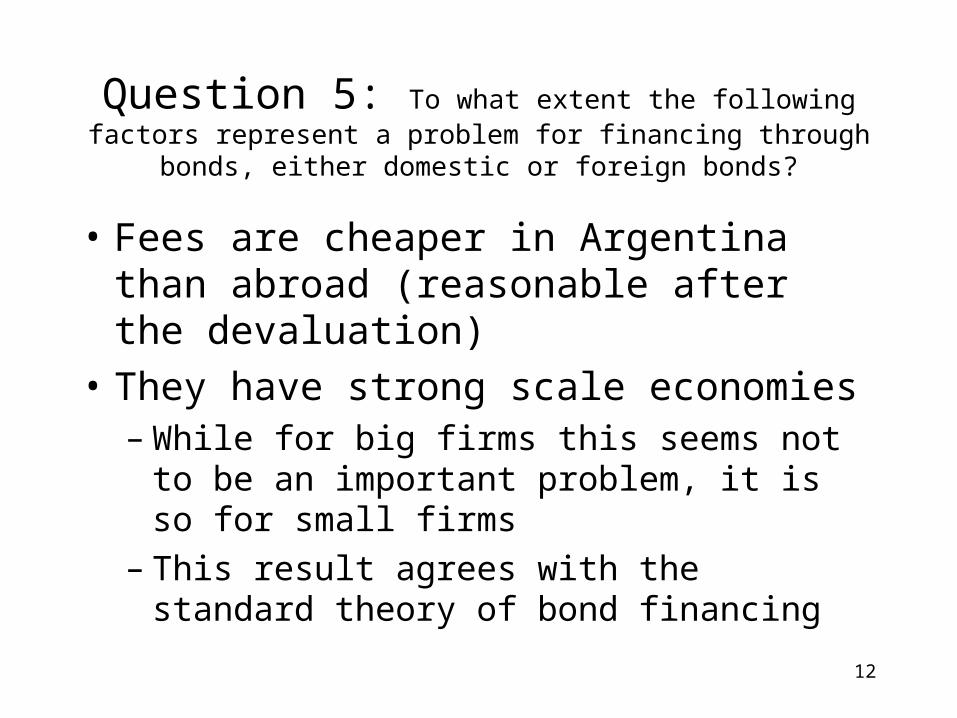

Question 5: To what extent the following factors represent a problem for financing through bonds, either domestic or foreign

bonds?

• Fees are cheaper in Argentina than abroad (reasonable after the devaluation)

• They have strong scale economies– While for big firms this seems not to be an

important problem, it is so for small firms– This result agrees with the standard theory

of bond financing

13

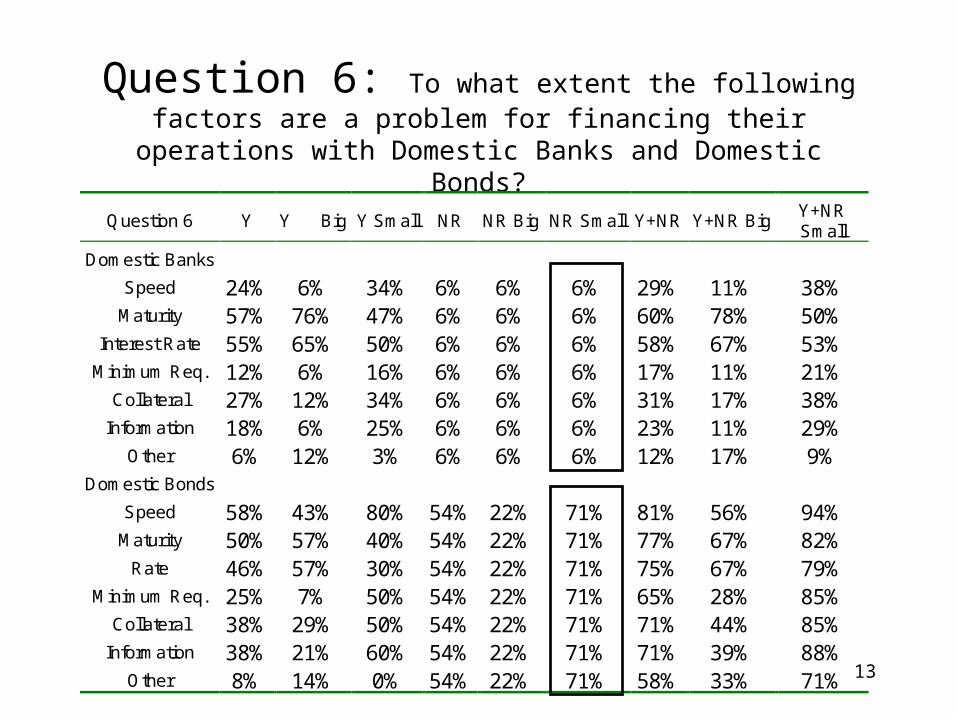

Question 6: To what extent the following factors are a problem for financing their operations with Domestic Banks and

Domestic Bonds?

Question 6 Y Y Big Y Small NR NR Big NR Small Y+NR Y+NR Big Y+NR Small

Domestic Banks Speed 24% 6% 34% 6% 6% 6% 29% 11% 38%

Maturity 57% 76% 47% 6% 6% 6% 60% 78% 50% Interest Rate 55% 65% 50% 6% 6% 6% 58% 67% 53%

Minimum Req. 12% 6% 16% 6% 6% 6% 17% 11% 21% Collateral 27% 12% 34% 6% 6% 6% 31% 17% 38%

Information 18% 6% 25% 6% 6% 6% 23% 11% 29% Other 6% 12% 3% 6% 6% 6% 12% 17% 9%

Domestic Bonds Speed 58% 43% 80% 54% 22% 71% 81% 56% 94%

Maturity 50% 57% 40% 54% 22% 71% 77% 67% 82% Rate 46% 57% 30% 54% 22% 71% 75% 67% 79%

Minimum Req. 25% 7% 50% 54% 22% 71% 65% 28% 85% Collateral 38% 29% 50% 54% 22% 71% 71% 44% 85%

Information 38% 21% 60% 54% 22% 71% 71% 39% 88% Other 8% 14% 0% 54% 22% 71% 58% 33% 71%

14

Question 6: To what extent the following factors are a problem for financing their operations with Domestic Banks and

Domestic Bonds?

• Small firms basically do not use bonds as a form of financing

15

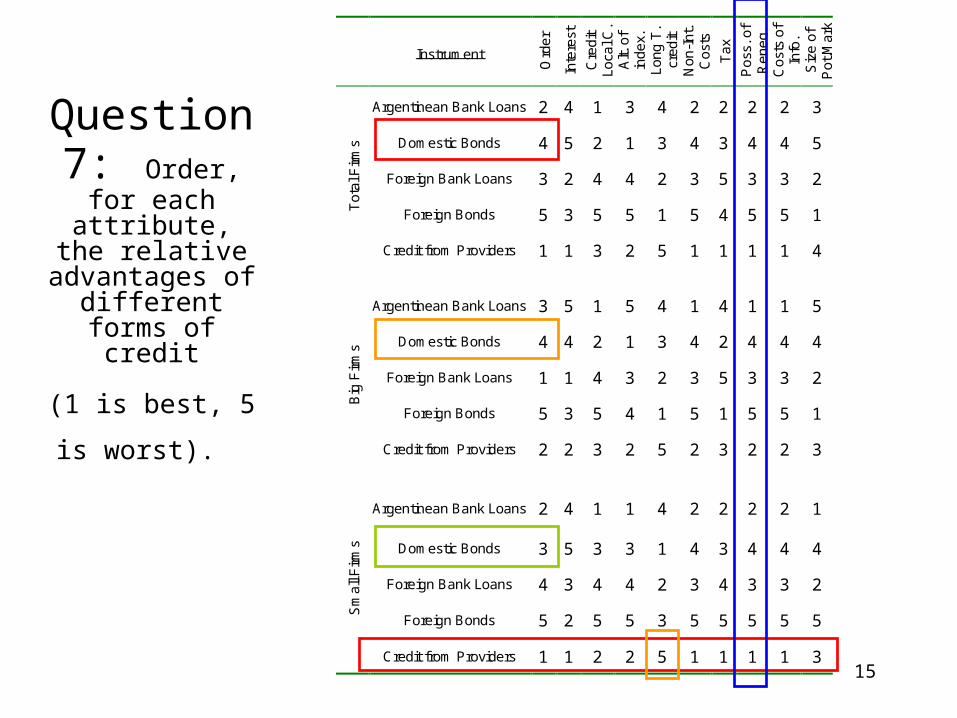

Question 7: Order, for each

attribute, the relative

advantages of different forms of

credit

(1 is best, 5 is

worst).

Instrument

Ord

er

Inte

rest

Cre

dit

Loca

l C.

Alt.

of

ind

ex.

Long

T.

cred

it N

on-I

nt.

Cos

ts

Tax

Pos

s. o

f R

ene

g.

Cos

ts o

f In

fo.

Siz

e of

P

ot.M

ark

Argentinean Bank Loans 2 4 1 3 4 2 2 2 2 3

Domestic Bonds 4 5 2 1 3 4 3 4 4 5

Foreign Bank Loans 3 2 4 4 2 3 5 3 3 2

Foreign Bonds 5 3 5 5 1 5 4 5 5 1 Tot

al F

irms

Credit from Providers 1 1 3 2 5 1 1 1 1 4

Argentinean Bank Loans 3 5 1 5 4 1 4 1 1 5

Domestic Bonds 4 4 2 1 3 4 2 4 4 4

Foreign Bank Loans 1 1 4 3 2 3 5 3 3 2

Foreign Bonds 5 3 5 4 1 5 1 5 5 1

Big

Firm

s

Credit from Providers 2 2 3 2 5 2 3 2 2 3

Argentinean Bank Loans 2 4 1 1 4 2 2 2 2 1

Domestic Bonds 3 5 3 3 1 4 3 4 4 4

Foreign Bank Loans 4 3 4 4 2 3 4 3 3 2

Foreign Bonds 5 2 5 5 3 5 5 5 5 5 Sm

all F

irms

Credit from Providers 1 1 2 2 5 1 1 1 1 3

16

Survey to the Demand side (41 answers)Question 4: main factors that limit the demand for

Corporate Bonds

• Low liquidity of the secondary market was the most important factor limiting the demand for Corporate Bonds (80%)

17

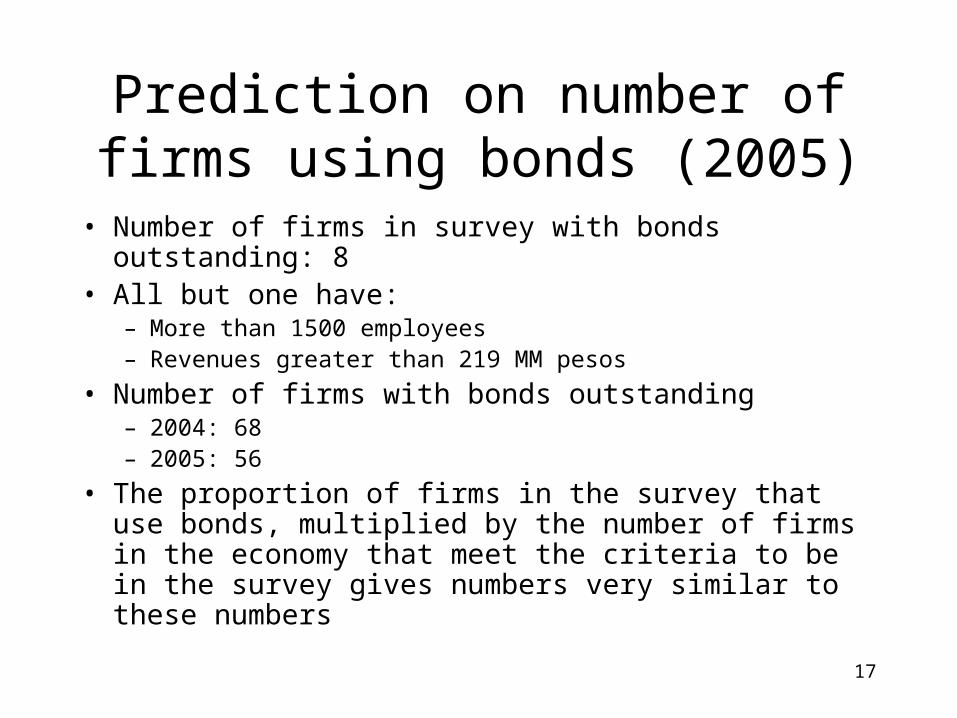

Prediction on number of firms using bonds (2005)

• Number of firms in survey with bonds outstanding: 8• All but one have:

– More than 1500 employees– Revenues greater than 219 MM pesos

• Number of firms with bonds outstanding– 2004: 68– 2005: 56

• The proportion of firms in the survey that use bonds, multiplied by the number of firms in the economy that meet the criteria to be in the survey gives numbers very similar to these numbers

18

Size of the firms is the relevant variable to understand use Bond as a

form of financing

• Econometric results and Survey confirm this

• But there are many different criteria of “size”, which one is the relevant to understand Bond Market development?

19

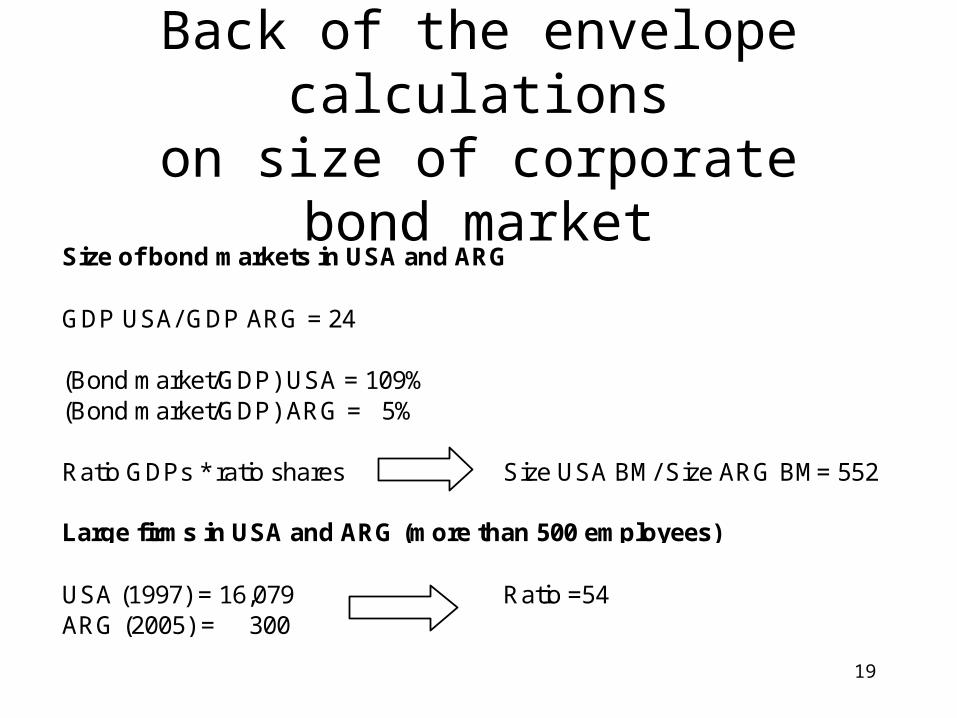

Back of the envelope calculationson size of corporate bond market

Size of bond markets in USA and ARG

GDP USA/ GDP ARG = 24

(Bond market/GDP) USA = 109%(Bond market/GDP) ARG = 5%

Ratio GDPs * ratio shares Size USA BM/ Size ARG BM= 552

Large firms in USA and ARG (more than 500 employees)

USA (1997) = 16,079 Ratio =54ARG (2005) = 300

20

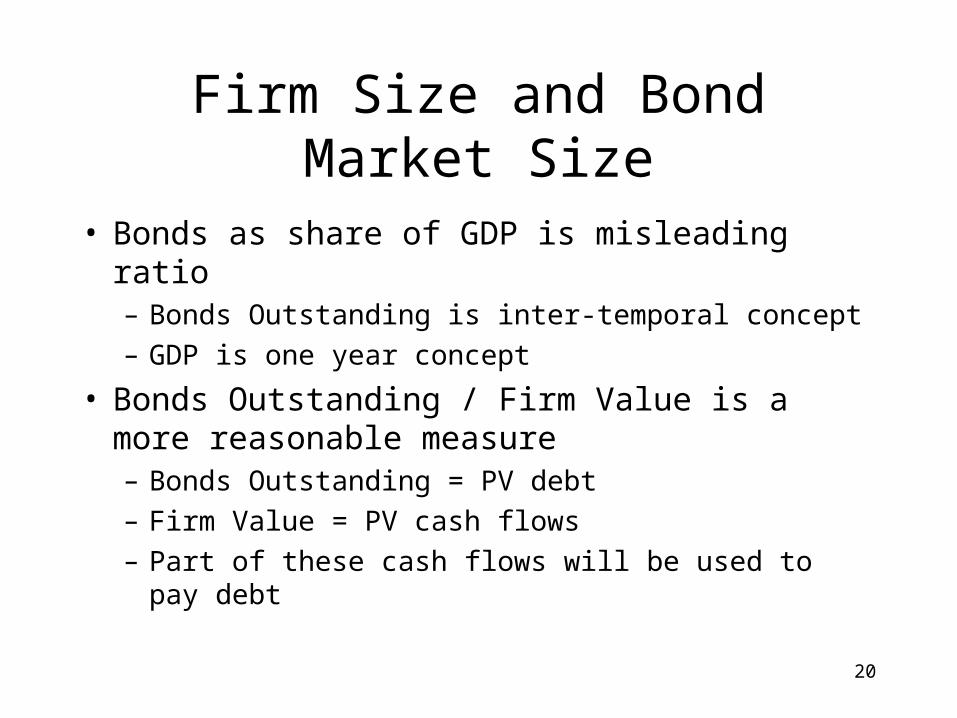

Firm Size and Bond Market Size

• Bonds as share of GDP is misleading ratio– Bonds Outstanding is inter-temporal concept– GDP is one year concept

• Bonds Outstanding / Firm Value is a more reasonable measure– Bonds Outstanding = PV debt– Firm Value = PV cash flows– Part of these cash flows will be used to pay debt

21

Back of the envelope calculations on size of bond market

Size of bond markets in USA and ARG

Ratio of bond market USA to bond market ARG = 552

Large firms in USA and ARG (more than 500 employees)

Ratio large firms USA to large firms ARG = 54

Value of large firms in USA and ARG (quoted on stock exchange)

Ratio firm value USA 500 to firm value ARG 10 = 322Ratio firm value USA 1000 to firm value ARG 20 = 317

22

Are Latin American bond markets underdeveloped?

Domestic Bond Markets in Different Regions of the World (in %)

Country Share of GDP

(1)

Share of total private debt

(2)

Share of financial system

(3) Argentina 4.8 19 5 Brazil 9.6 26 13 Chile 22.8 27 14 Colombia 0.2 1 1 Mexico 2.5 15 7 Peru 4.3 15 9 Latin American average 7.0 17 8 East Asia average 32.0 22 13 United States 109.0 72 38 High income average 40.0 27 18 Sources: BIS, IFS.

23

Are Latin American bond markets underdeveloped?

Domestic Bond Markets in Different Regions of the World (in %)

Country Share of GDP

(1)

Share of total private debt

(2)

Share of financial system

(3) Argentina 4.8 19 5 Brazil 9.6 26 13 Chile 22.8 27 14 Colombia 0.2 1 1 Mexico 2.5 15 7 Peru 4.3 15 9 Latin American average 7.0 17 8 East Asia average 32.0 22 13 United States 109.0 72 38 High income average 40.0 27 18 Sources: BIS, IFS.

24

Are Latin American bond markets underdeveloped?

• Perhaps, but our research points to another question:

– Why is the market value of firms so small in Argentina, and Latin America?