your point of independence questionnaire booklet8.pdf · the goal of this questionnaire is to jump...

TRANSCRIPT

YOUR POINT OF INDEPENDENCE QUESTIONNAIRE

Copyright © 2012 Russell Holcombe

Name

Happiness is being in control of your destiny.

The goal of this questionnaire is to jump start

your journey towards this peaceful place.

“THOUGHTFUL FINANCIAL

PLANS PROTECT LIFESTYLE,

AND YOUR LIFESTYLE IS

DEPENDENT ON CASH FLOW.”

– RUSSELL E. HOLCOMBE

Painted Picture

“EVERY DAY WHEN YOU AWAKE, ASK

YOURSELF, WHAT DO I REALLY, REALLY, REALLY

WANT. YOU HAVE TO SAY REALLY, REALLY,

REALLY, OTHERWISE YOU WON’T BELIEVE IT.”

Your Painted Picture is what your best life looks like. This picture slows

your dream down so you can catch it. For example, most people have a mental picture of their dream

house. The yard, the pool, the smell of fresh flowers, even the morning sunrise warming the master

bedroom. It’s so real.

Using this same process, create a mental picture of your life three years from today. What does it feel

like? What are you doing? What have you stopped doing? What hurdles have you cleared?

Fun exercise: Get your spouse/partner to do it separately and compare notes.

- Elizabeth Gilbert

Write as much as you can about your image below.

OurLeverage Points

WHEN YOU MAXIMIZE YOUR GIFTS,

FLOW HAPPENS. FLOW BY DEFINITION

IS EFFORTLESS ACCOMPLISHMENT.

In physics, leverage is the ability to move a large weight with minimal effort. We all have something special in our lives that gives us strength. When we

manage our strength properly, we create our own opportunity. Maximizing these opportunities increases

the likelihood of your financial independence. Write down the things that provide you strength. (i.e.

royalty income, income producing real estate, pensions, stock options, no debt, etc.)

Write down the things that provide you strength.

Hurdles and Torpedoes

HurdlesOk, remember your Painted Picture? What is standing in the way of it becoming a reality? What are the

frustrations and roadblocks? It may be the house you can’t sell, the business that isn’t performing or the

investment manager that never seems to get it. To make your Painted Picture come to life, you must do more

than wait for things to change, you must take the initiative and change them.

1 If I could , my life would be so much better.

2

3

4

5

TorpedoesTorpedoes sink ships. They are the silent enemies of our financial independence. Some we can anticipate

and others we can’t. Flight simulators take pilots to the emotional edge to build the proper instincts to

handle catastrophe. For this exercise, it is important to focus on the events in your life that could have

a major financial impact. Loss of job, pension stops because company goes bankrupt, you pull out in

front of a school bus full of children, partner terminates you unexpectedly, employee steals money, are

just some of the things we have seen. It does not matter how remote the possibility – the outcome is

precise. You must lean heavily into the impossible to expose the things that could go wrong.

1 I would be in big trouble if happens.

2

3

4

5

Write your hurdles below.

What would have a major economic outcome in your life?

Your Point of Independence is your finish line. When you have built sufficient, consistent cash flow to fund your wants and needs, you have reached the finish line. It does not mean you have to stop running, but that you have options. And having options is the secret to happiness.

On the following pages you fill find the building blocks of creating your own Point of Independence. Fill your numbers in on each page. You will see totals at the bottom.

YOUR POINT OF INDEPENDENCECALCULATED

Money In

MONEY IN

JOB SOCIAL SECURITY ALIMONY

PENSION

RENTAL INCOME

Below are common examples of Money In and

many blank spaces for you to fill in on your own.

Please use annual numbers only.

Money In is critical to our survival. Creating money inflows that are permanent is

the key to long term success. You must understand the building blocks of cash flow to figure out how

hard your investment accounts must work to keep you going. Therefore, you must ignore any money

inflows from your personal investment accounts including your IRA.

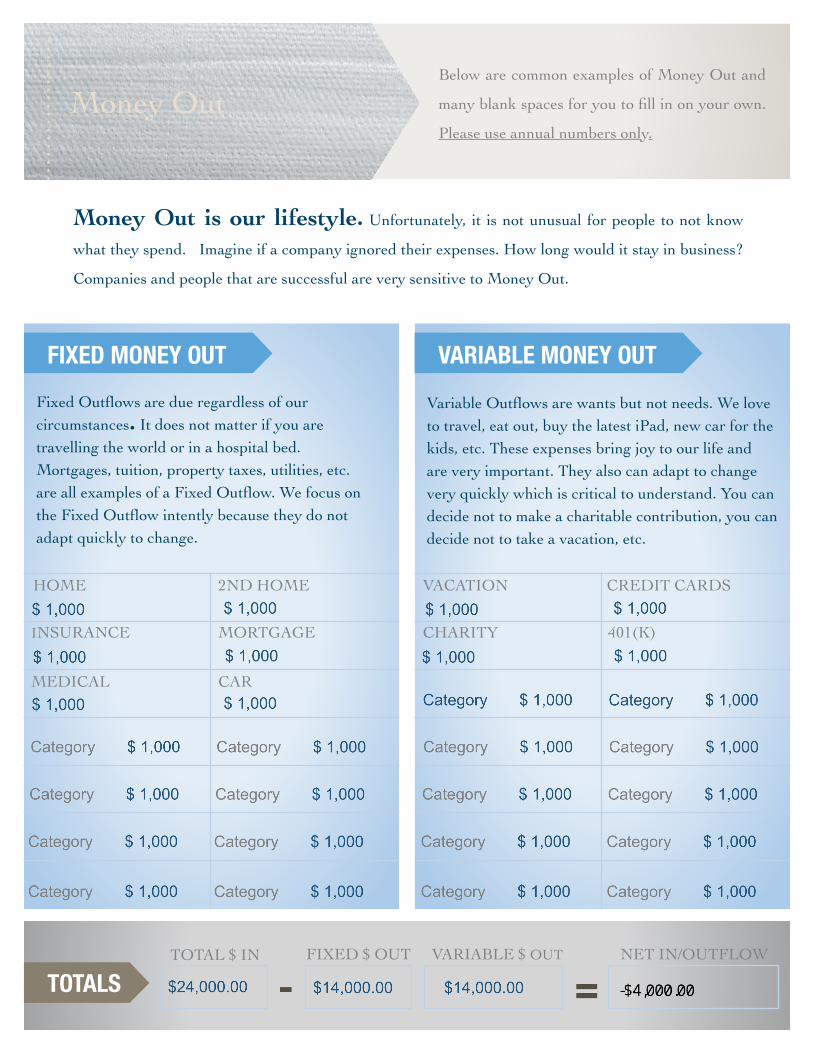

Money Out

TOTALS

HOME VACATION2ND HOME CREDIT CARDS

MORTGAGEINSURANCE 401(K)

CARMEDICAL

CHARITY

Below are common examples of Money Out and

many blank spaces for you to fill in on your own.

Please use annual numbers only.

TOTAL $ IN FIXED $ OUT VARIABLE $ OUT NET IN/OUTFLOW

- =

Variable Outflows are wants but not needs. We love to travel, eat out, buy the latest iPad, new car for the kids, etc. These expenses bring joy to our life and are very important. They also can adapt to change very quickly which is critical to understand. You can decide not to make a charitable contribution, you can decide not to take a vacation, etc.

Money Out is our lifestyle. Unfortunately, it is not unusual for people to not know

what they spend. Imagine if a company ignored their expenses. How long would it stay in business?

Companies and people that are successful are very sensitive to Money Out.

Fixed Outflows are due regardless of our circumstances. It does not matter if you are travelling the world or in a hospital bed. Mortgages, tuition, property taxes, utilities, etc. are all examples of a Fixed Outflow. We focus on the Fixed Outflow intently because they do not adapt quickly to change.

FIXED MONEY OUT VARIABLE MONEY OUT

Your Resources

ASSETS

NET WORTH

HOME

PARTNERSHIPS

2ND HOME

LINE OF CREDIT

IRA

BANK ACCOUNTS

CREDIT CARD

401(K)

MORTGAGE

CASH

CD

Our Assets are our tools. You know your Point of

Independence from the previous page and now you need to

complete this section to understand the resources available

to you. Please complete with the latest values available.

ASSETS $ DEBT $ NET WORTH

- =

DEBT

Cash Flow Stress Test

Imagine your income stopped tomorrow. How long can you survive? You can’t

predict financial hardship but you can predict how you can survive a major cash flow interruption.

You can include any asset that is liquid, meaning an asset that can be turned to cash in less than a

week without severe penalty, discount or tax. This includes cash, CDs, stocks and bonds and after-tax

accounts, but you have to exclude IRAs if you’re under 59 1/2. Now, divide the annual cash flow needs

by your liquid assets. This is the number of years you can survive a major cash flow interruption. The

longer you have, the safer your position.

LIQUID ASSETS

ANNUAL MONEY OUT

SURVIVAL PERIOD IN YEARS

÷

=

$

$

GO TO

WWW.HOLCOMBEFINANCIAL.COM/BLOGTO READ RUSTY’S BLOG

800-298-9904Contact Rusty

This is just the beginning...It is the framework we use to build a financial plan based on your

dreams and your risks. If you wish to have Rusty help you reach

your Point of Independence send an inquiry to the email below.

Copyright © 2012 Russell Holcombe