- habib bank uk

TRANSCRIPT

ANNUAL REPORT 2011

AN

NU

AL REPO

RT - 2011

1

Directors’ report 2

Statement of director’s responsibilities 8

Independent auditor’s report 9

Group financial statements

Consolidated profit and loss account 10

Consolidated balance sheet 11

Notes to the accounts 12-29

Holding company financial statements

Profit and loss account 30

Balance sheet 31

Notes to the accounts 32-48

Table of Contents

Directors’ ReportThe Directors have pleasure in presenting their Annual Report and Audited Financial Statements together with the Auditors’ Report thereon for the year ended 31 December 2011.For the purpose of this report the Group comprises of: Holding company: Habib Allied International Bank Plc (HBL UK) Subsidiary company: Habibsons Bank Limited

A key milestone for the Group was the acquisition of Habibsons Bank Limited (HS) on 20 April 2011. It is a UK incorporated Bank, authorised and regulated by the FSA. HS has been operating in the UK since 1984 and as at 31st December 2010, its total assets were circa GBP250 million. It had five branches in the UK and one in Zurich. The client base of HS is similar to that of HBL UK and the products and services not only include the usual commercial banking products but also services required by High Net Worth Individuals (HNWI). Their client reach extends beyond the UK to locations such as Southern and Eastern Africa.

The raison d’êtres for the acquisition centred around buying in to an accepted brand that has low cost deposits, achieving economies of scale through the utilization of built-up processing capacity at HBL UK, complementing the market strength of each Bank and through these, achieve one of our core objectives; enhance shareholder value.

It is the intention to have the two Banks operate distinctly as separate brands; HBL UK providing commercial banking services to its target clients whereas HS to provide products and services for the HNWIs.

Principal Activities

HBL UK and HS are both authorised institutions under the Financial Services and Markets Act 2000 and regulated by the Financial Services Authority (FSA). They provide a range of commercial banking services including all aspects of trade finance, short term finance, funds transfers including electronic remittances, FX & MM dealings and depository products within the scope of the authorisation granted by the FSA.

Business Review

This year the Group completed its tenth full year of operations and has made satisfactory progress during this period. This is reflected in sustainable business volumes and operating income in a difficult economic environment. The Group adopted a prudent approach to lending with a greater focus on trade related business (both funded and non-funded). During the year under review there were additional impairments that were recognized and after adjustments made to existing provisions, a net charge of GBP1.9 million was made to the profit and loss account.

While the non funded revenue remained flat over the year, funded revenue however reduced owing primarily to a conscious reduction of exposures to West Africa and Bangladesh where the margins previously had been healthy. New facilities had to pass a more stringent set of credit requirements which were enforced to safeguard against the continued market uncertainties. Greater focus was given to short term trade business from Financial Institutions. The distribution channel for down-selling these transactions was further enhanced successfully.

The Group remained liquid and took exceptional steps to ensure that placement of surplus liquidity was either in UK Gilts or other top rated sovereign paper. The focus was on preservation rather than increased earnings.

The customer deposit base continued to show stability although a few large savers withdrew their savings to invest in other high earning products. The Group maintained good liquidity and adequate regulatory capital during the year under review. Despite clear challenges in the financial sector, the Group is positioned to take advantage of the potential opportunities in the coming years and pursue its business objectives cautiously to ensure that it is aligned with its own business strategy and keeping within the guidelines of the regulator.

The Group offers personalised services to its customers with a commitment to quality and value to its clients. Its organisational structure is designed to support this objective whilst also ensuring that effective controls and oversight are maintained across the business. The Group has developed a cordial and professional relationship with all stakeholders which is essential for its future progress.

Over the years, shareholders funds have grown from GBP25 million to circa GBP50 million as at 31 December 2011. This is primarily due to the strategy of profit retention.

AN

NU

AL REPO

RT - 2011

3

The Directors are confident that the Group has the capacity, management skills and opportunity to continue to deliver steady growth in future years.

Principal Risks and Risk Management

Principal risks: Banks are, by their very nature, in the risk business and taking risk is an integral part of banking. The Group is primarily exposed to credit risk, market risk (including interest, FX and liquidity risks), operational risk (including risk of non-compliance with regulatory requirements) and reputational risk. All these risks are managed through adherence to documented policies and procedures together with a high level managerial oversight of the Group’s operations.

Given the conditions in the financial markets, the Group has consciously adopted a strategy to maintain adequate liquidity at all times, both in terms of amount and quality, to ensure that it continues to meet its obligations as they fall due. The Group regularly reviews its asset / liability maturity mismatches and maintains liquidity gaps within prescribed limits.

Risk Management: The Board of Directors has overall responsibility for the establishment and oversight of risk management and continues to maintain a “Risk Averse” policy to risk. The Group has established Risk Management systems and controls to ensure that all of its principal risks are identified and that policies and monitoring processes are in place to mitigate them. The Group’s risks are managed taking into account several main principles including responsibilities for management of risk and controls, assessment and measurement of all identified risks with a balance between risks versus return and undertaking an annual review of risk policies and the control framework to ensure optimal capital allocation and utilisation for relevant risks.

Those risks identified in the Group’s risk registers are at a level commensurate with current business operations and the proposed Business Plan. With regard to credit risk, given the unprecedented conditions in the market and economy, the controls in this area have been strengthened with additional oversight to ensure regular stress testing of the portfolio and a focussed strategy is adopted for nursing stressed borrowers.

With a view to maximising shareholder value, the risk management systems seek to ensure that the Group’s risk profiles are aligned to available financial and non-financial resources. To ensure this, the Board of Directors has established:

• Defined,clearandcoherentRiskManagementsystemsandcontrolscoveringvarioustypesofriskstotheGrouptoensure that all of its principal risks are identified and that internal monitoring processes, procedures and controls are in place to mitigate them;

• Suitableforumsfordiscussing,monitoringandmanagingtheserisks.Allkeydecisionsaresubjecttothe“foureyes”principle;

• ARiskManagementFrameworkwhichsetsouttheconstitution,rolesandresponsibilitiesoftheBoardofDirectors,Non Executive Directors, all the Committees, Chief Executive Officer, and Management.

To enable a better and more focused attention to the affairs of HBL UK, including the oversight of its subsidiary, Habibsons Bank, the Board has established a number of Committees, each with defined terms of reference, scope of work, roles and responsibilities to prepare the ground work for decision making and to assist the Board in monitoring the implementation of the policies, processes and procedures.

During the year the Group has substituted the Credit Policy Committee, which focused only on credit and counterparty risk and replaced it by establishing a Group Risk Management Committee (RMC). The terms of reference of the RMC include not just the credit and counterparty risks but also; market, operational and reputational risks.

All significant matters discussed and decided at each meeting of the Board Committees are reported to the Board by the Chairman of the respective Committees:

• AuditandComplianceCommittee

• GroupRiskManagementCommittee

• GroupHumanResourcesCommittee

• GroupIntegrationCommittee

The Risk management disclosures as required under Pillar III are available on the Group’s website: www.habibbankuk.com. These disclosures under the Pillar III include a detailed risk management analysis, Capital Management and details of overdue and impairment exposures.

Basel II Capital Resource Requirement: Under the Capital Requirement Directive, the Group has adopted the Standardised Approach to credit risk and the Basic Indicator Approach to operational risk. The Group has implemented the Basel II Capital Resource Requirement and maintains its capital adequacy within the Individual Capital Guidance (ICG) received from the FSA

after a supervisory review of the Internal Capital Adequacy Assessment Process (ICAAP). The Group has remained in compliance with its ICG requirements that includes maintaining a Capital Planning Buffer (CPB) during the year.

Liquidity Management: Under the new liquidity regulations, the Group has implemented the FSA’s requirements for liquidity risk management including embedding systems and controls.

Money Laundering and Terrorist Financing: The Group has adopted a risk based approach to prevent financial crime. Documented policies and procedures are in place to combat money laundering and terrorist financing which are independently monitored by the Compliance Department. All employees at regular intervals and new employees at the time of joining the service of the Group receive Anti-Money Laundering training to ensure their awareness of the risk of money laundering and terrorist financing while conducting business activities.

To identify any potential suspicious transactions that fall outside of a customer’s ‘Know Your Customer’ profile, the Group has an automated transaction monitoring system that monitors customer transactions against defined parameters. The Compliance Department reviews the alerts generated and where necessary, undertakes investigations to satisfy itself of the efficacy of the transaction or raises a suspicious activity report.

To check funds transfers to or from a person / entity on any of the various sanctions list, the Group monitors and filters, through a robust application, all transactions on a real-time basis.

Treating Customers Fairly: The Group fully supports the FSA’s initiative on ‘Treating Customers Fairly’ (TCF), and has adopted a proactive approach to ensuring compliance with Principle 6 of the FSA’s ‘Principles for Businesses’, which states “a firm must pay due regard to the interests of its customers and treat them fairly”. The Board and senior management continues to ensure that the concept of TCF is fully embedded into the culture of the Group at all levels. Policies are in place to guide employees in understanding how they can help the Group deliver on the commitment.

The Group has a complaints handling procedure and encourages customers to report instances where the Group’s service falls short of the expected high standards. This commitment remains a priority for the Group.

Internal Controls: The system of internal control is based on an ongoing process designed to identify the principal risks which are inherent in the Group’s business, to evaluate the nature and extent of those risks and to manage them efficiently and effectively.

The Group’s system of internal control includes appropriate levels of authorisation, segregation of duties and limits for each aspect of business. There are established procedures and MIS for regular reporting of financial information. Financial reports are presented to the Board in each of its meetings detailing results and other performance data.

Management assumes the responsibility of establishing and maintaining adequate internal controls and procedures while the Board of Directors is ultimately responsible for the internal control systems. For this purpose the Group has developed Procedure Manuals that are followed when conducting the various banking transactions. These Procedure Manuals are revised and updated as and when required.

The Internal Audit function of the Group reviews the adequacy and implementation of internal controls on a regular basis and deficiencies, if any, are followed up until they are rectified. Status of the unresolved significant issues is reviewed by the Audit and Compliance Committee (ACC) in each of its meetings. An audit programme is agreed annually with the ACC and the Head of Audit presents a summary of audit reports completed during the period and provides any explanation required by the Committee.

Anti-Bribery Policy: The Group places great value on all of its assets. Among those assets none has greater value or is of more importance to the Group than its reputation. The Board, senior management and every employee has a significant role to play in preserving and nurturing the Group’s reputation for honesty, integrity, and fair play in dealing with fellow employees, customers, regulators, suppliers and the general public. The Group expects all employees to conduct themselves in accordance with the highest standards of personal and professional integrity and to comply with all laws, regulations, corporate policies and procedures. The Group has adopted a formal Anti-Bribery Policy for prevention of bribery and has a zero tolerance approach towards any type of bribery. Staff members are required to report any bribery that comes to their attention. The Policy clearly states that any person found in breach of this Policy will expose themselves to necessary disciplinary proceedings and possible prosecution.

Financial Performance – Results

The Group’s financial statements for the year ended 31 December 2011 are set out in detail on pages 10 to 29. The profit on ordinary activities before tax for the financial year amounted to GBP 712,000 (2010: GBP 5,133,000). Financial statements of the parent for the year ending 31 December 2011 are set out in detail on pages 30 to 48.

AN

NU

AL REPO

RT - 2011

5

The Directors do not propose the payment of a dividend for the year (2010: Nil). Hence, the profit is retained in the Profit and Loss account.

Share Capital

There is no change in the fully Paid-up Capital of HBL UK during the year which remained at GBP 25,000,000 divided into 25,000,000 ordinary shares, with the following shareholding:

Habib Bank Limited 90.50% Allied Bank Limited

The Group raised lower Tier II and upper Tier II capital of US$ 33 million and US$ 10 million in December 2010 and December 2011 respectively and it remains adequately capitalised.

Directors

During the year under report, the Board of Directors held three meetings. The Directors who held the office at the date of this report are:

R Zakir Mahmood Chairman – Non Executive

Ayaz Ahmed Non Executive

David J Blatchford Independent Non Executive

Habib M Dawood Habib Non Executive (appointed 24 January 2011)

John N Cotton Independent Non Executive (appointed 14 July 2011)

Khalid A Sherwani Non Executive

Nauman K Dar Non Executive

Anwar M Zaidi Chief Executive Officer

Nauman K Dar relinquished and Anwar M Zaidi assumed the role of Chief Executive Officer for HBL UK on 24 May 2011. Mr Dar however continues as a Non-Executive Director.

The Board places on record its appreciation for the valuable services rendered by Mr Dar as CEO of the Bank and welcomes Mr Zaidi as the new CEO.

Director’s Interests

None of the directors who held office either during the year or at the end of the financial year under review had any disclosable interest in the shares of the Bank. No contract of significance in relation to the Bank’s business in which a director of the Bank has a material interest, whether directly or indirectly, subsisted at the end of the year or at any time during the year other than contracts entered in the normal course of business on an arms length basis or under a service contract.

Policy and Practice on Payment to its Suppliers

The Group has a regular cycle of obtaining services and releasing payments to the creditors and suppliers. The Group conforms to terms of settlement agreed with its suppliers as long as it is satisfied that goods or services have been supplied as agreed. It is not the Group’s policy to follow the terms of a standard code of payment practice. At the year end, the average days outstanding for trade creditors for HBL UK amounted to 11 days (2010: 26 days).

Political and Charitable Contributions

During the year, the Group made no political or charitable contributions.

Corporate Governance

The Board has ultimate responsibility for the proper stewardship of the Group. It meets regularly to discharge its responsibilities for all important aspects of the Group’s affairs, including monitoring performance, considering major strategic issues, approving budgets and business plans.

The Board is firmly committed to the highest standards of corporate governance. The Group’s corporate governance is directed not only towards regulatory and legal requirements but also towards adherence to sound business practices, transparency and disclosures to shareholders. The Group within its relationship with its borrowers, depositors, shareholders and other stakeholders

9.50%

has always maintained its fundamental principles of corporate governance – that of integrity, transparency and fairness, seeking to provide an enabling environment to harmonise the goals of maximising shareholder value and maintaining a customer centric focus.

The corporate governance framework of the Group is based on an effective and independent Board which is not involved in day-to-day management. The position of the Chairman of the Board of both the Banks and CEOs are held by separate individuals. The Board of Directors is entrusted with the formulation of policy guidelines, objective setting, strategic planning, organisational structure, supervising business activities, reviewing performance of management, ensuring regulatory compliance and safeguarding interests of the shareholders. The Management seeks to realise the Group’s strategic goals which are to maximise long term shareholder value and to maintain the required standards of integrity and transparency.

Board meetings are held at least three times a year. If required, additional meetings can be held to discuss any specific item of critical importance. The Company Secretary in consultation with the CEO and Chairman prepares a detailed agenda for the meetings. Agenda papers and other explanatory notes are circulated to the directors in advance. The directors have complete access to all information, and are free to recommend inclusion of any matter in the agenda for discussion. Senior management is also invited to attend the Board meetings as and when required, so as to provide additional input to the items or issues being reviewed or discussed by the Board.

For smooth operation, risk management and monitoring purposes, the Board has formed various committees. These Board committees conduct detailed analyses and reviews of various policies and critical issues and ensure that the activities of the Group are always conducted in accordance with appropriate ethical standards. All the significant matters discussed and decided at each meeting are reported to the Board by the Chairmen of the respective committees.

The Group has an independent Audit and Compliance function with the Head of Audit and Compliance reporting directly to the Chairman of the ACC who is an Independent Non Executive Director. The Committee reviews the Bank’s internal controls, Risk Management Systems, statutory and regulatory compliance. After detailed discussions on the findings of Internal Audit as well as the statutory auditor’s reports, the Committee initiates necessary corrective actions. The Committee apprises the Board of Directors of any significant issues and the corrective measures initiated. The Committee also follows up implementation of its various suggestions / decisions on a regular basis.

The Group has developed an experienced compliance team with the aim of ensuring adherence to regulatory requirements throughout the Group, as well as providing timely guidance to business areas. Compliance work is designed to ensure that the Group’s activities are undertaken in line with professional ethics and in accordance with relevant laws and regulations.

The Chief Executive Officer, who reports to the Chairman and the Board, is empowered by the Board of Directors for all operational issues and day-to-day management of the Bank. In carrying out his duties he is assisted by senior management and the following committees:

• Group Asset and Liability Committee• Group Operations Review Committee• Business Review Committee• Portfolio Review Committee• Group IT Steering Committee

Code of Ethics

Employees

As at 31 December 2011 the Group had 153 employees (2010: 84). Variable compensation of staff is related to performance and the Group encourages the involvement of all employees in the overall performance and profitability of the Group through an objective based appraisal system that focuses on qualitative and quantitative factors. The Group has a defined contribution pension scheme, whereby members are entitled to a minimum of 5% contribution of their basic salary by the employer. All regular employees enjoy life insurance cover to a minimum of 3 times their annual salary. The Group believes it enjoys a good relationship with its staff.

The standards of ethical conduct which the Group expects from its employees are laid down in the Group’s Code of Ethics and Business Conduct introduced in 2006 and updated if felt necessary. These are a set of principles that reinforce the rules and regulations reflected in the Group’s Policies and Procedures and cover important topics including prevention of money laundering and terrorist financing, fraud – theft or illegal activities, office decorum, confidentiality, conflicts of interest, insider trading, gifts and inducements. The Code of Ethics and Business Conduct for employees ensures that the employees conduct themselves with dignity and integrity and build customer confidence.

AN

NU

AL REPO

RT - 2011

7

Acknowledgement

The Board of Directors takes the opportunity to express its thanks and gratitude to all stakeholders including its customers for their continued support and cooperation without which the business growth of the Group would not have been possible.

The Board of Directors also records its appreciation to the Management and Staff for their dedication, commitment and team work, without which this year’s results would not have been possible.

Directors’ Representation

The directors’ who held office at the date of this Directors’ Report confirm that, so far as they are each aware, there is no relevant audit information of which the Group’s auditors are unaware; and each director has taken all steps that he ought to have taken as a director in order to make himself aware of any relevant audit information and to establish that the Group’s auditors are aware of that information.

The directors are unaware of any material events that have occurred since the end of the financial year to the date of signing this report that could impact the financial health of the Group.

Auditors

In accordance with section 489 of the Companies Act 2006, a resolution for the appointment of KPMG Audit Plc as auditors of the Group is to be proposed at the forthcoming Annual General Meeting.

By order of the Board of Directors

Anwar M Zaidi Chief Executive Officer Habib Allied International Bank Plc 63 Mark Lane London EC3R 7NQ

Dated: 12 March 2012

Statement of Directors’ Responsibilities in Respect of the Directors’ Report and the Financial StatementsThe directors are responsible for preparing the Directors’ Report and the financial statements in accordance with applicable law and regulations.

Company law requires the directors to prepare financial statements for each financial year. Under that law they have elected to prepare the group and parent company financial statements in accordance with UK Accounting Standards and applicable law (UK Generally Accepted Accounting Practice).

Under company law the directors must not approve the financial statements unless they are satisfied that they give a true and fair view of the state of affairs of the group and parent company and of their profit or loss for that period. In preparing each of the group and parent company financial statements, the directors are required to:

• selectsuitableaccountingpoliciesandthenapplythemconsistently;

• makejudgementsandestimatesthatarereasonableandprudent;

• statewhetherapplicableUKAccountingStandardshavebeenfollowed,subjecttoanymaterialdeparturesdisclosedand explained in the financial statements;

• preparethefinancialstatementsonthegoingconcernbasisunlessitisinappropriatetopresumethatthegroupandthe parent company will continue in business.

The directors are responsible for keeping adequate accounting records that are sufficient to show and explain the parent company’s transactions and disclose with reasonable accuracy at any time the financial position of the parent company and enable them to ensure that its financial statements comply with the Companies Act 2006. They have general responsibility for taking such steps as are reasonably open to them to safeguard the assets of the group and to prevent and detect fraud and other irregularities

The directors are responsible for the maintenance and integrity of the corporate and financial information included on the company’s website. Legislation in the UK governing the preparation and dissemination of financial statements may differ from legislation in other jurisdictions.

AN

NU

AL REPO

RT - 2011

9

Independent Auditor’s Report to the Members of Habib Allied International Bank PLCWe have audited the financial statements of Habib Allied International Bank PLC for the year ended 31 December 2011 set out on pages 10 to 48. The financial reporting framework that has been applied in their preparation is applicable law and UK Accounting Standards (UK Generally Accepted Accounting Practice).

This report is made solely to the company’s members, as a body, in accordance with Chapter 3 of Part 16 of the Companies Act 2006. Our audit work has been undertaken so that we might state to the company’s members those matters we are required to state to them in an auditor’s report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the company and the company’s members, as a body, for our audit work, for this report, or for the opinions we have formed.

Respective responsibilities of directors and auditor

As explained more fully in the Directors’ Responsibilities Statement set out on page 8, the directors are responsible for the preparation of the financial statements and for being satisfied that they give a true and fair view. Our responsibility is to audit, and express an opinion on, the financial statements in accordance with applicable law and International Standards on Auditing (UK and Ireland). Those standards require us to comply with the Auditing Practices Board’s (APB’s) Ethical Standards for Auditors.

Scope of the audit of the financial statements

A description of the scope of an audit of financial statements is provided on the APB’s website at www.frc.org.uk/apb/scope/private.cfm.

Opinion on financial statements

In our opinion the financial statements:

• giveatrueandfairviewofthestateofthegroup’sandoftheparentcompany’saffairsasat31December2011andofthe group’s and the parent company’s profit for the year then ended;

• havebeenproperlypreparedinaccordancewithUKGenerallyAcceptedAccountingPractice;and• havebeenpreparedinaccordancewiththerequirementsoftheCompaniesAct2006.

Opinion on other matter prescribed by the Companies Act 2006

In our opinion the information given in the Directors’ Report for the financial year for which the financial statements are prepared is consistent with the financial statements.

Matters on which we are required to report by exception

We have nothing to report in respect of the following matters where the Companies Act 2006 requires us to report to you if, in our opinion:

• adequateaccountingrecordshavenotbeenkeptbytheparentcompany,orreturnsadequateforouraudithavenotbeen received from branches not visited by us; or

• theparentcompanyfinancialstatementsarenotinagreementwiththeaccountingrecordsandreturns;or• certaindisclosuresofdirectors’remunerationspecifiedbylawarenotmade;or• wehavenotreceivedalltheinformationandexplanationswerequireforouraudit.

Paul Furneaux (Senior Statutory Auditor) for and on behalf of KPMG Audit Plc, Statutory Auditor Chartered Accountants London 12 March 2012

Consolidated Profit and Loss AccountFor the year ended 31 December 2011

Note Year ended 31 December

2011£’000

Year ended 31 December

2010£’000

Interest receivable Interest receivable and similar income arising from debt securities Other interest receivable and similar income

2,008 9,007

1,178

5,696

11,015 6,874

Interest payable (4,441) (1,838)

Net interest income 6,574 5,036

Fees and commissions receivable 5,855 3,800

Foreign exchange dealing profits 1,316 973

Other operating income 782 1,058

Total operating income 14,527 10,867

Administrative expenses

Depreciation

Amortisation of goodwill

2

7

8

(11,142)

(430)

(372)

(7,007)

(344)

-

Total operating expenditure (11,944) (7,351)

2,583 3,516

Provision for loan losses Impairment and reversal on debt securities

12 (1,871) -

(189) 1,806

Profit on ordinary activities before tax 712 5,133

Tax on profit on ordinary activities 4 (567) (1,863)

Profit on ordinary activities after tax 15 145 3,270

There are no recognised gains and losses other than the profit for the year as reported above. The result for the year is derived entirely from continuing activities. The notes on pages 12 to 29 form part of these financial statements.

AN

NU

AL REPO

RT - 2011

11

Consolidated Balance SheetAs at 31 December 2011

Note 2011 £’000

2010£’000

AssetsCash and balances at central banksLoans and advances to banksLoans and advances to customersDebt securitiesOther assetsPrepayments and accrued incomeTangible fixed assetsIntangible assets - goodwillDeferred taxation

6 10

7 8 9

1,038

253,257 199,376 159,711

1,955 2,790 3,150

10,780 4,051

392

165,390 121,964 91,980

756 1,099 2,314

- 4,279

Total Assets 636,108 388,174

Liabilities Deposits by banks Customer accounts Other liabilities Accruals and deferred income Subordinated liabilities

11

14

128,437 422,381

2,870 1,461

31,581

122,166

193,960 1,204

433 21,178

Total Liabilities 586,730 338,941

Shareholders’ funds Called up share capital Profit and loss account Other reserves

13 15 15

25,000 23,328

1,050

25,000 23,183 1,050

49,378 49,233

Total liabilities & Equity 636,108 388,174

The notes on pages 12 to 29 form part of these financial statements.

These financial statements were approved by the board of directors on March 12, 2012 and signed on its behalf by:

Anwar Zaidi Chief Executive Officer

Notes to the Consolidated Financial StatementFor the year ended 31 December 20111 The Group and its operations

Habib Allied International Bank Plc (the Bank) is incorporated in United Kingdom and is engaged in commercial banking services. The Bank’s registered office is located at 63 Mark Lane, London EC3R 7NQ.

The Group comprises of: Holding Company : Habib Allied International Bank Plc Subsidiary Company : Habibsons Bank Limited

The financial statements of the Bank as at and for the year ended 31 December 2011 comprises the bank and its subsidiary (together referred to as the “Group”).

(a) Accounting policies

The following accounting policies have been applied consistently in dealing with items which are considered material in relation to the Group’s financial statements.

(b) Basis of preparation

The financial statements cover the year from 1 January 2011 to 31 December 2011 and have been prepared under the historical cost convention and in accordance with the special provisions of Statutory Instrument 2008/410, Schedule 2 of the Companies Act 2006 relating to banking companies, applicable UK mandatory accounting standards and the British Banker’s Association Statements of Recommended Accounting Practice.

The preparation of these financial statements requires management to make estimates and judgments. This is particularly so in the assessment of provisions for bad and doubtful debts and in assessing impairment of debt securities. Making reliable estimates of the ability of customers and other counterparties to repay is often difficult even in periods of economic stability and becomes more difficult in periods of economic volatility. Therefore, while management believes it has utilised all available information to estimate adequate allowances for all identifiable risks in the current portfolios, there can be no assurance that the provisions for bad and doubtful debts or other impairment provisions will prove adequate for all losses ultimately realised.

The Group’s financial statements have been prepared on the going concern basis which the directors believe to be appropriate as there are no material uncertainties that may cast significant doubt about the Group’s ability to continue as a going concern. This conclusion is based on the following:

Review of the financial performance and outlook, principal risks and risk management as discussed in the Director’s report

Detailed assessments carried out by the management in respect to the key areas of the Group such as the liquidity, capital management, profit projections and litigation covering a period of twelve months from the date of signing the balance sheet.

The Risk management disclosures as required under Pillar III are available on the Group’s website: www.habibbankuk.com. These disclosures under the Pillar III include a detailed risk management analysis, Capital Management and details of overdue and impairment exposures.

(c) Basis for consolidation

On 20 April 2011 Habib Allied International Bank Plc acquired 100% of the share capital of Habibsons Bank Limited from Valona Finance.

Subsidiaries are entities controlled by the Group. Control exists when the Group has the power to govern the financial and operating policies of an entity, so as to obtain economic benefits from its activities. Business combinations are accounted for using the acquisition method as at the acquisition date, which is the date on which control is transferred to the Group.

The consolidated financial statements incorporate the financial statements of Habib Allied International Bank Plc and the financial statements of its subsidiary company, Habibsons Bank Limited, from the date that control commences until

(i)

(ii)

AN

NU

AL REPO

RT - 2011

13

the date that control ceases. The financial statements of such subsidiary company are incorporated on a line-by-line basis and the investment held by the Bank is eliminated against the corresponding share capital of the subsidiary in the consolidated financial statements.

The accounting policies of the subsidiary have been changed where necessary to align them with the policies adopted by the Group.

Material intra-group balances and transactions are eliminated.

(d) Intangible assets - goodwill

Goodwill that arises upon the acquisition of subsidiaries is included in intangible assets. The Group measures goodwill at the acquisition date as the total of:

- the fair value of the consideration transferred; less - the net recognised amount (generally fair value) of the identifiable assets acquired and liabilities assumed.

When this total is negative, it is recognised immediately in profit or loss.

Consolidated goodwill is measured at cost less accumulated amortisation and accumulated impairment losses. Goodwill will be amortised over the useful economic life of 20 years.

(e) Loans and advances

Advances cover loans, overdrafts and other methods of extending credit to borrowers.

Advances, net of amounts written off, are recorded in the balance sheet on the basis of the cost of the amount of the advance outstanding, less suspended interest debited to the customers’ account, specific and general provisions.

Specific provisions are made for advances which are recognised to be impaired. A loan is impaired when, based on current information and events, the Bank considers that the creditworthiness of the borrower has undergone a deterioration such that it no longer expects to recover the advance in full. Provisions made during the year are charged to revenue, net of recoveries. When there is no further likelihood of recovery, the remaining balance is written off. General provisions are also maintained at 1% of the customers exposure consisting of performing loans and advances, and acceptances outstanding under letters of credit. When a subsequent event (i.e. repayment by a debtor) causes the amount of impairment loss to decrease, the decrease in impairment loss is reversed through profit and loss.

(f) Foreign currencies

Transactions in foreign currencies are recorded at the rate ruling at the date of the transaction. Monetary assets and liabilities denominated in foreign currencies are translated into sterling at the exchange rates ruling at the balance sheet date. Surpluses and deficits arising on translation are accounted for in the profit and loss account for the year.

(g) Debt securities

Investments held to maturity are shown in the balance sheet at cost plus any discounts earned up to the balance sheet date or minus any premiums charged against profit as at the balance sheet date, less any provision for permanent impairment.

Where debt securities are purchased at a premium or discount, those premiums and discounts are amortised through the profit and loss account over the remaining maturity, using the straight line method.

(h) Depreciation and amortisation

Fixed assets are stated at cost less accumulated depreciation. Depreciation is computed using the straight line method. Rates applicable are as follows:

Nature of assets Rate of depreciation / amortisation

Buildings: Freehold properties 5%

Leasehold improvements 10% & over lease period

Furniture, fixtures and office equipment 10 - 20%

Computer software and hardware 20 - 33%

Goodwill 20 years

Depreciation is charged on fixed assets from the month these are brought into use, whereas no depreciation is charged on assets during the month of disposal.

Fixed assets that are unserviceable are written off and their book value charged to the profit and loss account in the year in which the write off takes place. Gains or losses on the disposal of fixed assets are taken to the profit and loss account.

(i) Derivative contracts

Derivative instruments used by the Group are forward exchange contracts. The Group does not enter into speculative derivative contracts. All such contracts are generally executed on behalf of customers.

Derivatives are initially recognised at fair value at the date a derivative contract is entered into and are subsequently re-measured to their fair value at each balance sheet date. The resulting gain or loss is recognised in profit or loss immediately based on market observable parameters.

(j) Claims and litigation

Provisions for restructuring costs and legal claims are recognised when the Group has a present legal or constructive obligation as a result of past events; it is more likely than not that an outflow of resources will be required to settle the obligation and the amount can be reliably estimated.

(k) Deferred taxation

Deferred taxation is recognised in accordance with FRS 19 “Deferred Tax” and in respect of timing differences that have originated but not reversed at the balance sheet date where transactions or events that result in an obligation to pay more tax in the future or a right to pay less tax in the future have occurred at the balance sheet date.

Deferred tax assets are regarded as recoverable and recognised in the financial statements to the extent that, on the basis of available evidence, it is more likely than not that there will be suitable taxable profits from which the future reversal of the timing difference can be deducted.

(l) Pension obligations

The Group operates a defined pension contribution arrangement and cost is recognised as and when contributions are made.

(m) Revenue recognition

Interest income is recognised in the profit and loss account as it accrues other than interest of doubtful collectibility which is credited to a suspense account and excluded from interest income. The balance on the suspense account is netted in the balance sheet against the amount debited to the borrower. Suspended interest is written off when there is no longer any realistic prospect of it being recovered.

Fees receivable which represent a return for services provided or risk borne or which are in the nature of interest are credited to income when the related service is performed or over the period of the transaction, depending on the nature of the income.

Dealing profits represent profits or losses on foreign exchange transactions.

(n) Leases

The Group enters into operating leases as referred to in note 3. Rentals under operating leases are charged on a straight line basis over the lease term. The Group has not entered into any finances leases during the year.

(o) Offsetting financial assets and financial liabilities

Financial assets and liabilities are offset and the net amount reported in the Balance Sheet when, in the event of default, the Group has a legal right to set off the recognised amounts and intends to settle on a net basis.

Income and expenses are presented on a net basis only when permitted by the accounting standards, or for gains or losses arising from a group of similar transactions.

AN

NU

AL REPO

RT - 2011

15

(p) Fiduciary activities

The Group commonly acts as trustee and in other fiduciary capacities that result in the holding or placing of assets on behalf of individuals and other institutions. Assets held in trust and fiduciary accounts do not become assets or liabilities of the Group and are segregated from the Group’s assets.

Year ended 31 December

2011£’000

Year ended 31 December

2010£’000

2 Administrative expenses

Staff costs:Wages, salaries and allowancesSocial security costsOther pension costs

Other administrative expenses

5,692

704 293

4,453

3,659

373 164

2,811

11,142 7,007

The average number of persons (including part-time employees) employed by the Group during the period was 159 (2010: 82). The total number of persons employed at 31 December 2011 was 153 (2010: 84).

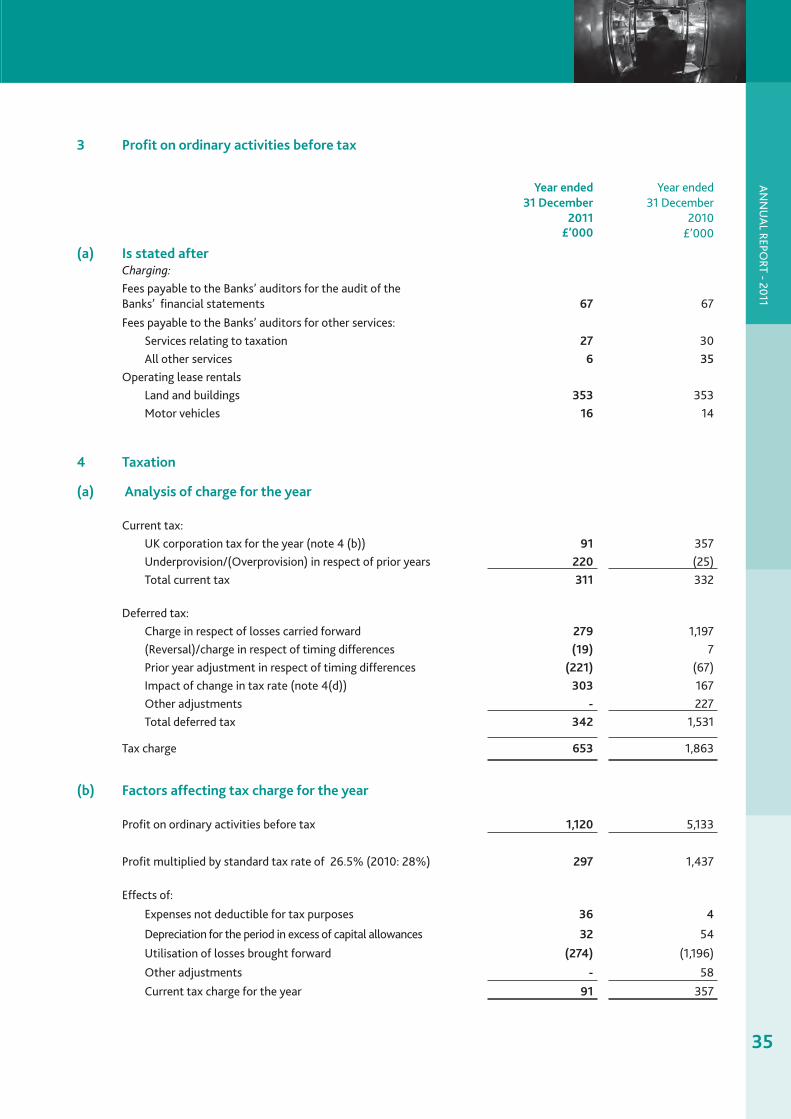

3 Profit on ordinary activities before tax

(a) Is stated after

Charging:

Fees payable to the Group’s auditors for the audit of the Group’s financial statementsFees payable to the Group’s auditors for other services:

Services relating to taxationAll other services

Operating lease rentalsLand and buildingsMotor vehicles

131

27 30

820

16

67

30 35

353

14

Year ended 31 December

2011£’000

Year ended 31 December

2010£’000

4 Taxation

(a) Analysis of charge for the year

Current tax:UK corporation tax for the year (note 4(b))Less: relief for foreign tax suffered Under provision in respect of prior years

172

(41) 220

357

- (25)

Total current taxForeign tax for current year

351 41

332 -

Total current tax 392 332

Deferred tax:Charge in respect of losses carried forward(Reversal)/charge in respect of timing differencesPrior year adjustment in respect of timing differencesImpact of change in tax rate (note 4(d))Other adjustments

279

(196)(207)

299 -

1,063

7 67

167 227

Total deferred tax 175 1,531

Tax charge 567 1,863

(b) Factors affecting tax charge for the year

Profit on ordinary activities before tax 712 5,133

Profit multiplied by standard tax rate of 26.5% (2010: 28%)

Effects of:Expenses not deductible for tax purposesDepreciation for the period in excess of capital allowancesUtilisation of losses brought forwardOther adjustments

189

224 33

(274)-

1,437

4 54

(1,196)58

Current tax charge for the year 172 357

(c) Factors that may affect the future tax charge

Since the Group is a 90.5% owned subsidiary of Habib Bank Limited, and has been granted the status of an authorised institution under the UK Financial Services and Markets Act 2000 by the Financial Services Authority, the assessed trading losses brought forward by Habib Bank Limited are available to offset against the future profits arising on the former activities of Habib Bank Limited. Corporation Tax returns have been agreed up to the year ended 31 December 2008 with HM Revenue and Customs. Tax losses amounting to £24,169,000 were unutilised as at that date (2009: £24,636,000 unutilised as at 31 December 2007). It is estimated that tax losses of £14,131,000 are unutilised as at 31 December 2011 (2010: £16,442,000).

As at 31 December 2010, based on the previous profitability of the Group and on the business plan for the five years to December 2015 (which forecasts that this profitability would continue), the directors decided that they should recognise a deferred tax asset of £4,279,000. As at 31 December 2011, based on this continued profitability, and on the business plan for the five years to 31 December 2016 which demonstrates that the Group will continue to be profitable over that period, the directors have decided that they should recognise a total deferred tax asset of £4,051,000. The deferred tax asset is expected to be reversed over the period of three to five years.

During the year an amount of £175,000 in respect of losses carried forward and timing differences has been recognised

AN

NU

AL REPO

RT - 2011

17

as a deferred tax charge against current year profit.

(d) The Emergency Budget on 22 June 2010 announced that the UK corporation tax rate will reduce from 28% to 24% over a period of 4 years from 2011. The Finance (No 2) Act 2010 enacted a 1% reduction in the UK corporation tax rate to 27% with effect from April 2011. In the budget announcement 23 March 2011, a further 1% reduction in the rate of UK corporation tax to 26% was announced and subsequently enacted on 29 March 2011. The Finance Act 2011 received Royal Assent on 19 July 2011 and also enacted an additional 1% reduction to the UK corporation tax with effect from April 2012. The Group has recognised deferred taxation at 25% and the current tax charge has been calculated at 26.5%. A further reduction of 1% in the tax rate will reduce the Group’s future current tax charge and reduce the Group’s deferred tax charge accordingly.

Year ended 31 December

2011£’000

Year ended 31 December

2010£’000

5 Emoluments of directors

Directors’ fees and emoluments 728 619Pension contributions 20 28

748 647

The total remuneration and benefits of the highest paid director were 272 375

Benefits under defined contribution pension arrangements accrued during the year to 4 Directors (2010: 2 Directors)

6. Debt securities - Held to maturity

2011 £’000

2010 £’000

Investment securities

Listed Government securities 63,870 26,151Others 95,841 65,829

159,711 91,980

(a) Market value

Market value of investments excluding impaired investments as at 31 December 2011 is £158,306,217 (2010 : £92,103,000).

(b) Debt securities movement 2011£’000

2010£’000

(Discount)/ Premium

£’000

Carrying value £’000

(Discount)/ Premium

£’000

Carrying value

£’000

At 31 December 2010 / 2009 182 91,980 62 45,677On acquisition (26) 6,838 - -

New investments 902 126,297 154 64,087Exchange adjustments 36 (132) (13) (40)Matured / disposed of during the year (445) (65,272) (21) (19,219)Reversal of impairment provision - - - 3,000Dividends received during the year - - - (1,381)Written off during the year - - - (144)

At 31 December 2011 / 2010 649 159,711 182 91,980

7 Tangible fixed assetsFreehold property

Leasehold improvements

Computers, furniture,

fixtures & equipment

Total

Cost or valuation

At 31 December 2010 1,778 1,575 961 4,314On acquisition - 873 3,222 4,095

Additions 47 163 167 377Disposals - (92) (186) (278)

At 31 December 20111,825 2,519 4,164 8,508

Accumulated depreciation and amortisation

At 31 December 2010 372 964 670 2,006On acquisition - 387 2,734 3,121

Charge for the year 94 77 259 430Depreciation on disposal - (56) (143) (199)

At 31 December 2011 466 1,372 3,520 5,358

Net book value at 31 December 2011 1,359 1,147 644 3,150

£’000 £’000£’000£’000

AN

NU

AL REPO

RT - 2011

19

8 Intangible assets - goodwill

2011£’000

2010£’000

Goodwill (a) 11,152 - Less: Amortisation (372) -

10,780 -

(a) During the year the Group acquired control of another UK incorporated bank, Habibsons Bank Limited through a 100% equity purchase. The transaction was completed on 20 April 2011 through a Sale and Purchase Agreement (SPA) signed between the Group, Valona Finance and the guarantors to the transaction. The amount paid as a consideration is subject to any potential warranties and indemnities that the purchaser may claim in the time period stipulated in the SPA. The above amount represents the amount paid as goodwill which is to be amortised over a period of 20 years and was calculated as below.

Note 20 April 11

Book Value£’000

Fair Value £’000

AssetsCash and balances at central banks 787 787Treasury bills and other eligible bills 7,439 7,439Loans and advances to banks 163,436 163,436Loans and advances to customers 77,626 77,173Tangible fixed assets 1,003 1,003Other assets 550 550Prepayments and accrued income 641 736

251,482 251,124

LiabilitesDeposits by banks 13,697 13,697Customer accounts 211,970 211,970Other liabilities 1,067 1,067Accruals and deferred income 926 926Subordinated liabilities - loan 3,660 3,660

231,320 231,320

Called up share capital 14,000 14,000Revaluation reserve (6) (6)Profit & loss account 6,168 5,810

Net book value 20,162 19,804

Investment at cost as per holding company accounts 30,956

Goodwill 8 11,152

Habibsons Bank made a profit of £6,000 from the beginning of its financial year 01 January 2011 to the date of acquisition 20 April 2011. In its previous financial year ended on 31 December 2010 its profit was £264,000.

9 Deferred tax asset

2011£’000

2010£’000

The movement in the year was as follows:

Beginning of the year 4,279 5,810On acquisition (53) -

Deferred tax charge recognised during the period (175) (1,531)

End of the year4,051 4,279

10 Other assets

Corporation tax - 219

Unrealised gain on forward contracts 159 -

Other assets 1,796 537

1,955 756

11 Other liabilities

Corporation tax 110 - Other liabilities 2,760 1,204

2,870 1,204

12 Provision for loan losses

Provisions Loans & advances 2011 2010Specific General Total Total

£ ‘000 £ ‘000 £ ‘000 £ ‘000

At 31 December 2010 4,848 1,033 5,881 5,692On acquisition 796 - 796 -

Provisions for the year 1,495 376 1,871 189Exchange adjustment 2 - 2 -

At 31 December 2011 7,141 1,409 8,550 5,881

(note 4)

AN

NU

AL REPO

RT - 2011

21

13 Share capital

2011£’000

2,010 £’000

Authorised

50,000 50,000

Allotted, called up and fully paid

25,000 25,000

14 Subordinated liabilities

Subordinated liabilities - Loans 14 (a) 6,440 - 14 (b) 21,254 21,17814 (c) 3,887 -

31,581 21,178

(a) During the year the Group has issued subordinated debt of $10,000,000 (equivalent to £6,440,000) to the parent Habib Bank Limited. These notes are perpetual and are repayable at the option of the Group after five years have passed from the date of issuance. The Financial Services Authority (FSA) classifies this as upper Tier II capital and approval from them is required prior to any repayment. Interest is payable on a six monthly basis at the rate of 5.75% per annum plus six month USD LIBOR.

(b) The Group has issued subordinated debt of $33,000,000 (equivalent to £21,254,000) to the parent Habib Bank Limited (2010: £21,178,000). These notes are perpetual and are repayable either at the option of the Group or five years after receipt of a repayment notice from the note holder. The Financial Services Authority (FSA) classifies this as lower Tier II capital and approval is required prior to repayment. Interest is payable on a six monthly basis at the rate of 5.5% per annum plus six month USD LIBOR.

(c) During 2010 the Group’s subsidiary issued a subordinated loan of $6,000,000. This is repayable in 2020 and carries interest at 2.00% per annum plus three month USD LIBOR. The loan is subordinated to the claims of depositors and other creditors. The Financial Services Authority (FSA) classifies this as lower Tier II capital and approval is required prior to repayment.

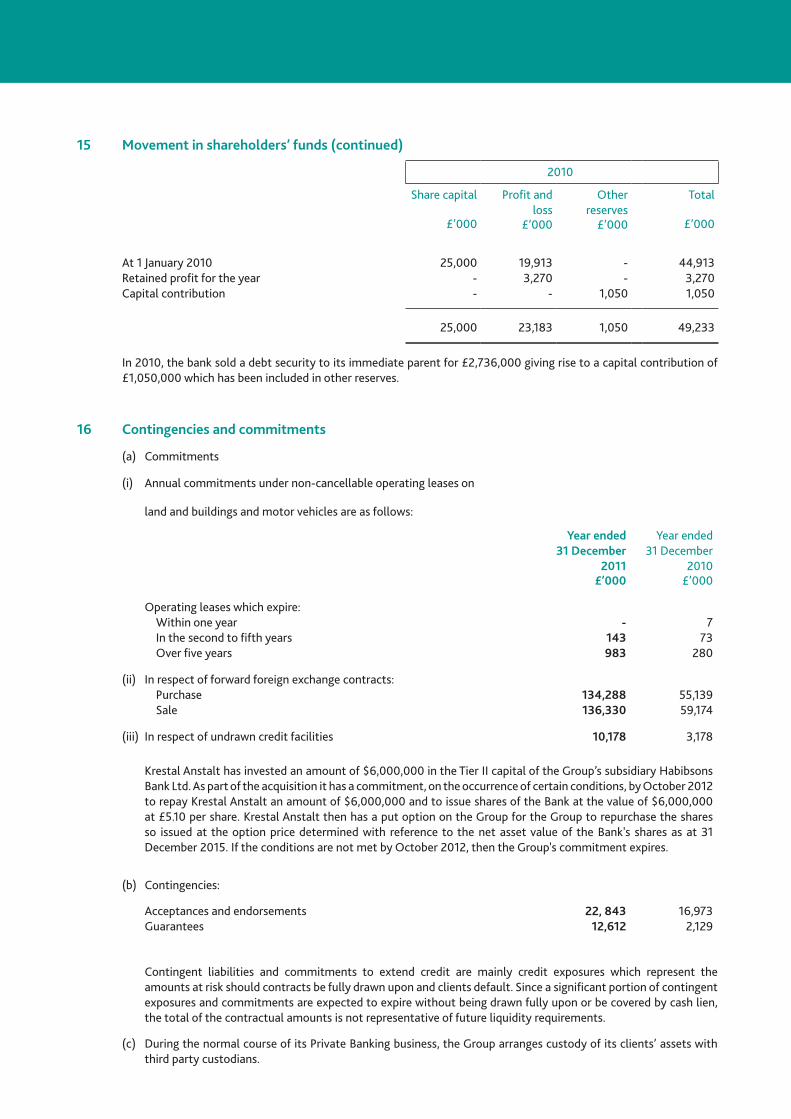

15 Movement in shareholders’ funds

2011

Share capital

£’000

Profit and loss

£’000

Other reserves

£’000

Total

£’000

At 1 January 2011 25,000 23,183 1,050 49,233Retained profit for the year - 145 - 145

25,000 23,328 1,050 49,378

Ordinary shares of £1 each

Ordinary shares of £1 each

15 Movement in shareholders’ funds (continued)

2010

Share capital

£’000

Profit and loss

£’000

Other reserves

£’000

Total

£’000

At 1 January 2010 25,000 19,913 - 44,913Retained profit for the year - 3,270 - 3,270Capital contribution - - 1,050 1,050

25,000 23,183 1,050 49,233

In 2010, the bank sold a debt security to its immediate parent for £2,736,000 giving rise to a capital contribution of £1,050,000 which has been included in other reserves.

16 Contingencies and commitments

(a) Commitments

(i) Annual commitments under non-cancellable operating leases on

Year ended 31 December

2011 £’000

Year ended 31 December

2010 £’000

Operating leases which expire:Within one yearIn the second to fifth yearsOver five years

-

143 983

7

73 280

(ii) In respect of forward foreign exchange contracts:PurchaseSale

134,288 136,330

55,139 59,174

(iii) In respect of undrawn credit facilities 10,178 3,178

Krestal Anstalt has invested an amount of $6,000,000 in the Tier II capital of the Group’s subsidiary Habibsons Bank Ltd. As part of the acquisition it has a commitment, on the occurrence of certain conditions, by October 2012 to repay Krestal Anstalt an amount of $6,000,000 and to issue shares of the Bank at the value of $6,000,000 at £5.10 per share. Krestal Anstalt then has a put option on the Group for the Group to repurchase the shares so issued at the option price determined with reference to the net asset value of the Bank's shares as at 31 December 2015. If the conditions are not met by October 2012, then the Group's commitment expires.

(b) Contingencies:

Acceptances and endorsementsGuarantees

22, 843 12,612

16,973 2,129

Contingent liabilities and commitments to extend credit are mainly credit exposures which represent the amounts at risk should contracts be fully drawn upon and clients default. Since a significant portion of contingent exposures and commitments are expected to expire without being drawn fully upon or be covered by cash lien, the total of the contractual amounts is not representative of future liquidity requirements.

(c) During the normal course of its Private Banking business, the Group arranges custody of its clients’ assets with third party custodians.

land and buildings and motor vehicles are as follows:

AN

NU

AL REPO

RT - 2011

23

On 31st October 2011, one of these custodians, MF Global UK Limited, entered Special Administration following an application to the High Court in London by the directors of MF Global UK Limited. The consequence of the Special Administration was the freezing of the client assets held by MF Global UK Limited on behalf of clients of Habibsons.

The Special Administrators are in the process of reviewing the affairs of MF Global UK Limited and are expected to make a determination as to an entitlement for the return of client assets during 2012.

17 Assets and liabilities denominated by currency

2011

Assets

£’000

Liabilities

£’000

Forward exchange contracts

£’000

Shareholders funds &

Reserves£’000

Net Exposure

£’000

GBP 240,577 193,552 2,042 49,378 (311)USD 285,382 286,615 (633) - (1,866)EURO 96,466 94,558 49 - 1937Other currencies 13,703 12,005 (1,458) - 240

636,108 586,730 - 49,378 -

2010

Assets

£’000

Liabilities

£’000

Forward exchange contracts

£’000

Shareholders funds &

Reserves£’000

Net Exposure

£’000

GBP 176,729 131,413 4,035 49,233 118USD 144,683 152,619 7,721 - (215)EURO 60,449 51,338 (9,112) - (1)Other currencies 6,313 3,571 (2,644) - 98

388,174 338,941 - 49,233 -

18 Concentration of credit risk

2011

Loans to customers

Loans to banks

Debt securities

Contingencies Total

Sectoral concentration: £’000 £’000 £’000 £’000 £’000

Textile 9,549 - - 2,585 12,134Construction - - - 812 812Automobile and transportation equipment 7,925 - - - 7,925Financial - 253,257 84,632 10,914 348,803Government - - 63,870 - 63,870Property investments 67,466 - - 1,750 69,216Production and transmission of energy - - - 1,453 1,453Foods, tobacco and beverages 27,437 - - - 27,437General traders 11,726 - - 6,620 18,346

18 Concentration of credit risk (continued)

Individuals 52,102 - - 2,306 54,408Others 23,171 - 11,209 9,015 43,395

199,376 253,257 159,711 35,455

2011

Loans to customers

Loans to banks

Debt securities

Contingencies Total

Geographical concentration: £’000 £’000 £’000 £’000 £’000

Europe 150,461 129,029 127,747 9,070 416,307North America 2,329 42,939 9,884 41 55,193Asia Pacific (including South Asia) 28,592 67,214 8,454 10,180 114,440Africa 15,530 11,361 3,274 12,925 43,090Middle East 618 2,714 5,650 3,239 12,221Australia 96 - 4,702 - 4,798South America 1,750 - - - 1,750

199,376 253,257 159,711 35,455

European exposure primarily pertains to UK, direct and in-direct exposure of £39,465,000 and £271,503,000 respectively. The Bank does not have any direct exposure on Portugal, Ireland, Italy, Greece, and Spain. Indirect exposure to these countries amounts to nil. Direct exposure is the direct investment by the Bank in sovereign papers or debt instrument guaranteed by sovereign.

2010

Loans to customers

Loans to banks

Debt securities

Contingencies Total

Sectoral concentration: £’000 £’000 £’000 £’000 £’000

Textile 9,972 - - - 9,972Construction - - - - -Automobile and transportation equipment 12,972 - - - 12,972Financial - 165,390 59,621 8,711 233,722Government - - 26,151 - 26,151Property investments 47,794 - - - 47,794Production and transmission of energy - - - - -Foods, tobacco and beverages 25,865 - - - 25,865General traders 6,801 - - 4,761 11,562Individuals 16,384 - - - 16,384Others 2,176 - 6,208 5,630 14,014

121,964 165,390 91,980 19,102

AN

NU

AL REPO

RT - 2011

25

18 Concentration of credit risk (continued)

2010

Loans to customers

Loans to banks

Debt securities

Contingencies Total

Geographical concentration: £’000 £’000 £’000 £’000 £’000

Europe 111,473 96,183 76,060 6,468 290,184North America 363 8,343 13,995 818 23,519Asia Pacific (including South Asia) 8,747 52,578 - 7,690 69,015Africa 1,381 6,065 - 3,843 11,289Middle East - 2,221 1,925 283 4,429Australia - - - - - South America - - - - -

121,964 165,390 91,980 19,102

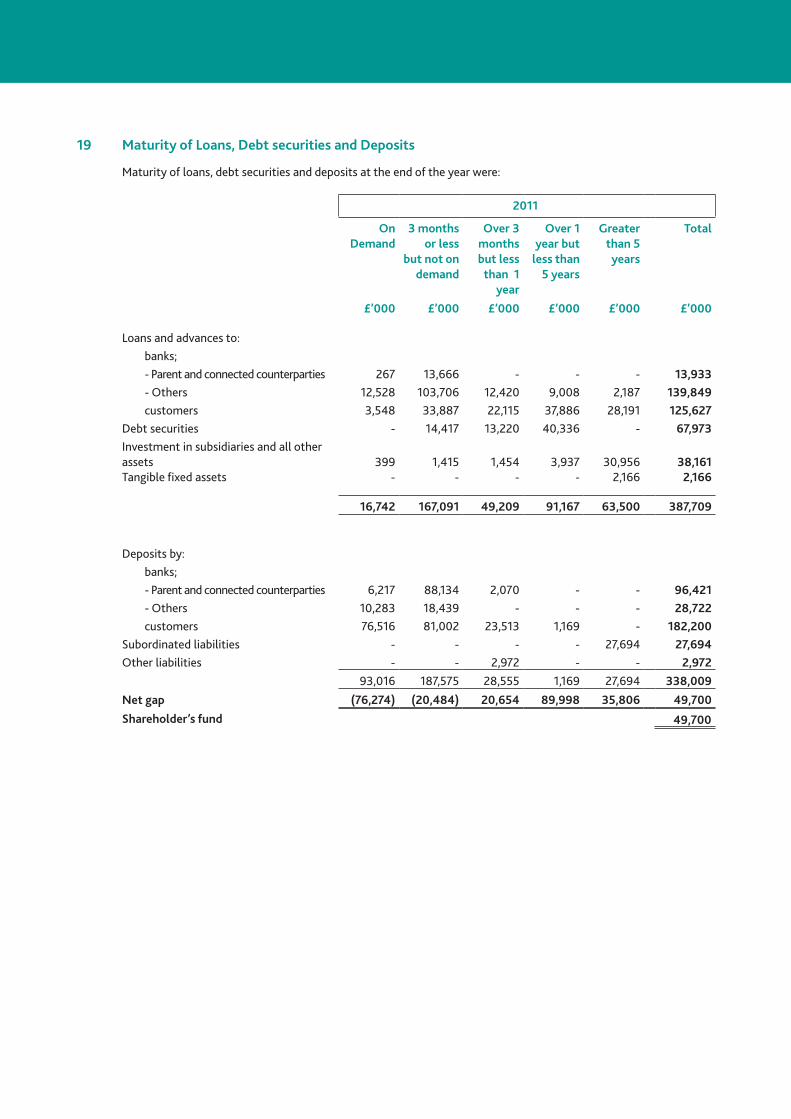

19 Maturity of loans, debt securities and deposits

Maturity of loans, debt securities and deposits at the end of the year were:

2011

On Demand

3 months or

less but not on

demand

Over 3 months but less

than 1 year

Over 1 year but

less than 5 years

Greater than 5 years

Total

£’000 £’000 £’000 £’000 £’000 £’000

Loans and advances to:banks; - Parent 270 13,666 - - - 13,936 - Others 22,762 179,800 21,948 12,624 2,187 239,321customers 10,582 68,355 33,776 54,538 32,125 199,376

Debt securities - 44,749 54,559 60,403 - 159,711Other assets 1,038 1,955 2,790 4,051 10,780 20,614Tangible fixed assets - - - - 3,150 3,150

34,652 308,525 113,073 131,616 48,242 636,108

Deposits by:banks; - Parent 6,217 78,173 2,070 - - 86,460 - Others 14,474 27,337 166 - - 41,977customers 158,835 230,959 31,418 1,169 - 422,381

Subordinated liabilities - - - - 31,581 31,581Other liabilities - - 4,331 - - 4,331

179,526 336,469 37,985 1,169 31,581 586,730

Net gap(144,874) (27,944) 75,088 130,447 16,661 49,378

Shareholder’s fund49,378

19 Maturity of loans, debt securities and deposits

2010

On Demand

3 months or

less but not on

demand

Over 3 months but less than 1

year

Over 1 year but less than

5 years

Greater than 5

years

Total

£’000 £’000 £’000 £’000 £’000 £’000

Loans and advances to:banks; - Parent 1,597 6,222 - - - 7,819 - Others 10,964 115,332 31,267 - 8 157,571customers 6,170 31,262 9,835 43,489 31,208 121,964

Debt securities - 24,099 18,018 47,286 2,577 91,980Other assets 392 756 1,099 4,279 - 6,526Tangible fixed assets - - - - 2,314 2,314

19,123 177,671 60,219 95,054 36,107 388,174

Deposits by:banks; - Parent 4,751 86,577 711 1,600 - 93,639 - Others 7,654 16,731 4,142 - - 28,527customers 72,657 102,908 18,260 135 - 193,960

Subordinated liabilities - - - - 21,178 21,178Other liabilities - - 1,637 - - 1,637

85,062 206,216 24,750 1,735 21,178 338,941

Net gap(65,939) (28,545) 35,469 93,319 14,929 49,233

Shareholder’s fund 49,233

The maturities of loans, debt securities and deposits have been shown according to their contractual maturities except for deposits held under lien which have been classified as per the maturities of the underlying exposure and impaired assets which have been classified in greater than 5 years net of their provision and interest in suspense.

Expected maturity dates do not differ significantly from the contract dates except for the maturity of £291,055,000 (2010: £128,163,000) of deposits representing retail deposit accounts considered by the Group as a stable source of funding of its operations.

AN

NU

AL REPO

RT - 2011

27

20 Interest rate sensitivity gaps

Interest rate risk primarily arises on the mis-matching of the Group’s assets with its funding. Interest rate sensitivity gaps in the Group at the end of the year were:

2011

Not more than

three months

More than

three months but not

more than 6

months

More than six months but not

more than 1

year

More than 1

year but not more

than 5 years

Greater than 5 years

Non interest bearing

Total

£’000 £’000 £’000 £’000 £’000 £’000 £’000

Loans and advances to:banks 216,499 5,422 16,525 11,344 - 3,467 253,257customers 179,001 - - - - 20,375 199,376

Debt securities 95,478 11,829 26,334 26,032 - 38 159,711Other assets - - - - - 23,764 23,764

490,978 17,251 42,859 37,376 - 47,644 636,108

Deposits by:banks 126,201 16 2,220 - - - 128,437customers 394,977 16,361 9,874 1,169 - - 422,381

Subordinated liabilities 3,887 27,694 - - - - 31,581 Other liabilities and Shareholders’ funds - - - - - 53,709 53,709

525,065 44,071 12,094 1,169 - 53,709 636,108

Overall gap (34,087) (26,820) 30,765 36,207 - (6,065) -

Cumulative gap (34,087) (60,907) (30,142) 6,065 6,065 - -

20 Interest rate sensitivity gaps (continued)

2010

Not more than

three months

More than

three months but not

more than 6

months

More than six months but not

more than 1

year

More than 1

year but not more

than 5 years

Greater than 5

years

Non interest bearing

Total

£’000 £’000 £’000 £’000 £’000 £’000 £’000

Loans and advances to:banks 133,996 22,950 7,961 - - 483 165,390customers 101,093 - - - - 20,871 121,964

Debt securities 67,924 - 11,418 10,061 2,577 - 91,980Other assets - - - - - 8,840 8,840

303,013 22,950 19,379 10,061 2,577 30,194 388,174

Deposits by:banks 117,313 4,853 - - - - 122,166customers 176,046 8,092 9,822 - - - 193,960

Subordinated liabilities - 21,178 - - 21,178Other liabilities and Shareholders’ funds - - - - - 50,870 50,870

293,359 34,123 9,822 - - 50,870 388,174

Overall gap 9,654 (11,173) 9,557 10,061 2,577 -

Cumulative gap 9,654 (1,519) 8,038 18,099 20,676 - -

Non interest bearing items comprise shareholders funds, provisions, fixed assets, impaired assets and other assets and liabilities not subject to interest.

21 Related party transactions

The Group is a subsidiary of and is controlled by Habib Bank Limited (HBL), its immediate parent, which is in turn a subsidiary of The Aga Khan Fund for Economic Development (AKFED) SA, the ultimate controlling party and ultimate parent undertaking of the Group. The Group has related party relationships with its immediate parent, subsidiaries and associates of the immediate parent, and key management personnel of the Group and its immediate parent.

Transactions with related parties are executed on the same terms, including interest rates (deposits/advances) and collateral, as those prevailing at the time for comparable transactions with unrelated parties other than those under the terms of employment and loans provided to employees under the staff loan scheme. Pension contributions are made in accordance with the terms of the pension contribution plan.

(20,676)

AN

NU

AL REPO

RT - 2011

29

Year ended 31 December

2011 £’000

Year ended 31 December

2010 £’000

The details of balances with the related parties are as follows:

Borrowing/deposits/Subordinated liabilities from:Immediate parent and associates 114,228 117,619Key management personnel 149 121

Receivable from:Immediate parent and associates 14,012 8,005Key management personnel 686 86Entities controlled by the key management personnel 3,384 978

Acceptances and endorsements related to:Immediate parent and associates 392 2,778

Net forward (purchase)/sale foreign exchange contracts outstanding with:

Immediate parent and associates 341 38

22 Fair value of financial instruments

The fair values of traded investments are based on quoted market prices. Fair value of these investments has been disclosed in note 6.

In the opinion of management, the fair value of the remaining financial assets and liabilities are not significantly different from their carrying values since assets and liabilities are either short-term in nature or in the case of customer loans and deposits are frequently repriced.

23 Management of delinquent debts on behalf of HBL & ABL

The Group is managing delinquent debts on behalf of Habib Bank Limited (“HBL”) and Allied Bank Limited (“ABL”) that arose prior to the transfer of business to the Group in 2001. The loan balances for HBL amounted to £7,496,000 (2010: £24,364,000) and for ABL amounted to £9,000 (2010: £9,000) which were fully provisioned. Other changes in the HBL account include exchange movements of £86,000 (2010: £973,000) on USD loans included in the balance. Any expenses / recoveries on these accounts are attributable to HBL and ABL.

24 Ultimate parent undertaking and parent undertaking of larger group of which the Group is a member

The Group is a subsidiary of Habib Bank Limited, registered in Pakistan, which is in turn a subsidiary of The Aga Khan Fund for Economic Development SA, registered in Switzerland, the ultimate parent undertaking. The smallest and largest group in which the results of the Group are consolidated is that headed by Habib Bank Limited. Copies of the group accounts for Habib Bank Limited can be obtained from Habib Bank Limited, I.I. Chundrigar Road, Karachi, Pakistan. No other group financial statements include the results of the Group.

Profit and Loss AccountFor the year ended 31 December 2011

Note

Year ended 31 December

2011£’000

Year ended 31 December

2010£’000

Interest receivableInterest receivable and similar income arising from debt securities 1,769 1,178

Other interest receivable and similar income 6,297 5,696

8,066 6,874

Interest payable (3,975) (1,838)

Net interest income 4,091 5,036

Fees and commissions receivable 3,964 3,800

Foreign exchange dealing profits 966 973

Other operating income 578 1,058

Total operating income 9,599 10,867

Administrative expenses

Depreciation and amortisation

2

7

(6,704)

(282)

(7,007)

(344)

Total operating expenditure (6,986) (7,351)

2,613 3,516

Provision for loan losses 12 (1,493) (189)Impairment and reversals on debt securities - 1,806

Profit on ordinary activities before tax1,120 5,133

Tax on profit on ordinary activities 4 (653) (1,863)

Profit on ordinary activities after tax 15467 3,270

There are no recognised gains and losses other than the profit for the year as reported above. The result for the year is derived entirely from continuing activities. The notes on pages 32 to 48 form part of these financial statements.

AN

NU

AL REPO

RT - 2011

31

Balance SheetAs at 31 December 2011

Note 2011 2010£’000 £’000

AssetsCash and balances at central banks 399 392Loans and advances to banks 153,782 165,390Loans and advances to customers 125,627 121,964Debt securities 6 67,973 91,980Other assets 10 1,415 756Prepayments and accrued income 1,454 1,099Tangible fixed assets 7 2,166 2,314Investment in subsidiary 8 30,956 - Deferred taxation 9 3,937 4,279

Total assets 387,709 388,174

LiabilitiesDeposits by banks 125,143 122,166Customer accounts 182,200 193,960Other liabilities 11 2,432 1,204Accruals and deferred income 540 433Subordinated liabilities 14 27,694 21,178

Total liabilities 338,009 338,941

Shareholders’ fundsCalled up share capital Profit and loss account Other reserves

13 15 15

25,000 23,650

1,050

25,000 23,183 1,050

49,700 49,233

Total liabilities & Equity387,709 388,174

The notes on pages 32 to 48 form part of these financial statements.

These financial statements were approved by the board of directors on March 12, 2012 and signed on its behalf by:

Anwar Zaidi Chief Executive Officer

Notes to the AccountsThese notes form part of the financial statements1 Accounting policies

The following accounting policies have been applied consistently in dealing with items which are considered material in relation to the Bank’s financial statements.

(a) Basis of preparation

The financial statements cover the year from 1 January 2011 to 31 December 2011 and have been prepared under the historical cost convention and in accordance with the special provisions of Statutory Instrument 2008/410, Schedule 2 of the Companies Act 2006 relating to banking companies, applicable UK mandatory accounting standards and the British Banker’s Association Statements of Recommended Accounting Practice.

The preparation of these financial statements requires management to make estimates and judgements. This is particularly so in the assessment of provisions for bad and doubtful debts and in assessing impairment of debt securities. Making reliable estimates of the ability of customers and other counterparties to repay is often difficult even in periods of economic stability and becomes more difficult in periods of economic volatility. Therefore, while management believes it has utilised all available information to estimate adequate allowances for all identifiable risks in the current portfolios, there can be no assurance that the provisions for bad and doubtful debts or other impairment provisions will prove adequate for all losses ultimately realised.

The Bank’s financial statements have been prepared on the going concern basis which the directors believe to be appropriate as there are no material uncertainties that may cast significant doubt about the bank’s ability to continue as a going concern. This conclusion is based on the following:

Review of the financial performance and outlook, principal risks and risk management as discussed in the Director’s report

Detailed assessments carried out by the management in respect to the key areas of the Bank such as the liquidity, capital management, profit projections and litigation covering a period of twelve months from the date of signing the balance sheet.

The Risk management disclosures as required under Pillar III are available on the Bank’s website: www.habibbankuk.com. These disclosures under the Pillar III include a detailed risk management analysis, Capital Management and details of overdue and impairment exposures.

(b) Loans and advances

Advances cover loans, overdrafts and other methods of extending credit to borrowers.

Advances, net of amounts written off, are recorded in the balance sheet on the basis of the cost of the amount of the advance outstanding, less suspended interest debited to the customers’ account, specific and general provisions.

Specific provisions are made for advances which are recognised to be impaired. A loan is impaired when, based on current information and events, the Bank considers that the creditworthiness of the borrower has undergone a deterioration such that it no longer expects to recover the advance in full. Provisions made during the year are charged to revenue, net of recoveries. When there is no further likelihood of recovery, the remaining balance is written off. General provisions are also maintained at 1% of the customers exposure consisting of performing loans and advances, and acceptances outstanding under letters of credit. When a subsequent event (i.e. repayment by a debtor) causes the amount of impairment loss to decrease, the decrease in impairment loss is reversed through profit and loss.

(c) Foreign currencies

Transactions in foreign currencies are recorded at the rate ruling at the date of the transaction. Assets and liabilities denominated in foreign currencies are translated into sterling at the exchange rates ruling at the balance sheet date. Surpluses and deficits arising on translation are accounted for in the profit and loss account for the year.

(i)

(ii)

AN

NU

AL REPO

RT - 2011

33

(d) Investments

Debt securities

Investments held to maturity are shown in the balance sheet at cost plus any discounts earned up to the balance sheet date or minus any premiums charged against profit as at the balance sheet date, less any provision for permanent impairment.

Where debt securities are purchased at a premium or discount, those premiums and discounts are amortised through the profit and loss account over the remaining maturity, using the straight line method.

Subsidiary

Investments in subsidiaries are stated at cost less any provision for permanent impairment.

(e) Depreciation

Fixed assets are stated at cost less accumulated depreciation. Depreciation is computed using the straight line method. Rates applicable are as follows:

Nature of Assets Rate of Depreciation

Buildings: Freehold properties 5%

Leasehold improvements over lease period

Furniture, fixtures and office equipment 20%

Computer software and hardware 20 - 33%

Depreciation is charged on fixed assets from the month these are brought into use, whereas no depreciation is charged on assets during the month of disposal.

Fixed assets that are unserviceable are written off and their book value charged to the profit and loss account in the year in which the write off takes place.