zgewvkxg âktgevqt 5vcvg %qctf 5vc j … · background checks, ... darren mickler georgia state...

TRANSCRIPT

2014 Executive Director & State Board Staff Conference

Savannah, GeorgiaMarch 3-5, 2014

1.

Monday, March 3, 2014

10:00 am – 3:00 pm EXECUTIVE DIRECTORS COMMITTEE MEETING Moorings (Committee Members Only)

5:00 – 6:00 pm REGISTRATION Grand Ballroom South

6:00 – 8:00 pm WELCOME RECEPTION River Lawn

Tuesday, March 4, 2014

8:00 – 9:30 am TABLE TOPICS BREAKFAST AICPA Practice Analysis Grand Ballroom A Discussion Leaders: RUSS FRIEDEWALD Executive Director, Illinois Board of Examiners MICHAEL DECKER Director of Examinations, AICPA JOE MASLOTT, CPA Senior Technical Manager, AICPA Background Checks, Convictions & Disciplinary Actions/ CPA Exam Multi-Testers Grand Ballroom B Discussion Leader: WADE JEWELL Executive Director, Virginia Board of Accountancy 9:30 – 9:45 am WELCOME (with Legal Counsel) Grand Ballroom C Presiding: MARK CROCKER, CPA Executive Director, Executive Director, Tennessee State Board of Accountancy

9:45 – 10:15 am NASBA REPORT (with Legal Counsel) Grand Ballroom C Moderator: MARK CROCKER, CPA Executive Director, Tennessee State Board of Accountancy Speakers: CARLOS JOHNSON, CPA. Ed.D. Chair, NASBA KEN L. BISHOP President/CEO, NASBA

10:15 – 10:30 am BREAK

10:30 – 11:00 am LEGISLATIVE UPDATE Grand Ballroom C Moderator: JIMMY CORLEY Executive Director, Arkansas State Board of Accountancy Speaker: JOHN JOHNSON Director, Legislative and Governmental Affairs, NASBA

2.

Tuesday, March 4, 2014 (continued)

11:00 – 12:00 pm NATIONAL REGISTRY OF CPE SPONSORS AND THE FUTURE OF LEARNING: EXPLORING NEW LEARNING METHODS FOR CPE Grand Ballroom C Moderator: OFELIA DURAN Executive Director, Colorado State Board of Accountancy Speakers: JESSICA LUTTRULL, CPA Manager, National Registry, NASBA MARIA CALDWELL, ESQ. ChiefLegalOfficer/Director,ComplianceServices,NASBA ERIC DINGLER Director,AuditChiefLearningOfficer Deloitte Service, LLP 12:00 – 1:30 pm LUNCH Grand Ballroom B

1:30 – 2:00 pm UPDATE ON ADMINISTRATION OF CPA EXAMINATION Grand Ballroom C Moderator: RUSS FRIEDEWALD Executive Director, Illinois Board of Examiners Speakers: MICHAEL DECKER Director of Examinations, AICPA KIMBERLY FARACE Senior Client Services Manager, Prometric PATRICIA HARTMAN Director, Client Services, NASBA 2:00 – 2:30 pm INVESTIGATOR TRAINING Grand Ballroom C Moderator: JIMMY CORLEY Executive Director, Arkansas State Board of Accountancy Speakers: FRANK X. TRAINOR, ESQ. Staff Attorney, North Carolina Board of CPA Examiners RANDALL A. ROSS, CPA Executive Director, Oklahoma Accountancy

2:30 – 3:00 pm FOREIGN CREDENTIAL EVALUATIONS STANDARDS Grand Ballroom C Moderator: DORIS CUBITT, CPA Executive Director, South Carolina Board of Accountancy Speakers: BRENTNI HENDERSON-KING Manager, International Evaluation Services, NASBA

3:00 – 3:30 pm UPDATE ON FEDERAL AGENCY OUTREACH Grand Ballroom C Moderator: PAMELA IVEY Executive Director, Wyoming Board of Accountancy Speakers: COLLEEN CONRAD, CPA Executive Vice President/COO, NASBA

3:30 – 3:45 pm BREAK

3.

Tuesday, March 4, 2014 (continued)

3:45 – 4:30 pm NASBA’S CPE AUDIT SERVICE FOR BOARDS Grand Ballroom C Moderator: WADE JEWELL Executive Director, Virginia Board of Accountancy Speakers: TOM DEGROODT Executive Director, Missouri State Board of Accountancy MARIA CALDWELL, ESQ. ChiefLegalOfficer/Director,ComplianceServices,NASBA REBECCA GEBHARDT Manager, Compliance Services, NASBA

4:30 – 5:00 pm Q& A SESSION FROM ROLL CALL MATERIALS/ NEW EDs Grand Ballroom C Moderator: MARK CROCKER, CPA Executive Director, Tennessee State Board of Accountancy

5:00 pm RECESS

Wednesday, March 5, 2014

8:00 – 9:30 am TABLE TOPICS BREAKFAST (continued from Tuesday) Grand Ballroom A&B

9:30 – 10:00 am STATE SOCIETY RELATIONS Grand Ballroom C Moderator: NICOLE KASIN Executive Director, South Dakota Board of Accountancy Speakers: RICH JONES WA State Society President & CEO RICK SWEENEY, CPA Executive Director, Washington State Board of Accountancy 10:00 – 10:30 am NASBA TECHNOLOGY UPDATE Grand Ballroom C Moderator: WADE JEWELL Executive Director, Virginia Board of Accountancy Speakers: CHERYL FARRAR ChiefInformationOfficer,NASBA 10:30 – 10:45 am BREAK

10:45 – 11:15 am INTERNAL REVENUE SERVICE Grand Ballroom C Moderator: DAVE SANFORD, CPA Executive Director, Guam Board of Accountancy Speakers: LEE D. MARTIN, PMP DeputyDirector,OfficeofProfessionalResponsibility,InternalRevenueService

4.

Wednesday, March 5, 2014 (continued)

11:15 – 11:45 am CIVIL LITIGATION Grand Ballroom C Moderator: PAMELA IVEY Executive Director, Wyoming Board of Accountancy Speakers: NOEL ALLEN, ESQ. Legal Counsel, NASBA 11:45 – 1:15 pm RECOGNITION LUNCH Grand Ballroom B Presiding: MARK CROCKER, CPA Executive Director, Tennessee State Board of Accountancy

1:15 – 1:30 pm REPORT FROM LEGAL COUNSEL Grand Ballroom C Moderator: MARK CROCKER, CPA Executive Director, Tennessee State Board of Accountancy Speaker: STACEY GROOMS Manager, Regulatory Affairs, NASBA

1:30 – 2:45 pm DEPARTMENT OF LABOR Grand Ballroom C Moderator: MARK CROCKER, CPA Executive Director, Tennessee State Board of Accountancy Speaker: IAN DINGWALL, CPA ChiefAccountant,U.S.DepartmentofLabor

2:45 – 4:45 pm BREAKOUT SESSIONS Executive Directors (only) Grand Ballroom C Moderator: MARK CROCKER, CPA Executive Director, Tennessee State Board of Accountancy Board Staff (only) Grand Ballroom A Moderator: DON MILLS, CPA Investigator, Tennessee State Board of Accountancy

4:45 – 5:00 pm Q & A SESSION WITH NASBA LEADERSHIP Grand Ballroom C Presiding: MARK CROCKER, CPA Executive Director, Tennessee State Board of Accountancy

5:00 – 5:15 pm REPORT TO NASBA LEADERSHIP Grand Ballroom C Presiding: MARK CROCKER, CPA Executive Director, Tennessee State Board of Accountancy

5:15 pm ADJOURN

6:30 pm MARDI GRAS GALA HarborLawn

Thursday, March 6, 2014

9:00 am - 12:00 pm EXECUTIVE DIRECTORS COMMITTEE MEETING Moorings (Committee Members Only)

1.

Jesse F. Dixon Accountancy Board of OhioTracey Fithen Accountancy Board of OhioJohn E. Patterson, Esq. Accountancy Board of OhioCarol J. Preston, CPA Alabama State Board of Public AccountancyMonica L. Petersen Arizona State Board of AccountancyJames Corley, CPA Arkansas State Board of Public AccountancyTim Montgomery Arkansas State Board of Public AccountancyOfelia Duran Colorado State Board of AccountancySonia Worrell Asare, Esq. Connecticut State Board of AccountancyClifford Cooks District of Columbia Board of AccountancyVeloria Kelly Florida Board of AccountancyDarren Mickler Georgia State Board of AccountancyDavid Sanford, CPA.CITP Guam Board of AccountancyKent Absec Idaho State Board of AccountancySue Lenon Idaho State Board of AccountancyTia Marie France Illinois Board of ExaminersRuss Friedewald Illinois Board of ExaminersMatt Hoffman Illinois Board of ExaminersRobert E. Lampe Iowa Accountancy Examining BoardSusan L. Somers Kansas Board of AccountancyRichard C. Carroll Kentucky State Board of AccountancyPhyllis Gordon Kentucky State Board of AccountancyDennis L. Gring Maryland State Board of Public AccountancyLinda Rhew Maryland State Board of Public AccountancyAlan J. Schefke Michigan State Board of AccountancyDoreen Frost Minnesota State Board of AccountancyRansom Jones Mississippi State Board of Public AccountancyAndy L. Wright Mississippi State Board of Public AccountancyRebekah Dalbey Missouri State Board of AccountancyThomas DeGroodt, CPA Missouri State Board of AccountancyGrace Berger Montana Board of Public AccountantsHeather Myers Nebraska State Board of Public AccountancyDan Sweetwood Nebraska State Board of Public AccountancyLeslie Walsh Nevada State Board of AccountancyViki A. Windfeldt Nevada State Board of AccountancyJennifer Baca, CFE New Mexico Public Accountancy BoardRobert N. Brooks North Carolina State Board of CPA ExaminersWalter C. Davenport, CPA North Carolina State Board of CPA ExaminersLisa R. Hearne North Carolina State Board of CPA ExaminersDavid R. Nance, CPA North Carolina State Board of CPA ExaminersPhyllis W. Wiggins-Elliott North Carolina State Board of CPA ExaminersBuck Winslow North Carolina State Board of CPA ExaminersJim Abbott, Ph.D North Dakota State Board of AccountancyCarlos E. Johnson, CPA, Ed. D. Oklahoma Accountancy BoardRandall Ross, CPA Oklahoma Accountancy BoardMartin Pittioni Oregon Board of AccountancyLuis Barreto Puerto Rico Board of AccountancyDoris Cubitt, CPA South Carolina Board of AccountancyBridgette Goff South Carolina Board of AccountancyNicole Kasin South Dakota Board of Accountancy

MEMBERS BY BOARD

2.

Darla M. Saux, CPA, CGMA State Board of CPAs of LouisianaMark H. Crocker, CPA, CGMA Tennessee State Board of AccountancyApril Serrano Texas State Board of Public AccountancyWilliam Treacy Texas State Board of Public AccountancyDonna Hiller Wier Texas State Board of Public AccountancyWade A. Jewell Virginia Board of AccountancyChantal Scifres Virginia Board of AccountancyJennifer Sciba Washington State Board of AccountancyRichard C. Sweeney, CPA Washington State Board of AccountancyBrenda Sue Turley West Virginia Board of AccountancyBrittany Lewin Wisconsin Accounting Examining BoardPamela Ivey Wyoming Board of Certified Public Accountants

Alfonzo Alexander President, NASBA Center for the Public Trust & CROEd Barnicott Vice President, Strategic Planning & Program ManagementKen L. Bishop President & Chief Executive OfficerColleen Conrad, CPA Executive Vice President & Chief Operating OfficerAnthony Cox Graphics DesignerDaniel J. Dustin, CPA Vice President, State Board RelationsCheryl Farrar Chief Information Officer Rebecca Gebhardt Manager, Compliance ServicesCassandra Gray Manager, CommunicationsLouise Dratler Haberman Vice President, Information and ResearchPatricia Hartman Director, Client ServicesBrentni Henderson-King Manager, International Evaluation ServicesSteve Hill Multimedia & Video Services MgrGene Holt Records Management CoordinatorJohn Johnson Director, Legislative & Governmental AffairsThomas G. Kenny Director, CommunicationsAngela Layton Senior Meeting PlannerJessica Luttrull, CPA Manager, National RegistryChris Mays Manager, National Candidate DatabaseMatthew Wilkins Report Product Manager

Michael Decker AICPASuzanne U. Jolicoeur AICPAOphir Lehavy AICPAJoseph Maslott, CPA AICPAMat Young AICPARandal Breaux CBT, Enterprise Project ManagerEric Dingler, CPA Deloitte Service, LLPNancy Wolven-Juron Deloitte LLPLee Martin Internal Revenue ServiceKim Farace PrometricIan Dingwall, CPA U.S. Department of LaborRich Jones, CPA Washington Society of CPAs

MEMBERS BY BOARD (CONTINUED)

NASBA STAFF

OTHER PARTICIPANTS

NOEL L. ALLEN, ESQ. Allen, Pinnix & Nichols, P.A.510 Glenwood – Suite 301 Phone: 919-755-0505Raleigh, NC 27603 Email: [email protected]

Noel L. Allen, Esq., has served as legal counsel for NASBA since 1997, and for the North Carolina State Board of CPA Examiners since the early 1980s. Prior to entering private practice, Mr. Allen was an assistant attorney general in the antitrust division of the North Carolina Department of Justice. He has authored books

on antitrust and trade regulation, including North Carolina Unfair Business Practice (Lexis, Third Edition), and is the U.S. editor of two multi-volume treatises, Competition Law in Western Europe and the U.S.A. (Kluwer), and Comparative Law of Monopolies (Kluwer). Mr. Allen has taught antitrust/trade regulation law and international business law as an adjunct professor and visiting lecturer at law schools in the U.S. and Europe and is recipient of International Service Awards for both the North Carolina World Trade Association and the North Carolina Bar Association. He is listed in the Bar Register of Preeminent Lawyers, and in U.S. News – Best Lawyers (Administrative/Regulatory & Antitrust Law). He earned his bachelor’s degree at Elon University, his J.D. at UNC-Chapel Hill, and a graduate diploma in International Competition law at the University of Amsterdam, the Netherlands. In 2009, Elon University awarded him an Honorary Doctorate. In its January 2013 issue, Business North Carolina profiled him as the state’s “Top Antitrust Lawyer.”

KEN L. BISHOPNational Association of State Boards of Accountancy (NASBA) 150 Fourth Avenue, North, Suite 700 Phone: 615-880-4201Nashville, TN 37219-2417 Email: [email protected]

Ken L. Bishop serves as President and Chief Executive Officer of NASBA, as well as Chief Executive Officer of NASBA’s ethics arm, the NASBA Center for the Public Trust (CPT). Prior to acceding to the president and CEO role in January 2012, Mr. Bishop served as executive vice president and chief operating officer of

NASBA, where he was responsible for leading NASBA’s business and testing operations. In recent years, Mr. Bishop has been instrumental in the adoption of legislation for “CPA Mobility,” whereby CPAs increase their ability to practice throughout the U.S. without the need to be licensed separately in each state. Additionally, he played a key role in the international administration of the U.S. CPA Examination, which is now offered in Japan, Bahrain, Kuwait, Lebanon, the United Arab Emirates and Brazil. Mr. Bishop joined NASBA on January 1, 2007, as president and chief executive officer of Professional Credential Services (PCS), NASBA’s former wholly-owned subsidiary, and director of CPA Examination Operations. During his tenure as president of PCS, the company grew to provide services to more than 50 professions, both nationally and internationally. Before joining NASBA, Mr. Bishop built a successful career in the areas of state government and law enforcement, having served in roles including executive director of the Missouri State Board of Accountancy, assistant director of the Missouri Department of Public Safety, undercover narcotics officer, under-sheriff, chief of police and commander of the Missouri Major Case Squad. A Missouri native, Mr. Bishop holds a bachelor’s degree in Education from the University of Missouri Columbia, as well as a master’s degree in Criminal Justice, and he is a graduate of Harvard University’s Kennedy School of Government Executive Program. He is also a graduate of the Missouri State Highway Patrol Academy and the Federal Criminal Justice Academy. His honors include being named to Accounting Today’s Top 100 Most Influential People in Accounting, in 2011, 2012 and 2013.

1.

MARIA CALDWELL, ESQ. National Association of State Boards of Accountancy (NASBA) 150 Fourth Avenue, North, Suite 700 Phone: 615-312-3771Nashville, TN 37219-2417 Email: [email protected]

Maria Caldwell, Esq., currently serves as NASBA’s Chief Legal Officer and Director of Compliance Services. She has also served as NASBA’s Director of Business Development from 2005 to early 2011, and NASBA’s General Counsel from 2003 until December 2011. Ms. Caldwell is a graduate of Duke University School

of Law and became a member of the Bar of the State of California in 1988, while working as an associate for the law firm of Gibson, Dunn & Crutcher. In 1991, Ms. Caldwell became a member of the Bar of the State of Tennessee and an associate with the law firm of Bass, Berry & Sims. Ms. Caldwell then served as General Counsel of Sirrom Capital Corporation, a public company formerly headquartered in Nashville. She joined NASBA in November of 2003 to create an in-house legal department and subsequently began the business development department. In February 2011, she was asked to head the Compliance Services department, and in January 2012, to act as Chief Legal Officer.

COLLEEN K. CONRAD, CPANational Association of State Boards of Accountancy (NASBA) 150 Fourth Avenue, North, Suite 700 Phone: 615-880-4207Nashville, TN 37219-2417 Email: [email protected]

Colleen K. Conrad, CPA, serves as Executive Vice President and Chief Operating Officer of NASBA. She is responsible for all NASBA operations, including CPA Examination Services, licensing, continuing education, IT and risk management. Ms. Conrad also oversees governmental, international and professional relationships.

She brings more than 25 years of accounting expertise and leadership to NASBA. As a former partner in a large regional CPA firm, she practiced in the Real Estate Services Group, providing real estate, attest, tax and consulting services to clients nationwide. From 1997 to 2007, Ms. Conrad served on the Missouri Board of Accountancy, with two terms as chair. Her contributions to NASBA as a committee member and featured speaker during NASBA forums date back to 1997. Ms. Conrad’s committee involvement included membership on the Strategic Initiatives Committee, Bylaws Committee, and Regulatory Response Committee, as well as the Education Committee’s 150-Hour Task Force. A long-time member of the AICPA, Ms. Conrad recently completed a three-year term on the AICPA Council. She was a member of the AICPA Board of Examiners for 10 years, serving one term as chair, and was also a member of the AICPA/NASBA International Examination Task Force. A Kansas native, Ms. Conrad is a member of the Missouri and Tennessee Societies of CPAs and past president and member of the St. Louis Society of Women CPAs. Among her numerous honors, she was named as an AICPA/Missouri CPA Woman-to-Watch, Experienced Leader, in 2008. She earned a bachelor’s degree in accounting from Truman State University and became a licensed CPA in 1987. She recently served as chair and board member of the University’s Accounting Alumni Board.

JAMES CORLEY, CPA Arkansas State Board of Public Accountancy 101 East Capitol, Suite 450 Phone: 501-682-5333Little Rock, AR 72201 Email: [email protected]

James (“Jimmy”) Corley, CPA, has served as Executive Director of the Arkansas State Board of Public Accountancy since August 2010. He has been licensed as a CPA in Arkansas since 2002. Mr. Corley graduated from the University of Central Arkansas in 2000. He began his professional career in public

accounting working for Arthur Andersen and PricewaterhouseCoopers for three and a half years. He also has six years of experience in private industry, working in the telecommunications and staffing industries. Mr. Corley is a member of the Arkansas Society of Certified Public Accountants and the Arkansas Society of Accountants, and currently serves on the NASBA Executive Directors Committee and the AICPA State Board and CPA Exam Practice Analysis Sponsor Group Committees.

2.

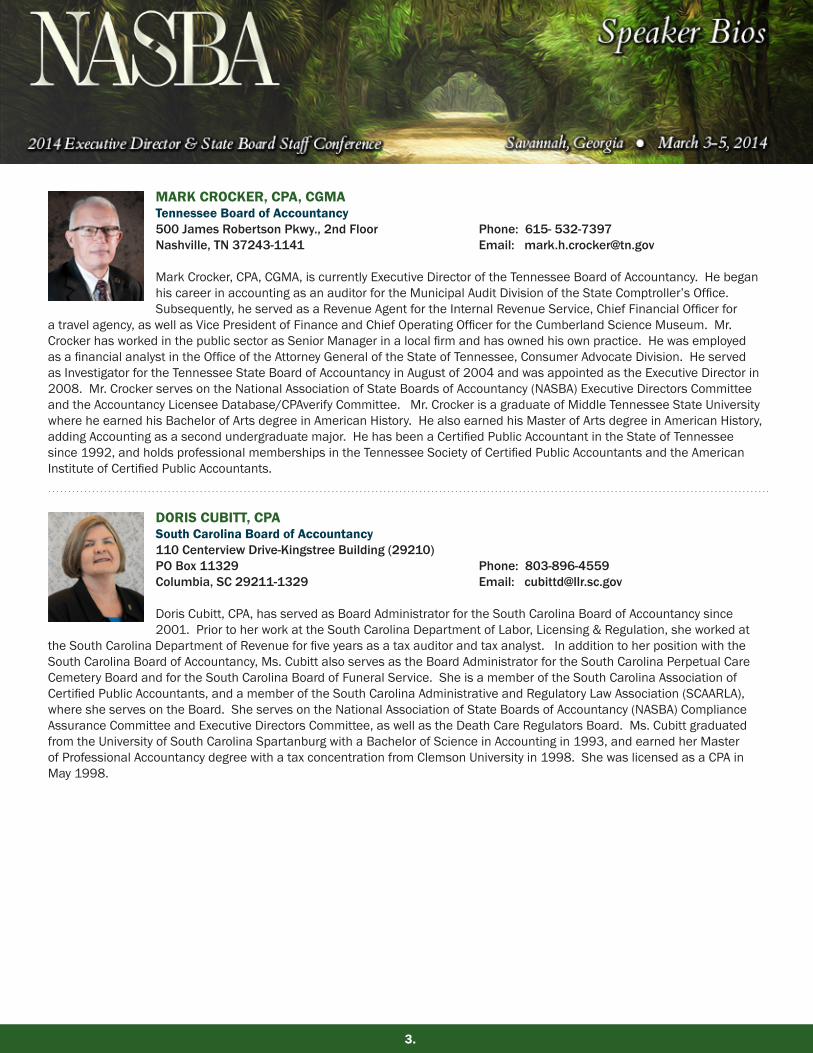

MARK CROCKER, CPA, CGMA Tennessee Board of Accountancy500 James Robertson Pkwy., 2nd Floor Phone: 615- 532-7397Nashville, TN 37243-1141 Email: [email protected]

Mark Crocker, CPA, CGMA, is currently Executive Director of the Tennessee Board of Accountancy. He began his career in accounting as an auditor for the Municipal Audit Division of the State Comptroller’s Office. Subsequently, he served as a Revenue Agent for the Internal Revenue Service, Chief Financial Officer for

a travel agency, as well as Vice President of Finance and Chief Operating Officer for the Cumberland Science Museum. Mr. Crocker has worked in the public sector as Senior Manager in a local firm and has owned his own practice. He was employed as a financial analyst in the Office of the Attorney General of the State of Tennessee, Consumer Advocate Division. He served as Investigator for the Tennessee State Board of Accountancy in August of 2004 and was appointed as the Executive Director in 2008. Mr. Crocker serves on the National Association of State Boards of Accountancy (NASBA) Executive Directors Committee and the Accountancy Licensee Database/CPAverify Committee. Mr. Crocker is a graduate of Middle Tennessee State University where he earned his Bachelor of Arts degree in American History. He also earned his Master of Arts degree in American History, adding Accounting as a second undergraduate major. He has been a Certified Public Accountant in the State of Tennessee since 1992, and holds professional memberships in the Tennessee Society of Certified Public Accountants and the American Institute of Certified Public Accountants.

DORIS CUBITT, CPA South Carolina Board of Accountancy110 Centerview Drive-Kingstree Building (29210)PO Box 11329 Phone: 803-896-4559Columbia, SC 29211-1329 Email: [email protected]

Doris Cubitt, CPA, has served as Board Administrator for the South Carolina Board of Accountancy since 2001. Prior to her work at the South Carolina Department of Labor, Licensing & Regulation, she worked at

the South Carolina Department of Revenue for five years as a tax auditor and tax analyst. In addition to her position with the South Carolina Board of Accountancy, Ms. Cubitt also serves as the Board Administrator for the South Carolina Perpetual Care Cemetery Board and for the South Carolina Board of Funeral Service. She is a member of the South Carolina Association of Certified Public Accountants, and a member of the South Carolina Administrative and Regulatory Law Association (SCAARLA), where she serves on the Board. She serves on the National Association of State Boards of Accountancy (NASBA) Compliance Assurance Committee and Executive Directors Committee, as well as the Death Care Regulators Board. Ms. Cubitt graduated from the University of South Carolina Spartanburg with a Bachelor of Science in Accounting in 1993, and earned her Master of Professional Accountancy degree with a tax concentration from Clemson University in 1998. She was licensed as a CPA in May 1998.

3.

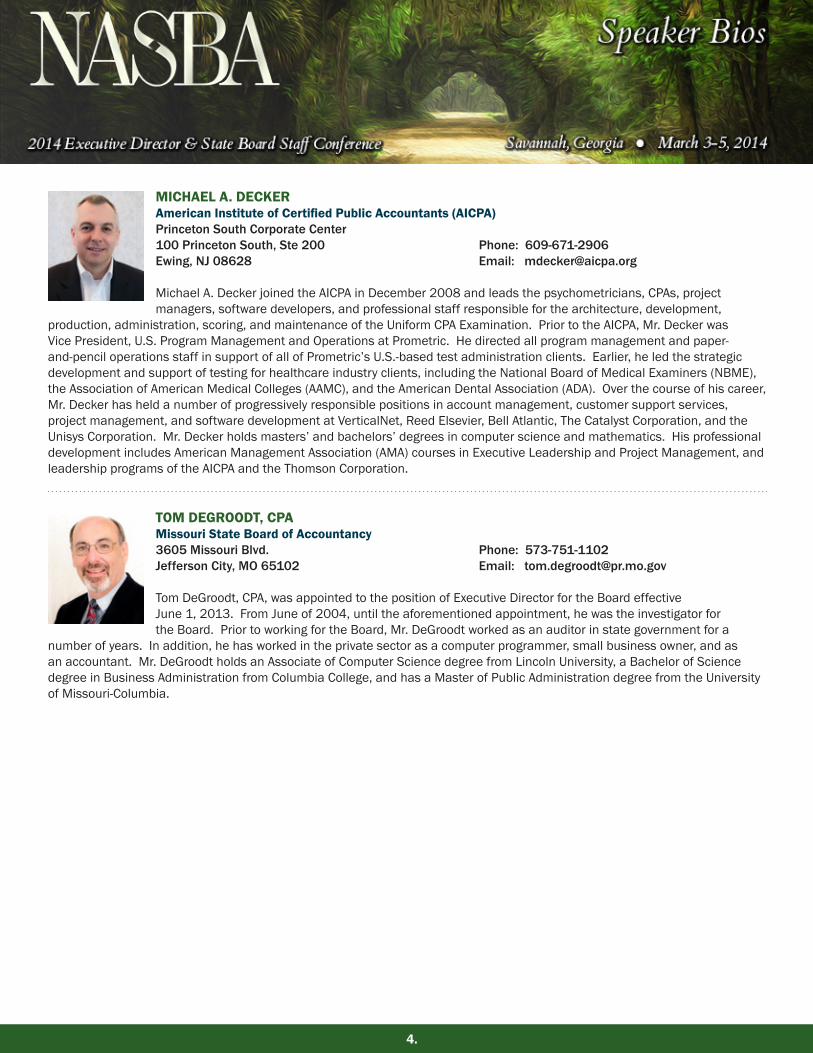

MICHAEL A. DECKERAmerican Institute of Certified Public Accountants (AICPA)Princeton South Corporate Center100 Princeton South, Ste 200 Phone: 609-671-2906Ewing, NJ 08628 Email: [email protected]

Michael A. Decker joined the AICPA in December 2008 and leads the psychometricians, CPAs, project managers, software developers, and professional staff responsible for the architecture, development,

production, administration, scoring, and maintenance of the Uniform CPA Examination. Prior to the AICPA, Mr. Decker was Vice President, U.S. Program Management and Operations at Prometric. He directed all program management and paper-and-pencil operations staff in support of all of Prometric’s U.S.-based test administration clients. Earlier, he led the strategic development and support of testing for healthcare industry clients, including the National Board of Medical Examiners (NBME), the Association of American Medical Colleges (AAMC), and the American Dental Association (ADA). Over the course of his career, Mr. Decker has held a number of progressively responsible positions in account management, customer support services, project management, and software development at VerticalNet, Reed Elsevier, Bell Atlantic, The Catalyst Corporation, and the Unisys Corporation. Mr. Decker holds masters’ and bachelors’ degrees in computer science and mathematics. His professional development includes American Management Association (AMA) courses in Executive Leadership and Project Management, and leadership programs of the AICPA and the Thomson Corporation.

TOM DEGROODT, CPAMissouri State Board of Accountancy3605 Missouri Blvd. Phone: 573-751-1102Jefferson City, MO 65102 Email: [email protected]

Tom DeGroodt, CPA, was appointed to the position of Executive Director for the Board effective June 1, 2013. From June of 2004, until the aforementioned appointment, he was the investigator for the Board. Prior to working for the Board, Mr. DeGroodt worked as an auditor in state government for a

number of years. In addition, he has worked in the private sector as a computer programmer, small business owner, and as an accountant. Mr. DeGroodt holds an Associate of Computer Science degree from Lincoln University, a Bachelor of Science degree in Business Administration from Columbia College, and has a Master of Public Administration degree from the University of Missouri-Columbia.

4.

ERIC DINGLER, CPADeloitte Service, LLP350 S. Grand Avenue, Suite 200 Phone: 213-593-4267Los Angeles, CA 90071 Email: [email protected]

Eric Dingler, CPA, is a Talent Development professional with 25 years of experience leading organizations through complex, large-scale changes. He joined Deloitte in 2008 as Chief Learning Officer for Deloitte Consulting. After five years, he became Director and Chief Learning Officer for Deloitte & Touche Audit. He

focuses on driving accelerated development for client service professionals through orchestrating an individual’s experiences, exposure and education against their expectations. While at Deloitte, he has led the implementation of a talent development strategy, development of marquee programs, a differentiated comprehensive learning curriculum and leaps forward in the technology and accessibility supporting the learner experience. This transformation included the implementation of Deloitte University, The Leadership Center, a physical university with a focus on leadership development. Mr. Dingler’s areas of specialization include such topics as adult learning theory, organizational and human dynamics, change-management, systems thinking, and coaching. His work emphasizes accelerating and sustaining shifts in mindsets and actions through a total ecosystem approach to building individual capabilities on a scale basis. Prior to joining Deloitte, Mr. Dingler held various leadership roles at Gap Inc., Bristol-Myers Squibb and The Coca-Cola Company. Most recently at Gap Inc, he served as Senior Director, Strategic Change and Senior Director of People and Organization Effectiveness, where he was directly responsible for learning and development, talent management, performance management, change management, and rewards and recognition. Previously, he served as Senior Director, Organizational Development, with Bristol-Myers Squibb, Princeton, New Jersey and Learning Consultant with The Coca-Cola Company in Atlanta, Georgia. In addition, he worked for 11 years in Arthur Andersen’s Business Consulting practice with a focus on consulting around the role talent plays in sustaining strategy and change. Mr. Dingler is a certified CPA. He has a bachelor’s degree in Business Administration – Accounting and Finance from the University of Pacific in Stockton, California and an M.B.A. from the University of California at Los Angeles.

IAN DINGWALL, CPAU.S. Department of Labor 122 C Street, NW, Suite 400 Washington, DC 20001

Ian Dingwall, CPA, assumed the position of the Employee Benefits Security Administration’s (EBSA) first chief accountant on July 1, 1988. He serves as EBSA’s primary adviser on accounting and auditing issues stemming from EBSA’s responsibilities under the Employee Retirement Security Act (ERISA) and the Federal

Employees’ Retirement System Act (FERSA). He was instrumental in developing and implementing the agency’s fiduciary audit plan for carrying out its responsibilities for the multi-billion dollar Federal Thrift Savings Plan. From 1969 to 1974, he was with the accounting firm of Ernst & Young, where he conducted financial audits and performed related tax services for clients. A graduate of the University of Maryland, Mr. Dingwall is a Certified Public Accountant in Maryland and a member of the American Institute of Certified Public Accountants and the Greater Washington Area Institute of CPAs. From 1974 to 1980, he was a senior accountant in the Division of Enforcement at the Securities and Exchange Commission, where he developed numerous cases involving accounting principles and auditing standards. Mr. Dingwall performed the functions of chief accountant to the Enforcement Division of the Federal Energy Regulatory Commission from 1980 to 1984. In 1984, he held the position of treasurer for Jack Kent, Inc. in Middleburg, Virginia. Previously, he was a supervisory auditor in the Special Litigation Division of the Office of the Solicitor, where he provided expert advice on accounting and auditing matters involving litigation of employee benefit plan cases. Mr. Dingwall was appointed to the AICPA’s first prestigious “Group of 100” to help shape the future role of the CPA profession. He received a “Hammer” award from former Vice President Al Gore for helping to “build a government that works better and costs less” and was listed as one of the”1997 Top 100 Most Influential People in Accounting” by the editors of Accounting Today. He is the recipient of the AICPA’s 2007 Outstanding CPA in Federal Government Award for his contributions to increase efficiency and effectiveness of government organizations and to the growth and enhancement of the profession. He presently serves as an observer “with privileges of the floor” to the Public Company Accounting Oversight Board’s Standing Advisory Group.

5.

OFELIA DURAN Colorado State Board of Accountancy1560 Broadway, Suite 1350 Phone: 303-894-7794Denver, CO 80202 Email: [email protected]

Ofelia Duran is the Program Director for Colorado’s Board of Accountancy, Offices of Barber and Cosmetology Licensure, Boxing, and Outfitters Registration. She has served in this capacity since June 2008. Prior to this role, she was the Assistant Director for the Office of Expedited Settlement, a centralized unit serving eight

different professions in settling pending disciplinary cases. Ms. Duran has served on NASBA’s Accountancy Licensee Database Task Force and currently serves on the Executive Directors Committee. She has extensive experience in regulatory matters and received her BSBA Degree in Business Management from the University of Colorado in 1999.

KIMBERLY FARACE, M.B.A. Prometric1501 South Clinton Street Canton Crossing Tower Phone: 443-455-6404Baltimore, MD 21224 Email: [email protected]

Kimberly Farace is a team leader for Client Services and Sales at Prometric. She is the account owner for the CPA Program and IQEX Program, and works directly with NASBA and the AICPA in administration of the

Uniform CPA Examination. Since starting at Prometric in November of 2000, she has worked with several key clients, including ETS International and Cisco. Prior to joining Prometric, she served as a financial analyst at Maryland General Physics in Columbia, MD, and as an analyst at Abt Associates in Bethesda, MD. Ms. Farace holds a Bachelor of Arts degree from Frostburg State University in Frostburg, MD, where she majored in international relations and economics. She also holds an M.B.A. from Loyola University Maryland’s Sellinger School of Business and Management in Baltimore, MD where she concentrated on international business.

CHERYL FARRARNational Association of State Boards of Accountancy (NASBA) 150 Fourth Avenue, North, Suite 700 Phone: 615-564-2140Nashville, TN 37219-2417 Email: [email protected]

Prior to joining NASBA as Chief Information Officer, Ms. Farrar served as an IT management consultant with The Kelso Group, a Nashville-based technology management consulting firm. Prior to The Kelso Group, she served as Senior Vice President for Strategic Sourcing with Universal Music Group’s global IT organization.

As Senior Vice President, Ms. Farrar was responsible for establishing the overall service provider and IT sourcing direction and management for the organization, and for providing leadership in the vision, planning, designing, implementation and maintenance of various critical information systems. A graduate of Pierce College with a Liberal Arts associate’s degree and The University of Phoenix with a bachelor’s degree in Business Management and Administration, Ms. Farrar is also the founder of the Spirit Oaks Ranch Equine Therapeutic Center (Los Angeles, CA) and White Fawn Farm Equine Therapeutic Center (Nashville, TN). Both centers specialize in providing equine therapeutic services to children with disabilities.

6.

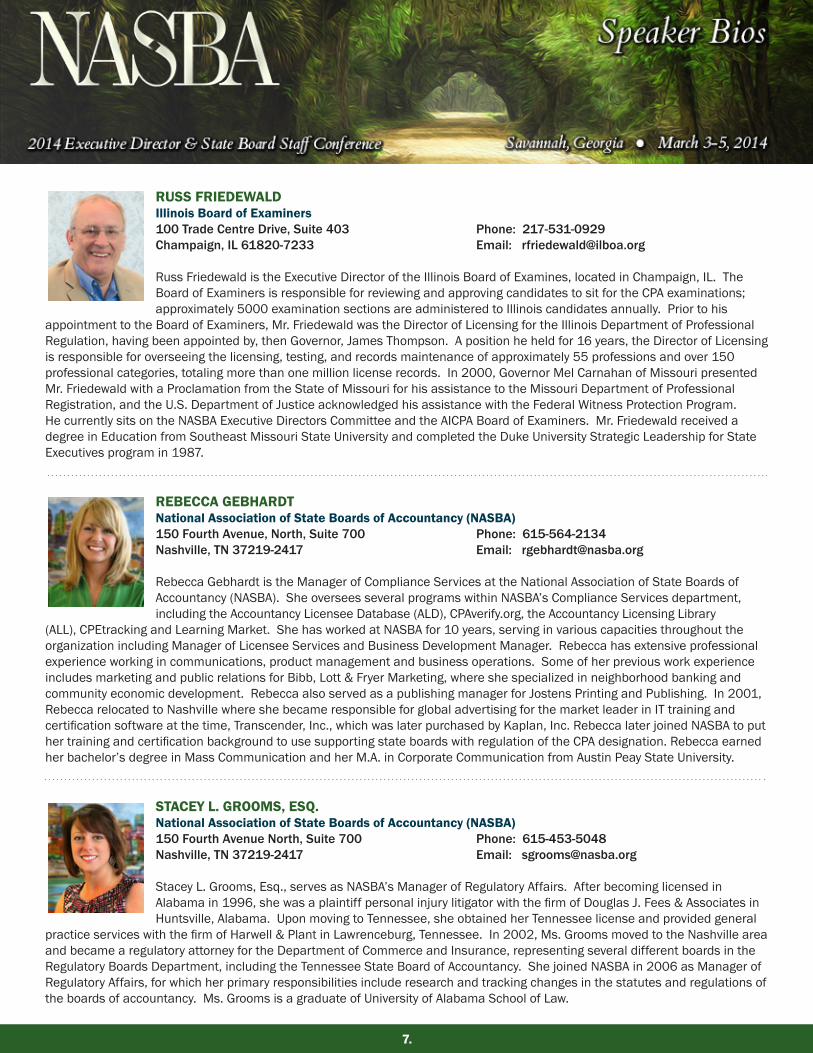

RUSS FRIEDEWALD Illinois Board of Examiners100 Trade Centre Drive, Suite 403 Phone: 217-531-0929Champaign, IL 61820-7233 Email: [email protected]

Russ Friedewald is the Executive Director of the Illinois Board of Examines, located in Champaign, IL. The Board of Examiners is responsible for reviewing and approving candidates to sit for the CPA examinations; approximately 5000 examination sections are administered to Illinois candidates annually. Prior to his

appointment to the Board of Examiners, Mr. Friedewald was the Director of Licensing for the Illinois Department of Professional Regulation, having been appointed by, then Governor, James Thompson. A position he held for 16 years, the Director of Licensing is responsible for overseeing the licensing, testing, and records maintenance of approximately 55 professions and over 150 professional categories, totaling more than one million license records. In 2000, Governor Mel Carnahan of Missouri presented Mr. Friedewald with a Proclamation from the State of Missouri for his assistance to the Missouri Department of Professional Registration, and the U.S. Department of Justice acknowledged his assistance with the Federal Witness Protection Program. He currently sits on the NASBA Executive Directors Committee and the AICPA Board of Examiners. Mr. Friedewald received a degree in Education from Southeast Missouri State University and completed the Duke University Strategic Leadership for State Executives program in 1987.

REBECCA GEBHARDTNational Association of State Boards of Accountancy (NASBA) 150 Fourth Avenue, North, Suite 700 Phone: 615-564-2134Nashville, TN 37219-2417 Email: [email protected]

Rebecca Gebhardt is the Manager of Compliance Services at the National Association of State Boards of Accountancy (NASBA). She oversees several programs within NASBA’s Compliance Services department, including the Accountancy Licensee Database (ALD), CPAverify.org, the Accountancy Licensing Library

(ALL), CPEtracking and Learning Market. She has worked at NASBA for 10 years, serving in various capacities throughout the organization including Manager of Licensee Services and Business Development Manager. Rebecca has extensive professional experience working in communications, product management and business operations. Some of her previous work experience includes marketing and public relations for Bibb, Lott & Fryer Marketing, where she specialized in neighborhood banking and community economic development. Rebecca also served as a publishing manager for Jostens Printing and Publishing. In 2001, Rebecca relocated to Nashville where she became responsible for global advertising for the market leader in IT training and certification software at the time, Transcender, Inc., which was later purchased by Kaplan, Inc. Rebecca later joined NASBA to put her training and certification background to use supporting state boards with regulation of the CPA designation. Rebecca earned her bachelor’s degree in Mass Communication and her M.A. in Corporate Communication from Austin Peay State University.

STACEY L. GROOMS, ESQ.National Association of State Boards of Accountancy (NASBA)150 Fourth Avenue North, Suite 700 Phone: 615-453-5048Nashville, TN 37219-2417 Email: [email protected]

Stacey L. Grooms, Esq., serves as NASBA’s Manager of Regulatory Affairs. After becoming licensed in Alabama in 1996, she was a plaintiff personal injury litigator with the firm of Douglas J. Fees & Associates in Huntsville, Alabama. Upon moving to Tennessee, she obtained her Tennessee license and provided general

practice services with the firm of Harwell & Plant in Lawrenceburg, Tennessee. In 2002, Ms. Grooms moved to the Nashville area and became a regulatory attorney for the Department of Commerce and Insurance, representing several different boards in the Regulatory Boards Department, including the Tennessee State Board of Accountancy. She joined NASBA in 2006 as Manager of Regulatory Affairs, for which her primary responsibilities include research and tracking changes in the statutes and regulations of the boards of accountancy. Ms. Grooms is a graduate of University of Alabama School of Law.

7.

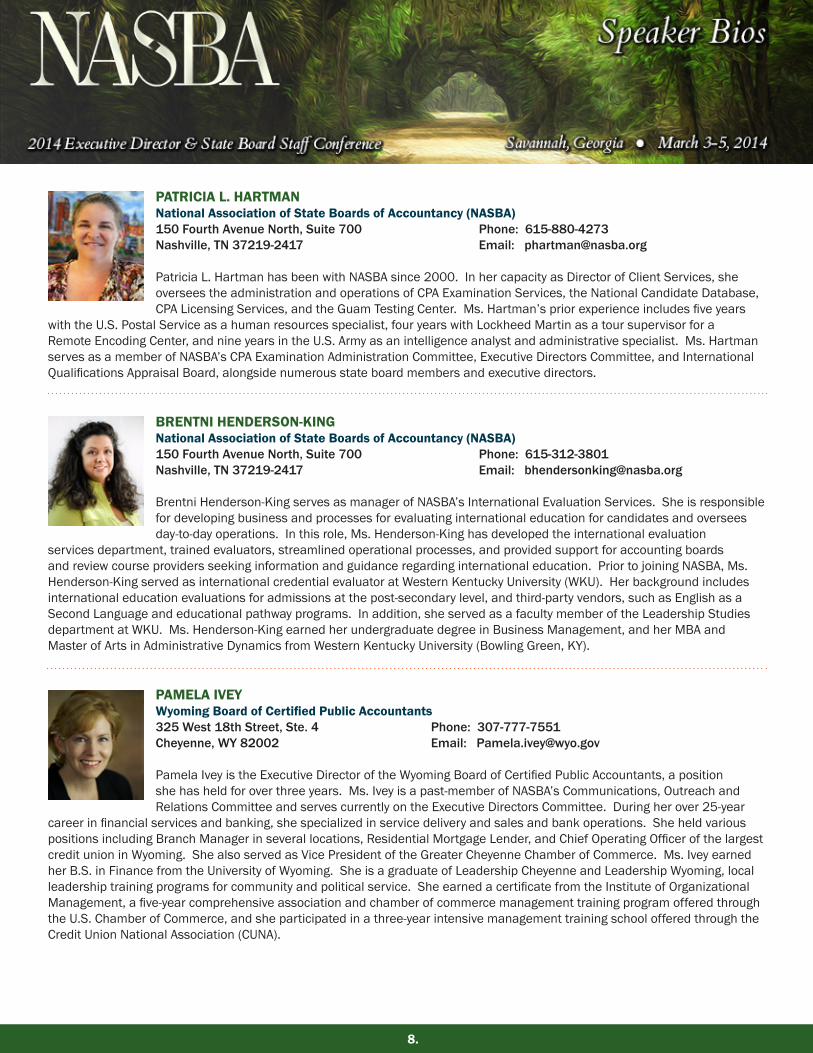

PATRICIA L. HARTMANNational Association of State Boards of Accountancy (NASBA)150 Fourth Avenue North, Suite 700 Phone: 615-880-4273Nashville, TN 37219-2417 Email: [email protected]

Patricia L. Hartman has been with NASBA since 2000. In her capacity as Director of Client Services, she oversees the administration and operations of CPA Examination Services, the National Candidate Database, CPA Licensing Services, and the Guam Testing Center. Ms. Hartman’s prior experience includes five years

with the U.S. Postal Service as a human resources specialist, four years with Lockheed Martin as a tour supervisor for a Remote Encoding Center, and nine years in the U.S. Army as an intelligence analyst and administrative specialist. Ms. Hartman serves as a member of NASBA’s CPA Examination Administration Committee, Executive Directors Committee, and International Qualifications Appraisal Board, alongside numerous state board members and executive directors.

BRENTNI HENDERSON-KINGNational Association of State Boards of Accountancy (NASBA)150 Fourth Avenue North, Suite 700 Phone: 615-312-3801Nashville, TN 37219-2417 Email: [email protected]

Brentni Henderson-King serves as manager of NASBA’s International Evaluation Services. She is responsible for developing business and processes for evaluating international education for candidates and oversees day-to-day operations. In this role, Ms. Henderson-King has developed the international evaluation

services department, trained evaluators, streamlined operational processes, and provided support for accounting boards and review course providers seeking information and guidance regarding international education. Prior to joining NASBA, Ms. Henderson-King served as international credential evaluator at Western Kentucky University (WKU). Her background includes international education evaluations for admissions at the post-secondary level, and third-party vendors, such as English as a Second Language and educational pathway programs. In addition, she served as a faculty member of the Leadership Studies department at WKU. Ms. Henderson-King earned her undergraduate degree in Business Management, and her MBA and Master of Arts in Administrative Dynamics from Western Kentucky University (Bowling Green, KY).

PAMELA IVEY Wyoming Board of Certified Public Accountants325 West 18th Street, Ste. 4 Phone: 307-777-7551Cheyenne, WY 82002 Email: [email protected]

Pamela Ivey is the Executive Director of the Wyoming Board of Certified Public Accountants, a position she has held for over three years. Ms. Ivey is a past-member of NASBA’s Communications, Outreach and Relations Committee and serves currently on the Executive Directors Committee. During her over 25-year

career in financial services and banking, she specialized in service delivery and sales and bank operations. She held various positions including Branch Manager in several locations, Residential Mortgage Lender, and Chief Operating Officer of the largest credit union in Wyoming. She also served as Vice President of the Greater Cheyenne Chamber of Commerce. Ms. Ivey earned her B.S. in Finance from the University of Wyoming. She is a graduate of Leadership Cheyenne and Leadership Wyoming, local leadership training programs for community and political service. She earned a certificate from the Institute of Organizational Management, a five-year comprehensive association and chamber of commerce management training program offered through the U.S. Chamber of Commerce, and she participated in a three-year intensive management training school offered through the Credit Union National Association (CUNA).

8.

WADE JEWELL Virginia Board of Accountancy9960 Mayland Drive, Suite 402 Phone: 804-367-8540Henrico, Virginia 23233 Email: [email protected]

As the Executive Director of the Virginia Board of Accountancy, Wade Jewell is responsible for providing regulatory enforcement, policy development, and coordination of services to constituents and stakeholders, budgeting, financial and operational management, and leadership to the organization. He has served

the Virginia State government since 1988. His early experience includes fifteen years with the Department of Corrections (to include positions in Financial Systems, Financial Reporting, and Budget Management), and shorter financial and operational management stints with the Department of Social Services, the Department of Transportation, and J. Sargeant Reynolds Community College. Just prior to joining the Board of Accountancy, Mr. Jewell spent almost three years with the State Compensation Board, leaving as the Assistant Executive Secretary with responsibilities for the Budget, Finance, Auditing, and Reporting & Policy Sections of the agency. Mr. Jewell holds a B.S. in Business Administration (Accounting) with honors from the University of Richmond. He is a 2004 graduate of the VDOT Executive Institute, a 2005 graduate of the Commonwealth Management Institute, a 2006 graduate of the Advanced Management Institute, and a 2008 graduate of the Virginia Executive Institute. He is a former board member and treasurer of the Virginia Executive Institute Alumni Association. Mr. Jewell currently serves on NASBA’s Executive Directors Committee and the ALD/CPAverify Committee.

CARLOS E. JOHNSON, CPA, ED.D.Oklahoma Accountancy Board3124 Lamp Post Lane Phone: 405-642-6235 Oklahoma City, OK 73120-5619 Email: [email protected]

Carlos E. Johnson, CPA, Ed. D., of Oklahoma City, Oklahoma, serves as chair of the National Association of State Boards of Accountancy (NASBA) Board of Directors for 2013-14. Previously, Mr. Johnson served as vice chair, director-at-large and southwest regional director of the NASBA Board. He is the chair of NASBA’s

newly established Leadership Development Group and former chair of NASBA’s Uniform Accountancy Act (UAA) Committee, Audit Committee, State Board Relevance and Effectiveness Committee, Legislative Support Committee and Substantial Equivalency Strike Force (Mobility Task Force). Additionally, Mr. Johnson is a former member of NASBA’s Administration & Finance, Regulatory Structures and Relations with Member Boards Committees. For 10 years, he served on the Oklahoma Accountancy Board, contributing three terms as chair and two terms as vice chair. Mr. Johnson currently serves as president of Carlos E. Johnson, CPA, PLLC, having retired from his position as senior investment banker with BOSC, Inc., a subsidiary of BOK Financial Corp. Additionally, he was a 24-year partner with KPMG, LLP, partner with the firm of Horne & Co. of Ada, Oklahoma, and Dean of the School of Business of East Central University of Ada, Oklahoma.

9.

JOHN W. JOHNSONNational Association of State Boards of Accountancy (NASBA)150 Fourth Avenue North, Suite 700 Phone: 615-880-4232Nashville, TN 37219-2417 Email: [email protected]

John W. Johnson is NASBA’s Director of Legislative and Governmental Affairs. Prior to joining NASBA, Mr. Johnson served as Director of Governmental Affairs for the Florida Institute of Certified Public Accountants (FICPA), where he was a registered lobbyist, responsible for the administration of the FICPA’s government

relations program (this included serving as staff liaison to the Florida State Tax Section, the State Legislative Policy Committee, State and Local Government Section, and the Common Interest Realty Association Section). A graduate of Florida State University, with degrees in Accounting and Political Science, Mr. Johnson became involved in government at a young age as an intern for former Florida State Senator, Van B. Poole. Upon graduating from FSU, he began his career as an auditor for the Division of Pari-Mutuel Wagering for the Department of Business and Professional Regulation, where he served for 12 years, and continued to move up through the ranks to Tax Audit Supervisor, Audit Administrator, Chief of Operations, Chief of Audit, and finally, Deputy Director. In 2002, he became Executive Director for the Florida Board of Accountancy and served in that capacity for four years.

RICHARD E. JONES, CPA, CGMAWashington Society of CPAs902 140th Avenue, NE Phone: 425-586-1124Bellevue, WA 98005 Email: [email protected]

Richard (“Rich”) E. Jones, CPA, CGMA is the President & CEO of the Washington Society of Certified Public Accountants, headquartered in Bellevue, Washington. The WSCPA has approximately 9,600 members and is the only organization in the State of Washington dedicated to serving the professional needs of

CPAs. Mr. Jones was named to this position in January 2005. Prior to assuming his leadership role at the WSCPA, he was an active member of the accounting profession, having served with Ernst & Young for over 33 years in their San Francisco, San Jose and Seattle offices. When he retired from Ernst & Young in 2004, he was Director of Tax for their Pacific Northwest offices, a position held since relocating to Seattle in 1989. Mr. Jones is an honors graduate of the University of California at Berkeley with a B.S in Accounting and attended the E&Y Executive Development Program, Kellogg School of Management, at Northwestern University. He is active in many civic and professional organizations, including the Fred Hutchinson Cancer Research Center (1995-2010)—Board of Directors, Treasurer; the Seattle Cancer Care Alliance (1998-Present)— Past Chair of Board, Chair of Integrity Committee; UW Medicine (2006-Present)—Vice Chair of Board, Chair of Compliance Committee; the Pacific Science Center (1996-2004)—Board of Directors, Treasurer; the Washington CPA Foundation (2005-2010)—Executive Director; Washington CPA/PAC (2005-Present);the CPA Society Executives Association (2006-Present)—Board of Directors, Past President; and the Accounting Careers Awareness Program (2005-2010)—Board of Directors. Mr. Jones is a licensed CPA in California and Washington and is a member of the California Society of CPAs, the Washington Society of CPAs, and the American Institute of CPAs. He has served on the Uniform Accountancy Act Committee and the Peer Review Board of the AICPA and on its Horizons 2025 Task Force.

10.

NICOLE KASIN, M.B.A. South Dakota Board of Accountancy 301 E. 14th Street, Suite 200 Phone: 605-367-5770 Sioux Falls, SC 57104 Email: [email protected]

Nicole Kasin is the Executive Director of the South Dakota Board of Accountancy, a position she has held since May 2006. Prior to her position with the Board, she was a Tax Program Representative with the South Dakota Department of Labor and Regulation. Ms. Kasin is the past chair of NASBA’s Executive

Directors Committee and is a former member of NASBA’s Communications, Outreach and Relations Committee, and Enforcement Resource Committee. Ms. Kasin received her B.A. and M.B.A. degrees in Business Administration from the University of Sioux Falls.

JESSICA LUTTRULL, CPANational Association of State Boards of Accountancy (NASBA)150 Fourth Avenue, North, Suite 700 Phone: 615-880-4245Nashville, TN 37219-2417 Email: [email protected] Jessica Luttrull, CPA, currently serves as NASBA’s Manager of the National Registry of CPE Sponsors. Ms. Luttrull graduated from the University of Tennessee (Knoxville) summa cum laude and became a Certified Public Accountant in the State of Tennessee in 1994. She joined NASBA as the Manager of the National

Registry in June 2010. Her primary responsibilities include the day-to-day operations of the National Registry of CPE Sponsors, which is a program to recognize organizations that provide continuing professional education (CPE) programs in accordance with nationally recognized standards. Ms. Luttrull also serves as the staff liaison to NASBA’s CPE Committee. Prior to joining NASBA, Ms. Luttrull spent her entire career with Ernst & Young in Nashville in the Company’s audit practice where she led audit and other transaction efforts with public and private companies in a variety of industries, including consumer products, hospitality, manufacturing, retail, healthcare and venture capital.

LEE D. MARTIN Internal Revenue ServiceSE:OPR, Room 7238/IR1111 Constitution Avenue NW Phone: 202-317-6375 Washington, DC 20224 Email: [email protected]

Lee D. Martin is the Deputy Director, Office of Professional Responsibility, Internal Revenue Service. Prior to this position, he was the Director, Enterprise Networks Operations in the Information Technology

organization. In that role, he was responsible for providing executive leadership over the operations and maintenance of the enterprise network infrastructure, while working closely with IT executives to ensure delivery of a world-class converged network and high quality services. Prior to joining the IRS, Mr. Martin held management positions with AT&T as Assistant Vice President-Project Management, Vice President-Information Systems/Chief Technologist for SBC Interactive - SmartPages.com, an on-line Directory Service, and Regional VP - Frame/ATM Provisioning Service Operations where he was responsible for ordering, design, provisioning, maintenance and repair of high-speed data services across SBC’s territory. He also has an extensive background in billing and collections with SBC, where he played a key strategic role at TelCel in Mexico City and Cable Northwest in Preston, England. Mr. Martin has an M.B.A. from Webster University in St. Louis and a Bachelor of Science Degree with dual majors in Math and Chemistry from Friends University. He is a Certified Project Management Professional and Six Sigma Green Belt. He was a recipient of the 2006 AT&T Excellence in Project Management Achievement Award for Leadership. Mr. Martin has received two NOVA Achievement Awards from Southwestern Bell for innovations to the business. He is a graduate of the Summer2008 Candidate Development Program.

11.

JOE MASLOTT, CPAAmerican Institute of Certified Public Accountants (AICPA)Princeton South Corporate Center100 Princeton South, Ste 200 Phone: 212-596-6200Ewing, NJ 08628 Email: [email protected]

Joseph Maslott, CPA, is the Senior Technical Manager for Test Development with the AICPA Examinations team, located in Ewing, NJ, since October 2006. Mr. Maslott has fifteen years of accounting experience as

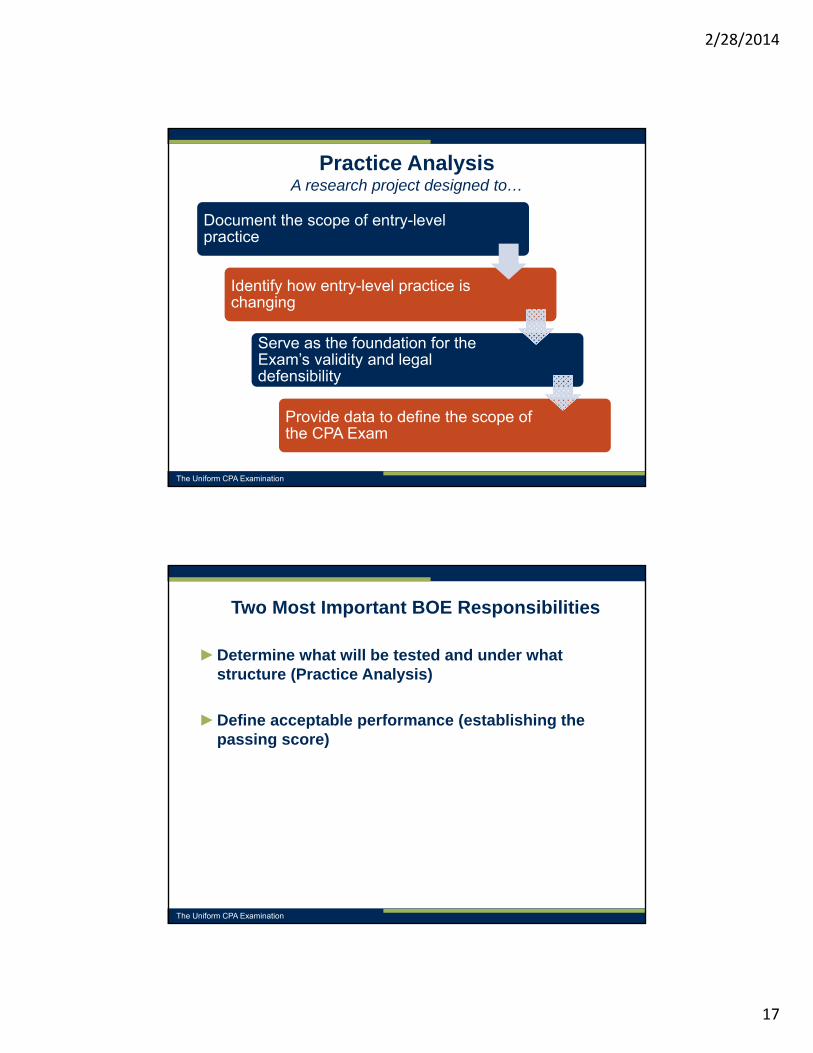

a CPA and has brought his expertise to the test development team at AICPA. He began his career at PriceWaterhouseCoopers in Toledo, Ohio, and then joined AT&T World Headquarters and E*TRADE Financial in management positions in accounting. As a lead CPA on the AICPA Examinations team, he has served in various roles including Staff Liaison for the AUD subcommittee and business owner of Simulation Development and Multiple Choice Question process reengineering. Mr. Maslott is currently the business owner for the upcoming practice analysis, a research project designed to document the scope of entry-level practice as well as serve as the foundation for the Exam’s validity and legal defensibility. Mr. Maslott earned his BS in Accounting from Bowling Green State University in Ohio in 1999.

DONALD A. MILLS, CPA, CFE, CFFTennessee Board of Accountancy500 James Robertson Pkwy., 2nd Floor Phone: 615.943.7040Nashville, TN 37243-1141 Email: [email protected]

Donald A. Mills, CPA, has been an Investigator for the Tennessee State Board of Accountancy since 2009. Prior to that, he was the Audit Manager for the Hamilton County Department of Education. He has also worked in public accounting and was a senior auditor with the Tennessee Division of Municipal Audit. Mr.

Mills is a graduate of the University of Tennessee at Knoxville. He is a Certified Public Accountant, a Certified Fraud Examiner, and holds the Certification in Financial Forensics from the American Institute of Certified Public Accountants. Mr. Mills is a member of the Tennessee Society of CPAs, the American Institute of CPAs, the Association of Certified Fraud Examiners, the Forensic CPA Society, and the Antique Automobile Club of America.

RANDALL A. ROSS, CPA, M.B.A.Oklahoma Accountancy Board201 NW 63rd Street, Suite 210 Phone: 405-317-1244 Oklahoma City, OK 3116 Email: [email protected]

Randall (“Randy”) Ross, CPA, is currently the Executive Director of the Oklahoma Accountancy Board. He received both his B.S. in Accounting and his M.B.A. from the University of Central Oklahoma while earning All-American status in wrestling. His career has comprised a broad background of public, private, and

governmental accounting and work experience. He served as Director of Business Taxes at the Oklahoma Tax Commission, and Corporate Controller for an international manufacturing concern, among positions in public accounting during his career. Mr. Ross has received numerous awards including National Administrator of the Year in 1995, Outstanding CPA in Industry in Oklahoma in 2006, Mayor of the Year in Oklahoma for cities over 5,000 in 2011, and most recently, he was honored as a Distinguished Former Student by the University of Central Oklahoma.

12.

DAVID N. SANFORD, CPA.CITP Guam Board of Accountancy 335 South Marine Corps Dr, Ste 101 Phone: 671-647-0813 x102 Tamuning, Guam 9691 Email: [email protected] [email protected] Dave N. Sanford, CPA.CITP, has served as the Executive Director of the Guam Board of Accountancy since 2004, under an administrative services contract between Sanford Technology Group LLC (STG) and the

Board. He has lived and worked in Guam, Saipan and Micronesia since 1978, and has worked throughout the Far East in public accounting. He subsequently served as a financial controller for Duty Free Shoppers Ltd (DFS) in Saipan and Guam, and was also appointed as VP-Finance for the DFS credit card subsidiary, formed in Hong Kong in 1982. After relocating the DFS corporate accounting office from Honolulu to San Francisco in late 1984, Mr. Sanford returned to Guam and subsequently formed an integrated computer services company with his spouse, Toni, in 1986. Today, STG provides payroll processing and IT services throughout Guam, CNMI and Micronesia. Augmenting Dave’s professional endeavors are his memberships and service with various community and business organizations, including his parish financial council, Guam and CNMI tax commissions, and chambers of commerce. In service to the CPA profession, he has participated in all aspects of the Guam Society of CPAs administration since 1980, and served as a member of the AICPA Governing Council from 2003 through 2012.

RICHARD C. SWEENEY, CPA Washington State Board of AccountancyP. O. Box 9131 Phone: 360- 586-0163Olympia, WA 98507-9131 Email: [email protected]

Richard C. Sweeney, CPA, was appointed Executive Director of the Washington State Board of Accountancy in 2005. Previously, he served as the Director for Regulatory Affairs for the Washington State Auditor. His responsibilities included monitoring CPA contractors providing services to state and local government, and

monitoring developments in accounting and auditing oversight by the Washington State Board of Accountancy, the General Accountability Office, and the Public Company Accounting Oversight Board. Mr. Sweeney also maintained a private consulting business. As a private consultant, his activities included providing litigation support for attorneys in CPA malpractice defense cases, and consulting services to CPA firms and other enterprises. He also developed and delivered tailored training programs for numerous professional and business organizations. Mr. Sweeney is licensed to practice public accounting in Washington State. He is a member of the AICPA. Mr. Sweeney served on NASBA’s Executive Directors Committee and is a former chair of that Committee. He has also previously served on the Accountancy Licensee Database (ALD) Task Force. He is a current member of NASBA’s Legislative Support Committee (the 2012-2013 successor to the former Legislative Support and State Board Relevance and Effectiveness Committees) and NASBA’s Awards Committee. Mr. Sweeney is the 2013 recipient of the Lorraine P. Sachs Standard of Excellence Award.

FRANK X. TRAINOR, ESQ.North Carolina State Board of CPA Examiners1101 Oberlin Road, Suite 104 PO Box 12827 Phone: 919-715-9185Raleigh, NC 27605-2827 Email: [email protected]

Frank X. Trainor, Esq., has been the staff attorney for the North Carolina State Board of CPA Examiners since 2011. He provides general legal advice to the Board and also is in charge of the Board’s Professional

Standards section which focuses on the discipline of CPAs in the State of North Carolina and enforcement against the unauthorized use of the CPA title in the State. Prior to his current position, Mr. Trainor was in private practice focusing on administrative law. He represented other occupational licensing boards as well as numerous licensees facing disciplinary action. He earned his bachelor’s degree at the University of North Carolina in Chapel Hill and his J.D. at Tulane University.

13.

1.

ALABAMA STATE BOARD OF PUBLIC ACCOUNTANCY

Budget Constraints Alabama’s Governor lifted the freeze on merit pay raises beginning January 1, 2014. The freeze had been in place since January 1, 2009.

Board Staff Changes At the November 2013 board meeting, the Alabama Board approved the following personnel action: Created a temporary part-time accountant position to assist the board with the implementation of the Alabama Immigration Law, which requires licensing boards to verify citizenship or lawful presence in the United States for individuals renewing a professional license.

Technology Changes The Board’s website underwent a revamping during the summer of 2013, to improve the aesthetics and make it more user-friendly. A new web application was also added to enable board members to access board materials electronically. Board staff continue to work toward making Board disciplinary actions available on the Board’s website.

On-line License Renewals. The Board discontinued mailing paper registration forms, beginning with fiscal year October 1, 2013 – September 30, 2014. All licensees were notified by mail, followed by three email reminders to register on-line for the 2013-2014 registration period. On-line license renewals for the first quarter increased to 85% for 2013-2014 registration period, as opposed to about 30% for the previous years.

Disciplinary and Enforcement Activities including SEC and IG Referrals The Alabama Board held Administrative Hearings on January 31, 2014 and took the following disciplinary actions:

- Revoked 21 CPA certificates and one firm for failure to register and renew their annual licenses. In addition, 52 CPA certificates were revoked for failure to respond to the Board’s inquiries related to the Alabama Immigration Law, a violation of Board Rules and Statute.

ALASKA STATE BOARD OF PUBLIC ACCOUNTANCY The Board will have one long-term Board member (Kathleen Thompson, CPA) term out as of 3/1/14. New Board member (Leslie Schmitz, CPA) has already been appointed, effective 3/1/14.

HB302 was introduced. This bill contains clean-up and clarifying language.

Budget Issues - The Board continues to encounter issues with obtaining approval for all requested Board/staff travel.

- The Division continues to review/work on third-party reimbursements; currently, there is a cap on the amount of third-party reimbursements that can be accepted for all boards within the Division. **Third-party reimbursements are trips that are paid for by outside organizations; State policy requires that the State reimburse the staff or Board member and then ‘bill’ the outside organization after the trip. At this time, the Boards are required to estimate a full fiscal year ahead and then the allowable total is shared for all professions within the Division (currently capped at $20k). - HB187 was introduced by the Division. This bill intends to have the general fund pay $1.7 million in investigative (personnel) costs. This change would reduce the amount of costs being charged directly to boards within the Division.

2.

ARIZONA STATE BOARD OF ACCOUNTANCY

Statutes and RulesThe Arizona Board of Accountancy passed Laws 2013, Ch. 136 (HB 2260), which was effective September 13, 2013. The primary purpose of the legislation was to better organize the statutes in our Title to be more clear and readable. For instance, we have three separate statutes dealing with certification that have now been drafted in one section. We also had references to fees throughout the title, which are now all contained in a single statute. The legislation creates reinstatement requirements for cancelled (A.R.S. §32-730.02), expired (A.R.S. §32-730.03), retired (A.R.S. §32-730.04), relinquished (A.R.S. §32-741.04), and revoked (A.R.S. §32-741.03) certificates. The Board also created a retirement status and authorized the adoption of MRAs. The Board also reduced the registration fees for retired and inactive status from $300 every two years to $50 and $150 respectively.

The Board also adopted new rules that became effective February 4, 2014. The rules were updated to address issues due to the passage of Laws 2013, Ch. 136, HB 2260, effective September 13, 2013; to address issues delineated in the Board’s 2008 Five Year Rule Review, which could not be addressed sooner due to a moratorium on rule making; to ensure that the rules reflect the Board’s operating practice; and to provide technical, clarifying, and conforming changes to improve the organization and readability of the rules for the public. Among many things, the rules provide that reinstatement applicants must provide evidence of completed CPE (course outlines and certificates of completion) and the Board now allows for CPE credit in half-hour increments for periods of not less than one hour, whereas CPE is currently only credited in whole hours.

Fees and Fines As a part of its rule package, the Board increased its late fee for registrations from $25 to $50.

International Professionals Seeking Recognition/Mutual Recognition Agreements As part of Laws 2013, Ch. 136, HB 2260, the Board has now adopted all NASBA approved mutual recognition agreements and will accept IQEX in lieu of the Uniform CPA exam.

Sunset Legislation or Reviews The Board will be undergoing a sunset review in the summer of 2014.

Retired Status Approvals

3.

ARKANSAS STATE BOARD OF PUBLIC ACCOUNTANCY

Rule Changes - CPA exam candidates can now sit with a bachelor’s degree (150 hours still required for licensure) - New retired status created for those CPAs who sign an affidavit stating that they are no longer working in any capacity. New status relieves the CPA of any CPE reporting and annual registration.

Proposed Rule Change- Currently, we require four (4) hours of ethics every three years; new rule will require one (1) of the four (4) hours to be on state board laws and rules.

Operations- Changed license database from GL Suite to Access based application.- Scanned all licensee files for better security/ease of access to information.

CALIFORNIA BOARD OF ACCOUNTANCY

Mobility Effective July 1, 2013, California implemented a no-fee and no-notice practice privilege (mobility) program. One public protection element of the program is that California is required to post a list of all CPAs who were disciplined by the SEC and PCAOB on its website. Additionally, the disciplined CPA is required to request approval from the CBA prior to practicing in California under mobility. CBA staff contacts the CPAs and informs them of this requirement via regular mail. Please visit the CBA website www.cba.ca.gov to search for CPAs listed from your jurisdiction. Mobility Stakeholders GroupIn 2012, California passed legislation that allowed mobility for California. The same legislation created the Mobility Stakeholder Group (MSG) for the purpose of considering whether the provisions of California’s practice privilege law are consistent with the CBA’s duty to protect the public, and whether the provisions of practice privilege law satisfy the objectives of stakeholders of the accounting profession in California, including consumers. The members of the MSG have been appointed and it will hold its first meeting in March 2014. Peer Review ReportingWhen California’s peer review requirement first took effect in January 2010, the CBA established a three-year phase-in period for reporting. This phase-in period began in July 1, 2011 and was completed July 1, 2013. This initial phase-in period was based on the last two digits of a licensee’s license number. The CBA revised the reporting requirement to now occur at the time of license renewal, which began January 1, 2014. FingerprintingBeginning with licenses that expire after December 31, 2013, all licensees renewing their license in an active status who have not previously submitted fingerprints as a condition for initial licensure or for whom no electronic record of the licensee’s fingerprints exists with the California Department of Justice (DOJ) must submit fingerprints for the purpose of having a State and federal criminal offender record background check. Continued Exploration of California’s Attest Experience Requirement and Allowing Academia as Qualifying Experience for CPA LicensureFor a significant portion of 2013, the CBA established a Taskforce (known as the Taskforce to Examine Experience for CPA Licensure) that explored California’s experience requirement for CPA licensure. As a result of the Taskforce’s work, for the upcoming year, the CBA will be undertaking a research project regarding the attest experience requirement and moving forward with sponsoring legislation to allow for experience earned in academia to qualify toward California’s general experience requirement.

continues

4.

CALIFORNIA BOARD OF ACCOUNTANCY (continued)

The research project associated with the continued exploration of California’s attest experience requirement will entail performing a survey of California’s licensees. The CBA will be engaging the services of a consultant to aid in the data collection and preparing a final report. Additionally, the CBA will be surveying other state boards of accountancy to obtain relevant data and information. As for allowing academia experience to qualify, the Taskforce recommended that the CBA explore allowing qualifying academia experience, as it believed it could aid in bridging the gap between theory and practice, and benefit both the students and accounting profession. The CBA adopted the Taskforce’s recommendation to allow for experience earned in academia to qualify for general accounting experience. For the upcoming year, the CBA will be sponsoring legislation to amend California’s Accountancy Act and will begin discussion on establishing a framework for how academia experience will qualify.

COLORADO STATE BOARD OF ACCOUNTANCY

Review of the past YearThe Board adopted new rules on March 20, 2013, and they became effective on July 1, 2013, except for the CPE Chapter 7, which became effective, January 1, 2014, to line up with the start of the next CPE reporting period.

Amendments were made to all twelve chapters. Some had substantive changes and others did not.

Challenges2013 Renewal:- The CPA licenses in Colorado expired on November 30, 2013, one month before the end of the CPE reporting period (December 31, 2013). The Board office heard concerns about this shift and it caused some confusion because the renewal attestation contained language that said, “(1) I have completed all Required CPE for the Reporting Period; OR (2) I will complete all Required CPE by the end of the Reporting Period (December 31, 2013). I understand that my compliance with the continuing education requirements is subject to an audit by the Board.”

- During the 2013 renewal, the CPAs were discouraged from changing the status of the license until the renewal was complete. Change of status requires a separate notice or application and fee (inactive-no fee or retired-fee).

Future Initiates/Outreach- Since early February, the division staff and IT staff have been in the initial stages of discovering/testing the file layout for ALD implementation.

- Given the nature of the rule changes and the fast approaching June 30, 2015 deadline for the 150 change, there are plenty of outreach opportunities that will be explored to inform the various stakeholders about the upcoming changes, and to reinforce the changes/expectations of the licensed stakeholder group.

COMMONWEALTH OF THE NORTHERN MARIANA ISLANDS

No update has been provided for Commonwealth of the Northern Mariana Islands.

CONNECTICUT STATE BOARD OF ACCOUNTANCY

No update has been provided for Connecticut.

DELAWARE STATE BOARD OF ACCOUNTANCY

No update has been provided for Delaware.

5.

DISTRICT OF COLUMBIA BOARD OF ACCOUNTANCY

It is an exciting time for the District of Columbia Board of Accountancy. The Board will be tackling several major projects this year. At the top of the list, the Board is working to make the District of Columbia “a hub” for examination and licensure of foreign nationals. We believe this is an important goal, as expanding licensure in this way promotes higher standards, leading to a higher quality of public accounting services, and protection of the public, for both our citizens and citizens in other nations. We are working with local institutions of higher education, including Howard University, to create a local chapter of the Student Center for Public Trust. The Board will also be working this year to revise and update its statutes and regulations to bring them in line with current practices. Administratively, our operations continue to flow smoothly. We continue to innovate and improve our electronic application and licensing platform. The Board looks forward to a productive year in the District of Columbia, and will continue to tackle any challenges presented in the name of protecting the public.

FLORIDA BOARD OF ACCOUNTANCY

The Florida Board of Accountancy has begun promulgating rules to implement peer review as a condition for firm licensure, effective for the 2015 renewal cycle. In July of 2013, the Board began conducting level one background checks for those applicants applying for licensure. Legislation has been introduced in the 2014 session to expand this requirement for individuals applying to sit for the CPA examination.

The Board’s staff was expanded to include three administrative support positions, two additional full time investigators, bringing the total to three investigators, and for the first time, two attorneys dedicated to prosecuting accountancy cases.

In an effort to decrease surplus cash; the Board reduced individual renewal fees for the 2013 and 2014 renewal cycles. For the fiscal year ending June 30, 2014, the Board was appropriated $100,000 for an advertising program to combat unlicensed activity; up from $60,000 in the previous fiscal year.

In August of 2013, the Board, through the Clay Ford Scholarship Program, awarded $192,000 in scholarships to minorities seeking to complete education for licensure as certified public accountants. The Board’s appropriation for scholarships was increased from $100,000 in 2012 to $200,000 for the budget which took effect July 1, 2013. Governor Rick Scott has released his proposed budget for the next year and again included $200,000 for the Board’s scholarship program.

For calendar year 2014, we will be working to redesign our website and are looking to create at least one informational video.

GEORGIA STATE BOARD OF ACCOUNTANCY

No update has been provided for Georgia.

GUAM BOARD OF ACCOUNTANCY

The Guam Board of Accountancy (the Board) has drafted legislation to adopt mobility and to update the Guam Accountancy Act and rules for other UAA changes recommended over the last 7-8 years. We will submit this draft to our legislative oversight committee in March and we expect this legislation to pass by the end of 2014.

The Board is slowly recuperating from the loss of over 80% of the Japanese candidates sitting in the Guam Computer Test Center (GCTC), which is celebrating its 10th anniversary in April 2014, having administered the very first computer-based CPA exam in April 2004 on Guam, “where America’s day begins”! We are seeing increased numbers of Chinese candidates from mainland China, as well as Hong Kong and Taiwan, but the visa process for the mainland Chinese is lengthy and costly, so we are still left with a GCTC volume of candidates about equal to our 2004-2005 volume.

continues

6.

GUAM BOARD OF ACCOUNTANCY (continued)

Even so, the Board has accumulated a surplus in excess of $1mm and is pushing a plan to implement the Guam Accountancy Endowment Fund, as an “agency-advised” endowment fund with the University of Guam Foundation. As an agency-advised endowment, the Board is able to act as an advisor with oversight of and participation in the programs conducted, and can be reimbursed with endowment funds for activities conducted on behalf of the University of Guam (UOG) Accounting program. The goal of this endowment is to supplement the UOG Accounting program with visiting professors, a lecture series and such, to bolster the University’s ability to meet the 150 hour educational requirement for Guam resident CPA exam candidates.

The Board has unanimously opposed firm mobility, and sees no real benefit from such, other than for multi-jurisdiction firms, especially so in a closed economic environment such as Guam. Without clarifying firm mobility implementation, it is difficult to see any benefit exceeding the costs of lost board revenues, expenditure of political capital, magnified enforcement uncertainty and jeopardized relevancy.

The Board continues to operate with our same staff of four (since 2001), and has issued over 2,000 licenses, with more than 600 of these active today.

HAWAII BOARD OF PUBLIC ACCOUNTANCY

- The Board continues to work on the implementation of mandatory peer review, which is required for firms to renew their permits to practice for renewal period beginning January 1, 2018. Preliminary registration requirements become effective on or before December 31, 2015.

- In spite of the fact that Hawaii is the last state to adopt individual CPA mobility, it appears that efforts to propose mobility legislation for this legislative session have been exhausted.

- Online license/permit renewals continue to be very successful, with participation rates of 90% or better.

IDAHO STATE BOARD OF ACCOUNTANCY

- The Idaho Board welcomed one new member this past year, David Westfall, CPA. There are currently seven board members who each have a term of five years. Two board members will see their terms expire in 2014.

- The online license renewal system continued to be utilized by Idaho licensees with 97.8% of renewals in 2013 occurring through the online system. Online CPE reporting continued to be close to 100%.

- The Idaho Board has begun discussions with our database vendor to begin supplying firm information to the ALD. With the help of NASBA’s ALD team, hopefully this will be complete during 2014.

- There were no rule changes taken to the Idaho Legislature by the Accountancy Board during the 2014 session but 2015 looks to be a different story at this point. There are also no current bills in the legislature that would have a major impact to the Accountancy Board. Last session, Senate Bill 1068 was passed and became effective in Idaho on July 1, 2013. It gave the Board the authority to promulgate rules to implement this legislation, which would expedite CPA licensure for active duty service members and their spouses.

- Formal complaints filed increased in 2013 over the previous year but were still in line with averages over the five years prior to 2012.

7.

ILLINOIS BOARD OF EXAMINERS

- Passed a new sunset legislation through 2024

- Discontinued our relationship with the University of Illinois, which began in 1903—110 years

- Affiliated exclusively with Northern Illinois University

- Moved our office from Champaign, IL to Naperville, IL

- Hired eight (8) new staff members

ILLINOIS DEPARTMENT OF FINANCIAL AND PROFESSIONAL REGULATION

The Illinois Public Accounting Act went through sunset review in 2013. As a follow-up from this legislation, the Rules for the profession will be reviewed to determine what changes need to be made to accommodate the revisions to this Act.

INDIANA BOARD OF ACCOUNTANCY

A total of 955 CPE audits were conducted for the 2012 renewal period. There were 204 licensees found to be noncompliant for the continuing education audit. The maximum fine assessed was $5000.

The Board and the Indiana Society is in support of new legislation that is asking for increased terms for board members, adding a retired status, definition of attest, and increasing the board’s investigative fund cap to $1,000,000 before it reverts to the general fund.

The Peer Review Oversight Committee in 2013 has reviewed ten reports. The Committee has referred seven reports to the Office of the Attorney General for investigation.

Approximately 264 reviews were processed during year one of the licensing cycle (2012).

Approximately 158 reviews will be processed during year two of the licensing cycle (2013).

Approximately 162 reviews will be processed during year three of the licensing cycle.

IOWA ACCOUNTANCY EXAMINING BOARD

No update has been provided for Iowa.

KANSAS BOARD OF ACCOUNTANCY

- Rule changes to update materials made by reference

KENTUCKY STATE BOARD OF ACCOUNTANCY

- Under the governor’s budget proposal, we are to have $500,000 transferred out of our surplus account and into the general fund.

- We were going to try to come up with a plan for scholarships, but that is no longer a priority.

8.

STATE BOARD OF CPAs OF LOUISIANA

Employee ChangesBoth our executive director and deputy director retired within the past year after 17 and 25 years of service, respectively. Seventy-five percent of our staff is relatively new, having worked for our agency about two years or less. That brings a lot of challenges and a big learning curve for everyone, but it also allows for opportunities to review our processes to determine what changes might be needed.

CommunicationWe are focusing on communication with our licensees on many tracks. One goal is to generate electronic communications, such as a quarterly newsletter, to communicate and educate our licensees and other interested parties on such things as CPE rules, disciplinary actions, new CPA exam passers, board meetings, etc.