yellowstone club market view

DESCRIPTION

An interesting perspective from afar.TRANSCRIPT

Third Quarter 2010

M A R K E T V IE W A Comparative Market Study of the Premier Rocky Mountain Resort Communities

M A R K E T V IE W A Comparative Market Study of the Premier Rocky Mountain Resort Communities

4 5 6 7 8 9

1010 11 11 1212 13 14 15 16 1617

3

IntroductionBig Sky Market OverviewAspen Market OverviewDeer Valley Market OverviewJackson Hole Market OverviewSun Valley Market OverviewGraph: Average Single Family Residence Price Per Square Foot Graph: Average Single Family Residence Sale PriceGraph: Average Condominium Price Per Square FootGraph: Average Condominium Sale PriceGraph: Total Sale VolumeGraph: Total Number of TransactionsTelluride Market Overview Vail Valley Market OverviewYellowstone Club Market OverviewProperty ClockGraph: Historical Interest RatesMarket Outlook

IN T R O D U C T IO N

What a difference a year makes! Yellowstone Club, the world’s only private ski and golf community, is thriving under new ownership, new amenities, new energy, and new members. The Real Estate markets are improving, with activity and transaction numbers up. Late in the winter season of 2010 brought increased market activity as well as the best powder days of the year, with snow continuing into May. July kicked off another amazing Montana summer, which meant activity-filled days spent hiking, biking, golfing, and fly-fishing our blue ribbon rivers. New ownership is making unprecedented improvements to the Club, including a new fitness facility, pool, challenge course and sports courts, which is virtually unheard of in this economic environment. We have been building sales momentum throughout 2010 in order to jump-start 2011, which we anticipate will be another strong selling year for us. Over the past year, we have seen encouraging economic signs both locally and on a national scale. In recent months, there has been a considerable increase in transaction volume in the general Rocky Mountain resort mar-kets and specifically at the Yellowstone Club. Since new ownership took over in July 2009, Yellowstone Club has had almost 50 transactions and over $170,000,000 in sales activity, adding 30 new Members to the Club. Since mid-April we have averaged one closing per week as a direct result of an extremely active late winter selling ini-tiative. In addition, our pipeline of qualified prospects looks strong, confirming our confidence in the long-term resilience of the unique Yellowstone Club experience. As a sales force, we are continually challenging ourselves to work harder, smarter, and more creatively to bring the Club to new families and new markets. In June 2010, the Yellowstone Club Sales and Marketing Team visited what we believe to be the seven mountain towns we compete with and complement Yellowstone Club. We visited Aspen, Big Sky, Deer Valley, Jackson Hole, Sun Valley, Telluride, and Vail/Beaver Creek. These resort towns may appeal to the same demographic of potential and current Yellowstone Club Members. We spent several days in each town visiting properties with similar price points to those at the Club. We met with the premier brokers in each market to get a feel for what was happening and to investigate the trends of both sellers and buyers. We collected raw data from each market (2005 – Third Quarter of 2010) to understand where, comparatively, Yellowstone Club stands in terms of pricing and deal veloc-ity. Lastly, it was an opportunity to introduce YC to the brokers we met, letting them know what is happening at Yellowstone Club as we enter a new chapter in the Club’s history. We are confident that these meetings will result in increased prospect visits and future growth for the Club. In our research, we discovered that each market has its own strengths, weaknesses, challenges, and opportunities. Many of these premier mountain towns have found the bottom of the market and are experiencing improved inter-est, deal velocity, and overall sales volume, similar to what we are experiencing at YC. However, the credit crisis and the overall economy had a profound impact on these markets and continues to act as a governor to growth. While several extremely well-located submarkets in each of these towns have shown great resilience to the overall deterioration of value, it is safe to say that a significant correction has taken place with values adjusting 20-50% since the end of 2007. All of the professionals in the markets that we visited felt it would be a prolonged recovery with nominal appreciation over the next 12 months, and they all are watching their supply closely. The bottom line is that it is an incredible time to be in the market for premier mountain Real Estate, given the quality and quantity of the supply, and the historically low interest rates.

4

The following pages include a market overview of seven Rocky Moun-tain Resort Communities, as well as an analysis of how Yellowstone Club compares in transaction volume, price per square foot, average sales, and number of transactions. While one cannot attach an actual value to the completely unique Yellowstone Club family experience, we can compare and contrast pricing. The Yellowstone Club Sales and Marketing Team is confident that our findings will demonstrate great value in our properties.

Big Sky Market Overview

Yellowstone Club and Big Sky share in many relationships, both work-ing and uniting as a community, but when focusing on Real Estate, they demonstrate trends that make these two markets distinct from each other. The Big Sky Real Estate market has seen renewed interest, activity, and sales volume after being battered for the past 24 months. After experiencing unprecedented growth from 2003-2007, Big Sky saw a 65% decline in sales volume in 2008-2009. In the same period, the number of units sold declined by 48%. The good news is that 2010 YTD sales volume has increased by 35% over 2009 and total number of units sold has increased by nearly 60%. The vast majority of the transaction activity has occurred in the ‘Condominium’ market with 81 closed deals YTD 2010. This is a sharp increase over 2009 activity, when only 38 such transactions closed. It is safe to say that Big Sky buyers are sweeping the bottom of the market and that the market is slowly working its way through the low and mid-end of the abundant supply. Big Sky is also home to The Club at Spanish Peaks, a 5,700 acre pri-vate community featuring a Championship Weiskopf designed golf course and direct private lift access into Big Sky Resort. Spanish Peaks has also seen renewed sale activity and dollar volume with the most active summer sales season since 2005. Through the Third Quarter of 2010, Spanish Peaks has transacted 22 deals with a dollar volume in excess of $19,000,000. One factor that will aid Big Sky’s recovery was highlighted recently in Powder Magazine. It named Bozeman, just 45 miles from Big Sky, as North America’s “number one place to live to ski.” The combination of uncrowded slopes, abundant trout streams, affordability, and world class outdoor pursuits makes Southwest Montana virtually unbeat-able in terms of livability for locals and second homeowners alike.

Note: Due to the lack of specific aND available Data, big sky is Not iNcluDeD iN the graphs that follow.

O V E R V IE W S

Aspen Market Overview

In general, Real Estate activity in Aspen and the upper Roaring Fork Valley has a promising outlook. The Second Quarter of 2010 has experienced a markedly higher dollar volume of sales and has seen an increase in sales trans-actions of all property types when compared to both the Second Quarter of 2009 and the First Quarter of 2010. ‘Single Family Homes’ in both Aspen and Snowmass Village, have been boosted by a 2010 Second Quarter jump in sales, in the $4,000,000 to $6,000,000 range. Although ‘Condominium’ sales have historically accounted for a much larger percentage of sales than ‘Single Family Homes,’ the statistics of the past two years show that the trend is changing and the gap between the number of ‘Single Family Home’ sales and ‘Condominium’ sales is narrow-ing. Due to over-pricing and a strong dependency on lending sources and mortgages, the ‘Condominium’ market in Aspen continues to be stressed. In the first six months of 2010, there were 16 sales, each over $6,000,000. Most ‘Single Family Home’ sales in Aspen occurred above $4,000,000 in the Second Quarter of 2010, suggesting a stronger luxury ‘Single Family Home’ market than might have been thought. Transaction numbers of ‘Single Family Homes’ through August of 2010 have already matched the total number of transactions that occurred in 2009. ‘Con-dominium’ sales prices are still maintaining their value on an average sale basis at just over $1,500,000. However, there has been an approximate 75% decrease in the number of ‘Condominium’ transactions. In the Second Quarter of 2010, the ‘Single Family Home’ market strengthened by 26% when comparing the sale price to original ask price ratio, now selling at an average of 87% of their final asking price. This reflects the fact that property prices are becoming more realistic and the distance between the ‘ask price’ and ‘sold price’ appears to be narrowing. Pricing remains a considerable challenge in Aspen, as so many personal and subjective factors dictate actual sold events, rather than solid market data. In general, relevant sales comparisons continue to be difficult to find. Snowmass Village sales are struggling: construction has halted, developer-lending sources are reportedly non-existent, and the uncertainty of the build-out of the new Snowmass Base Village continues. Although the recent quarterly analysis for 2010 of the Aspen and Snowmass Village residential market is positive, it is far from the peaks of 2006 and 2007. The overall picture of the Aspen Real Estate market has many similarities to Yellowstone Club including an upswing in sales from the previous year as well as an increase in recent sales of ‘Single Family Homes’ as compared to ‘Condominiums.’ Sales activity is gaining momentum. The months of July and August saw steady sales activity with just under 30 combined closings. Sold pricing varied from $590,000 for a ‘Condominium’ to $8,200,000 for a ‘Single Family Home’ with the price per square foot ranging from $470/sq. ft. - $1,463/sq. ft. Sales activity picked up in Septem-ber, as is typical this time of year, with 26 mixed unit type closings during the month. October is historically the strongest month of the year for closings in the Aspen area, and it appears that they are on track for that to remain true again this year. Recently, most prospective buyers have mainly been interested in Aspen’s base area ‘Condo-miniums’ and ‘Vacant Land’ sales.

6

Deer Valley Market Overview

Deer Valley, located within Park City Proper, continues to be a leader in the Western Ski Resort Market. Essentially Deer Valley is a resort within a resort. The town of Park City, with a population base of 7,500 inhabitants, has a vibrant ski town feel with over 200 restaurants in the downtown area, giving it a big city feel in a quaint mountain village setting. In the First Quarter of 2010, the Deer Valley market surpassed the Vail Valley market in sales for the first time in a number of years. This is a direct reflection of the 30-40% price reduction on larger vertical product for sale from the peak markets of 2007. Another key factor to continued sales and stabilization is the location. Deer Valley is 35 minutes away from the Salt Lake City International Airport and this accessibility to a major airport and the greater Salt Lake City area continues to be paramount for sales success. The high-end market continues to be the focus with cash buyers, and until the lending institutions start being more liberal in their lending practices, the mid-to-low range markets continue to be saturated with inventory. In the past twelve months, Deer Valley has recorded the following ‘Single Family Home’ sales, which are broken down into three regions: Empire Pass, Upper Deer Valley, and Lower Deer Valley. Empire Pass had seven homes listed from $5,600,000 - $16,000,000 with two recorded sales. Upper Deer Valley had 18 homes listed from $2,700,000 - $5,000,000 with eight recorded sales. Lower Deer Valley had 33 homes listed from $1,800,000 - $3,500,000 with 16 recorded sales. With a total of 58 listed and 26 sold, roughly 45% of the listed ‘Single Family Homes’ have sold over the past 12 months. The Park City/Deer Valley ‘Condominium’ market has sold 79% of their 2009 inventory. Empire Pass had 48 ‘Con-dominiums’ listed in the $1,500,000 - $6,000,000 range with 42 recorded sales. Upper Deer Valley had 37 ‘Condo-miniums’ listed from $1,500,000 - $4,000,000 with 24 recorded sales. Lower Deer Valley had 84 ‘Condominiums’ listed in the $300,000 - $4,100,000 with 68 recorded sales. In the first eight months of 2010, Deer Valley has already closed nearly $290,000,000 in sales. Although this is more than 2008 and 2009 volume numbers, they are still down considerably from the peak. There is a potential saturation of product in both ‘Single Family Home’ and ‘Condominium’ sectors in the next 24 months. This market dynamic will continue to drive the value shoppers who are lured in by the enticement of getting the deal. Deer Valley is in an upward market trend with increasing sales. The 2010 summer Real Estate market in Deer Valley had more traffic than the summer of 2009, but buyers are still very hesitant to transact. The demand in the marketplace for ultra-exclusive ski-in/ski-out homes was low; Deer Val-ley had only two deals over $5,000,000 this summer. Most summer activity has been in the ‘Single Family Home’ market. Properties that were previously listed for $4,000,000 - $5,000,000 are now selling in the $1,000,000 -$3,000,000 range where the value is apparent. As Deer Valley moves into it’s 2010-2011 winter season, more and more people are looking for value properties.

7

Jackson Hole Market Overview

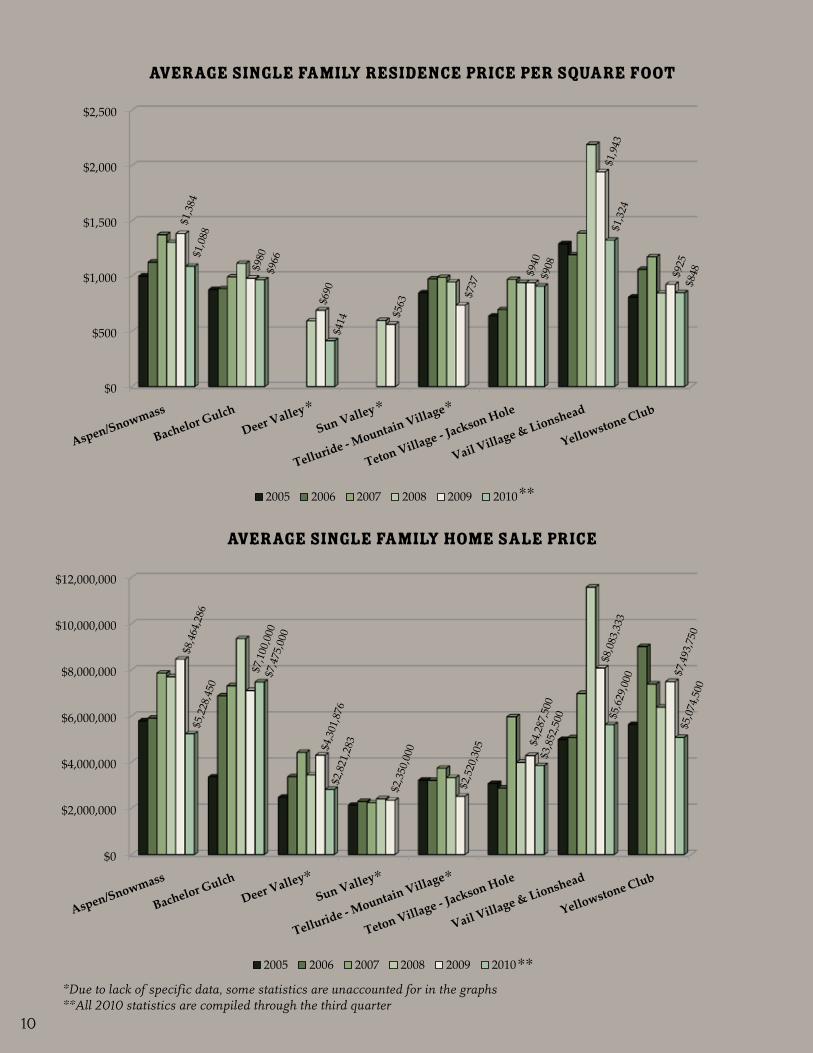

Jackson Hole, Wyoming is, and continues to be, a compelling Real Estate destination for the affluent United States high net worth Buyer. The area has some unique characteristics that make it attractive to this demographic and help keep the market fairly stable even during turbulent economic times. Some of these characteristics include the lack of state, personal, or corporate income tax, no capital gains tax, and low sales taxes. Additionally, there is a finite amount of developable land within the Jackson Hole area, as almost 97% of the land is protected by the US government through private land trusts and conservancies. The scarcity of new available property coming to the market helps to limit inventories and maintains more consistent pricing. Finally, over the years, the town of Jack-son has attracted some high profile business, political, and entertainment personalities, and many “old wealth” families who helped to establish the town as a foundation for a growing art community and many conservation efforts. Jackson is a year round community that experiences two thirds to three quarters of its economic success in the summer and fall months, due to its proximity to Teton and Yellowstone National Parks. The Jackson Hole ski area is a very popular and challenging mountain, which contributes greatly to the attractiveness of the area in the winter months. We find the Jackson Real Estate market complex to analyze, as there are very distinct micro-markets within Jack-son: the downtown market, which includes ‘Single Family Homes’ and ‘Condominiums’; the large property and homes market, which are generally situated in outlying areas and are near water and/or have views of the Tetons; the Jackson Hole ski market, including the Teton Village and the surrounding areas, specifically designed to cater to winter skiing clientele; and finally, the more traditional private golf club market. For matters of comparison to Yellowstone Club, this report focused solely on the ski and golf properties. Though the general Real Estate mar-ket in Jackson has been lack luster over the past 18 months as it relates to the number of transactions (down by over 40% from the peak), in the mid-summer of this year, a more consistent level of activity resumed. The two primary private golf clubs, Three Creeks and Shooting Star, had some activity in both Real Estate ($1,200 per square foot for Lodge Cabins at Shooting Star) and Membership sales (over 20 sold at Three Creeks). Over the past year, ski accessible properties have maintained their value, ranging from $900 to $1,020 per square foot, though the velocity of transactions was down compared to previous winters. Pricing has softened throughout the area in the range of 30% to 35% since the peak in 2007; however, due to the factors noted above, the pricing has not diminished on a percentage basis to the same extent as it has in the other Rocky Mountain markets. After a slow June and July, August showed signs of life in Jackson Hole, and the results for the quarter were con-sistent with showing that there is renewed interest in Real Estate. The interest was focused at the higher end of the market, as there were 10 sales in the Third Quarter that exceeded $3,000,000 versus four in the same quar-ter the previous year. Sales volume was up 92% county wide and the number of transactions was up 51%, both significant increases from the previous year’s third quarter activity. Days on the market for all levels of property continue to be at historic highs with ‘Single Family Homes’ now on the market for an average of 275 days. Not-ing again the increase in activity in the higher dollar sales, the top six grossing sales for the Quarter exceeded $40,000,000. Even with three ranch sales in that mix, it is indicative of the higher end of the market becoming more active again.

8

Sun Valley Market Overview

Sun Valley, the market with the richest history amongst any Ameri-can ski resort, has a town and atmosphere that can rival any other worldwide ski destination. Sun Valley’s Real Estate market has had a solid track record. With sustained long-term growth, Sun Valley has built their reputation on a deep history, an unbeatable ski culture, two ski mountains, multiple ski lodges, and many other great attri-butes on which it thrives. In today’s economic environment, these fundamental characteristics are being put to the test, as the Sun Val-ley Real Estate market continues to struggle through this economic downturn. Sales volumes have seen a drastic decrease over the last five years, amounting to over a 75% decrease in total volume from 2005 to 2009. In looking at sales statistics and talking with local Real Estate experts, it is estimated that Sun Valley has seen a price correction of approximately 40% through the collapse of the eco-nomic and Real Estate markets. The biggest area of weakness for this market is in the ‘Condomin-ium’ segment. Most significantly, a major local developer defaulted on his ‘Condominium’ developments and handed those projects back to the bank. This flooded the market with ‘Condominiums’ available at a price others struggle to compete with. Today’s average sales prices of ‘Condominiums’ are having difficulty achieving 50% of what they were getting at the peak in 2007. In 2007 the average ‘Condominium’ sale was at nearly $1.2 million, whereas today, the average sale is only slightly over $500,000. The other significant challenge presenting itself right now, similar to other western ski resorts, is the demand for the product. Some sellers are still fixed on achieving 2007 prices and are not willing to deviate from those high prices. Their hopes for selling their property at these high levels are unrealistic. This is causing the number of transactions in this valley to fall significantly. Five years ago, there were 835 Real Estate trans-actions, and in 2009, this number fell to 316. ‘Single Family Home’ sales alone have fallen by over 71% during this period. Other sellers are either recognizing that the market has changed drastically, or are in a position where they have to sell and are adjusting their num-bers accordingly. As this adjustment continues to go downward, the Sun Valley market has yet to reach it’s bottoming point, and it is unclear where and when the bottom will be found. Sun Valley, through the summer of 2010, continued to lack a strong direction, as it struggled to find the bottom of its market. One month would be strong with sales, but would be followed by another weak month. Dollar values of all product types continued to drop. Even with these price reductions, the market is still struggling to find traction and velocity. Short sales and foreclosures are where the prevailing interest has been in Sun Valley. These products are at such low prices, that new construction and lot sales are becom-ing fewer and fewer, as they cannot compete with the price of the foreclosures. The brokers hope through the sales of these distressed properties, the bottom can finally be set in the market, and Sun Val-ley can move forward from this difficult market cycle.

Yellowstone ClubSki Market Real Estate Analysis

Composed by Grant SythQuestions/Comments: 406-995-4900

$0

$2,000,000

$4,000,000

$6,000,000

$8,000,000

$10,000,000

$12,000,000

2005 2006 2007 2008 2009 2010

Average Single Family Home Sale Price

Yellowstone ClubSki Market Real Estate Analysis

Composed by Grant SythQuestions/Comments: 406-995-4900

$0

$500

$1,000

$1,500

$2,000

$2,500

2005 2006 2007 2008 2009 2010

Average Single Family Residence Price Per Square Foot

**

***Due to lack of specific data, some statistics are unaccounted for in the graphs**All 2010 statistics are compiled through the third quarter

10

***

***

Yellowstone ClubSki Market Real Estate Analysis

Composed by Grant SythQuestions/Comments: 406-995-4900

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

2005 2006 2007 2008 2009 2010

Average Condominium Price Per Square Foot

Yellowstone ClubSki Market Real Estate Analysis

Composed by Grant SythQuestions/Comments: 406-995-4900

$0

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

$6,000,000

2005 2006 2007 2008 2009 2010

Average Condominium Sale Price

**

**

11

***

***

Yellowstone ClubSki Market Real Estate Analysis

Composed by Grant SythQuestions/Comments: 406-995-4900

$0

$100,000,000

$200,000,000

$300,000,000

$400,000,000

$500,000,000

$600,000,000

$700,000,000

2005 2006 2007 2008 2009 2010 YTD

Aspen Bachelor Gulch Village Deer Valley

Sun Valley & Elkhorn Telluride - Mountain Village Teton Village - Jackson Hole

Vail Village & Lionshead Yellowstone Club

Total Sale Volume

Yellowstone ClubSki Market Real Estate Analysis

Composed by Grant SythQuestions/Comments: 406-995-4900

0

50

100

150

200

250

300

350

2005 2006 2007 2008 2009 2010 YTD

Aspen/Snowmass Bachelor Gulch Deer Valley

Sun Valley Telluride - Mountain Village Teton Village - Jackson Hole

Vail Village & Lionshead Yellowstone Club

Total Number of Transactions

**

12

**

*Due to lack of specific data, some statistics are unaccounted for in the graphs**All 2010 statistics are compiled through the third quarter

**

Telluride Market Overview

Telluride is a tale of two Real Estate markets: Old Town Telluride and the Telluride Mountain Village. The Old Town Telluride market is showing the signs of a recovering market, while the Mountain Village market is still in decline. This difference in the markets of these two areas, which are so geographically connected, can be ex-plained by supply and demand. Old Town Telluride is in high demand for many reasons. It offers the phenomenal opportunities for dining, entertainment, and retail and is easily navigable on foot. Old Town Telluride is vibrant with long standing local culture and tradition. Friendly and knowledgeable people whom embody the mountain culture, inhabit this idyllic and historic mining town. The supply of Real Estate in Old Town Telluride is tradition-ally and currently relatively limited, with a very manageable inventory of available property within the city limits. In sharp contrast, the Telluride Mountain Village seems almost devoid of any culture. The Mountain Village con-sists largely of multi-unit hotel and ‘Condominium’ buildings, which do not maintain the architecture or charm of Old Town Telluride. As such, the Mountain Village Real Estate market is still declining and has a saturated inventory of available properties. ‘Vacant Land’ is in extremely limited supply in both Old Town Telluride and the Mountain Village. Ironically, ‘Vacant Land’ has suffered the greatest erosion of value, largely due to the fact that there is a swollen inventory of built product in ‘Condominiums’ and ‘Single Family Homes.’ Built products of all types are trading between $600 and $1,200 per square foot: ‘Condominiums’ are widely available in both Old Town Telluride and the Mountain Village and vary widely in style. Those that are selling, offer great views and ski access. The Telluride market has followed a similar trend to the Yellowstone Club market: phenomenal success and price increases from 1998 to the Second Quarter of 2008, followed by a substantial softening in the second half 2008 to the Third Quarter 2009. The 2010 market has begun to capitulate as buyers have returned to the market and sellers are becoming more realistic about market conditions. There is a tremendous premium on living in Old Town Telluride as the retail, dining, and entertainment are some of the best in the entire Rocky Mountain region and the strict town planning keeps the look of a consistent historic Victorian mining town. Sales in Telluride are split between summer, 60%, and winter, 40%. The summer programming is unrivalled as there are festivals of all types virtually every weekend of the season and the town is bustling with activity and excitement. The Telluride Association of Realtors called the First Quarter of 2010 an inspiring start and sales figures contin-ued to reflect that throughout this year. Through July of 2010, there were $171 million in sales in Telluride and surrounding areas. This was a sharp contrast when compared to the $56 million in sales during the same period a year ago. The $171 million in sales this year has been distorted by a few significant high-end sales (one $46.5 million sale in particular) but Telluride realtors are being smart about these statistics and are cautiously optimistic for the future. The realtors are not convinced that the market has fully turned around, but they do recognize a changing trend and are beginning to gain confidence looking forward to the winter season.

13

Vail Valley Market Overview

Historically, the Vail Valley has boasted some of the highest price per square foot sales of any of the Western high-end ski markets. Vail is a well-established resort and ski community, rich in culture and ski history. For Real Estate in Vail, 2009 was one of the most difficult years the valley has experienced. The 2009 totals for Real Estate transac-tions closed, amounted to $898,000,000; the first year since 1996 under $1,000,000,000 and well below the 2007 peak. In 2010, the Real Estate market began to improve. Overall transactions and sales volume escalated towards the end of the 2009/2010 ski season and the same trend carried on into spring. There were 276 transactions in Eagle County in the First Quarter of 2010 totaling $318,726,934, which is twice the amount of the First Quarter of 2009. The high-end Real Estate market is seeing the most significant recovery as heavily discounted ‘Single Family Homes,’ ‘Townhomes’ and ‘Condos’ around the Vail Valley are attracting savvy investors. There were 18 residen-tial closings over $5,000,000 in all of 2009 and 14 residential closings over $5,000,000 within the first four months of 2010. Following the success in Bachelor Gulch, The Ritz Carlton is now opening in Vail with an ad-ditional residential offering. Two additional brand new, high-end ‘Condominium’ and penthouse properties have also just been completed or are nearing completion: Solaris and The Four Seasons. Solaris, the “New Center of Vail Village,” is a combination of 77 ‘Condominium’ and penthouse residences, a new triplex theatre, luxury bowling alley, and three restaurants. Solaris has contracted 54 of their residences through pre-sale (prior to construction completion) process and they have closed ten at an average price of $2,600 per square foot, but are expecting up to 30 deals to fall apart.* The Ritz and The Four Seasons are both scheduled to be completed for the 2010/2011 ski season and are offering luxury ‘Condominiums’ in the $1,500 - $2,200 per square foot range. They too have contracted pre-sales and are seeing a small percentage of them close while expecting several deals to disappear as well. The overall consensus in Vail is that the market is on the rebound. It appears that the bottom has been hit and Vail should see an increase in transactions in the upcoming 2010/2011 ski season. Another interesting aspect in Vail Valley is the overwhelming number of “ski clubs” where a skier can purchase a membership which allows them premier access to skiing, including slope side parking, locker rooms, ski storage, concierge services, and an exclusive club-like atmosphere with an exceptional social calendar. These clubs help to alleviate the challenges that are typically associated with the average skier experience: parking, carrying gear, nowhere to change and a place to leave your personal belongings. Starting at approximately $35,000 to join and around $5,000 in annual dues, these ski clubs make Vail much more competitive with some of the amenities and services YC offers, especially the ease of access. These clubs can only provide a temporary escape, as Vail Mountain can host upwards of 25,000 skiers in a single day, failing to rival Yellowstone Club’s private skiing. For Vail Valley, the summer of 2010 was a turning point. The Real Estate market had found the bottom and was on the rise, building upward momentum once again. Transactions on all types of properties from the prior summer showed increases in volume as well as the average price points. Sales volume for Vail Valley was at $716,000,000 through the first six months of 2010, an increase of 88% from the same period a year ago. The average sales price went up as well, demonstrating a 12% increase valley wide to $1,237,506. There was significant interest in the high-end market, with 25 sales over $5,000,000 in the first 6 months of 2010. Specifically, the resort areas had the most sales interest in the Vail Valley. Vail Village alone consumed nearly 20% of the sales volume (this figure is somewhat distorted by the fact that many of these sales were closings on pre-sales for Solaris units occurring in 2007-2008). Other ski communities clearly had high sales interest as well, with Beaver Creek maintaining 12% of the total vol-ume and Lionshead with nearly 9% of the Valley’s total volume.

*Solaris is not included in the 2010 graphs, due to pre-selling in 2007-2008.14

The past year has brought profound and positive change to the Yellow-stone Club. CrossHarbor Capital Partners was successful in acquiring the Club in July 2009. CrossHarbor has partnered with Discovery Land Company, the world’s premier developer of exclusive club prop-erties, to run the operations, development and Real Estate sales. The new ownership team has injected capital, infrastructure, amenities, and new energy into a club that desperately needed revitalizing. Some of the capital improvements include new comfort stations on the golf course, sugar shacks on the ski mountain, extensive landscaping and road improvements, a new fitness center, pool, multi-sport court, tennis and platform tennis courts, and a world class ropes challenge course. More importantly, the ownership team breathed new life, energy and confidence into the YC Membership. The Club now has what most Members and guests describe as a positive “vibe” that has resulted in increased prospect visits and positive deal velocity. As previously stated, since July 2009, the Club has done over $170,000,000 in transaction volume while attracting over 30 new Members. In addition, the new ownership has established a newfound confidence in the Membership that has had a tremendously positive impact on Member referrals, which has, and will allow the Club to grow and prosper. During the winter of 2010, the Club hosted over 150 prospects, which was a 52% increase over the prior year. During the summer of 2010, YC hosted over 70 prospects. The goal of Yellowstone Club’s Owner-ship is to create a more even flow of potential buyer visits over the course of the calendar year. This will be accomplished through in-creased summer and winter activities, special events, and off-season marketing. The early results of these efforts, driven by Discovery Land Company, have been outstanding. Since July 2009, there have been 12 sales of ‘Single Family Homes’ with an average price of $848 per square foot. Additionally, there have been 23 lots sales with an average price of $538,923 per acre. These figures represent a discount of 25-30% on ‘Single Family Homes’ and 45-50% discount on land from the peak market of 2006/2007. In-terestingly, the delta between ‘ask price’ and ‘sale price’ has been 17% over the course of approximately one year with that gap narrowing. This clearly shows that the market is in recovery mode. Our average sale price per square foot represents a clear value when compared to markets such as Vail/Beaver Creek and Aspen, neither of which of-fers a private skiing environment. During the months of August and September, there were seven trans-actions put under agreement, representing a total dollar volume of $35,000,000. This is a direct result in the confidence of buyers in the stability and long-term viability of the Yellowstone Club. Given the deal velocity achieved over the past year, and the great interest and flow of new prospects that have and will attend Club events, we are predicting a reasonably swift recovery of the YC market. In addition, with limited long term supply, the concept of scarcity will soon begin to drive the market. The unique and casual environment at the Club, in addition to over 2,200 skiable acres of Private Powder™, makes Yel-lowstone Club a truly world-class alpine retreat.

Yellowstone Club Overview

*Solaris is not included in the 2010 graphs, due to pre-selling in 2007-2008.

Falling

Bottoming

Peaking

Rising

Sun Valley

Deer Valley

TellurideVail Valley

Aspen

Yellowstone ClubJackson Hole

This Property Clock is used to demonstrate where each Ski Market sits within the Real Estate market cycle. Gener-ally, Markets will move clockwise around the clock. In 2006 and 2007, at the peak of the Real Estate market, each individual Market was positioned near the top at 12 o’clock. However, after the fall of the market in 2008, each Market is now on a different part of the Property Clock. The determination of the relative positions for each Market on the Clock was arrived at by a combination of analysis of the market data, and an individual investigation of each market area and on-going firsthand conversations with those active in each Market segment. In the winter of 2010, Yellowstone Club reached the 6 o’clock mark and buyers took full advantage of the bottomed market. Throughout this summer, Yellowstone Club has had a continued rise in sales after a strong winter sales season, and thus YC is moving forward and up, giving it a position in the rising market quadrant of the clock.

Comparative Market Clock

Historical Interest Rates

3.00%

5.00%

7.00%

9.00%

11.00%

13.00%

15.00%

17.00%

19.00%

1972 1975 1980 1985 1990 1995 2000 2005 2010

Rate

Big Sky

16

As we look forward to the conclusion of 2010 and the start of 2011, we become increasingly optimistic. Over the course of 2010, the smart money saw that the value opportunity was in land deals and existing built product. As with any harsh market re-pricing episode, tremendous opportunities have begun and will continue to emerge over the next several quarters for savvy, well-capitalized buyers. They recognize that due to the very unique confluence of circumstances that exist, high-quality assets and opportunities will be available at pricing not likely to be seen again for multiple economic cycles. This holds particularly true for those markets that have already found the bot-tom and are seeing increased activity and actual deal volume, such as the Yellowstone Club. However, the relative window of opportunity for buyers in these markets to take advantage of the best pricing may prove to be short lived. Once significant data points are set, the crowd will invariably follow. Traditionally, in the highest priced mar-kets, scarcity will rule the day. The most favorable pricing will be achieved by those who return first as 2010-2011 should ultimately prove to be the most favorable entry point for selective buyers. These assumptions hold true for all of the markets that we have studied. Additionally, key interest rates are at historic lows, which will create real opportunity for those who wish to responsibly leverage such property acquisitions. Yellowstone Club is particularly poised to rebound after 30 months of near paralysis from transaction activity. With the emergence of new capital, new ownership, and new operating mechanics, the Club has discovered a new energy within its ranks. CrossHarbor Capital Partners and Discovery Land Company have strategically deployed capital over the past 12 months to finish long promised capital improvements, added unique and defining amenities, and have created stability where it did not previously exist. As a result of capital being invested while the market was recovering, the world’s only private ski and golf community, Yellowstone Club, is poised to see value apprecia-tion well in advance of comparable markets. Although we are extremely optimistic about the future of Real Estate sales activity at the Yellowstone Club, we are carefully monitoring the capital markets as they have a profound impact on Rocky Mountain Resort Real Estate. Assuming the markets continue to stabilize over the next several quarters, properties such as the Yellowstone Club will show their relative strengths during the eventual economic recovery. As the overall economy improves, the stage will be set for the beginning of a longer and more stable cycle hopefully featuring a greater sustainable pace of growth. We welcome that stability, as we responsibly continue to develop the Yellowstone Club as the premier destination for families to spend cherished time together.

17

M A R K E T O U T L O O K

“I spent 50 years traveling the world with my skis and camera, looking for the ‘closeto perfect’ mountain where I could settle down and live. I first skied PioneerPeak and what has become the Yellowstone Club in 1997. I followed my own advice,‘If you don’t do it this year, you’ll be one year older when you do.’ I’ve spentevery winter at YC since.”

All rights reserved. All information contained herein is from sources deemed reliable; however, no representation or warranty is made as to the accuracy thereof. The statements made in YC’s Market View represent the opinions of the authors and should not be relied upon exclusively to make real estate decisions. A potential buyer and/or seller is advised to make an independent investigation of the market and of each property before deciding to purchase or sell. To the extent the statements made herein report facts or conclusions taken from other sources, the information is believed by the authors to be reliable, however, the authors make no guarantee concerning the accuracy of the facts and conclusions reported herein.

(888)700-7748 ^ (406) 995-4900 ^ [email protected] P.O. Box 161097 ^Big Sky, Montana 59716

www.yellowstoneclub.com

11/10