introduction to financial accounting, 10e...

TRANSCRIPT

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

Introduction to Financial Accounting, 10e (Horngren) Chapter 2 Measuring Income to Assess Performance

Learning Objective 2.1 Questions

2.1-1) Net income isA) the only way to evaluate for-profit corporations.B) not appropriate for individuals.C) not applicable to not-for-profit entities.D) the bottom line according to IRS accounting.E) the primary way of evaluating the financial performance for an entity.Answer: EDiff: 1Objective: L.O. 2-1

2.1-2) Revenues areA) increases in liabilities resulting from delivering goods or services to customers.B) decreases in assets resulting from delivering goods or services to customers.C) increases in retained earnings resulting from delivering goods or services to customers.D) decreases in retained earnings resulting from delivering goods or services to customers.E) another term for assets.Answer: CDiff: 2Objective: L.O. 2-1

2.1-3) For which company would it seem sensible to use a fiscal year ending on June 1?A) A landscaping companyB) A clothing retailerC) A swimming pool retailerD) A snow blower sellerE) A law firmAnswer: DDiff: 2Objective: L.O. 2-1

2.1-4) Alfano Industries sold inventory costing $300 for $500 on account. If Alfano Industries operates under the accrual basis, what effect will this transaction have on the owners' equity side of the balance sheet?A) None, since the customer to whom the inventory was sold has not yet paidB) None, since sales and/or cost of goods sold are income statement accountsC) Decrease owners' equity by $300D) Increase owners' equity by $200E) Increase owners' equity by $800Answer: DDiff: 3Objective: L.O. 2-1

1Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

2.1-5) An accountant records a transaction when cash is paid or received under which basis of accounting?A) CashB) AccrualC) DeferralD) PrepaidE) Cost recoveryAnswer: ADiff: 1Objective: L.O. 2-1

2.1-6) Which of the following circumstances would result in a decrease in income under the accrual basis but would not result in a decrease in income under the cash basis?A) Purchase of inventory on accountB) Payment of 2 months' rent in advanceC) The expiration of prepaid rentD) The return of defective inventory purchased on account, where full credit was givenE) The payment of the current period's utility billAnswer: CDiff: 3Objective: L.O. 2-1

2.1-7) Bairas Salon records revenue as cash is received. Which method of income measurement is Bairas Salon using?A) The accrual basisB) The cash basisC) The recognition basisD) The revenue basisE) The realization basisAnswer: BDiff: 2Objective: L.O. 2-1

2.1-8) Which of the following circumstances would result in an increase in income under the cash basis and an increase in income under the accrual basis?A) The return of defective inventory purchased on account, where full credit was givenB) Cash collection from a credit customerC) The cash sale of inventory at a sales price in excess of costD) The expiration of prepaid rentE) The sale of inventory on account, at a sales price in excess of costAnswer: CDiff: 3Objective: L.O. 2-1

2Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

2.1-9) Which of the following circumstances would result in a decrease in income under both the accrual and cash basis?A) The payment of last period's utilitiesB) The payment of this period's utilitiesC) The payment of next period's utilitiesD) The cash purchase of inventoryE) The purchase of inventory on accountAnswer: BDiff: 2Objective: L.O. 2-1

2.1-10) The operating cycle is the time it takes for a company to buy goods.Answer: FALSEDiff: 1Objective: L.O. 2-1

2.1-11) Because of the difficulty of measuring income, there is no reason to compare income levels between different companies.Answer: FALSEDiff: 1Objective: L.O. 2-1

2.1-12) The additional owners' equity generated by income or profits is known as retained earnings.Answer: TRUEDiff: 1Objective: L.O. 2-1

2.1-13) Because net income is the excess of revenues over expenses, retained earnings increases by the amount of net income reported during the period less any dividends.Answer: TRUEDiff: 1Objective: L.O. 2-1

2.1-14) Net income is a measure of the entity's performance in generating net assets.Answer: TRUEDiff: 2Objective: L.O. 2-1

2.1-15) According to accounting rules, fiscal years are required to be established over calendar years.Answer: FALSEDiff: 1Objective: L.O. 2-1

2.1-16) An interim period is a time span that is less than a year and is established for accounting purposes.Answer: TRUEDiff: 1Objective: L.O. 2-1

3Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

2.1-17) For revenue to be earned under the cash basis of accounting, the cash from the customer must be received.Answer: TRUEDiff: 1Objective: L.O. 2-1

2.1-18) Cash for services performed in 20X8 is received in 20X9. Using the accrual basis of accounting, the revenue would appear on the 20X9 income statement.Answer: FALSEDiff: 2Objective: L.O. 2-1

2.1-19) Revenue is produced when accounts receivable are collected under the cash basis of accounting.Answer: TRUEDiff: 1Objective: L.O. 2-1

2.1-20) Under the accrual method, revenue is produced when cash is collected.Answer: FALSEDiff: 1Objective: L.O. 2-1

2.1-21) The accrual basis of accounting is a better measure of economic performance than the cash basis.Answer: TRUEDiff: 1Objective: L.O. 2-1

2.1-22) Why doesn't the cash basis of accounting require adjusting accounts with accruals?Answer: The cash basis of accounting only records revenues and expenses when cash changes hands, while the accrual basis of accounting recognizes revenues when they are earned and expenses when they are incurred. Adjustments are necessary under the accrual basis of accounting since revenue can be earned and expenses can be occurred regardless of when cash is received.Diff: 2Objective: L.O. 2-1

2.1-23) Describe the advantages of the accrual basis of accounting and the cash basis of accounting.Answer: The cash basis of accounting has the advantage of producing financial statements when cash is received, giving users a clearer picture of the company's cash position. Proponents suggest that this is important since companies can appear to be doing well based on net income, yet go bankrupt for a lack of cash. The accrual basis of accounting has the advantage of producing a more complete summary of the entity's value-producing activities since it recognizes revenues when they are earned and expenses when they are incurred.Diff: 2Objective: L.O. 2-1

4Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

Learning Objective 2.2 Questions

2.2-1) The recognition of revenues requires thatA) revenue be earned and realized.B) revenue be realized only.C) revenue be earned only.D) revenue be received in the form of cash.E) revenue be received in a timely fashion.Answer: ADiff: 2Objective: L.O. 2-2

2.2-2) Which of the following is an example of revenue that may be realized but not yet earned?A) A customer paying in advance for services to be performed in the futureB) A credit sale made to a customer who has a prior history of previous sales and collection of the cash from those salesC) A credit sale made to a customer with a weak credit history such that the collection of the outstanding receivable is questionableD) The cash sale of a fixed asset, as opposed to the sale of inventoryE) It is impossible to have revenue which is realized but not earned.Answer: ADiff: 3Objective: L.O. 2-2

2.2-3) Performing a service and immediately collecting the cash wouldA) increase net income.B) decrease assets.C) increase liabilities.D) decrease expenses.E) decrease revenue.Answer: ADiff: 1Objective: L.O. 2-2

2.2-4) Better Mulch Services is a local landscaping company specializing in mulching outdoor landscaping beds. When should Better Mulch Services recognize revenue from its mulching service?A) When the customer calls for mulch deliveryB) When the invoice is mailed to the customerC) When the mulch is delivered to the customerD) When the payment is received from the customerE) When the financial statements are prepared that includes this saleAnswer: CDiff: 2Objective: L.O. 2-2

5Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

2.2-5) Weber Phone Company sells phones and related accessories. Which of these situations demonstrate proper revenue recognition for Weber Phone Company?A) Rent is paid a month in advance of the due date because the accountant will be on vacation when the next rent payment should be made.B) Phones are sold to customers, but customers can opt to have the additional charges added to their next monthly bill.C) Phones are purchased for sale to customers, but the accountant has not yet paid the bill.D) An interest bearing certificate of deposit is purchased. Interest will be paid at the end of 60-day note.E) Employees are paid for hours worked last month.Answer: BDiff: 2Objective: L.O. 2-2

Learning Objective 2.3 Questions

2.3-1) Nordmann, Inc., purchased equipment for $18,000 on January 1, 20X9, and believes the equipment has a useful life of 72 months. What will be the effect of the equipment's depreciation on the balance sheet equation?A) Decreases the asset account of Equipment and decreases Stockholders' EquityB) Decreases the asset account of Equipment and increases Stockholders' EquityC) Increases the asset account of Equipment and decreases Stockholders' EquityD) Increases the asset account of Equipment and increases Stockholders' EquityE) There is no effect on the balance sheet equation.Answer: ADiff: 2Objective: L.O. 2-3

2.3-2) Expenses areA) increases in assets resulting from operations.B) decreases in retained earnings resulting from operations.C) increases in liabilities resulting from purchasing assets.D) increases in retained earnings resulting from operations.E) increases in equity resulting from operations.Answer: BDiff: 2Objective: L.O. 2-3

2.3-3) The recording of expenses in the same time period as the related revenues are recognized is known asA) cost recovery.B) realization.C) matching.D) recognition.E) period costs.Answer: CDiff: 2Objective: L.O. 2-3

6Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

2.3-4) Which of the following costs are identified directly as expenses of the time period in which they are incurred?A) Product costsB) Period costsC) Both product and period costsD) Neither product nor period costsE) Period costs as long as the goods have not been soldAnswer: BDiff: 2Objective: L.O. 2-3

2.3-5) One year's worth of insurance is paid in advance. The accountant records the payment as an asset, Prepaid Insurance, and expenses 1/12 of the amount each month as Insurance Expense. This is an example of which of the following concepts?A) RecognitionB) NeutralityC) RealizationD) MatchingE) Product costsAnswer: DDiff: 2Objective: L.O. 2-3

2.3-6) Which of the following accounts may be thought of as stored costs that are carried forward to future periods rather than immediately charged against revenue?A) Prepaid rentB) Rent expenseC) Advertising expenseD) Depreciation expenseE) Cost of goods soldAnswer: ADiff: 1Objective: L.O. 2-3

2.3-7) What is the effect on a company's balance sheet equation when depreciation expense is recognized?A) This transaction affects only the income statement, so no change on the balance sheet will occur.B) Total assets and total stockholders' equity will decrease by the same amount.C) There will be no change in the total assets, liabilities, and stockholders' equity account.D) Total liabilities will increase and total stockholders' equity will decrease by the same amount.E) Without knowing the exact dollar amount of depreciation, the effect on the balance sheet cannot be determined.Answer: BDiff: 3Objective: L.O. 2-3

7Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

2.3-8) When a portion of prepaid rent expires, what will be the effect on the balance sheet equation?A) This transaction affects only the income statement, so there will be no effect on the balance sheet.B) There will be no overall effect on total assets, because two different asset accounts will change by the exact dollar amount, with one increasing and the other decreasing.C) Total assets and total liabilities will go down by the exact same dollar amount.D) Total assets and total stockholders' equity will go down by the exact same dollar amount.E) Without knowing the dollar amount of the transaction, the effect on the balance sheet equation cannot be determined.Answer: DDiff: 3Objective: L.O. 2-3

2.3-9) Which of the following costs may be shown on the balance sheet?A) Product costsB) Period costsC) Both product and period costsD) R&D costsE) Product costs, as long as the goods have been soldAnswer: ADiff: 2Objective: L.O. 2-3

2.3-10) On September 1, 20X9, Beard Entertainment paid $4,000 for September, October, November and December's rent in advance. The company recorded this transaction by increasing the balance in the Prepaid Rent account. The balance in the Prepaid Rent account as of October 31, 20X9, will beA) $-0-.B) $1,000.C) $2,000.D) $3,000.E) $4,000.Answer: CDiff: 2Objective: L.O. 2-3

2.3-11) On May 1, 20X9, the Brock Company paid 6 months' insurance in advance, covering the period of May 1 to October 31, 20X9. The total payment was $5,400. At the time of the payment, the entire amount was used to increase the balance in the Prepaid Insurance account. What will be the balance in the Prepaid Insurance account as of May 31, 20X9?A) $-0-B) $900C) $3,600D) $4,500E) $5,400Answer: DDiff: 2Objective: L.O. 2-3

8Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

2.3-12) Which situation violates the matching principle?A) Employees are paid for wages worked in a previous month.B) Consulting fees incurred have been recognized even though a bill has not yet been received.C) Depreciation was recorded for equipment even though the equipment was purchased on a date other than January 1.D) A 1-year insurance policy was paid in full on January 1 and the total amount of the bill was recognized in January.E) Customers are billed for services even though the company knows a portion of the customers will never pay.Answer: DDiff: 2Objective: L.O. 2-3

2.3-13) Accrual accounting uses the matching principle.Answer: TRUEDiff: 1Objective: L.O. 2-3

2.3-14) The matching concept is closely related to the cash basis of accounting.Answer: FALSEDiff: 1Objective: L.O. 2-3

2.3-15) Expenses, such as utilities, whose benefit is consumed by the passage of time rather than by the level of sales, are known as period costs.Answer: TRUEDiff: 2Objective: L.O. 2-3

2.3-16) Costs that are linked with revenues and are charged as expenses when the related revenue is recognized are known as product costs.Answer: TRUEDiff: 2Objective: L.O. 2-3

2.3-17) The process of allocating the cost of long-lived or fixed assets to expense is referred to as depreciation.Answer: TRUEDiff: 1Objective: L.O. 2-3

2.3-18) Assets such as prepaid rent may be thought of as costs that are stored to be carried forward to future periods and recorded as expenses in the future.Answer: TRUEDiff: 2Objective: L.O. 2-3

9Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

2.3-19) Under the accrual basis of accounting, prepaid assets become expenses when they expire.Answer: TRUEDiff: 1Objective: L.O. 2-3

2.3-20) Use the following balance sheet equation format to show the effect of the following transactions. Write the account names that will be used for each transaction.

Account name Total assets

Total liabilities

Paid-incapital

Retained Earnings

1. The owners invest $30,000 in the company.2. The company purchases equipment costing $4,000, paying $1,000 with the remainder as a note payable.3. The company acquires inventory costing $2,500, paying $1,500 with the remainder on account.4. Depreciation on the equipment was $300.Answer: Item Account name

Total assets

Total liabilities

Paid-incapital

Retained Earnings

1. Cash 30,000Paid-in capital 30,000

2. Equipment 4,000Cash (1,000)Note payable 3,000

3. Inventory 2,500Cash (1,500)Accounts payable 1,000

4.Depreciation expense (300)Accumulated Depreciation-Equipment (300)

Diff: 2Objective: L.O. 2-2 & 3

10Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

2.3-21) Specify whether each of the following terms belong on the balance sheet, income Statement, or statement of retained earnings and whether each is an asset, liability, revenue, expense, or neither.1. operating cycle2. sales3. trade receivables4. note payable5. cost of sales6. prepaid rent7. equipment8. net earnings9. dividends10. predictive valueAnswer: Financial statement Account 1. neither neither2. income statement revenue3. balance sheet asset4. balance sheet liability5. income statement expense6. balance sheet asset7. balance sheet asset8. income statement neither9. statement of retained earnings neither10. neither neitherDiff: 2Objective: L.O. 2-2 & 3

2.3-22) Describe how the matching concept is necessary to produce an income statement.Answer: The matching concept is necessary to relate product/service costs to the revenues that are generated in a given time period. Expenses are matched with revenue whenever it is reasonable and practicable to do so. Thus, the recognition of expense on the income statement is tied to the recognition of revenues.Diff: 2Objective: L.O. 2-1 & 3

Learning Objective 2.4 Questions

2.4-1) Net income is defined asA) revenues minus expenses.B) expenses minus revenues.C) assets minus revenues.D) assets plus revenues.E) owners' equity assets minus expenses.Answer: ADiff: 1Objective: L.O. 2-4

11Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

2.4-2) Under cash basis accounting, the payment of salaries to employees wouldA) increase assets.B) increase owners' equity.C) increase net income.D) decrease net income.E) decrease revenue.Answer: DDiff: 1Objective: L.O. 2-4

2.4-3) The ________ account links the income statement with the balance sheet.A) Paid-in capitalB) Retained earningsC) DividendsD) Net incomeE) Stockholders' equityAnswer: BDiff: 1Objective: L.O. 2-4

Table 2-1The following data pertains to Cavalier Corporation. Total assets at January 1, 20X9, were $290,000; at December 31, 20X9, total assets were $334,000. During 20X9, sales were $995,000; cash dividends were $10,000; and operating expenses (exclusive of cost of goods sold) were $545,000. Total liabilities at December 31, 20X9, were $128,000; at January 1, 20X9, total liabilities were $105,000. There was no additional paid-in capital during 20X9.

2.4-4) Referring to Table 2-1, what was the amount of stockholders' equity as of January 1, 20X9?A) $450,000B) $440,000C) $185,000D) $635,000E) $175,000Answer: CDiff: 1Objective: L.O. 2-4

2.4-5) Referring to Table 2-1, what was net income for 20X9?A) $26,000B) $31,000C) $201,000D) $440,000E) $450,000Answer: BDiff: 3Objective: L.O. 2-4

12Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

2.4-6) Referring to Table 2-1, what was cost of goods sold for 20X9?A) $450,000B) $435,000C) $429,000D) $419,000E) $440,000Answer: DDiff: 3Objective: L.O. 2-4

2.4-7) Sency Karate Company's January 1, 2009, balance sheet showed total assets of $500,000, total liabilities of $400,000, and total stockholders' equity of $100,000. There were no beginning retained earnings. During the month of January, Sency Karate Company earned revenues of $120,000 and incurred expenses of $30,000. No other transactions occurred. What amount did Sency Karate Company's stockholders' equity account increase by in January?A) $90,000B) $120,000C) $100,000D) $70,000E) $190,000Answer: ADiff: 2Objective: L.O. 2-4

2.4-8) An income statement is a report of all revenues and expenses pertaining to a specific date.Answer: FALSEDiff: 1Objective: L.O. 2-4

2.4-9) Net income appears on the income statement and balance sheet.Answer: FALSEDiff: 1Objective: L.O. 2-4

2.4-10) The balance sheet provides a snapshot of an entity's financial position at an instant of time, while the income statement provides a moving picture of events over a span of time.Answer: TRUEDiff: 2Objective: L.O. 2-4

2.4-11) The ending balance in retained earnings appears on the income statement.Answer: FALSEDiff: 1Objective: L.O. 2-4

13Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

2.4-12) The Clardy Company began business operations on May 1, 20X9. The following transactions occurred during May 20X9:1. The owner invested $32,000 in the company.2. Inventory costing $13,000 was purchased. $900 in cash was paid; the remainder was put on account.3. Equipment costing $18,000 was purchased, of which one-fourth was paid in cash. The remainder was paid with a note payable. Ignore interest expense. Depreciation for the month relating to the equipment was $500.4. The rent for May, June, and July 20X9 was paid. The rent payment was $1,800.5. Cash sales during the month totaled $5,900. The cost of the inventory sold was $3,100.6. Credit sales during the month totaled $7,800. The cost of the inventory sold was $4,200.7. The wages earned by the employees for the month were $4,000, although only $3,500 had been paid as of the end of the month.

Given the previous transactions, determine the net income or loss using the accrual basis for the Clardy Company for the month of May, 20X9.Answer: Sales revenue ($5,900 + $7,800) $13,700Expenses:

Cost of goods sold ($3,100 + $4,200) 7,300Wage expense 4,000Rent expense 600Depreciation expense 500

Total expenses 12,400Net income $ 1,300Diff: 2Objective: L.O. 2-4

14Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

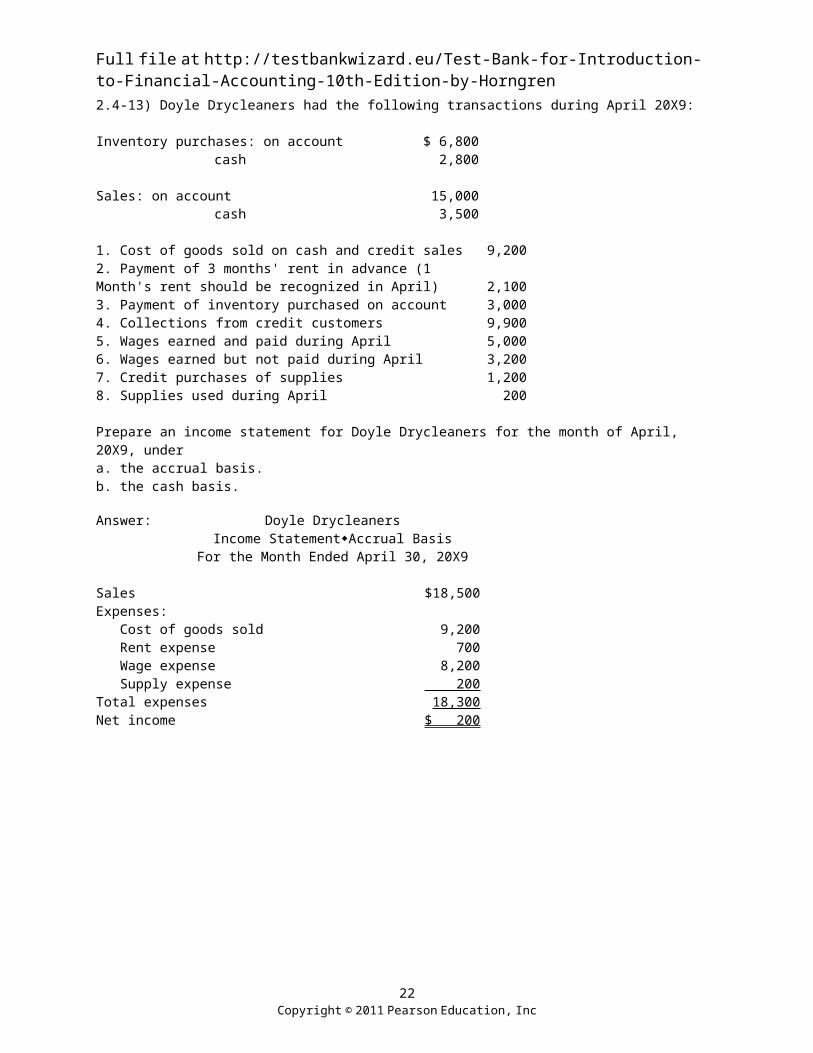

2.4-13) Doyle Drycleaners had the following transactions during April 20X9:

Inventory purchases: on account $ 6,800cash 2,800

Sales: on account 15,000cash 3,500

1. Cost of goods sold on cash and credit sales 9,2002. Payment of 3 months' rent in advance (1Month's rent should be recognized in April) 2,1003. Payment of inventory purchased on account 3,0004. Collections from credit customers 9,9005. Wages earned and paid during April 5,0006. Wages earned but not paid during April 3,2007. Credit purchases of supplies 1,2008. Supplies used during April 200

Prepare an income statement for Doyle Drycleaners for the month of April, 20X9, undera. the accrual basis.b. the cash basis.

Answer: Doyle DrycleanersIncome StatementAccrual Basis

For the Month Ended April 30, 20X9

Sales $18,500Expenses:

Cost of goods sold 9,200Rent expense 700Wage expense 8,200Supply expense 200

Total expenses 18,300Net income $ 200

15Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

Doyle DrycleanersIncome StatementCash Basis

For the Month Ended April 30, 20X9

Cash receipts:From cash sales $ 3,500Collections from credit customers 9,900Total cash receipts $13,400

Cash disbursements:Purchase of inventory $ 2,800Rent payment 2,100Payment of inventory purchased on account 3,000Payment of wages 5,000Total cash disbursements 12,900

Increase in cash $ 500Diff: 2Objective: L.O. 2-4

2.4-14) Following is the balance sheet for Evans Manufacturing as of May 31, 20X9:

Evans ManufacturingBalance SheetMay 31, 20X9

Assets LiabilitiesCash $ 7,100 Accounts Payable $ 6,200Accounts Receivable 4,000 Notes Payable 8,300Merchandise Inventory 13,500 Total Liab. and

Stockholders'Equity 14,500Prepaid Rent 3,300 Paid-in Capital $17,600Store Equipment 15,600 Retained Earnings 11,400

Total Stockholders' equity 29,000Total Assets $43,500 Total Liab. and Stockholders' Equity$43,500

The following transactions occurred during June:1. The company paid $2,100 of the accounts payable.2. The company acquired $3,500 of merchandise inventory, paying 40% in cash and the remainder on open account.3. The utility bill of $600 for the month of June was paid.4. The company received $2,200 from its credit customers.5. Sales of merchandise inventory for the month of June totaled $12,900, of which $5,400 was paid in cash and the remaining amount was on open account. The cost of the merchandise sold was $8,100.6. The company paid $1,600 of the note payable. Ignore interest expense.7. Depreciation on the store equipment was $600 for the month.8. Additional store equipment of $1,700 was acquired. Of this amount, $700 was paid in cash and the remainder was added to the note payable balance.9. The balance in the prepaid rent account represented 3 months' worth of rent paid in advance as of May 31, 20X9.Prepare an income statement for the month ended May 31, 20X9.

Answer: Evans ManufacturingIncome Statement

For the Month Ended May 31, 20X9

16Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

Sales $12,900Expenses:

Cost of goods sold 8,100Depreciation expense 600Utility expense 600Rent expense 1,100

Total expenses 10,400Net income $ 2,500Diff: 3Objective: L.O. 2-4

2.4-15) Following is the balance sheet for the Gormley Company as of March 31, 20X9:

Gormley CompanyBalance Sheet

March 31, 20X9

Assets Liabilities Cash $ 7,100 Accounts Payable $ 6,200

Accounts Receivable 4,000 Notes Payable8,300Merchandise Inventory 13,500 Total Liab.14,500

Prepaid Rent 3,300 Paid-in Capital$17,600Store Equipment 15,600 Retained Earnings 11,400

Total Stockholders' equity 29,000Total Assets $43,500 Total Liab. and Stockholders' Equity$43,500

The following transactions occurred during April:1. The company paid $2,100 of the accounts payable.2. The company acquired $3,500 of merchandise inventory, paying 40% in cash and the remainder on open account.3. The utility bill of $600 for the month of April was paid.4. The company received $2,200 from its credit customers.5. Sales of merchandise inventory for the month of April totaled $12,900, of which $5,400 was paid in cash and the remaining amount was on open account. The cost of the merchandise sold was $8,100.6. The company paid $1,600 of the note payable.7. Depreciation on the store equipment was $600 for the month.8. Additional store equipment of $1,700 was acquired. Of this amount, $700 was paid in cash and the remainder was added to the note payable balance.9. The balance in the prepaid rent account represented 3 months' worth of rent paid in advance as of March 31, 20X9.10. Net income for the month ended April, 20X9, was $2,500.

Prepare a balance sheet dated April 30, 20X9.

Answer: Gormley CompanyBalance SheetApril 30, 20X9

Assets Liabilities Cash $ 8,300 Accounts Payable $ 6,200 Accounts Receivable9,300 Notes Payable 7,700 Merchandise Inventory8,900 Total Liabilities 13,900 Prepaid Rent 2,200 Paid-in Capital $17,600 Store Equipment 17,300 Retained Earnings 13,900

17Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

Accum. Depreciation(600) Total Stockholders' equity 31,500

Total Assets $45,400 Total Liab. and Stockholders' Equity$45,400Diff: 3Objective: L.O. 2-4

Learning Objective 2.5 Questions

2.5-1) On July 21, 20X9, the Hallock Company declared a $5,000 cash dividend payable on August 2, 20X9. The effect of the July 21 transaction on the Hallock Company would be toA) decrease the balance in the cash account and decrease the balance in the retained earnings account by $5,000.B) increase the balance in the dividend expense account and increase the balance in the dividend payable account by $5,000.C) increase the balance in the dividend expense account and increase the balance in the retained earnings account by $5,000.D) increase the balance in the dividend payable account and increase the balance in the prepaid dividend account by $5,000.E) increase the balance in the dividend payable account and decrease the balance in the retained earnings account by $5,000.Answer: EDiff: 2Objective: L.O. 2-5

18Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

2.5-2) On February 23, 20X9, the Herriman Company declared a $9,000 cash dividend payable on March 3, 20X9. The effect of the March 3, 20X9, transaction on the Herriman Company would be toA) increase the balance in the cash account and decrease the balance in the prepaid dividend account by $3,000.B) decrease the balance in the cash account and decrease the balance in the dividend payable account by $3,000.C) decrease the balance in the cash account and increase the balance in the dividend expense account by $3,000.D) decrease the balance in the cash account and increase the balance in the prepaid dividend account by $3,000.E) decrease the balance in the cash account and decrease the balance in the retained earnings account by $3,000.Answer: BDiff: 2Objective: L.O. 2-5

2.5-3) Cash dividendsA) are distributions of cash to trade creditors.B) are expenses like rent and depreciation.C) should not be deducted from revenues because they are not directly linked to the generation of revenues or the costs of operating activities.D) must be paid annually, regardless of the amount of cash in the bank.E) cannot be paid if a net loss is incurred.Answer: CDiff: 2Objective: L.O. 2-5

2.5-4) The Jacobs Company had the following balances in its stockholders' equity accounts as of December 31, 20X9:

Paid-in Capital $53,000Retained Earnings $31,000

During the year ended December 31, 20X9, the Jacobs Company generated $36,000 in net income, and declared and paid $16,000 in dividends. The ending balance in the retained earnings account at December 31, 20X8, wasA) $11,000.B) $26,000.C) $13,000.D) $67,000.E) $40,000.Answer: ADiff: 2Objective: L.O. 2-5

19Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

2.5-5) The Kearney Company's balance sheet on June 30, 20X9, has total assets of $75,000, total liabilities of $30,000, paid-in-capital of $25,000, and retained earnings of $20,000. During the month of July, the Kearney Company recognized revenues of $38,000, cost of goods sold of $27,000, depreciation expense of $3,000, the payment of August and September's rent totaling $1,000, and salary expense of $4,000. The retained earnings balance at July 31, 20X9, will beA) $24,000.B) $29,000.C) $23,000.D) $21,000.E) $25,000.Answer: ADiff: 3Objective: L.O. 2-5

2.5-6) Kosman's Catering balance sheet on August 31, 20X9, has total assets of $73,000, total liabilities of $20,000, paid-in capital of $30,000, and retained earnings of $23,000. During the month of September, Kosman's Catering recognized revenues of $73,000, cost of goods sold of $47,000, depreciation expense of $12,000, the payment of October and November's rent totaling $2,500, and salary expense of $8,000. The retained earnings balance at September 30, 20X9, will beA) $29,000.B) $27,750.C) $31,000.D) $41,000.E) $26,500.Answer: ADiff: 3Objective: L.O. 2-5

2.5-7) Cash dividends are an expense, and therefore they appear on the income statement.Answer: FALSEDiff: 1Objective: L.O. 2-5

2.5-8) The date the board of directors declares a dividend is known as the record date or the payment date.Answer: FALSEDiff: 2Objective: L.O. 2-5

2.5-9) Frequently, the statement of retained earnings is added to the bottom of the balance sheet.Answer: FALSEDiff: 1Objective: L.O. 2-5

20Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

2.5-10) Determine the missing values.Revenues $250Expenses 200Dividends Declared 20Additional investments by owners ANet income BRetained EarningsBeginning CRetained EarningsEnding 110Paid-in CapitalBeginning 60Paid-in CapitalEnding 60Total AssetsBeginning DTotal AssetsEnding 250Total LiabilitiesBeginning 95Total LiabilitiesEnding EAnswer: A = 0 Beginning Paid-in Capital + Additional Investments by Owners = Ending Paid-in Capital; 60 + A = 60B = 50 Net income = Revenues - Expenses; B = 250 - 200C = 80 Retained Earnings, Beg + Net income - Dividends = Retained Earnings, End; C + 50 - 20 = 110D =235 Assets, Beg = Liabilities, Beg + (Retained Earnings, Beg + Paid-in Capital, Beg) D = 95 + (80 + 60)E = 80 Assets, End = Liabilities, End + (Retained Earnings, End + Paid-in Capital, End) 250 = E + (110 + 60)Diff: 2Objective: L.O. 2-4 & 5

2.5-11) The Marcque Company had net income during 20X9 of $55,000. During the year, dividends of $14,000 were declared, of which $21,000 had been paid as of year end. As of the beginning of 20X9, the Paid-in Capital account had a balance of $38,000 and the Retained Earnings account had a balance of $62,000. Prepare a Statement of Retained Earnings for the Marcque Company for the year ended December 31, 20X9.Answer: The Marcque Company

Statement of Retained EarningsFor the Year Ended December 31, 20X9

Retained Earnings, Beginning Balance $ 62,000Add: Net Income 55,000Less Dividends Declared (14,000)Retained Earnings, Ending Balance $ 103,000Diff: 2Objective: L.O. 2-5

21Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

Learning Objective 2.6 Questions

2.6-1) ________ is a quality of information meaning free of error or bias; dependable.A) RelevanceB) ReliableC) VerifiableD) ValidityE) NeutralityAnswer: BDiff: 2Objective: L.O. 2-6

2.6-2) What is the concept that differentiates a corporation from its management?A) EntityB) Going concernC) ReliabilityD) Cost-benefit criterionE) MaterialityAnswer: ADiff: 1Objective: L.O. 2-6

2.6-3) The cost-benefit concept is of most concern toA) banks.B) accounting regulators.C) owners.D) creditors.E) workers.Answer: BDiff: 2Objective: L.O. 2-6

2.6-4) The reason that companies use historical costs is theA) entity concept.B) materiality concept.C) going concern concept.D) period cost principle.E) neutrality principle.Answer: CDiff: 2Objective: L.O. 2-6

22Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

2.6-5) Reliability is defined asA) a correspondence between the accounting numbers and the resources or events those numbers purport to represent.B) the capability of information to make a difference to the decision maker.C) the quality of information that allows decision makers to depend on it to represent the conditions or events that it purports to represent.D) choosing accounting policies without attempting to achieve purposes other than measuring economic impact.E) a quality of information such that there would be a high extent of consensus among independent measurers of an item.Answer: CDiff: 2Objective: L.O. 2-6

2.6-6) Reliability is the assumption that, ordinarily, an entity persists indefinitely.Answer: FALSEDiff: 1Objective: L.O. 2-6

2.6-7) The cost-benefit criterion asserts that an item should be included in a financial statement if its omission or misstatement would tend to mislead the reader.Answer: FALSEDiff: 1Objective: L.O. 2-6

2.6-8) The stable monetary unit concept is based on a principle of low inflation.Answer: TRUEDiff: 2Objective: L.O. 2-6

2.6-9) Reliability refers to whether the information makes a difference to the decision maker.Answer: FALSEDiff: 2Objective: L.O. 2-6

2.6-10) The assumption that in all ordinary situations an entity persists indefinitely is known as the reliability assumption.Answer: FALSEDiff: 1Objective: L.O. 2-6

23Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

2.6-11) Name which of the following concepts is applicable to each situation.

EntityReliabilityGoing ConcernMaterialityCost-benefitStable monetary unitConfirmatory valuePredictive value

1. Morgan Enterprises acquired equipment with a fair market value of $12,000 and a trade-in value of $9,000, yet paid $10,000 for the equipment. Morgan Enterprises recorded the equipment at $10,000.

2. Swanson Industries has divisions in several countries. Before publishing financial statements, Swanson Industries translates its divisional financial information to U.S. dollars.

3. Novotny, Inc., is experiencing financial difficulties due to poor economic conditions. The organization has been in existence for 50 years and has experienced these conditions in the past with little financial impact to the organization. Although Novotny, Inc., may be impacted, there is no reason to believe that it will go bankrupt.

4. Poloha Manufacturing is owned by Lynn Roberts and Dale Shiley, after each deposited $50,000 into the business's bank account. Both Lynn and Dale have access to the bank account and periodically transfer money from their personal accounts to the business account, but they never access the business account for personal use.

5. Pittman Bar and Grill prepares monthly financial statements. Each month after they are Prepared, the owner, Bill Scodd, reviews them in an effort to forecast future revenues and expenses.

6. Searle Company is inquiring about new machinery for the plant. The current machinery is paid in full; however, new machinery would need to be financed, thus incurring monthly payments that include interest. If Searle Company decides to purchase the new machinery, the decision makers must believe that the advantages exceed the expenditures.

Answer: 1. Cost principle2. Stable monetary unit3. Going concern4. Entity5. Predictive value6. Cost-benefitDiff: 2Objective: L.O. 2-6

24Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

2.6-12) Why is the concept of going concern necessary for financial statements to be useful?Answer: If a firm is to be terminated immediately, then all of the items on the balance sheet are valued at liquidation value. For a going concern, it is reasonable to historical cost to record long-term assets and reports liabilities at the amount due at maturity. The going concern supports the accounting conventions used such as historical cost and the matching principle.Diff: 2Objective: L.O. 2-6

Learning Objective 2.7 Questions

2.7-1) Which financial ratio is required to be reported on the face of the income statement of publicly-held corporations?A) Earnings per shareB) Price-earnings ratioC) Dividend-yield ratioD) Dividend payout ratioE) Inventory turnover ratioAnswer: ADiff: 2Objective: L.O. 2-7

2.7-2) Which financial ratio measures how much the investing public is willing to pay for a company's prospects for earnings?A) Earnings per shareB) Price-earnings ratioC) Dividend-yield ratioD) Dividend payout ratioE) Profit margin ratioAnswer: BDiff: 2Objective: L.O. 2-7

Table 2-2McGinty, Inc., had 20X9 earnings of $600,000. Cash dividends per share were $1.25. The company had an average of 225,000 shares of common stock outstanding. The market price of the stock at the end of the year was $25 per share.

2.7-3) Referring to Table 2-2, the earnings per share for 20X9 isA) $ 1.50.B) $24.00.C) $ 1.25.D) $ 2.67.E) This cannot be determined from the information given.Answer: DDiff: 2Objective: L.O. 2-7

25Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

2.7-4) Referring to Table 2-2, what was the price-earnings ratio for Cleary Systems?A) 0.10B) 18.4C) 9.36D) 24.0E) Cannot be determined from the information providedAnswer: CDiff: 2Objective: L.O. 2-7

2.7-5) Referring to Table 2-2, what was the dividend-yield for Cleary Systems?A) 5%B) 12%C) 47%D) 15%E) Cannot be determined from the information providedAnswer: ADiff: 2Objective: L.O. 2-7

Table 2-3Megyes Corporation had 20X9 earnings of $1,500,000. Cash dividends per share were $0.50. The company had an average of 1,225,000 shares of common stock outstanding. The market price of the stock at the end of the year was $6.00 per share.

2.7-6) Referring to Table 2-3, what was the earnings per share for 20X9?A) $0.60B) $0.75C) $1.22D) $1.25E) $5.50Answer: CDiff: 2Objective: L.O. 2-7

2.7-7) Referring to Table 2-3, what was the price-earnings ratio for Megyes Corporation?A) 6.5B) 4.91C) 3.00D) 12E) 5.20Answer: BDiff: 2Objective: L.O. 2-7

26Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

2.7-8) Referring to Table 2-3, what was the dividend-yield for Megyes Corporation?A) 12.00%B) 10.00%C) 20.33%D) 8.33%E) Cannot be determined from the information providedAnswer: DDiff: 2Objective: L.O. 2-7

2.7-9) Which financial ratio measures the return on an investment in common stock by dividing the cash dividends per share by the market price per share?A) Earnings per shareB) Price-earnings ratioC) Dividend-yield ratioD) Dividend payout ratioE) Accounts receivable turnover ratioAnswer: CDiff: 2Objective: L.O. 2-7

2.7-10) The dividend-yield ratio must appear on the face of the balance sheet.Answer: FALSEDiff: 1Objective: L.O. 2-7

2.7-11) A low P-E ratio indicates that investors think a stock is underpriced.Answer: TRUEDiff: 2Objective: L.O. 2-7

2.7-12) The price-earnings ratio is earnings per share of common stock divided by the market price per share of common stock.Answer: FALSEDiff: 2Objective: L.O. 2-7

2.7-13) The dividend-yield ratio is computed as the current market price of the stock divided by the current dividend per share.Answer: FALSEDiff: 2Objective: L.O. 2-7

2.7-14) Companies with exceptional growth (growth stocks) tend to pay a higher percentage of their earnings in dividends.Answer: FALSEDiff: 1Objective: L.O. 2-7

27Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

2.7-15) The dividend-payout ratio is computed as common dividends per share divided by earnings per share.Answer: TRUEDiff: 2Objective: L.O. 2-7

2.7-16) Following is a list of selected financial data for a series of companies:

| Per-share Data | Ratios and Percentages Company | Price Earnings Dividends | P - E Dividend - yield Dividend - payoutAlpha | $50 $1.75 A | B C 30%Beta | $35 D $2.25 | E F 40%Charlie | G $5.25 $1.75 | 12.0 I J

1. Compute the missing figures and identify the company witha. the highest dividend-yield.b. the highest dividend-payout percentage.c. the lowest market price relative to earnings.

2. Assume that you know nothing about any of these companies other than the data given and the computations you have made from the data. If you were interested in receiving dividend income, which company would you choose asa. the most attractive investment? Why?b. the least attractive investment? Why?Answer: 1. A = .53 Dividend-payout = dividends/earnings; .30 = A/1.75

B = 28.6 P-E = Price/earnings; B = 50/1.75;C = .0106 Dividend-yield = Dividends/Price; C = .53/50; C = 1.06%D = 5.63 Dividend-payout = dividends/earnings; .40 = 2.25/D; D = 5.63E = 6.22 P-E = Price/earnings; E = 35/5.63; E = 6.22F = .0643 Dividend-yield = Dividends/Price; F = 2.25/35; F = 6.43%G = 63 P-E = Price/earnings; 12.0 = G/5.25; G = 63I = .0278 Dividend-yield = Dividends/Price; I = 1.75/63 = 2,78%J = 33% Dividend Payout = dividends/earnings; J = 1.75/5.25 = .33

a. Betab. Betac. Beta

2. a. BetaBeta has the highest dividend-yield and has the highest dividend-payout. It also has the highest dividends per share.

b. AlphaAlpha has the lowest dividend-yield ratio and the lowest dividend-payout ratio.Diff: 2Objective: L.O. 2-7

Learning Objective 2.8 Questions

2.8-1) R&D costs are expensed in the period that they occur,A) which is a violation of the matching principle.B) because FASB determined that the benefits of R&D are often harder to pinpoint than the costs.

28Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

C) because is was the only way FASB could get verifiability.D) because IASB lobbied FASB to do so.E) because the U.S. Congress passed a law on it.Answer: BDiff: 2Objective: L.O. 2-8

2.8-2) The primary driver for FASB rule-making isA) consistency.B) representational faithfulness.C) validity.D) the cost-benefit criterion.E) the matching concept.Answer: DDiff: 2Objective: L.O. 2-8

2.8-3) Accounting regulation is difficult because ofA) the congressional oversight.B) company lobbying.C) the trade-off between relevance and reliability.D) IRS rules conflicting with financial rules.E) period costs that are difficult to identify.Answer: CDiff: 2Objective: L.O. 2-8

2.8-4) Financial accounting standardsA) are products of airtight logic.B) are issued by the FASB without the input of parties such as corporate accountants or analysts.C) are often the result of compromises among the interested parties.D) have never been overturned by the SEC.E) None of the above statements is true.Answer: CDiff: 2Objective: L.O. 2-8

29Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

2.8-5) The FASB's main criterion in making decisions about reporting requirements is theA) usefulness of the information provided.B) benefit of implementing a particular standard.C) cost versus the benefit of implementing a particular standard.D) cost of implementing a particular standard.E) None of the above statements is correct.Answer: CDiff: 1Objective: L.O. 2-8

2.8-6) ________ is the capability of information to make a difference to the decision maker.A) VerifiabilityB) ReliabilityC) RelevanceD) ValidityE) NeutralityAnswer: CDiff: 2Objective: L.O. 2-8

2.8-7) Relevance is defined asA) choosing accounting policies without attempting to achieve purposes other than measuring economic impact.B) the capability of information to make a difference to the decision maker.C) the quality of information that allows users to depend on it to represent the conditions or events that it purports to represent.D) a correspondence between the accounting numbers and the resources or events those numbers purport to represent.E) a quality of information such that there would be a high extent of consensus among independent measurers of an itemAnswer: BDiff: 2Objective: L.O. 2-8

2.8-8) ________ is a quality of information producing a high extent of consensus among independent measurers of an item.A) ValidityB) RelevanceC) VerifiabilityD) ReliabilityE) NeutralityAnswer: CDiff: 2Objective: L.O. 2-8

30Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

2.8-9) Verifiability is defined asA) the quality of information that allows users to depend on it to represent the conditions or events that it purports to represent.B) the capability of information to make a difference to the decision maker.C) choosing accounting policies without attempting to achieve purposes other than measuring economic impact.D) a correspondence between the accounting numbers and the resources or events those numbers purport to represent.E) a quality of information such that it can be checked to ensure it is correct.Answer: EDiff: 2Objective: L.O. 2-8

2.8-10) Neutrality is defined asA) information which is free from bias and not slanted to influence the behavior of decision makers.B) the capability of information to make a difference to the decision maker.C) the quality of information that allows users to depend on it to represent the conditions or events that it purports to represent.D) a correspondence between the accounting numbers and the resources or events those numbers purport to represent.E) a quality of information such that there would be a high extent of consensus among independent measures of an item.Answer: ADiff: 2Objective: L.O. 2-8

2.8-11) Charging all research and development costs to expense as incurred is an example ofA) materiality.B) conservatism.C) reliability.D) accrual accounting.E) relevance.Answer: BDiff: 2Objective: L.O. 2-8

2.8-12) Which of the following statements is incorrect?A) Verifiability means there would be a high extent of consensus among independent measurers of an item.B) Validity means a correspondence between the account number and the resources and events those numbers purport to represent.C) Neutrality means choosing accounting policies without attempting to achieve purposes other than measuring economic impact.D) Relevance is the capability of information to make a difference to a decision-maker.E) Materiality means that the cost/benefit trade-off in the determination of instituting new accounting policies and procedures has been applied with due diligence.Answer: EDiff: 2Objective: L.O. 2-82.8-13) Devising an accelerated method of depreciation for financial statement purposes that would promote a national goal of increased investment in capital equipment would be an example of a lack ofA) neutrality.B) consistency.

31Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

C) matching.D) conservatism.E) recognition.Answer: ADiff: 2Objective: L.O. 2-8

2.8-14) Using LIFO to value inventory one year and using FIFO the next is a violation of which accounting principle?A) ConservatismB) RecognitionC) NeutralityD) MatchingE) ConsistencyAnswer: EDiff: 2Objective: L.O. 2-8

2.8-15) Relevance means that the information can be counted on to represent faithfully the condition of the company, given the rules in use.Answer: FALSEDiff: 2Objective: L.O. 2-8

2.8-16) There is often a conflict between applying the concept of relevance and the concept of reliability.Answer: TRUEDiff: 2Objective: L.O. 2-8

2.8-17) Verifiability is a correspondence between numbers and the effects portrayed.Answer: FALSEDiff: 2Objective: L.O. 2-8

2.8-18) The cost-benefit criterion states that an accounting system should be changed when the expected additional benefits of the change exceed its expected additional costs.Answer: TRUEDiff: 1Objective: L.O. 2-8

2.8-19) U.S. financial reporting follows the IASB framework for decision usefulnessAnswer: FALSEDiff: 2Objective: L.O. 2-8

32Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

2.8-20) Relevance and validity are the two main qualities that make accounting information useful for decision making.Answer: FALSEDiff: 1Objective: L.O. 2-8

2.8-21) One of the major relevance characteristics is neutrality.Answer: FALSEDiff: 2Objective: L.O. 2-8

2.8-22) Describe the trade-off between relevance and reliability in a paragraph or two.Answer: The trade-off occurs because the primary driver for regulation is the decision usefulness for decision-makers, which implies that relevance should have first priority. But, the identification of relevant information is often difficult because of problems with verifiability of what is relevant and with representational faithfulness of that information. Neutrality is also a problem when the objectivity of relevant information is called into question.Diff: 2Objective: L.O. 2-8

2.8-23) Define three of the following:a. Neutralityb. Relevancec. Reliabilityd. Consistencye. VerifiabilityAnswer: a. Neutrality: choosing accounting policies that do not attempt to achieve purposes other than measuring economic impactb. Relevance: the capability of information to make a difference to the decision-makerc. Reliability: the quality of information that allows users to depend on it to represent the conditions or events that it purports to representd. Consistency: using the same accounting policies and procedures from period to periode. Verifiability: A quality of information such that it can be checked to ensure it is correctDiff: 2Objective: L.O. 2-8

33Copyright © 2011 Pearson Education, Inc

Full file at http://testbankwizard.eu/Test-Bank-for-Introduction-to-Financial-Accounting-10th-Edition-by-Horngren

2.8-24) For each example, write the qualitative characteristic(s) or accounting term that best corresponds.a. The use of a different inventory method every year is not an example of thisb. An error of $100 of revenue for Sherry's Dairy King versus $100 of revenue for McDonald'sc. Record revenue when it is earned and record expenses when incurred regardless of when cash changes handsd. A parent corporation, a subsidiary, and a retail store are examples of this concepte. Applying lower-of-cost-or-market methods to asset valuationf. Three auditors count the same amount of cashAnswer: a. consistencyb. materialityc. accrual accountingd. entitye. conservatismf. verifiabilityDiff: 2Objective: L.O. 2-6 & 8

34Copyright © 2011 Pearson Education, Inc