year book 2015 - nbfi & modaraba

TRANSCRIPT

Year Book 20

15

Year Book 2015

1

Contents1 Vision, Mission, Our Values & Core Objective 2

2 International & Regional Leasing Associations 4

3 Association’s Secretariat 5

4 Executive Committee Members 8

5 Messages

Ÿ Mr. Mohammad Ishaq Dar 12

Ÿ Mr. Zafar Ul Haq Hijazi 13

Ÿ Mian Muhammad Adrees 15

Ÿ Mr. Shahid Mahmood 16

6 Messages - NBFI & MAP

Ÿ Mr. Mahfuz-ur-Rehman Pasha 18

Ÿ Mr. Shuja Malik 20

Ÿ Ms. Effat Assad 21

7 Secretary General’s Report 22

8 Articles

Ÿ Anti-money Laundering & Counter Financing of Terrorism 28

Ÿ Ijarah; Practical Issues and their solutions- Shariah Perspective 30

Ÿ Role of Central Bank in Supporting NBFCs for Growth & Progress of SMEs 35

Ÿ A snap-shot of Islamic Banking & Finance in Sri Lanka 39

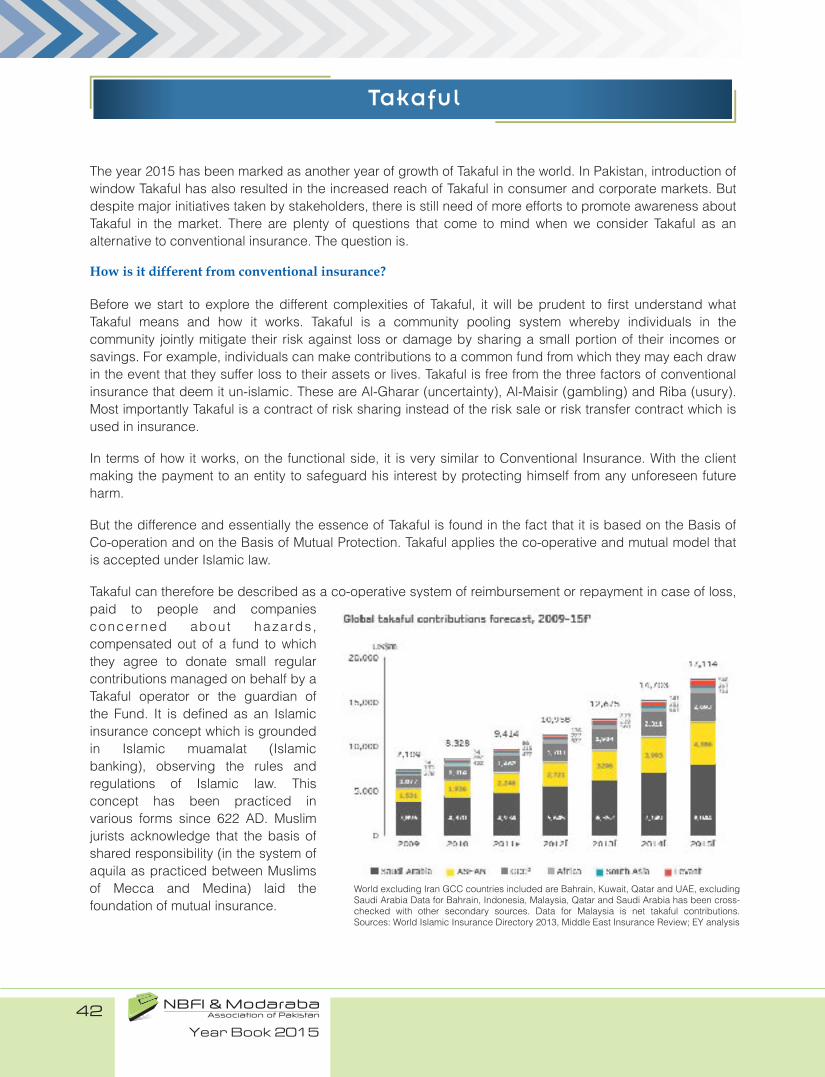

Ÿ Takaful 42

9 Events and Activities

Ÿ Launching Ceremony of Year Book 2014 46

Ÿ Best Performance Awards - 2014 47

Ÿ Fifth Annual General Meeting (AGM) 48

Ÿ MoU Signing Ceremony Between Pak Qatar General Takaful Ltd. & the Association 49

Ÿ Half Day Workshop On “Anti Money Laundering” 51

Ÿ Workshop on “Islamic Finance” For Directors & Senior Executives 52

Ÿ Interview on Business Plus TV Channel 53

Ÿ IBA – Centre for Excellence in Islamic Finance (CEIF) 53

Ÿ The Federation of Pakistan Chambers of Commerce & Industry (FPCCI) 54

Ÿ Meeting with World Bank Group Mission 55

Ÿ SECP’s Three Days Conference On “Non-Bank Financial Sector & Capital Market 56

Ÿ Achievements of Members 57

Ÿ New Entrants in the NBFI & Modaraba Sector 59

10 Macro Perspective

Ÿ Sectors Performance 62

Ÿ Statistical Overview 69

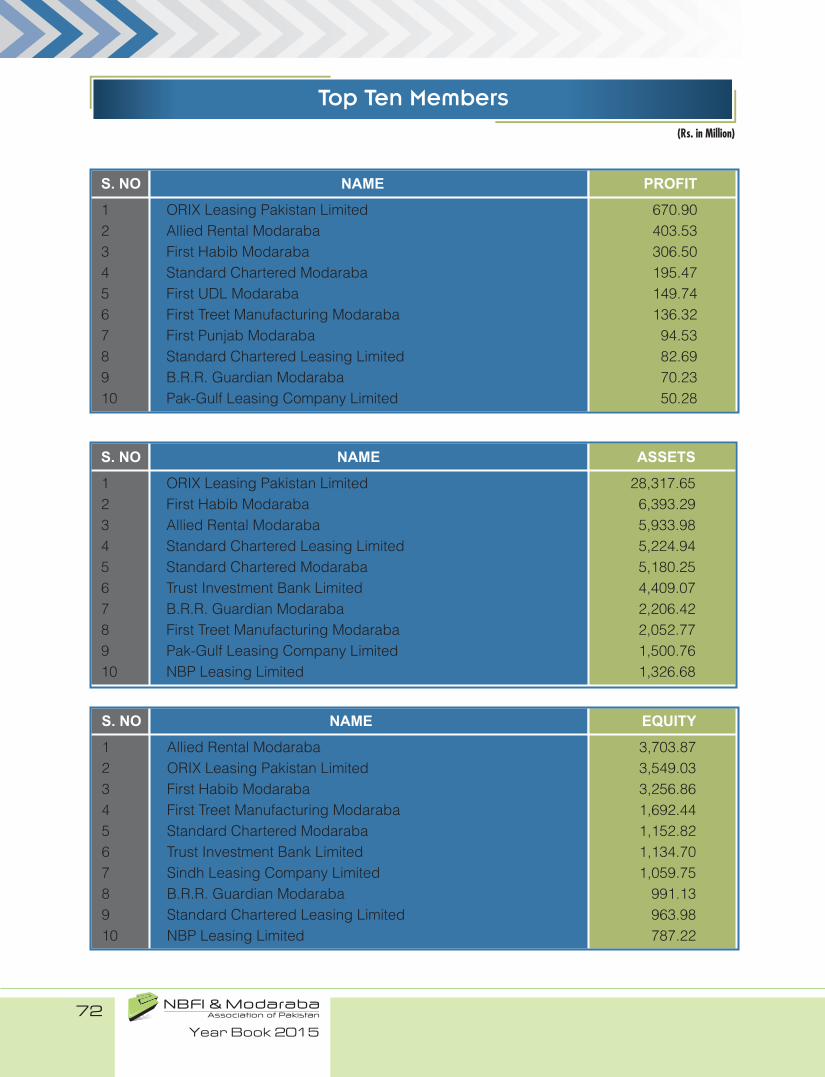

11 Top ten members 72

12 Members at a Glance

Ÿ Financial Overview 76

Ÿ Comparative position of payout 77

Ÿ Market Capitalization 78

13 Company Profiles 80

14 Glossary 120

15 Members’ Directory 126

16 Advertisements 131

Year Book 2015

2

MISSION STATEMENT

NBFI & Modaraba Association of Pakistan

To provide effective forum to address common and/or relevant issues, make available necessary support, facilitate to succeed through effective liaison, appropriate counselling, product innovation, research, capacity building and create conducive working environment based on trust, integrity and reliability.

To serve as an effective platform for the members of NBFI and Modaraba sector, to facilitate the growth, profiling and competitive power of NBFI & Modaraba Association members through collective and coordinated efforts.

Vision

Year Book 2015

3

NBFI & Modaraba Association of Pakistan

Collaboration

Integrity

Fairness

Excellence

Responsiveness

Ÿ To represent, profile and promote NBFI and Modaraba industry and protect the interest of Members.

Ÿ To encourage Islamic trade and finance through Modaraba venture and provide innovative Shariah compliant financial solutions for further progress and growth of the Modaraba sector.

Ÿ To maintain an active coordination and a relationship of trust with the regulatory authorities to achieve a consultative and supportive regulatory environment.

Ÿ To support environment where members work together to solve common challenges by sharing ideas and helping & supporting each other.

Ÿ To migrate best international practices and make information and analysis available on the profile and performance of individual members and the sector.

Ÿ To broaden the base of association through induction of new members from different segments within the NBFIs sector.

Ÿ To promote good governance, encourage performance based culture within members.

Ÿ To enhance professional capacity of members through workshops, seminars and interactive sessions.

Our Values

Core Objective

Year Book 2015

4

INTERNATIONAL FINANCE & INTERNATIONAL FINANCE &

LEASING ASSOCIATIONLEASING ASSOCIATIONNa Pankraci 310/60, 140 00 Praha 4, Na Pankraci 310/60, 140 00 Praha 4,

Czech RepublicCzech Republic

Tel: +420 602231495Tel: +420 602231495

Fax: +420 222 012 363Fax: +420 222 012 363

E-mail: [email protected]: [email protected]

Website: www.ifla.comWebsite: www.ifla.com

ASIAN FINANCIAL SERVICES ASIAN FINANCIAL SERVICES

ASSOCIATION (AFSA)ASSOCIATION (AFSA)EightyEight@Kasablanka, Tower A, 7th Floor, EightyEight@Kasablanka, Tower A, 7th Floor,

Unit D, JI. Casablanca Kavling 88, Unit D, JI. Casablanca Kavling 88,

Jakarta Selatan 12870,Jakarta Selatan 12870,

IndonesiaIndonesia

Tel: +62 21 2982 0180Tel: +62 21 2982 0180

Fax: +62 21 2982 0191Fax: +62 21 2982 0191

E-mail: [email protected]: [email protected]

Website: www.afsaworld.orgWebsite: www.afsaworld.org

INTERNATIONAL FINANCE &

LEASING ASSOCIATIONNa Pankraci 310/60, 140 00 Praha 4,

Czech Republic

Tel: +420 602231495

Fax: +420 222 012 363

E-mail: [email protected]

Website: www.ifla.com

ASIAN FINANCIAL SERVICES

ASSOCIATION (AFSA)EightyEight@Kasablanka, Tower A, 7th Floor,

Unit D, JI. Casablanca Kavling 88,

Jakarta Selatan 12870,

Indonesia

Tel: +62 21 2982 0180

Fax: +62 21 2982 0191

E-mail: [email protected]

Website: www.afsaworld.org

International & Regional Leasing Associations

FELALEASE - FEDERACION FELALEASE - FEDERACION

LATINOAMERICANA DE LEASINGLATINOAMERICANA DE LEASINGRua Diogo Moreira, 132 8º andar conj. 806 São Rua Diogo Moreira, 132 8º andar conj. 806 São

Paulo, BrazilPaulo, Brazil

Tel: +55 11 3095 9100,Tel: +55 11 3095 9100,

Fax +55 11 3095 9105Fax +55 11 3095 9105

E-mail: [email protected]: [email protected]

Website: www.felalease.orgWebsite: www.felalease.org

NBFI & MODARABA ASSOCIATION OF NBFI & MODARABA ASSOCIATION OF

PAKISTANPAKISTAN602, Progressive Centre, 30-A, Block-6, PECHS, 602, Progressive Centre, 30-A, Block-6, PECHS,

Shahrah-e-Faisal, Karachi-75400,Shahrah-e-Faisal, Karachi-75400,

PakistanPakistan

Tel: 92-21-34389774, 34322440Tel: 92-21-34389774, 34322440

Fax: 92-21-34389775Fax: 92-21-34389775

E-mail: [email protected]: [email protected]

Website: www.nbfi-modaraba.com.pkWebsite: www.nbfi-modaraba.com.pk

FELALEASE - FEDERACION

LATINOAMERICANA DE LEASINGRua Diogo Moreira, 132 8º andar conj. 806 São

Paulo, Brazil

Tel: +55 11 3095 9100,

Fax +55 11 3095 9105

E-mail: [email protected]

Website: www.felalease.org

NBFI & MODARABA ASSOCIATION OF

PAKISTAN602, Progressive Centre, 30-A, Block-6, PECHS,

Shahrah-e-Faisal, Karachi-75400,

Pakistan

Tel: 92-21-34389774, 34322440

Fax: 92-21-34389775

E-mail: [email protected]

Website: www.nbfi-modaraba.com.pk

LEASEUROPE, THE EUROPEAN FEDERATION LEASEUROPE, THE EUROPEAN FEDERATION

OF LEASING COMPANY ASSOCIATIONSOF LEASING COMPANY ASSOCIATIONSBoulevard Louis Schmidt 87, B - 1040 Brussels,Boulevard Louis Schmidt 87, B - 1040 Brussels,

BelgiumBelgium

Tel: +32 2 778 05 60Tel: +32 2 778 05 60

Fax: +32 2 778 05 78Fax: +32 2 778 05 78

E-mail: [email protected]: [email protected]

Website: www.leaseurope.orgWebsite: www.leaseurope.org

LEASEUROPE, THE EUROPEAN FEDERATION

OF LEASING COMPANY ASSOCIATIONSBoulevard Louis Schmidt 87, B - 1040 Brussels,

Belgium

Tel: +32 2 778 05 60

Fax: +32 2 778 05 78

E-mail: [email protected]

Website: www.leaseurope.org

Year Book 2015

5

Registered Office

602, Progressive Centre, 30-A,

Block-6, P.E.C.H.S., Shahrah-e-Faisal,

Karachi-75400, Pakistan

Phone: (92-21) 34389774, 34322440Fax: (92-21) 34389775

E-mail: [email protected]: www.nbfi-modaraba.com.pk

Auditors

Baker Tilly Mehmood Idrees Qamar

Chartered Accountants

Tax Advisor

Legal Advisor

Bankers

Shekha & Mufti

Chartered Accountants

Mohsin Tayebaly & Co.

Advocates & Legal Consultants

BankIslami Pakistan Limited

Mr. Muhammad Samiullah, Secretary General, holds a master degree in Economics, L.L.B, DAIBP, PGD in Islamic Finance & Banking having a vast experience of banking and financial sector. Prior to joining Modaraba Association of Pakistan in 2001, he was Company Secretary, First Habib Bank Modaraba. He also officiated as Chief Executive of First Habib Bank Modaraba for quite some time.

He has been appointed as Chairman, FPCCI Standing Committee on NBFI & Modaraba for the year 2016. He was an active Member of FPCCI, Standing Committee for Islamic Banking & Takaful during the year 2015 and will continue the position for the year 2016 as well. He is also a Member of Arbitration Panel of Pakistan Stock Exchange Limited.

Association’s Secretariat

Muhammad SamiullahSecretary General

Year Book 2015

6

Year Book 2015

7

Executive Committee

Members

Year Book 2015

8

Mr. Pasha posseses B.Sc. (Electrical Engineering) Degree from, Peshawar University. He is an Associate Member of the Institute of Engineers in Pakistan and holds Diploma in German Language.

He has served in the communication & work Department of KPK province as Assistant Executive Engineer from 1973-1981. In September 1981 he joined the Civil Services of Pakistan (Initially Income Tax group later renamed as Inland Revenue Service). Mr. Pasha served as Deputy Commissioner, Additional Commissioner & Commissioner in various branches of the service i.e. Audit, Enforcement, Legal, Tax Facilitation & Human Resource Development. In 2011 he retired in BS-21 after having served the Department for 30 years.

As Secretary International Taxes in the Federal Board of Revenue and Deputy Secretary, Economic Affairs Division, Ministry of Finance, Government of Pakistan, he actively interfaced with DFIs of Pakistan and their respective foreign investment agencies, besides various international multilateral financial institutions. Presently he is working as CEO of Pak-Gulf Leasing Company Limited

Executive Committee 2015-2016

Mahfuz-ur-Rehman PashaChairman

Mr. Shuja Malik is an Accounting and Finance graduate from the University of East London. He has experience of over 17 years in banking, sales and marketing of agro chemicals, stock market trading, pharmaceuticals, etc. He had previously been on the boards of two public limited companies, namely Searle Pakistan Limited and United Brands Limited. Currently he is on the board of First UDL Modaraba.

Shuja Malik

Senior Vice Chairman

Ms. Effat Assad is a Fellow Member of The Institute of Chartered Accountants of Pakistan. She joined the Finance Department of ORIX Leasing Pakistan Limited (OLP) in 1990 and served in various positions until 1999. Ms. Assad left the Company in April 1999 and was associated with the Institute of Chartered Accountants of Pakistan as a free lancer until September, 2005 when she rejoined OLP’s Finance Department. She assumed the charge of Company Secretary in September 2011.

Effat AssadVice Chairperson

Year Book 2015

9

Executive Committee 2015-2016

Syed Wajih Hassan is Fellow of Chartered Accountant. He holds 20+ years of professional experience serving in MNC’s including leading Financial Institutions and IT companies at middle to senior level positions, before joining as CEO of First Paramount Modaraba. Having vast experience in the field of business and finance, Wajih has been instrumental in introducing new ventures to the Modaraba using Musharika and Modaraba modes of investments.

Syed Wajih Hassan

Member

Mr. Shiraz Butt holds Master Degree in Business Administration and has an experience of over 15 years in the Modaraba / Leasing and Investment Banking Sectors. Currently he is working as Chief Operating Officer of First IBL Modaraba. Mr. Shiraz started his professional carrier back in 1996 with a leasing company, and in 1999 he moved to Modaraba sector.

He initially worked on corporate financing side and in 2005 he switched over Micro and Small Enterprise (MSE) financing division in a Modaraba for extending Ijarah / Lease / Musharakah / Murabahah facilities to lower income/poor communities in order to enhance/ improve their income stream in collaboration with Swiss Agency for Development and Cooperation (SDC).

Shiraz ButtMember

Mr. Jalaluddin Ahmed holds degree in B.A. Economics Statistics and has over 30 years of experience in Commercial Banking and Islamic Financial Products. His Commercial Banking experience including 10 years of International exposure by serving United Bank Limited in various countries in the Middle East. Mr. Jalal is CEO of First Al-Noor Modaraba.

Jalaluddin AhmedMember

Year Book 2015

10

Executive Committee 2015-2016

Mrs. Hamida Aqeel is working as Chief Operating Officer / Company Secretary of Trust Modaraba is an MBA from Institute of Business Administration, Karachi, having over 15 years of experience of credit and corporate affairs. She also holds a Diploma in "Management for General Manager" from Netherlands. She has previously worked in Pak-Libya Holding Co. (Pvt) Ltd. and was on the Board of AI-Zamin Leasing Modaraba as their nominee till 1995. She has been with Al Zamin Modaraba Management (Pvt) Limited since year 2000.

Qazi Obaid Ullah is a MBA-Banking & Finance and CA Intermediate, having more than 24 years of experience of Finance and Accounts, Audit, Fund Management Corporate & Legal Affairs, Capital Market Operations, having a diversified experience of IT and Financial Sector. Presently he is working as CFO, First Equity Modaraba.

Muhammad Siddique is working as CFO and Company Secretary of Standard Chartered Modaraba. He is an associate member of Institute of Chartered Accountants of Pakistan. He has over 14 years of experience in Audit, Finance, Company Sectretary and Treasury. Prior to joining SCM, he worked as CFO and Company Secretary of Standard Chartered Leasing Limited and Head of Finance Standard Chartered Bank (Pakistan) Limited – Islamic Banking Division.

Mr. Sajjad Haider Khan is Associate member of Cost & Management Accountants of Pakistan (ICMAP). He has vast experience in handling accounts and finance. He joined the Company in 1997. Presently he is serving to First Treet Manufacturing Modaraba as Chief Accountants.

Hamida AqeelMember

Qazi Obaid Ullah AnsariMember

Muhammad SiddiqueMember

Sajjad Haider KhanMember

Year Book 2015

11

Messages

Year Book 2015

12

I am pleased to learn about the initiative taken by the NBFI &

Modarabas Association of Pakistan for publishing its Year Book for

the financial year 2014-2015 which represents a comprehensive

collation and analysis of all Leasing Companies, Investment Banks

and Modarabas operating in Pakistan.

The NBFIs (non-bank financial institutions), whether conventionally

operating, or on a Shariah-compliant basis, are meant to fulfil the

credit requirements and investment management needs, in

particular, of the individual entrepreneur and those of association of

persons (AoPs), falling under the category of Small & Medium

Enterprises (SMEs). Together, both constitute the primary level for

capital formation, which gradually evolves into larger manufacturing

and services providing enterprises, contributing to the overall

development and growth of the country’s economy. There is still a

great need for strengthening, expanding and promoting the NBFIs

Sector in Pakistan and our Government is prepared to play her part in

this matter, in consultation with NBFIs & Modarabas Association of

Pakistan and the Securities & Exchange Commission of Pakistan

(SECP).

Modaraba is an effective vehicle for undertaking an array of financial

services for the benefit of business and industrial enterprises

choosing to operate on Shariah-compliant basis. Modaraba Sector

has great potential for expansion and our Government is fully

cognizant of this sector’s immense utility in the years to come.

I wish the NBFI & Modarabas Association of Pakistan and all its

Member Institutions every success in their respective business

undertakings, while promising them my full support on behalf of our

Government.

Mr. Mohammad Ishaq DarMinister for Finance,

Revenue, Economic Affairs,

Statistics and Privatization

Message

Year Book 2015

13

The Year Book of the NBFI and Modaraba Association has been an

important publication providing information for reviewing and

assessing the performance of the sector on a regular basis. I

congratulate the Association for launching the Year book for 2015.

Non-Banking Financial Institutions (NBFIs) have been an integral

part of the country’s regulated financial sector for the last more than

two decades. However, these institutions have not been able to make

the desired contribution to the overall financial system and the assets

of these institutions account for around 6% of the banking sector

assets only.

With the objective of nurturing Non-Bank Financial (NBF) Sector, the

Securities and Exchange Commission of Pakistan (SECP) has

revamped the entire regulatory framework.

The concept of small and mid-sized non-deposit taking Non-Banking

Finance Companies (NBFCs) with significantly reduced equity and

other requirements has been introduced. Contrary to the former

regime, the companies not incorporated as NBFCs but fulfill the

prescribed eligibility criteria may also obtain license for lending

activities.

A new class of NBFCs i.e. Non-Bank Micro Finance Companies has

been introduced along with a comprehensive framework for

providing finance to low income individuals and micro enterprises. In

order to regulate the non-bank micro finance institutions under NBFC

regime, appropriate amendments have also been incorporated.

Considering the interest of depositors, the concept of Capital

Adequacy Ratio (CAR) has been introduced and deposit raising

ability of NBFCs has been linked with equity, credit rating and CAR

along with introduction of various other risk management measures.

Instead of following a one-size-fits-all strategy, different eligibility

criteria encompassing various aspects such as type of company,

number of directors, rating requirements etc. have been prescribed

in view of the unique and diversified characteristics of each business

activity of NBFCs.

Mr. Zafar Ul Haq HijaziChairman, SECP

Message

Year Book 2015

14

Although, leasing companies have shown 11% growth in their assets over the last year, however only one

company out of nine leasing companies has distributed dividend in the year 2015. Despite the fact that

Modaraba can undertake a wide range of business activities and also enjoy tax free status, only six Modarabas

out of twenty five have distributed dividend above 10% for the financial year ended June 30, 2015.

The industry players must strive to explore relatively untapped markets such as SMEs and microfinance sector in

order to generate better returns for their shareholders. There is a strong need for majority players of industry to

assess their business operations’ viability in order to provide some reasonable return to their investors.

Modarabas through increased focus on product innovation and customer service, can play a vital role in

promoting Islamic mode of financing which has an immense growth potential.

The role of the Association is commendable as it has always contributed positively and provided the support

needed by the sectors in distressful times. However, the Association needs to be more vibrant and should lead

the way by crystallizing the future road map for the industries it represents. The NBFI and Modaraba association

has to critically review the performance of its members and shall help them in improving corporate governance,

risk management and Shariah compliance by imparting regular trainings. Although support and facilitation from

SECP shall always be available, nevertheless, we would expect the Association to make further efforts towards

development of a vibrant and progressive financial sector of the country.

In the end, I wish to emphasize that SECP is fully committed to support the NBFI and Modaraba sector.

Year Book 2015

15

I congratulate the members of NBFI & Modaraba Association of

Pakistan for publishing their sixth Year Book for the year ended 30th

June 2015. The sustained efforts of the Association to document the

performance of NBFI & Modaraba sector is indeed commendable. I

am confident that this will serve as a useful tool for information on

NBFI & Modaraba sectors for all the stakeholders including potential

investors, research analysts & others.

NBFI & Modaraba sectors which include Leasing Companies,

Modarabas and Investment Banks, owing to their unique nature have

immense potential to support the overall financial system of the

country. The Modarabas have a great potential to grow through

covering the untapped markets i.e. SMEs, Microfinance and

Agriculture.

The Federation of Pakistan Chambers of Commerce & Industry

(FPCCI) is playing a very important role in the promotion of Islamic

Banking in the business community. The federation has constituted a

FPCCI Standing Committee on Islamic Banking and Takaful which is

organizing workshops / seminars with the help of other chambers in

the country to give awareness about the Islamic Products not only to

the business community but general public as well.

FPCCI fully support NBFI & Modaraba Association of Pakistan and

wish that the Association continues to play its due role in the growth of

the Islamic Finance Industry in Pakistan.

Mian Muhammad AdreesPresident, FPCCI

Message

Year Book 2015

16

I am pleased to note that the NBFI & Modaraba Association of

Pakistan is publishing its sixth year book - 2015. The year book has

been a source of information for the stakeholders, investors and

research analysts. Regular publication of the yearbook is creating

general awareness about the activities of NBFIs and Modaraba

Sector.

During the period 2014-15, 4 new companies were registered as

Modaraba companies under the Modaraba Ordinance, 1980. One

modaraba company floated a Modaraba. The remaining 3 Modaraba

Companies are expected to float Modarabas in near future. As per

the financial statements of 25 operational Modarabas as of June 30,

2015, the aggregate equity of the Modaraba was Rs.15.89 billion and

total assets of the Modaraba sector stood at Rs. 30.74 billion.

Out of 25 operational Modarabas, 21 modarabas declared cash

dividend. However, a critical analysis of the financial figures for the

year 2015 has revealed that except a few, dividend declared by the

bigger chunk is not up to the mark. The meagre returns being offered

by Modarabas cannot be considered competitive with the returns

offered by similar players in the financial sector. All the modaraba

companies need to review their performance and come up with new

business plans and strategies to boost the business, profitability and

returns of modarabas managed by them. I assure you that the SECP

would facilitate the modaraba sector in this drive.

Modarabas have great potential to grow as the appetite for Islamic

finance and products are increasing day-by-day. Modaraba sector

needs to tap the opportunity by offering unique and diversified

services and products to the customers. Securities and Exchange

Commission of Pakistan is committed to provide every help in

achieving this goal.

Mr. Shahid MahmoodRegistrar Modaraba,

SECP

Message

Year Book 2015

17

Messages -NBFI & MAP

Year Book 2015

18

It gives me immense pleasure to present the 6th Year Book of the

NBFI & Modaraba Association of Pakistan covering the performance,

activities, analysis and other related data and information of not only

the individual members of the Association, but also of the entire NBFI

& Modaraba Sectors (excluding Mutual Funds), during the year

ended 30th June, 2015.

NBFI & Modaraba Association is presently a representative body for

a total of 38 Member Institutions, comprising of 10 Leasing

Companies, 25 Modarabas and 3 Investment Banks. The expected

addition, as a member, of Awwal Modaraba, sponsored by Pak

Brunei Investment Company Limited with a Paid-up Capital of Rs.

One billion, following completion of post-floatation formalities, shall

strengthen the Modaraba Sector’s position within the Association.

During the year under review, Securities & Exchange Commission of

Pakistan has registered four Modaraba Management Companies

under the Modaraba Ordinance, 1980, out of which one modaraba

management company has floated its Modaraba, while the

remaining three are expected to issue IPO’s in the near future.

Despite low economic growth, the Modaraba Sector has positioned

itself as a stable provider of a wide spectrum of Shariah compliant

financial products for its customers and has continued to perform

reasonably well. As per audited financial statements of 25

operational modarabas as on 30th June, 2015, the aggregate equity

of all modarabas stood at Rs.15,897 million with total assets of

Rs.30,739 million.

Likewise, the Leasing Sector consisting of 10 companies has also

performed well by booking a total profit of Rs.655 million against total

assets of Rs.40,624 million and total equity Rs.6,887 million.

In order to give a better environment to the Leasing & Modaraba

Sectors, SECP took various measures such as amending the NBFC

Regulations, 2008 and the NBFC Rules, 2003, besides issuing Draft

Modaraba Regulations, 2015 for comments and professional input of

the stakeholders.

Mr. Mahfuz-ur-Rehman PashaChairman

Chairman’s Message

Year Book 2015

19

In order for the Modarabas to be strictly Sharia-compliant, Insurance of assets has been switched from the

conventional to the Takaful (Islamic) mode. The Association, following discussions on the subject with various

Takaful companies, has finally entered into a MoU with Pak Qatar General Takaful Limited, under which the latter

shall provide better and competitive rates to all members of the Association. This would encourage the members

to promote Sharia-compliant insurance cover to assets financed by them on account of their clients.

The Association has also supported SECP in its Investor Education Program, under the brand name of “Jama

Punji”. All member institutions have published advertisements for this brand in their respective annual reports

for making the investors more aware of the products offered by NBFIs and Modarabas and of the inherent risks

and rewards for making use of them. The Association is also contributing advertisements in the prominent

newspapers, on behalf of the SECP, for making the latter’s print media campaign for this purpose.

NBFI & Modaraba Association is playing an important role in promoting the sectors it represents by enhancing its

activities, with a view to making it an active and professionally vibrant representative body for its constituents.

This proactive involvement of the Association for the benefit of its Member Institutions shall continue to be

enlarged and expanded in the time to come.

On behalf of the NBFI & Modaraba Association, I thank Mr. Muhammad Ishaq Dar, Federal Minister for Finance,

Mr. Zafarul Haq Hijazi, Chairman, SECP, Mr. Zafar Abdullah, Commissioner (SCD), SECP, Mr. Asif Jalal Bhatti,

Executive Director, Mr. Shahid Naseem, Executive Director, Mr. Shahid Mahmood, Registrar Modaraba and

other officials of SECP for their continued support and guidance.

I also express my gratitude to the members of NBFI & Modaraba Association and members of the Executive

Committee for their confidence reposed in me for electing me as Chairman of the Association.

I also wish to place on record my appreciation of the consistent hard work undertaken by Mr. Muhammad

Samiullah, Secretary General of the Association and the contribution of other staff, towards making the

Association’s position, efforts and output more meaningful for our Members.

Year Book 2015

20

It is a matter of immense pride that NBFI & Modaraba Association is

publishing its Sixth Year Book. Over a period of time the year book

has attained the status of a useful document which provides

comprehensive details about the NBFI & Modaraba Sectors to its

stakeholders, investors and analysts.

Since 1980, when the Modaraba Ordinance was promulgated, the

Modaraba Sector has witnessed ups and downs. The number of

modarabas at one time, rose to 52 and thereafter, due to many factors

have reduced to 25, however, the performance of the Sector is on an

improving trend which is evident from the statistics. Moreover, the

Modaraba sector over the years is now not limited to financial

activities but a few have also entered into manufacturing and Trading

as well.

During the year 2014-15 the modaraba sector booked a profit of

Rs.1,353 million, whereas, the total assets were Rs.30,738 million

and the total equity was Rs.15,894 million. The modarabas declared

cash dividend to its certificate holders between the range of 0.90% to

90% and the payout was Rs.1,049 million.

The leading modarabas in terms of profit declared during the year

were Allied Rental Modaraba Rs.403 million, First Habib Modaraba

Rs.306 million, Standard Chartered Modaraba Rs.195 million, First

UDL Modaraba Rs.150 million and Treet Manufacturing Modaraba

Rs.136 million. The dividend declared by the modarabas are 90% by

First Imrooz Modaraba, 45% by First UDL Modaraba, 33% by

Standard Chartered Modaraba, 23% by First paramount modaraba,

22% by First Habib modaraba and 20% By Allied Rental Modaraba.

One of the milestones achieved by the Modaraba Sector is that

Proper Shariah Guidelines for the sector are now in place and the

activities are now monitored by a shariah advisor. Therefore, when

making investment decisions, the investors are now more confident

of the Modaraba sector regarding Shariah compliance. The

association is also working very hard for the improvement in the

shariah compliance and shariah audit mechanism and other aspects

of shariah to strengthen the modarabas as a true Islamic sector.

I wish NBFI & Modaraba Association, every success in its endeavors.

Mr. Shuja MalikSenior Vice Chairman

Message

Year Book 2015

21

I would like to congratulate NBFI & Modaraba Association of Pakistan

on bringing out its sixth year book for the year ended 30th June, 2015.

Leasing sector is an important segment of Pakistan’s financial sector

which played a vital role in the development of SME Sector.

In Pakistan leasing started, as an organized sector, in the mid-

eighties with the establishment of the first leasing company in 1984.

Over the period the number of leasing companies in the Country rose

to 41 until it was hit by liquidity crisis in 2008 – 2009. Non-availability

of long-term funds and withdrawal of credit lines by the banks after

the financial crisis of 2008-2009 resulted in closure / merger of a

number of leasing companies. Over a decade, only one new leasing

company has acquired the leasing license which has revived the

overall market sentiments. At present, number of active leasing

companies stands at 10.

The Securities & Exchange Commission of Pakistan amended NBFC

Regulations, 2008 and NBFC Rules, 2003. According to new

regulations, NBFCs have been segregated between deposit-taking

and non-deposit taking entities. Minimum capital requirement for

non-deposit taking entity is reduced drastically in order to encourage

such companies. This is likely to facilitate new companies to enter

into leasing business and encourage informal players to register as

leasing companies.

Leasing Sector during the year under review has performed well and

booked a profit of Rs.655 million as compared to a profit of Rs.585

million in the corresponding period. The Asset base of the leasing

sector was Rs.40,624 million while the total equity was Rs.6,887

million. The payout to its shareholders was Rs.369 million. ORIX

Leasing Pakistan Limited is the major player of the leasing sector

whose assets alone were Rs.28,449 million and equity was Rs.3,548

million and profit of Rs.671 million.

I congratulate all the Chief Executives and concerned CFOs and their

teams for providing the data enabling the Association to compile a

valuable information. The General Secretary of the Association and

his team also deserve appreciation for their effort to publish the Year

Book for years so regularly.

Ms. Effat AssadVice Chairperson

Message

Year Book 2015

22

Mr. Muhammad SamiullahSecretary General

Secretary General’s Report

The NBFI & Modaraba Association of Pakistan undertook following

activities during the year ended 30th June, 2015:

LAUNCHING OF YEAR BOOK – 2014:

Launching of 5th Year Book of NBFI & Modaraba Association of

Pakistan was held on 26th February, 2015 at Pearl Continental Hotel,

Karachi. Mr. Fida Hussain Samoo, Commissioner (Insurance), SECP

presided over the ceremony while Mr. Shahid Nasim, Executive

Director and Mr. Tariq Soomro, Director, SECP also attended the

ceremony.

BEST PERFORMANCE AWARDS FOR 2014:

In order to acknowledge the performance, the Association every year

gives Best Performance Awards to the outstanding performers of the

NBFI & Modaraba Sectors.

Based on the results of 30th June, 2014, the following members were

adjudged best performers for the year 2014 in accordance with the

criteria approved by the Executive Committee:

1st Position - Allied Rental Modaraba

2nd Position - ORIX Leasing Pakistan Limited

3rd Position - First Habib Modaraba & Standard Chartered

Modaraba (jointly) both the members acquired equal

marks as such they were declared joint winners of

third position.

5TH ANNUAL GENERAL MEETING:

Fifth Annual General Meeting of NBFI & Modaraba Association of

Pakistan was held on 17th September, 2015 at the Conference Hall of

Year Book 2015

23

the Association. In the said meeting Annual Accounts of the Association for the period ended 30th June, 2015

were approved by the General Body and Auditors for the year 2015-16 were re-appointed. The Election

Commission announced the results of the Office Bearers and Executive Committee Members for the year 2015-

16. The outgoing Chairman highlighted the performance of the NBFI & Modaraba Sector and activities of the

Association during his tenure. The incoming Chairman appreciated the work done by the Executive Committee

and assured that he will continue the pace of the work and make more efforts to complete some of the goals

which could not be achieved during the last tenure such as Tax Refund of the Association etc.

TAX REFUND OF THE ASSOCIATION:

Due to the persistent efforts of the Association, tax refund amounting to Rs.522,852 for the three years have been

received by the Income Tax Authorities. Refund of Tax for the period 2014 and a portion of refund for other years

could not be issued due to certain IT problems which were being faced by the Department however, the

Department has assured that as soon as the problems are resolved balance refund would also be issued. The

Association is following up the matter vigorously.

INTERACTION WITH THE REGULATORS:

Ÿ Amendments in NBFC Regulations, 2008 & NBFC Rules, 2003:

Securities & Exchange Commission of Pakistan (SECP) issued Draft Amendments in NBFC Regulations,

2008 and Draft Amendments in NBFC Rules, 2003 and invited comments/input from all the stakeholders.

The NBFI & Modaraba Association undertook an in-depth discussion with the members and after getting

feedback from them, forwarded comprehensive recommendations to SECP. Thereafter, a delegation from

the Association went to Islamabad for detailed discussion with the SECP Officials. Now the final

amendments in the NBFC Regulations, 2008 & NBFC Rules, 2003 have been received from SECP.

Ÿ Amendments in Modaraba Regulations, 2015:

The Registrar Modaraba issued Draft Modaraba Regulations, 2015 and invited comments/input from the

Association. The Association held various discussions with the members and after their concurrence

finalized the recommendations to the Registrar Modaraba for consideration, which is still pending with the

SECP.

Ÿ Companies Act, 2015

SECP issued Draft Companies Bill, 2015 wherein amendments and consolidation of law relating to

Companies, Non-Banking Finance Companies for the purpose of regulation of the entire corporate sector

and for protection of investors and creditors, promotion of investments and development of economy and

other matters connected have been made. SECP also invited comments/input of the stakeholders on the

above.

TRAINING & WORKSHOPS:

Ÿ WORKSHOP ON ANTI-MONEY LAUNDERING

Half day Workshop on “Anti-Money Laundering, Counter Terrorist Financing & Sanctions” was organized on

Year Book 2015

24

16th June, 2015 at the Conference Hall of the Association. Ms. Farhat Ansari, Head of Legal, Compliance &

HR, Standard Chartered Leasing Limited conducted the workshop. Employees from Leasing and

Modaraba Sector attended the workshop.

Ÿ WORKSHOP ON ISLAMIC FINANCE FOR DIRECTORS & SENIOR EXECUTIVES

The Association organized a workshop on “Islamic Finance” for Directors and Senior Executives of the NBFI

& Modaraba Sector on 19th November, 2015 at Pearl Continental Hotel, Karachi. The workshop was

conducted by Mufti Irshad Ahmed Aijaz, Chairman, Shariah Board, Bank Islami Pakistan and Mufti Zeeshan

Abdul Aziz, Shariah Advisor, Sindh Modaraba. The workshop was attended by a large number of Directors

and Senior Executives particularly six directors from Sindh Modaraba attended the workshop.

Mr. Mahfuz-ur Rehman Pasha, Chairman, NBFI & Modaraba Association inaugurated the workshop and

emphasized the importance of seminars and workshops in the development of Islamic financial industry in

the country. On conclusion of the workshop participants were given certificates by Mr. Mahfuz-ur Rehman

Pasha, Mr. Basheer A. Chowdry and Mr. Muhammad Shoaib Ibrahim.

Ÿ THREE DAYS CONFERENCE ON NON-BANKING FINANCE SECTOR & CAPITAL

MARKET

Securities & Exchange Commission of Pakistan (SECP) in collaboration with USAID organized three days

Conference on Non-Banking Finance Sector & Capital Market from 13th to 15th January, 2016 at Marriot

Hotel, Karachi. There were eight sessions in the Conference which included two sessions on (i) Leasing

Sector and (ii) Modaraba Sector.

In the first session the Speakers were Mr. Mahfuz-ur Rehman Pasha, Chairman, NBFI & Modaraba

Association & CEO, Pak Gulf Leasing Limited, Mr. Teizoon Kisat, CEO, ORIX Leasing Pakistan Limited, Mrs.

Arjumand A. Qazi, Group Head, Pak Brunei Investment Limited and Mr. Ravi Tessera, Chief Executive –

LOLC Sri Lanka, while in the Panel discussion Mr. Basheer A. Chowdry was the Moderator and the Panel

was comprised of Mr. Mahfuz-ur Rehman Pasha, Mr. Teizoon Kisat, Mrs. Arjumand A. Qazi and Mr. Ravi

Tessera and Mr. Raja Hassanein Jawed, Provincial Chief, SMEDA, Punjab.

In the second session the Speakers were Mr. Saeed Ahmed, Deputy Governor, State Bank of Pakistan, Mr.

Raheel Q. Ahmad, CEO, Standard Chartered Modaraba, Mr. Zamir Iqbal, Head – World Bank Global Islamic

Finance Development Centre and Mr. Muhammad Tahir Mansoori. Member, Shariah Advisory Board, SECP

and Mr. Zamir Iqbal was the Moderator while in the Panel discussion Mr. Saeed Ahmed, Mr. Raheel Q.

Ahmad, Mr. Tahir Mansoori, Dr. Muhammad Imran Usmani and Mr. Khaleel Ahmed, CIO – Global Financial

Institutions Group – IFC participated.

Both the sessions were very useful and informative and the participants discussed various aspects of the

Leasing and Modaraba Sectors and recommended a number of suggestions for the improvement of both

the sectors.

MoU SIGNING CEREMONY:

NBFI & Modaraba Association of Pakistan signed an MoU with Pak Qatar General Takaful Limited on 30th

September, 2015 to launch a powerful program for promoting Shariah Compliant Takaful Products for the

members of the modarabas. Mian Muhammad Adrees, President, FPCCI the Chief Guest appreciated this joint

Year Book 2015

25

initiative and said that this is a significant event in the history of both the institutions and this collaboration is a big

milestone for the promotion of Islamic financial system. Mr. Muhammad Shoaib Ibrahim, the then Chairman, NBFI

& Modaraba Association and Mr. Javed Muslim, Chief Executive Officer, Pak Qatar General Takaful Limited

addressed the participants. In conclusion Mr. Basheer A. Chowdry, CEO, Trust modaraba thanked the Chief

Guest for sharing his thoughts with the participants.

MEDIA PARTICIPATION:

Ÿ Business Recorder celebrated its golden Jubilee on 27th April, 2015. On this occasion, Business Recorder

published a special supplement in which NBFI & Modaraba Association of Pakistan also participated and a

half page advertisement was extended to them depicting names and logos of all the members of the

Association.

Ÿ In order to give awareness to the general public about the Modaraba, an interview was arranged on

Business Plus TV Channel in a program “Aap aur Karobar” in which Mr. Muhammad Shoaib Ibrahim,

Chairman and Mr. Muhammad Samiullah, Secretary General participated.

FLEET OPERATORS ASSOCIATION OF PAKISTAN:

During the year under review the NBFI & Modaraba Association of Pakistan continued to provide corporate

services to the Fleet Operators Association of Pakistan and completed various tasks. The Association earned an

amount of Rs.600,000/- during the year on account of rendering services to FOAP.

FUTURE OUTLOOK:

In order to make the Association a fully active, vibrant and profit making entity, various measures have been

planned during the year 2015-16. Moreover to give awareness and highlight the existence & importance of NBFI

& Modaraba sectors in the financial industry of Pakistan interaction with various institutions such as FPCCI, IBA

Centre of Excellence in Islamic Banking, Islamic Banks and Pakistan Stock Exchange Limited etc. have been

enhanced.

CONCLUSION:

In the month of October, 2015, the new Executive Committee took over the charge under the Chairmanship of Mr.

Mahfuz-ur Rehman Pasha and took various measures to improve the working of the Association. I assure the

Executive Committee that the Secretarial staff will extend its full support and facilitate all the members in all the

aspects of NBFI & Modaraba Sector.

I wish NBFI & Modaraba Association, every success in its endeavors.

Year Book 2015

26

Year Book 2015

27

Articles

Year Book 2015

28

What scares a criminal most is that his criminal activities are discovered and the criminal proceeds that he has

hard earned are confiscated by the authorities. Such rational fears have given rise to different techniques which

are used by the criminals to a) disguise the criminal proceeds into legal money and b) getting rid of the

incriminating evidences that can lead back to their crimes. For years, criminals have sought to launder dirty

money, for example, by converting illicit money into gold, as gold can be melted and converted into different

forms or through investments in art work.

But those were the days when laws did not reflect money laundering trends much and often criminal proceeds

went undetected. In today’s age and era, globalization has lent a hand in both, combating money laundering

and terrorist financing, as well as providing criminals with more opportunities, what with the reduced travel

barriers and ability of wiring amounts to different jurisdictions.

But what is money laundering and how exactly do criminals achieve it? It is the process a criminal adopts to

disguise the true origin of criminal proceeds, in anticipation of utilizing those proceeds for legal and illegal

activities.

For starters, criminal, or someone hired by the criminal, invests the ill-gotten money into financial institutions and

different businesses. Then the money is re-invested, moved through different jurisdictions, funnelled into off-

shore accounts and bought-with luxury items; creating a complex trail of transactions to obscure the true origin

of the criminal proceeds. Finally, the money is re-introduced into the financial system by means of normal or

personal transactions. This gives off the perception of a legal source and so by this stage, it is increasingly

difficult for law agencies to separate illegal money from legal source and indict criminals.

Here, the criminal and the person involved in managing the criminal proceeds, both are punishable under laws

of many countries. Aiding, facilitating, commissioning and participating in money laundering are considered as

offences of money laundering. Tipping-off the criminal of investigation, confiscation of criminal

proceeds/property or of arrest is also included in the offenses. Though there still are many countries with high-

levels of corruption that have not included such acts as money laundering offenses and deemed as punishable.

Criminalisation of money laundering serves to take the profit out of the crime, as money laundering encourages

criminals and serves to stifle the economy and growth of legitimate businesses, leading to demoralization,

corruption, organized crimes, bribery and terrorist funding.

However, Terrorist Financing (TF) does not need to be conducted using illicit money only. Whereas, funds used

for money laundering are derived from criminal activities, terrorist financing may include funds from perfectly

legitimate sources used to finance acts of terrorism. Unlike money laundering, terrorists seek to disguise the

“purpose” of the funds rather than the source. They structure their transactions in such ways to avoid reporting

and often use financial systems that offer secrecy and immediate access to funds. Terrorist organisations

smartly disguise themselves behind entities such as NGOs, charities etc. The money collected for charities and

such causes is used to fund terrorism instead.

Money Laundering and Terrorist Financing are both, global and national issues. At global level, an inter-

governmental body, Financial Action Task Force (FATF) is present, with 36 members currently and two main

objectives: To set standards & to promote effective implementation of legal, regulatory and operational

measures for combating money laundering, terrorist financing (TF) and other related threats to the integrity of the

international financial system. Countries are encouraged to strengthen their AML/CFT laws, using FATF

recommendations as guidelines. Countries with weak AML/CFT controls pose high risks to global economy and

may become subject to sanctions.

Anti-money Laundering & Counter Financing Of Terrorism

Year Book 2015

29

Since money laundering can serve to destabilize the soundness of financial system and adversely impact the

economy, many countries are taking steps toward strengthening their AML/CFT laws. Even though ML can be

conducted using different mediums, but due to the high number of products provided by financial institutions,

they are also the most vulnerable.

Since aiding criminals by providing financial services to them is a money laundering offence and one that can

lead to heavy penalties, imprisonment of involved parties and reputational damage, it has become imperative for

Financial Institutions (FIs) to form policies and procedures that can help prevent criminals from using their

organization for siphoning criminal proceeds out of the country.

Strict Know Your Client (KYC) and Customer Due Diligence (CDD) procedures at institution’s level can help

prevent from entering into business with criminal or sanctioned individuals/entities. Identification and verification

of customer, business, source of income/funds/wealth, purpose of account opening or investment etc can help

in knowing the client better. FIs should monitor clients’ account activity and should report suspicions to

authorities with evidence. Failure to report suspicion in certain countries is also considered offense and can

result in heavy penalties.

Pakistan is a member state of Asian Pacific Group on Money Laundering (APG), which is one of the observing

associate members of FATF. Pakistan has been actively involved in mitigating AML / CFT risks being faced at

national level. It established its Financial Intelligence Unit in December 2007. For prevention of ML and forfeiture

of property derived from ML and other incidental matters, Government of Pakistan (GoP) enacted Anti Money

Laundering Ordinance (AMLO) in 2007. After it lost its legal authority in 2009, Anti-Money Laundering Act

(AMLA), 2010 was passed by the parliament as measure to provide for prevention of money laundering,

financing of terrorism and forfeiture of property derived from, or involved in money laundering and financing of

terrorism and for matters connected and incidental thereto.

From time to time Financial Monitoring Unit (FMU) issues AML Regulations, providing further guidelines to FIs on

AML/CFT related issues and also format of reports that can be filed to FMU in case of suspicious transactions

and activities. Recently, parliament has also passed Anti-Money Laundering Act (amendment) bill, 2015, in its

attempt to strengthen Pakistan’s AML/CFT laws.

Countries all over the world are working toward combating money laundering and counter financing of terrorism,

policies are being revised to reflect the latest trends and techniques being used by money launderers and

terrorist financers. Though with each money laundering/terrorist financing case we lose the battle, but with our

continuous endeavours at strengthening legal system, we can win the war against criminals.

This Article has been written by Ms. Farhat Ansari, Head of Legal Compliance & HR, Standard Chartered Leasing Company Ltd

Year Book 2015

30

Ijarah; Practical Issues and their solutions- Shariah PerspectiveIjarah; Practical Issues and their solutions- Shariah Perspective

Ijarah Muntahiya Bit Tamlik is a product that has widely been used by Islamic Financial Institutions and

Modarabas, about which much has been written so far and Shari’ah Scholars have extensively explained

Shari’ah Principles of Ijarah Muntahiya Bit Tamlik thereupon. AAOIFI has a complete set of Standard

dedicated to Shari’ah Rulings of Ijarah. These Principles and Shari’ah Rulings are not intended to discuss in

this Article, rather it is my intention to discuss the practical issues being faced by most of the Islamic

Financial Institutions and Modarabas in today’s dynamical environment of Islamic Finance Industry. In fact, I

had an opportunity to work with an institution whose core business is Ijarah, where I experienced several

practical forms of Ijarah with their distinct Process Flows, without applying the correct Process Flow,

sometimes resulting a transaction impermissible/unlawful.

In the following paras, these issues are being discussed which are generally found in Ijarah:-

1. Direct Ijarah:

What I mean from Direct Ijarah is, an Islamic Financial Institution upon request of its client, purchases the

required asset directly from supplier, upon purchase and physical possession thereof, leases out to the

client. For example, a client requests an Islamic Financial Institution to purchase Honda City Car, Model

2015 and to lease him out, the Islamic Financial Institution issues a Purchase Order to Honda Atlas Cars

(Pakistan) Limited and makes payment of the Car and after some period,the Car reaches the

Showroom.

In this matter it is essential to understand that unless the car reaches the showroom, Ijarah Agreement

can’t be executed, however; “Undertaking to take the asset on Ijarah” can be signed. Here, at this stage

sometimes, Ijarah Agreement is signed alongwith Undertaking, whereas the Car is still under booking,

therefore; it is evident that this contract is impermissible in the light of Shari’ah Principles, hence; this

must be avoided. Ijarah transaction should only be processed upon physical delivery of Car by the

Company.

In this matter, there is yet another drawback that comes up while paying for Registration Expenses and

Takaful of the Car, which are as per Shari’ah Principles, the prime responsibility of the Car Owner who is

in this case the Islamic Financial Institution.

In this situation, permissible way is the Islamic Financial Institution to pay for these charges by itself and

may recover the same through lease installments in the light of Shari’ah Guidelines, but; sometimes it so

happens that Islamic Financial Institution upheld its clients liable to pay Registration and Takaful

Charges of the Car and doesn’t pay these charges at its end, nor include the same in lease installments

which is impermissible as per Shari’ah Guidelines. Nevertheless, the right way is that Islamic Financial

Institution to pay for these expenses from its sources directly or else through appointing the client as its

Agent for the payment of these charges, however; such payments can be recovered by including in

lease installments.

Year Book 2015

31

2. Car Ijarah thru Dealers’ Quota:

It has been a routine practice that Cars’ Manufacturers appoint Authorized Dealers of their cars in

various cities for the convenience of general public who prefer to purchase cars ex-stock for ready

delivery instead of booking with the manufacturer and wait. The manufacturing companies allocate

quota to dealers per their capacity. Once the car has been delivered to the Authorized Dealers, now it’s

their risk and responsibility in all respects being the owners of the cars. Now that any client requests an

Islamic Financial Institution that he intends to take a car on Ijarah from Authorized Dealer’s quota, in this

case the appropriate way is that the Islamic Financial Institution will purchase car from the Authorized

Dealer, take the physical possession and then lease out to the client on Ijarah. In this kind of matter,

usually there occurs a mistake that Islamic Financial Institution issues Purchase Order to the Car

Manufacturing Company him whereas the Car already exists in the Dealer’s Showroom and Ijarah

Transaction is executed with the customer directly without execution of sale agreement between Car

Dealer and Islamic Financial Institution. According to Shari’ah Principles it is incorrect because in this

situation Islamic Financial Institution leased out to its Customer the Car which is not owned by them,

rather the Car is owned by the Authorized Dealer and Purchase Order has been issued to the Car

Manufacturing Company.

The right way of doing transaction is to purchase from the Authorized Dealer whose property is the Car

by execution of sale deed between Car dealer and Islamic Financial Institution, then after; Ijara

agreement could be signed with the customer, not merely issuing Purchase Order to the Car

Manufacturing Company for the permissibility of the Lease Contract.

3. Sale and Lease Back:

Sometimes, it so happen that Sale and Lease Back transaction is done on a vehicle or any Asset, which

means the Islamic Financial Institution purchases the asset from a seller and leases back the same asset

to him, in this case transaction is processed in the following two ways:

1. The asset is property of the Client from whom the Islamic Financial Institution purchases then leases

out the same asset to its Client.

2. The asset is not a property of the Client rather he intends to purchase from the market/unauthorized

dealer, in this situation, the Client is appointed as its agent as there being no authorized dealer from

whom the Islamic Financial Institution could purchase the asset directly, therefore; the Client acting

as the agent of Islamic Financial Institution purchases the asset and the Islamic Financial Institution

pays the price to the Client who ultimately pays to the Supplier and subsequently, the asset is leased

out to the Client.

There are some practical issues in the both above mentioned cases of the Sale and Lease Back

Transaction. Insufficient knowledge of the transaction sometimes causes to making mistakes which are

very critical and need to be rectified and their solutions are being discussed in the following paras:

a In the first kind of the Sale and Lease Back Transaction, it is essential that Sale and Lease must be

separate in two contracts one after another.

Here, it happens sometimes that Lease Agreement is signed first by the Customer, then after Sale

Transaction is completed, that means the Islamic Financial Institution has leased out an asset which

is not in its ownership, in other words, Islamic Financial Institution has leased out an asset before

having it in its ownership. The reason why this problem is faced that Sale and Lease Agreements are

signed in the same meetings instead of separate meetings for each subject.

Year Book 2015

32

To overcome this problem it is necessary that Sale and Lease are contracted after one by one, Sale

Contract should be executed first and then Ijarah (Lease Agreement) be executed in the second

phase. It is recommended to execute these two contracts in two separate meetings with the gap of

at least one day.

b According to Shari’ah Principles Sale does not held completed unless the Sale Contract is signed by

both, Seller and Buyer. Therefore; in case Sale is thru written agreement and only one party has

signed, it does not held a complete Sale until the other party signs too.

In first kind of Sale and Lease Back Transaction, it so happens sometimes that Sale and Lease

Agreement both are given to the Client together for his signature whereas the Islamic Financial

Institution has not yet signed any one of them, however; the Client first signed the Sale Agreement

and then Lease Agreement, after signing by the Client, Islamic Financial Institution first signs Sale

Agreement then Lease Agreement. It is evident that in this situation the Client has signed Lease

Agreement prior to completion of Sale Agreement which is absolutely wrong in the light of Shari’ah

Rulings. Therefore; appropriate way is both the parties first complete the Sale Agreement then

proceed to Lease Agreement.

Keeping in view the above theoretical situation, there are some practical issues which need to be

addressed as well. Often, it happens that the Islamic Financial Institution and Client are not located

in the same place, in this case; if Sale Agreement is signed first by both the parties, then the official

of the Islamic Financial Institution will have to go to the Client once again for getting his signature on

Ijarah Agreement which may be difficult practically. Although we prefer that there should be a gap of

one day in signing Sale and Ijarah Agreements means one day Sale Agreement is signed and the

other day Lease Agreement is signed which is as per the spirit of Shari’ah Principles but where it is

really difficult to overcome this issue, in this case; when Sale and Lease Agreements are given to the

Client then the Islamic Financial Institution would sign the Sale Agreement first and handover both

the agreements to the Client advising him to first sign the Sale Agreement then the Lease Agreement

to fulfill the Shari’ah requirement in true sense.

c There is yet another issue which needs to be described here necessarily that sometimes officials of

the Islamic Financial Institutions don’t reach to the Customer’s place for signing the Agreements,

instead, dispatch the same to him by post or TCS. In this case, there are doubtless possibilities that

the Customer signs Lease Agreement first and then the Sale Agreement. Evidently, it is not correct

according to the Shari’ah Principles. In such a situation, it is mandatory to advise the Customer

either by telephone or by an email to follow the Shari’ah Principles by signing first the Sale

Agreement and then Lease Agreement. Further, it is mandatory for the Islamic Financial Institution to

sign the Sale Agreement before sending both the Agreements to the Client as described earlier.

Some Issues related to 2nd kind of Sale and Lease Back:

In this situation, the asset is not a property of the Client rather he intends to purchase from the market.

Since the Supplier of the asset is not an Authorized Dealer, therefore; the Islamic Financial Institution

can’t purchase the asset from the suppliers directly. In this situation, usually the Client is appointed as

the Agent and he purchases the asset from the Supplier on behalf of the Islamic Financial Institution and

thereafter, such asset is given to the Client on Ijarah. In this case, price of the Leased asset can’t be paid

directly to Supplier, therefore; the Islamic Financial Institution pays the amount to the Client who

ultimately pays to the Supplier.

Year Book 2015

33

In this kind of Sale and Lease, yet there are certain issues being faced by the Islamic Financial

Institutions which are elaborated hereinbelow:-

1. Sometimes the Client had purchased asset but full price of the asset has not been paid instead only

token money has been paid. Since the Client doesn’t have the balance amount to be paid to the

Supplier, he approaches the Islamic Financial Institution for leasing the same. In this case the Client

is the owner of the asset but he doesn’t have the physical possession, therefore; it is un-Islamic for

the Islamic Financial Institution to purchase such asset from the Client and lease out to him because

he (client) does not has its physical possession due to non-payment of full price to supplier. Further,

Islamic Financial Institution can’t purchase that asset from an Unauthorized Dealer because the

asset is not owned by him, in fact, it is owned by the Client.

In this case, Ijarah is only possible when:-

a The Customer cancels his previous deal,

b Thereafter, Islamic Financial Institution appoints its Client as Agent to purchase that asset from

the Supplier,

c After purchasing the asset, Lease Agreement can be signed with the Client.

In case the deal is not cancelled as explained above, then it will become un-Islamic, therefore; it is

the responsibility of the Islamic Financial Institution to ensure while dealing with an Unauthorized

Dealer that the Client has not concluded deal of the asset with Unauthorized Dealer and in case if

the Client has done so that must be cancelled before proceeding to Agency, Sale and Lease as

described in above paras.

2. In some cases it happens that the Islamic Financial Institutions appoint its Clients as their agents to

purchase assets from the Unauthorized Dealers whereas the asset is lying ex-stock and is ready or

in finished form, the Customer issues a Purchase Order instead signing the Sale Agreement with the

Unauthorized Dealer then after, Islamic Financial Institution signs Ijarah with its Customer. Here, it

must be remembered that this transaction is impermissible because the property is not owned by

Islamic financial Institution and the basic principle behind this is the Purchase Order simply is an

order for supply of asset and Sale Agreement can only be completed upon having the physical

possession of the asset or by execution sale agreement (offer and acceptance), therefore; in this

situation Ijarah Contract prior to having physical possession of the asset is incorrect as per Shari’ah

Principles. As for solution, the Client should not only issue the Purchase Order but also executes the

Sale Agreement with the Supplier, after signing the Sale Agreement, the asset will become the

property of the Islamic Financial Institution. Thereafter, the Islamic Financial Institution is at liberty to

sign the Lease Agreement with its customer.

4. General Issues:

Now hereunder, following issues are described which are being generally faced in Ijarah Transaction:-

1. As per Shari’ah Ruling under Ijarah, the Islamic Financial Institution is responsible for loss of asset

related to ownership. To cover themselves from such losses, the Islamic Financial Institutions opt for

Takaful, hence; in case of any loss, Takaful Companies reimburse the amount of loss but Takaful

Companies don’t bear the amount of depreciation on that asset e.g. a car was on lease with a

customer, in an accident the door of the car was severally damaged, whereas cost of the door is

Year Book 2015

34

approx. Rs. 50,000/- while against the claim, Takaful Company will reimburse Rs. 40,000/-

considering the depreciation factor. In this case who will be responsible for the balance Rs. 10,000/-

? In case of Ijarah this becomes the responsibility of the Islamic Financial Institution subject to such

loss is occurred not due to negligence of the Customer. Most of times the Islamic Financial

Institutions didn’t pay such claims even on demand of the Customers which is against the Shari’ah

Principles. Therefore; in such matters, Islamic Financial Institutions should bear these kinds of losses

to fulfill their Shari’ah Obligations.

2. In Ijarah, asset is the property of the Islamic Financial Institutions but they opt for general insurance

instead Takaful, this is against Shari’ah in the situations where the facility of Takaful is available.

Keeping in view the prevailing situation, most of the Insurance Companies have also started Takaful

windows, therefore; it has become so easy to avail Takaful facility for the coverage of the assets,

hence; it is mandatory for the Islamic Financial Institutions to adopt Takaful instead of general

insurance, particularly for Modarabas whose value of the assets is not high in volume that Takaful or

Window Takaful Companies can’t cover.

3. Registration charges of cars are responsibility of the Islamic Financial Institutions, likewise; Takaful

Contribution is also responsibility of the Islamic Financial Institutions, however; it is permissible to

include these expenses in the Lease Rentals.

Sometimes the Islamic Financial Institutions appoint their Client as their agents to pay registration and

Takaful charges who pays off on their behalf and the Islamic Financial Institutions don’t bear this burden.

As per Shari’ah Principles, it is wrong, such expenses are the responsibility of the Islamic Financial

Institutions even in case the Islamic Financial Institutions have appointed their Client and the Client has

paid off such expenses then it is responsibility of the Islamic Financial Institutions to reimburse these

expenses to the Client. There is yet another possibility that the Client pays off for these expenses and

deduct the same amount from Lease Rentals.

According to the ruling of the SECP, it is mandatory to appoint Shari’ah Advisor at the Islamic Financial

Institutions and Modaraba Companies and Al Hamdo Lillah, Shari’ah Advisors are now working at all

Mudaraha Companies, therefore; it is compulsory for all Islamic Financial Institutions to abide by their

Shari’ah Advisors’ guidelines while doing transactions and by way of this, Islamic Financial Institutions

will safeguard them of doing anything un-Islamic.

Mufti Ibrahim EssaDecember 05, 2015

This article has been written by mufti Ibrabim Essa, Shariah Advisor

Year Book 2015

35

Role of Central Bank in Supporting NBFCs for Growth & Progress of SMEs

Demographic Dividend

The ‘demographic transition’ in Pakistan, which may lead to high fertility rates; longer spans of life due to

decreasing mortality rates; increasing urbanization; and lower utilization of labor in agrarian activities, is at a

nascent stage: yet too far from a position to distribute any demographic dividend to the National Income. But

we can see around us changes in our demographic complexion, which if duly harnessed, could reduce the

usual transition period from 5 decades to a lesser period.

We have a huge population of around 189 million, growing at the rate of 1.64% per annum; the Median Age

is at 23.2 years; average life span has grown to around 67.73 years, and the high fertility rate of 3.22 has

given rise to one of the highest number of potential work force (39%), which is aged between 15 to 39 years.

Not only is there an increased inflow of population to the cities, with the Urban Population standing at 38%,

but rural areas are continuously getting urbanized at a fast pace due to advancement, among other things,

in electronic communication.

Contribution of Small & Medium Enterprises (SMEs) to National Economy

According to SMEDA’s assessment, 80% of Pakistan’s non-agricultural workforce is employed with Small &

Medium Enterprises (SMEs), which constitute 90% of all the enterprises of the country contributing 40% to

the country’s GDP.

Most SMEs in Pakistan are carrying out the very important job of being the Vendor Industry for most Large

Scale Manufacturing entities (LSMs). The continuing escalation in the sale of Motor Vehicles, for instance,

would not be possible without the support of a huge number of SMEs producing smaller automobile parts

and accessories. Same is true for electronic and electrical vendor industry servicing the needs of so many

varieties of locally manufactured and finished consumer products, such as televisions, refrigerators, air

conditioners, fans, washing machines, generators and motorized pumps of various specification, not to

mention the active contribution of such vendors in heavier mechanical products, some of which are also

used by the Defense Production Industry. Construction, transportation and real estate development

industries also benefit from services provided by SMEs.

Fulfilling Funding Requirements of SMEs

The foregoing preamble is necessary to highlight the importance of the non-traditional borrowers comprising

mainly of SMEs, which tend to remain disenfranchised from the usual credit facilities offered by Commercial

Banks and Development Financial Institutions (DFIs) falling under the regulatory umbrella of the State Bank

of Pakistan (Central Bank).

All of us are aware of the reluctance of Banks & DFIs in Pakistan to undertake high credit risk and the cost of

administration thereof, when interest arbitrage options are available by channeling funds in gilt-edged

securities. The fringe borrowers, chiefly the SMEs, are therefore left to approach Non-Banking Finance

Companies (NBFCs) including Modarabas, which are more inclined, if only for the sake of their own survival,

to find ways of fulfilling the credit needs of such SMEs.

Securities & Exchange Commission of Pakistan (SECP) versus State Bank of Pakistan (SBP)

The Securities & Exchange Commission of Pakistan (SECP), not differently from SEC’s role in the U.S.,

ensures administration of Laws governing NBFCs, albeit those primarily associated with the Securities

Year Book 2015

36

Market. In contradiction, however, to the extensive and all-inclusive role assumed by the Federal Reserve

Board of the U.S. in ensuring the financial viability and liquidity profile not only of Commercial Banks, but

also the Shadow Banking System (including NBFCs), the State Bank of Pakistan (SBP) has chosen since the

end of year 2002 , not to have anything to do with the aforesaid key issues relating to NBFCs. SBP has left

the entire regulatory control of NBFCs to SECP, without the latter having the fiduciary wherewithal to

monetarily manage, support or bail out NBFCs in financial distress.

Adverse Impact on NBFCs Arising from Delinking with SBP

Most NBFCs, excluding those carrying out Securities Operations, are quasi-banking institutions, in as much

as they are required to channelize their Financial Resources (Equity+ Certificates of Deposits+ Bank

Borrowings) into Lending Operations in the form usually of Medium Term commitments. Consequently, their

core assets comprise of term financing, requiring prudential credit risk management. Funding by NBFCs, for

such operations is arranged by leveraging their Equity by creating a liabilities portfolio comprising of funds

borrowed from the Public and/or other Financial Institutions. The quality of their fund management

determines their ability to keep their cost of funds low and ensuring that there are no mismatches between

the funds advanced and borrowed and that any surplus between the sources/uses remains profitably and

securely invested. More importantly, such NBFCs must ensure that there are no hiccups in recovery of their

advances from their borrowers on due dates.

A Central Bank has the wherewithal, by the very nature of its regulatory experience and access to both

macro as well as micro aspects of the Economy of the country, to ensure that all the foregoing norms are

duly fulfilled and wholeheartedly complied with, in the prescribed manner, by the NBFCs. Backing of a

Central Bank is also important to provide security and psychological comfort to investors and lenders of any

NBFC. The presence of a Lender of Last Resort, access to the Central Bank’s Discount Window and, if

available, the fall back on a Depositors’ Insurance Fund, all taken together, ensure liquidity and competent

risk management for NBFCs. Hence, despite their limited scope of activities, NBFCs attain the ability to enjoy

a respectable place among Financial Intermediaries, including Commercial Banks and DFIs, enabling them,

as a result, to also become an active participant in the Inter-bank Money Market operations.

When the entire regulatory control of NBFCs was transferred in late 2002, by SBP to SECP, it was perhaps

inadvertently overlooked that SECP would have no fiduciary powers, as opposed to SBP. Moreover, an

administrative control alone by the SECP would not, like the SBP, have the capacity to devise policies for

NBFCs, based on fiscal management comprising of money supply, credit expansion, interest rates and

sector-wise distribution of NBFCs collective credit portfolio.

Law Makers also failed to perceive that NBFCs, under SECP’s sole Regulatory umbrella, would be deprived

of the multifarious and lucrative Refinancing and Long Term Specialized Financing Schemes offered by SBP

(including those reserved for SMEs, in particular), to only those Banks and Financial Institutions which

functioned under SBP’s direct regulatory control.

Competition from Commercial Banks

A rather unexpected phenomenon, resulting from withdrawal of SBP’s control over NBFCs, was the sudden

increase in the propensity of commercial banks to offer those very services, which had hitherto been the

domain exclusively of NBFCs. Not that commercial banks were previously debarred from carrying out

“NBFCs-specific” functions. However, they were earlier reluctant to get into the field as they did not possess

the professionally competent Human Resource to manage those functions. They had been eyeing the

feasibility of undertaking transactions carried out by the NBFCs, in the backdrop of the significant growth of

NBFCs from 1985 to 2002, but were shy of taking a plunge in the field. With the SBP having withdrawn as a

Regulator of NBFCs, at the end of 2002, an immediate decline was witnessed in the growth and profitability

Year Book 2015

37

of NBFCs. As a consequence thereof, adequate Human Resource from NBFCs was willing to switch sides

by joining commercial banks to contribute in terms of its expertise in enabling banks to competently carry

out NBFCs-specific functions.