year-end closing

DESCRIPTION

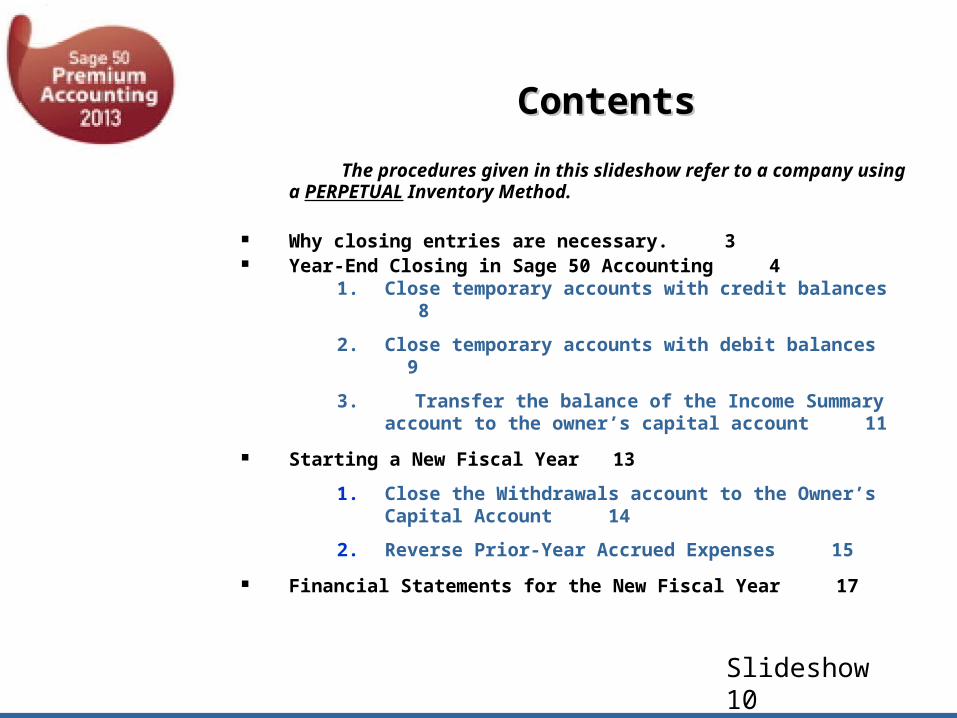

Year-End Closing. Slideshow 10. Contents. The procedures given in this slideshow refer to a company using a PERPETUAL Inventory Method. Why closing entries are necessary. 3 Year-End Closing in Sage 50 Accounting 4 1. Close temporary accounts with credit balances 8 - PowerPoint PPT PresentationTRANSCRIPT

Year-EndClosing

Slideshow 10

The procedures given in this slideshow refer to a company using a PERPETUAL Inventory Method.

Why closing entries are necessary. 3 Year-End Closing in Sage 50 Accounting 4

1. Close temporary accounts with credit balances 8

2. Close temporary accounts with debit balances 9

3. Transfer the balance of the Income Summary account to the owner’s capital account 11

Starting a New Fiscal Year 13

1. Close the Withdrawals account to the Owner’s Capital Account 14

2. Reverse Prior-Year Accrued Expenses 15

Financial Statements for the New Fiscal Year 17

ContentsContents

Slideshow 10

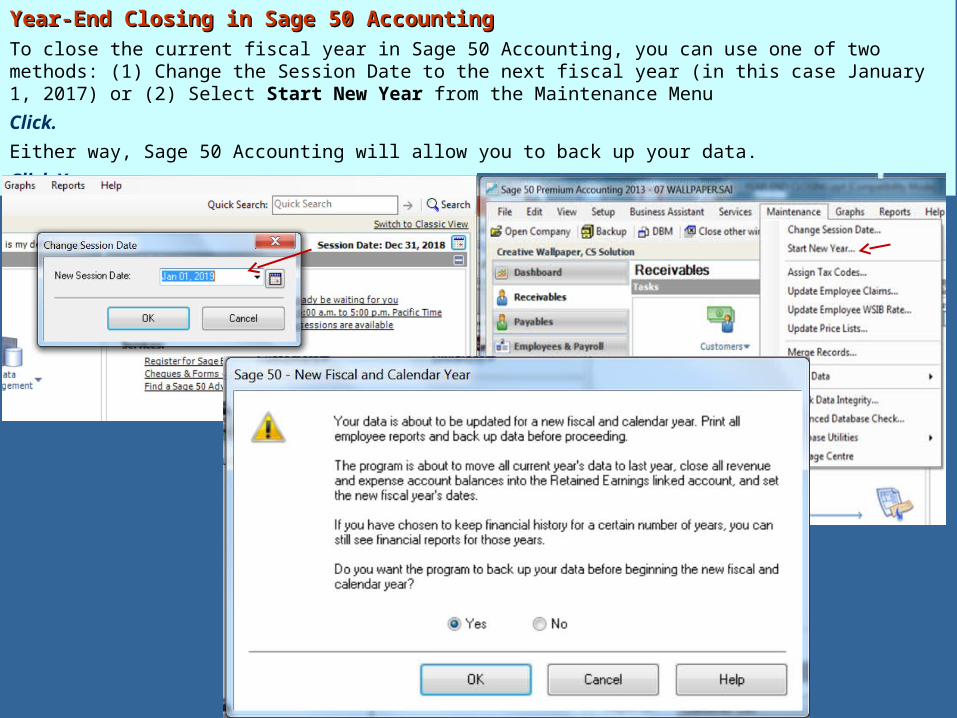

Year-End Closing in Sage 50 AccountingYear-End Closing in Sage 50 AccountingTo close the current fiscal year in Sage 50 Accounting, you can use one of two methods: (1) Change the Session Date to the next fiscal year (in this case January 1, 2017) or (2) Select Start New Year from the Maintenance Menu

Click.

Either way, Sage 50 Accounting will allow you to back up your data.

Click Yes.

Year-End Closing in Sage 50 Year-End Closing in Sage 50 AccountingAccounting(continued)(continued)

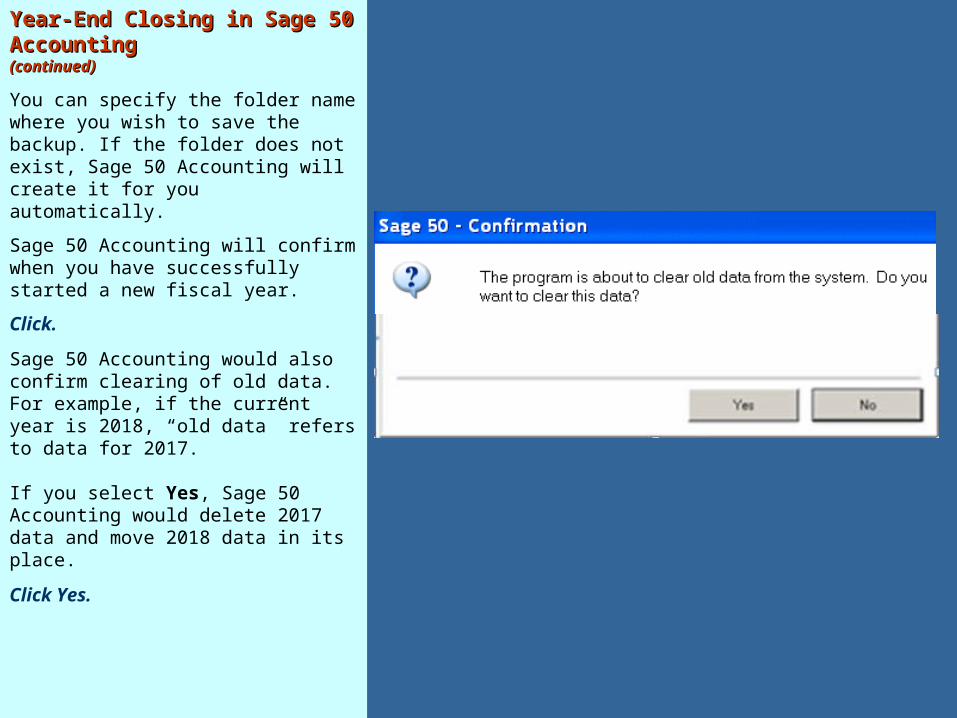

You can specify the folder name where you wish to save the backup. If the folder does not exist, Sage 50 Accounting will create it for you automatically.

Sage 50 Accounting will confirm when you have successfully started a new fiscal year.

Click.

Sage 50 Accounting would also confirm clearing of old data. For example, if the current year is 2018, “old data” refers to data for 2017.

If you select Yes, Sage 50 Accounting would delete 2017 data and move 2018 data in its place.

Click Yes.

Year-End Closing in Sage 50 Year-End Closing in Sage 50 AccountingAccounting(continued)(continued)

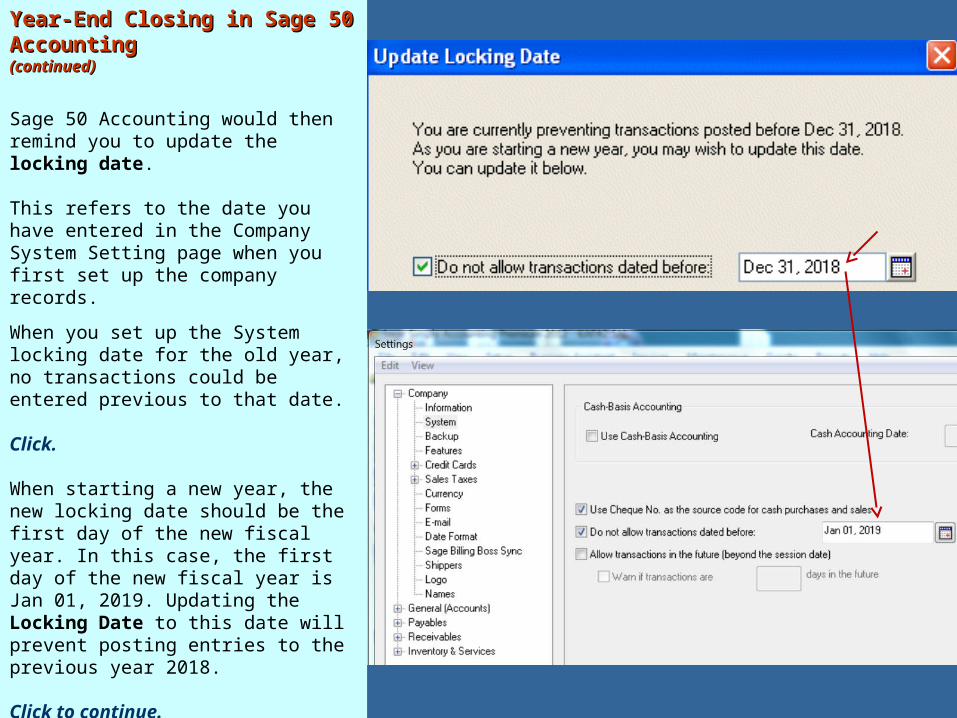

Sage 50 Accounting would then remind you to update the locking date.

This refers to the date you have entered in the Company System Setting page when you first set up the company records.

When you set up the System locking date for the old year, no transactions could be entered previous to that date.

Click.

When starting a new year, the new locking date should be the first day of the new fiscal year. In this case, the first day of the new fiscal year is Jan 01, 2019. Updating the Locking Date to this date will prevent posting entries to the previous year 2018.

Click to continue.

Automatic Closing EntriesAutomatic Closing Entries

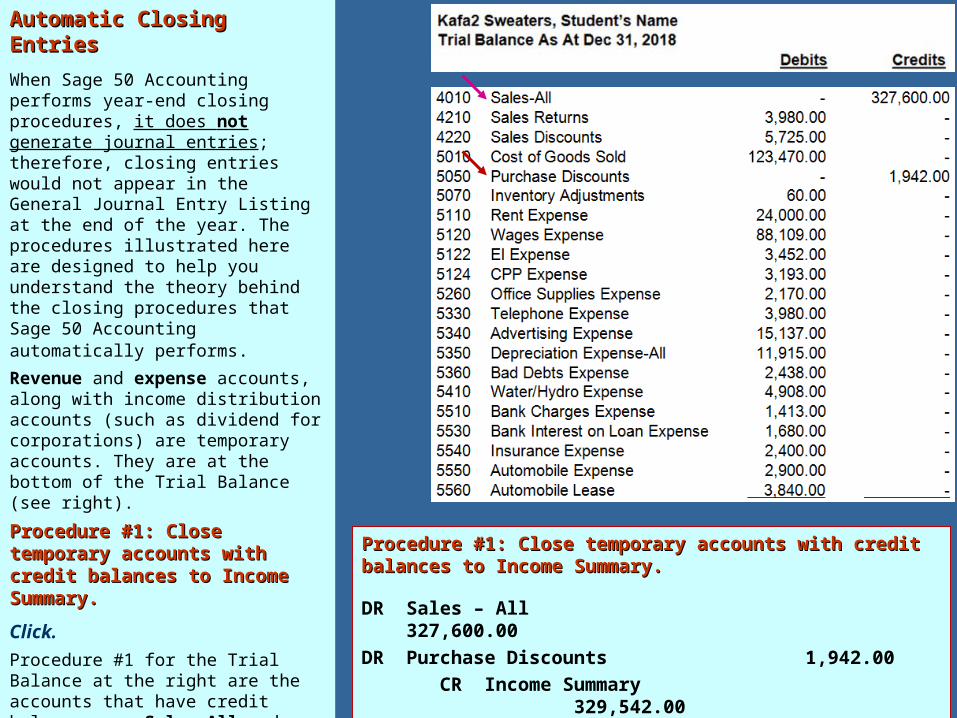

When Sage 50 Accounting performs year-end closing procedures, it does not generate journal entries; therefore, closing entries would not appear in the General Journal Entry Listing at the end of the year. The procedures illustrated here are designed to help you understand the theory behind the closing procedures that Sage 50 Accounting automatically performs.

Revenue and expense accounts, along with income distribution accounts (such as dividend for corporations) are temporary accounts. They are at the bottom of the Trial Balance (see right).

Procedure #1: Close temporary Procedure #1: Close temporary accounts with credit balances to accounts with credit balances to Income Summary.Income Summary.

Click.

Procedure #1 for the Trial Balance at the right are the accounts that have credit balances are Sales-All and Purchase Discounts. They will be closed to the Income Summary account.

Click to continue.

Procedure #1: Close temporary accounts with credit balances to Procedure #1: Close temporary accounts with credit balances to Income Summary.Income Summary.

DR Sales – All 327,600.00

DR Purchase Discounts 1,942.00

CR Income Summary 329,542.00

Automatic Closing Entries:Automatic Closing Entries:

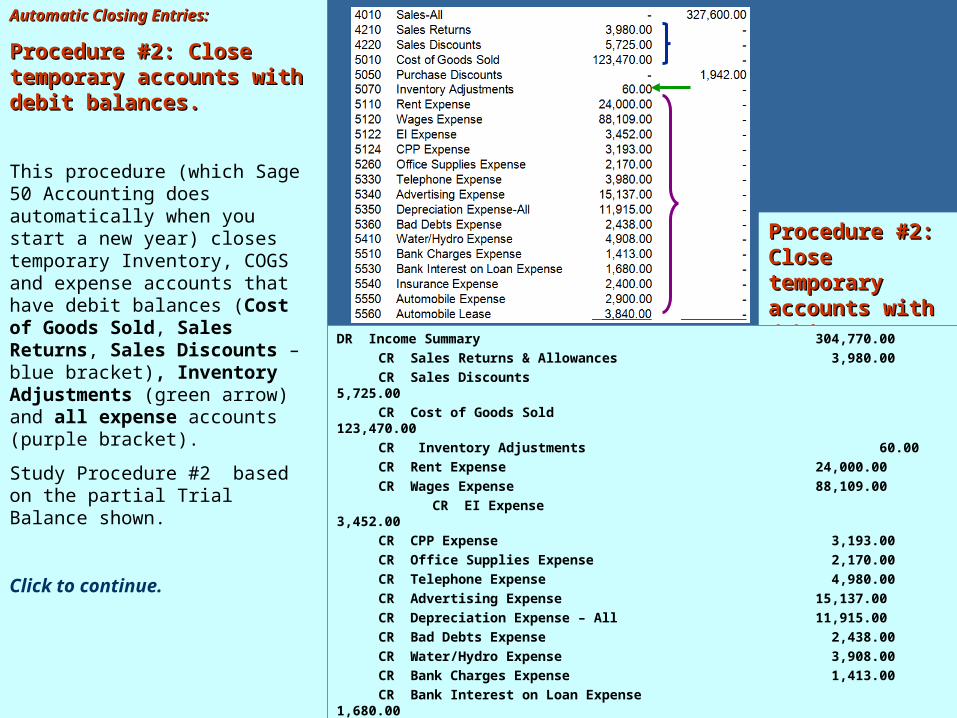

Procedure #2: Close Procedure #2: Close temporary accounts with debit temporary accounts with debit balances.balances.

This procedure (which Sage 50 Accounting does automatically when you start a new year) closes temporary Inventory, COGS and expense accounts that have debit balances (Cost of Goods Sold, Sales Returns, Sales Discounts – blue bracket), Inventory Adjustments (green arrow) and all expense accounts (purple bracket).

Study Procedure #2 based on the partial Trial Balance shown.

Click to continue.

Procedure #2: Procedure #2: Close temporary Close temporary accounts with accounts with debit balances.debit balances.

DR Income Summary 304,770.00

CR Sales Returns & Allowances 3,980.00

CR Sales Discounts 5,725.00

CR Cost of Goods Sold 123,470.00

CR Inventory Adjustments 60.00

CR Rent Expense 24,000.00

CR Wages Expense 88,109.00

CR EI Expense 3,452.00

CR CPP Expense 3,193.00

CR Office Supplies Expense 2,170.00

CR Telephone Expense 4,980.00

CR Advertising Expense 15,137.00

CR Depreciation Expense – All 11,915.00

CR Bad Debts Expense 2,438.00

CR Water/Hydro Expense 3,908.00

CR Bank Charges Expense 1,413.00

CR Bank Interest on Loan Expense 1,680.00

CR Insurance Expense 2,400.00

CR Automobile Expense 2,900.00

CR Automobile Lease 3,840.00

Automatic Closing Entries:Automatic Closing Entries: ((continued)continued)

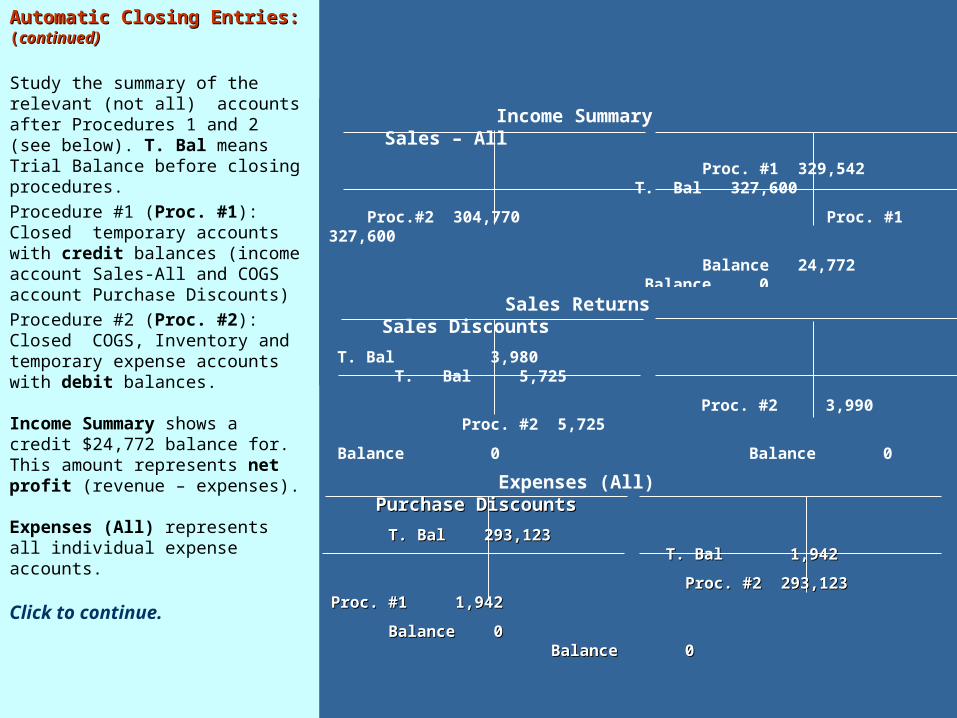

Study the summary of the relevant (not all) accounts after Procedures 1 and 2 (see below). T. Bal means Trial Balance before closing procedures.

Procedure #1 (Proc. #1): Closed temporary accounts with credit balances (income account Sales-All and COGS account Purchase Discounts)

Procedure #2 (Proc. #2): Closed COGS, Inventory and temporary expense accounts with debit balances.

Income Summary shows a credit $24,772 balance for. This amount represents net profit (revenue – expenses).

Expenses (All) represents all individual expense accounts.

Click to continue.

Income Summary Sales – All

Proc. #1 329,542 T. Bal 327,600

Proc.#2 304,770 Proc. #1 327,600

Balance 24,772 Balance 0

Sales Returns Sales Discounts

T. Bal 3,980 T. Bal 5,725

Proc. #2 3,990 Proc. #2 5,725

Balance 0 Balance 0

Expenses (All) Purchase Discounts Purchase Discounts

T. Bal 293,123 T. Bal 1,942T. Bal 293,123 T. Bal 1,942

Proc. #2 293,123 Proc. #1 1,942 Proc. #2 293,123 Proc. #1 1,942

Balance 0Balance 0 Balance 0 Balance 0

Automatic Closing Entries (continued)Automatic Closing Entries (continued)

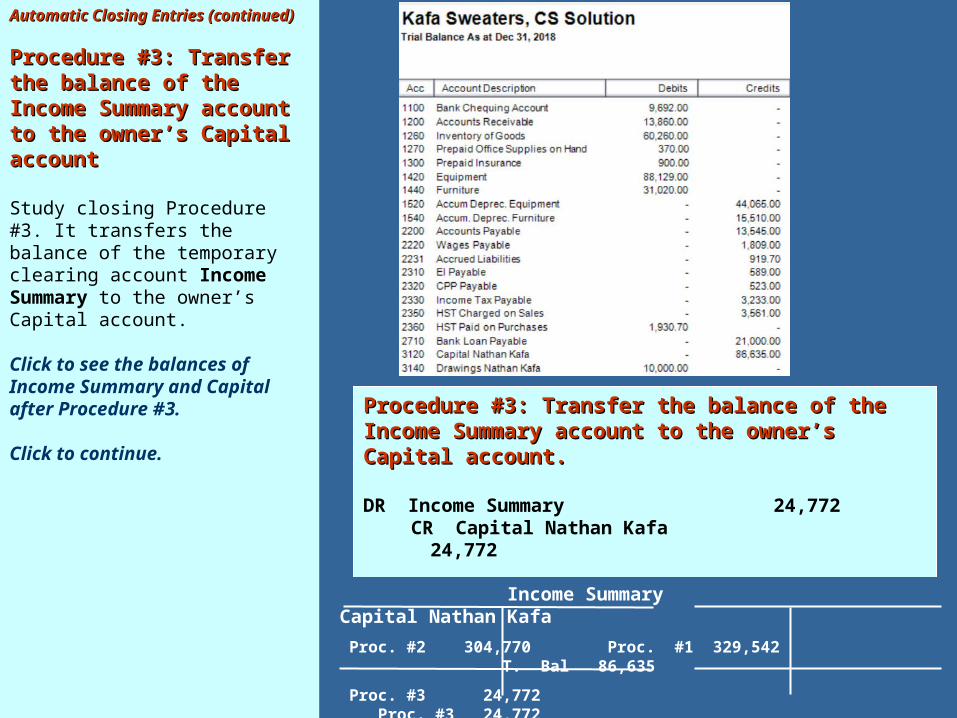

Procedure #3: Transfer the Procedure #3: Transfer the balance of the Income balance of the Income Summary account to the Summary account to the owner’s Capital accountowner’s Capital account

Study closing Procedure #3. It transfers the balance of the temporary clearing account Income Summary to the owner’s Capital account.

Click to see the balances of Income Summary and Capital after Procedure #3.

Click to continue. Procedure #3: Transfer the balance of the Income Procedure #3: Transfer the balance of the Income Summary account to the owner’s Capital account.Summary account to the owner’s Capital account.

DR Income Summary 24,772 CR Capital Nathan Kafa 24,772

Income Summary Capital Nathan Kafa

Proc. #2 304,770 Proc. #1 329,542 T. Bal 86,635

Proc. #3 24,772 Proc. #3 24,772

Balance 0 Balance 111.407

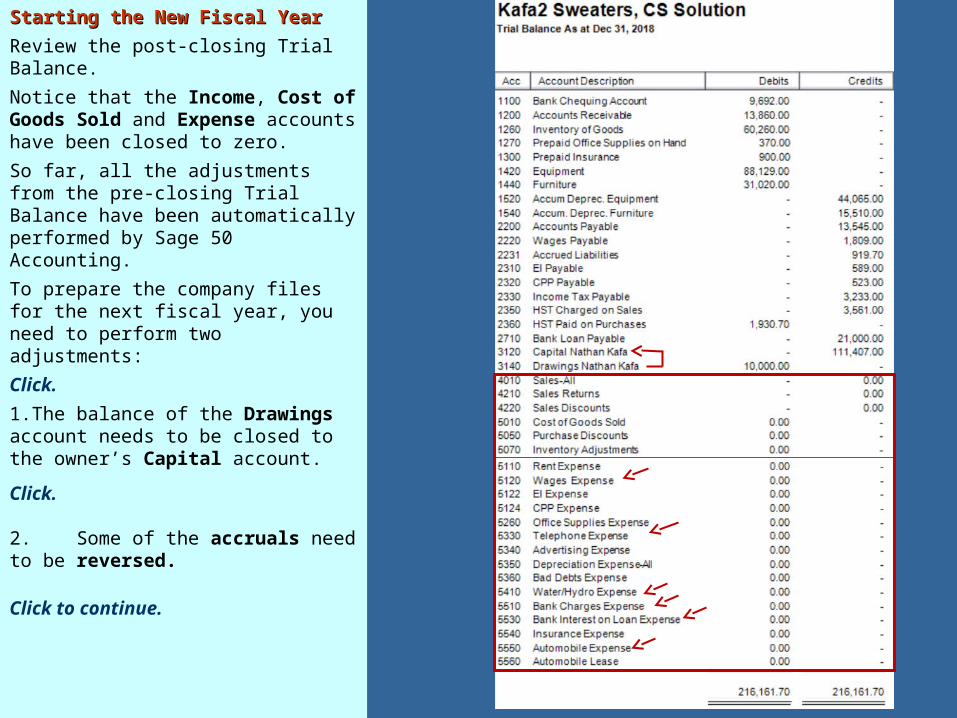

Starting the New Fiscal YearStarting the New Fiscal Year

Review the post-closing Trial Balance.

Notice that the Income, Cost of Goods Sold and Expense accounts have been closed to zero.

So far, all the adjustments from the pre-closing Trial Balance have been automatically performed by Sage 50 Accounting.

To prepare the company files for the next fiscal year, you need to perform two adjustments:

Click.

1.The balance of the Drawings account needs to be closed to the owner’s Capital account.

Click.

2. Some of the accruals need to be reversed.

Click to continue.

Starting the New Fiscal Starting the New Fiscal YearYear

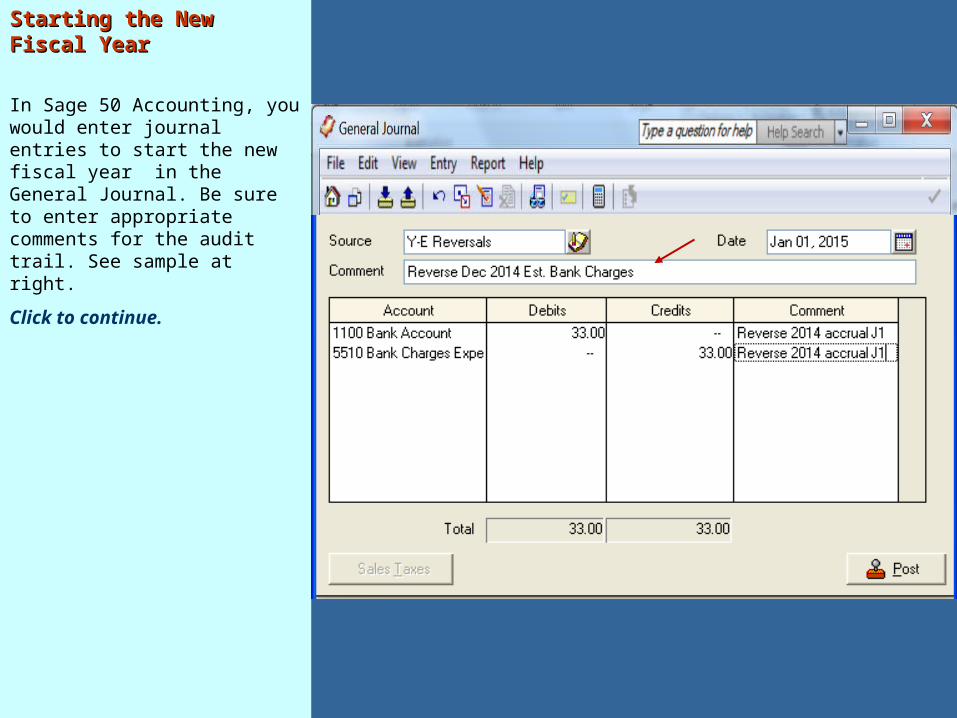

In Sage 50 Accounting, you would enter journal entries to start the new fiscal year in the General Journal. Be sure to enter appropriate comments for the audit trail. See sample at right.

Click to continue.

Starting the New Fiscal Year:Starting the New Fiscal Year:

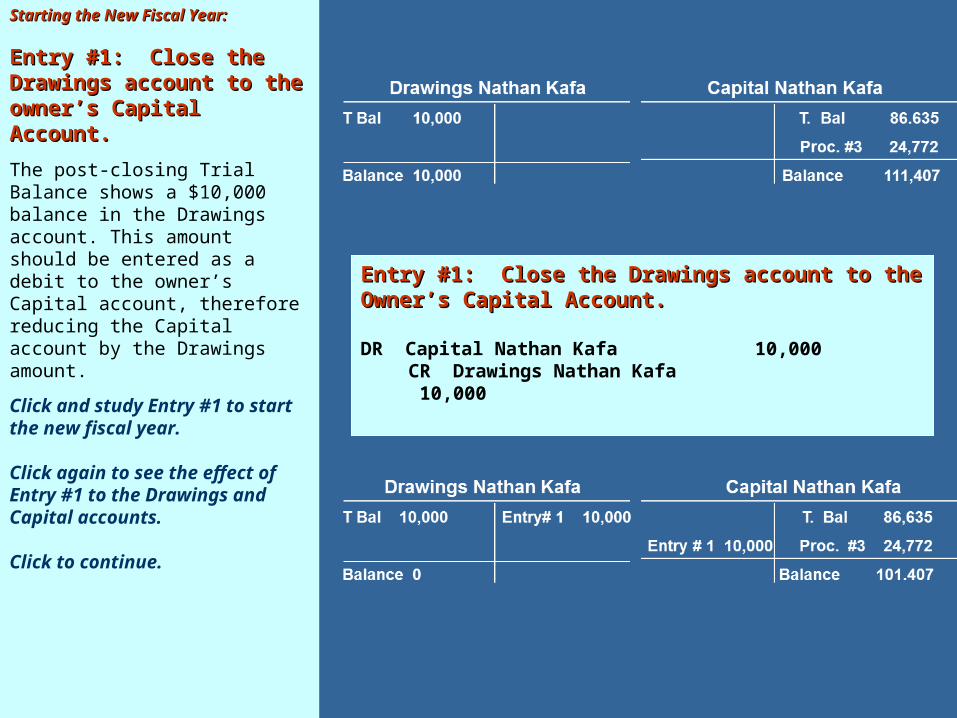

Entry #1: Close the Drawings Entry #1: Close the Drawings account to the owner’s account to the owner’s Capital Account.Capital Account.

The post-closing Trial Balance shows a $10,000 balance in the Drawings account. This amount should be entered as a debit to the owner’s Capital account, therefore reducing the Capital account by the Drawings amount.

Click and study Entry #1 to start the new fiscal year.

Click again to see the effect of Entry #1 to the Drawings and Capital accounts.

Click to continue.

Entry #1: Close the Drawings account to the Owner’s Entry #1: Close the Drawings account to the Owner’s Capital Account.Capital Account.

DR Capital Nathan Kafa 10,000 CR Drawings Nathan Kafa 10,000

Starting a New Fiscal Year:Starting a New Fiscal Year:

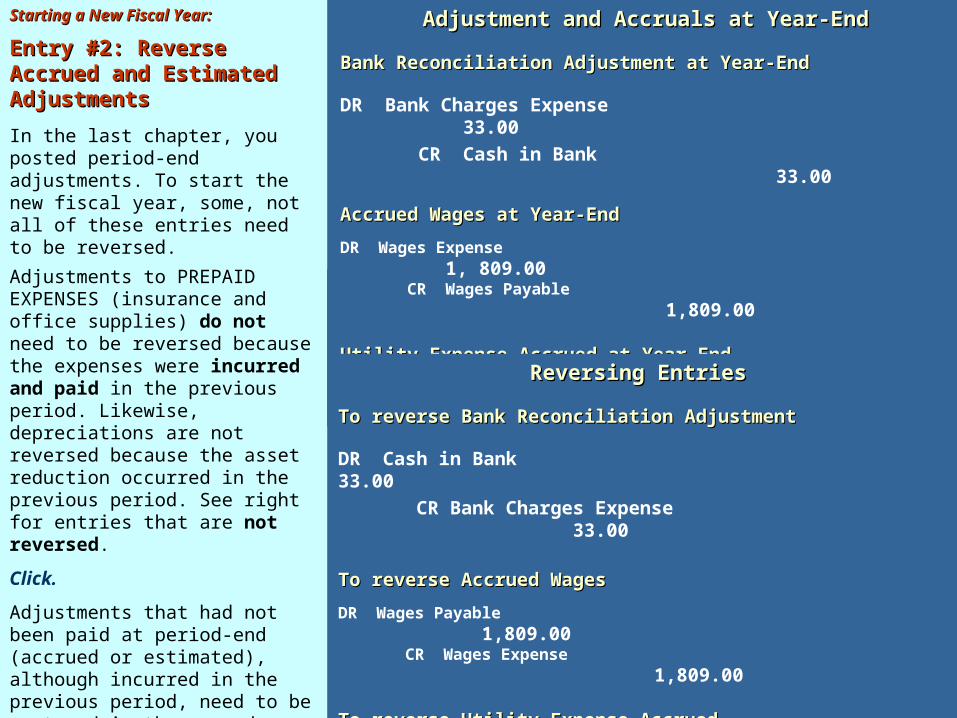

Entry #2: Reverse Entry #2: Reverse Accrued and Estimated Accrued and Estimated AdjustmentsAdjustments

In the last chapter, you posted period-end adjustments. To start the new fiscal year, some, not all of these entries need to be reversed.

Adjustments to PREPAID EXPENSES (insurance and office supplies) do not need to be reversed because the expenses were incurred and paid in the previous period. Likewise, depreciations are not reversed because the asset reduction occurred in the previous period. See right for entries that are not reversed.

Click.

Adjustments that had not been paid at period-end (accrued or estimated), although incurred in the previous period, need to be restored in the records; otherwise, when the expenses need to be paid, the account balance will not reflect the full amount of the invoice due.

Click to see the reversing entries.

Click to continue.

Insurance Expense Adjustment at Year-EndInsurance Expense Adjustment at Year-End

DR Insurance Expense 50.00

CR Prepaid Insurance 50.00

Depreciation Adjustment at Year-EndDepreciation Adjustment at Year-End

DR Deprec. Expense – Computer Equip. 580.00

CR Accrued Liabilities 580.00

Office Supplies Adjustment at Year-EndOffice Supplies Adjustment at Year-End

DR Office Supplies Expense 285.00

CR Prepaid Office Supplies 285.00

Journal Entries that are NOT reversedJournal Entries that are NOT reversed

Adjustment and Accruals at Year-EndAdjustment and Accruals at Year-End

Bank Reconciliation Adjustment at Year-EndBank Reconciliation Adjustment at Year-End

DR Bank Charges Expense 33.00

CR Cash in Bank 33.00

Accrued Wages at Year-EndAccrued Wages at Year-End

DR Wages Expense 1, 809.00 CR Wages Payable 1,809.00

Utility Expense Accrued at Year-EndUtility Expense Accrued at Year-End

DR Water/Hydro Expense 340.00 CR Accrued Liabilities 340.00Reversing EntriesReversing Entries

To reverse Bank Reconciliation Adjustment To reverse Bank Reconciliation Adjustment

DR Cash in Bank 33.00

CR Bank Charges Expense 33.00

To reverse Accrued Wages To reverse Accrued Wages

DR Wages Payable 1,809.00 CR Wages Expense 1,809.00

To reverse Utility Expense Accrued To reverse Utility Expense Accrued

DR Accrued Liabilities 340.00 CR Water/Hydro Expense 340.00

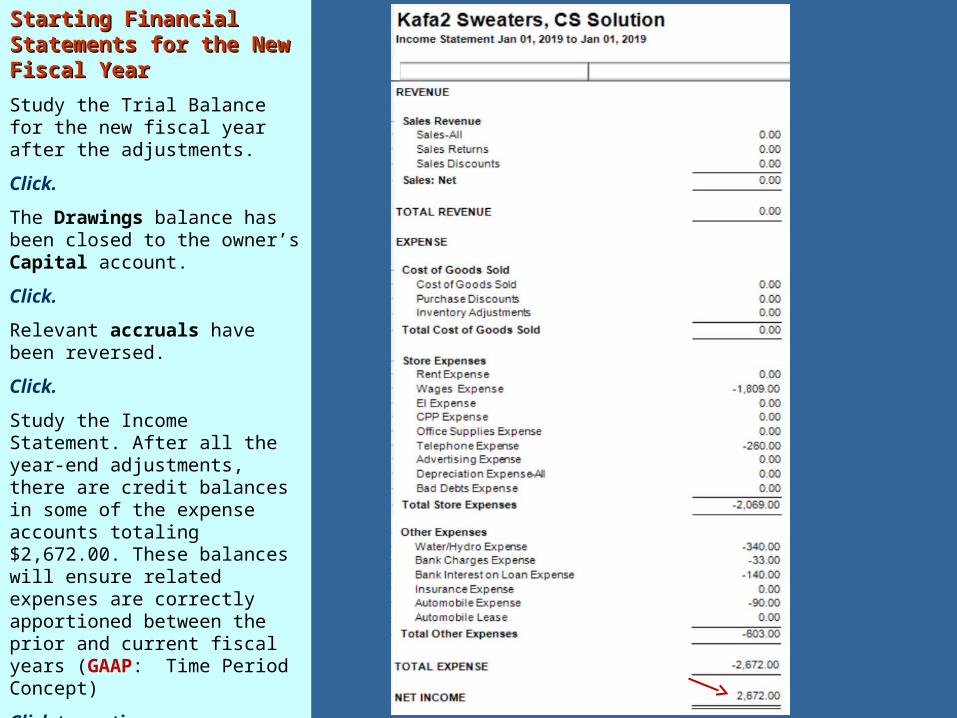

Starting Financial Starting Financial Statements for the New Statements for the New Fiscal YearFiscal Year

Study the Trial Balance for the new fiscal year after the adjustments.

Click.

The Drawings balance has been closed to the owner’s Capital account.

Click.

Relevant accruals have been reversed.

Click.

Study the Income Statement. After all the year-end adjustments, there are credit balances in some of the expense accounts totaling $2,672.00. These balances will ensure related expenses are correctly apportioned between the prior and current fiscal years (GAAP: Time Period Concept)

Click to continue.

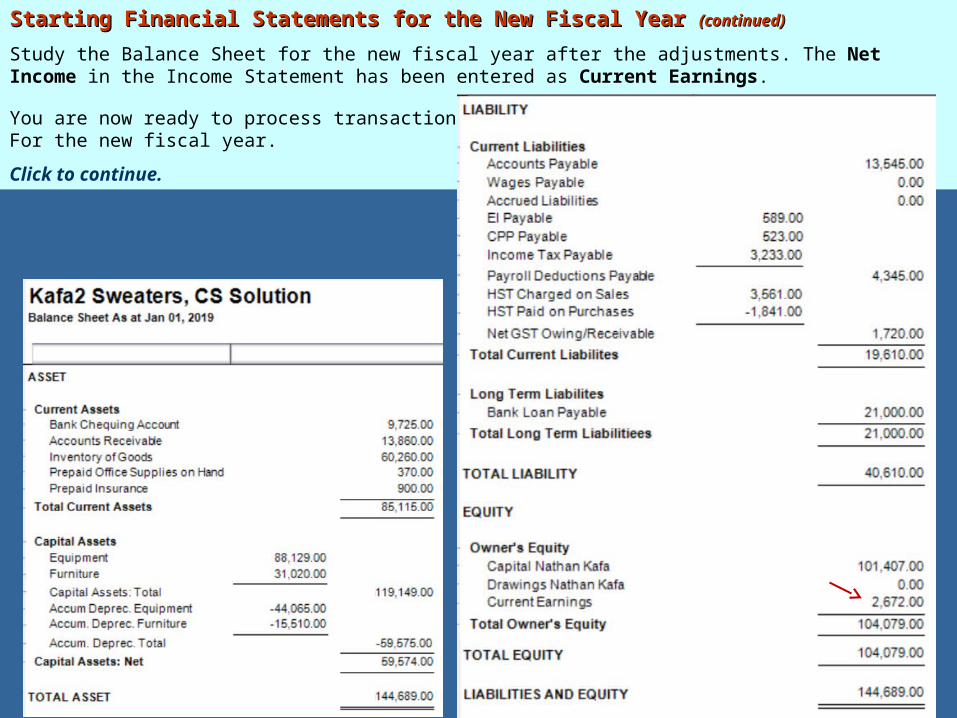

Starting Financial Statements for the New Fiscal Year Starting Financial Statements for the New Fiscal Year (continued)(continued)

Study the Balance Sheet for the new fiscal year after the adjustments. The Net Income in the Income Statement has been entered as Current Earnings.

You are now ready to process transactionsFor the new fiscal year.

Click to continue.

More…More…

Go back to your text and Go back to your text and proceed from where you have proceed from where you have left off.left off.

Review this slideshow when Review this slideshow when you finish the chapter to better you finish the chapter to better prepare yourself for the next prepare yourself for the next chapter.chapter.

Press ESC now, then click the Press ESC now, then click the EXIT button.EXIT button.

EXITEXIT