xlviii foro nacional de la industria química - aniq · mark eramo, vice-president . ihs markit ....

TRANSCRIPT

Mark Eramo, Vice-President IHS Markit Global Business Development, Chemicals [email protected]

XLVIII Foro Nacional de la Industria Química

Impact of Oil & Gas On Global Petrochemical Market Developments Presented By:

October 27-28, 2016 Hyatt Regency - Mexico City, Mexico

© 2016 IHS Markit. All Rights Reserved.

IHS and Markit are now IHS Markit IHS Markit thinks about the world in a unique way.

We call this The New Intelligence.

IHS Markit’s singular ability to look across complex industries, financial markets, and government actions that drive the global economy and provide our customers with insights, perspective and solutions for what really matters.

Energy Chemical Automotive Financial Markets

Product Design Technology, Media & Telecom

Maritime & Trade Aerospace, Defense & Security

© 2016 IHS MARKIT

• The Chemical Industry Enables and Provides…

• Impact of Energy on Chemical Investment Decisions

• Select Regional Perspectives

• Ethylene & Propylene In An Era Of “Energy at the Extremes”

• Strategic Considerations

3

Impact of Oil & Gas On Petrochemical Markets AGENDA

© 2016 IHS MARKIT

The Global Chemical Industry… … Enabling Modern Living

Automotive / transportation Consumer products Packaging Building / construction Recreation / sport Industrial Medical Pharmaceutical Personal care Textiles Electrical / electronics Aircraft / aerospace Business equipment

CUSTOMERS Formulated products / performance materials

Plastics and engineering resins • Extruded films, pipe,

profiles, coatings, sheet, foams

• Blow-molded parts • Composites

Synthetic fibers Rubber products Paints and coatings Adhesives and sealants Lubricants Water treatment products Cleaning products Industrial chemicals Flame retardants

Commodities

Differentiated commodities

Technical specialties

Chemical Intermediates

Base Chemicals

Olefins (ethylene, propylene, butylene)

Aromatics (benzene,

toluene, xylenes)

Chlor-akali (chlorine, caustic

soda)

Others (ammonia, phosphorous)

CHEMICAL INDUSTRY VALUE CHAIN ENERGY & FEEDSTOCKS

Mining, drilling, refining,

gas processing

Oil Gas Coal Minerals Renewables

ENERGY & FEEDSTOCKS

4

© 2016 IHS MARKIT

Global Energy & Economic Fundamentals Impact Chemical Investment Decisions

• Crude oil price trends impact regional competitiveness and profitability for chemicals.

• Ethane/gas based investments in North America and coal-based assets in China, see lower margins in low crude oil market.

• Assumptions on economy and energy drive key decisions of location, feedstock, technology, scale, cost position, trade, etc.…

• Uncertainty results in delayed approvals; when combined with steady growth leads to tighter market conditions in certain markets

• Crude oil (energy) “at the extremes” impacts demand for chemicals and plastics. On the high end, it can “destroy” demand and on the low end it can stimulate demand.

5

© 2016 IHS MARKIT

Gas-to-Crude Ratio Drives Regional Investment Activity In The Chemical Industry

0%

20%

40%

60%

80%

100%

120%

0.0

3.0

6.0

9.0

12.0

15.0

18.0

90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20

Crude (WTI) Natural Gas Gas-to-Crude Ratio

Regional Energy Pricing Trends : Low Gas-to-Crude Ratio Favors North America Investments

Source: IHS

$ / M

M B

tu

Gas

-to-C

rude

Rat

io

6

© 2016 IHS MARKIT

Impact of Changing Energy Dynamics On Regional Chemical Capacity Additions

-30%

0%

30%

60%

90%

120%

-10

0

10

20

30

40

91 93 95 97 99 01 03 05 07 09 11 13 15 17 19 21

Gas

-to-C

rude

Oil

BTU

Rat

io, %

Mill

ion

Met

ric T

ons

China Asia Less China (with India)Middle East North AmericaWest Europe Gas-To-Crude BTU Ratio, %

Annual Change - Total Basic Chemicals Capacity: Ethylene, Propylene, Methanol, Benzene, Paraxylene, Chlorine

7

© 2016 IHS MARKIT

-30%

0%

30%

60%

90%

120%

-10

0

10

20

30

40

91 93 95 97 99 01 03 05 07 09 11 13 15 17 19 21

Gas

-to-C

rude

Oil

BTU

Rat

io, %

Mill

ion

Met

ric T

ons

China Asia Less China (with India)Middle East North AmericaWest Europe Gas-To-Crude BTU Ratio, %

Annual Change - Total Basic Chemicals Capacity: Ethylene, Propylene, Methanol, Benzene, Paraxylene, Chlorine

8

Impact of Changing Energy Dynamics On Regional Chemical Capacity Additions

© 2016 IHS MARKIT

-30%

0%

30%

60%

90%

120%

-10

0

10

20

30

40

91 93 95 97 99 01 03 05 07 09 11 13 15 17 19 21

Gas

-to-C

rude

Oil

BTU

Rat

io, %

Mill

ion

Met

ric T

ons

China Asia Less China (with India)Middle East North AmericaWest Europe Gas-To-Crude BTU Ratio, %

Annual Change - Total Basic Chemicals Capacity: Ethylene, Propylene, Methanol, Benzene, Paraxylene, Chlorine

9

Impact of Changing Energy Dynamics On Regional Chemical Capacity Additions

© 2016 IHS MARKIT

-30%

0%

30%

60%

90%

120%

-10

0

10

20

30

40

91 93 95 97 99 01 03 05 07 09 11 13 15 17 19 21

Gas

-to-C

rude

Oil

BTU

Rat

io, %

Mill

ion

Met

ric T

ons

China Asia Less China (with India)Middle East North AmericaWest Europe Gas-To-Crude BTU Ratio, %

Annual Change - Total Basic Chemicals Capacity: Ethylene, Propylene, Methanol, Benzene, Paraxylene, Chlorine

10

Impact of Changing Energy Dynamics On Regional Chemical Capacity Additions

© 2016 IHS MARKIT

• The Chemical Industry Enables and Provides…

• Impact of Energy on Chemical Investment Decisions

• Select Regional Perspectives

• Ethylene & Propylene In An Era Of “Energy at the Extremes”

• Strategic Considerations

11

Impact of Oil & Gas On Petrochemical Markets AGENDA

© 2016 IHS MARKIT

Benzene

Chlorine

Ethylene

Methanol

Paraxylene Propylene PG

Global Base Chemical Assets By Location

12

580 MM metric tons in 2015

© 2016 IHS MARKIT

0

150

300

450

600

750

900

90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20 22 24

China Asia Less China (with India)North America Middle East + AfricaEurope South America

Base Chemicals – Total Capacity By Region Ethylene, Propylene, Methanol, Benzene, Paraxylene, Chlorine

Source: IHS © 2016 IHS

Mill

ion

Met

ric T

ons

Base Chemical Capacity To Exceed 750 MM Metric Tons By 2025, Dominated By Growth Across Asia/Pacific

Chemical Investment “Rules”

• Secure an energy & feedstock advantage.

• Leverage current technology and build world-scale.

• Invest with proximity to local markets and/or access to trade routes.

• Build to leverage an upstream and/or downstream integrated position.

13

© 2016 IHS MARKIT

Beyond 2020…Where Will The Next Wave Of Capacity Be Built? Region 2015 2025 Delta

North America

90

137

47

South America

24

26

2

Europe

89

101

12 Middle East / Africa

77

119

42

Asia/India w/o China

130

163

33

China

172

241

69

Total

582

787

205

Total Basic Chemical* Capacity (Million Metric Tons)

* Ethylene, Propylene, Methanol, Benzene, Paraxylene, Chlorine

14

© 2016 IHS MARKIT

Investment Decisions Must Evaluate Many Factors Beyond Energy & Economy

Investment Assumptions: • Global crude oil price scenarios • Global economic growth outlook • Geo-political considerations

• Iran sanctions • North American energy market • Current state of the profit cycle • China structural changes • Non-conventional technology • Sustainability • Levels of integration • Regional CAPEX differentials • Logistics investments

15

Braskem-Idesa Ethylene/PE Plant Nanchital, Veracruz, Mexico

Start-Up: June 2016

Investment Assumptions: • Global crude oil price scenarios • Global economic growth outlook • Geo-political considerations

• Iran sanctions • North American energy market • Current state of the profit cycle • China structural changes • Non-conventional technology • Sustainability • Levels of integration • Regional CAPEX differentials • Logistics investments

© 2016 IHS MARKIT

China Slower Pace Of New Investments & Focus On: > Industry Competitiveness > Safety & Pollution control > Segment Consolidation

16

• The government balancing between economic growth, social stability, industry restructuring.

• Tighten pollution control; industry safety performance; rationalize inefficient assets.

• Develop modern coal chemicals asset base.

• Consolidation of 100+ chemical industry parks into seven national chemical industrial zones.

• Rapid growth in private investment potentially changes future behavior.

• Overseas investment activity is also very active.

China 13th Five Year Plan

© 2016 IHS MARKIT

China 13th 5-Year Plan Slows Pace Of New Investments; Focus Shifts To Competitive Position, Safety & Pollution, Consolidation

17

0

50

100

150

200

250

90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20 22 24

Propylene (PG/CG) Ethylene Paraxylene

Benzene Methanol Chlorine

China - Base Chemical Total Capacity

Source: IHS © 2016 IHS

Mill

ion

Met

ric T

ons

Basic chemicals expansions of 200 MM metric tons over two decades (2005 – 2025). Self-sufficiency in propylene 85+% by 2020; ethylene remains near 60%.

© 2016 IHS MARKIT

Middle East Rate Of Investment Slows; Adding Diverse Feedstocks; Focused On Operational Efficiencies

18

• Ethane prices in Saudi Arabia raised to reflect transition in strategy for future investments.

• Low crude prices sharpen focus on operational costs.

• Sadara project represents measured approach in Saudi Arabia to diversify businesses within chemicals industry.

• Lifting of nuclear sanctions on Iran has re-opened plans to expand the chemical space; insurance and financing remain an issue.

• Regional significant dependence on exports continues well into the future.

© 2016 IHS MARKIT

Middle East Focus Shifting To Feed-slate Diversity And Improving Operational Efficiencies

19

0

20

40

60

80

100

120

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

Mill

ion

Met

ric T

ons

Propylene (PG/CG) Ethylene ParaxyleneBenzene Methanol Chlorine

Middle East Base Chemical Capacity

© 2016 IHS MARKIT

North America: An Attractive Place For Chemicals Investments Once Again

• Low cost energy and natural gas liquids provide sustainable advantage.

• Advantaged feedstock will enable an additional wave beyond 2020, assuming crude oil price recovery (near $80/bbl) and low natural gas pricing (near $4/MM BTU).

• Domestic and International companies seek to invest; leveraging the low-cost opportunities. New entrants to create increased competition in domestic markets

• Logistics & port infrastructure investment needed to support higher level of exports.

20

© 2016 IHS MARKIT

North America Low Cost Brings Back Base Chemical & Associated Derivative Investments

-10

10

30

50

70

90

110

130

150

90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20 22 24

Ethylene Propylene (PG/CG) Methanol Chlorine Benzene Paraxylene

North America - Base Chemical Total Capacity

Source: IHS © 2016 IHS

Forecast

Mill

ion

Met

ric T

ons

21

© 2016 IHS MARKIT

• The Chemical Industry Enables and Provides…

• Impact of Energy on Chemical Investment Decisions

• Select Regional Perspectives

• Ethylene & Propylene In An Era Of “Energy at the Extremes”

• Strategic Considerations

22

Impact of Oil & Gas On Petrochemical Markets AGENDA

© 2016 IHS MARKIT

Energy At The Extremes Has Catalyzed A “New Era” In Light Olefins Production

23

• For decades, light olefins supply based on refinery & naphtha cracker integrated sites

• Ethane crackers emerged where ethane was advantaged; USGC, Mexico, Alberta, Middle East; other areas where liquids rich gas was “trapped”.

• Propylene was a byproduct of refining and heavy or flexible steam cracking.

• Today light olefins are being made on purpose via a variety of technologies beyond refining and steam cracking: PDH, CTO/P, MTO/P, Metathesis, GTO/P, OCM

Propylene

Ethylene

PDH = Propane Dehydro CTO = Coal to Olefins CTP = Coal to Propylene MTO = Methanol to Olefins MTP = Methanol to Propylene GTO = Natural gas to Olefins GTP = Natural gas to Propylene OCM = Oxidative Coupling of methane

© 2016 IHS MARKIT

Beyond 2020…what are todays conversations about where the next wave of light olefins investments will be located?

Ethylene

Propylene PG

© 2016 IHS MARKIT

Energy & Feedstocks Will Influence Location & Technology For New Capacity Decisions

25

0

5

10

15

20

25

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024

Brent Crude Henry Hub Gas USGC Ethane

USGC Propane NEA Naphtha China Coal

Crude Oil – vs – Natural Gas & NGLs

© 2016 IHS

Con

stan

t 20

14$

Per M

MB

tu

Notes: China Coal is on a 6000kcal/kg basis, Qinhuangdao FOB Source: IHS

© 2016 IHS MARKIT

Non-conventional Technology Providing Options For Future Olefins Investments

0

200

400

600

800

1000

1200

1400

USEthane

US PDH NEA PDH NEANaphtha

WEPNaphtha

2011 2013 2015

Conventional Olefins Cash Cost (US$ / MT)

US GTP US GTO NEA CTO NEA MTO

Non-conventional Olefins Cash Costs (US$ / MT)

PDH = Propane Dehydro; GTP = Gas to Propylene; GTO = Gas to Olefins; CTO = Coal to Olefins; MTO = Methanol to Olefins

26

© 2016 IHS MARKIT

Ethylene Market Key Issues

27

• New Ethylene Capacity: delayed

start up timing of all “first wave” US ethylene units. Pushed out and/or removed some additions in China (MTO/CTO)

• Build-cycle Disruption: under investing in new capacity during 2020-21 period, supporting margin “up-cycle” .

• Effective Global Operating Rates: expected to be high over the next 5 years assuming steady economic growth, current new-build profile, unplanned outages.

• Naphtha crackers: required to balance demand; increasing cash cost combined with need for more naphtha cracking will push ethylene prices higher.

© 2016 IHS MARKIT

75

80

85

90

95

100

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Global Op Rate Global Op Rate (Steam Cracker)NEA Op Rate WEP Op RateNAM Op Rate

Global Ethylene Nameplate Operating Rates

© 2016 IHS

Perc

ent

Source: IHS

North America “Wave” Of Capacity Will Not Overwhelm The Global Balance

28

© 2016 IHS MARKIT

5,089 5,726

12,458

-2,844 -3,060 -3,828

-597 -564 -1,759

14,041

18,266 19,686

-8,323

-10,550

-14,768

-390 -440 -1,103

-7,356 -9,521

-10,604

Ethylene Net Equivalent Trade Growth continues in Advantaged Regions

2011

2016

2021

*Others: Africa, Indian Sub., CIS & Baltic, Central Europe

North America

West Europe

Others*

South America Middle East

Southeast Asia

Northeast Asia

© 2016 IHS MARKIT

Propylene Market Key Issues

Propylene Requires On-Purpose Investment: margins for incremental supply will have to support new investments On-Purpose Technology Will Vary: dependent on regional feedstock advantage - PDH in U.S., Middle East, and Asia along with coal to olefins in China; Chinese PDH units based on propane imports that compete into fuels market. MTP is high cost. Build phase is delayed: investment in North American on-purpose propylene production delayed as questions over energy and the economy persist; “GTP under study”. Regional imbalance causes price volatility: overcapacity in propylene will cause major price shifts regionally but balance out over time. US monomer balance is long, derivatives are tighter. Low prices stimulate demand: propylene demand growth is seeing strength due to ample low cost supplies.

30

© 2016 IHS MARKIT

On-Purpose Propylene Supply To Reach 25% By 2020 Changing Competitive Landscape For Derivative Markets

0%

5%

10%

15%

20%

25%

30%

0

50

100

150

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

% O

n- P

urpo

se

Stm. Crackers FCC Splitters DehydroMetathesis Olefin Cracking Methanol to OlefinsMethanol to Propylene Coal to Olefins Coal to PropyleneHS FCC Others On-Purpose % On-Purpose

Global Propylene Supply By Technology

Mill

ion

Met

ric T

ons

On Purpose Co-Product

31

© 2016 IHS MARKIT

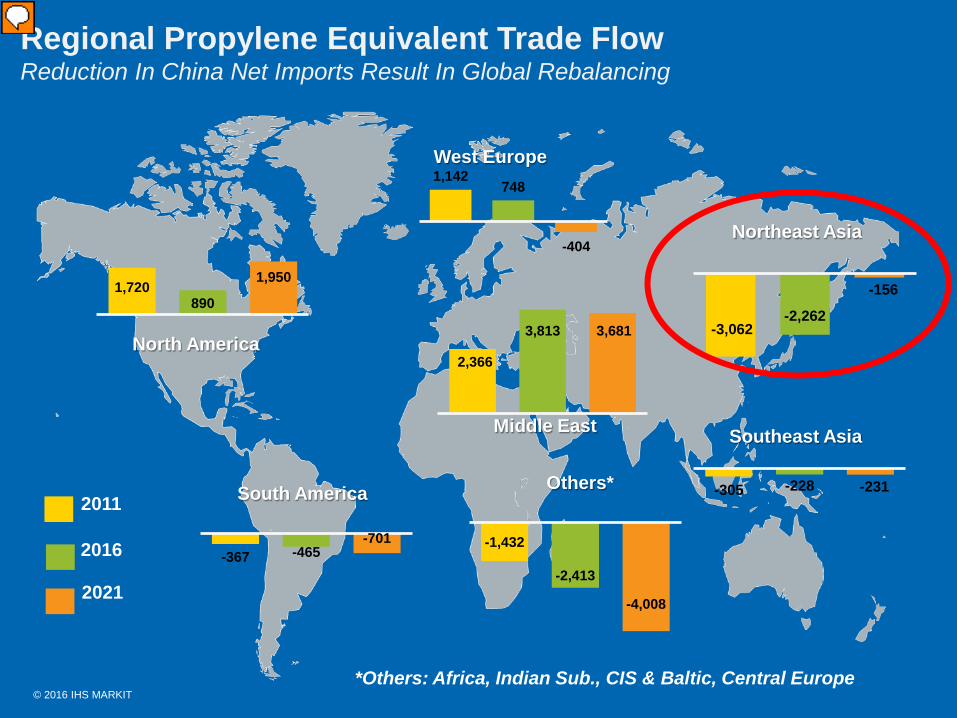

Regional Propylene Equivalent Trade Flow Reduction In China Net Imports Result In Global Rebalancing

2011

North America

South America

West Europe

Middle East

Northeast Asia

Southeast Asia

2016

Others*

2021

*Others: Africa, Indian Sub., CIS & Baltic, Central Europe

1,720 890

1,950

-367 -465 -701

1,142 748

-404

-1,432

-2,413

-4,008

2,366

3,813 3,681 -3,062 -2,262

-156

-305 -228 -231

© 2016 IHS MARKIT

Pathways To A Competitive Petrochemical Industry…

Strategic Implications

• Energy markets impact chemical investment decisions. High level of uncertainty presents difficult scenarios for planning the best path forward.

• The investment landscape is changing with non-conventional options on technology and feedstock selection.

• Board level decisions require higher returns for approval; CAPEX is higher; Risk premiums escalate; approvals delayed.

• Investment decisions delays in 2015/16 could lead to supply limitations in the 2020+.

• Ethylene capacity additions globally outpace demand growth; Naphtha crackers required to balance demand; co-products (propylene, benzene) require new “on-purpose” supply options.

33

Mark Eramo, Vice-President IHS Markit Global Business Development, Chemicals [email protected]

XLVIII Foro Nacional de la Industria Química

Impact of Oil & Gas On Global Petrochemical Market Developments Presented By:

October 27-28, 2016 Hyatt Regency - Mexico City, Mexico

GRACIAS!!