© 2001 prentice hall business publishing financial accounting, 4/e harrison and horngren 10b-1...

TRANSCRIPT

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-1

CHAPTER 10Part B

Accounting for Long-Term Investments and International Operations

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-2

ACCOUNTING FOR INTERNATIONAL

OPERATIONS

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-3

ACCOUNTING FOR INTERNATIONAL OPERATONS

The exhibit below shows the percentages of international sales for three large U. S. companies:

Company Percent of International Sales

Coca-Cola 62%

IBM 57

Intel 56

Company Percent of International Sales

Coca-Cola 62%

IBM 57

Intel 56

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-4

• Accounting for business activities across national boundaries makes up the field of international accounting

ACCOUNTING FOR INTERNATIONAL OPERATONS

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-5

FOREIGN CURRENCIES AND EXCHANGE RATES

• The measure of one currency against another is called the foreign-currency exchange rate

• Using an exchange rate to convert the cost of an item given in one currency to its cost in a second currency is called a translation

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-6

Foreign-Currency Exchange Rates at One Point in Time

Canada

European Common Market

France

Germany

Great Britain

Italy

Japan

Mexico

Dollar

Euro

Franc

Mark

Pound

Lira

Yen

Peso

$0.66

1.06

0.16

0.54

1.59

0.0005

0.0086

0.107

CountryMonetary

UnitDollarValue

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-7

• If an item costs 200 French francs,its translation to dollars is found by multiplying the amount in francs by the conversion rate: 200 French francs x $0.16 = 32

FOREIGN CURRENCIES AND EXCHANGE RATES

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-8

• Two main factors determine the supply and demand for a particular currency– The ratio of a country’s imports to its

exports• When exports exceed imports, customers must

buy the unit of currency in the international currency market to pay for their purchases

FOREIGN CURRENCIES AND EXCHANGE RATES

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-9

• This demand drives up the price (the foreign exchange rate) of a currency

• Conversely, as the supply of a currency increases, its price decreases

– The rate of return available in the country’s capital market

• The rate of return available in a country’s capital markets affects the amount of investment funds flowing into the country

FOREIGN CURRENCIES AND EXCHANGE RATES

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-10

• When rates of return are high, international investors buy stocks, bonds, and real estate in that country

• This activity increases the demand for the nation’s currency and drives up its exchange rate

• The exchange rate of a strong currency is rising relative to other nations’ currencies

• The exchange rate of a weak currency is falling relative to other currencies

FOREIGN CURRENCIES AND EXCHANGE RATES

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-11

Shipp Belting sells goods to Artes de Mexico for a price of 1 million pesos on July 28. On that date, a peso was worth $0.107. On August 28, when the peso is worth only $0.104, Shipp receives 1 million pesos from Artes, but the dollar value of Shipp’s cash receipt is $3,000 less than expected. The following journal entries show how Shipp would account for these transactions:

July 28 Accounts Receivable - Artes(1,000,000 pesos x $0.107) 107,000

Sales Revenue 107,000

Sale on account

July 28 Accounts Receivable - Artes(1,000,000 pesos x $0.107) 107,000

Sales Revenue 107,000

Sale on account

Aug. 28 Cash (1,000,000 pesos x $0.104) 104,000

Foreign Currency Transaction Loss 3,000

Accounts Receivable - Artes 107,000

Collection on account

Aug. 28 Cash (1,000,000 pesos x $0.104) 104,000

Foreign Currency Transaction Loss 3,000

Accounts Receivable - Artes 107,000

Collection on account

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-12

• Shipp exposed itself to foreign-currency exchange risk and experienced a $3,000 foreign-currency transaction loss

• If the peso had increased in value, Shipp would have experienced a foreign-currency transaction gain

FOREIGN CURRENCIES AND EXCHANGE RATES

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-13

Assume Shipp Belting buys inventory from Gesellschaft Ltd., a Swiss company. The two companies decide on a price of 20,000 Swiss francs. On September 15, when Shipp receives the goods, the Swiss franc is quoted at $0.7999. When Shipp pays on September 29, the Swiss franc has decreased in value to $0.7810. Shipp would record the purchase and payment as follows:

Assume Shipp Belting buys inventory from Gesellschaft Ltd., a Swiss company. The two companies decide on a price of 20,000 Swiss francs. On September 15, when Shipp receives the goods, the Swiss franc is quoted at $0.7999. When Shipp pays on September 29, the Swiss franc has decreased in value to $0.7810. Shipp would record the purchase and payment as follows:

Sept. 15 Inventory (20,000 Swiss francs x $0.7999) 15,980

Accounts Payable - Gesellschaft Ltd. 15,980

Purchase on account

Sept. 15 Inventory (20,000 Swiss francs x $0.7999) 15,980

Accounts Payable - Gesellschaft Ltd. 15,980

Purchase on account

Sept. 29 Accounts Payable - Gesellschaft Ltd. 15,980

Cash (20,000 Swiss francs x $0.781) 15,620

Foreign Currency Transaction Gain 360

Payment on account

Sept. 29 Accounts Payable - Gesellschaft Ltd. 15,980

Cash (20,000 Swiss francs x $0.781) 15,620

Foreign Currency Transaction Gain 360

Payment on account

If the Swiss franc had strengthened against the dollar, Shipp would have had a foreign-currency transaction loss

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-14

• The company reports the net amount of foreign currency transaction gains and losses on the income statement as Other Revenues and Gains, or Other Expenses and Losses

FOREIGN CURRENCIES AND EXCHANGE RATES

OtherOther

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-15

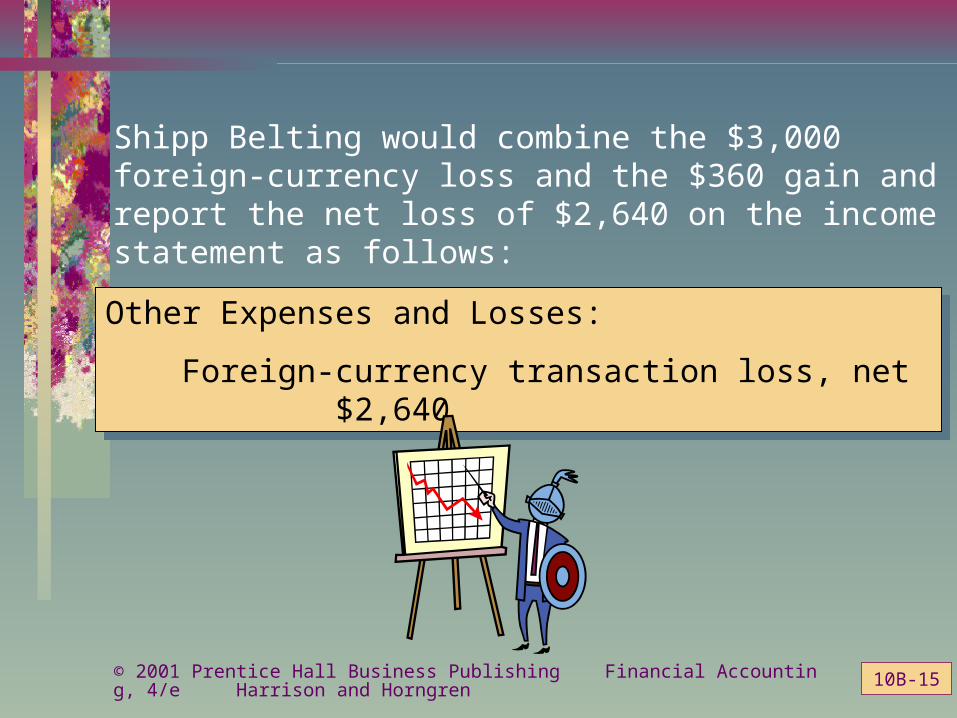

Shipp Belting would combine the $3,000 foreign-currency loss and the $360 gain and report the net loss of $2,640 on the income statement as follows:

Other Expenses and Losses:

Foreign-currency transaction loss, net $2,640

Other Expenses and Losses:

Foreign-currency transaction loss, net $2,640

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-16

• One way for U. S. companies to avoid foreign-currency transaction losses is to insist that international transactions be settled in dollars

• Another way for a company to protect itself is by hedging– Protection from transaction losses by

engaging in a counterbalancing transaction

FOREIGN CURRENCIES AND EXCHANGE RATES

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-17

• Some companies buy futures contracts which are contracts for foreign currencies to be received in the future

• Futures contracts can effectively create a payable to exactly offset a receivable, and vice versa

FOREIGN CURRENCIES AND EXCHANGE RATES

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-18

CONSOLIDATION OF FOREIGN SUBSIDIARIES

• The consolidation of a foreign subsidiary poses two special challenges– Accountants must first bring the

subsidiary’s statements into conformity with American GAAP

– When the subsidiary statements are expressed in foreign currency, they must be translated into dollars

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-19

• The process of translating a foreign subsidiary’s financial statements into dollars usually creates a foreign-currency translation adjustment– Assets and liabilities in the foreign

subsidiaries’ financial statements are translated into dollars at the exchange rate in effect on the date of the statements

– Stockholders’ equity is translated into dollars at the historical exchange rates

CONSOLIDATION OF FOREIGN SUBSIDIARIES

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-20

• The foreign-currency translation adjustment is the balancing amount that brings the dollar amount of the total liabilities and stockholders’ equity of a foreign subsidiary into agreement with the dollar amount of its total assets

CONSOLIDATION OF FOREIGN SUBSIDIARIES

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-21

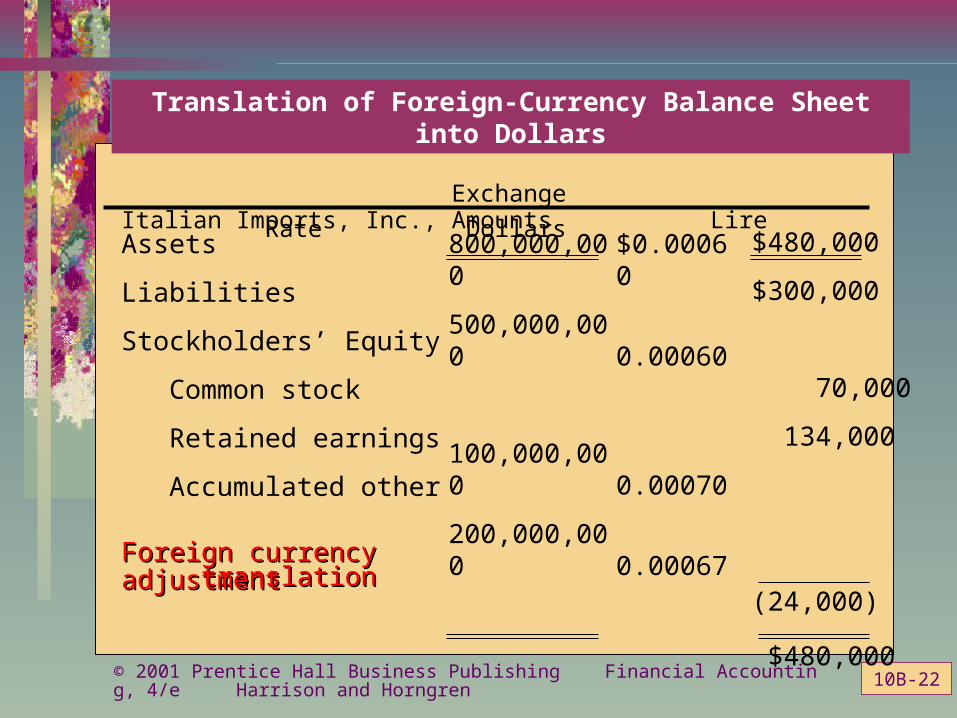

U. S. Express Corporation owns Italian Imports, Inc., whose financial statements are expressed in lire

• When U. S. Express acquired Italian Imports in 20X1, a lira was worth $0.00070

• When Italian Imports earned its retained income during 20X1 - 20X6, the average exchange rate was $0.00067

• On the balance sheet date in 20X6, a lira is worth only $0.00060

The following exhibit shows how to translate Italian Imports’ balance sheet into dollars and shows how the translation adjustment arises:

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-22

Assets

Liabilities

Stockholders’ Equity

Common stock

Retained earnings

Accumulated other

comprehensive income:

Foreign currencyForeign currency translation adjustmenttranslation adjustment

800,000,000

500,000,000

100,000,000

200,000,000

800,000,000

$0.00060

0.00060

0.00070

0.00067

$480,000

$300,000

70,000

134,000

(24,000)

$480,000

ExchangeItalian Imports, Inc., Amounts Lire Rate Dollars

Translation of Foreign-Currency Balance Sheet into Dollars

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-23

United States

Germany

Japan

United Kingdom

Specific unit cost, FIFO, LIFO, weighted average

Similar to U.S.

Similar to U.S.

LIFO is unacceptable for tax purposes and is not widely used

Amortized over period not to exceed 40 years

Amortized over 5 years

Amortized over 5 years

Amortized over useful life or not amortized if life is indefinite

Expensed as incurred

Expensed as incurred

May be capitalized and amortized over 5 years

Expense research cost Some development costs may be capitalized

Country Inventories GoodwillResearch and

Development Costs

Differences in accounting principles exist among countries around the world as shown below:

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-24

INTERNATIONAL ACCOUNTING STANDARDS

• A company that sells its stock through a foreign stock exchange must follow the accounting principles of the foreign country

• The globalization of business enterprises and capital markets is creating much interest in establishing common, worldwide accounting standards

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-25

• The primary organization working to achieve worldwide harmony of accounting standards is the International Accounting Standards Committee (IASC)

INTERNATIONAL ACCOUNTING STANDARDS

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-26

USING THE SCF TO INTERPRET INVESTING ACTIVITIES

• The purchase and sale of investments in the stocks and bonds of other companies are investing activities that are reported on the cash-flow statement

• Investing activities are on the statement of cash flows as the second category, as shown in the following exhibit:

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-27

Cash Flows from Operating Activities 1. Net cash provided by operating activities $ 1,185

Cash Flows from Investing ActivitiesCash Flows from Investing Activities 2. Purchases of plant assets2. Purchases of plant assets (391) (391) 3. Sales of plant assets3. Sales of plant assets 21 21 4. Businesses acquired4. Businesses acquired (1,255) (1,255) 5. Sales of businesses5. Sales of businesses 12 12 6. Other6. Other (45) (45) 7. Net cash used in investing activities7. Net cash used in investing activities (1,658) (1,658)

Cash Flows from Financing Activities 8. Long-term borrowings 312 9. Repayments of long-term borrowings (29)10. Short-term borrowings 1,08711. Repayments of short-term borrowings (662)12. Dividends paid (295)13. Other 1314. Net cash provided (used in) financing activities 426

CAMPBELL SOUP CO.Consolidated Statement of Cash Flows

(In millions) 19X5

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-28

• Campbell Soup spent $1.255 billion to acquire other companies (line 4)

• It sold other companies for a total of $12 million (line 5)

• Campbell Soup financed acquisitions of other businesses through operating activities (line 1)

USING THE SCF TO INTERPRET INVESTING ACTIVITIES

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-29

• Long-term borrowing (line 8) and short-term borrowing (line 10) far exceeded repayments of borrowings (lines 9 and 11)– This means that the company had the cash

to expand

USING THE SCF TO INTERPRET INVESTING ACTIVITIES

© 2001 Prentice Hall Business Publishing Financial Accounting, 4/e Harrison and Horngren

10B-30

END OF CHAPTER 10

Harrison &

Horngren